👶 Economics Basics

Learn basic Economics concepts

Meaning

- Economics is popularly known as the

Queen of Social Sciences. It studies economic activities of a man living in a society. Economic activities are those activities, which are concerned with the efficient use of scarce means that can satisfy the wants of man. After the basic needs viz., food, shelter and clothing have been satisfied, the priorities shift towards other wants. - Human wants are unlimited, in the sense, that as soon as one want is satisfied another crops up. Most of the means of satisfying these wants are limited, because their supply is less than demand. These means have alternative uses; there emerge a problem of choice.

- Resources being scarce in nature ought to be utilized productively within the available means to derive maximum satisfaction. The knowledge of economics guides us in making effective decisions.

- The subject matter of economics is concerned with wants, efforts and satisfaction. In other words, it deals with decisions regarding the commodities and services to be produced in the economy, how to produce them most economically and how to provide for the growth of the economy.

- Economics is primarily study of Man.

Subject matter of economics

- Economics has subject matter of its own. Economics tells how a man utilizes his limited resources for the satisfaction of unlimited wants. Man has limited amount of time and money. He should spend time and money in such a way that he derives maximum satisfaction. A man wants food, clothing and shelter. To get these things he must have money. For getting money he must make an effort. Effort leads to satisfaction. Thus,

wants-efforts-satisfactionsums up the subject matter of economics initially in a primitive society where the connection between wants efforts and satisfaction is direct.

Divisions of Economics

The subject matter of economics can be explained under two approaches viz., Traditional approach and Modern approach.

Traditional Approach

It considered economics as a science of wealth and divided it into four divisions viz., production, consumption, exchange and distribution.

Production

It is defined as the creation of utility. It involves the processes and methods employed in transformation of tangible inputs (raw materials, semi-finished goods, or subassemblies) and intangible inputs (ideas, information, know -how) into goods or services.

Consumption

It means the use of wealth to satisfy human wants. It also means the destruction of utility or use of commodities and services to satisfy human wants.

Exchange

It implies the transfer of goods from one person to the other. It may occur among individuals or countries. The exchange of goods leads to an increase in the welfare of the individuals through creation of higher utilities for goods and services.

Distribution

- Distribution refers to sharing of wealth that is produced among the different factors of production. It refers to personal distribution and functional distribution of income.

- Personal distribution relates to the forces governing the distribution of income and wealth among the various individuals of a country.

- Functional distribution or factor share distribution explains the share of total income received by each factor of production viz., land, labour, capital and organisation.

Modern Approach

This approach divides subject matter of economics into two divisions i.e., micro economics and macroeconomics. The terms “micro” and “macro” economics were first coined and used by Ragnar Frisch in 1933.

Micro-Economics or Price Theory

- The term “micro-economics” is derived from the Greek word “micro”, which means small or a millionth part.

- It is also known as

price theory. - It is an analysis of the behaviour of small decision-making unit, such as a firm, or an industry, or a consumer, etc. It studies only the employment in a firm or in an industry.

- It also studies the flow of economic resources or factors of production from the resource owners to business firms and the flow of goods and services from the business firms to households. It studies the composition of such flows and how the prices of goods and services in the flow are determined.

- A noteworthy feature of micro-approach is that, while conducting economic analysis on a micro basis, generally an assumption of

full employmentin the economy as a whole is made. On that assumption, the economic problem is mainly that of resource allocation or oftheory of price.

Importance of Micro-Economics

- Functioning of free enterprise economy: It explains the functioning of a free enterprise economy. It tells us how millions of consumers and producers in an economy take decisions about the allocation of productive resources among millions of goods and services.

- Distribution of goods and services: It also explains how through market mechanism goods and services produced in the economy are distributed.

- Determination of prices: It also explains the determination of the relative prices of various products and productive services.

- Efficiency in consumption and production: It explains the conditions of efficiency both in consumption and production.

- Formulation of economic policies: It helps in the formulation of economic policies calculated to promote efficiency in production and the welfare of the masses.

Limitations of Micro-Economics

- It does not give an idea of the functioning of the economy as a whole. It fails to analyse the aggregate employment level of the economy, aggregate demand, inflation, gross domestic product, etc.

