💻 Digital Finance & P2P Lending

Overview of digital banking models, neo-banks, Open Credit Enablement Network (OCEN), and Peer to Peer (P2P) lending guidelines.

Digital Finance — P2P Lending via FinTech

What is Digital Lending?

In the conventional lending model, a borrower physically visits a bank branch, submits paper-based documentation (salary slips, property documents, identity proofs), and awaits a manual credit appraisal that could take days or weeks. The decision rests with a human officer who assesses risk using a narrow set of financial indicators.

Digital lending replaces this entire process with automated, technology-driven workflows. Every stage — from loan discovery to disbursal — is conducted remotely through mobile and web-based platforms. Creditworthiness is assessed within minutes using algorithmic models that analyse alternative data such as transaction history, device behaviour, and social patterns, removing the need for physical presence or paper documentation.

Key definitions:

- Digital Lending — A remote and automated lending process executed entirely through digital technologies, without requiring the borrower to visit a physical institution.

- Digital Lending Apps — Mobile and web-based platforms that connect borrowers with digital lenders and manage the loan lifecycle end-to-end.

- The RBI Working Group on Digital Lending identifies this transformation as the emergence of Bank 4.0 — an era in which FinTech capabilities are deeply integrated into traditional banking operations.

The FinTech Ecosystem — Technologies and Sectors

FinTech (Financial Technology) refers to the application of technology to deliver financial services more efficiently. It is not a single technology but an ecosystem of tools, platforms, and business models.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Digital Finance — P2P Lending via FinTech

What is Digital Lending?

In the conventional lending model, a borrower physically visits a bank branch, submits paper-based documentation (salary slips, property documents, identity proofs), and awaits a manual credit appraisal that could take days or weeks. The decision rests with a human officer who assesses risk using a narrow set of financial indicators.

Digital lending replaces this entire process with automated, technology-driven workflows. Every stage — from loan discovery to disbursal — is conducted remotely through mobile and web-based platforms. Creditworthiness is assessed within minutes using algorithmic models that analyse alternative data such as transaction history, device behaviour, and social patterns, removing the need for physical presence or paper documentation.

Key definitions:

- Digital Lending — A remote and automated lending process executed entirely through digital technologies, without requiring the borrower to visit a physical institution.

- Digital Lending Apps — Mobile and web-based platforms that connect borrowers with digital lenders and manage the loan lifecycle end-to-end.

- The RBI Working Group on Digital Lending identifies this transformation as the emergence of Bank 4.0 — an era in which FinTech capabilities are deeply integrated into traditional banking operations.

The FinTech Ecosystem — Technologies and Sectors

FinTech (Financial Technology) refers to the application of technology to deliver financial services more efficiently. It is not a single technology but an ecosystem of tools, platforms, and business models.

Core Functional Areas of FinTech:

These are the domains within which FinTech operates:

- Financial Regulation — compliance and reporting tools

- Risk Management — automated fraud detection, credit scoring

- Funding — digital capital allocation and crowdfunding

- Valuation — algorithmic asset pricing and wealth management

Technologies Powering FinTech:

Each technology solves a specific financial problem:

| Technology | Role in Finance |

|---|---|

| Distributed Ledger / Blockchain | Tamper-proof, decentralised record-keeping — eliminates need for a central authority |

| Artificial Intelligence (AI) | Automated credit decisions, fraud detection, personalised financial advice |

| Big Data Analytics | Processing millions of data points to assess risk and understand customer behaviour |

| Internet of Things (IoT) | Real-time asset monitoring for insurance and lending |

| Cloud Computing | Scalable, low-cost infrastructure for financial platforms |

| Cyber Security | Protection of digital financial transactions and data |

| Quantum Computing | Future capability for complex financial modelling |

| Virtual/Augmented Reality | Emerging interfaces for financial services |

| Automation / Robotics | Process automation in back-office operations |

FinTech Verticals (Sectors):

FinTech has fragmented into specialised industries:

- PaymentsTech — UPI, digital wallets, payment gateways

- Digital Banking — neo-banks, mobile-first banking

- FinTech Lending — P2P platforms, digital credit

- Digital Wealth Management — robo-advisors, automated investment

- Capital Markets (Algo Trading) — algorithmic and high-frequency trading

- Equity Crowdfunding — retail investment in startups

- InsurTech — digital insurance products

- BigTech — large technology companies offering financial services

- PropTech — technology applied to real estate transactions

Global Context — Why Digital Lending Emerged

The 2008 global financial crisis acted as a structural catalyst for digital lending. In its aftermath, traditional financial institutions significantly tightened credit standards — individuals with limited credit histories, small businesses, and informal sector workers found themselves effectively excluded from formal credit markets.

