🛡️ Principles of Sound Lending

Understanding the foundational concepts of bank lending, risk management, and the key principles: Safety, Liquidity, Profitability, Purpose, and Diversification.

Principles of Sound Lending

Introduction to Banking & Lending

Banking Basics

- Accept public deposits: Banks act as secure custodians of public funds. They accept deposits from individuals and businesses, creating a safe and reliable system for the public to park their money while earning interest.

- Provide loans: The fundamental economic role of a bank is extending credit. They lend the pooled public deposits for business, varied economic activities, and specialized investments.

- Act as financial intermediaries: Banks are the crucial bridge connecting the economy's vital parts: those with surplus funds (depositors who want to save) and those in need of funds (borrowers who need capital to grow or spend).

Types of Deposits

- Banks cater to diverse customer needs by offering funds in varied forms:

- Savings accounts: For everyday transactional needs with moderate interest.

- Current accounts: Used primarily by businesses for high-volume, unrestricted transactions (usually earning no interest).

- Fixed deposits (Term deposits): Locked-in funds for a specific period earning higher interest.

- Flexi deposits: A hybrid offering liquidity along with better interest rates.

- These varied choices depend directly on a depositor's individual needs for safety, income generation, and liquidity.

Depositor Preferences

- Depositors want guaranteed safety of their money above everything else. A bank's entire existence relies on this fundamental trust.

- They desire interest income on their idle money. Some prefer monthly payouts for steady cash flow, while others prefer to let the interest compound and reinvest.

- They deeply value robust transactional abilities: easy access to funds through issuing cheques, Net Banking, and widespread ATM card usage.

Central Bank's Role

- The Central Bank (like the RBI in India) strictly regulates overall banking operations to ensure banks don't take undue risks with public money.

- By setting strict guidelines, the central bank actively enhances and maintains public trust in banks.

- This strong regulatory framework successfully drives significant deposit inflow to banks by ensuring systemic stability across the financial ecosystem.

Banker's Responsibility & Obligations

- Maintain trust: A bank must continuously nurture a trusted and transparent relationship with every depositor.

- Effective utilization: The bank ensures these pooled funds are utilized effectively and safely by lending them prudently.

- Return on demand: Banks have an absolute obligation to return deposits when required unconditionally (based on the deposit type's terms).

- Owe interest: The bank owes and must transparently pay interest on the accepted deposits based on defined rates.

- Maintain Liquidity: To meet sudden and ongoing withdrawal requests, the bank needs to proactively maintain sufficient liquidity (ready cash or easily convertible assets) specifically for meeting repayment demands.

Effective Fund Management

- Managing bank funds is a tightrope walk. Money should be strictly balanced between three critical factors: being safe (minimizing default risk), liquid (available when depositors want it), and income-generating (earning enough to pay deposit interest and make a profit).

- Because of this delicate balance, the overwhelming focus of a bank remains on making loans and investments that are repaid reliably and consistently.

Bank's Primary Income

- A large portion of bank revenue—the core of its business model—stems from the net interest margin (interest earned on loans and advances minus interest paid on deposits).

- Therefore, there naturally lies a huge, existential importance on highly efficient and disciplined lending.

- Aside from loans, banks also actively invest surplus funds (like in government securities) for additional, stable income.

Challenges and Risks in Lending

Challenges in Lending

- Lending money inherently carries significant risks—chiefly, the risk that the borrower will not pay it back (credit risk).

- Individual lenders or private citizens generally lack the deep, necessary expertise for widespread lending and conducting highly accurate multi-variable risk assessments.

- Conversely, borrowers find it significantly easier, faster, and more standardized to approach established banks than attempting to source large funds from individual persons for required loans.

Banks vs. Peer-to-Peer Lending

- Banks are vastly better equipped and structurally designed to manage sophisticated lending risks. They use advanced analytics, historical data, and diversified portfolios.

- While direct peer-to-peer (P2P) lending between individuals is entirely possible, it remains highly risky due to potential, unprotected defaults where the individual lender bears 100% of the loss.

Inherent Risks in Lending

- Defaults in banking are complex and are not solely due to bad bank appraisals or borrower dishonesty.

- Even honest borrowers fail. Powerful external factors like severe market shifts, sudden economic recessions, intense competition, or sudden product obsolescence can fundamentally and unexpectedly destroy a borrower's repayment capacity.

