💳 Banking & Digital Payments

UPI, IMPS, RTGS, NEFT, AEPS, USSD, ISO 20022, EMV 3DS, credit cards, digital wallets for UPSSSC AGTA.

Digital Payment Systems — Overview

India has rapidly transformed into a digital payment economy. The government and RBI (Reserve Bank of India) have promoted cashless transactions through multiple systems managed primarily by NPCI (National Payments Corporation of India).

NPCI was founded in 2008 by RBI and IBA (Indian Banks' Association) to operate retail payment systems in India.

UPI — Unified Payments Interface

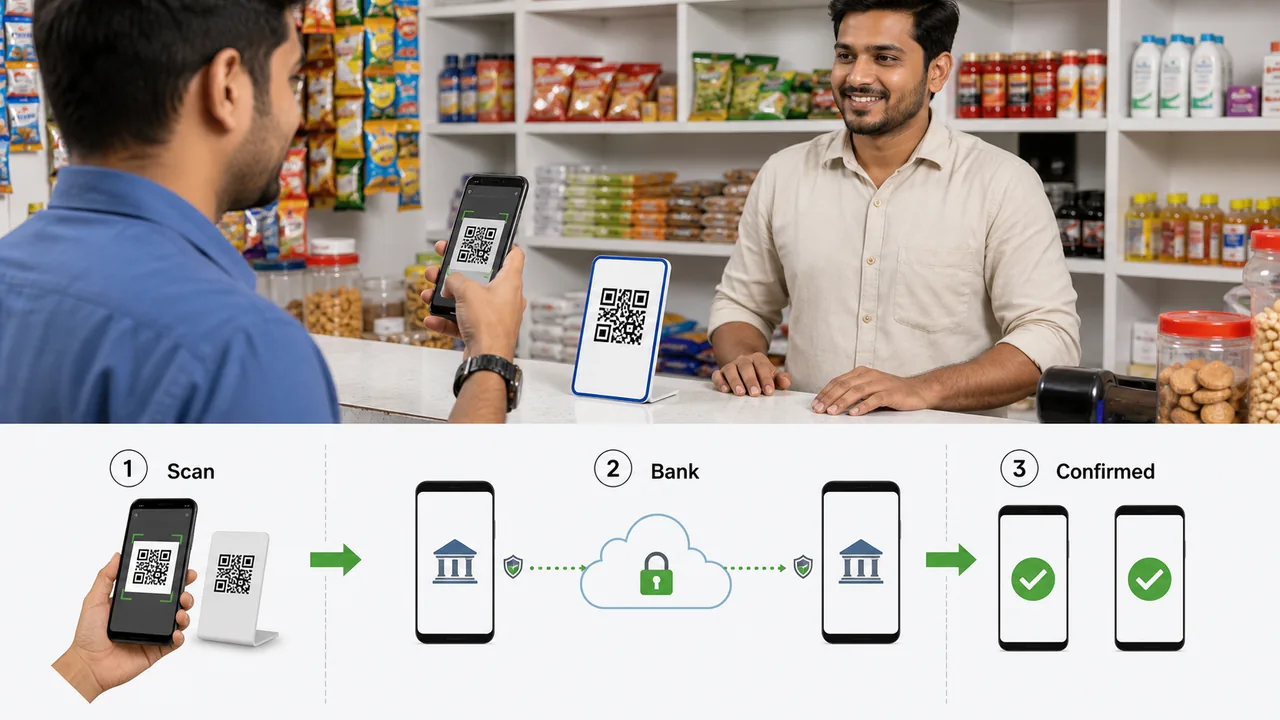

UPI is a real-time payment system that allows instant money transfer between bank accounts using a mobile phone.

| Feature | Details |

|---|---|

| Full Form | Unified Payments Interface |

| Launched | 2016 |

| Operated by | NPCI |

| How it works | Links bank account to a UPI ID (e.g., farmer@upi) |

| Transfer Limit | Up to ₹1 lakh per transaction (₹2 lakh for some banks) |

| Availability | 24×7×365 — including holidays |

| Cost | Free for users |

| Apps | BHIM, PhonePe, Google Pay, Paytm, Amazon Pay |

- BHIM (Bharat Interface for Money) — government's official UPI app

- UPI uses Virtual Payment Address (VPA) — no need to share bank details

- Supports: person-to-person, person-to-merchant, bill payments, QR code payments

