💱 Exchange Rates

Understanding foreign exchange rates - direct, indirect, buying, selling, spot and forward rates

What is Exchange Rate?

Exchange Rate is the rate at which one currency is exchanged for another.

- Example: 1 USD = ₹89.52

This means to buy 1 US Dollar, you need to pay ₹89.52 in Indian Rupees.

Variants of Exchange Rates

There are several types of exchange rates based on different factors:

| Variant Type | Description |

|---|---|

| Direct or Indirect Rate | How the rate is quoted (home vs foreign currency) |

| Buying or Selling Rate | Whether bank is buying or selling FC |

| Spot or Forward Rate | When the transaction will be settled |

Value Date

- The actual date of delivery of currencies/funds under a sale or purchase contract

- Also called settlement date

- This is when the actual exchange of currencies takes place

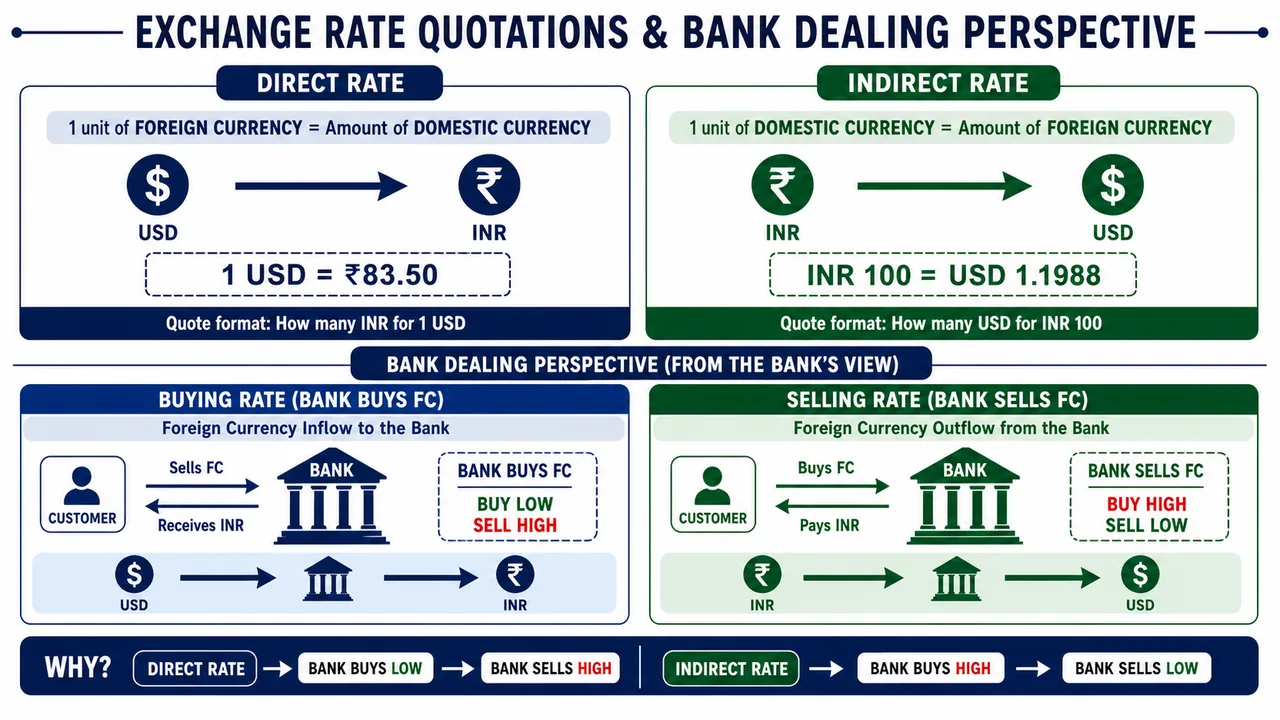

Direct Rate vs Indirect Rate

Direct Rate

- Quoted as fixed unit of Foreign Currency (FC) and variable units of Home Currency

- OR: Domestic currency per unit of foreign currency

- Example: 1 USD = ₹89.52 (or ₹89.70)

- In India, direct rate is used for most of currencies

- Maxim: Buy Low, Sell High

Indirect Rate

- Quoted as fixed unit of Home Currency and variable units of Foreign Currency

- OR: Foreign currency per unit of home currency

- Example: ₹100 = USD 1.12 (or 1.11)

- Maxim: Buy High, Sell Low

- Used for JPY, Lira, Indonesian Rupiah etc.

| Feature | Direct Rate | Indirect Rate |

|---|---|---|

| Fixed Unit | Foreign Currency | Home Currency |

| Variable Unit | Home Currency | Foreign Currency |

| Example | 1 USD = ₹89.52 | ₹100 = USD 1.12 |

| Maxim | Buy Low, Sell High | Buy High, Sell Low |

| Used for | Most currencies | JPY, Lira, Rupiah |

Buying Rate vs Selling Rate

These are from the perspective of the bank.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

What is Exchange Rate?

