💧 Liquidity Management Policy

Understanding CRR, SLR, exemptions, and impacts on liquidity.

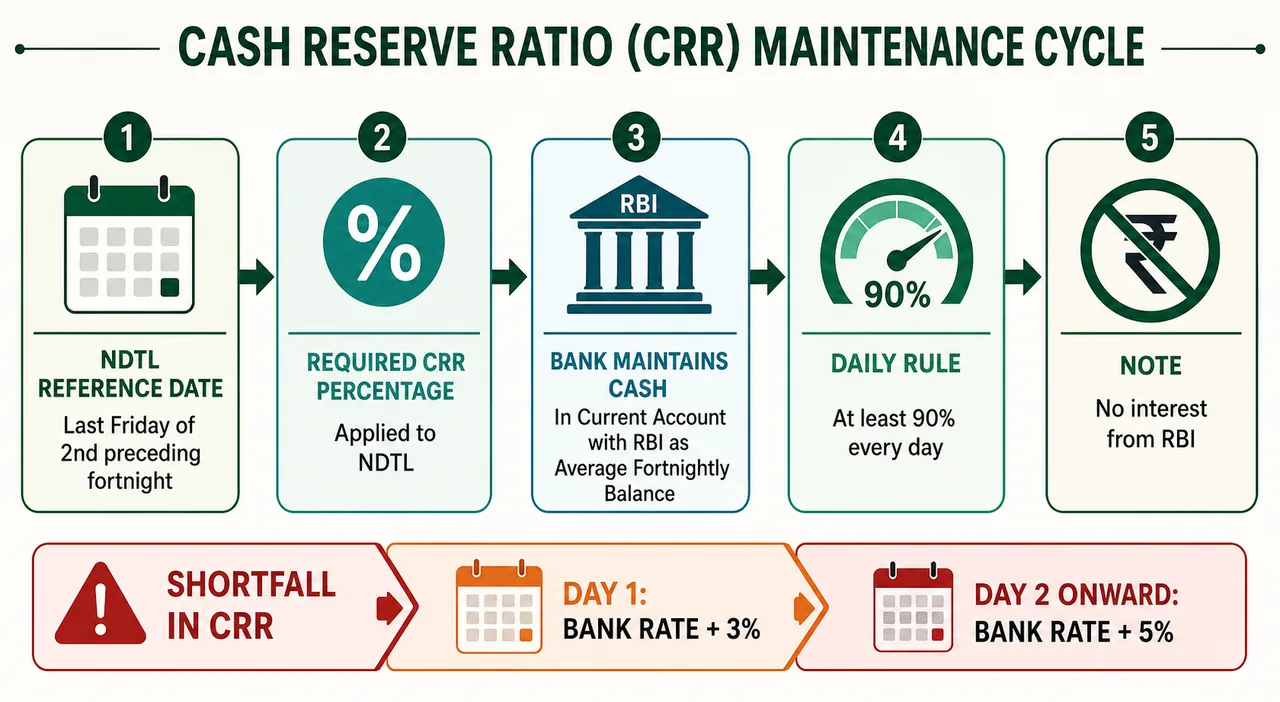

Cash Reserve Ratio (CRR)

- Legal provisions: Section 42 (1) of RBI Act.

- Rate: Min (floor) & Max (ceiling) decided by RBI (no statutory floor or ceiling) as % of NDTL as on last Friday of 2nd preceding fortnight. Previously limits were 3%–20%, but RBI Act was amended to give RBI complete discretion.

- How maintained: As average fortnightly balance on reporting Friday.

