₹ Priority Sector Lending

Comprehensive guide to priority sector lending guidelines, targets, and compliance requirements for banks.

Priority Sector Lending

Purpose

These Directions are issued with a view to delineating a framework for ensuring adequate flow of credit from the banking system to the sectors of the economy which are crucial for their contribution to socio-economic development, with focus on specific segments whose credit needs remain underserved despite being credit worthy.

Applicability

The provisions of these Directions shall, unless otherwise provided, apply to every Commercial Bank [including Regional Rural Bank (RRB), Small Finance Bank (SFB), Local Area Bank (LAB)] and Primary (Urban) Co-operative Bank (UCB) other than Salary Earners’ Bank.

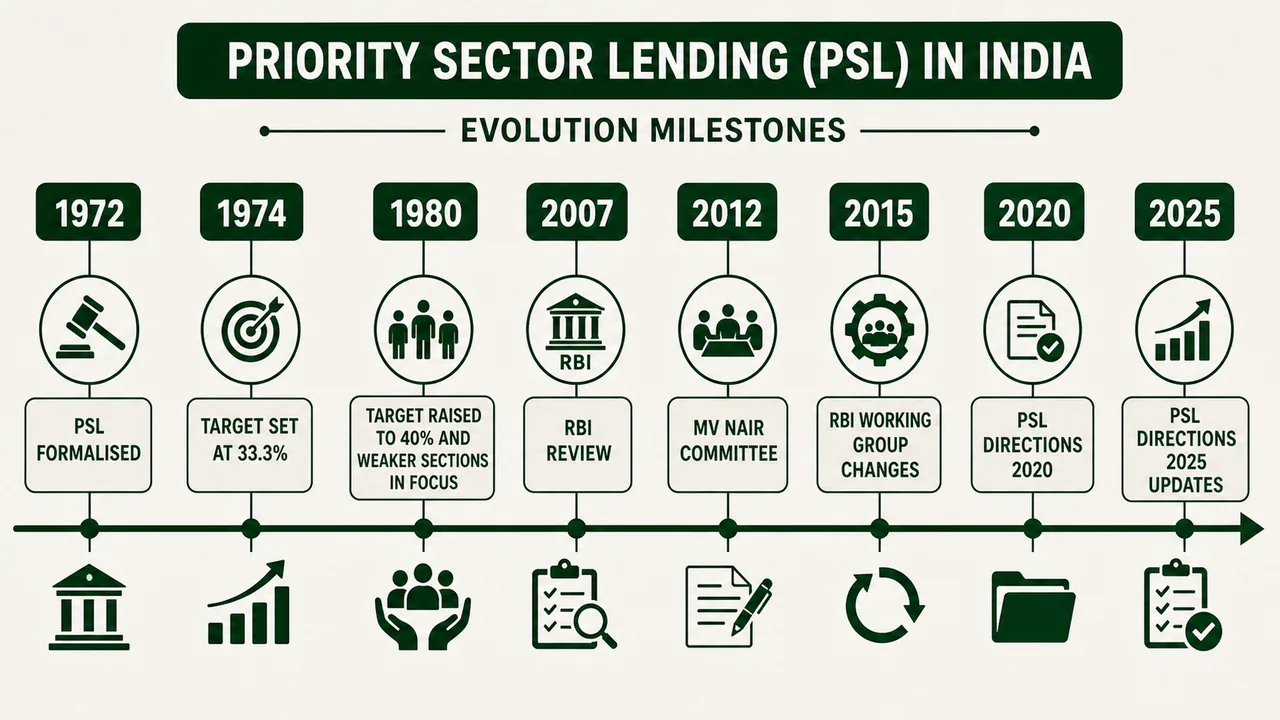

Origin and evolvement of PS Lending

| Year | Milestone |

|---|---|

| 1972 | Description of PS lending formalised |

| 1974 | 33.3% target fixed (1/3rd). To be achieved by March 1979 [Indira Gandhi] |

| 1980 | Target revised to 40%. Concept of Weaker section introduced. |

| 2007 | Review by RBI in-house group |

| 2012 | Major changes MV Nair Committee |

| 2015 | Major changes RBI working group w.e.f. 23.04.15 |

| 2020 | Issue of RBI (PSL) Directions 2020 (4.9.20). --> Main circular |

| 2025 | Issue of RBI (PSL) Directions 2025 (1.4.2025) --> Updates in main circular |

PS Lending Activities (Mnemonic: AAMEE HASRO)

- Agriculture

- Micro, Small and Medium Enterprises (MSME)

- Export Credit

- Education loans

- Housing loans

- Social infrastructure

- Renewable Energy

- Other Priority Sector loans

Terms

“On-lending” means loans sanctioned by banks to eligible intermediaries for onward lending. Such loans, extended for creation of priority sector assets and which remain deployed in such assets, will be eligible for classification under PSL.

