🛫 Farm Planning & Budgeting

Learn about Farm Planning and Farm Budgeting

Farm Planning

- A farm plan is a programme of total farm activity of a farmer drawn up in advance.

- A farm plan should show the enterprises to be taken up on the farm; the practices to be followed in their production, use of labour, investments to be made and similar other details.

- Farm planning enables the farmer to achieve his objectives (Profit maximization or cost minimization) in a more organized manner. It also helps in the analysis of existing resources and their allocation for achieving higher resource use efficiency, farm income and farm family welfare. Farm planning is an approach which introduces desirable changes in farm organization and operation and makes a farm viable unit.

Type of Farm Plans

Simple farm planning

- It is adopted either for a part of the land or for one enterprise or to substitute one resource to another. This is very simple and easy to implement.

- The process of change should always begin with these simple plans.

Complete or whole farm planning

- This is the planning for the whole farm.

- This planning is adopted when major changes are contemplated in the existing organization of farm business.

Characteristics of Good Farm Plan

- It should be written.

- It should be flexible.

- It should provide for efficient use of resources.

- Farm plan should have balanced combination of enterprises.

- Such combination in turn ensures:

- Production of food, cash and fodder crops.

- Maintain soil fertility.

- Increase in income.

- Improve distribution of and use of labour, power and water requirement throughout the year.

- Avoid excessive risks.

- Utilize farmer’s knowledge and experience and take account of his likes and dislikes.

- Provide for efficient marketing.

- Provision for borrowing, using and repayment of credit.

- Provide for the use of latest technology.

Farm Budgeting

- Budgeting can be used to select the most profitable plan from among a number of alternatives and to test the profitability of any proposed change in plan.

- It involves testing a new plan before implementing it, to be sure that it will improve profit. Farm budgeting is a method of estimating expected income, expenses and profit for a farm business.

- So, planning and budgeting go side by side.

Types of farm budgets

Enterprise Budget

- An enterprise is defined as a single crop or livestock commodity being produced on the farm. An enterprise budget is an estimate of all income and expenses associated with a specific enterprise and estimate of its profitability.

- Enterprise budget can be developed for each actual and potential enterprise in a farm plan such as paddy enterprise, wheat enterprise or a cow enterprise

- Each is developed on the basis of small common unit such as one acre or one hectare for crops or one head for livestock. This permits easier comparison of the profit for alternative and competing enterprises.

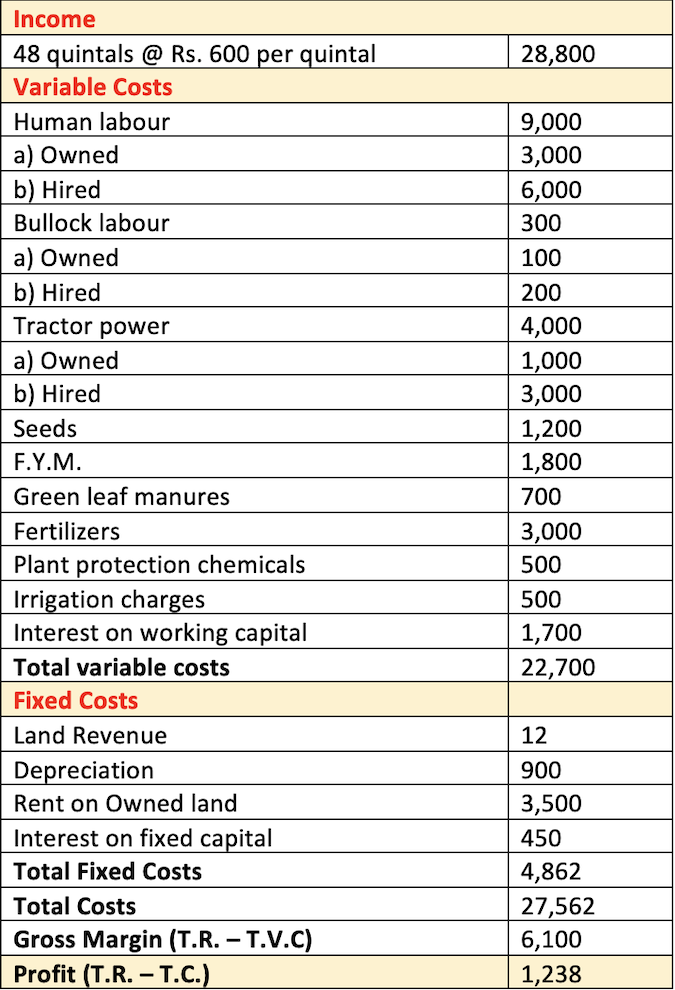

- Enterprise budget can be organized and presented in three sections income, variable costs and fixed costs.

