🤝 Income Support, Infrastructure & Welfare Schemes for Farmers

Complete guide to PM-KISAN, PMFBY, PM-KMY, PM-AASHA, PM KUSUM, AIF, AHIDF, PMMSY, PMFME, NABARD schemes, Kisan Vikas Patra, and SMAM -- with agricultural examples, comparisons, and exam tips.

Why Income Support Matters

A marginal rice farmer in Odisha earns Rs 40,000 from his 0.5 hectare Kharif crop. After deducting input costs of Rs 25,000, his net income is just Rs 15,000 for six months. During the Rabi season, he has no irrigation and no income. Income support schemes bridge this gap by providing guaranteed cash transfers, pensions, fair prices, clean energy, savings instruments, and mechanization support -- ensuring farmers can sustain their families year-round.

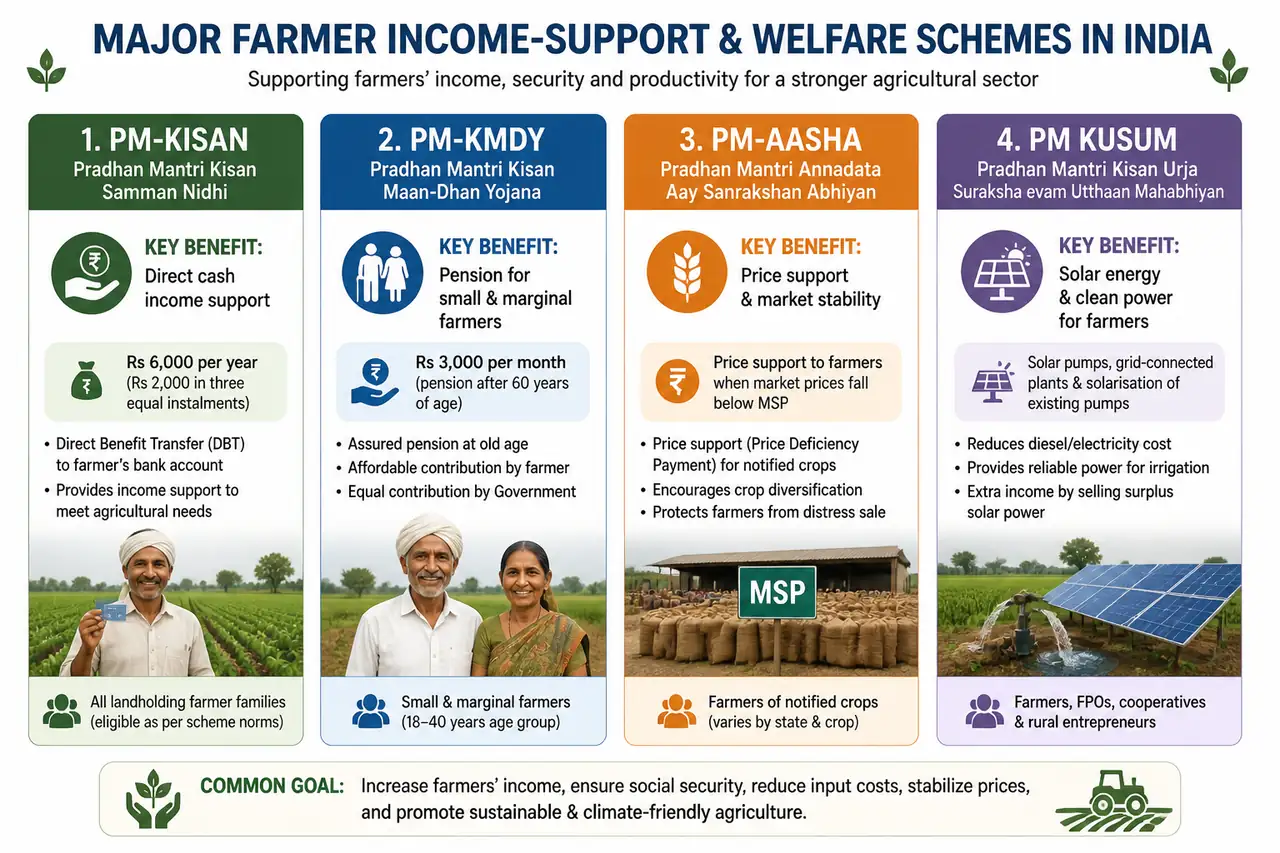

PM-KISAN (Pradhan Mantri Kisan Samman Nidhi)

One of the largest direct income support schemes in the world. It provides guaranteed cash transfers to every eligible farmer household regardless of crop output or market conditions.