Interactive Preview

Try the embedded exercise below. Full lesson access still requires Pro.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Priority Sector Lending

Purpose

These Directions are issued with a view to delineating a framework for ensuring adequate flow of credit from the banking system to the sectors of the economy which are crucial for their contribution to socio-economic development, with focus on specific segments whose credit needs remain underserved despite being credit worthy.

Applicability

The provisions of these Directions shall, unless otherwise provided, apply to every Commercial Bank [including Regional Rural Bank (RRB), Small Finance Bank (SFB), Local Area Bank (LAB)] and Primary (Urban) Co-operative Bank (UCB) other than Salary Earners’ Bank.

Origin and evolvement of PS Lending

| Year | Milestone |

|---|---|

| 1972 | Description of PS lending formalised |

| 1974 | 33.3% target fixed (1/3rd). To be achieved by March 1979 [Indira Gandhi] |

| 1980 | Target revised to 40%. Concept of Weaker section introduced. |

| 2007 | Review by RBI in-house group |

| 2012 | Major changes MV Nair Committee |

| 2015 | Major changes RBI working group w.e.f. 23.04.15 |

| 2020 | Issue of RBI (PSL) Directions 2020 (4.9.20). --> Main circular |

| 2025 | Issue of RBI (PSL) Directions 2025 (1.4.2025) --> Updates in main circular |

PS Lending Activities (Mnemonic: AAMEE HASRO)

- Agriculture

- Micro, Small and Medium Enterprises (MSME)

- Export Credit

- Education loans

- Housing loans

- Social infrastructure

- Renewable Energy

- Other Priority Sector loans

Terms

“On-lending” means loans sanctioned by banks to eligible intermediaries for onward lending. Such loans, extended for creation of priority sector assets and which remain deployed in such assets, will be eligible for classification under PSL.

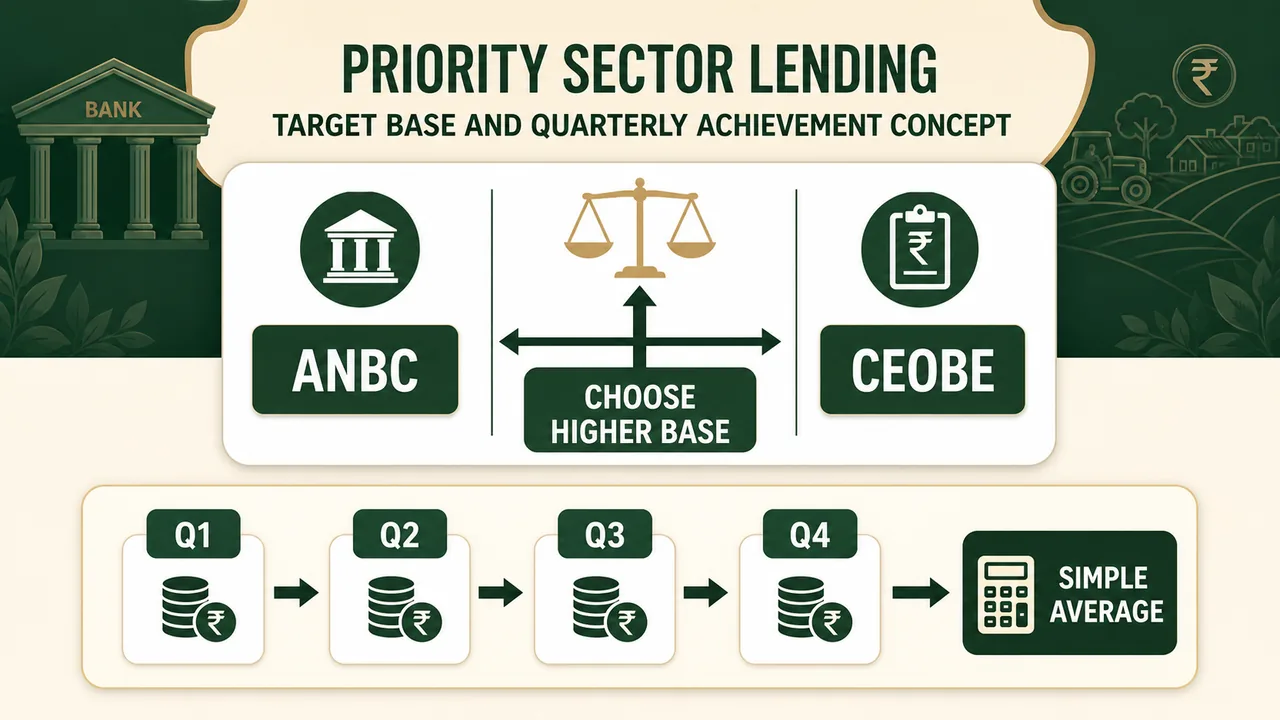

Linkage of PS Lending Targets

Targets expressed as Percentage of ANBC or CEOBE whichever is higher, as on corresponding date of preceding year.