Bank Lending Necessity

- Despite these daunting risks, banks strictly must lend to prevent deposited funds from remaining idle.

- Idle funds cost the bank money (because they still owe interest to depositors). Lending is the primary engine that actively generates income for the bank to survive and thrive.

Risk Management in Lending

- A core function of a bank's lending department is managing lending risks.

- Crucially, these risks can't be totally avoided, they can only be continuously monitored and managed.

- Critical management strategies include:

- Setting appropriate margins (demanding borrower contributions to projects).

- Accurate loan pricing (charging higher interest for higher risk).

- Broad diversification (not putting all eggs in one basket).

- Creating an optimized product mix to ensure lending overall remains consistently profitable despite isolated defaults.

Importance of Lending & Banking Evolution

- Lending represents the central, defining, and most critical function of modern banking.

- Professional bankers are rigorous subject matter experts, akin to highly skilled professionals like doctors and lawyers.

- Deep financial appraisal and ongoing client relationship management skills form the key components of effective banking execution.

- Banks have actively lent money for generations over centuries, meaning their deep institutional expertise has continually refined, tested, and optimized massive lending principles and practices over time.

The 5 Principles of Sound Lending

The basic, vital principles of sound lending fundamentally involve balancing safety, liquidity, and profitability, encompassing five core pillars that every banker must memorize:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Principles of Sound Lending

Introduction to Banking & Lending

Banking Basics

- Accept public deposits: Banks act as secure custodians of public funds. They accept deposits from individuals and businesses, creating a safe and reliable system for the public to park their money while earning interest.

- Provide loans: The fundamental economic role of a bank is extending credit. They lend the pooled public deposits for business, varied economic activities, and specialized investments.

- Act as financial intermediaries: Banks are the crucial bridge connecting the economy's vital parts: those with surplus funds (depositors who want to save) and those in need of funds (borrowers who need capital to grow or spend).

Types of Deposits

- Banks cater to diverse customer needs by offering funds in varied forms:

- Savings accounts: For everyday transactional needs with moderate interest.

- Current accounts: Used primarily by businesses for high-volume, unrestricted transactions (usually earning no interest).

- Fixed deposits (Term deposits): Locked-in funds for a specific period earning higher interest.

- Flexi deposits: A hybrid offering liquidity along with better interest rates.

- These varied choices depend directly on a depositor's individual needs for safety, income generation, and liquidity.

Depositor Preferences

- Depositors want guaranteed safety of their money above everything else. A bank's entire existence relies on this fundamental trust.

- They desire interest income on their idle money. Some prefer monthly payouts for steady cash flow, while others prefer to let the interest compound and reinvest.

- They deeply value robust transactional abilities: easy access to funds through issuing cheques, Net Banking, and widespread ATM card usage.

Central Bank's Role

- The Central Bank (like the RBI in India) strictly regulates overall banking operations to ensure banks don't take undue risks with public money.

- By setting strict guidelines, the central bank actively enhances and maintains public trust in banks.

- This strong regulatory framework successfully drives significant deposit inflow to banks by ensuring systemic stability across the financial ecosystem.

Banker's Responsibility & Obligations

- Maintain trust: A bank must continuously nurture a trusted and transparent relationship with every depositor.

- Effective utilization: The bank ensures these pooled funds are utilized effectively and safely by lending them prudently.

- Return on demand: Banks have an absolute obligation to return deposits when required unconditionally (based on the deposit type's terms).

- Owe interest: The bank owes and must transparently pay interest on the accepted deposits based on defined rates.

- Maintain Liquidity: To meet sudden and ongoing withdrawal requests, the bank needs to proactively maintain sufficient liquidity (ready cash or easily convertible assets) specifically for meeting repayment demands.

Effective Fund Management

- Managing bank funds is a tightrope walk. Money should be strictly balanced between three critical factors: being safe (minimizing default risk), liquid (available when depositors want it), and income-generating (earning enough to pay deposit interest and make a profit).

- Because of this delicate balance, the overwhelming focus of a bank remains on making loans and investments that are repaid reliably and consistently.

Bank's Primary Income

- A large portion of bank revenue—the core of its business model—stems from the net interest margin (interest earned on loans and advances minus interest paid on deposits).

- Therefore, there naturally lies a huge, existential importance on highly efficient and disciplined lending.

- Aside from loans, banks also actively invest surplus funds (like in government securities) for additional, stable income.