IMPORTANT

PM-KISAN: Income support of Rs 6,000/year in 3 instalments of Rs 2,000 each. Effective from 1.12.2018. Now covers all farmers irrespective of land holding. It is a Central Sector scheme with 100% Central funding.

| Feature | Detail |

|---|---|

| Full name | Pradhan Mantri Kisan Samman Nidhi |

| Scheme type | Central Sector (100% funded by Centre) |

| Effective from | 1 December 2018 |

| Income support | Rs 6,000 per year |

| Instalments | 3 instalments of Rs 2,000 each (Apr-Jul, Aug-Nov, Dec-Mar) |

| Original eligibility | Small and marginal farmers (up to 2 hectares) |

| Revised eligibility | All land-owning farmers irrespective of land holding |

| Transfer mode | Direct Benefit Transfer (DBT) to bank accounts |

| Nodal ministry | Department of Agriculture, Cooperation & Farmers Welfare |

| Family definition | Husband, wife, and minor children |

| Beneficiary identification | Responsibility of State/UT Governments |

| Installments released | 22 installments as of March 2026 |

| Top beneficiary states | Uttar Pradesh > Maharashtra |

| eKYC | AADHAAR eKYC mandatory since 2023 |

| Budget 2025-26 | Rs 63,500 crore (up from Rs 60,000 crore) |

Agricultural example: A wheat farmer in UP with 3 hectares receives Rs 2,000 directly in his bank account every four months. Over the year, he gets Rs 6,000 -- enough to buy 2 bags of DAP fertilizer for his next crop.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Why Income Support Matters

A marginal rice farmer in Odisha earns Rs 40,000 from his 0.5 hectare Kharif crop. After deducting input costs of Rs 25,000, his net income is just Rs 15,000 for six months. During the Rabi season, he has no irrigation and no income. Income support schemes bridge this gap by providing guaranteed cash transfers, pensions, fair prices, clean energy, savings instruments, and mechanization support -- ensuring farmers can sustain their families year-round.

PM-KISAN (Pradhan Mantri Kisan Samman Nidhi)

One of the largest direct income support schemes in the world. It provides guaranteed cash transfers to every eligible farmer household regardless of crop output or market conditions.

IMPORTANT

PM-KISAN: Income support of Rs 6,000/year in 3 instalments of Rs 2,000 each. Effective from 1.12.2018. Now covers all farmers irrespective of land holding. It is a Central Sector scheme with 100% Central funding.

| Feature | Detail |

|---|---|

| Full name | Pradhan Mantri Kisan Samman Nidhi |

| Scheme type | Central Sector (100% funded by Centre) |

| Effective from | 1 December 2018 |

| Income support | Rs 6,000 per year |

| Instalments | 3 instalments of Rs 2,000 each (Apr-Jul, Aug-Nov, Dec-Mar) |

| Original eligibility | Small and marginal farmers (up to 2 hectares) |

| Revised eligibility | All land-owning farmers irrespective of land holding |

| Transfer mode | Direct Benefit Transfer (DBT) to bank accounts |

| Nodal ministry | Department of Agriculture, Cooperation & Farmers Welfare |

| Family definition | Husband, wife, and minor children |

| Beneficiary identification | Responsibility of State/UT Governments |

| Installments released | 22 installments as of March 2026 |

| Top beneficiary states | Uttar Pradesh > Maharashtra |

| eKYC | AADHAAR eKYC mandatory since 2023 |

| Budget 2025-26 | Rs 63,500 crore (up from Rs 60,000 crore) |

Agricultural example: A wheat farmer in UP with 3 hectares receives Rs 2,000 directly in his bank account every four months. Over the year, he gets Rs 6,000 -- enough to buy 2 bags of DAP fertilizer for his next crop.

Who is Excluded?

- Institutional landholders

- Former and current holders of constitutional posts

- Serving or retired government officers and employees

- Income tax payers

- Professionals (doctors, engineers, lawyers, chartered accountants)

Beneficiary Statistics (as of December 2019)

| State | Beneficiaries |

|---|---|

| Uttar Pradesh | 1.97 crore (highest -- largest agricultural population) |

| Maharashtra | 81 lakh |

| Rajasthan | 56 lakh |

| West Bengal | 0 (state refused to share data; runs own Krishak Bandhu scheme) |

| Lakshadweep | 0 |

| Total | 8.62 crore |

Revised scheme expected to cover ~14.5 crore beneficiaries with estimated Central expenditure of Rs 87,217.50 crore (2019-20).

Latest PIB-Backed PM-KISAN Developments (2025-26)

The scheme is no longer tested only as “Rs 6,000 in three instalments”. In the latest PIB releases, PM-KISAN is presented as both:

- a direct income-support scheme

- a digitally verified farmer-benefit platform

21st instalment context

PIB’s 14 November 2025 note stated that PM-KISAN had already crossed:

- ₹3.70 lakh crore in direct transfers

- to over 11 crore farmer families

- through 20 instalments

The same official release also highlighted the digital-strengthening layer:

- Aadhaar-based eKYC

- PM-KISAN mobile app

- Kisan-eMitra

- launch of Farmer Registry

This is important because Farmer Registry is being used as a verified data bridge between:

- farmer identity

- land-linked records

- future scheme delivery

22nd instalment context

The official 19 March 2026 PIB backgrounder on the 22nd instalment reported:

- DBT of over ₹18,640 crore

- to 9.32 crore farmers

PIB's later 24 March 2026 release pushed the cumulative scheme picture further. It stated that PM-KISAN had disbursed over:

- ₹4.27 lakh crore

- through 22 instalments

- since inception

This makes PM-KISAN relevant not only as a welfare fact, but also as one of the largest recurring rural liquidity support platforms in Indian agriculture.