Exchange Rate is the rate at which one currency is exchanged for another.

- Example: 1 USD = ₹89.52

This means to buy 1 US Dollar, you need to pay ₹89.52 in Indian Rupees.

Variants of Exchange Rates

There are several types of exchange rates based on different factors:

| Variant Type | Description |

|---|---|

| Direct or Indirect Rate | How the rate is quoted (home vs foreign currency) |

| Buying or Selling Rate | Whether bank is buying or selling FC |

| Spot or Forward Rate | When the transaction will be settled |

Value Date

- The actual date of delivery of currencies/funds under a sale or purchase contract

- Also called settlement date

- This is when the actual exchange of currencies takes place

Direct Rate vs Indirect Rate

Direct Rate

- Quoted as fixed unit of Foreign Currency (FC) and variable units of Home Currency

- OR: Domestic currency per unit of foreign currency

- Example: 1 USD = ₹89.52 (or ₹89.70)

- In India, direct rate is used for most of currencies

- Maxim: Buy Low, Sell High

Indirect Rate

- Quoted as fixed unit of Home Currency and variable units of Foreign Currency

- OR: Foreign currency per unit of home currency

- Example: ₹100 = USD 1.12 (or 1.11)

- Maxim: Buy High, Sell Low

- Used for JPY, Lira, Indonesian Rupiah etc.

| Feature | Direct Rate | Indirect Rate |

|---|---|---|

| Fixed Unit | Foreign Currency | Home Currency |

| Variable Unit | Home Currency | Foreign Currency |

| Example | 1 USD = ₹89.52 | ₹100 = USD 1.12 |

| Maxim | Buy Low, Sell High | Buy High, Sell Low |

| Used for | Most currencies | JPY, Lira, Rupiah |

Buying Rate vs Selling Rate

These are from the perspective of the bank.

Buying Rate

- Used for inflow of FC (bank receives FC - delivers INR)

- Bank is the buyer of foreign currency

- Example: Purchase of FC export bill or cancellation of FC DD issued by bank

- Customer sells FC → Bank buys FC → Bank pays customer in INR

Selling Rate

- Used for outflow of FC (bank delivers FC - receives INR)

- Bank is the seller of foreign currency

- Example: Issue of FC DD to customer or payment of FC import bill on behalf of an importer

- Customer buys FC → Bank sells FC → Customer pays bank in INR

Spread or Margin

- The difference between buying rate and selling rate

- Also known as trading margin

- This is the bank's profit on forex transactions

- Formula: Spread = Selling Rate - Buying Rate

Fixed Rate vs Floating Rate

Fixed Rate

- Fixed by Monetary Authority (Central Bank)

- Pegged to one or more currencies

- Exchange rate remains constant unless government changes it

Floating Rate

- India adopted in 1993

- Value decided by demand and supply in the market

- Also called market-determined exchange rate

- RBI may intervene to manage volatility (managed float)