- ANBC: Adjusted net bank credit (i.e. Fund based exposures)

- CEOBE: Credit equivalent of off-balance sheet exposure (i.e. non-fund-based exposures)

Target Achievement: Simple average of 4 quarterly outstanding PS loans during the current year or to be taken.

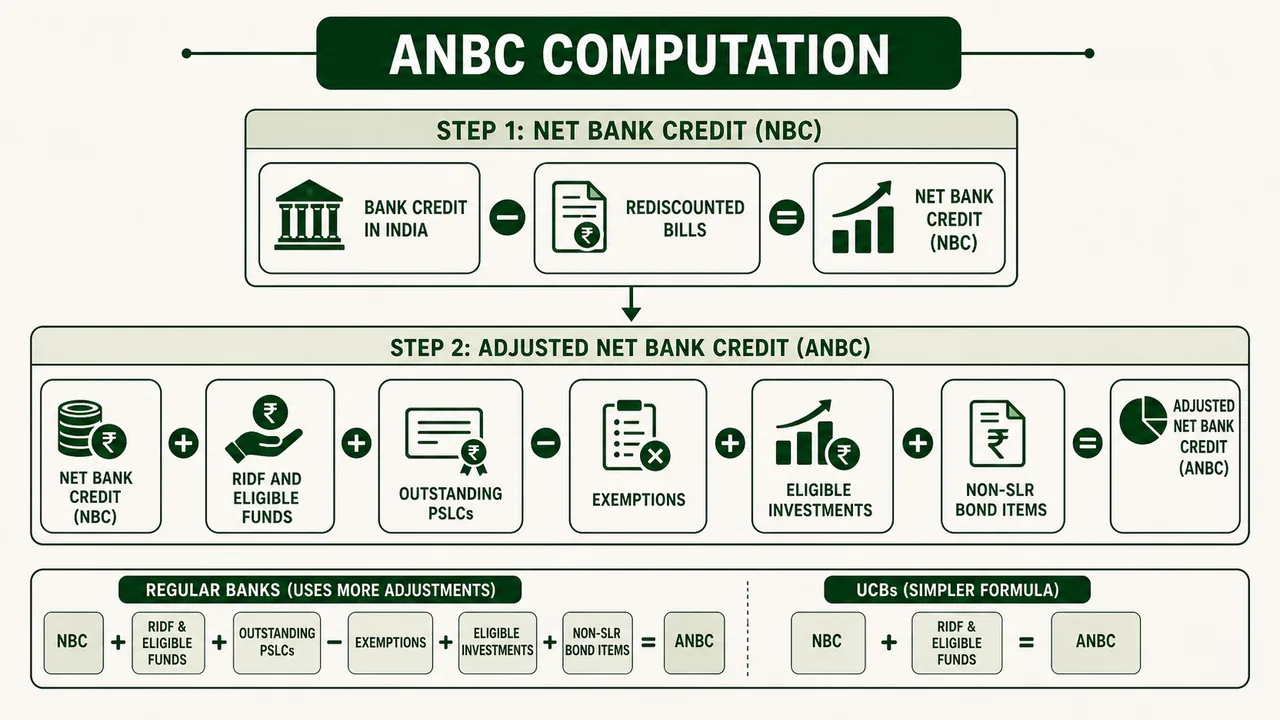

Computation of Adjusted Net Bank Credit (ANBC)

For the purpose of priority sector lending, ANBC shall be computed as follows:

| Item | Description |

|---|---|

| I | Bank Credit in India [as prescribed in item No.VI of Form 'A’ under Section 42(2) of the RBI Act, 1934] |

| II | Bills rediscounted with RBI and other approved Financial Institutions. This represents the loans (bills) the Bank has "passed on" to the RBI in exchange for immediate cash. (Bank give money to business (Bill of Exchange) with some interest. Then bank sells this to RBI, i.e. rediscount). |

| III | Net Bank Credit (NBC)* (I-II). When a Bank rediscounts a bill with the RBI, the Bank effectively sells that loan to the RBI and gets its money back immediately. |

| IV | Outstanding Deposits under RIDF and other eligible funds with NABARD, NHB, SIDBI and MUDRA Ltd in lieu of non-achievement of priority sector lending targets/sub-targets + outstanding PSLCs. (Bank to deposit that shortfall amount). |

