💳 Agricultural Credit - Types, Classification & Principles of Farm Finance

Understand agricultural credit from basics to advanced - types of loans, 3Rs and 5Cs of credit, 7 principles of farm finance, security types, and repayment capacity with agricultural examples

Why Does a Farmer Need Credit?

Imagine a wheat farmer in Punjab preparing for the Rabi season. He needs money for seeds, fertilizers, diesel for irrigation, and labor wages. His previous crop income was spent on family expenses and repaying old debts. Without credit, he cannot even begin sowing. This is the reality of millions of Indian farmers -- agricultural credit is the lifeline that keeps farming alive.

What is Credit?

- The word "Credit" comes from the Latin word "Credo" meaning "I believe". The entire credit system rests on mutual trust between lender and borrower.

- Definition: Credit is a certain amount of money provided for a specific purpose, on agreed conditions, with interest, to be repaid within a defined period.

NOTE

Remember for exams: Credit = "Credo" = "I believe" (Latin origin).

- According to Professor Galbraith, credit is the:

"Temporary transfer of asset from one who has to other who has not."

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Why Does a Farmer Need Credit?

Imagine a wheat farmer in Punjab preparing for the Rabi season. He needs money for seeds, fertilizers, diesel for irrigation, and labor wages. His previous crop income was spent on family expenses and repaying old debts. Without credit, he cannot even begin sowing. This is the reality of millions of Indian farmers -- agricultural credit is the lifeline that keeps farming alive.

What is Credit?

- The word "Credit" comes from the Latin word "Credo" meaning "I believe". The entire credit system rests on mutual trust between lender and borrower.

- Definition: Credit is a certain amount of money provided for a specific purpose, on agreed conditions, with interest, to be repaid within a defined period.

NOTE

Remember for exams: Credit = "Credo" = "I believe" (Latin origin).

- According to Professor Galbraith, credit is the:

"Temporary transfer of asset from one who has to other who has not."

This highlights the redistributive nature of credit -- moving resources from surplus holders to those who need them for productive purposes.

Credit Needs of Indian Farmers

Indian farmers need credit for four main reasons, arranged from immediate to long-term needs:

| Need | Type | Example |

|---|---|---|

| Buying inputs | Recurring/seasonal | Seeds, fertilizers, pesticides, feed for cattle |

| Family survival | Consumption | Food and expenses during crop failure years |

| Hiring resources | Operational | Irrigation equipment, labor, machinery rental |

| Capital investment | Long-term | Buying land, tractors, making permanent improvements |

TIP

Mnemonic -- "ISHC": Inputs, Survival, Hiring, Capital -- the four credit needs of a farmer.

Why is Agricultural Credit Important?

Before institutional credit, farmers depended on private moneylenders who charged exorbitant interest rates, trapping families in generational debt. Today, a multi-agency approach (cooperatives, commercial banks, RRBs) provides cheaper, timely, and adequate credit.

Role of Credit in Indian Agriculture

- Acts as a bridge between agricultural potential and actual achievement

- Plays a catalytic role -- purchased inputs like HYV seeds + fertilizers = higher productivity

- Enables adoption of modern technology that farmers otherwise cannot afford

- Drives capital formation -- farm assets and infrastructure raise income and living standards

- Reduces regional economic imbalances by channeling credit to underdeveloped areas

- Creates forward linkages (processing, marketing) and backward linkages (demand for seeds, fertilizers, machinery)

- Builds supporting infrastructure -- irrigation, storage, market connectivity

- Funds large-scale public investments -- major irrigation projects, rural electrification, fertilizer plants

Classification of Agricultural Credit

Agricultural credit can be classified in eight different ways. Let us study each systematically.