- The first step in developing an enterprise is to estimate the total production and expected output price. The estimated yield should be an average yield expected under normal weather conditions given the soil type and input levels to be used. The output price should be the manager’s best estimate of the average price expected during the next year or next several years. Variable costs are estimated by knowing the quantities of inputs to be used (such as seed, fertilizer, labour, manures) and their prices. The fixed costs in a crop enterprise budget are depreciation on machinery, equipment, implements, livestock, farm building etc., rental value of land, land revenue, interest on fixed capital.

- Example: Enterprise budget for paddy production (one hectare)

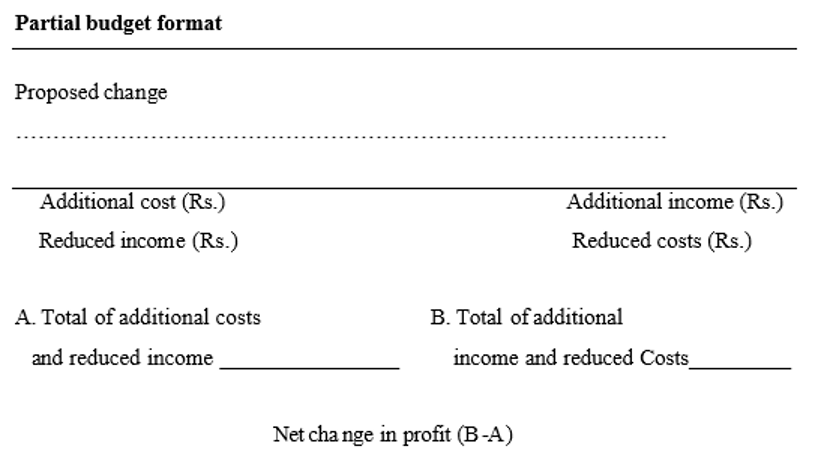

Partial budget (Enterprise Budgeting)

- It is used to calculate the expected change in profit for a proposed change in the the farm business. Partial budget is best adopted to analyze relatively small change in the whole farm plan.

- Partial budgeting is used where the change in the activity under study would not affect the farm, organization vitally. Under such budgeting only variable costs are evaluated and only marginal costs and marginal returns are estimated here.

- Changes in the farm plan or organization adopted to analysis by use of partial budget are of three types.

- Enterprise substitution: This includes a complete or partial substitution of one enterprise for another. For example, substitution of sunflower for groundnut.

- Input substitution: Example: Machinery for labour, changing livestock rations, owning a machine instead of hiring, increasing or decreasing fertilizers or chemicals.

- Size or scale of operation: This includes changing in total size of the farm business or in the size of the single enterprise, buying or renting of additional land, expanding or decreasing an enterprise.

1. Additional costs

- A proposed change may cause additional costs because of a new or expanded enterprise requiring the purchase of additional inputs.

2. Reduced income

- Income may be reduced if the proposed change would eliminate an enterprise, reduce the size of an enterprise or cause a reduction in yield.

3. Additional income

- A proposed change may cause an increase in total farm income if a new enterprise is being added, if an enterprise is being expanded or if the change will cause yield levels to increase.

4. Reduced costs

- Costs may be reduced if the change results in elimination of an enterprise, or reduction in size of an enterprise or some change in technology which decreases the need for variable resources.

👉🏻 Partial budgeting is intermediate in scope between enterprise budgeting and whole farm planning. A partial budget contains only those income and expense items which will change if the proposed modification in the farm plan is implemented. Only the changes in income are included and not total values. The final result is an estimate of the increase or decrease in profit.

Complete Budget or Whole farm budget

- The cost-and-return analysis of the whole farm as a single unit is estimated in the case of drastic changes of the farm business is called complete budgeting.

- Complete budgeting involves complete reorganization of the farm business. lt considers all the crops, livestock producing methods and estimate costs and returns for the farm as a whole. Here both the costs i.e. variable and fixed costs are included, in the computation of full farm budgeting.

- Complete farm budgeting is needed in

- Before starting farming on a new farm.

- Comparative cost-and-return analysis of alternative farm plans.