| V | Eligible amount for exemptions on issuance of long-term bonds for infrastructure and affordable housing as per circular DBOD.BP.BC.No.25/08.12.014/2014-15 dated July 15, 2014 |

| VI | Advances extended in India against the incremental FCNR (B)/NRE deposits, qualifying for exemption from CRR/SLR requirements, as per the Reserve Bank’s circulars DBOD.No.Ret.BC.36/12.01.001/2013-14 dated August 14, 2013 read with DBOD.No.Ret.BC.93/12.01.001/2013-14 dated January 31, 2014... |

| VII | Investments made by public sector banks in the Recapitalization Bonds floated by Government of India |

| VIII | Other investments eligible to be treated as priority sector (e.g. investments in securitisation notes) |

| IX | Bonds/debentures in non-SLR categories under HTM category |

| X | For UCBs: Investments made after August 30, 2007, in permitted non SLR bonds held under ‘Held to Maturity’ (HTM) category |

ANBC (Other than UCBs) = III + IV - (V + VI + VII) + VIII + IX ANBC for UCBs = III + IV - VI + X

- For the purpose of priority sector computation only. Banks shall not deduct / net any amount like provisions, accrued interest, etc. from NBC.

ANBC for Different Bank Types

- For Regular Banks: Formula with items 1-9.

- For UCBs (Urban Co-operative Banks): Simpler formula with fewer adjustments.