This makes the current-exam version of PM-KISAN stronger than the old static note. You should now remember:

- scheme amount

- instalment count

- latest beneficiary count

- cumulative transfers

- digital-delivery architecture

IMPORTANT

PM-KISAN questions now increasingly combine money amount + instalment number + beneficiary count + digital verification mechanism.

PM-KISAN and KCC Convergence

The Government launched a drive to ensure all PM-KISAN beneficiaries also get KCC:

- All KCC charges (processing, documentation, inspection, ledger folio, service charges) waived for loans up to Rs 3 lakh by Indian Banks' Association (IBA)

- Banks must issue KCC within 14 days (2 weeks) of receiving a completed application

- PM-KISAN beneficiaries can approach their PM-KISAN account bank branch for KCC

Agricultural example: A sugarcane farmer in Karnataka who already receives PM-KISAN can walk into the same bank and get a KCC within 2 weeks with zero charges -- combining income support with cheap credit.

TIP

Exam mnemonic -- PM-KISAN "6-3-2": Rs 6,000/year, 3 instalments, Rs 2,000 each.

PMFBY (Pradhan Mantri Fasal Bima Yojana)

Income support alone does not protect a farmer when the crop itself is damaged. That is where PMFBY becomes important. In exam terms, PM-KISAN supports income flow, while PMFBY protects against crop-loss shock.

IMPORTANT

PMFBY was launched from Kharif 2016 as India's flagship crop-insurance scheme. The current-affairs angle became stronger after the 18 November 2025 reform that expanded localised-risk cover.

| Feature | Detail |

|---|---|

| Full name | Pradhan Mantri Fasal Bima Yojana |

| Launch | Kharif 2016 |

| Core purpose | Crop-risk insurance against yield loss and notified calamities |

| Current affairs reform date | 18 November 2025 |

| New localised-risk cover | Wild animal attack |

| Reintroduced localised calamity | Paddy inundation |

| Rollout timing for reform | From Kharif 2026 |

| Loss reporting rule | Within 72 hours |

| Reporting mode | Crop Insurance App with geotagged photographs |

| Budget 2025-26 | Rs 15,000 crore |

Why the 2025 PMFBY reform matters

The PIB note shows that PMFBY is becoming more responsive to actual farm-level risk, not just broad weather categories.

The reform matters especially for:

- forest-adjacent districts where wild animal damage is common

- flood-prone paddy belts where field inundation causes crop loss

- states where farm losses are highly localised, even when district-level production looks normal

This is an important policy direction: PMFBY is moving toward a more granular localised-risk framework.

PM-KISAN vs PMFBY

| Scheme | What it protects |

|---|---|

| PM-KISAN | basic household liquidity and seasonal spending support |

| PMFBY | compensates when crop output is hit by insured risks |

Agricultural example: A paddy farmer in Assam may still receive the regular PM-KISAN instalment, but if her crop is damaged by notified inundation under the revised PMFBY framework, insurance support addresses the actual production shock.

Comparison with State Income Support Schemes

PM-KMY / PM-KMDY (Pradhan Mantri Kisan Maan-Dhan Yojana)

Addresses the critical issue of old-age security for farmers. Unlike salaried workers with pension benefits, most farmers have no retirement income.

NOTE

PM-KMY is still active in 2026. It provides a minimum assured pension of ₹3,000/month after age 60 to eligible small and marginal farmers. Entry age is 18-40 years, monthly contribution is ₹55 to ₹200, the Central Government matches the contribution rupee-for-rupee, and the pension fund is managed by LIC.

| Feature | Detail |

|---|---|

| Full name | Pradhan Mantri Kisan Maan-Dhan Yojana |

| Type | Voluntary and contributory pension scheme |

| Effective from | 9 August 2019 |

| Eligibility | Small and Marginal Farmers (land up to 2 hectares) |

| Entry age | 18 to 40 years |

| Monthly pension | ₹3,000 on attaining age 60 |

| Monthly contribution | ₹55 (entry at age 18) to ₹200 (entry at age 40) |

| Government matching | Equal to farmer's contribution |

| Pension Fund Manager | LIC (Life Insurance Corporation of India) |

| Spouse eligibility | Separate pension of ₹3,000 on making separate contributions |

| Family pension | Surviving spouse gets 50% pension = ₹1,500/month after subscriber's death post-vesting |

| Enrolled farmers | 24.95 lakh as of 2 February 2026 |

Agricultural example: A 25-year-old paddy farmer in Assam joins PM-KMY by contributing ₹80/month. The Government matches it with another ₹80. At age 60, he receives ₹3,000 every month for life. If his wife also enrolls separately, the couple can receive ₹6,000/month together after both turn 60.

Why PM-KMY Matters

PM-KISAN gives current income support, but PM-KMY addresses a different problem: old-age income security. Small and marginal farmers often have no formal retirement benefit, no provident fund, and irregular farm income. PM-KMY creates a pension bridge for the years after active cultivation declines.