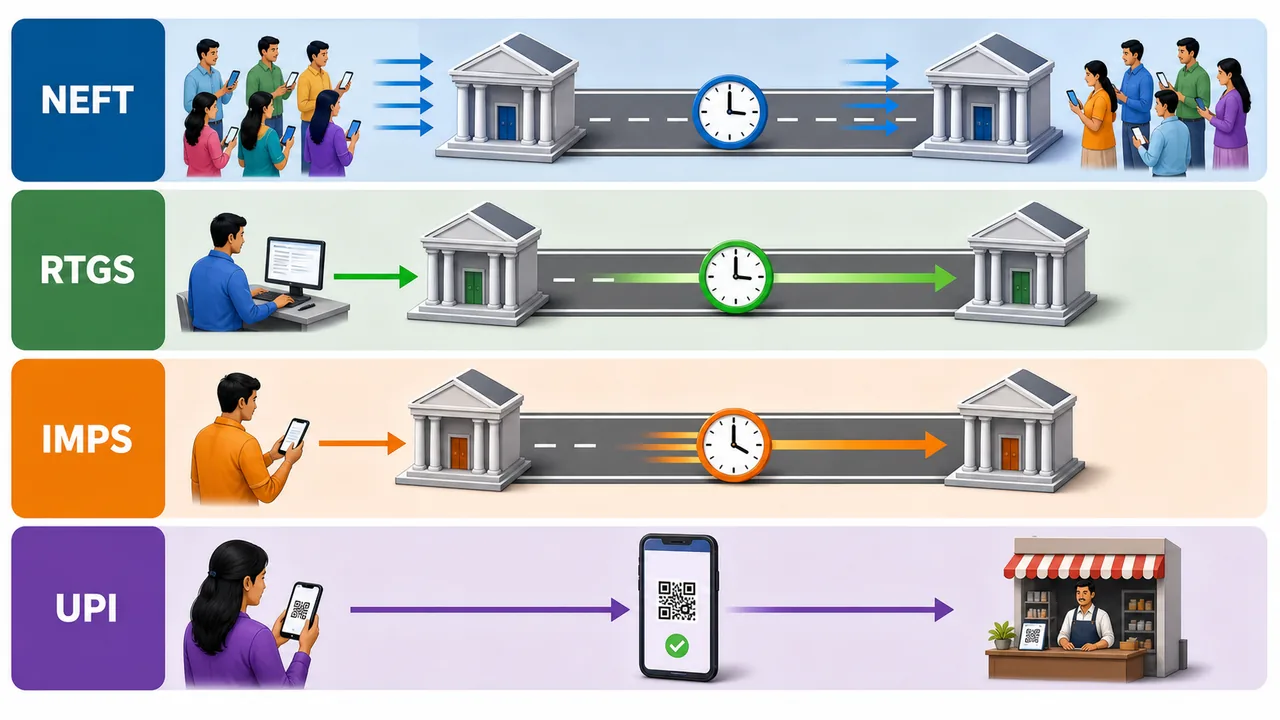

IMPS — Immediate Payment Service

IMPS provides instant, 24×7 interbank electronic fund transfer.

| Feature | Details |

|---|---|

| Full Form | Immediate Payment Service |

| Launched | 2010 |

| Operated by | NPCI |

| Speed | Instant (real-time) |

| Availability | 24×7×365 |

| Limit | Up to ₹5 lakh |

| Requires | MMID (Mobile Money Identifier) + mobile number |

| Channel | Mobile, internet banking, ATM |

MMID = 7-digit number issued by the bank, linked to your mobile number and account.

NEFT — National Electronic Funds Transfer

NEFT is an electronic fund transfer system for transferring money between bank accounts across India.

| Feature | Details |

|---|---|

| Full Form | National Electronic Funds Transfer |

| Launched | 2005 |

| Operated by | RBI |

| Processing | Originally batch processing (every 30 min); now 24×7 since December 2019 |

| Minimum | No minimum amount |

| Maximum | No upper limit |

| Speed | Near real-time (within minutes now) |

| Settlement | Deferred Net Settlement (DNS) |

RTGS — Real Time Gross Settlement

RTGS is for high-value, real-time fund transfers.

| Feature | Details |

|---|---|

| Full Form | Real Time Gross Settlement |

| Operated by | RBI |

| Minimum | ₹2 lakh |

| Maximum | No upper limit |

| Speed | Instant (real-time) |

| Availability | 24×7 since December 2020 |

| Settlement | Gross settlement — each transaction settled individually |

| Use | Large business transactions, property deals |

Key Difference: NEFT = Net Settlement (batches); RTGS = Gross Settlement (individual, real-time)