- In the drastic changes in the farm organization and farm operations i.e. in the case of complete re-organization of the farm business e.g. adoption of new crop rotation, new methods of crop production and livestock rearing.

Cash flow budget

- It is summary of cash inflows and outflows for a business over a given time period. Its primary purpose is to estimate the future borrowing needs and loan repayment capacity of the farm business.

Basic Steps in Farm Planning and Budgeting

I. Resource Inventory

- The development of whole plan is directly dependent upon an accurate inventory of available resources. The resources provide the means for production and profit. The type and quality of resources available determine the inclusion of enterprise in whole farm plan.

1) Land

- Land resource should receive top priority when completing the resource inventory. It is one of the fixed resources. The following are some of the important items to be included in land inventory

- Total number of acres available

- Soil types (slope, texture, depth)

- Soil fertility levels

- Water supply or potential for developing an irrigation system

- Drainage problems and possible corrective measures

- Existing soil conservation practices

- Existing and potential pest and weed problems which might affect enterprise selection and crop yields.

- Climatic factors including annual rainfall, growing seasons etc.

2) Buildings

- Listing of all farm buildings along with their size, capacity and potential uses. Livestock enterprises and crop storage may be severely limited in both number and size of the buildings available.

3) Labour

- Labour should be analyzed for both quantity and quality. Quantity can be measured in man days of labour available from the farm operator (farmer), family members and hired labour.

- Labour quality is more difficult to measure, but any special skills, training and experience should be noted.

4) Machinery

- It is also a fixed resource. The number, size and capacity of the available machinery should be included in the inventory.

5) Capital

- The farmer’s own capital and estimate of amount which can be borrowed represent the capital available for developing whole farm plan.

6) Management

- The assessment of the management resources should include not only overall management ability but also special skills, training, strengths, weaknesses of manager.

- Good management is reflected in higher yields and more efficient use of resources.

II. Identifying enterprises

- Based on resource inventory, certain crop and livestock enterprises will be feasible alternatives.

- Care should be taken to include all possible enterprises to avoid missing enterprise with profit potential.

- Custom and tradition should not be allowed to restrict the list of potential enterprises.

III. Estimation of coefficients

- Each enterprise should be defined on small unit such one acre or hectare for crops and one head for livestock.

- The resource requirements per unit of each enterprise or the technical coefficients must be estimated. The technical coefficients become very important in determining the maximum size of enterprise and the final enterprise combination.

IV. Estimating gross margins

- A gross margin is estimated for a single unit of each enterprise. Gross margin is the difference between total income and total variable costs.

- Calculation of gross margin requires the farmer’s best estimate of yields for each enterprise and expected prices for the output. The calculation of total variable cost requires a list of each variable input needed, the amount required and the price of each input.

V. Developing the whole farm plan

- All information necessary to organize a whole farm plan is now ready for use. The systematic procedure to whole farm planning is identifying the most limiting resource and selecting those enterprises with greatest gross margin per unit of resource.

- Land will generally be a limiting resource and it provides a good starting point. At some point in the planning procedure, a resource other than land may become more limiting and emphasis shifts to identifying enterprises with greatest return or gross margin per unit of this resource.

Farm Planning

- A farm plan is a programme of total farm activity of a farmer drawn up in advance.

- A farm plan should show the enterprises to be taken up on the farm; the practices to be followed in their production, use of labour, investments to be made and similar other details.

- Farm planning enables the farmer to achieve his objectives (Profit maximization or cost minimization) in a more organized manner. It also helps in the analysis of existing resources and their allocation for achieving higher resource use efficiency, farm income and farm family welfare. Farm planning is an approach which introduces desirable changes in farm organization and operation and makes a farm viable unit.

Type of Farm Plans

Simple farm planning

- It is adopted either for a part of the land or for one …

Become Successful With AgriDots

Learn the essential skills for getting a seat in the Exam with

🦄 You are a pro member!

Only use this page if purchasing a gift or enterprise account

Plan

Rs

- Unlimited access to PRO courses

- Quizzes with hand-picked meme prizes

- Invite to private Discord chat

- Free Sticker emailed

Lifetime

Rs

1,499

once

- All PRO-tier benefits

- Single payment, lifetime access

- 4,200 bonus xp points

- Next Level

T-shirt shipped worldwide

Yo! You just found a 20% discount using 👉 EASTEREGG

High-quality fitted cotton shirt produced by Next Level Apparel