IMPORTANT

Do not confuse the two schemes:

- PM-KISAN = ₹6,000/year income support in 3 instalments

- PM-KMY = ₹3,000/month pension after age 60 under a contributory model

Key Provisions

| Scenario | What Happens |

|---|---|

| Farmer dies before age 60 | Spouse can continue the scheme by paying regular contribution, or exit and take back subscriber contribution with applicable interest under scheme rules |

| Farmer dies after age 60 | Spouse receives 50% of pension = ₹1,500/month as family pension |

| Both farmer and spouse die | Accumulated corpus returns to Pension Fund |

| Exit before 10 years | Subscriber's contribution returned with savings bank interest |

| Exit after 10 years but before age 60 | Subscriber's contribution returned with actual fund return or savings bank interest, whichever is higher |

| Default in contributions | Scheme can be revived by paying outstanding dues with prescribed/nominal interest |

| PM-KISAN linkage | Farmer can auto-debit contribution from PM-KISAN instalments |

TIP

Exam mnemonic -- PM-KMY "3-60-55-200": ₹3,000 pension at age 60; contribution ranges from ₹55 to ₹200 per month.

Eligibility and Exclusions

PM-KMY is meant for landholding small and marginal farmers only.

- Cultivable landholding must be up to 2 hectares

- Farmer must be in the 18-40 years age band at enrollment

- Farmer must be identified through the State/UT land records

Major exclusion categories:

- Farmers already covered under NPS, ESIC, EPFO, or other statutory social security schemes

- Farmers who have opted for PM-SYM or other overlapping Government pension/social-security schemes

- Higher-income / institutional exclusion categories as defined in scheme guidelines

Contribution Slab at a Glance

| Entry Age | Farmer Contribution | Government Contribution | Total Monthly Pension Fund Contribution |

|---|---|---|---|

| 18 years | ₹55 | ₹55 | ₹110 |

| 25 years | ₹80 | ₹80 | ₹160 |

| 30 years | ₹105 | ₹105 | ₹210 |

| 35 years | ₹150 | ₹150 | ₹300 |

| 40 years | ₹200 | ₹200 | ₹400 |

The contribution remains fixed according to entry age until the subscriber reaches 60 years.

Enrollment, Status Check, and eKYC Context

Farmers can enroll or verify scheme status through:

- Official PM-KMY/PM-Kisan documents and portal flow

- Students should remember maandhan.in as the operational portal/brand most commonly associated with registration and status support

- Common Service Centres (CSCs)

- Maandhan helpline: 1800-267-6888

Operationally, the scheme is Aadhaar-linked and bank-account linked, and enrollment is done through authenticated records. PM-KISAN eKYC is explicitly mandatory, while for PM-KMY the official scheme documents emphasize Aadhaar-based enrollment, bank auto-debit, and authenticated beneficiary records. In practice, students should remember the scheme as part of the broader Aadhaar-seeded farmer-benefit ecosystem.

PM-AASHA (Pradhan Mantri Annadata Aay Sanrakshan Abhiyan)

Ensures farmers receive fair prices for their produce. While MSP is announced for many crops, effective procurement at MSP was historically limited to wheat and rice in a few states. PM-AASHA fills this gap.

IMPORTANT

PM-AASHA (approved September 2018) has 3 sub-schemes: PSS (physical procurement by NAFED), PDPS (bank transfer of price difference for oilseeds), and PPPS (private sector procurement pilot).

| Feature | Detail |

|---|---|

| Full name | Pradhan Mantri Annadata Aay Sanrakshan Abhiyan |

| Approved | September 2018 |

| Aim | Ensuring remunerative prices (covering cost of production + reasonable profit) |

| MSP formula | 1.5 times the all-India weighted average Cost of Production (recommended by Swaminathan Commission) |

| Budget 2026-27 allocation | Rs 7,200 crore |

Three Sub-Schemes Compared

| Feature | PSS (Price Support) | PDPS (Price Deficiency Payment) | PPPS (Private Procurement Pilot) |

|---|---|---|---|

| Mechanism | Physical procurement at MSP | Cash transfer of MSP-market price difference | Private agencies procure at MSP |

| Crops | Pulses, oilseeds, copra | Oilseeds only | Selected crops |

| Implementing agency | NAFED (Central Nodal Agency) | Direct bank transfer | Selected private agencies |

| Government liability | Procurement expenditure + losses up to 25% of production | Difference between MSP and market price | Losses up to 15% of MSP |

| Physical procurement? | Yes | No | Yes (by private sector) |

Agricultural examples:

- PSS: Tur dal price in Latur (Maharashtra) falls to Rs 4,500/quintal against MSP of Rs 6,000. NAFED steps in and buys at Rs 6,000.

- PDPS: Soybean sells at Rs 3,200/quintal in the mandi against MSP of Rs 3,880. The farmer receives Rs 680/quintal directly in his bank account.

- PPPS: A private company is authorized to procure mustard at MSP in selected districts of Rajasthan, with Government compensating any losses.

TIP

Exam mnemonic -- PM-AASHA "PPP": PSS (Physical procurement), PDPS (Price difference payment), PPPS (Private procurement pilot).

