🏦 Financial Inclusion - PMJDY, MUDRA & NAFIS Survey

Complete guide to financial inclusion in India - Rangarajan Committee definition, PMJDY scheme, MUDRA loans (Shishu-Kishor-Tarun), and NABARD's NAFIS survey findings with exam-focused facts

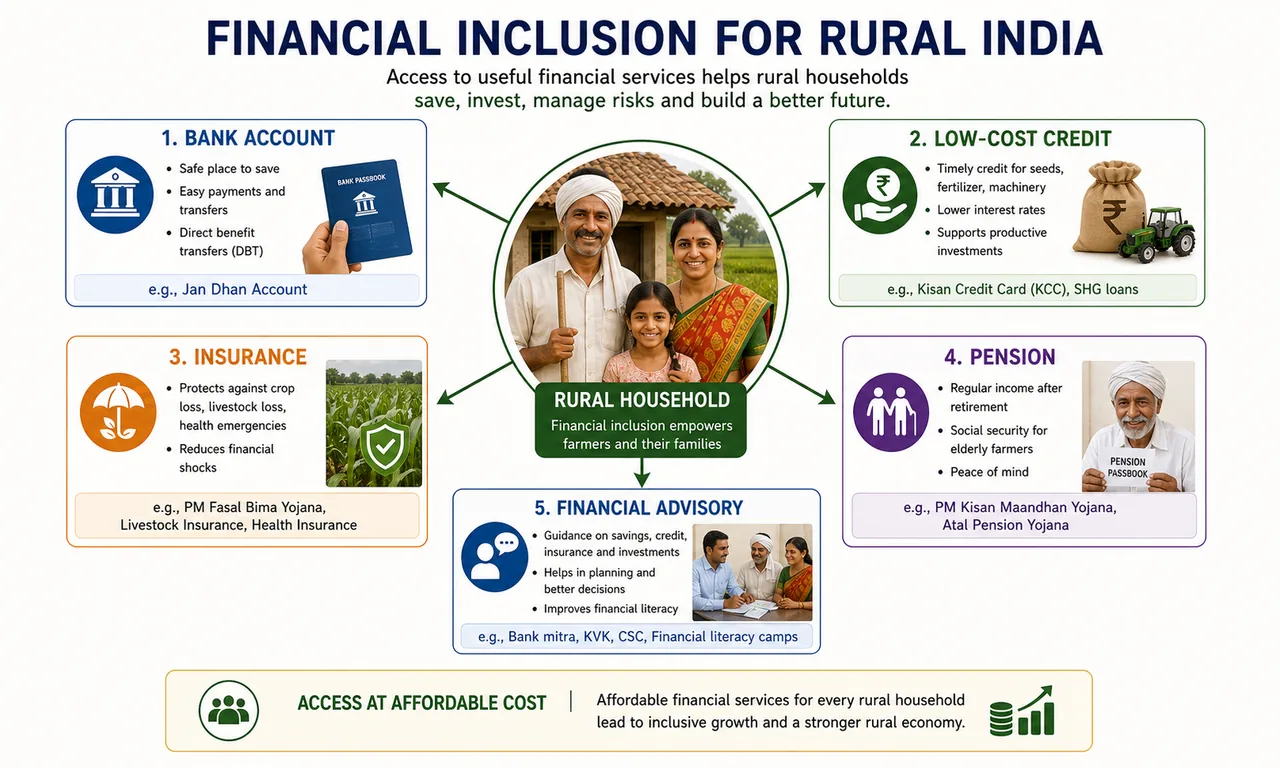

Why Financial Inclusion Matters for Farmers

Consider a marginal farmer in Bundelkhand who needs Rs 20,000 for rabi sowing. Without a bank account, his only option is the village moneylender charging 5% per month (60% per year). By the time he sells his wheat, half his income goes to interest. If this farmer had a bank account and access to a Kisan Credit Card at 4-7% annual interest, he would save thousands of rupees. This is why financial inclusion is not just a banking concept -- it is a matter of farmer survival.

What is Financial Inclusion?

