🏦 Sources of Agricultural Credit - Cooperatives, Banks, RBI & NABARD

Complete guide to institutional sources of agricultural credit - cooperative structure (PACS to SCB), commercial banks, RRBs, RBI, SBI, and NABARD with history, functions, and exam-focused facts

How Does Credit Reach the Farmer?

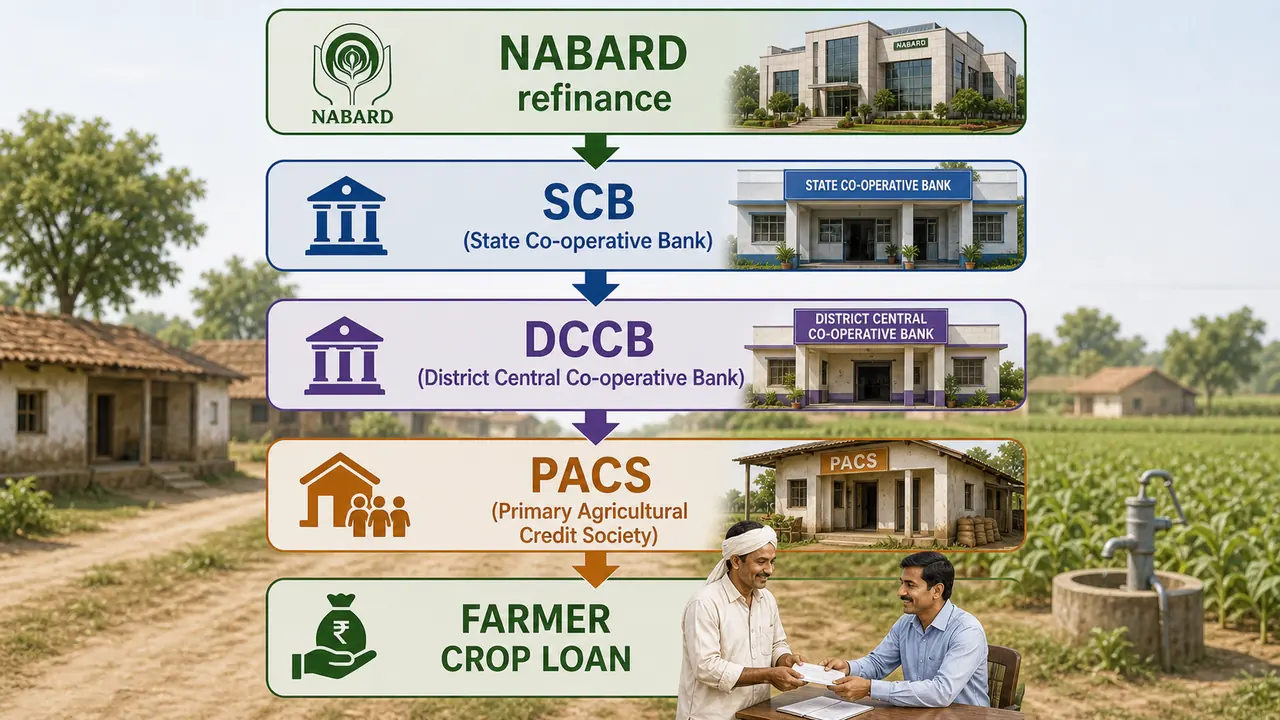

A rice farmer in Tamil Nadu walks into his village PACS (Primary Agricultural Credit Society) to get a crop loan. The PACS does not have unlimited funds -- it borrows from the District Central Cooperative Bank (DCCB), which in turn borrows from the State Cooperative Bank (SCB), which gets refinance from NABARD. This chain -- from NABARD down to the farmer's village -- is the institutional credit delivery system of India. Understanding this structure is essential for every agricultural finance exam.

Cooperatives in India

What is a Cooperative?

- A cooperative society is a basic institution for the socio-economic growth of villagers, bringing people together to pool resources and work collectively for mutual benefit.

- Founding principle: "Each for all and all for each"

- Minimum members required to register: 10

- Cooperatives originated in Europe; Britain is the homeland of the cooperative store movement

10 Principles of Cooperative Society UPPSC 2021

| No. | Principle | Meaning |

|---|---|---|

| 1 | Open and voluntary association | Membership open to all without discrimination |

| 2 | Democratic organisation | One member = one vote, regardless of share capital |

| 3 | Service | Primary aim is serving members, not maximizing profit |

| 4 | Self-help and mutual help | Members help themselves and each other |

| 5 | Distribution of profits/surpluses | Surplus shared equitably among members |

| 6 | Political and religious neutrality | No alignment with any party or religious group |

| 7 | Education | Members educated about cooperative values |

| 8 | Thrift | Encouraging savings and prudent financial management |

| 9 | Publicity | Promoting awareness of the society's activities |

| 10 | Honorary service | Office bearers serve voluntarily without compensation |

TIP

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

How Does Credit Reach the Farmer?