PM KUSUM (Kisan Urja Suraksha evam Utthaan Mahabhiyan)

Tackles the dual challenge of energy security and water security for farmers by promoting solar energy in agriculture.

| Feature | Detail |

|---|---|

| Full name | Kisan Urja Suraksha evam Utthaan Mahabhiyan |

| Launched by | Ministry of New and Renewable Energy (MNRE) |

| Objective | Financial and water security for farmers |

| Target solar capacity | 25,750 MW by 2022 |

| Beneficiaries | 20 lakh farmers (standalone solar pumps) + 15 lakh farmers (grid-connected) |

Three Components Compared

| Feature | Component A | Component B | Component C |

|---|---|---|---|

| What | Ground-mounted solar power plants | Standalone solar pumps | Solarisation of grid-connected pumps |

| Capacity | 500 kW to 2 MW per project | Up to 7.5 HP per pump | Solar PV up to 2x pump capacity |

| Who sets up | Farmers, FPOs, cooperatives, panchayats | Individual farmers | Individual farmers |

| Revenue | Sell power to DISCOMs at Feed-in-Tariff | Save on diesel/electricity | Use solar for irrigation + sell surplus to DISCOM |

| Land | Barren/fallow land | -- | -- |

| General states subsidy | -- | 60% (30% Centre + 30% State) | 60% (30% Centre + 30% State) |

| Special states subsidy | -- | 80% (50% Centre + 30% State) | 80% (50% Centre + 30% State) |

| Farmer's share (general) | -- | 40% (can get bank loan for 30%) | 40% (can get bank loan for 30%) |

| Farmer's share (special) | -- | 20% (can get bank loan for 10%) | 20% (can get bank loan for 10%) |

Special category states: North-Eastern States, Sikkim, J&K, Himachal Pradesh, Uttarakhand, Lakshadweep, A&N Islands.

Agricultural examples:

- Component A: A farmer cooperative in Rajasthan installs a 1 MW solar plant on 5 acres of barren rocky land. The DISCOM buys power at the Feed-in-Tariff, earning the cooperative Rs 5-6 lakh/year.

- Component B: A vegetable farmer in Bihar replaces his diesel pump with a 5 HP solar pump. He saves Rs 30,000/year on diesel and irrigates whenever needed -- free of cost.

- Component C: A sugarcane farmer in Maharashtra with a grid-connected 7.5 HP pump installs 15 kW solar panels (2x capacity). He uses solar power for irrigation and sells surplus electricity, earning Rs 15,000-20,000/year.

TIP

DISCOM = Distribution Company (distributes electricity to consumers). Feed-in-Tariff (FiT) = guaranteed price at which DISCOM buys solar power. FPO = Farmer Producer Organisation.

AIF (Agriculture Infrastructure Fund)

Moves beyond direct income support and strengthens the post-harvest ecosystem. Farmers lose income not only because yields fail, but also because storage, grading, cold chain, and aggregation are weak. AIF addresses that infrastructure gap.

IMPORTANT

AIF is a Central Sector Scheme launched on 15 May 2020 with a corpus of ₹1 lakh crore for medium- and long-term debt financing of post-harvest management infrastructure and community farming assets.

| Feature | Detail |

|---|---|

| Launch date | 15 May 2020 |

| Corpus | ₹1 lakh crore |

| Scheme duration | FY 2020-21 to 2032 |

| Scheme type | Central Sector Scheme |

| Ministry | Department of Agriculture & Farmers Welfare |

| Interest subvention | 3% p.a. on loans up to ₹2 crore |

| Subvention period | Up to 7 years |

| Credit guarantee | CGTMSE for eligible loans up to ₹2 crore |

| Borrower contribution | Minimum 10% of project cost |

| Moratorium | 6 months to 2 years |

Eligible Beneficiaries

- PACS, marketing cooperatives, and multipurpose cooperatives

- FPOs and FPO federations

- SHGs and JLGs

- Individual farmers, agri-entrepreneurs, and start-ups

- PPP projects sponsored by Central/State agencies or local bodies

Eligible Infrastructure

- Warehouses, silos, and godowns

- Cold storage and cold chain projects

- Assaying, grading, sorting, and pack houses

- Primary processing centers

- Community irrigation or other community farming assets

Agricultural example: An FPO in Nashik sets up a pre-cooling and onion storage unit under AIF. Instead of distress-selling immediately after harvest, members store produce and sell later at a better price, raising realized income.

Latest PIB-Backed AIF Progress (2026)

The current-affairs value of AIF increased after PIB's 3 February 2026 update, which highlighted that from July 2020 to 26 January 2026:

- sanctioned loan amount reached ₹80,224.15 crore

- total projects reached 1,50,431

- total mobilised investment reached ₹1,27,508 crore

This matters because AIF should not be read only as a "loan scheme". It is part of the structural resilience side of agricultural finance:

- better storage reduces distress sale

- better grading and assaying improves price discovery

- better primary processing supports value addition

- stronger post-harvest assets reduce income instability after harvest

In descriptive answers, AIF can be framed as the infrastructure pillar of farmer income security, just as PM-KISAN is the cash-support pillar and PMFBY is the crop-risk pillar.

AHIDF (Animal Husbandry Infrastructure Development Fund)

Income support is not limited to crop farming. A large share of rural cash flow comes from dairy, meat, feed, and livestock value chains. AHIDF finances this side of farm income.