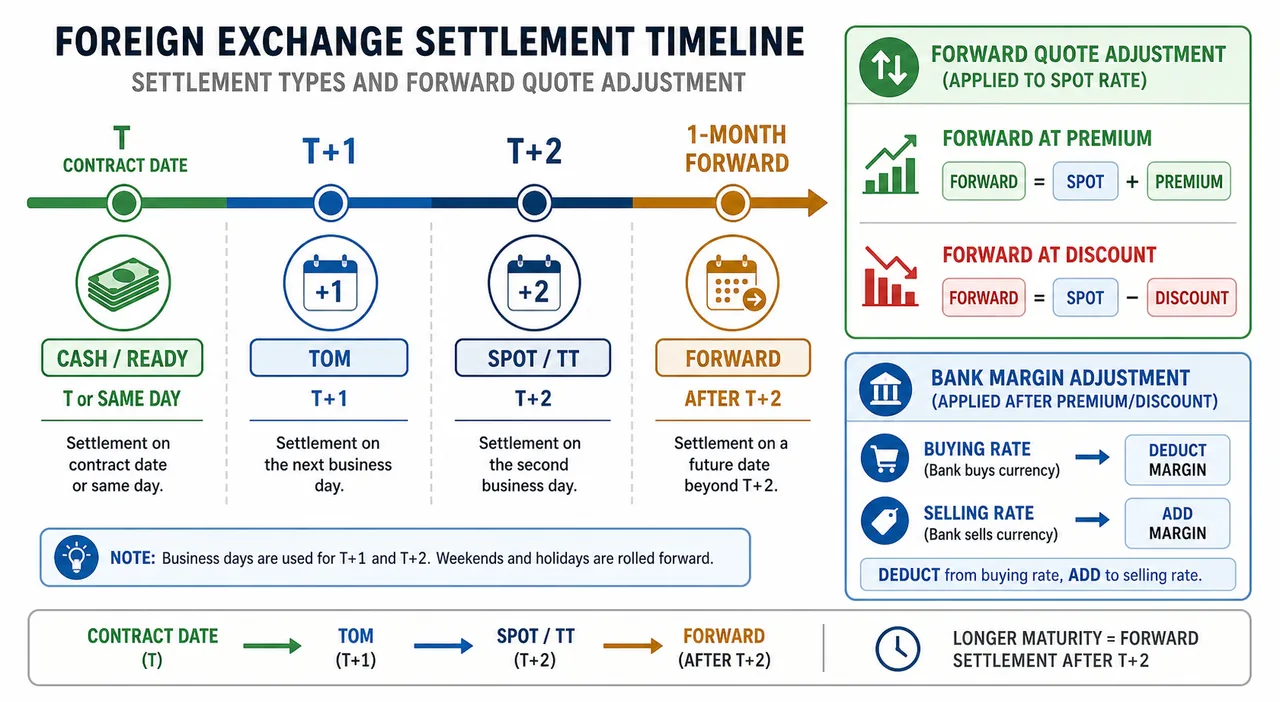

Spot Rate vs Forward Rate

Spot Rate

- Used for spot transactions (settled in T + 2 working days i.e. next two working days)

- Also called TT Rate (Telegraphic Transfer Rate)

| Settlement Type | Description | Example |

|---|---|---|

| Same day (T-0) | Cash or Ready rate | Contract: Jan 12 (Fri) → Delivery: Jan 12 |

| T+1 day | Tom rate (Tomorrow) | Contract: Jan 12 (Fri) → Delivery: Jan 15 (Mon) |

| T+2 days | Spot or TT rate | Contract: Jan 12 (Fri) → Delivery: Jan 16 (Tue) |

Forward Rate

- Used for forward transactions (after T+2 working days)

- Agreed today for delivery on a future date

Forward Rate Scenarios:

| Scenario | Condition | Action |

|---|---|---|

| Forward @ Premium | Future rate > Spot rate | Premium added to spot rate |

| Forward @ Discount | Spot rate > Future rate | Discount deducted from spot rate |

Bank Margin Adjustment:

- Deduct from buying rate AND add to selling rate

- Applied after adjusting premium or discount

📝 Example: Bank Margin Calculation

Given:

- Spot rate: 1 USD = ₹84.00 / 84.20 (Bid/Offer)

- Forward premium (1 month): 20 paise

- Bank margin: 5 paise

Step 1: Adjust for Premium/Discount

| Rate Type | Spot Rate | + Premium | After Premium |

|---|---|---|---|

| Buying (Bid) | ₹84.00 | + 0.20 | ₹84.20 |

| Selling (Offer) | ₹84.20 | + 0.20 | ₹84.40 |

Step 2: Apply Bank Margin (AFTER premium)

| Rate Type | After Premium | Margin Adjustment | Final Rate |

|---|---|---|---|

| Buying | ₹84.20 | - 0.05 (deduct) | ₹84.15 |

| Selling | ₹84.40 | + 0.05 (add) | ₹84.45 |

Final Forward Rates:

- Bank's Buying Rate: ₹84.15 per USD

- Bank's Selling Rate: ₹84.45 per USD

- Bank's Spread: ₹0.30 (84.45 - 84.15)

Key Memory Point: Margin always works in bank's favor - they buy cheaper (deduct) and sell higher (add)

Bid/Offer Rates

Inter-bank market rates are quoted as:

1 USD = ₹89.10 / 89.20

- 1st part (₹89.10) = Bid Rate (bank's rate to buy)

- 2nd part (₹89.20) = Offer Rate (bank's rate to sell)

Cross Rates

When rate between 2 currencies is not directly given/available, it is calculated through a 3rd common currency.