IMPORTANT

Rangarajan Committee (2008) defined financial inclusion as: "The process of ensuring access to financial services and timely and adequate credit where needed by vulnerable groups at an affordable cost."

Financial inclusion means ensuring that every person -- especially the poor, rural, and marginalized -- has access to:

| Financial Service | Why It Matters for Farmers |

|---|---|

| Bank accounts | Safe place to save; receive government subsidies via DBT |

| Low-cost credit | Affordable loans for seeds, fertilizers, equipment |

| Insurance | Protection against crop failure, death, accidents |

| Pension | Old-age security when farming income stops |

| Financial advisory | Guidance on savings, investment, and loan management |

Why is Financial Inclusion Necessary?

- Broadens the resource base -- when rural households save in banks instead of keeping cash at home or buying gold, these savings become available for productive lending, creating a virtuous cycle of growth

- Protects against emergencies -- access to formal savings and credit prevents families from falling into debt traps during crop failures, medical crises, or natural disasters

- Reduces exploitation -- informal moneylenders charge 36-120% interest per annum vs 4-12% by banks; formal banking access breaks the cycle of perpetual debt

TIP

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Why Financial Inclusion Matters for Farmers

Consider a marginal farmer in Bundelkhand who needs Rs 20,000 for rabi sowing. Without a bank account, his only option is the village moneylender charging 5% per month (60% per year). By the time he sells his wheat, half his income goes to interest. If this farmer had a bank account and access to a Kisan Credit Card at 4-7% annual interest, he would save thousands of rupees. This is why financial inclusion is not just a banking concept -- it is a matter of farmer survival.

What is Financial Inclusion?

IMPORTANT

Rangarajan Committee (2008) defined financial inclusion as: "The process of ensuring access to financial services and timely and adequate credit where needed by vulnerable groups at an affordable cost."

Financial inclusion means ensuring that every person -- especially the poor, rural, and marginalized -- has access to:

| Financial Service | Why It Matters for Farmers |

|---|---|

| Bank accounts | Safe place to save; receive government subsidies via DBT |

| Low-cost credit | Affordable loans for seeds, fertilizers, equipment |

| Insurance | Protection against crop failure, death, accidents |

| Pension | Old-age security when farming income stops |

| Financial advisory | Guidance on savings, investment, and loan management |

Why is Financial Inclusion Necessary?

- Broadens the resource base -- when rural households save in banks instead of keeping cash at home or buying gold, these savings become available for productive lending, creating a virtuous cycle of growth

- Protects against emergencies -- access to formal savings and credit prevents families from falling into debt traps during crop failures, medical crises, or natural disasters

- Reduces exploitation -- informal moneylenders charge 36-120% interest per annum vs 4-12% by banks; formal banking access breaks the cycle of perpetual debt

TIP

Exam Tip: Financial inclusion has three benefits -- broadens resource base, protects in emergencies, reduces exploitation by moneylenders.

NABARD All India Financial Inclusion Survey (NAFIS)

The NAFIS survey by NABARD is one of the most comprehensive studies of rural household finances in India. Key facts are frequently asked in exams.

Survey Overview

| Parameter | Detail |

|---|---|

| Conducted by | NABARD |

| Reference year | 2015-16 |

| Households covered | 40,327 rural households |

| Villages | 2,016 villages in 245 districts across 29 states |

| Population covered | 1,87,518 |

| Data collection | Paperless -- Computer Aided Personal Interview (CAPI) |

| Commissioned | 2016 |

Key Income Findings

| Parameter | Agricultural Households | Non-Agricultural Households | All Rural Households |

|---|---|---|---|

| Average annual income | Rs 1,07,172 | Rs 87,228 | Rs 96,708 |

| Income advantage | 23% higher than non-agricultural | -- | -- |

NOTE

Agricultural households earn 23% more than non-agricultural households. Farm households = those with >Rs 5,000 value of produce from agricultural operations.

Income Sources of Agricultural Households:

| Source | Share |

|---|---|

| Cultivation | 34% |

| Wages | 34% |

| Salaries | 16% |

| Livestock | 8% |

| Non-farm sector | 6% |

| Others | 2% |

Key fact: 48% of rural families are agricultural households -- slightly less than half of all rural households are directly engaged in farming.