IMPORTANT

AHIDF was launched on 14 July 2020 to finance animal husbandry infrastructure. The revised outlay is ₹29,610.25 crore, applications are accepted up to 31 March 2026, and disbursements are permitted up to 31 March 2027.

| Feature | Detail |

|---|---|

| Launch date | 14 July 2020 |

| Revised outlay | ₹29,610.25 crore |

| Ministry | Fisheries, Animal Husbandry & Dairying |

| Loan coverage | Up to 90% of project cost |

| Interest subvention | 3% p.a. |

| Subvention period | 8 years including moratorium |

| Repayment period | Up to 10 years |

| Moratorium | Up to 2 years |

| DIDF merger | Merged into AHIDF in February 2024 |

Eligible Activities

- Milk processing and value-added dairy products

- Meat processing units

- Animal feed plants

- Breed multiplication farms

- Waste-to-wealth projects

- Veterinary vaccine and drug production

Margin Requirement

| Category | Beneficiary Contribution |

|---|---|

| Micro & Small enterprises | 10% |

| Medium enterprises | 15% |

| Others | 25% or more |

Credit Support

- AHIDF-specific guarantee fund managed by NABARD

- Additional CGTMSE support for eligible smaller loans

Agricultural example: A dairy entrepreneur in Punjab sets up a paneer and flavored milk unit with AHIDF support. Instead of selling raw milk alone, the farmer captures value addition and earns higher margins.

PMMSY (Pradhan Mantri Matsya Sampada Yojana)

Fisheries is one of the fastest-growing allied sectors, so it is important in agricultural finance even for AFO preparation.

IMPORTANT

PMMSY was launched on 10 September 2020 as the flagship fisheries scheme. Original outlay is ₹20,050 crore, and the scheme has been extended to FY 2025-26.

| Feature | Detail |

|---|---|

| Launch date | 10 September 2020 |

| Ministry | Department of Fisheries |

| Outlay | ₹20,050 crore |

| Vision | Blue Revolution |

| Duration | Extended to FY 2025-26 |

| Target fish production | 22 million metric tons |

| Aquaculture productivity target | 5 tons/hectare |

| Export target | ₹1,00,000 crore |

| Employment target | 55 lakh opportunities |

PM-MKSSY Under PMMSY

On 8 February 2024, the Cabinet approved PM-MKSSY as a sub-scheme under PMMSY:

- Outlay: ₹6,000 crore

- Duration: FY 2023-24 to 2026-27

- Focus: formalization and digital identity through the National Fisheries Digital Platform (NFDP)

Subsidy Pattern

| Category | Support |

|---|---|

| General category | 40% subsidy |

| SC/ST/Women | 60% subsidy |

| NE/Himalayan States under CSS | 90:10 Centre:State |

| Other States under CSS | 60:40 Centre:State |

Agricultural example: An inland fish farmer in West Bengal upgrades pond aeration and seed stocking under PMMSY, improving fish survival and increasing annual yield per hectare.

PMFME (Pradhan Mantri Formalization of Micro Food Processing Enterprises)

PMFME matters because farm income rises when produce is processed, branded, and sold with value addition, not just marketed raw.

NOTE

PMFME was launched on 29 June 2020 by the Ministry of Food Processing Industries with a total outlay of ₹10,000 crore over 5 years.

| Feature | Detail |

|---|---|

| Launch date | 29 June 2020 |

| Ministry | MoFPI |

| Outlay | ₹10,000 crore |

| Duration | 2020-21 to 2024-25 |

| Strategic approach | ODOP (One District One Product) |

| Capital subsidy | 35% of eligible project cost |

| Subsidy ceiling | Up to ₹10 lakh per unit |

| Borrower contribution | Minimum 10% |

| Credit guarantee | NCGTC |

Support Components

- Individual micro-enterprise upgradation

- SHG seed capital of ₹40,000 per member

- Common branding and marketing support

- Common infrastructure support at SHG federation or group level

Agricultural example: A tomato grower group in Kolar develops a small ketchup and puree unit under PMFME. Instead of dumping surplus tomato during a glut, they convert it into branded processed products.

Major NABARD Schemes

NABARD schemes are important because many agriculture finance questions ask not only about farmer-level schemes, but also about the institutional funds through which rural infrastructure, irrigation, warehousing, fisheries, and tribal livelihoods are supported.

| Scheme | Key Fact |

|---|---|

| RIDF | Rural Infrastructure Development Fund, launched 1995-96, funded from banks' PSL shortfalls |

| LTIF | Long Term Irrigation Fund, launched in Budget 2016-17 for stalled irrigation projects |

| RHF | Rural Housing Fund, launched 2008-09 for rural housing credit support |

| FIDF | Fisheries and Aquaculture Infrastructure Development Fund, corpus ₹7,522.48 crore, effective rate around 5% due to 3% subvention |

| AIF | Agriculture Infrastructure Fund; NABARD acts as a refinance support institution |

| SHG-BLP | Self Help Group-Bank Linkage Programme, pilot launched in 1992-93; world's largest microfinance linkage program |

| TDF | Tribal Development Fund, supports tribal livelihood through the Wadi model |

| WIF | Warehouse Infrastructure Fund, corpus ₹10,000 crore |

| MIF | Micro Irrigation Fund, corpus ₹10,000 crore |

High-Yield Exam Points

- RIDF = created out of PSL shortfall deposits

- FIDF = fisheries infra fund, not the same as PMMSY

- SHG-BLP = NABARD's major financial inclusion contribution

- TDF/Wadi = tribal orchard-based livelihood model

- MIF = drip and sprinkler expansion support for states

Agricultural example: A state government uses RIDF support to build rural roads and minor irrigation infrastructure; farmers benefit through lower transport costs and better water access even though the loan is not given directly to individual cultivators.