Challenges and Risks in Lending

Challenges in Lending

- Lending money inherently carries significant risks—chiefly, the risk that the borrower will not pay it back (credit risk).

- Individual lenders or private citizens generally lack the deep, necessary expertise for widespread lending and conducting highly accurate multi-variable risk assessments.

- Conversely, borrowers find it significantly easier, faster, and more standardized to approach established banks than attempting to source large funds from individual persons for required loans.

Banks vs. Peer-to-Peer Lending

- Banks are vastly better equipped and structurally designed to manage sophisticated lending risks. They use advanced analytics, historical data, and diversified portfolios.

- While direct peer-to-peer (P2P) lending between individuals is entirely possible, it remains highly risky due to potential, unprotected defaults where the individual lender bears 100% of the loss.

Inherent Risks in Lending

- Defaults in banking are complex and are not solely due to bad bank appraisals or borrower dishonesty.

- Even honest borrowers fail. Powerful external factors like severe market shifts, sudden economic recessions, intense competition, or sudden product obsolescence can fundamentally and unexpectedly destroy a borrower's repayment capacity.

Bank Lending Necessity

- Despite these daunting risks, banks strictly must lend to prevent deposited funds from remaining idle.

- Idle funds cost the bank money (because they still owe interest to depositors). Lending is the primary engine that actively generates income for the bank to survive and thrive.

Risk Management in Lending

- A core function of a bank's lending department is managing lending risks.

- Crucially, these risks can't be totally avoided, they can only be continuously monitored and managed.

- Critical management strategies include:

- Setting appropriate margins (demanding borrower contributions to projects).

- Accurate loan pricing (charging higher interest for higher risk).

- Broad diversification (not putting all eggs in one basket).

- Creating an optimized product mix to ensure lending overall remains consistently profitable despite isolated defaults.

Importance of Lending & Banking Evolution

- Lending represents the central, defining, and most critical function of modern banking.

- Professional bankers are rigorous subject matter experts, akin to highly skilled professionals like doctors and lawyers.

- Deep financial appraisal and ongoing client relationship management skills form the key components of effective banking execution.

- Banks have actively lent money for generations over centuries, meaning their deep institutional expertise has continually refined, tested, and optimized massive lending principles and practices over time.

The 5 Principles of Sound Lending

The basic, vital principles of sound lending fundamentally involve balancing safety, liquidity, and profitability, encompassing five core pillars that every banker must memorize:

- Safety

- Liquidity

- Profitability

- Purpose of Loan

- Diversification of Risk

1. Safety in Lending

Key principle: Always ensure funds are repaid exactly as agreed in the contract.

IMPORTANT

Safety is entirely considered the absolute primary principle of lending. If safety is compromised, the very survival of the bank is at stake.

Factors determining successful repayment naturally fall into two distinct buckets:

- Borrower's Capacity: The literal ability to pay. This means the operational success, steady cash flows, and fundamental financial viability of the borrower's enterprise or employment.

- Borrower's Willingness: The intention to pay. The character, track record, and fundamental integrity of the borrower directly determines their willingness to repay, even when times are tough.

Loan Application & Appraisal:

- Borrowers can either approach the bank directly needing funds, or be actively approached by the bank for a loan (proactive sales).

- The core purpose of a meticulous loan appraisal is to rigorously validate all facts presented by a loan applicant—never take information at face value.

- Professional appraisal checks explicitly encompass:

- Independently verifying facts and analyzing underlying business profitability and market realities.

- Assessing past financial performance (audited statements) and making grounded, realistic future income estimations.

- Evaluating overall collateral value to comfortably cover the loan exposure if the primary business completely fails.

Tools & Techniques for Appraisal:

- In modern banking, the safety of a credit proposal is measured objectively using data, not just gut feeling.

- Standard financial tools heavily utilized include: Cash Flow Analysis (tracking money in and out), NPV (Net Present Value) for long-term projects, Breakeven analysis (when a business turns profitable), and various crucial financial ratios.

- The analysis cautiously considers both business risks (which are systemic, numeric & measurable) and management risks (which focus on the leaders' competence and are more subjective).

External vs. Inherent Risks:

- Even if an enterprise is incredibly well-run by a genius team, it may eventually face unavoidable external challenges (e.g., a global pandemic or new government tariffs).

- Typically, external, uncontrollable risks make up an estimated 25-30% of total loan risks.

- However, properly and rigorously assessing the inherent, controllable risks gives the lender a solid 70% accurate baseline view of the overall credit risk.