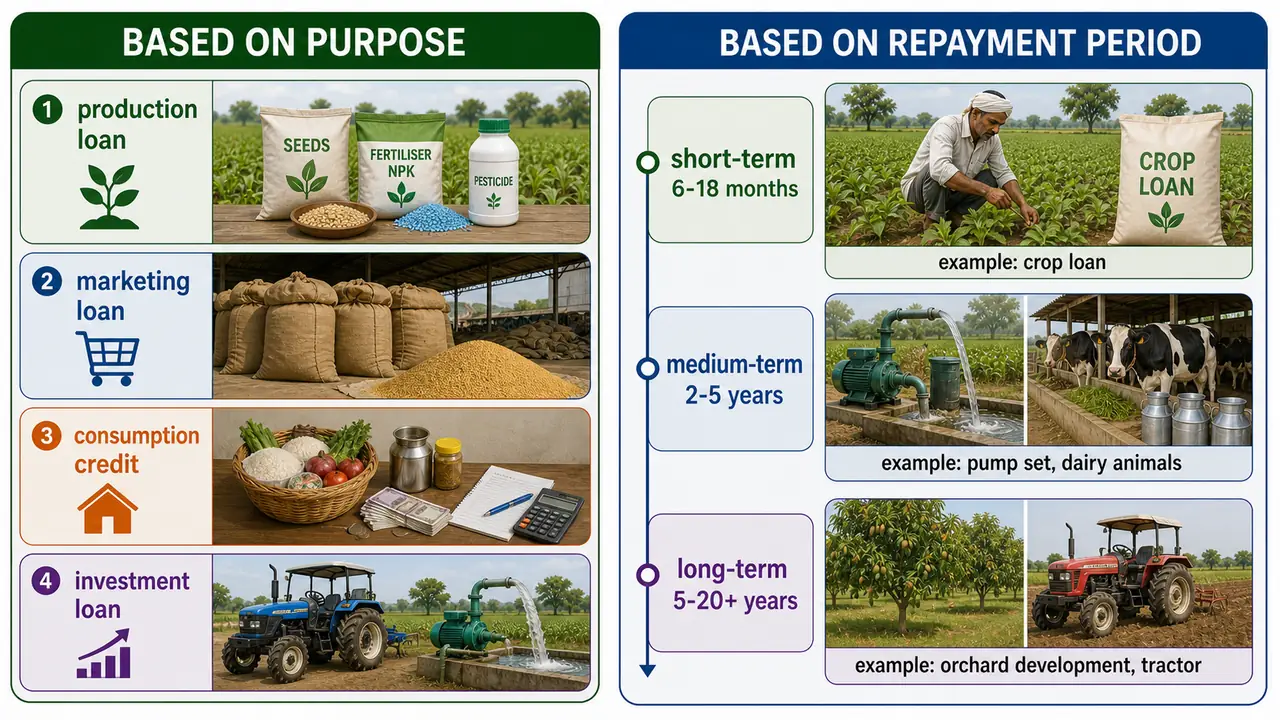

1. Based on Purpose

| Type | Purpose | Example |

|---|---|---|

| Production loans | Finance crop cultivation (also called SAO/crop loans) | A rice farmer buying seeds and fertilizers for kharif season |

| Marketing loans | Prevent distress sales, hold produce for better prices | A soybean farmer storing produce in warehouse after harvest |

| Consumption credit | Meet family living expenses | A marginal farmer feeding his family during drought |

| Investment loans | Buy durable assets with multi-year productivity | A farmer purchasing a tractor or installing a tube well |

TIP

Exam Tip: Production loans = SAO loans = Short-term loans = Crop loans. All are the same thing.

2. Based on Repayment Period

| Type | Duration | Purpose | Repayment | Example |

|---|---|---|---|---|

| Short-term | 6-18 months | Working capital for cultivation | Lumpsum after harvest | Crop loan for purchasing paddy seeds and urea |

| Medium-term | 2-5 years | Purchase of implements and animals | Half-yearly/annual installments | Buying a pump-set or dairy animals |

| Long-term | 5-20+ years | Permanent improvements and major assets | Annual installments over many years | Land reclamation, tractor purchase, orchard establishment |

IMPORTANT

Medium-term + Long-term loans combined are called term loans or investment loans.