Kisan Vikas Patra (KVP)

A savings instrument (not a credit or subsidy scheme) that encourages long-term saving among rural populations through a simple, guaranteed-return investment available at post offices.

TIP

KVP Key Facts: Amount doubles in 124 months (10 years 4 months). Interest rate: 6.9%. Lock-in period: 30 months. First launched: 1988 by India Post. Re-launched: 2014. No Section 80C tax benefit.

| Feature | Detail |

|---|---|

| First launched | 1988 by India Post |

| Discontinued | 2011 (Shyamala Gopinath Committee flagged money laundering risk) |

| Re-launched | 2014 |

| Denominations | Rs 1,000, Rs 5,000, Rs 10,000, Rs 50,000 |

| Minimum investment | Rs 1,000 |

| Maximum investment | No upper limit |

| Interest rate | 6.9% (as of April 2020 - March 2021) |

| Doubling period | 124 months (10 years 4 months) |

| Lock-in (maturity) period | 30 months (2 years 6 months) |

| Tax benefit under Sec 80C | No |

| TDS on maturity | Exempt |

| Premature encashment | Not permitted (only on death, forfeiture by pledge, or court order) |

Who can purchase:

- An adult (in own name or on behalf of a minor)

- A Trust

- Two adults jointly

Important distinction: The lock-in period (30 months) is when premature withdrawal is first allowed, while the doubling period (124 months) is when the investment doubles in value. These are different concepts often confused in exams.

Agricultural example: A dairy farmer in Gujarat invests Rs 50,000 from the sale of her buffaloes in KVP. After 10 years and 4 months, she receives Rs 1,00,000 -- a reliable nest egg for retirement, requiring no financial expertise.

TIP

Exam mnemonic -- KVP "1-30-124": Min Rs 1,000; lock-in 30 months; doubles in 124 months.

SMAM (Sub-Mission on Agricultural Mechanization)

Addresses one of the biggest constraints on Indian productivity: low farm mechanization. While developed countries have 4-6 kW/ha of farm power, India's average is much lower.

| Feature | Detail |

|---|---|

| Launched | 2014 (revised 2016-17) |

| Plan period | 12th Five-Year Plan |

| Target farm power | 2 kW/ha (minimum threshold for efficient mechanized farming) |

| Implemented in | All states |

Fund Sharing Pattern

| Category | Centre : State |

|---|---|

| General states | 60 : 40 |

| North-Eastern & Himalayan states | 90 : 10 |

Agricultural example: A small farmer in Telangana wants a power tiller costing Rs 1,50,000. Under SMAM, she receives a subsidy covering a significant portion of the cost. The power tiller helps her prepare 5 hectares in 3 days instead of 15 days with bullocks -- enabling timely sowing and better yields.

Why 2 kW/ha matters: Higher mechanization leads to:

- Timely sowing and harvesting (critical for yield)

- Reduced drudgery (especially for women farmers)

- Lower crop losses during harvesting

- Improved overall productivity

Major Scheme Launch Dates

| Scheme | Launch/Announcement Date |

|---|---|

| NFSM (National Food Security Mission) | October 2007 |

| MIDH (Mission for Integrated Development of Horticulture) | 1 April 2014 |

| NLM (National Livestock Mission) | 2014-15 |

| NMSA (National Mission for Sustainable Agriculture) | 2014-15 |

| SHC (Soil Health Card) | 19 February 2015 |

| E-NAM (National Agriculture Market) | 14 April 2016 |

| PMFBY (Pradhan Mantri Fasal Bima Yojana) | Kharif 2016 |

| Operation Greens | Budget 2018-19 |

| PM-KISAN | 24 February 2019 |

| PM KUSUM | 8 March 2019 |

| PM-KMY | 9 August 2019 |

| AHIDF | 14 July 2020 |

| PMFME | 29 June 2020 |

| FPO Scheme (10,000 FPOs) | 29 February 2020 |

| AIF (Agriculture Infrastructure Fund) | 15 May 2020 |

| PMMSY (PM Matsya Sampada Yojana) | 10 September 2020 |

| ONOF (One Nation One Fertilizer) | August 2022 |

| PM Dhan-Dhaanya Krishi Yojana | Budget 2025-26 |

TIP

Exam Tip: Group by year: 2014-15 cluster (MIDH, NLM, NMSA, SHC) and 2018-19 cluster (Operation Greens, PM-KISAN, PM KUSUM) are frequently tested.