NEFT vs RTGS vs IMPS vs UPI — Comparison Table

| Feature | NEFT | RTGS | IMPS | UPI |

|---|---|---|---|---|

| Speed | Near real-time | Real-time | Instant | Instant |

| Min Amount | ₹1 | ₹2 lakh | ₹1 | ₹1 |

| Max Amount | No limit | No limit | ₹5 lakh | ₹1 lakh |

| Availability | 24×7 | 24×7 | 24×7 | 24×7 |

| Operated by | RBI | RBI | NPCI | NPCI |

| Settlement | Net (DNS) | Gross | Instant | Instant |

| Channel | Net banking | Net banking | Mobile/Net banking | Mobile app |

| Launched | 2005 | 2004 | 2010 | 2016 |

In practice, RTGS is used for high-value real-time transfers with a minimum amount of ₹2 lakh, while UPI is designed for fast everyday digital payments.

AEPS — Aadhaar Enabled Payment System

AEPS allows bank transactions using Aadhaar number + biometric authentication (fingerprint/iris).

- No debit card, internet, or smartphone needed

- Transactions through a Business Correspondent (BC) with a micro-ATM device

- Services: cash withdrawal, cash deposit, balance inquiry, fund transfer

- Targeted at rural and unbanked population

- Operated by NPCI

USSD — *99# Service

USSD (Unstructured Supplementary Service Data) enables mobile banking on basic feature phones without internet.

| Feature | Details |

|---|---|

| Access | Dial *99# from any phone |

| Internet | Not required |

| Smartphone | Not required — works on basic phones |

| Services | Balance inquiry, fund transfer, mini statement |

| Limit | ₹5,000 per transaction |

| Operated by | NPCI |

USSD-based banking through *99# is important because it works even without internet access and supports digital payments on basic phones.

Credit Card vs Debit Card

| Feature | Credit Card | Debit Card |

|---|---|---|

| Source of Money | Bank's money (loan/credit) | Your own money (bank balance) |

| Spending Limit | Pre-approved credit limit | Limited to account balance |

| Interest | Charged if not paid by due date | No interest (your money) |

| Bill | Monthly credit card bill | Instant deduction from account |

| Overspending | Possible (up to credit limit) | Cannot exceed balance |

| Rewards | Cashback, reward points, miles | Limited rewards |

| EMI | Available | Not available |

| Example | HDFC Regalia, SBI Card | SBI ATM card, RuPay card |

EMV Chip & 3D Secure

EMV Chip

EMV stands for Europay, Mastercard, Visa — the global standard for chip-based payment cards.

- Chip cards are more secure than magnetic stripe cards

- Chip generates a unique code for each transaction — cannot be cloned

- RBI has mandated EMV chip cards in India

EMV 3D Secure (3DS)

3D Secure is an additional authentication layer for online card payments.

- Adds OTP verification during online transactions

- Reduces fraud in Card Not Present (CNP) transactions

- "3D" = 3 domains: Acquirer, Issuer, Interoperability domain

- Branded as: Visa Secure, Mastercard Identity Check, RuPay Secure

ISO 20022

ISO 20022 is a global messaging standard for financial transactions.

| Feature | Details |

|---|---|

| What | Universal financial messaging standard |

| Purpose | Standardize payment messages worldwide |

| Replaces | Older formats like SWIFT MT messages |

| Benefits | Richer data, structured format, better compliance |

| Adopted by | RBI (for RTGS/NEFT), SWIFT, central banks globally |

- Supports richer, more structured data in payment messages

- Enables better fraud detection and compliance

- India's RTGS and NEFT have migrated to ISO 20022

Digital Wallets & Prepaid Instruments

A digital wallet stores money electronically for making payments without using a physical card or bank account directly.

| Wallet | Type | Provider |

|---|---|---|

| Paytm Wallet | Semi-closed | One97 Communications |

| Amazon Pay | Semi-closed | Amazon |

| Mobikwik | Semi-closed | Mobikwik |

Types of Prepaid Payment Instruments (PPI):

| Type | Feature |

|---|---|

| Open | Issued by banks, used for purchases + cash withdrawal |

| Semi-closed | Cannot withdraw cash; used for purchases at merchants |

| Closed | Issued by entity for its own platform only (e.g., Ola Money for rides) |

RBI regulates all prepaid instruments. KYC is mandatory for wallets above ₹10,000.