This credit vacuum was filled by technology-driven entrants. Big Tech companies, e-commerce platforms, and telecom service providers leveraged their existing customer data and digital infrastructure to enter the lending space — either independently or in partnership with regulated financial institutions.

Among the most significant innovations was the emergence of Peer-to-Peer (P2P) lending platforms — digital intermediaries that directly connected individuals willing to lend with individuals seeking to borrow, bypassing the traditional bank model entirely.

The Four Digital Lending Models:

These models describe who lends to whom in the digital ecosystem:

| Model | Full Form | Description |

|---|---|---|

| P2P | Person-to-Person | An individual lends directly to another individual |

| P2B | Person-to-Business | An individual lends to a business entity |

| B2P | Business-to-Person | A business entity lends to an individual |

| B2B | Business-to-Business | One business lends to another |

The significance of these models is that they demonstrate how the role of a bank as a financial intermediary has been disaggregated — any combination of parties can now form a lending relationship through a digital platform.

India's Digital Lending Ecosystem

India's digital lending ecosystem is still in a developmental phase, with participation growing but unevenly distributed. NBFCs currently lead digital lending in India, having adopted digital processes more rapidly than traditional banks, which are gradually transitioning.

The Two Structural Forms of Digital Lending in India:

1. Balance Sheet Lending (BSL)

In this model, the lending entity deploys its own capital to fund loans. The institution directly bears the credit risk — if a borrower defaults, the institution absorbs the loss. Traditional banks and NBFCs that lend from their own funds operate under this model.

The key feature: the lender has skin in the game — their own money is at risk, which incentivises careful credit assessment.

2. Market-Place Lending (MPL)

In this model, the platform acts purely as an intermediary or marketplace, connecting lenders (investors) with borrowers. The platform does not deploy its own capital and bears no credit risk — it simply facilitates the match and earns fees for doing so.

The key feature: because the intermediary has no capital at risk, the regulatory challenge is ensuring it still performs rigorous credit assessment on behalf of lenders.

P2P lending is the most direct form of MPL. Platforms operating as marketplaces are classified as Lending Service Providers (LSPs).

Three Types of Digital Lenders — A Regulatory Classification

RBI categorises entities operating in the digital lending space into three types. This classification determines their regulatory obligations:

Type 1: Traditional Lenders Operating Digitally

These are established banks, NBFCs, and other RBI-regulated entities that have added digital channels to their existing operations — implementing e-KYC, digital documentation, and online application processes. They continue to lend from their balance sheet and remain fully regulated by RBI.

The digital channel is an enhancement; the regulatory framework is unchanged.

Type 2: Lending Service Providers (LSPs)

LSPs are technology-driven platforms that partner with regulated entities (banks, NBFCs) to facilitate lending. Their value lies in their technological capability — they build the customer-facing application, run the credit assessment algorithm, and acquire customers. The regulated partner entity provides the capital and bears the credit risk.

Because LSPs function as service providers to regulated entities (rather than as lenders themselves), they fall under RBI's regulatory radar only to the extent of outsourcing guidelines. There are two sub-categories:

-

(a) RBI-Regulated LSPs — entities that have been granted specific registration by RBI, such as:

- NBFC-Account Aggregator (NBFC-AA) — aggregates financial data with user consent

- NBFC-Peer to Peer Lending Platform (NBFC-P2P) — facilitates direct person-to-person loans

-

(b) Unregulated LSPs — entities that operate entirely outside the regulatory ecosystem, with no RBI registration or oversight. These are the entities that create the most systemic risk.