A rice farmer in Tamil Nadu walks into his village PACS (Primary Agricultural Credit Society) to get a crop loan. The PACS does not have unlimited funds -- it borrows from the District Central Cooperative Bank (DCCB), which in turn borrows from the State Cooperative Bank (SCB), which gets refinance from NABARD. This chain -- from NABARD down to the farmer's village -- is the institutional credit delivery system of India. Understanding this structure is essential for every agricultural finance exam.

Cooperatives in India

What is a Cooperative?

- A cooperative society is a basic institution for the socio-economic growth of villagers, bringing people together to pool resources and work collectively for mutual benefit.

- Founding principle: "Each for all and all for each"

- Minimum members required to register: 10

- Cooperatives originated in Europe; Britain is the homeland of the cooperative store movement

10 Principles of Cooperative Society UPPSC 2021

| No. | Principle | Meaning |

|---|---|---|

| 1 | Open and voluntary association | Membership open to all without discrimination |

| 2 | Democratic organisation | One member = one vote, regardless of share capital |

| 3 | Service | Primary aim is serving members, not maximizing profit |

| 4 | Self-help and mutual help | Members help themselves and each other |

| 5 | Distribution of profits/surpluses | Surplus shared equitably among members |

| 6 | Political and religious neutrality | No alignment with any party or religious group |

| 7 | Education | Members educated about cooperative values |

| 8 | Thrift | Encouraging savings and prudent financial management |

| 9 | Publicity | Promoting awareness of the society's activities |

| 10 | Honorary service | Office bearers serve voluntarily without compensation |

TIP

Mnemonic -- "OD SSEP PT H": Open, Democratic, Service, Self-help, Equitable profit, Political neutrality, Thrift, Publicity, Honorary, Education. Group them: governance (O,D), purpose (S,S,E), neutrality (P), operations (T,P,H,E).

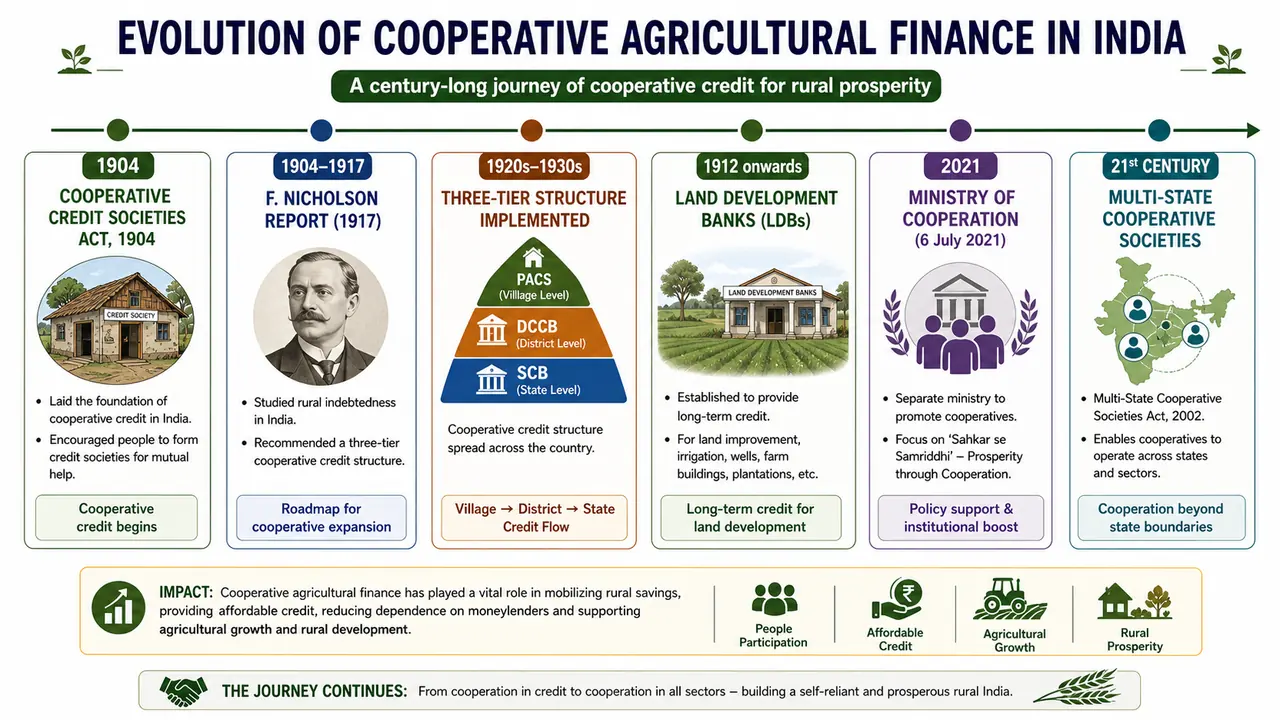

History of Cooperative Movement

IMPORTANT

Four Phases (Pre-Independence): Initiation (1904-1911) -- Modification (1912-1918) -- Expansion (1919-1929) -- Restructuring (1930-1946)