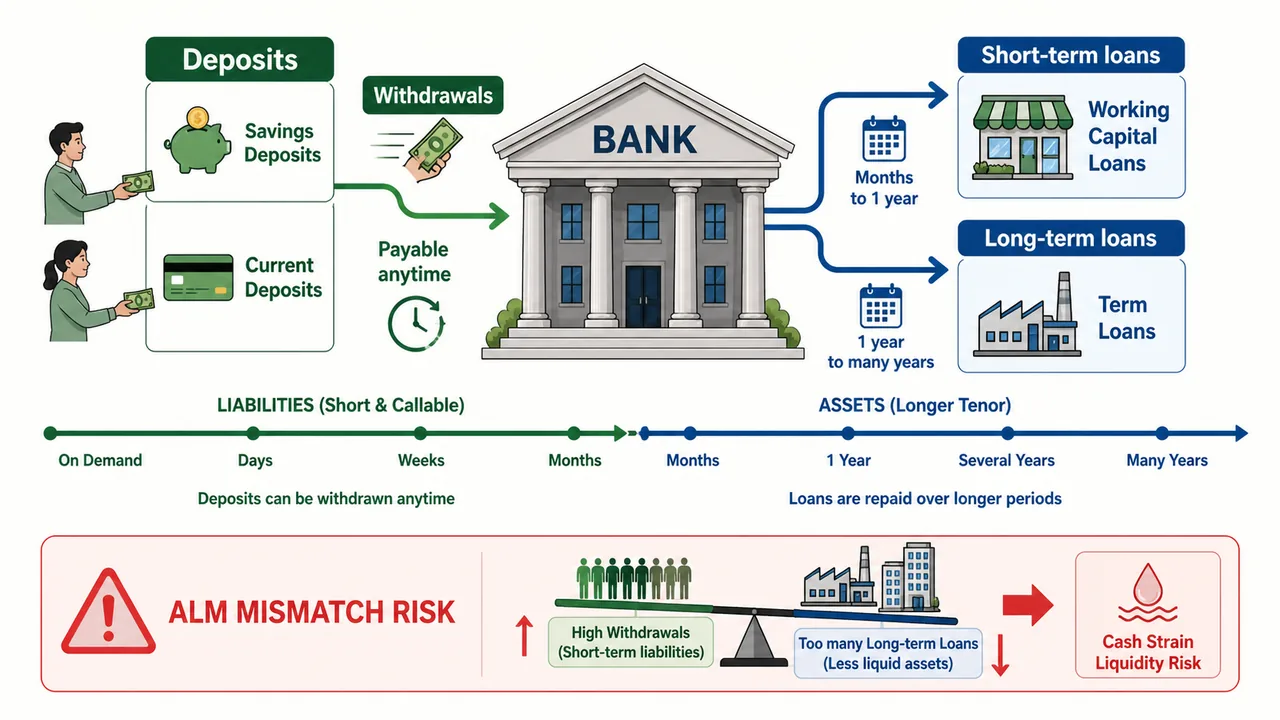

2. Liquidity

Liquidity in Commercial Banks:

- Commercial banks essentially operate as short-term lenders primarily due to their ongoing, massive need to frequently repay on-demand deposits.

- A massive portion of bank deposits, such as Current and Savings Accounts (CASA), are fundamentally volatile; they can be withdrawn or paid to others anytime without prior notice.

- If banks aggressively invest these highly volatile, short-term funds in very long-term, locked-in ventures (like 30-year mortgages without proper matching), they risk a fatal scenario: not having immediate liquidity (cash) for sudden, massive deposit withdrawals.

Liquidity Management:

- Banks face intense, continuous challenges in ensuring they proactively maintain liquidity to meet depositor commitments and daily transactional demands smoothly.

- To effectively and safely manage liquidity, banks often aggressively lend for working capital purposes (like inventory loans). These are technically short-term where repayment can technically be demanded at any time (payable on demand).

- Banks meticulously monitor their deposit portfolios' various maturities to preemptively prevent deep, dangerous liquidity mismatches.

- Loans are granted expecting punctual, timely cash repayments from the business's natural operations; otherwise, the bank proactively may have to painfully seize and sell charged assets.

- Assets provided strictly as primary security should fundamentally have strong, recognized marketable value and be easily, rapidly sellable to restore liquidity quickly.