3. Based on Security

Secured Loans

Loans given against some form of security. The main types are:

| Security Type | What is Pledged | Example |

|---|---|---|

| Personal security | Borrower's own guarantee (promissory note) | Small crop loan based on farmer's reputation |

| Collateral security | Movable properties (LIC bonds, FD receipts, warehouse receipts) | Farmer pledging warehouse receipt of stored wheat |

| Chattel loans | Movable valuables pledged to pawn-brokers | Farmer pawning gold jewellery for emergency cash |

| Mortgage | Immovable property (land, buildings) | Farmer mortgaging agricultural land for long-term loan |

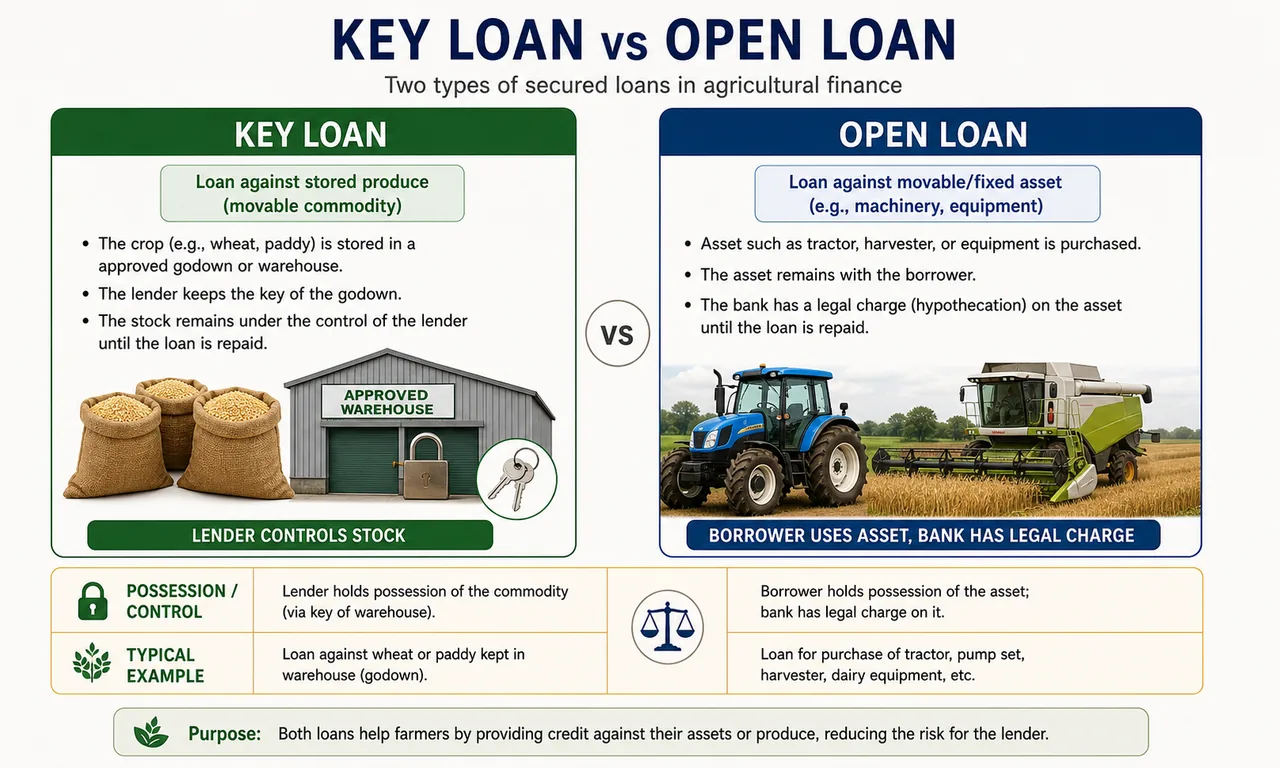

| Hypothecation | Movable assets (borrower keeps possession, bank has legal right) | Tractor loan -- farmer uses tractor but cannot sell it until loan is repaid |

Types of Mortgage:

| Type | Property | Registration | Cost |

|---|---|---|---|

| Simple mortgage | Ancestrally inherited | Must register property in bank's name | Higher (registration charges on borrower) |

| Equitable mortgage | Self-acquired | No registration needed (title deeds suffice) | Lower and simpler |

- The person creating the mortgage = Mortgagor (borrower)

- The person in whose favour it is created = Mortgagee (banker)

Types of Hypothecated Loans:

| Type | What is Held | Control | Example |

|---|---|---|---|

| Key loans | Agricultural produce | Kept under lender's control (locked storage) | Farmer's rice stored in bank-controlled godown; released when prices rise |

| Open loans | Machinery/equipment | Physical possession with borrower; legal ownership with bank | Farmer uses purchased harvester but cannot sell it |

- The person creating the charge = Hypothecator (borrower)

- The person in whose favour it is created = Hypothecatee (bank)

Unsecured Loans

Loans given purely on trust without any security. Usually for smaller amounts based on the borrower's creditworthiness and past repayment record.