Timeline of Key Events

| Year | Event | Significance |

|---|---|---|

| 1904 | Cooperative Credit Societies Act | First cooperative law; only credit societies allowed |

| -- | F. Nicholson | Father of cooperative movement in India; studied European cooperatives |

| 1912 | New Act passed | Provision for non-credit societies and central cooperative societies |

| 1914 | Sir Macglan Committee | Recommended cooperative education, cooperative banks, provincial societies, careful scrutiny before lending |

| 1920 | First mortgage bank | Established in Punjab |

| 1929 | Central Land Mortgage Bank | Established at Madras for centralizing debenture issuance |

| 1939 | Multipurpose Cooperative Societies | First established in Orissa |

| 1942 | Multi-unit Cooperative Societies Act | Governs cooperatives operating across more than one state |

| 1944 | Agricultural Finance Sub-committee | Under Prof. D.R. Gadgil -- studied cooperative movement |

| 1945 | Cooperative Planning Committee | Submitted report in 1946 |

| 1951 | All India Rural Survey Committee | Chairman: A.D. Gorwala -- recommended large cooperatives, marketing cooperatives, SBI establishment |

| 1954 | Landmark year for rural credit | Recommended large-size cooperative societies; beginning of organized rural credit policy |

| 1959 | Nagpur Session of INC | Resolution on Agrarian Economy -- radical change in cooperative policy |

| 1962 | NCDC Act | National Cooperative Development Corporation -- plans, promotes, finances cooperative development |

NOTE

Exam Quick Recall: Father of Indian cooperatives = F. Nicholson | Movement started = 1904 | Origin = Europe | Cooperative store homeland = Britain

