🔮 RBI 2026 IRAC Directions — ECL Framework

RBI 2026 overhaul of IRAC norms — Expected Credit Loss (ECL) model, three-stage classification, EIR method, IT automation, and transition arrangements. Effective April 1, 2026.

RBI 2026 IRAC Directions — ECL Framework

Background & Source: On April 27, 2026, the RBI issued the new (Commercial Banks – Asset Classification, Provisioning and Income Recognition) Directions, 2026, completely overhauling the IRAC framework and replacing the 2025 norms (effective April 1, 2027). The most significant shift is the transition from the traditional incurred loss model to a forward-looking Expected Credit Loss (ECL) model.

Distinction from the 2019 Framework: It is critical to distinguish these 2026 ECL Directions from the June 7, 2019 Circular ("Prudential Framework for Resolution of Stressed Assets"). While the 2019 framework overhauled the identification and resolution of early stress (e.g., introducing SMA classifications), it retained the legacy "Incurred Loss" methodology for provisioning. By contrast, the April 2026 ECL Directions fundamentally alter the underlying mathematical framework that banks must use to calculate and hold provisions against those assets. (Similar ECL amendment directions were also issued simultaneously for RRBs, UCBs, NBFCs, and SFBs).

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

RBI 2026 IRAC Directions — ECL Framework

Background & Source: On April 27, 2026, the RBI issued the new (Commercial Banks – Asset Classification, Provisioning and Income Recognition) Directions, 2026, completely overhauling the IRAC framework and replacing the 2025 norms (effective April 1, 2027). The most significant shift is the transition from the traditional incurred loss model to a forward-looking Expected Credit Loss (ECL) model.

Distinction from the 2019 Framework: It is critical to distinguish these 2026 ECL Directions from the June 7, 2019 Circular ("Prudential Framework for Resolution of Stressed Assets"). While the 2019 framework overhauled the identification and resolution of early stress (e.g., introducing SMA classifications), it retained the legacy "Incurred Loss" methodology for provisioning. By contrast, the April 2026 ECL Directions fundamentally alter the underlying mathematical framework that banks must use to calculate and hold provisions against those assets. (Similar ECL amendment directions were also issued simultaneously for RRBs, UCBs, NBFCs, and SFBs).

Why the Change — Incurred Loss vs ECL

The Old System: Incurred Loss Model

Under the old incurred-loss model, a bank waited until a loan actually went bad — only then did it book a provision. The logic was conservative: don't recognize a loss until it is "incurred."

The flaw: By the time a loan hits NPA, the damage has already spread and the P&L takes a sudden, large hit. The bank had made no gradual provision during the years the loan was quietly deteriorating. This makes banks look artificially healthy during good times and artificially sick during downturns.

The New System: ECL Model

ECL fixes this by shifting the question from "has a loss occurred?" to "what is the expected loss from today?"

Provisioning now happens before default, based on probability-weighted forward-looking analysis. Buffers are built during good times — not just when loans sour.

The ECL Formula

| Term | Stands For | Meaning |

|---|---|---|

| PD | Probability of Default | Likelihood the borrower fails to pay |

| LGD | Loss Given Default | % of exposure lost if default happens (after recovery from security) |

| EAD | Exposure at Default | Total outstanding amount at the time of default |

Example: Loan of ₹100. PD = 10%, LGD = 60%, EAD = ₹100. ECL = 0.10 × 0.60 × 100 = ₹6 provision today, even though no default has occurred yet.

ECL is probability-weighted across multiple economic scenarios (base case, optimistic, stressed). Banks must think: "what if a drought hits?" and weight those outcomes by their likelihood. This makes provisioning forward-looking and countercyclical — buffers built in good times absorb stress in bad times.

Three-Stage Asset Classification

All financial assets now get an ECL stage based on how much credit risk has changed since the loan was originated:

Stage 1: Performing (No significant increase in credit risk)

- Condition: The loan is healthy. There has been no significant increase in credit risk (SICR) since the loan was given.

- Provisioning Basis: 12-month ECL. The bank asks, "What is the probability of default in the next 12 months?" and provisions for that expected loss.

Stage 2: Under-Performing (Significant increase in credit risk)

- Condition: There has been a significant increase in credit risk, but the borrower has not yet defaulted.

- Provisioning Basis: Lifetime ECL. Because the risk has increased, the bank must now calculate the probability of default over the entire remaining life of the loan.