4. Based on Lender

| Type | Lender | Interest Rate | Example |

|---|---|---|---|

| Institutional credit | Cooperatives, commercial banks, RRBs | Regulated, lower (4-12% p.a.) | KCC loan from SBI |

| Non-institutional credit | Moneylenders, traders, commission agents, relatives | Unregulated, often exploitative (36-120% p.a.) | Loan from village moneylender |

5. Based on Borrower

- By activity: Crop farmers, dairy farmers, poultry farmers, fishermen, rural artisans -- each has different credit needs and risk profiles

- By farm size: Agricultural laborers, marginal farmers (<1 ha), small farmers (1-2 ha), medium farmers, large farmers

- By location: Hill farmers, tribal farmers -- face unique challenges like difficult terrain, remoteness, and limited infrastructure

6. Based on Liquidity

| Type | Income Generation | Repayment | Risk Level | Example |

|---|---|---|---|---|

| Self-liquidating loans | Immediate (within one season) | Lumpsum within 1 year | Low | Crop loan for wheat -- repaid after selling harvest |

| Partially-liquidating loans | Gradual (over multiple years) | Installments over 2-5+ years | Higher | Dairy loan -- cow gives milk income gradually over years |

7. Based on Approach

| Approach | Description | Example |

|---|---|---|

| Individual approach | Loan to individual based on personal profile | Farmer applying for KCC |

| Area-based approach | Loans for specific geographic areas | DPAP (Drought Prone Area Programme) loans |

| DRI approach | Loans to weaker sections at 4% per annum | Landless laborer getting concessional loan |

8. Based on Contact

| Type | Description | Example |

|---|---|---|

| Direct loans | Bank lends directly to the farmer | Crop loan disbursed to farmer's account |

| Indirect loans | Loans to agro-firms that indirectly benefit farmers | Loan to fertilizer company ensuring affordable inputs reach farms |

Economic Feasibility Tests of Credit (3Rs of Credit)

Before sanctioning a loan, the banker must answer three questions:

- Will the investment generate returns greater than costs?

- Will the returns create a surplus sufficient to repay the loan on time?

- Can the farmer withstand the risk and uncertainty inherent in farming?

These are the 3Rs of Credit:

| R | Meaning | What It Tests |

|---|---|---|

| Returns | Income from proposed investment | Will the borrowed money earn more than it costs? |

| Repayment Capacity | Ability to repay on time | After all expenses, is there enough surplus to repay? |

| Risk-Bearing Ability | Ability to absorb financial losses | Can the farmer survive if things go wrong? |

IMPORTANT

The 3Rs of credit are the most important indicators of a farmer's creditworthiness. Always evaluate all three before sanctioning any loan.

Returns from the Investment

The farmer must generate incremental returns that cover the additional costs of borrowed funds. Returns depend on five key farm management decisions:

- What to grow? (crop selection)

- How to grow? (technology choice)

- How much to grow? (scale of production)

- When to sell? (timing of marketing)

- Where to sell? (market selection)

Example: A farmer borrows Rs 50,000 for hybrid maize cultivation. If the hybrid yields Rs 1,20,000 vs Rs 80,000 from local variety, the incremental return of Rs 40,000 exceeds the loan cost, making credit worthwhile.

Repayment Capacity

Repayment capacity is the ability to repay the loan within the stipulated time. It depends on both quantitative and qualitative factors:

Y = f(X1, X2, X3, X4, X5, X6, X7...)

| Variable | Factor | Effect on Repayment |

|---|---|---|

| X1 (+) | Gross returns from the enterprise | Increases capacity |

| X2 (-) | Working expenses | Decreases capacity |

| X3 (-) | Family consumption expenditure | Decreases capacity |

| X4 (-) | Other loans due | Decreases capacity |

| X5 (+) | Literacy | Increases capacity |

| X6 (+) | Managerial skill | Increases capacity |

| X7 (+) | Moral character (honesty, integrity) | Increases capacity |

Repayment capacity formulas:

For crop loans (self-liquidating):

Gross Income - (Working expenses excluding proposed crop loan + Family living expenses + Other loans due + Miscellaneous expenditure)