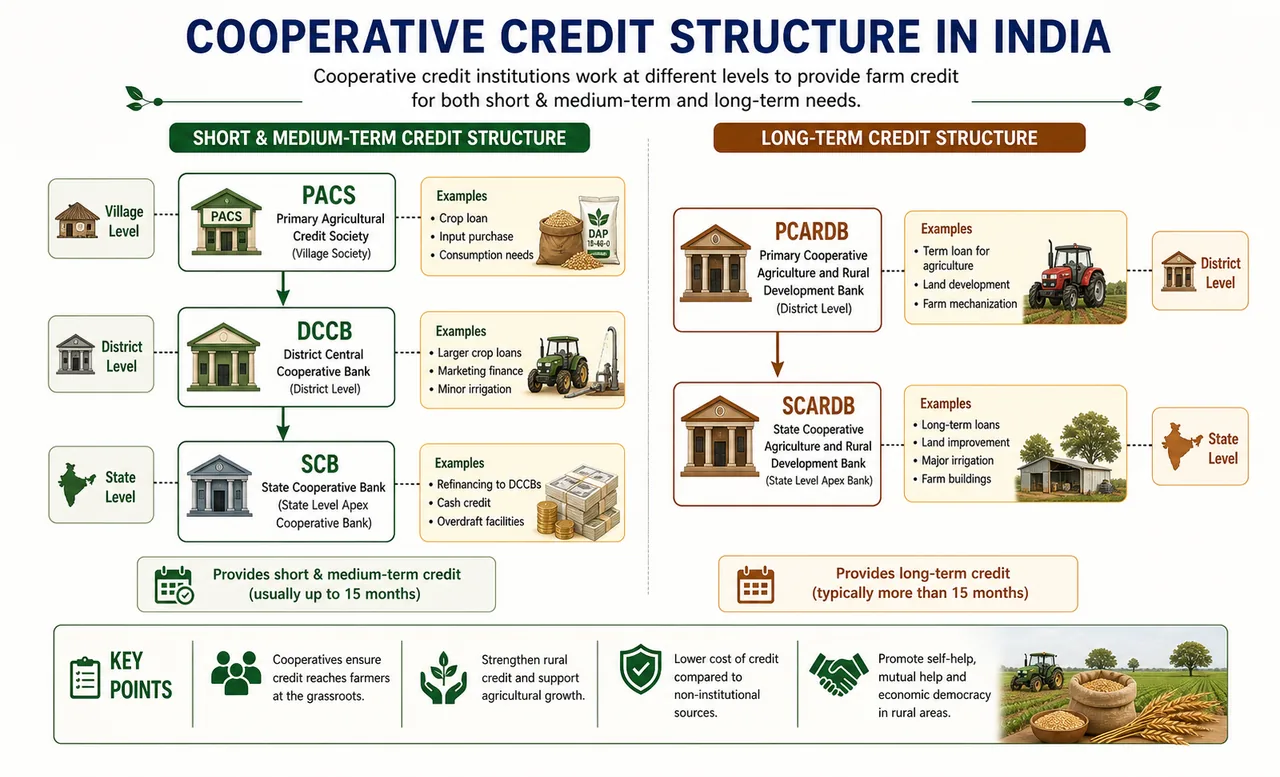

Cooperative Credit Structure

The cooperative credit structure in India has two parallel streams:

| Stream | Purpose | Structure |

|---|---|---|

| Short and Medium-term Credit | Crop loans, input purchase, working capital | PACS --> DCCB --> SCB |

| Long-term Credit | Land improvement, machinery, permanent assets | PCARDBs --> SCARDBs |

a) Primary Agricultural Credit Society (PACS)

PACS is the foundation stone of the entire cooperative credit structure. It operates at the village level and is the farmer's first point of contact.

| Feature | Detail |

|---|---|

| Established since | 1904 (first Cooperative Credit Societies Act) |

| Original objective | Provide cheap credit to free farmers from moneylenders |

| Level of operation | Village |

| Credit type | Short-term and medium-term loans |

Functions of PACS:

- Promote economic interests of members through cooperative principles

- Provide short and medium-term loans

- Promote savings habit among members

- Supply agricultural inputs -- fertilizers, seeds, insecticides, implements

- Provide marketing facilities for agricultural produce

- Supply domestic products -- sugar, kerosene, etc. (PDS distribution)

Example: A wheat farmer in Madhya Pradesh gets a crop loan from his village PACS, buys subsidized fertilizer from the same PACS, and sells his wheat through the PACS-linked marketing cooperative -- all under one roof.

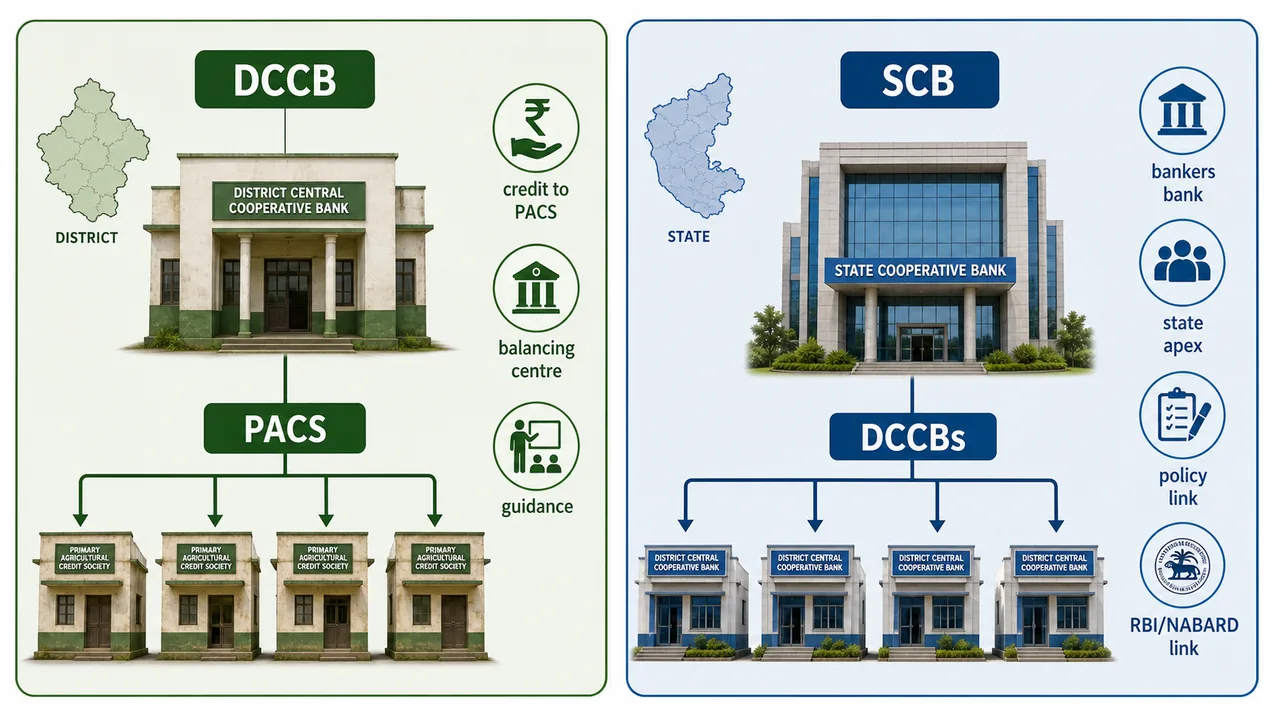

b) District Central Cooperative Banks (DCCBs)

DCCBs form the middle tier linking PACS with SCBs.