- It assumes the existence of “full employment” in the whole economy, which is practically impossible.

Macro-Economics or Theory of Income and Employment

- The term “macro-economics” is derived from the

Greekword “macro”, which means “large”. - Macro-economics is an analysis of aggregates and averages pertaining to the entire economy, such as national income, gross domestic product, total employment, total output, total consumption, aggregate demand, aggregate supply, etc.

- Macro-economics looks to the nation’s total economic activity to determine economic policy and promote economic progress.

Importance of Macro-Economics

- It is helpful in understanding the functioning of a complicated economic system. It also studies the functioning of global economy. With growth of globalisation and WTO regime, the study of macro-economics has become more important.

- It is very important in the formulation of useful economic policies for the nation to remove the problems of unemployment, inflation, rising prices and poverty.

- Through macro-economics, the national income can be estimated and regulated. The per capita income and the people’s living standard are also estimated through macroeconomic study.

Limitations of Macro-Economics

- Individual is ignored altogether. For example, in macro-economics national saving is increased through increasing tax on consumption, which directly affects the consumer welfare.

- The macro-economic analysis overlooks individual differences. For instance, the general price level may be stable, but the prices of food grains may have gone up which ruin the poor. A steep rise in manufactured articles may conceal a calamitous fall in agricultural prices, while the average prices were steady. The agriculturists may be ruined.

Definition

- The word economics has been derived from the

GreekWord “OIKONOMICAS” with “OIKOS” meaning a household and “NOMOS” meaning management. - Kautilya, the great Indian statesman, named his book on state crafts as “Arthashastra‟.

Wealth Definition of Economics

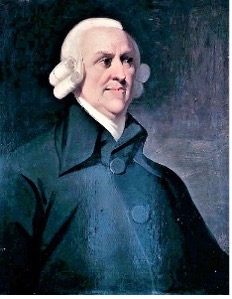

Adam Smith defined Economics as

“An enquiry into the nature and causes of wealth of nations”

in his book, entitled Wealth of Nations. He is regarded as the Father of Economics.

Welfare Definition of Economics

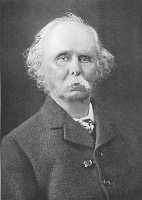

Alfred Marshall in his book Principles of Economics defined

Political Economy or Economics as a study of mankind in the ordinary business of life".

- It examines that part of individual and social action which is most closely connected with the attainment and with the use of the material requisites of well-being.

- Thus it is on the one side a study of wealth, and on the other, and more important side, a part of the

study of man.

Scarcity Definition of Economics

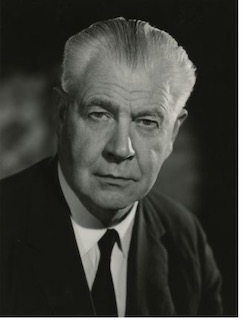

Lionel Robbins in his publication Nature and Significance of Economic Science formulated his conception of Economics based on the scarcity concept.

“Economics is the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses”.

Growth Definition of Economics

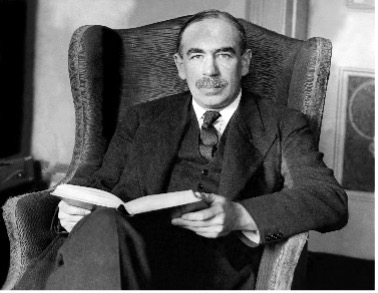

John Maynard Keynes is known as the Father of Modern Economics. He defined economics as

“The study of the administration of scarce resources and of the determinants of employment and income”.

In the words of Nobel prize winner Poul Samuelson,

“Economics is the study of how people and society end up choosing with or without the use of money, to employ scarce productive resources that could have alternative uses, it produces various commodities over time and distributes them for consumption, now or in the future, among various persons and groups in society. It analyses costs and benefits of improving patterns of resources allocation.”

Importance of Economics

- Economics analyses the economic problems of the society. It plays a major role in the economic development of the country by proposing the optimum allocation of resources.

- Knowledge of economics is useful in understanding various national and international events and trends.