- Collateral property security is very often taken merely as a backup net—it is highly illiquid and only used in case the primary security (like cash flow) falls materially short.

Asset Liability Management (ALM):

- In banking, managing liquidity while lending strictly means ensuring the banker does not face a severe Asset Liability Mismatch (ALM). (Assets = Loans; Liabilities = Deposits. Their timelines must generally match).

- The Central Bank (like the Reserve Bank of India) strongly requires commercial banks to rigorously monitor their structural liquidity regularly, day by day.

- Banks must dutifully submit a specific, detailed monthly statement to the regulator, meticulously detailing any liquidity mismatches over various short and long-time intervals.

- The ultimate, non-negotiable goal is to absolutely ensure dynamic, ongoing liquidity and prevent significant, dangerous mismatches that cause bank runs.

3. Profitability

- Commercial banks are not charities; they fundamentally aim to make strong profits for their shareholders.

- Therefore, the exact pricing of loans (setting the interest rate) is exceedingly vital for continuous, compounding profitability.

- Assigned interest rates heavily vary based on the specific loan type (home vs. personal) and the borrower's exact, calculated credit rating (like a CIBIL score).

WARNING

Crucially, banks can't lend below the Marginal Cost of funds based Lending rate (MCLR). This is a strict regulatory rule heavily enforced since April 2016 in India to ensure banks don't lend money cheaper than it costs them to acquire it, which guarantees losses.

- Naturally, high credit-rated, low-risk customers command and easily receive loans at measurably lower interest rates because they are "safe bets."

- Conversely, low credit-rated customers will likely be asked to pay notably higher "risk premium" interest, despite potentially offering very good physical security.

- Extreme caution, strict monitoring, and high compensating pricing is needed when deliberately lending to known high-risk borrowers.

- A critical, bottom-line indicator of a bank's total management effectiveness is whether deposits are raised at minimal costs (cheap CASA funds) and successfully lent out with adequate, safe margins.

- Proper, granular risk management in lending is strictly crucial for enduring, multi-generational banks.

- Accumulating massive amounts of unsatisfactory, non-performing loans (NPAs) can severely and permanently damage a bank's public reputation and shareholder value.

- Even simple, widespread delays or mild defaults on loans can drastically and negatively impact a bank's ultimate profitability due to required provisioning (setting aside profits to cover expected losses).

- Ultimately, the lending department's overall effectiveness ensures that distributed loans are demonstrably balancing being both safe and highly profitable.

4. Purpose of Loan

- Banks exclusively lend for heavily specific, documented reasons; they never disburse funds just on a raw, unspecified request for variable "cash."

- Disbursed funds must be used visibly and verifiably wisely for the stated purpose, not just arbitrarily or recklessly spent differently.

- Banks enthusiastically lend for productive purposes, such as active, daily working capital needs (buying raw materials) or necessary capital expenditure (buying new factory machinery) which actually generate the revenue to repay the loan.

CAUTION

Banks must strictly refrain from lending for speculative purposes (like gambling on the stock market or highly volatile real estate flipping). These activities are far too risky for depositors' money.

- The Central Bank has strict, established rules on firmly prohibited lending sectors depending on national economic policies.

- Banks readily and aggressively provide personal loans specifically for tangible assets: medical emergencies, education degrees, travel, vehicles, and housing loans. These are broadly grouped and massive known as retail loans.

- Modern technology advancements and data analytics have drastically streamlined processing and makes retail loans easier and faster to deploy in high volumes.

- Banks, often driven by government mandates, importantly also deeply support the crucial agriculture and MSME (Micro, Small and Medium Enterprises) sectors with highly specialized, often subsidized loans.

5. Diversification of Risk

- The absolute significance of wide diversification everywhere in lending is simple: it minimizes the total catastrophic risk to the entire loan portfolio.

Why Diversification Matters (The 'Eggs in One Basket' Rule)

If a bank lends 80% of its money to the local real estate sector, and the housing market crashes, the bank will likely fail. By spreading loans across real estate, agriculture, retail, software, and manufacturing, a crash in one sector only impacts a small, manageable portion of the bank's total profits.- Banks should strictly and consciously avoid lending exclusively to only one sector due to the deadly risk of concentration: they intentionally do not focus exclusively on one giant borrower, one specific purpose, or one tight geographic location.

- Any single industry may be predictably subject to massive, volatile fluctuations due to deep business cycles (boom and bust periods), massively affecting local loan repayment abilities.