Functions:

- Meet credit requirements of member PACS

- Perform banking business

- Act as balancing centres -- divert surplus funds from some PACS to those facing shortages

- Guide and supervise the PACS

- Undertake non-credit activities

c) State Cooperative Bank (SCB)

SCB is the apex institution at the state level, linking PACS with the money market, RBI, and NABARD.

Functions:

- Act as bankers' bank to DCCBs -- supervise, control, and guide them

- Mobilize financial resources and deploy them across cooperative sectors

- Coordinate with development agencies and help government in cooperative planning

- Formulate and execute uniform credit policies for the cooperative movement

d) Land Development Banks

| Feature | Detail |

|---|---|

| First mortgage bank | 1920 in Punjab |

| Central Land Mortgage Bank | 1929 at Madras |

| Renamed to | Land Development Bank (LDB) -- during 3rd Five Year Plan |

| Current names | SCARDBs (State level) and PCARDBs (District/Taluk/Block level) |

| Purpose | Long-term credit for durable farm assets and permanent land improvements |

| Repayment period | Up to 20 years in installments |

What long-term credit is used for: Machinery purchase, livestock acquisition, well construction, land levelling and reclamation, farm building construction, pump-set installation, orchard establishment, redemption of old debts.

Sahakar-Se-Samriddhi (From Cooperation to Prosperity)

TIP

Cooperative Reach: 8.5 lakh registered cooperatives | 29 crore+ members | 98% villages covered by PACS | 19% of agriculture finance through cooperatives | Ministry of Cooperation established July 2021

| Statistic | Figure |

|---|---|

| Registered cooperatives | 8.5 lakh |

| Members | 29 crore+ (mainly marginalized and lower-income rural groups) |

| Village coverage by PACS | 98% |

| Share of agriculture finance | 19% |

| Ministry of Cooperation | Established July 2021 |

| Computerization target | 63,000 functional PACS |

Multi-State Cooperative Societies (MSCS):

- Governed by Multi-State Cooperative Societies Act, 2002 (replaced 1984 Act)

- 1,528 registered societies including 66 Multi-State Cooperative Banks with deposits of approximately Rs 2.6 lakh crore

- Maharashtra leads with 661 cooperatives, followed by Delhi and Uttar Pradesh

Other Cooperative Finance Institutions

LAMPS (Large-Sized Adivasi Multi-Purpose Cooperative Societies)

| Feature | Detail |

|---|---|

| Recommended by | Committee under Shri Bawa (1971) |

| Operating area | Hill and tribal areas |

| Unique approach | Single-window service for all needs of tribal communities |

Functions of LAMPS:

- Provide all types of credit including for social obligations and consumer needs

- Provide technical guidance for agriculture modernization

- Supply inputs and essential commodities

- Arrange marketing of agricultural produce, minor forest products, and subsidiary occupation products

FSS (Farmers' Service Society)

| Feature | Detail |

|---|---|

| Problem addressed | PACS were controlled by better-off sections; small/marginal farmers excluded |

| Recommended by | National Commission on Agriculture |

| Launched | 1973 |

| Detailed recommendation by | T.A. Pai committee (1974) |

| Purpose | Change power structure in favor of weaker sections while adopting commercial banking principles |

Why FSS was needed: By the 1970s, multi-purpose PACS had failed to diversify operations, reach weaker sections, or become financially viable. Elite capture undermined the cooperative ideal of inclusive development.