Type 3: Fringe Lenders

Shadow balance sheet lenders — entities that lend money from their own funds but have not registered themselves with any regulatory authority. Operating under cover of digital anonymity, these platforms charge predatory interest rates, employ coercive recovery practices, and evade oversight. Identifying and monitoring such entities in real time is a significant regulatory challenge.

The Rent-an-NBFC Model — A Regulatory Arbitrage

This model represents one of the most significant regulatory concerns in India's digital lending ecosystem. It works as follows:

The problem it exploits: An unregistered FinTech company wishes to engage in lending but lacks an RBI licence. To circumvent this, it enters into an arrangement with a small, registered NBFC.

How the arrangement works:

- The FinTech company sources borrowers, performs credit assessment, and determines loan terms.

- The NBFC formally disburses the loan (since it has the regulatory licence to lend).

- To induce the NBFC to participate, the FinTech provides a First Loss Default Guarantee (FLDG) — a contractual commitment to absorb the first portion of any credit losses.

Why this is problematic:

- The FinTech entity assumes all substantive credit risk off its own balance sheet, thereby avoiding RBI's capital adequacy requirements — it has the economic exposure without the regulatory obligation.

- The NBFC earns volume without performing its own credit function, becoming a mere conduit or "rent-a-licence" vehicle.

- Operating under digital anonymity, the FinTech faces no effective oversight — creating conditions for money laundering, regulatory evasion, and systemic risk.

- This structure allows unregulated entities to lend without meeting prudential norms, undermining the purpose of the regulatory framework.

In essence, the model separates the economic reality of lending from its regulatory form, allowing unregulated entities to perform regulated activities.

RBI's Guidelines on Digital Lending — Regulatory Response

Recognising the systemic risks from unregulated digital lending, RBI constituted a Working Group on Digital Lending in January 2021. Its recommendations were accepted by RBI in August 2022, and updated comprehensive guidelines were issued in September 2022.

The guidelines are structured around four pillars:

Pillar 1: Money Flow Discipline

The core problem in many fraudulent digital lending schemes was that intermediaries were intercepting and misusing loan funds. RBI addressed this directly:

- All loan disbursements and repayments must flow directly between the borrower's bank account and the Regulated Entity (RE) — no LSP or intermediary may touch or route the funds.

- LSP fees and charges must be paid directly by the RE to the LSP — LSPs are prohibited from deducting their fees from borrower disbursals.

Why this matters: It ensures that every rupee of loan money is traceable and flows only through regulated entities.

Pillar 2: Pre-Contractual Transparency

Borrowers were often unaware of the true cost of digital loans until after disbursement. RBI mandated:

- A mandatory Key Fact Statement (KFS) must be provided to the borrower before loan execution — clearly disclosing all terms.

- The KFS must include the Annual Percentage Rate (APR) — the complete, annualised cost of borrowing inclusive of all fees and charges. This allows borrowers to make meaningful comparisons across products.

Why APR matters: Without it, lenders could quote a low nominal interest rate while burying additional charges in fees. APR combines everything into one number.

Pillar 3: Borrower Rights

- No automatic credit limit increases — any increase in a borrower's credit limit requires their explicit prior consent.

- Cooling-off period — borrowers have a defined window after loan disbursal during which they may repay the principal and exit the loan without any prepayment penalty.

- Both REs and LSPs must maintain designated grievance redressal officers — a named individual responsible for resolving borrower complaints.

Pillar 4: Data Protection Rights

- Data collection must be need-based — lenders and platforms may only collect data that is necessary for the lending purpose.

- Borrowers hold the right to accept, deny, or revoke consent to data collection at any point in time.

Credit Bureau Integration:

- All loans sourced through digital platforms must be reported to Credit Information Companies (CICs) — this ensures a borrower's total digital debt is visible to all future lenders and prevents over-leverage across multiple platforms.

Growth Drivers of Digital Lending in India

The rapid growth of digital lending in India is explained by a convergence of supply-side enablers and demand-side pressures.