For term loans (partially-liquidating):

Gross Income - (Working expenses + Family living expenses + Other loans due + Miscellaneous expenditure + Annual installment due for term loan)

Why Do Indian Farmers Have Poor Repayment Capacity?

| Cause | Explanation |

|---|---|

| Small farm holdings | Fragmentation reduces scale economies |

| Low productivity | Traditional methods yield less output |

| High family expenditure | Large families consume more |

| Price fluctuations | Volatile commodity prices reduce income |

| Loan diversion | Credit used for unproductive purposes |

| Low net worth | Limited owned assets as financial cushion |

| Poor technology adoption | Lack of access to improved inputs |

| Poor resource management | Inefficient use of available resources |

How to Strengthen Repayment Capacity

- Increase net income through better farm organization

- Adopt improved technology to raise production and cut costs

- Remove imbalances in resource availability

- Align loan repayment schedule with flow of income (repay after harvest)

- Improve net worth of farm households

- Diversify farm enterprises (crop + dairy + poultry = multiple income streams)

- Adopt risk management -- crop insurance, livestock insurance, price hedging

Risk-Bearing Ability

Risk-bearing ability is the farmer's capacity to withstand financial loss. It can be measured using statistical tools like coefficient of variation (CV) and standard deviation (SD).

| Type of Risk | Example |

|---|---|

| Production/physical risk | Crop failure from pest attack or disease |

| Technological risk | New HYV seed fails in local conditions |

| Personal risk | Farmer falls ill during harvest season |

| Institutional risk | Government changes MSP or subsidy policy |

| Weather uncertainty | Drought, flood, unseasonal hailstorm |

| Price risk | Tomato price crashes from Rs 40/kg to Rs 2/kg |

Repayment capacity under risk:

Deflated Gross Income - (Working expenses excluding proposed crop loan + Family living expenses + Other loans due + Miscellaneous expenditure)

The deflated gross income adjusts expected income downward to account for the probability of adverse events.

How to Strengthen Risk-Bearing Ability

- Increase owner's equity/net worth -- a larger cushion absorbs shocks

- Reduce farm and family expenditure

- Develop moral character (honesty, integrity, dependability) -- these together form the credit rating

- Undertake reliable and stable enterprises with steady income

- Build ability to borrow during both good and bad times

- Save a portion of farm earnings for future emergencies

- Take crop, livestock, and machinery insurance -- transfers risk to the insurer

5 Cs of Credit

The 5 Cs of Credit is a framework bankers use to evaluate a borrower's creditworthiness:

| C | Meaning | What the Banker Checks | Agricultural Example |

|---|---|---|---|

| Character | Moral and mental integrity | Honesty, past repayment history, commitment | Has the farmer repaid previous KCC loans on time? |

| Capacity | Ability to repay (C = f(Y), Y = income) | Income level, farm productivity | Does the farmer's 5-acre sugarcane farm generate enough income? |

| Capital | Net worth (assets minus liabilities) | Available money and assets | Does the farmer own land, livestock, equipment worth more than his debts? |

| Condition | Loan terms and external factors | Economic climate, market conditions, procedures | Is it a good year for cotton prices? Are markets accessible? |

| Commonsense | Mutual understanding between lender and borrower | Clear expectations about loan purpose and repayment | Does the farmer understand the repayment schedule? |

TIP

Mnemonic -- "3C + 2C": Character, Capacity, Capital (borrower traits) + Condition, Commonsense (transaction traits).

7 Ps of Farm Credit (Principles of Farm Finance)

These seven principles guide how agricultural credit should be designed, disbursed, and managed:

| Principle | Core Idea | Agricultural Example |

|---|---|---|

| Productive Purpose | Loan must generate additional income | Loan for dairy cow that gives milk income daily |

| Personality | Trustworthiness of borrower matters | Farmer with good repayment history gets easier access |

| Productivity | Credit should increase productivity of all factors | HYV seeds increase not just yield but also productivity of fertilizers and water used |

| Phased Disbursement | Loan released in stages to ensure proper use | Well-digging loan released: 50% at start, 50% after half completion |

| Proper Utilization | Funds used only for the stated purpose | Crop loan used for buying seeds, not for a family wedding |

| Payment | Repayment schedule aligned with income flow | Crop loan repaid 2-3 months after harvest (grace period for marketing) |

| Protection | Safety measures to protect lender and borrower | Crop insurance, warehouse receipt financing, DICGC guarantee |

TIP

Mnemonic -- "7 Ps": Productive Purpose, Personality, Productivity, Phased disbursement, Proper utilization, Payment, Protection.