- Crucial Note: "Lifetime ECL" does not mean provisioning 100% of the loan. It just refers to the timeframe of the probability calculation. For example, if a ₹100 Cr loan has 10 years left, a 5% lifetime probability of default, and a 40% Loss Given Default (LGD), the provision is just 5% × 40% × ₹100 Cr = ₹2 Crore, not the full ₹100 Cr.

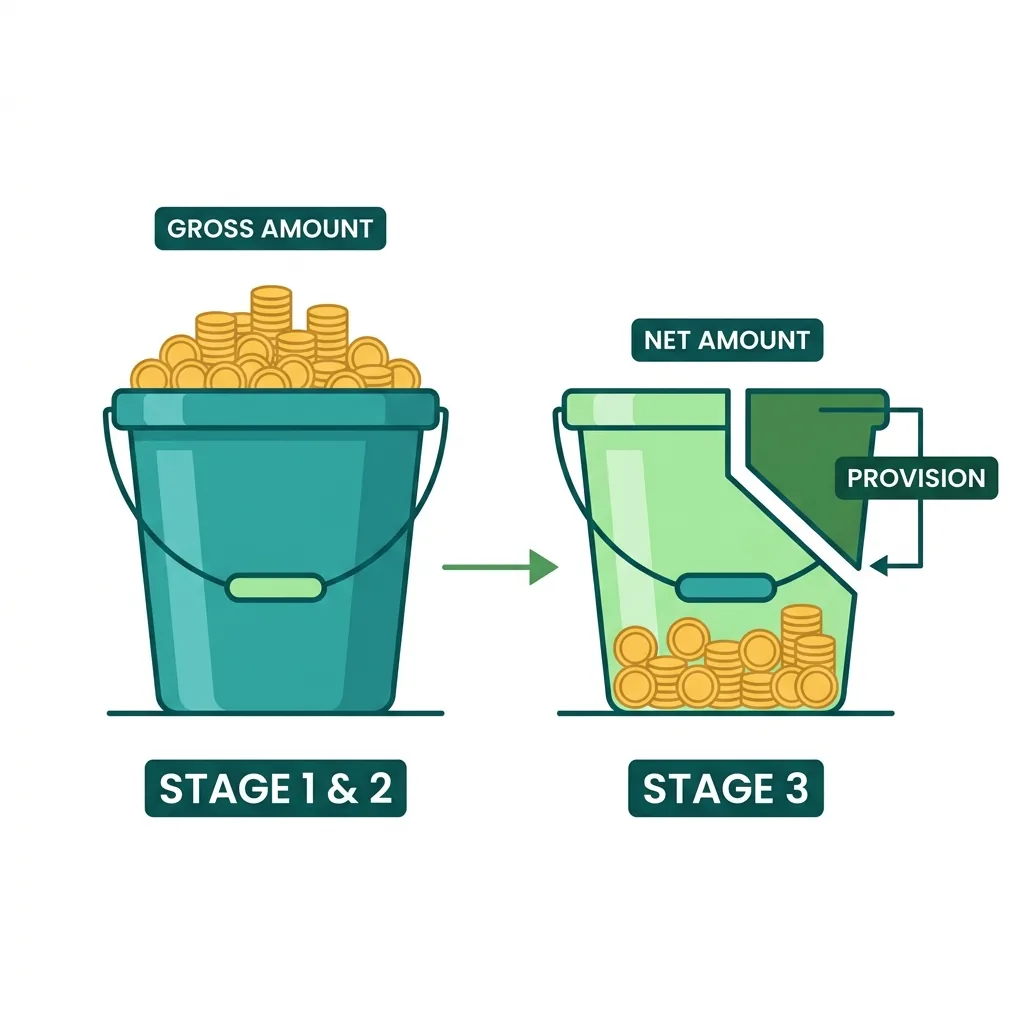

Stage 3: Non-Performing / Credit-Impaired (NPA)

- Condition: The borrower has defaulted. The loan is an NPA.

- Provisioning Basis: Lifetime ECL. Because default has already occurred, the Probability of Default (PD) is mathematically 100% (or 1.0). Therefore, the exact provision percentage is driven entirely by the Loss Given Default (LGD) — i.e., how much the bank actually expects to lose after selling off any collateral. Additionally, interest income can now only be calculated on the net carrying amount (Gross balance minus the ECL provision).

Stage 2 — The Key Innovation

Under the old model, a rating drop from BBB to BB attracted zero extra provision (the loan hadn't defaulted yet). Under ECL, the same rating drop triggers Stage 2 — and the bank must now provision for the entire remaining life of that loan.