Supply Side — What Made Digital Lending Technologically Feasible:

a. Technological Advancements

Several technologies made real-time credit assessment at scale possible:

- APIs — enabled seamless data exchange between financial institutions and platforms

- Artificial Intelligence — automated loan underwriting with minimal human intervention

- Big Data Analytics — allowed lenders to assess creditworthiness using non-traditional data

- Blockchain — provided secure, tamper-proof transaction records

- Cloud Computing, Alternative Data Sources, Vertical Search Engines — reduced infrastructure costs and expanded data availability

b. Digital Infrastructure — Connectivity

Without widespread internet access, digital lending cannot reach scale:

- Internet subscribers: 61% of India's population (March 2021)

- Broadband connections: 57% of population (March 2021)

- Mobile connections: 89% of population (March 2021)

c. Government Initiatives — The Policy Foundation

The Indian government built the enabling infrastructure for digital finance through:

- Jan Dhan Yojana — created bank accounts for previously unbanked populations, giving digital lenders a channel for disbursement and repayment

- Aadhaar Enrolment — established a universal digital identity infrastructure, enabling e-KYC

- Digital India — a comprehensive programme to build digital infrastructure and literacy

- India Stack — a collection of open API frameworks and technology products maintained by various government agencies, enabling private platforms to plug into public infrastructure (Aadhaar, UPI, DigiLocker, etc.)

India Stack is particularly significant: it is what allows a private lending app to verify your identity via Aadhaar, check your bank account via account aggregators, and receive repayments via UPI — all within a single, regulated framework.

Demand Side — What Made Digital Lending Socially Necessary:

a. Economic Development

- Growth of IT/ITeS employment created a large population of salaried urban workers with digital literacy and credit needs.

- Urban migration and rising per capita incomes expanded the addressable market.

b. Unmet Credit Demand — The Structural Gap

This is the most important demand driver: formal banks systematically under-served large segments of the population.

- Informal workers, small traders, agricultural labourers, and first-time borrowers lack the formal income documentation and credit history that traditional banks require.

- Banks were reluctant to lend small-ticket loans (<₹1 lakh) to individuals with no credit bureau records — these borrowers were termed sub-prime or first-time borrowers.

- Digital lenders, using alternative data, could assess these borrowers where banks could not.

c. COVID-19 — Behavioural Acceleration

The pandemic acted as a forced accelerant:

- Physical bank visits became impossible — digital channels became the only option.

- E-commerce and e-payment adoption surged, familiarising populations with digital financial transactions.

- Pandemic-induced income loss and financial stress increased demand for credit.

- Social distancing reduced the social stigma around borrowing digitally.

d. Demographics

- India has one of the world's youngest populations — a generation of digital natives who are more comfortable transacting on a smartphone than at a bank branch.

- Higher literacy rates among this cohort translate to more informed use of digital financial products.