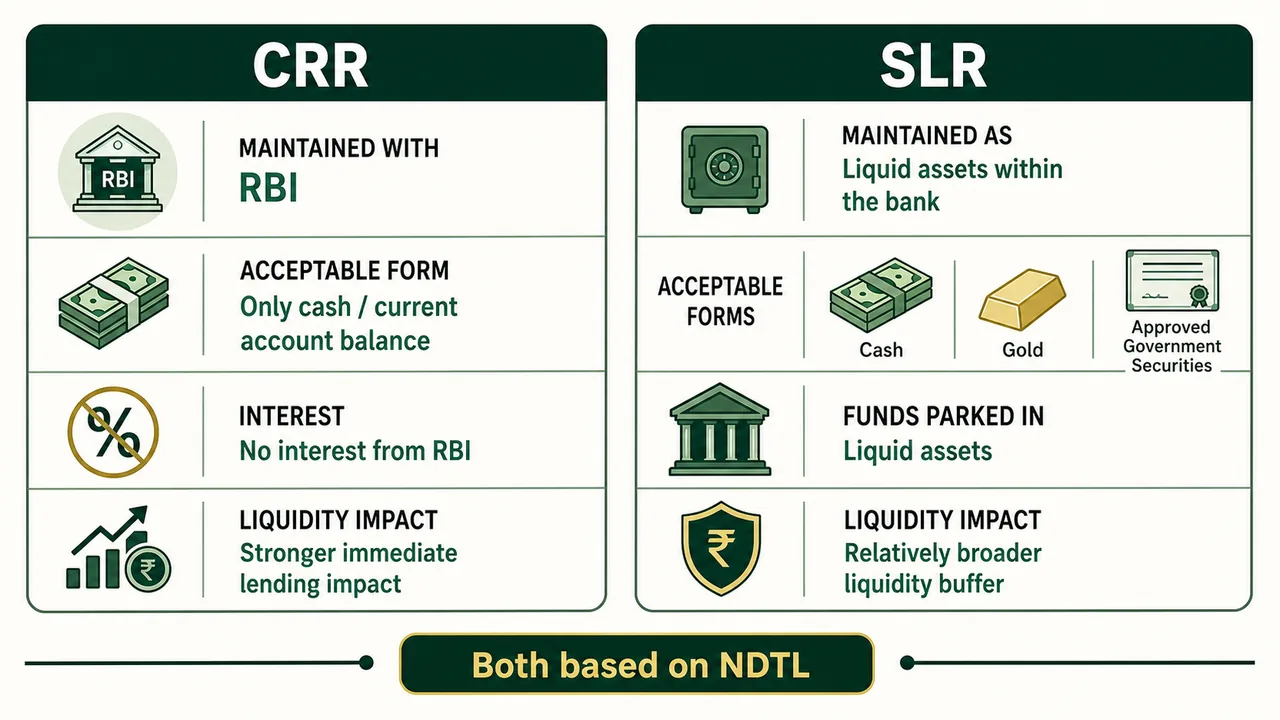

- Where maintained: In a current account with RBI.

- Min daily balance: Min 90% of average fortnightly balance — banks don't need the exact average every day, but must not fall below 90% of required average on any given day.

- Interest: No interest w.e.f. fortnight ended 31st Mar 2007.

- Default in maintaining CRR: Bank to pay interest to RBI at bank rate + 3% pa for 1st day and subsequently, bank rate + 5% pa for 2nd day onward for default period and amount.

- Return: Form A (Fortnightly — provisional within 7 days, final within 20 days).

- Change impact: Reduction increases bank liquidity & vice versa.

Example: If and , the Average balance required .

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Cash Reserve Ratio (CRR)

- Legal provisions: Section 42 (1) of RBI Act.

- Rate: Min (floor) & Max (ceiling) decided by RBI (no statutory floor or ceiling) as % of NDTL as on last Friday of 2nd preceding fortnight. Previously limits were 3%–20%, but RBI Act was amended to give RBI complete discretion.

- How maintained: As average fortnightly balance on reporting Friday.

- Where maintained: In a current account with RBI.

- Min daily balance: Min 90% of average fortnightly balance — banks don't need the exact average every day, but must not fall below 90% of required average on any given day.

- Interest: No interest w.e.f. fortnight ended 31st Mar 2007.

- Default in maintaining CRR: Bank to pay interest to RBI at bank rate + 3% pa for 1st day and subsequently, bank rate + 5% pa for 2nd day onward for default period and amount.