NPCI Products

NPCI operates all major retail payment systems in India:

| Product | Purpose |

|---|---|

| UPI | Instant mobile payments |

| IMPS | Instant interbank transfer |

| RuPay | India's own card payment network |

| NACH | National Automated Clearing House — bulk debits/credits (EMI, salary) |

| BBPS | Bharat Bill Payment System — utility bill payments |

| NETC | National Electronic Toll Collection — FASTag |

| AePS | Aadhaar-based payments |

| *99# | USSD-based banking |

RuPay Card

RuPay is India's own card payment network, launched by NPCI in 2012.

- Alternative to Visa and Mastercard

- Lower processing fees — promotes financial inclusion

- Linked to Jan Dhan Yojana accounts

- Accepted at all ATMs and POS terminals in India

- International variant: RuPay International (accepted in Singapore, Bhutan, UAE, etc.)

Other Digital Banking Services

| Service | Description |

|---|---|

| Mobile Banking | Banking through bank's app (SBI YONO, iMobile) |

| Net Banking / Internet Banking | Banking through bank's website via browser |

| SWIFT | Society for Worldwide Interbank Financial Telecommunication — international transfers |

| NACH | Automated bulk transactions (salary credits, loan EMIs, SIP) |

| BBPS | Centralized bill payment system (electricity, water, gas, DTH) |

FASTag

FASTag is an electronic toll collection system using RFID (Radio Frequency Identification) technology.

| Feature | Details |

|---|---|

| Technology | RFID-based |

| System | NETC (National Electronic Toll Collection) |

| Operated by | NPCI |

| Mandate | Mandatory for all 4-wheelers on NH since February 2021 |

| How | Prepaid tag on windshield; toll deducted automatically |

| Validity | 5 years |

QR Code Payments

QR Code (Quick Response Code) is a 2D barcode scanned by smartphones to initiate payments.

- Static QR — fixed amount or merchant ID (printed at shops)

- Dynamic QR — generated per transaction with specific amount

- Bharat QR — interoperable QR by NPCI (works with RuPay, Visa, Mastercard)

- UPI QR codes — scan and pay via any UPI app

RBI Guidelines on Digital Payments

- Two-factor authentication (2FA) mandatory for online card transactions

- Tokenization of cards — actual card number replaced with token for security

- Recurring payments need additional authentication for first transaction

- Digital payment complaints: RBI Ombudsman Scheme

- Zero liability for unauthorized electronic transactions if reported within 3 days

UPI — Latest Statistics & Updates

| Metric | Value (June 2025) |

|---|---|

| Transactions | 18.39 billion |

| Value | ₹24.03 lakh crore |

| Daily Average | ~61 crore transactions per day |

UPI 2.0 Features

| Feature | Description |

|---|---|

| Overdraft Account Linking | Link overdraft (OD) accounts to UPI — not just savings/current |

| Invoice in QR | Merchant can embed invoice details inside QR code |

| Signed Intent | Digitally signed payment requests — prevents tampering |

| One-time Mandate | Pre-authorize a future payment (e.g., IPO application) |

UPI Lite

UPI Lite enables small-value offline transactions without entering UPI PIN.

- Transaction limit: Up to ₹500 per transaction

- Wallet limit: ₹2,000 at any time

- Works even when bank server is down — uses on-device wallet

- Reduces load on banking infrastructure

e-RUPI

e-RUPI is a purpose-specific digital payment voucher — a prepaid, cashless, contactless instrument.

| Feature | Details |

|---|---|

| Launched | August 2021 |

| How | Delivered as QR code or SMS to beneficiary's phone |

| Key Feature | No bank account, smartphone, or internet needed by the beneficiary |

| Purpose | Government can issue vouchers for specific services (medicine, fertilizer, nutrition) |

| Developed by | NPCI in collaboration with DFS and NHA |

Exam tip: e-RUPI is NOT a cryptocurrency or digital currency — it is a purpose-specific voucher.

NACH & BBPS

NACH (National Automated Clearing House)

NACH is a centralized system for bulk and recurring payments.

| Feature | Details |

|---|---|

| Operated by | NPCI |

| Use Cases | EMI payments, insurance premiums, SIP, salary credits, dividend payments |

| Types | NACH Debit (auto-deduction from customer) and NACH Credit (bulk credit to many accounts) |

BBPS (Bharat Bill Payment System)

BBPS is a unified platform for all recurring bill payments across India.

| Feature | Details |

|---|---|

| Operated by | NPCI (through NBBL — NPCI Bharat BillPay Ltd.) |

| Bills Covered | Electricity, water, gas, DTH, telecom, insurance, municipal tax, education fees |

| Access | Through any bank app, BHIM, or authorized agent |

| Key Feature | Interoperable — pay any biller through any BBPS-enabled channel |