- Sharp, sudden raw material price fluctuations and wild, unexpected political disturbances can ruinously impact specific niche businesses overnight.

- Unpredictable natural calamities (floods, earthquakes) can entirely halt normal business operations in a specific geographic zone.

- Massive, unavoidable global issues, exactly like the sweeping 2008 financial crisis, showcase the terrifying, rapid ripple effect across deeply interconnected global sectors.

- Therefore, banks should relentlessly and systematically maintain a vastly varied business mix in their loan book, stringently avoiding any single-sector or single-borrower focus.

- Sector-wise lending limits are strictly stipulated by risk departments to manage hard total exposure for highly volatile sectors like: steel, textiles, commercial real estate, pharmaceuticals, etc.

- Explicit, non-negotiable caps are proactively established on total individual borrow limits and wider corporate group borrowings to prevent giant domino-effect collapses.

- Funds are methodically, strategically allocated for broad corporate syndicates, vital national priority sectors, and countless consumer retail loans.

- Ultimately, spreading the lending risk widely across dozens of industries and totally different, unrelated borrower types ensures a vastly safer, resilient, and profitable long-term loan portfolio.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Role of banks | Accept public deposits, provide loans, act as financial intermediaries between surplus (depositors) and deficit (borrowers) units |

| Types of deposits | Savings (moderate interest), Current (no interest, business use), Fixed/Term (locked-in, higher interest), Flexi (hybrid liquidity + interest) |

| Depositor preferences | Safety of funds (paramount), interest income, and liquidity (easy access via cheques, ATMs, net banking) |

| Central Bank's role | RBI regulates banking operations, enhances public trust, ensures systemic stability, drives deposit inflow |

| Banker's obligations | Maintain trust, utilize funds effectively, return deposits on demand, pay interest, maintain liquidity |

| Bank's primary income | Net interest margin (interest earned on loans minus interest paid on deposits); also income from investments in govt securities |

| Credit risk | Risk that the borrower will not repay; even honest borrowers may fail due to external factors (recession, competition, obsolescence) |

| Why banks must lend | Idle funds cost money (interest owed to depositors); lending is the primary income engine |

| Risk management strategies | Setting appropriate margins, accurate loan pricing, broad diversification, optimized product mix |

| 5 Principles of Sound Lending | (1) Safety, (2) Liquidity, (3) Profitability, (4) Purpose of Loan, (5) Diversification of Risk |

| 1. Safety (primary principle) | Ensure funds are repaid as agreed; assessed via borrower's capacity (ability to pay) and willingness (character/integrity) |

| Loan appraisal tools | Cash Flow Analysis, NPV, Breakeven analysis, financial ratios; considers both business risks and management risks |

| External vs. inherent risks | External (uncontrollable) risks = 25-30% of total; inherent (assessable) risks give ~70% accurate baseline view |

| 2. Liquidity | Banks are short-term lenders; CASA deposits are volatile and withdrawable anytime; must avoid Asset Liability Mismatch (ALM) |

| ALM monitoring | Banks submit monthly structural liquidity statement to RBI; goal is to prevent dangerous mismatches causing bank runs |

| Primary vs. collateral security | Primary security should be easily marketable; collateral (e.g., property) is a backup net and highly illiquid |

| 3. Profitability | Loan pricing varies by loan type and credit rating; banks cannot lend below MCLR (since April 2016) |

| MCLR | Marginal Cost of funds based Lending Rate — regulatory floor ensuring banks don't lend cheaper than their cost of funds |

| NPAs and profitability | Non-performing assets damage reputation and shareholder value; even mild delays require provisioning (setting aside profits) |

| 4. Purpose of loan | Banks lend only for specific, documented, productive purposes (working capital, capex); speculative lending is prohibited |

| Retail loans | Personal loans for medical, education, travel, vehicles, housing; technology has streamlined high-volume retail lending |

| Priority sectors | Banks support agriculture and MSME sectors with specialized, often subsidized loans (govt mandated) |

| 5. Diversification of risk | Spread loans across multiple sectors, borrowers, geographies to minimize catastrophic portfolio risk |

| Concentration risk | Avoid lending exclusively to one sector, one giant borrower, or one geographic location |

| Sector-wise lending limits | Strict caps set by risk departments on volatile sectors (steel, textiles, real estate, pharma); caps on individual and group borrowings |

Lesson Doubts

Ask questions, get expert answers