Debt, Savings & Insurance Findings

| Parameter | Agricultural Households | Non-Agricultural Households | All Rural |

|---|---|---|---|

| Incidence of Indebtedness (IOI) | 52.5% | 42.8% | 47.4% |

| Average Outstanding Debt (indebted) | Rs 1,04,602 | Rs 76,731 | Rs 91,407 |

| Bank account ownership | 55% | -- | 88.1% |

| Average savings per annum | -- | -- | Rs 17,488 |

| Insurance coverage | 26% | 25% | -- |

| Pension coverage | 20.1% | 18.9% | -- |

TIP

Exam Fact: Higher IOI among agricultural households (52.5% vs 42.8%) reflects the capital-intensive nature of farming. Bank account ownership at 88% but only 26% insurance coverage shows that account opening alone is not enough -- financial literacy and services must follow.

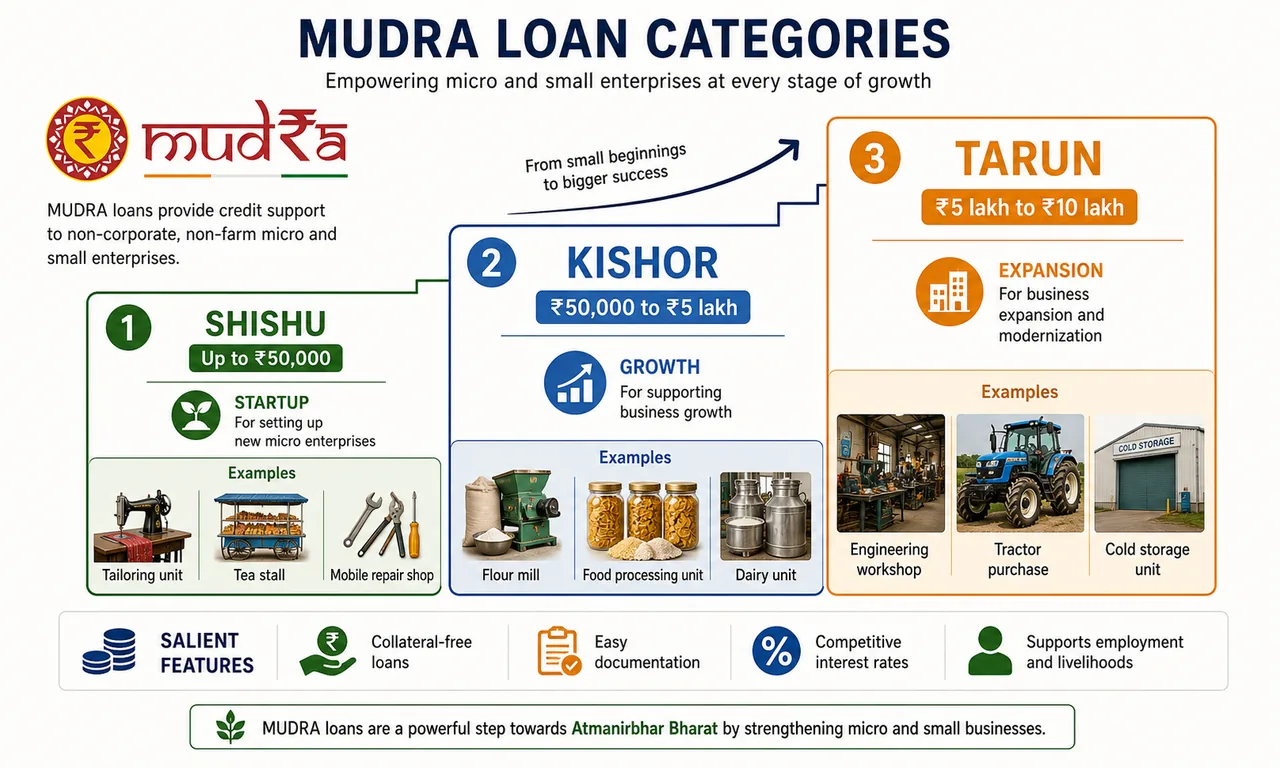

Pradhan Mantri Mudra Yojana (PMMY)

IMPORTANT

PMMY launched on 8th April, 2015 to "fund the unfunded". MUDRA is a refinancing institution (subsidiary of SIDBI) -- it does NOT lend directly to borrowers.