Commercial Banks

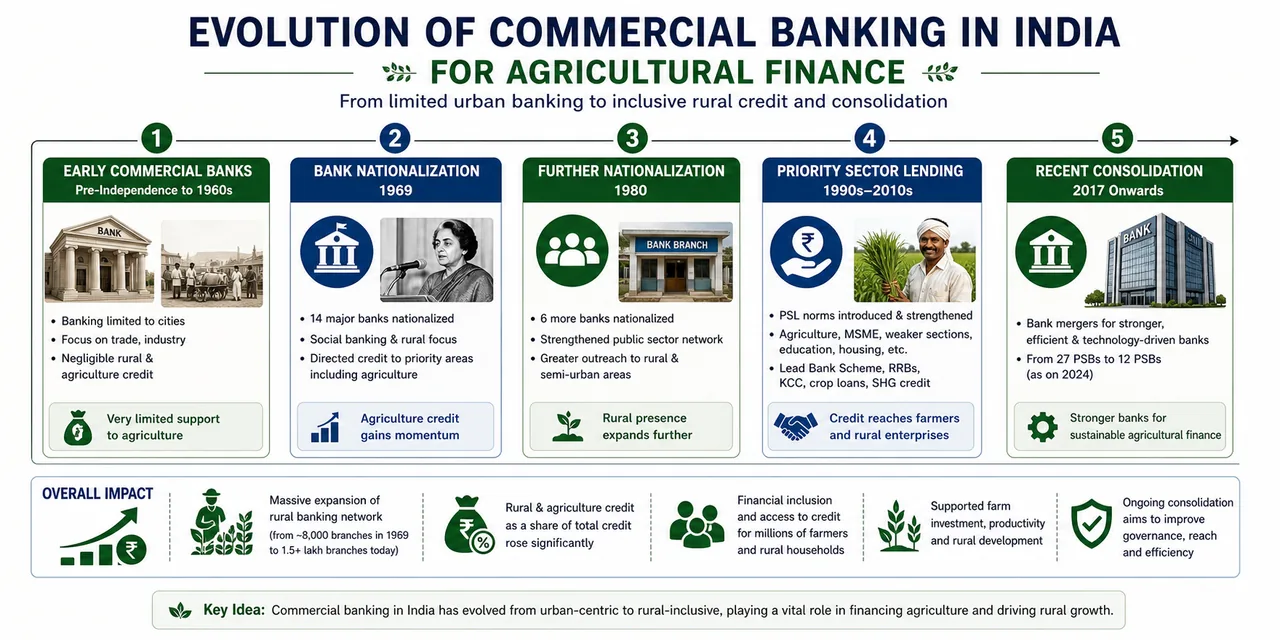

Nationalization of Banks

Nationalization was the most significant event in Indian banking history -- it redirected bank credit toward agriculture and priority sectors.

IMPORTANT

Bank Nationalization: First round: 14 banks in 1969 (deposits > Rs 50 crore). Second round: 6 banks in 1980 (deposits > Rs 200 crore). Currently 12 Public Sector Banks after mergers.

| Round | Year | Banks Nationalized | Criterion |

|---|---|---|---|

| First | 1969 | 14 banks | Deposits exceeding Rs 50 crore |

| Second | 1980 | 6 banks | Deposits exceeding Rs 200 crore |

| After mergers | Present | 12 Public Sector Banks | Consolidation for larger, stronger institutions |