Also called Chain Rule method.

Examples:

Example 1: Euro to Rupee

- Euro/USD rate: 1 Euro = 1.18 USD

- USD/Rupee rate: 1 USD = ₹89.20

- Euro-Rupee rate = 1.18 × 89.20 = ₹105.56

Example 2: INR to Yen

- USD/JPY rate = 156.43 (JPY quoted per 100 units)

- USD/INR = 89.20

- INR/JPY = (89.20 / 156.43) × 100 = ₹57.02 per 100 Yen

FC Rates for Specific Transactions

Understanding which rate to apply depends on two factors:

- Is the bank buying or selling FC? (Bank's perspective)

- Is there a bill/document involved? (TT vs Bills rate)

Key Rule: Bank always profits - uses lower rate when buying FC, higher rate when selling FC

| Sr. | Transaction | Rate to Apply |

|---|---|---|

| 1 | Issue of FC DD | TT Selling rate |

| 2 | Cancellation of FC DD issued by bank | TT Buying rate |

| 3 | Encashment of FC DD | TT Buying rate |

| 4 | Purchase of FC export bill from exporter | Bills Buying rate |

| 5 | Reversal of dishonoured FC export bill | TT Selling rate |

| 6 | Crystallization of overdue FC export bill | TT Selling rate |

| 7 | Payment of FC import bill | Bills Selling rate |

| 8 | Crystallization of overdue FC import bill under LC | Bills Selling rate |

| 9 | Transfer of funds from FCNR to NRE | TT Buying rate |

| 10 | Transfer of funds from NRE to FCNR | TT Selling rate |

| 11 | Payment in INR after credit of FC in NOSTRO a/c | TT Buying rate |

| 12 | Receipt of FC in NOSTRO a/c after payment in Rupee | Bills Buying rate |

Explanation of Each Transaction

📝 Click to see detailed explanations

1. Issue of FC DD → TT Selling rate

- Customer wants FC (in form of DD), bank is selling FC

- No bill involved, so TT rate applies

2. Cancellation of FC DD issued by bank → TT Buying rate

- Bank takes back the FC DD, effectively buying back FC from customer

- Customer gets INR refund

3. Encashment of FC DD → TT Buying rate

- Customer brings FC DD, wants INR

- Bank is receiving FC = buying FC from customer

4. Purchase of FC export bill from exporter → Bills Buying rate

- Exporter has FC bill (document), sells to bank

- Bank is buying FC + bill handling = Bills Buying rate

5. Reversal of dishonoured FC export bill → TT Selling rate

- Original transaction was bills buying (bank bought FC)

- Dishonour means bank reverses = selling FC back to exporter

- No bill now (it's been dishonoured), so TT rate

6. Crystallization of overdue FC export bill → TT Selling rate

- Export bill was sent abroad but became overdue/unpaid

- Bill is no longer valid (failed abroad) - no documents in hand

- Bank debits exporter's account = selling FC to exporter

- TT rate because no active bill transaction exists now

7. Payment of FC import bill → Bills Selling rate

- Importer needs to pay in FC

- Bank is selling FC to importer + bill handling

8. Crystallization of overdue FC import bill under LC → Bills Selling rate

- Import bill under LC became overdue

- Bank still holds the shipping documents (LC means bank is holding docs)

- Bank crystallizes = selling FC to importer against those documents

- Bills rate because documents are still with the bank (bill transaction continues)

9. Transfer from FCNR to NRE → TT Buying rate

- Converting FC (FCNR) to INR (NRE)

- Bank is receiving FC from customer = buying FC

- No bill, so TT rate

10. Transfer from NRE to FCNR → TT Selling rate

- Converting INR (NRE) to FC (FCNR)

- Bank is giving FC to customer = selling FC

11. Payment in INR after credit of FC in NOSTRO a/c → TT Buying rate

- Bank already received FC in its NOSTRO account

- Now paying INR to customer = bank bought FC

- TT rate (telegraphic transfer)