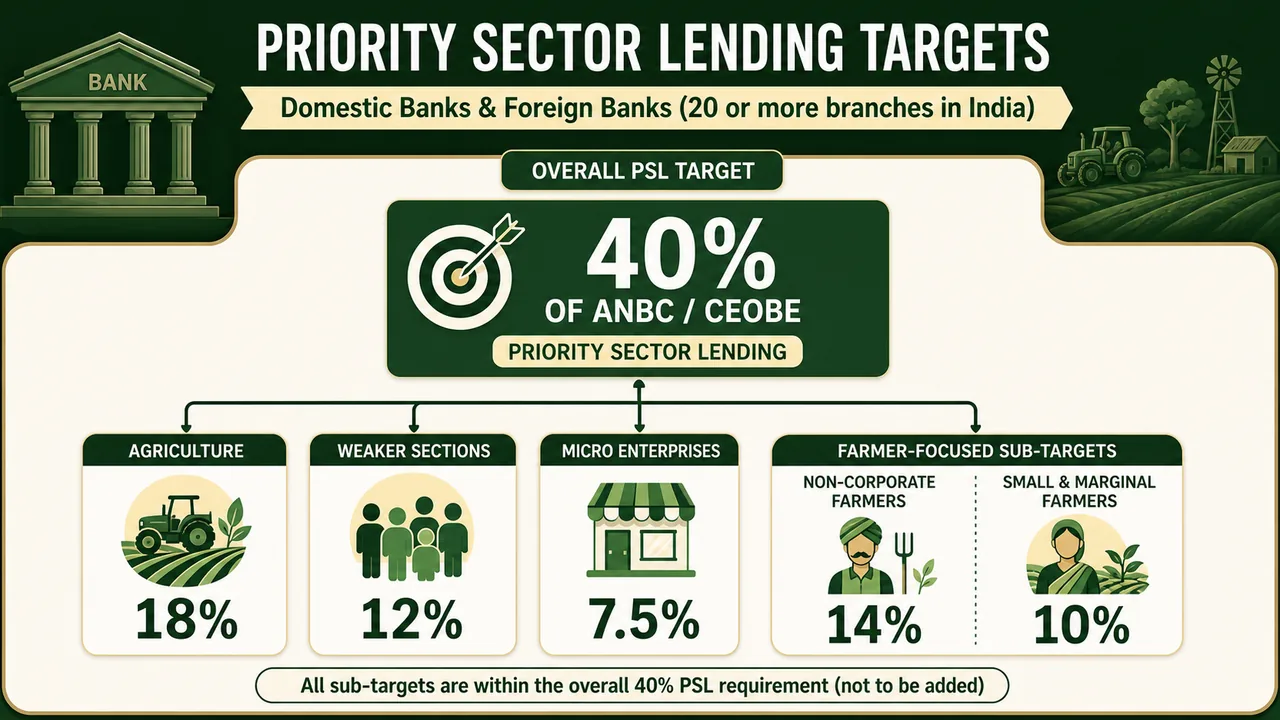

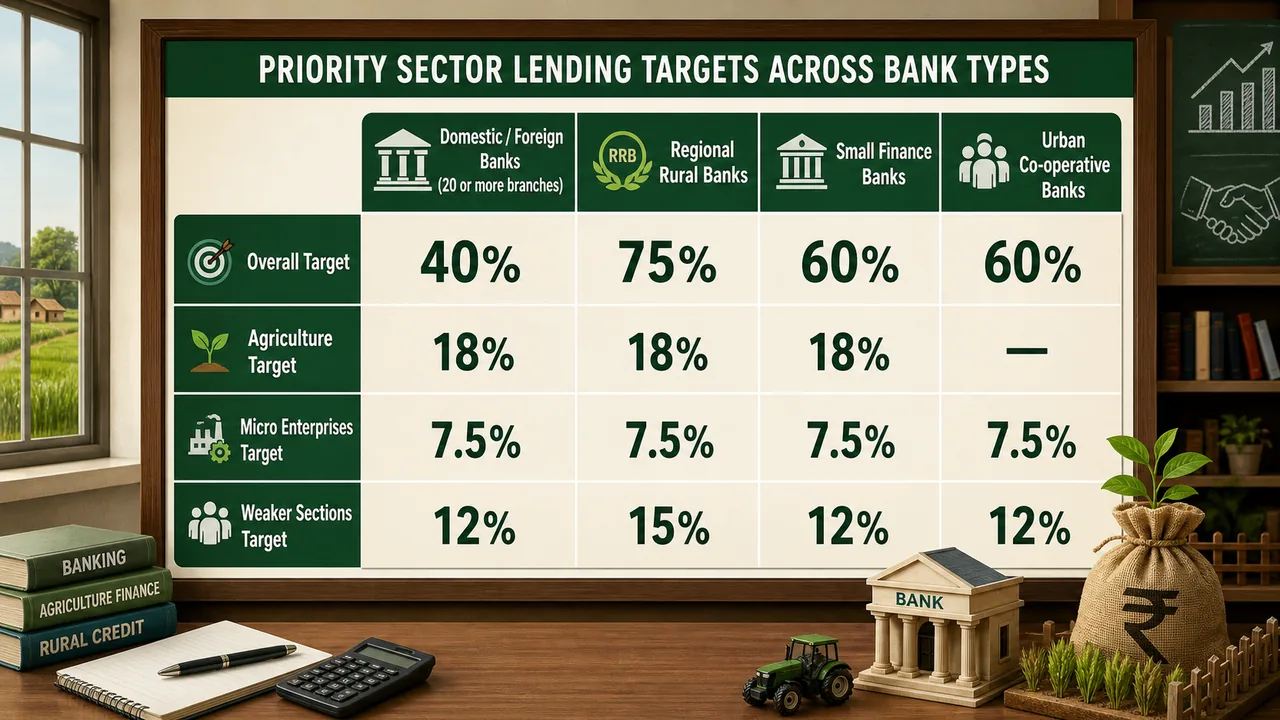

PSL Targets for Domestic Banks + Foreign Banks (20 or more branches)

Priority Sector Loans - Min 40% of ANBC or CEOBE (whichever is higher, either fund based or non-fund-based bank credit)

Mandatory Sub-targets within 40%:

-

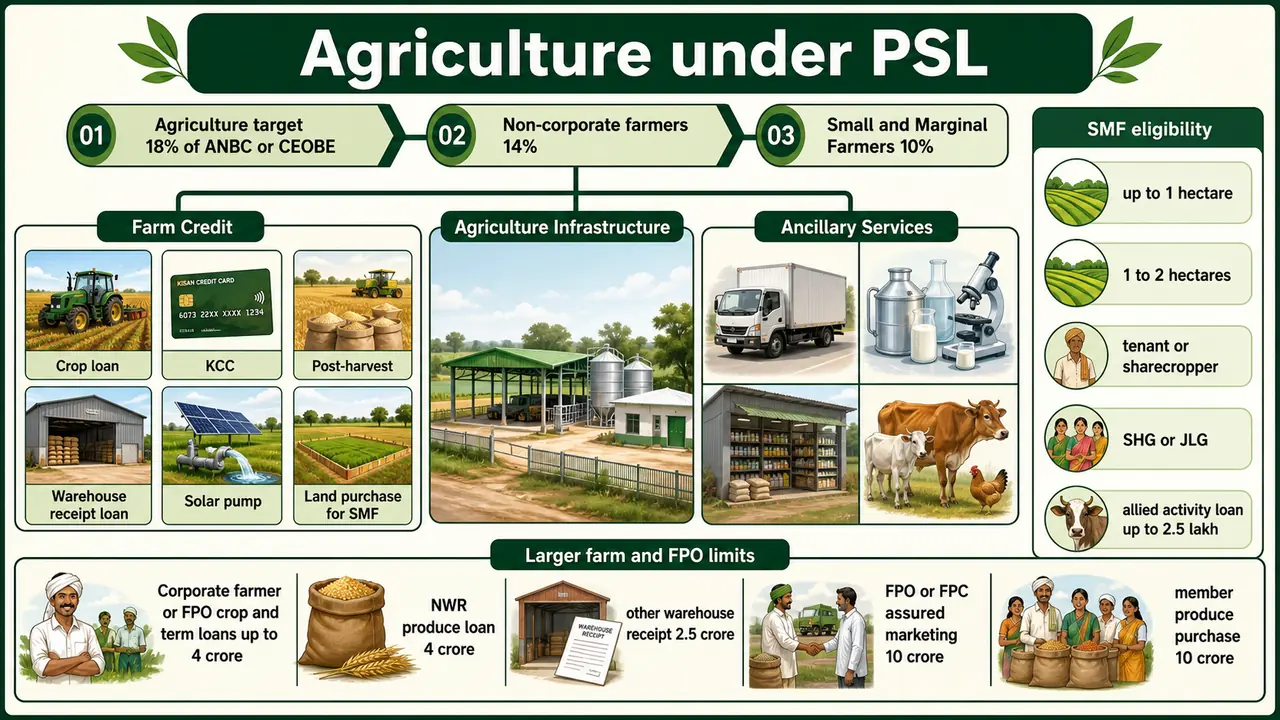

Agriculture: 18% of ANBC or 45% of PS loans.

- Loans to non-corporate farmers: min 14% ANBC.

- Loans to Marginal and Small Farmers: 10% of ANBC (It was 8% earlier, increased to 9% by 31.03.22, 9.5% by 31.03.23 and 10% by 31.3.24).

- MF = LH up to 1 hectare. SF = LH above 1 up to 2 hectares.

- System-wide average for loans to non-corporate farmers: Last 3 years achievement with regard to overall direct lending to non-corporate farmers is notified by RBI, every year.

-

Loans to Weaker Sections:

- 31.03.22 = 11%

- 31.3.23 = 11.5%

- 31.03.24 = 12%

-

Sub Target for Micro Enterprises: 7.5% of ANBC. (All loans to KVIC sector, to be classified as Loans to micro enterprises).

Weaker Section Activities

- Small & Marginal Farmers.

- Artisans & VC Industries loans up to Rs. 2 lac.

- Self Help Groups.

- SC/ST.

- Distressed farmers for debt-swap of non-institutional loans.

- Distressed persons other than farmers (Loan up to Rs. 1 lac) for debt swap.

- Individual women beneficiaries (Loan up to Rs.2 lac).

- Disabled persons.

- Beneficiaries of Deendayal Antodhya Yojna - National Rural Livelihood Mission) DAY-NRLM.

- Beneficiaries of Deendayal Antodhya Yojna National Urban Livelihood Mission (DAY-NULM).

- Beneficiaries of Differential Rate of Interest (DRI).

- Scheme for Rehabilitation of Manual Scavengers (SRMS).

- Jan Dhan Yojna (OD up to Rs. 10,000) annual income max Rs. 1 lac in rural and Rs.1.60 lac other.

- Transgenders.

- Minority communities as may be notified by Govt. of India.

PM Task Force Targets:

- Annual increase in no. of micro enterprise loan A/Cs: 10%

- Annual increase in MSE advances: 20%

- 60% of MSE lending should be to micro enterprises

Targets under Govt. Sponsored Schemes:

- DRI: No overall target. Within DRI 40% to SC/ST & Within DRI 2/3rd disbursement through Rural & Semi-urban Branches.

- PMEGP: 50% of total cases through Rural Branches.

- NRLM: All loans to women SHG, which should be 50% for SC/ST, 3% for disabled and 15% for minority community.

- NULM: SC/ST: In ratio of local population. Women: 30%, Disabled: 3%, Minorities: 15%.

Example of foreign bank with > 20 branches:

- Standard Chartered Bank: ~100 branches (Largest network).

- DBS Bank India: ~600+ branches (After acquiring Lakshmi Vilas Bank).

- HSBC India: ~26 branches (Recently received RBI approval to open 20 more).