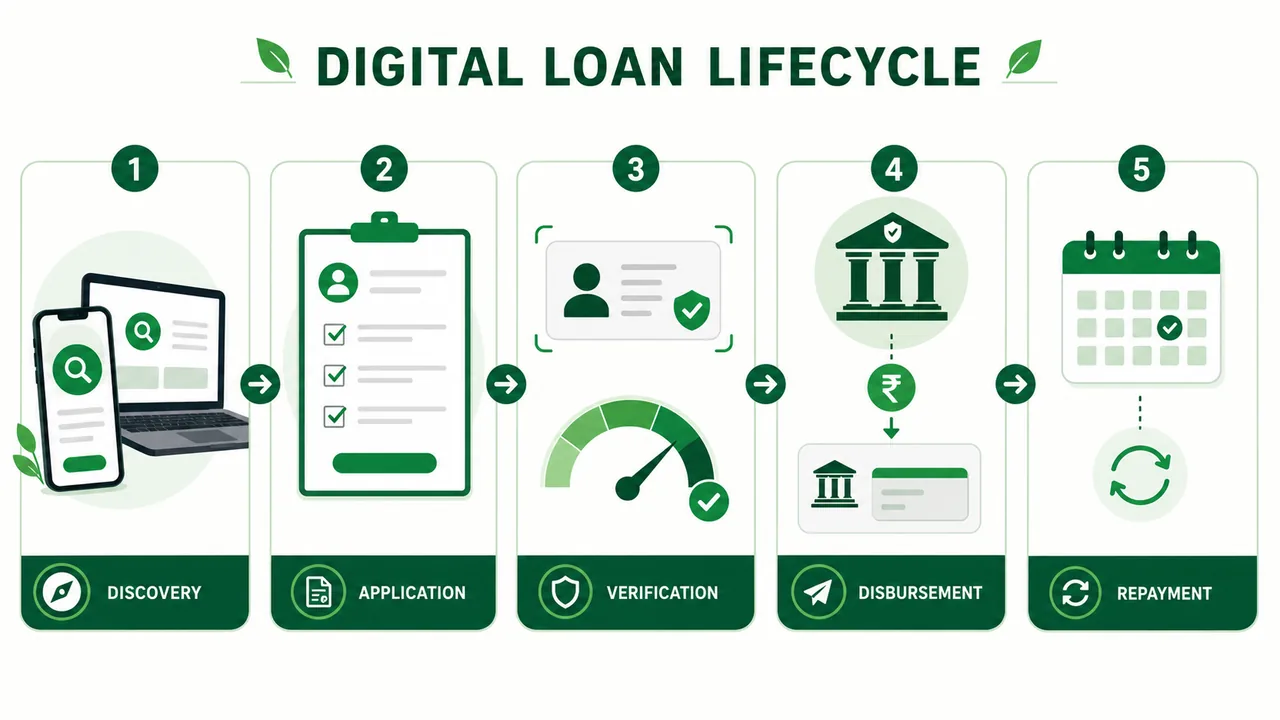

The Digital Loan Lifecycle — Five Stages

Every digital loan follows a standardised lifecycle, regardless of the platform. Understanding each stage clarifies what happens to a borrower's data, money, and obligations at each point.

Stage 1 — Discovery and Registration

A borrower discovers the lending application through online search, app store listings, or digital marketing. During registration, the platform collects basic identifiers (email, mobile number) and requests various device permissions. Note: excessive permission requests (contacts, camera without necessity) were a key abuse pattern that RBI's data consent guidelines addressed.

Stage 2 — Application Processing

The borrower submits personal and financial information — occupation, income, purpose of loan, and any existing liabilities. This data feeds into the platform's credit assessment model.

Stage 3 — User Verification

The platform conducts identity verification (e-KYC using Aadhaar), generates a credit score by querying Credit Information Companies (CICs) and using proprietary models, and presents the borrower with eligible loan products — specifying amount, tenure, and interest rate. Document authentication completes this stage.

Stage 4 — Disbursement

Upon acceptance of loan terms, funds are transferred directly to the borrower's account — via e-wallets, bank accounts, or cash brokers. Per RBI guidelines, this transfer must flow directly from the Regulated Entity — not through the LSP.

Stage 5 — Repayment

The borrower repays via pre-authorised e-mandates (ECS/NACH), scheduled online transfers, or credit card. In the event of default, the LSP intervenes for collection — subject to RBI's fair practices guidelines on recovery.

Digital Banking Unit (DBU) — Formalising Digital Service Delivery

A Digital Banking Unit (DBU) is a specialised, fixed-point business unit established by a bank to deliver digital banking products and services in a structured physical setting.

The DBU concept addresses a gap in India's banking landscape: while urban consumers are comfortable with fully mobile banking, large segments of the population — particularly in Tier 3 to Tier 6 towns — require physical assistance to access and use digital banking services. A DBU provides this in both self-service mode (customers operate digital interfaces independently) and assisted mode (bank staff guide customers through digital processes).

Key Regulatory Features of DBUs:

- Scheduled Commercial Banks with demonstrated digital banking experience may open DBUs in any centre from Tier 1 to Tier 6, without requiring separate RBI approval for each location.

- Each DBU must be physically distinct — housed separately from the regular branch with dedicated entry/exit — to reinforce its identity as a digital-only service point.