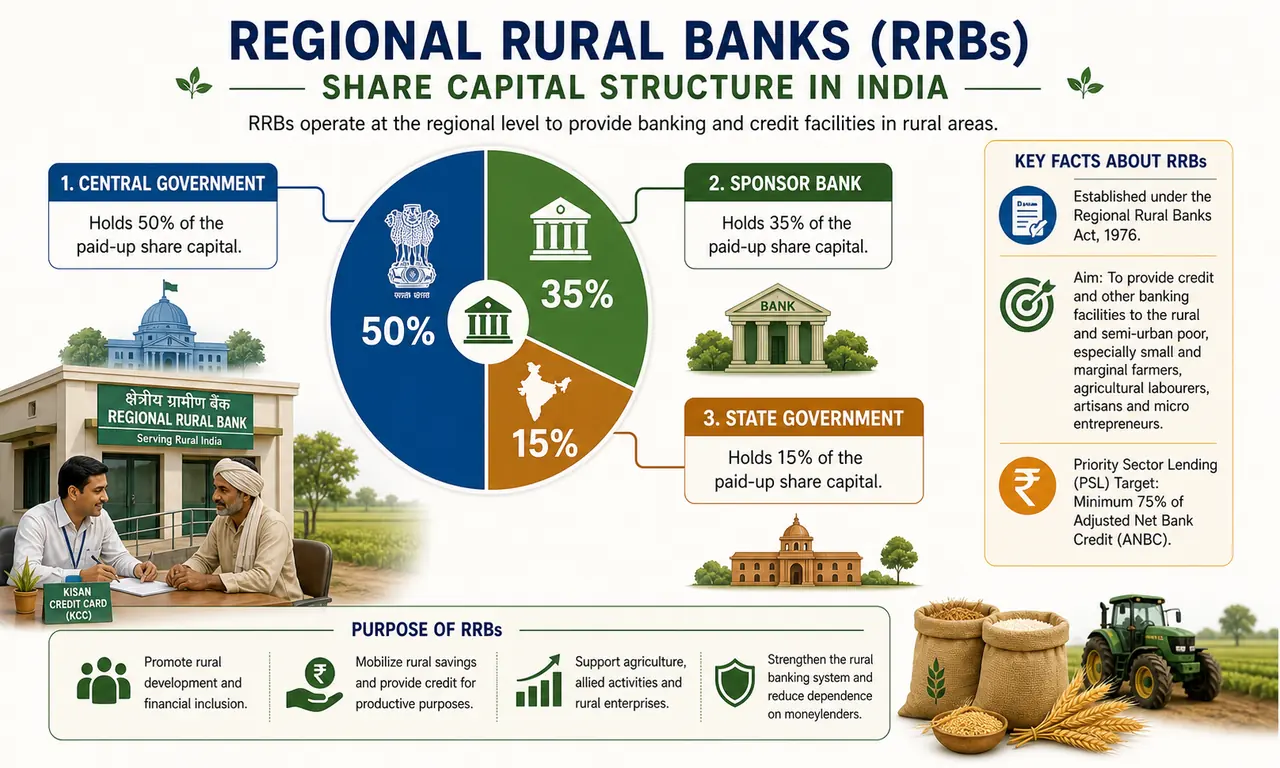

Regional Rural Banks (RRBs)

TIP

RRB Key Facts: Recommended by Narasimhan Committee (1975) | Established under RRB Act 1976 | PSL target = 75% (vs 40% for commercial banks) | Currently 43 RRBs | Share: Centre 50%, State 15%, Sponsor Bank 35%

| Feature | Detail |

|---|---|

| Recommended by | M. Narasimhan Committee (1975) |

| Established under | 20-point economic programme (1975) by Indira Gandhi |

| Legal basis | RRB Act of 1976 (ordinance of 26 September 1975) |

| Context | 90% of India's population was rural at that time |

| Main objective | Credit to small/marginal farmers, agricultural laborers, artisans, small entrepreneurs |

| Design concept | Combine local reach of cooperatives + professional management of commercial banks |

Share Capital Structure:

| Contributor | Share |

|---|---|

| Central Government | 50% |

| Sponsor Bank | 35% |

| State Government | 15% |

- Authorized capital: Rs 1 crore per bank

- Paid-up capital: Rs 25 lakh per bank

- PSL target: 75% (nearly double the 40% for commercial banks)

- Current count: 43 RRBs (reduced from 190+ through consolidation)

Evaluation: Prof. M.L. Dantwala committee (1977, report in 1980) confirmed that RRBs were essential for providing credit even in areas where PACS were already functioning.

Reserve Bank of India (RBI)

NOTE

RBI Quick Facts

- Established: 1st April 1935 (RBI Act 1934)

- Nationalized: 1st January 1949

- First Governor: Osborne A. Smith

- First Indian Governor: C.D. Deshmukh

- Headquarters: Mumbai

- Governor's term: 3 years

- Deputy Governors: 4

| Feature | Detail |

|---|---|

| Established | 1st April 1935 |

| Act | RBI Act, 1934 |

| Nationalized | 1st January 1949 |

| First Governor | Osborne A. Smith (1 Jan 1935 - 30 June 1937) |

| First Indian Governor | C.D. Deshmukh |

| Headquarters | Mumbai |

| Governor's term | 3 years |

| Deputy Governors | 4 |

Functions of RBI

| Function | Relevance to Agriculture |

|---|---|

| Issue of currency | Sole authority for printing and distributing currency notes |

| Custodian of Forex | Maintains exchange rate stability affecting agricultural exports |

| Payment system regulation | Enables digital payments for farmers (UPI, NEFT) |

| Banking regulation | Directs banks to lend to agriculture through PSL norms |

| Monetary authority and credit control | Repo rate, CRR, SLR influence cost and availability of farm credit |

State Bank of India (SBI)

| Event | Year | Detail |

|---|---|---|

| Bank of Bengal | 1806 | One of three Presidency banks |

| Bank of Bombay | 1840 | Second Presidency bank |

| Bank of Madras | 1843 | Third Presidency bank |

| Imperial Bank of India | 1921 | Merger of all three Presidency banks |

| State Bank of India | 1955 | Nationalization of Imperial Bank via SBI Act 1955 |

SBI was created to extend banking to rural and semi-urban areas and serve as the principal agent of the RBI.

NABARD (National Bank for Agriculture and Rural Development)

IMPORTANT

NABARD: Established 12th July, 1982 under NABARD Act 1981 | Recommended by Sivaraman Committee (CRAFICARD, 1979) | HQ: Mumbai | Fully owned by Govt of India | Authorized capital: Rs 30,000 crore

Overview

| Feature | Detail |

|---|---|

| Full name | National Bank for Agriculture and Rural Development |

| Nature | Apex development finance institution |

| Ownership | Fully owned by Government of India |

| Established | 12th July, 1982 |

| Act | NABARD Act, 1981 |

| Headquarters | Mumbai |

| Authorized capital | Rs 30,000 crore |

| Initial paid-up capital | Rs 100 crore (50:50 by GoI and RBI) |

| Paid-up capital (March 2020) | Rs 14,080 crore |

History -- Why Was NABARD Created?