What is MUDRA?

A rural woman in Bihar runs a small pickle-making business from home. She needs Rs 30,000 for glass jars, raw materials, and a sealing machine. No bank would give her a loan -- she has no collateral, no formal business registration. PMMY was designed precisely for entrepreneurs like her.

- Full form: Micro Units Development and Refinance Agency

- Purpose: Fund non-corporate, non-farm small/micro enterprises that were invisible to the formal banking system

- Activities covered: Manufacturing, Services, Retail, and Agriculture Allied Activities

- Loan limit: Up to Rs 10 lakh for non-farm income generating activities

- Lending model: MUDRA is a refinancing institution -- it provides funds to banks and lending institutions at lower rates, which in turn lend to end borrowers (similar to how NABARD refinances agricultural loans)

- Parent body: Wholly owned subsidiary of SIDBI (Small Industries Development Bank of India)

- Online application: Available on Udyamimitra portal (www.udyamimitra.in)

MUDRA Loan Categories

| Category | Loan Amount | Stage Symbolized | Target |

|---|---|---|---|

| Shishu (Child) | Up to Rs 50,000 | Inception/startup phase | At least 60% of total credit must flow here |

| Kishor (Adolescent) | Rs 50,000 to Rs 5 lakh | Growth phase | Balance shared with Tarun |

| Tarun (Young Adult) | Rs 5 lakh to Rs 10 lakh | Maturity/expansion phase | Balance shared with Kishor |

TIP

Mnemonic -- "SKT": Shishu (smallest, 60% priority) --> Kishor (middle) --> Tarun (largest). Think: a business grows from child to youth.

Where to Get MUDRA Loans

Borrowers can approach any of these institutions:

- Public Sector Commercial Banks

- Regional Rural Banks (RRBs)

- Small Finance Banks (SFBs)

- Micro Finance Institutions (MFIs)

- Non-Banking Finance Companies (NBFCs)

Eligibility

- Any Indian citizen with a business plan for non-farm income generating activity

- Credit need must be less than Rs 10 lakh

- Budget 2019-20 special provision: Every verified women SHG member with a Jan-Dhan account gets Rs 5,000 overdraft; one woman per SHG eligible for loan up to Rs 1 lakh under MUDRA

Borrower-Friendly Features

| Feature | Detail |

|---|---|

| Processing fees | None |

| Collateral | Not required |

| Repayment period | Up to 5 years |

| Subsidy | No subsidy under PMMY, but if linked to a Government scheme providing capital subsidy, that subsidy applies |

| Default condition | Applicant must not be a defaulter of any bank/financial institution |

Implementation Structure

- Government proposes to set up MUDRA Bank through statutory enactment

- MUDRA Bank regulates and refinances all MFIs lending to micro/small business entities

- Partners with state/regional coordinators to provide finance to Last Mile Financers (local cooperative banks, NBFCs, MFIs at grassroots level)

Pradhan Mantri Jan Dhan Yojana (PMJDY)

IMPORTANT

PMJDY announced on 15th August, 2014 as a National Mission on Financial Inclusion. It is the world's largest financial inclusion programme with approximately 40 crore accounts opened.

The Problem PMJDY Solved

Before PMJDY, millions of rural households -- including farming families -- had no bank accounts. Government subsidies meant for farmers were siphoned off by intermediaries. A farmer entitled to Rs 6,000 under PM-KISAN would never receive it without a bank account. PMJDY created the infrastructure for Direct Benefit Transfer (DBT), the JAM trinity (Jan Dhan-Aadhaar-Mobile), and digital payments in rural India.