- DBUs must offer products on both sides of the balance sheet:

- Liability side: savings accounts, fixed deposits — fully digital account opening

- Asset side: online application, processing, and disbursal of retail, MSME, and government scheme loans — with end-to-end digital processing

The DBU is therefore a structured mechanism through which banks extend digital lending and banking access to geographically and digitally underserved populations.

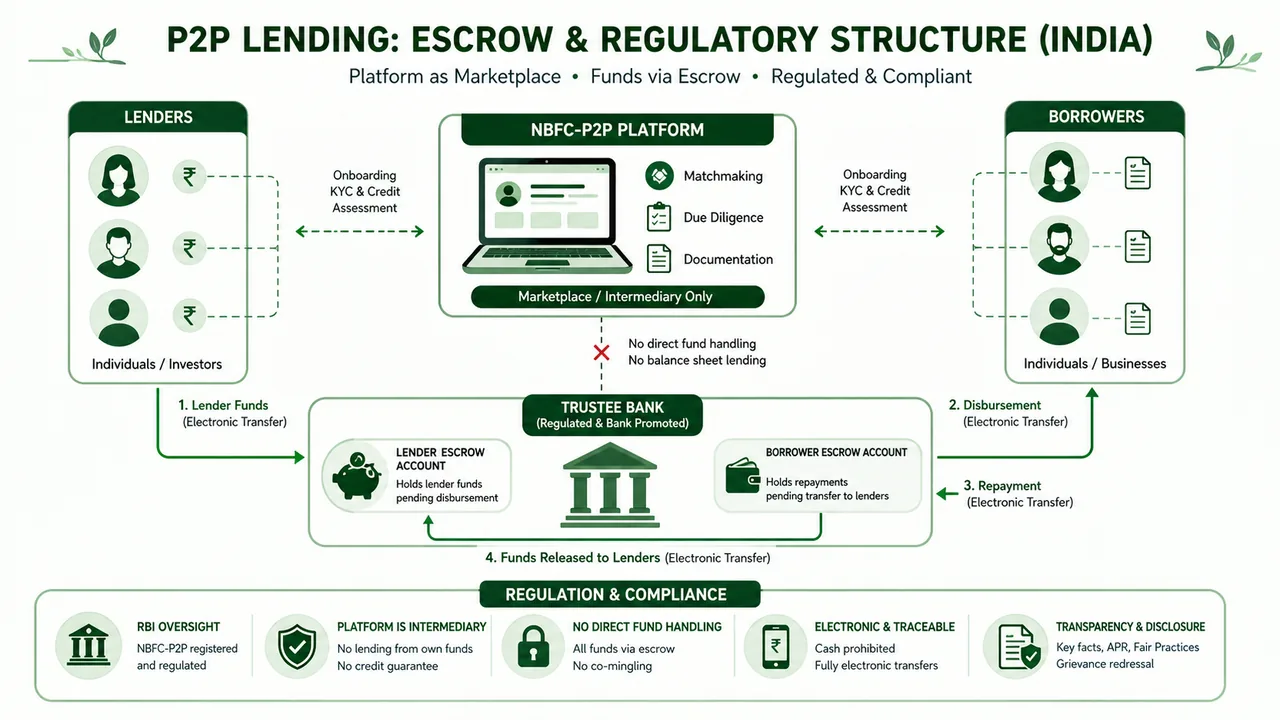

Peer-to-Peer (P2P) Lending in India — RBI's Regulatory Framework

P2P lending is the most direct disintermediated lending model: individuals with surplus funds lend directly to individuals or businesses seeking funds, without a bank acting as the intermediary. The P2P platform earns a fee for facilitating this match but does not itself lend or borrow.

Per RBI's Master Direction, a Peer-to-Peer Lending Platform is an online intermediary that facilitates lending between participants. The corporate entity operating such a platform is registered and regulated as a Non-Banking Financial Company – Peer to Peer Lending Platform (NBFC-P2P).