- Amarthya Sen, Bharat Ratna recipient was awarded Nobel Prize for Economics (Welfare).

Methods of Economics Investigation

There are two methods of economic investigation that are used in economic theory:

Deductive Method

- This method involves reasoning or inference from the general to the particular or

from the universal to the individuals. - It is also known as the abstract, analytical, hypothetical or apriori method.

Deduction involves four steps:

- Selecting the problems

- Formulating the assumptions

- Formulating the hypothesis through the process of logical reasoning whereby inferences are drawn and

- Verifying the hypothesis

Inductive Method

- This method is also known as

Concrete method,historical methodorrealistic method. It involves reasoning from particulars to the general or from the individual to the universal. This method derives economic generalisations on the basis of experiments and observations. - In this method detailed data are collected on certain economic phenomenon and effort is then made to arrive at certain generalizations which follow from the observations collected.

Economics a Science and an Art

- Science is a systematized body of knowledge in which the facts are so arranged that they speak for themselves. Judged by this standard, economics is certainly a science.

- Economics is also an art because it lays down precepts or formulas to guide people to reach their goals. Economics therefore is a science as well as an art.

Economics – A Social Science

- Economics deal with the activities of people living in an organized community or society, in such activities which relate to the earning and use of wealth or with the problems of scarcity, choice and exchange. Hence it called a social science.

Positive Economics and Normative Economics

- Positive economics is concerned with “what is” whereas Normative economics is concerned with “what ought to be”.

- Positive economics describe economic behaviours without any value judgment while normative economics evaluate them with moral judgment.

- Positive economics is objective while normative economics is subjective.

- The statement, “Price rise as demand increase” is related to positive economics, whereas the statement, “Rising prices is a social evil” is related to normative economics.

Economic Laws

- Economic laws are the principles that govern the actions of the individuals in their economic activities.

“Economic laws are statements of uniformities, which govern human behavior concerning the utilization of limited resources for the achievement of unlimited ends” (Robbins)

Characteristics of Economic Laws

- Economic laws are not the Government laws: The laws of Government are very stringent and any violation of these laws amounts to punishment. Economic laws, on the other hand, are applicable if certain conditions are satisfied.

- Economic Laws are Merely the Statements of tendencies: They only indicates what is likely to happen & not what must happen.

- Economic Laws are Hypothetical: Applicable with certain conditions (conditional) and use ceteris peribus phrase (other factors are held constant).

- Economic Laws are Positive but not Normative: They only describe the economic phenomenon but do not prescribe how it should be. (Not Moral Laws)

- Some Economic Laws are Axiomatic in Character: It means that they are

self-evidentas that of law of diminishing marginal utility and generalizations drawn areuniversally valid. - Economic Laws lack Exactness of the Laws of Science: This prompted

Marshallto compare the economic laws to the laws of tides rather than the simple laws of gravitation. (Not Physical Laws)

Meaning

- Economics is popularly known as the

Queen of Social Sciences. It studies economic activities of a man living in a society. Economic activities are those activities, which are concerned with the efficient use of scarce means that can satisfy the wants of man. After the basic needs viz., food, shelter and clothing have been satisfied, the priorities shift towards other wants. - Human wants are unlimited, in the sense, that as soon as one want is satisfied another crops up. Most of the means of satisfying these wants are limited, because their supply is less than demand. These means have alternative uses; there emerge a problem of choice.

- Resources being scarce in nature ought to be utilized productively within the available means to derive maximum satisfaction. The knowledge of …

Become Successful With AgriDots

Learn the essential skills for getting a seat in the Exam with

🦄 You are a pro member!

Only use this page if purchasing a gift or enterprise account

Plan

- Unlimited access to PRO courses

- Quizzes with hand-picked meme prizes

- Invite to private Discord chat

- Free Sticker emailed

Lifetime

- All PRO-tier benefits

- Single payment, lifetime access

- 4,200 bonus xp points

- Next Level

T-shirt shipped worldwide

Yo! You just found a 20% discount using 👉 EASTEREGG

High-quality fitted cotton shirt produced by Next Level Apparel