Objectives

- Bring financially excluded poor into the banking system

- Cover both urban and rural areas

- Reduce corruption in government subsidies through DBT

- Support Digital India -- PMJDY accounts form the foundation of digital payments

- Strengthen the Indian economy through greater financial participation

Salient Features

| Feature | Detail |

|---|---|

| Account type | Basic Saving Deposit Bank Account (BSBD) -- zero balance, no minimum balance |

| Overdraft facility | Rs 10,000 for Aadhaar-linked accounts (after 6 months of satisfactory operation) |

| Debit card | RuPay card (India's indigenous card network by NPCI) |

| Accident insurance | Rs 1 lakh personal accident cover (HDFC Ergo) |

| Life cover | Rs 30,000 (LIC) |

| Business correspondents | Minimum Rs 5,000 monthly remuneration to BCs providing last-mile banking |

Phased Implementation

| Phase | Period | Focus |

|---|---|---|

| Phase I | 15 Aug 2014 - 14 Aug 2015 | Universal banking access within 5 km; one BSBD account per household with RuPay card; financial literacy at village level; DBT expansion; KCC issuance |

| Phase II | 15 Aug 2015 - 14 Aug 2018 | Micro-insurance; unorganized sector pension (Swavalamban) through BCs |

| Phase III | Beyond 14 Aug 2018 | Shift from "Every Household" to "Every Adult"; enhanced benefits |

Phase III Enhancements

| Feature | Before Phase III | After Phase III |

|---|---|---|

| Coverage target | Every household | Every adult |

| Overdraft limit | Rs 5,000 | Rs 10,000 |

| Unconditional overdraft | None | Up to Rs 2,000 (no conditions) |

| OD age limit | 18-60 years | 18-65 years |

| Accidental insurance (new accounts after 28.8.18) | Rs 1 lakh | Rs 2 lakh |

Achievements

| Metric | Achievement |

|---|---|

| Total accounts | Approximately 40 crore (as of Nov 2019) |

| Total deposits | Over Rs 1.30 lakh crore |

| Women account holders | 53% of all Jan Dhan accounts |

| Rural/semi-urban accounts | 59% of all Jan Dhan accounts |

Impact

- Created infrastructure for DBT -- saved the government over Rs 2.2 lakh crore by eliminating fake and duplicate beneficiaries

- During COVID-19, under Pradhan Mantri Garib Kalyan Yojana, Rs 1,500 per account was remitted in three equal monthly installments to 20 crore women Jan Dhan account holders within days of the lockdown announcement

- Demonstrated that PMJDY is not just about opening accounts -- it is about building a delivery infrastructure for welfare

TIP

Exam Quick Recall for PMJDY

- Launch date: 15 Aug 2014

- Accounts: 40 crore

- Women account holders: 53%

- Rural accounts: 59%

- Overdraft: Rs 10,000

- RuPay insurance: Rs 2 lakh (post-2018)

- Life cover: Rs 30,000

Summary Cheat Sheet

| Topic | Key Facts |

|---|---|

| Financial Inclusion definition | Rangarajan Committee (2008) -- access to financial services at affordable cost for vulnerable groups |

| NAFIS Survey | NABARD; 2015-16; 40,327 households; Agri income Rs 1,07,172 vs Non-agri Rs 87,228 |

| Farm vs Non-farm income | Agricultural households earn 23% more |

| Rural IOI | 47.4% overall; 52.5% for agricultural households |

| PMMY/MUDRA | 8 April 2015; "Fund the unfunded"; subsidiary of SIDBI; refinancing institution |

| MUDRA categories | Shishu (up to 50K, 60% priority), Kishor (50K-5L), Tarun (5L-10L) |

| MUDRA features | No processing fee, no collateral, up to 5 years repayment |

| PMJDY | 15 Aug 2014; world's largest financial inclusion; ~40 crore accounts |

| PMJDY features | BSBD account, RuPay card, Rs 10K OD, Rs 2L accident cover, Rs 30K life cover |

| PMJDY Phase III | Every adult (not just household); Rs 2,000 unconditional OD; age 18-65 |

| COVID relief via PMJDY | Rs 1,500 x 3 months to 20 crore women account holders |