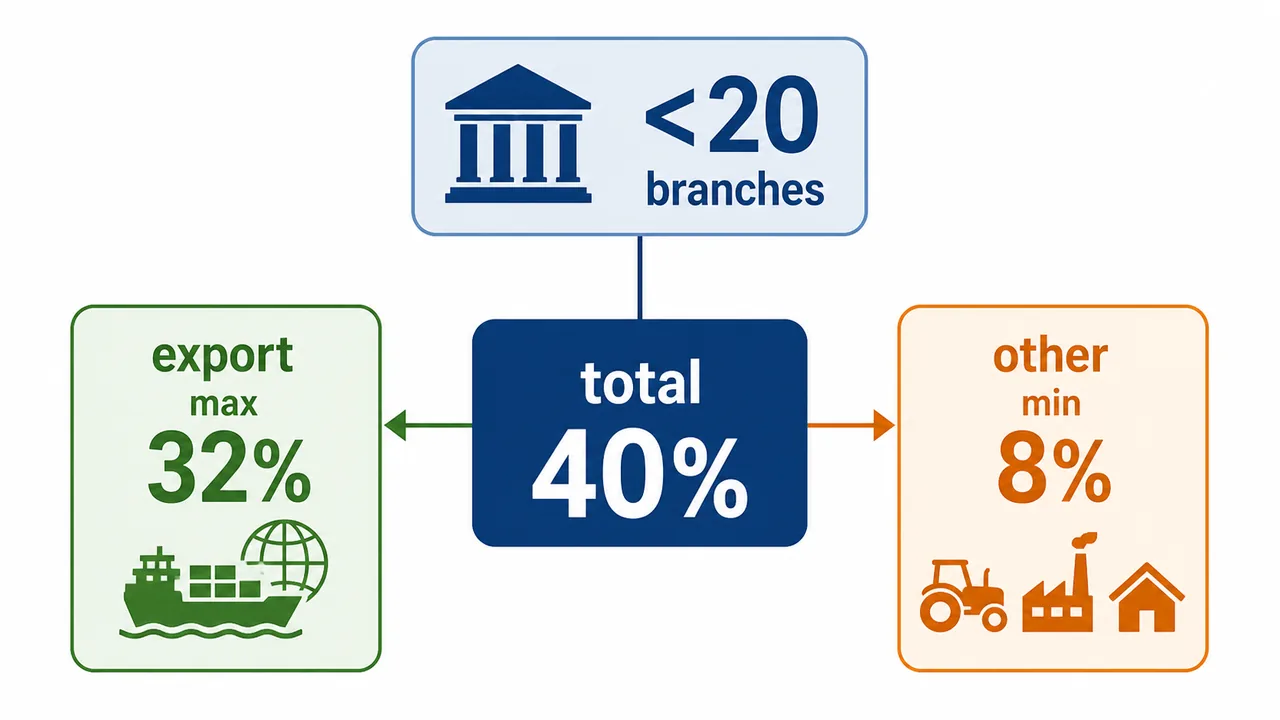

PSL Targets for Foreign Banks (< 20 branches)

Priority Sector Loans: 40% of ANBC or CEOBE

Sub-targets:

- Max 32% as export credit

- Min 8% as other than export credit

- No specific target for MSEs, Agriculture, Housing etc.

Example:

- Deutsche Bank (17 branches)

- SBM Bank (India) (~12–15 branches)

- Citibank India (~14 branches)

- BNP Paribas (~8 branches)

PSL Targets for Regional Rural Banks (RRBs)

PS Lending - 75% of ANBC or CEOBE

Sub Target:

- Agriculture:

- 18% of ANBC or CEOBE, whichever is higher.

- 14% of ANBC for non-corporate farmers.

- 10% of ANBC should be for small and marginal farmers.

- Micro enterprises: 7.5% of ANBC or CEOBE, whichever is higher.

- Weaker Section: 15% of ANBC or CEOBE, whichever is higher.

- Ceiling: However, lending to Medium Enterprises, Social Infrastructure and Renewable Energy shall be reckoned for priority sector achievement up to 15 per cent of ANBC only.

PSL Targets for Small Finance Banks

PS Lending - 60% of ANBC or CEOBE (Updated recently from 75 to 60%)

Sub-Target:

- Agriculture:

- 18% of ANBC or CEOBE, whichever is higher.

- 14% of ANBC for non-corporate farmers.

- 10% of ANBC should be for small and marginal farmers.

- Micro enterprises: 7.5% of ANBC or CEOBE, whichever is higher.

- Weaker Section: 12% of ANBC or CEOBE, whichever is higher.

Example Bank Highlights (2025):

- AU Small Finance Bank: Largest SFB in India. Recently merged with Fincare SFB (April 2024). First SFB to apply for Universal Banking license.

- Equitas Small Finance Bank: Strong focus on micro-lending and commercial vehicle finance.

- Ujjivan Small Finance Bank: Known for microfinance roots. Applied for Universal Bank license.

PSL Targets for Primary Urban Coop Banks

Priority Sector loans: 60% of ANBC or CEOBE whichever is higher. (From existing 40% to 60% in phases).

Sub-Target:

- Micro enterprises: 7.5% of ANBC or CEOBE, whichever is higher.

- Weaker Section: 12% of ANBC or CEOBE, whichever is higher (from existing 10% to 12% in phases - 31.03.24-11.5%, 31.3.25 - 11.75%, 31.3.26 - 12%).