Key Details of Each Principle

Productive Purpose: Small and marginal farmers need consumption credit alongside crop loans so they do not divert production loans for household expenses. Crop loans should be supported with income-generating assets (dairy, poultry, sheep) acquired through term loans.

Personality: A farmer who defaults due to crop failure from natural calamity is not a willful defaulter. A large farmer who earns profits but refuses to repay is a willful defaulter. The safety of the loan depends on the credit character of the borrower, not just the security offered.

Productivity: Credit should have a multiplier effect. Using HYV seeds not only increases crop yield but also makes fertilizers and irrigation water more productive.

Phased Disbursement: Loan for perennial crops (mango orchard) or investment activities (well construction) is released in phases. This prevents diversion but increases the cost of credit due to multiple disbursements.

Proper Utilization: Possible only when quality inputs (seeds, fertilizers) are available without adulteration and infrastructure (storage, transport, markets) exists.

Payment: For crop loans -- repaid in lumpsum after harvest with a 2-3 month grace period. For term loans -- repaid in annual installments based on incremental returns. If crops fail, repayment is extended and fresh loans are provided.

Protection: Safety measures include:

- Insurance coverage for crops, livestock, and machinery

- Linking credit with marketing -- sale proceeds used for repayment

- Warehouse receipt financing -- stored produce acts as security

- Sureties through hypothecation or mortgage

- DICGC (Deposit Insurance and Credit Guarantee Corporation) reimburses banks for unrecovered loans to weaker sections

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Credit origin | Latin "Credo" = "I believe"; system rests on mutual trust |

| Galbraith's definition | "Temporary transfer of asset from one who has to other who has not" |

| 4 Credit Needs | ISHC — Inputs, Survival, Hiring resources, Capital investment |

| Production loans | Also called SAO/crop loans; finance crop cultivation (short-term) |

| Marketing loans | Prevent distress sales; hold produce for better prices |

| Investment loans | Buy durable assets; also called term loans (medium + long-term) |

| Short-term credit | 6-18 months; working capital; repaid lumpsum after harvest |

| Medium-term credit | 2-5 years; implements and animals; half-yearly/annual installments |

| Long-term credit | 5-20+ years; permanent improvements; annual installments |

| Collateral security | Movable properties — LIC bonds, FD receipts, warehouse receipts |

| Mortgage | Immovable property (land); Simple (ancestral, registered) vs Equitable (self-acquired, no registration) |

| Hypothecation | Movable assets; borrower keeps possession; Key loans (lender control) vs Open loans (borrower possession) |

| Mortgagor / Mortgagee | Borrower / Banker |

| Institutional credit | Cooperatives, commercial banks, RRBs; regulated, lower interest (4-12% p.a.) |

| Non-institutional credit | Moneylenders, traders; unregulated, exploitative (36-120% p.a.) |

| Self-liquidating loans | Repaid within 1 season; low risk (e.g., crop loans) |

| Partially-liquidating | Repaid over 2-5+ years; gradual income (e.g., dairy loans) |

| DRI loans | To weaker sections at 4% per annum |

| 3Rs of Credit | Returns (income > costs?), Repayment Capacity (surplus to repay?), Risk-Bearing Ability (can absorb losses?) |

| Repayment formula (crop) | Gross Income − (Working expenses excl. proposed loan + Family + Other loans + Misc) |

| 5Cs of Credit | Character, Capacity, Capital, Condition, Commonsense |

| 7Ps of Farm Finance | Productive Purpose, Personality, Productivity, Phased disbursement, Proper utilization, Payment, Protection |

| Phased disbursement | Loan released in stages to prevent diversion (e.g., 50% at start, 50% after half completion) |

| Payment principle | Repayment schedule aligned with income flow — crop loans repaid 2-3 months after harvest |

| DICGC | Deposit Insurance and Credit Guarantee Corporation; reimburses banks for unrecovered loans to weaker sections |