Registration Eligibility:

An entity may only operate a P2P lending platform if it:

- Is incorporated under the Companies Act, 2013

- Is registered with RBI specifically as an NBFC-P2P

- Maintains minimum Net Owned Funds of ₹2 crore — demonstrating financial standing

The Fundamental Character of NBFC-P2P — Pure Intermediary:

The defining principle is that an NBFC-P2P is exclusively a marketplace operator, not a financial institution. It may:

- Provide the online platform for matching lenders and borrowers

- Conduct due diligence on participants

- Handle loan documentation, coordinate disbursement, and assist in repayment and recovery

- Obtain credit information with explicit participant consent

It may not engage in any activity that converts it into a lender or risk-bearer. The prohibited activities, and the reasoning behind each prohibition, are:

| Prohibited Activity | Regulatory Rationale |

|---|---|

| Accepting deposits from participants | NBFC-P2P is not a bank — deposit-taking requires a separate banking licence |

| Lending from its own funds | Would convert it from intermediary to lender — destroying the P2P model |

| Providing credit guarantee or credit enhancement | If the platform guarantees repayment, lenders have no incentive to assess risk themselves; it also creates off-balance sheet risk |

| Holding lender/borrower funds on its own balance sheet | Prevents co-mingling of platform funds with participant funds; mitigates fraud |

| Permitting international fund flows | Cross-border P2P lending would bypass capital account controls |

| Cross-selling unrelated products | Creates conflicts of interest — platform would prioritise product sales over quality loan matching |

Only clean loans are permitted — unsecured loans with no collateral, credit guarantee, or enhancement attached.

Prudential Limits for NBFC-P2P — The Exam-Critical Numbers

RBI imposes specific quantitative limits on the P2P ecosystem to contain systemic risk. Each limit serves a distinct protective purpose:

Leverage Limit:

- Maximum Leverage Ratio: 2 — the NBFC-P2P's total liabilities may not exceed twice its net owned funds. This controls the scale at which the platform can operate relative to its own capital base.

Lender Protection Limits:

- Aggregate lender exposure (across all P2P platforms): ₹50 lakh — a single individual may not lend more than ₹50 lakh in total across all P2P platforms. This caps the maximum financial exposure of any retail lender to P2P credit risk.

- CA certificate requirement: for investments exceeding ₹10 lakh — lenders who invest more than ₹10 lakh must provide a certificate from a Chartered Accountant confirming a minimum net worth of ₹50 lakh. The rationale: higher exposure to unguaranteed risk requires demonstrated financial capacity to absorb potential losses.

Borrower Protection Limits:

- Aggregate borrower exposure (across all P2P platforms): ₹10 lakh — prevents any individual from accumulating excessive unsecured debt across multiple P2P platforms.

- Maximum loan tenure: 36 months — P2P lending is intended as short-to-medium-term credit, not long-term financing.

Concentration Limit (Diversification Requirement):

- A single lender's exposure to a single borrower (across all platforms): ₹50,000 — this is perhaps the most important limit. By capping any one lender's exposure to any one borrower at ₹50,000, RBI compels lenders to distribute their funds across multiple borrowers. This diversification reduces the impact of any individual borrower default.

Mandatory Risk Disclosure:

Lenders must formally declare their understanding of the risks involved and explicitly acknowledge that P2P platforms provide no guarantee of principal repayment or interest payment. The platform is a facilitator — the risk of borrower default rests entirely with the lender.

Fund Transfer Mechanism — The Escrow Structure

To ensure integrity in the movement of funds between lenders and borrowers, RBI mandates a specific fund flow architecture:

All P2P lending transactions must be routed through escrow accounts maintained by a bank-promoted trustee.

An escrow account is a neutral, third-party-managed account that holds funds until specified conditions are met. In P2P lending, the trustee (a bank) manages these accounts on behalf of lenders and borrowers — the NBFC-P2P has no direct access to the funds.

Minimum Two Escrow Accounts Required:

- Lender-side Escrow — holds funds received from lenders awaiting matching and disbursement to borrowers

- Borrower-side Escrow — holds repayment amounts received from borrowers awaiting transfer to the respective lenders

Operational Rules:

- Cash transactions are entirely prohibited — every transaction must be electronic and traceable

- Funds may not be released from escrow until the conditions for disbursement or repayment are properly satisfied

- Idle funds held in escrow may only be invested by the NBFC-P2P in instruments specified by RBI — trading in securities or speculative investments is not permitted

The escrow structure ensures that lender and borrower funds are never co-mingled with the NBFC-P2P's own funds and cannot be misappropriated by the platform operator.