12. Receipt of FC in NOSTRO a/c after payment in Rupee → Bills Buying rate

- Bank paid INR first, FC credited later

- Bank is buying FC with documentation delay

- Bills rate for the handling

Foreign Currency Positions

FC Position

- FC position = Amount payable or receivable in FC

- Position can be closed or open

Closed Position

- Matched position (sale = purchase)

- No risk position

Open Position

- Mismatched position (sale ≠ purchase) → Risk position

- Position limit fixed by Board of Directors and reported to RBI

- Sale > Purchase = Short position

- Purchase > Sale = Long position

Effect of Rate Change

| Position | Rate Increases | Rate Decreases |

|---|---|---|

| Long (purchase > sale) | Gain ✅ | Loss ❌ |

| Short (sale > purchase) | Loss ❌ | Gain ✅ |

Day Light vs Overnight Position

- Day light position = Balance during day time (higher balance allowed)

- Overnight position = Balance at close of day (lower balance limit)

Swap

- Exchange of FC flows relating to different value dates between two parties

- Swap involves 2 transactions simultaneously:

- Combination of spot and forward

- Combination of 2 forwards

- These are in opposite direction

Example:

- Sale of FC spot @ 1 USD = ₹89.15

- AND simultaneous purchase of FC 2 month forward @ 1 USD = ₹89.75

- (or vice-versa)

Objective: To cover the forex fluctuation risk

Arbitrage

- Practice of taking advantage of price difference in FC rates between 2 or more markets

- Example: Purchase of FC in one market (where rate is lower) and simultaneous sale of same currency in another market (where rate is higher)

- Objective: To make profit due to rate difference in two markets

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Exchange Rate | Rate at which one currency is exchanged for another |

| Value Date | Actual date of delivery (settlement date) |

| Direct Rate | Fixed FC, variable home currency (Buy Low, Sell High) |

| Indirect Rate | Fixed home currency, variable FC (Buy High, Sell Low) |

| India Uses | Direct rate for most currencies |

| Indirect Rate For | JPY, Lira, Indonesian Rupiah |

| Buying Rate | FC inflow (bank receives FC, pays INR) |

| Selling Rate | FC outflow (bank delivers FC, receives INR) |

| Spread/Margin | Difference between buying and selling rate |

| Fixed Rate | Set by Monetary Authority, pegged to currency |

| Floating Rate | India adopted 1993, demand/supply driven |

| Spot Rate (T+2) | Settled in 2 working days (TT rate) |

| Cash Rate (T-0) | Same day settlement (Ready rate) |

| Tom Rate (T+1) | Next day settlement |

| Forward Rate | Settlement after T+2 days |

| Forward @ Premium | Future rate > Spot rate (add premium) |

| Forward @ Discount | Spot rate > Future rate (deduct discount) |

| Margin Adjustment | Deduct from buying, add to selling (after premium/discount) |

| Bid Rate | Bank's rate to buy FC (1st part of quote) |

| Offer Rate | Bank's rate to sell FC (2nd part of quote) |

| Cross Rate | Calculated through 3rd common currency (Chain Rule) |

FC Transaction Rate Quick Reference

| Transaction | Rate Used |

|---|---|

| Issue DD to customer | TT Selling rate |

| Purchase FC export bill | Bills Buying rate |

| Payment of FC import bill | Bills Selling rate |

| Dishonoured export bill | TT Selling rate |

| FCNR to NRE transfer | TT Buying rate |

| Crystallisation of export bill | TT Selling rate |

FC Positions Quick Reference

| Term | Definition |

|---|---|

| FC Position | Amount payable or receivable in FC |

| Closed Position | Sale = Purchase (no risk) |

| Open Position | Sale ≠ Purchase (risk position) |

| Long Position | Purchase > Sale (gain if rate ↑) |

| Short Position | Sale > Purchase (gain if rate ↓) |

| Day Light Position | Balance during day time (higher limit) |

| Overnight Position | Balance at close of day (lower limit) |

| Position Limit | Fixed by BOD, reported to RBI |

Swap & Arbitrage

| Concept | Definition |

|---|---|

| Swap | 2 opposite FC transactions at different value dates |

| Swap Types | Spot + Forward OR Forward + Forward |

| Swap Objective | Cover forex fluctuation risk |

| Arbitrage | Profit from rate difference between markets |

| Arbitrage Method | Buy low in one market, sell high in another |

Lesson Doubts

Ask questions, get expert answers