Budget Outlay: Key Agriculture Schemes (2024-25 vs 2025-26)

| Scheme / Head | Budget 2024-25 (Rs Crore) | Budget 2025-26 (Rs Crore) |

|---|---|---|

| Urea Subsidy | 1,09,300 | 1,18,900 |

| MGNREGS | 86,000 | 86,000 |

| PM-KISAN | 60,000 | 63,500 |

| MISS (Modified Interest Subvention) | 23,000 | 24,000 |

| NBS (Nutrient Based Subsidy) | 16,000 | 17,500 |

| PMFBY | 14,600 | 15,000 |

| PM KUSUM | 1,996 | 2,500 |

| NFSM | 2,200 | 2,500 |

| MIDH | 2,200 | 2,500 |

| PMMSY | 2,025 | 2,500 |

| RKVY | 1,200 | 1,500 |

| AIF | 750 | 1,300 |

| PM Dhan-Dhaanya Krishi Yojana | -- | 1,250 |

| NLM | 800 | 1,000 |

| NMEO (Edible Oils) | 600 | 900 |

| Digital Agriculture Mission | 450 | 800 |

| SMAM | 600 | 750 |

| Total Agriculture Ministry Budget | ~1,22,000 | ~1,36,000 |

TIP

Top 5 by allocation: Urea Subsidy > MGNREGS > PM-KISAN > MISS > NBS. These five cover over 80% of agriculture-related budget.

Summary Cheat Sheet

| Scheme | Key Fact | Exam Tag |

|---|---|---|

| PM-KISAN | Rs 6,000/year in 3 instalments of Rs 2,000; all farmers; Central Sector scheme | AFO 2021 |

| PM-KISAN effective from | 1 December 2018 | -- |

| PM-KISAN beneficiaries (target) | ~14.5 crore | -- |

| PM-KISAN installments released | 22 (as of Mar 2026) | -- |

| PM-KISAN eKYC | AADHAAR mandatory since 2023 | -- |

| PM-KISAN budget 2025-26 | Rs 63,500 crore | -- |

| PM-KISAN cumulative transfers by Nov 2025 | ₹3.70 lakh crore+ to 11 crore+ farmer families | -- |

| PM-KISAN 22nd instalment | ₹18,640 crore to 9.32 crore farmers | -- |

| PM-KISAN cumulative transfers by 24 Mar 2026 | ₹4.27 lakh crore+ through 22 instalments | -- |

| PM-KISAN latest digital layer | Farmer Registry + mobile app + Kisan-eMitra + Aadhaar eKYC | -- |

| KCC issuance for PM-KISAN | Within 14 days; all charges waived up to Rs 3 lakh | -- |

| PMFBY | Crop insurance scheme launched in Kharif 2016 | -- |

| PMFBY reform date | 18 Nov 2025 | -- |

| PMFBY new localised-risk cover | Wild animal attack | -- |

| PMFBY reintroduced localised calamity | Paddy inundation | -- |

| PMFBY reform rollout | Kharif 2026 | -- |

| PMFBY reporting rule | 72 hours via app with geotagged photos | -- |

| PMFBY budget 2025-26 | Rs 15,000 crore | -- |

| PM-KMY | ₹3,000/month pension at age 60; contribution ₹55-200/month | -- |

| PM-KMY effective from | 9 August 2019 | -- |

| PM-KMY fund manager | LIC | -- |

| PM-KMY spouse pension | Separate ₹3,000/month if spouse enrolls separately | -- |

| PM-KMY family pension | 50% = ₹1,500/month for surviving spouse | -- |

| PM-KMY enrolled | 24.95 lakh farmers as of 2 Feb 2026 | -- |

| PM-AASHA approved | September 2018; Budget 2026-27: Rs 7,200 crore | -- |

| PM-AASHA sub-schemes | PSS, PDPS, PPPS | -- |

| PDPS applicable to | Oilseeds only | -- |

| PSS implementing agency | NAFED | -- |

| MSP formula | 1.5 times Cost of Production (Swaminathan Commission) | -- |

| PM KUSUM target | 25,750 MW solar capacity | -- |

| PM KUSUM Component B | Solar pumps up to 7.5 HP; 60% subsidy (general), 80% (special states) | -- |

| AIF | ₹1 lakh crore corpus; 3% interest subvention up to ₹2 crore | -- |

| AIF progress by 26 Jan 2026 | ₹80,224.15 crore sanctioned; 1,50,431 projects; ₹1,27,508 crore mobilised investment | -- |

| AHIDF | ₹29,610.25 crore outlay; 3% interest subvention | -- |

| PMMSY | ₹20,050 crore outlay; fisheries Blue Revolution scheme | -- |

| PM-MKSSY | ₹6,000 crore sub-scheme under PMMSY | -- |

| PMFME | ₹10,000 crore; 35% capital subsidy up to ₹10 lakh | -- |

| RIDF | NABARD fund created from PSL shortfalls | -- |

| FIDF | ₹7,522.48 crore fisheries infrastructure fund | -- |

| SHG-BLP | Pilot launched in 1992-93 by NABARD | -- |

| KVP launched/re-launched | 1988 / 2014 | RRB-SO & AFO 2021 |

| KVP interest rate | 6.9% | RRB-SO & AFO 2021 |

| KVP doubling period | 124 months | -- |

| KVP lock-in | 30 months | -- |

| SMAM launched | 2014 | -- |

| SMAM target | 2 kW/ha farm power | -- |

| SMAM fund share | 60:40 (general); 90:10 (NE & Himalayan) | -- |