Credit Information and Disclosure Requirements

CIC Membership and Reporting:

- Every NBFC-P2P must be a member of all Credit Information Companies (CICs) in India.

- They are obligated to submit complete, accurate, and up-to-date credit data on all borrowers to CICs — with participant consent. This ensures that a borrower's P2P obligations are visible across the formal credit system, preventing a borrower from taking simultaneous loans from multiple P2P platforms beyond prescribed limits.

Participant Disclosures:

The platform must disclose to lenders: complete borrower details, credit scores, loan terms, and interest rates. Similarly, borrower details are shared with lenders and vice versa. Participant information is maintained confidentially with respect to third parties.

Public Disclosures (Website):

NBFC-P2Ps must publish the following on their websites for stakeholder transparency:

- Credit assessment methodology

- Data usage and protection policy

- Grievance redressal mechanism

- Portfolio performance data (aggregate default rates, returns, etc.)

- Business model

Interest Rate Presentation:

All interest rates must be presented in Annualised Percentage Rate (APR) format — ensuring borrowers can compare the true cost of a P2P loan against other credit products.

A Fair Practices Code must be maintained on the platform's website, setting out the standards of conduct participants may expect.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Digital Lending | Remote & automated lending using digital tech |

| RBI Working Group | Formed January 2021, recommendations accepted August 2022 |

| Updated Guidelines | Issued September 2022 |

| Bank 4.0 | Blending FinTech and traditional banking |

| Digital Lending Models | P2P, P2B, B2P, B2B |

| India Leaders | NBFCs lead; banks adopt digital processes |

| Two Forms in India | Balance Sheet Lending (BSL) & Market-Place Lending (MPL) |

| 3 Types of Lenders | Traditional (regulated), LSPs (tech platforms), Fringe (shadow/unregistered) |

| LSP Types | (a) RBI-regulated (NBFC-AA, NBFC-P2P) (b) Outside regulatory ecosystem |

| Rent-an-NBFC | Unregulated entities lend via FLDG with small NBFCs |

| KFS | Mandatory Key Fact Statement before loan execution |

| APR Disclosure | Required in KFS |

| Cooling-off Period | Borrowers can exit loans without penalty |

| Data Consent | Explicit; borrower can accept, deny, or revoke |

| Internet Penetration | 61% of population (Mar 2021) |

| Mobile Penetration | 89% of population (Mar 2021) |

| Broadband | 57% of population (Mar 2021) |

| Govt Initiatives | Jan Dhan, Aadhaar, Digital India, India Stack |

| Loan Lifecycle | 5 stages: Discovery → Processing → Verification → Disbursement → Repayment |

| DBU | Digital Banking Unit — self-service + assisted mode |

| DBU Location | Tier-1 to Tier-6 centres (no specific RBI permission needed) |

| NBFC-P2P Registration | Companies Act 2013 + RBI registration |

| Min Net Owned Funds | ₹2 crore for NBFC-P2P |

| NBFC-P2P Role | Intermediary only — no deposits, no lending on own |

| Loan Type | Clean loans only (no secured/guaranteed lending) |

| Max Leverage Ratio | 2 |

| Lender Aggregate Cap | ₹50 lakh across all P2P platforms |

| CA Certificate Needed | For lenders investing > ₹10 lakh (net worth ≥ ₹50 lakh) |

| Borrower Aggregate Cap | ₹10 lakh across all P2Ps |

| Max Loan Term | 36 months |

| Single Borrower Exposure | ₹50,000 per lender |

| Fund Transfer | Via escrow accounts (bank-promoted trustee) |

| Escrow Accounts | Minimum 2 required |

| Cash Transactions | Prohibited |

| CIC Membership | Mandatory for all NBFC-P2Ps |

| Interest Rate Format | APR (Annualized Percentage Rate) |

| P2P Guarantee | Platform does NOT guarantee principal or interest |

Lesson Doubts

Ask questions, get expert answers