Before NABARD, three separate units of RBI handled rural credit:

| RBI Unit | Function | Transferred to NABARD |

|---|---|---|

| Agricultural Credit Department (ACD) | Short-term refinance to cooperatives | Yes |

| Rural Planning and Credit Cell (RPCC) | Dealt with RRBs since 1979 | Yes |

| Agricultural Refinance and Development Corporation (ARDC) | Medium and long-term agricultural refinance (originally ARC, est. 1963; renamed ARDC in 1975) | Yes |

In 1979, the Sivaraman Committee (CRAFICARD) recommended creating a single apex institution to provide undivided attention and focused direction to agricultural and rural credit. This led to NABARD's establishment in 1982.

TIP

Exam Mnemonic: NABARD took over ACD + RPCC + ARDC from RBI. Think: "A Rural Powerhouse" (ACD, RPCC, ARDC --> combined into NABARD).

Functions of NABARD

A. Finance

Direct Finance:

| Fund/Scheme | Purpose |

|---|---|

| RIDF (Rural Infrastructure Development Fund) | Critical rural infrastructure projects |

| NIDA (NABARD Infrastructure Development Assistance) | Infrastructure support |

| PMAY-G (Pradhan Mantri Awaas Yojana - Grameen) | Rural housing |

| SBM-G (Swachh Bharat Mission - Gramin) | Sanitation |

| LTIF (Long-Term Irrigation Fund) | Irrigation projects |

| MIF (Micro Irrigation Fund) | Water-efficient irrigation (drip, sprinkler) |

| Warehouses, Cold Storage, Cold Chain | Reducing post-harvest losses |

| Food Processing Fund | Food processing units in designated food parks |

| DIDF (Dairy Processing and Infrastructure Development Fund) | Dairy infrastructure |

| CFF (Credit Facility to Federations) | Supporting farmer federations |

| DRA (Direct Refinance to DCCBs) | Short-term multipurpose credit |

| PACS financing | Strengthening village-level cooperatives |

| Producers' organizations | Supporting FPOs and FPCs |

| UPNRM (Umbrella Programme for Natural Resource Management) | Watershed, soil, water conservation |

| AIFs (Alternative Investment Funds) | Strategic agricultural investments |

Indirect Finance:

- Short-term loans (e.g., KCC refinance to banks for crop loans)

- Long-term loans (refinance for investment credit)

B. Supervision

NABARD conducts statutory inspection of StCBs, DCCBs, and RRBs to ensure their financial health and governance.

C. Developmental Functions

| Activity | Purpose |

|---|---|

| Institution development | Improve health of RRBs, StCBs, DCCBs, PACS, SCARDBs, PCARDBs |

| Marketing initiatives | Rural haats, rural marts, exhibitions/melas, geographical indications |

| Financial inclusion | Ensuring every rural household has basic financial services |

| Watershed development | Soil and water conservation in rain-fed areas |

| Research support | Funding research in agriculture and rural development |

| Climate change adaptation | Promoting climate-resilient agriculture and rural livelihoods |

Summary Cheat Sheet

| Institution / Topic | Key Facts |

|---|---|

| Cooperatives | Origin: Europe; India: 1904; Father: F. Nicholson; Principle: "Each for all and all for each"; Min 10 members |

| PACS | Village level; foundation of cooperative credit; short and medium-term loans; multi-service centre |

| DCCB | District level; middle tier; balancing centre between PACS |

| SCB | State level; apex; links PACS to money market and RBI |

| LDB/SCARDB | Long-term credit; up to 20 years; first mortgage bank: Punjab (1920) |

| LAMPS | Tribal areas; Bawa Committee (1971); single-window service |

| FSS | T.A. Pai (1974); for weaker sections; replaced elite-captured PACS |

| Bank Nationalization | 1969 (14 banks, >50 Cr) + 1980 (6 banks, >200 Cr) = now 12 PSBs |

| RRBs | Narasimhan (1975); RRB Act 1976; PSL 75%; 43 RRBs; Share: 50:35:15 |

| RBI | 1 April 1935; nationalized 1 Jan 1949; first governor: Osborne A. Smith; HQ: Mumbai |

| SBI | Imperial Bank (1921) nationalized in 1955; principal agent of RBI |

| NABARD | 12 July 1982; Sivaraman Committee; HQ: Mumbai; apex for agri finance; took over ACD+RPCC+ARDC |

| Cooperative reach | 8.5 lakh societies; 29 Cr members; 98% villages; 19% of agri finance |

| Ministry of Cooperation | Established July 2021 |

| NCDC | Act of 1962; plans, promotes, finances cooperative development |