This is the biggest practical change: deteriorating-but-still-performing loans now carry a much larger provisioning burden.

What Triggers SICR (Significant Increase in Credit Risk)?

A loan moves from Stage 1 to Stage 2 when any of these occur:

- Credit spread widening

- CDS (Credit Default Swap) price increase

- External or internal rating downgrade

- Delisting threat

- Deterioration in financial instruments

SICR Exemptions — Not Required For:

- SLR-eligible investments

- Direct Central Government claims

- Central Government-guaranteed exposures

- Zero-risk-weight foreign sovereigns / MDBs / BIS / IMF

NPA Rules — Retained with Clarifications

The 90-day NPA rule is unchanged. RBI has kept the existing NPA framework but added explicit clarifications:

| Clarification | Rule |

|---|---|

| Borrower-level classification | If one facility = NPA, all facilities to that borrower = NPA |

| Co-lending (CLA) | If either lender classifies as SMA/NPA, same applies to the other lender |

| Credit cards | Minimum Amount Due not paid within 90 days = NPA |

| Partial Credit Enhancement | Outstanding for 90 days or more = NPA |

| LC bills | Not accepted on presentation — NPA from the date other facilities were classified NPA |

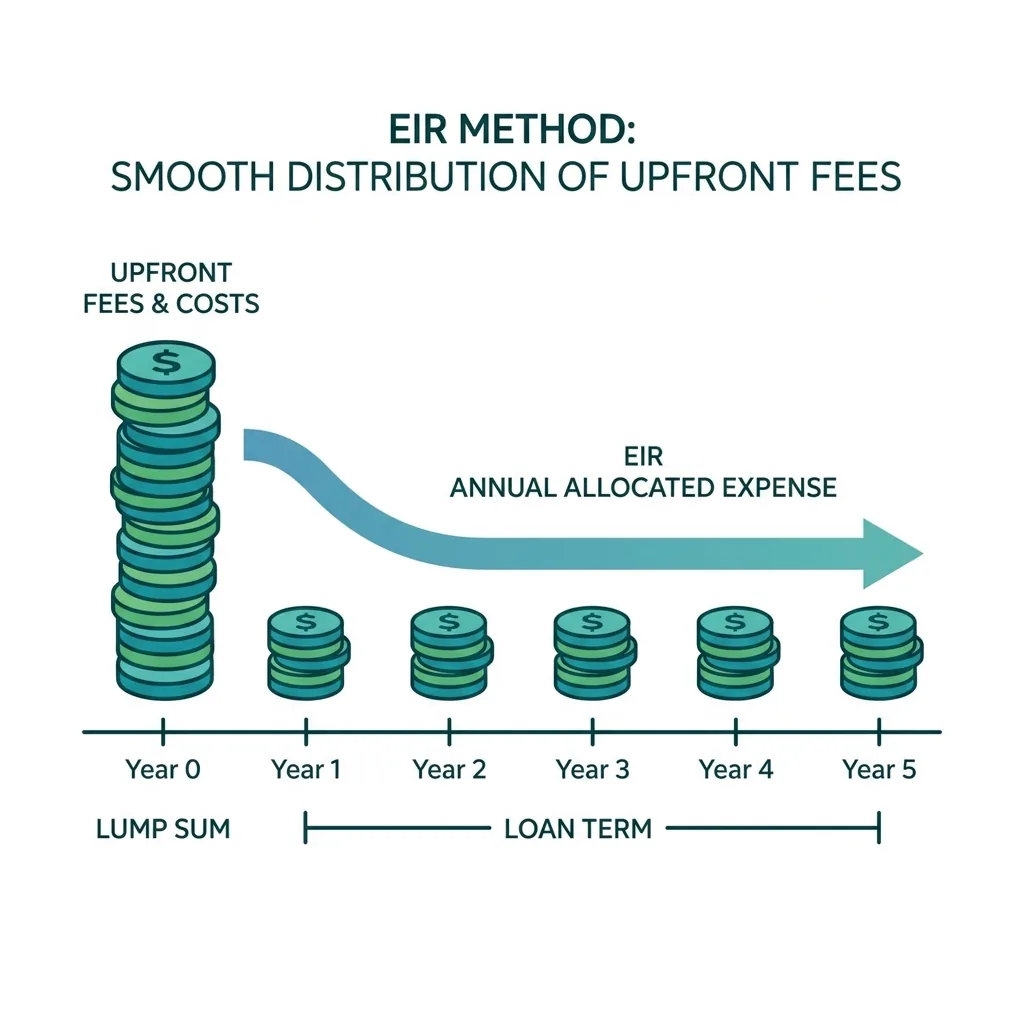

Effective Interest Rate (EIR) Method

Income recognition shifts from the contractual rate to the EIR method. EIR spreads all fees, transaction costs, and discounts over the life of the loan — giving a more accurate picture of true interest income.