- Return: Form A (Fortnightly — provisional within 7 days, final within 20 days).

- Change impact: Reduction increases bank liquidity & vice versa.

Example: If and , the Average balance required .

Major Demand and Time Liabilities for CRR

Major Liabilities Exempted from Calculation of NDTL:

- Paid up capital and Reserves & surplus.

- Borrowing or refinance from RBI and apex institutions such as NABARD, NHB etc.

- No. of other small items.

Liabilities Excluded from Calculation of CRR:

These are excluded to prevent double-counting of reserves within the banking system and to encourage specific refinancing.

a. Liabilities to the banking system. b. Credit balance in ACU account. c. DTL in respect of off-shore banking units. d. Inter-bank term deposit up to 1 year maturity. e. Incremental Auto & Home, MSME Loans given wef 14.2.20 to 31.7.20, exempted for 5 years. f. New MSME borrowers who did not avail any loan till 1.1.2021, shall be excluded for loans up Rs.25 lac disbursed till 31.12.21, for 1 year.

Statutory Liquidity Ratio (SLR)

- Legal provisions: Section 24 of B R Act.

- Rate: RBI can fix up to 40% (Max) of NDTL — no minimum statutory floor. Section 24 of BR Act caps SLR at 40% but sets no statutory minimum. NDTL as on last Friday of 2nd preceding fortnight (same as CRR).

- Form of SLR investments (maintained as specified assets — unlike CRR which is cash only):

- cash balance

- balance with other banks and excess CRR balance with RBI

- investment in gold / gold bonds (subject to some conditions)

- investment in unencumbered approved securities (govt. securities / trustee securities including purchase under LAF).

- Default in maintaining SLR: Interest payment as in CRR.

- SLR return: Form VIII by the 20th of every month.

- Impact of change: Reduction frees funds from investment, which can be used for lending purpose (and vice versa).

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| CRR — Legal Provision | Section 42(1) of RBI Act |

| CRR — Rate | Min & Max decided by RBI (no statutory floor or ceiling) as % of NDTL on last Friday of 2nd preceding fortnight |

| CRR — How Maintained | As average fortnightly balance on reporting Friday |

| CRR — Where Maintained | In a current account with RBI |

| CRR — Min Daily Balance | Not less than 90% of average fortnightly balance |

| CRR — Interest | No interest paid w.e.f. fortnight ended 31 Mar 2007 |

| CRR — Default Penalty | Bank rate + 3% p.a. for 1st day; bank rate + 5% p.a. from 2nd day onward |

| CRR — Return | Form A (Fortnightly — provisional within 7 days, final within 20 days) |

| CRR — Change Impact | Reduction increases bank liquidity; increase reduces it |

| NDTL Exemptions | Paid-up capital & reserves; borrowings/refinance from RBI, NABARD, NHB; other small items |

| CRR Exclusions | Liabilities to banking system; ACU credit balance; offshore banking DTL; inter-bank term deposits ≤ 1 year; incremental auto/home/MSME loans (14.2.20–31.7.20, 5-yr exemption); new MSME borrowers (no prior loan till 1.1.21, loans ≤₹25L till 31.12.21, 1-yr exemption) |

| SLR — Legal Provision | Section 24 of BR Act |

| SLR — Rate | RBI can fix up to 40% (max) of NDTL; no minimum statutory floor |

| SLR — Form of Investment | (1) Cash balance, (2) balance with other banks & excess CRR with RBI, (3) gold/gold bonds, (4) unencumbered approved securities (govt./trustee securities incl. LAF) |

| SLR — Maintained As | Specified assets (cash, gold, unencumbered approved securities) — unlike CRR which is cash only |

| SLR — Default Penalty | Same as CRR (bank rate + 3% / +5%) |

| SLR — Return | Form VIII by the 20th of every month |

| SLR — Change Impact | Reduction frees funds for lending; increase locks more funds in approved securities |

| CRR vs SLR Key Difference | CRR = cash with RBI only; SLR = broader liquid assets (cash + gold + securities) |

Lesson Doubts

Ask questions, get expert answers