NPCI International — UPI Goes Global

NPCI International Payments Limited (NIPL) promotes UPI and RuPay adoption globally.

| Country | UPI Status |

|---|---|

| Singapore | UPI-PayNow linkage (live since February 2023) |

| UAE | UPI accepted at select merchants |

| Sri Lanka | UPI QR payments accepted |

| France | UPI accepted at Eiffel Tower and select locations |

| Mauritius | UPI-MauCAS linkage |

Jan Dhan Yojana — Financial Inclusion

Pradhan Mantri Jan Dhan Yojana (PMJDY) is the world's largest financial inclusion programme.

| Feature | Details |

|---|---|

| Launched | 28 August 2014 |

| Accounts Opened | 52+ crore (as of 2025) |

| Key Features | Zero-balance bank account, RuPay debit card, ₹2 lakh accident insurance, ₹30,000 life cover |

| Overdraft | Up to ₹10,000 for eligible accounts |

| Guinness Record | Most bank accounts opened in one week (1.8 crore) |

PMJDY is the J in the JAM Trinity (Jan Dhan + Aadhaar + Mobile).

RBI CBDC — Digital Rupee (e₹)

CBDC (Central Bank Digital Currency) is the digital form of India's fiat currency, issued by RBI.

| Feature | Details |

|---|---|

| Name | Digital Rupee (e₹) |

| Pilot Launch | December 2022 |

| Types | e₹-W (Wholesale) — for interbank settlement; e₹-R (Retail) — for general public |

| Technology | Blockchain-based distributed ledger |

| Difference from UPI | CBDC is actual digital currency (like holding digital cash); UPI is a payment system that moves bank money |

Exam tip: CBDC is government-backed and regulated; Cryptocurrency (Bitcoin) is decentralized and NOT backed by any government.

ISO 20022 Migration

ISO 20022 is being adopted globally by SWIFT for cross-border payments.

| Feature | Details |

|---|---|

| What | New global messaging standard for financial transactions |

| Why | Provides richer data format — more fields for compliance, remittance info, beneficiary details |

| India Status | RBI has already migrated RTGS and NEFT to ISO 20022 |

| SWIFT Deadline | Full migration by November 2025 |

Summary Points

| Concept | Key Details |

|---|---|

| UPI | Instant mobile payment, NPCI, 2016, VPA-based |

| IMPS | Instant 24×7, NPCI, ₹5 lakh limit, needs MMID |

| NEFT | Net settlement, RBI, no limit, 24×7 since 2019 |

| RTGS | Gross settlement, RBI, min ₹2 lakh, real-time |

| AEPS | Aadhaar + fingerprint, no internet needed |

| *USSD (99#) | Works on basic phones without internet |

| NPCI | Operates UPI, IMPS, RuPay, NACH, BBPS, FASTag |

| RuPay | India's card network, NPCI, 2012, Jan Dhan linked |

| Credit Card | Bank's money, interest if unpaid |

| Debit Card | Your money, instant deduction |

| EMV | Chip-based cards, anti-cloning |

| 3D Secure | OTP for online card payments |

| ISO 20022 | Global financial messaging standard |

| FASTag | RFID toll collection, NETC, mandatory since 2021 |

| BHIM | Government's official UPI app |

| Digital Wallet | Electronic money storage (Paytm, Amazon Pay) |

| SWIFT | International interbank messaging |

| Bharat QR | Interoperable QR code by NPCI |

| QR Code | Quick Response Code — 2D barcode for payments |

| UPI (June 2025) | 18.39 billion transactions, ₹24.03 lakh crore |

| UPI 2.0 | Overdraft linking, Invoice in QR, Signed Intent |

| UPI Lite | ≤₹500 no PIN, offline, on-device wallet |

| e-RUPI | Purpose-specific voucher (Aug 2021), no bank account needed |

| NACH | Bulk recurring — EMI, salary, SIP, dividends |

| BBPS | Unified bill payments — electricity, water, gas, DTH |

| NPCI International | UPI in Singapore, UAE, France, Sri Lanka, Mauritius |

| Jan Dhan | 52+ crore accounts, zero-balance, RuPay card, ₹2L insurance |

| CBDC e₹ | Digital Rupee by RBI (Dec 2022) |

| e₹-W | Wholesale CBDC — interbank settlement |

| e₹-R | Retail CBDC — general public |

| ISO 20022 | Global messaging standard, richer data, RTGS/NEFT migrated |

Lesson Doubts

Ask questions, get expert answers