- Loans originated from April 1, 2027 → Must use EIR from day one.

- Legacy loans → May use the simple contractual rate (the rate written on the loan agreement) temporarily.

- Full migration to EIR by March 31, 2030 → All old legacy loans must switch to the EIR method by this mandatory deadline.

- Stage 1 and Stage 2 assets → Interest income is calculated on the gross carrying amount. (Because these loans are healthy or only slightly stressed, the bank calculates interest on the full loan balance since they reasonably expect to collect it all.)

- Stage 3 assets → Interest income is calculated on the net carrying amount (Gross minus the ECL provision). (Since these loans are defaulted NPAs, calculating interest on the full amount would artificially inflate profits with money they will never see. Banks must calculate interest only on the realistic portion they actually expect to recover.)

Mandatory IT Automation

RBI has ended the era of manual NPA classification adjustments:

- All borrowal accounts must be covered under an automated IT system

- NPA downgrade AND upgrade must happen via Straight Through Process (STP) — zero manual intervention

- Backend data changes are banned — all changes must flow through the front-end system only

This prevents banks from quietly adjusting classifications to avoid NPA recognition — a common regulatory evasion tactic.

Transition Arrangements (Capital Relief)

The shift from incurred-loss to ECL will change provision levels for most banks. RBI has built in transitional relief:

| Scenario | Treatment |

|---|---|

| ECL provisioning > old provisions | Phased capital relief over transition years |

| ECL < old provisions | Surplus adjusted in retained earnings as on April 1, 2027 (not via P&L) |

| Accounts classified NPA as on March 31, 2027 | Not upgraded solely due to new Directions |

The "surplus into retained earnings" rule prevents banks from booking a profit windfall when ECL is lower than their existing provisions. The surplus is locked in equity — not distributed.

What This Means in Practice

| Old System | New System |

|---|---|

| Provision after default (incurred) | Provision before default (expected) |

| Binary: Standard or NPA | Three stages with gradual build-up |

| Point-in-time credit assessment | Through-the-cycle, multi-scenario modelling |

| Manual NPA classification adjustments possible | STP-only, no backend changes |

| Contractual interest rate for income recognition | EIR method |

| Sudden P&L hit when loan goes NPA | Gradual provisioning — smoother P&L |

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Directions Issued | April 27, 2026 |

| Effective Date | April 1, 2027 |

| Replaces | 2025 IRAC Directions |

| Key Shift | Incurred loss → Expected Credit Loss (ECL) |

| ECL Formula | PD × LGD × EAD |

| Stage 1 | No SICR → 12-month ECL |

| Stage 2 | SICR triggered → Lifetime ECL |

| Stage 3 | Credit-impaired / NPA → Lifetime ECL (full) |

| Stage 2 Key Point | Rating drop (still performing) → full lifetime provision required |

| SICR Triggers | Credit spread widening, CDS price increase, rating downgrade, delisting threat, financial deterioration |

| SICR Exemptions | SLR investments, direct Central Govt claims, Central Govt-guaranteed, zero-risk-weight foreign sovereigns / MDBs / BIS / IMF |

| 90-day NPA Rule | Unchanged |

| Borrower-Level Classification | One facility NPA = all facilities to that borrower NPA |

| Co-lending (CLA) | If either lender classifies as SMA/NPA → same applies to the other |

| Credit Card NPA | Minimum Amount Due not paid within 90 days |

| EIR Method | Full migration mandatory by March 31, 2030 |

| Stage 1/2 Income | On gross carrying amount |

| Stage 3 Income | On net carrying amount |

| IT Automation | All accounts — STP only, no backend changes |

| ECL > Old Provisions | Phased capital relief |

| ECL < Old Provisions | Surplus to retained earnings (not P&L) |

| NPA on 31.03.2027 | Not upgraded solely due to new directions |

| Scope | Commercial banks + 13 amendment directions for RRBs, UCBs, NBFCs, AIFIs, SFBs, cooperatives |

Lesson Doubts

Ask questions, get expert answers