- No Agri Target.

UCBs — Phased Stipulated Targets

| FY | Total PS | Micro Enterprises | Advances to Weaker Sections |

|---|---|---|---|

| 2019-20 | 40% | 7.5% | 10.00% |

| 2020-21 | 45% | 7.5% | 11.00% |

| 2021-22 | 50% | 7.5% | 11.50% |

| 2022-23 | 55% | 7.5% | 11.50% |

| 2023-24 | 60% | 7.5% | 11.50% |

| 2024-25 | 65% | 7.5% | 11.75% |

| 2025-26 | 75% | 7.5% | 12.00% |

Quick Notes on ANBC Computation

- If write-offs are made at the Corporate/Head Office level, they must be subtracted from net bank credit.

- Credits written off in priority sector and its sub-sectors should also be deducted based on categories.

- All loans, investments, or other items classified as priority sector should be part of ANBC.

- Small Finance Banks (SFBs) must follow RBI norms from October 06, 2016, especially concerning "grandfathered loans" for ANBC computation.

- For CEOBE calculation, guidelines from the Master Circular on Exposure Norms are to be used.

- UCBs need to adhere to the Master Circular on 'Prudential Norms on Capital Adequacy - UCBs'.

Agriculture

Crop Durations - Vyas Comm

Crop classification

- Crops are either short duration or long duration.

- Short Duration - harvested within 12 months

- Long duration - harvested after 12 months

- Classification of individual crop as short duration or long duration, based on State Level Bankers' Committee decision in each State.

Crop Seasons (Traditional)

- Rabi Season - Oct - May

- Khariff season - May – Oct

Cultures & Revolutions

- Sericulture - Silk Production

- Aquaculture - Shrimp farming, fish production

- Apriculture - Mushroom

- Apiculture - Rearing of Honey bees

- Pisciculture - fish farming

- Olericulture - Vegetable production

- White revolution - Milk Production

- Green Revolution - Crop Production

- Yellow revolution – Oilseeds and Pulses production

- Blue revolution – Pisciculture

Farm Credit - Individual farmers

This category comprises of loans to individual farmers [including Self Help Groups (SHGs) or Joint Liability Groups (JLGs) i.e., groups of individual farmers, provided banks maintain disaggregated data of such loans] and proprietorship firms of farmers, directly engaged in agriculture and allied activities. Such loans will include:

- Crop loans including loans for traditional/non-traditional plantations, horticulture and allied activities.

- Medium and long-term loans for agriculture and allied activities (e.g. purchase of agricultural implements and machinery and developmental loans for allied activities).

- Loans for pre and post-harvest activities viz., spraying, harvesting, grading and transporting of own farm produce.

- Loans to distressed farmers indebted to non-institutional lenders.

- Loans under the Kisan Credit Card Scheme.

- Loans to small and marginal farmers (SMFs) for purchase of land for agricultural purposes.

- Loans against pledge/hypothecation of agricultural produce (including warehouse receipts) for a period not exceeding 12 months subject to a limit up to ₹90 lakh against Negotiable Warehouse Receipt (NWRs)/Electronic Negotiable Warehouse Receipt (eNWRs) and up to ₹60 lakh against warehouse receipts other than NWRs/eNWRs.

- Loans to farmers for installation of stand-alone solar agriculture pumps and for solarisation of grid connected agriculture pumps.

- Loans to farmers for installation of solar power plants on barren/fallow land or in stilt fashion on agriculture land owned by farmer.

Farm Credit - Corporate farmers, FPOs/FPCs

- (a) Aggregate limit of ₹4 crore per borrowing entity for:

- i. Crop loans to farmers (incl. plantations, horticulture, and allied activities).

- ii. Medium and long-term loans for agriculture and allied activities.

- iii. Loans for pre and post-harvest activities.

- (b) Produce Loans: Up to ₹4 crore against NWRs/eNWRs and up to ₹2.5 crore against other warehouse receipts (max 12 months).

- (c) FPOs/FPCs: Loans up to ₹10 crore per borrowing entity undertaking farming with assured marketing.

- (d) Member Produce: Loans up to ₹10 crore for purchase of the produce of members directly engaged in agriculture and allied activities.

NOTE

UCBs are not permitted to lend to co-operatives of farmers._

Agriculture Infrastructure

Loans for agriculture infrastructure will be subject to an aggregate sanctioned limit of ₹100 crore per borrower from the banking system.

Ancillary Services

- i. Agri-clinics and agro business centre scheme of NABARD.

- ii. Start-ups: Loans up to ₹50 crore that are engaged in agriculture and allied services.

- iii. Food and Agro-processing: Loans up to an aggregate sanctioned limit of ₹100 crore per borrower.

- iv. Export credit to the agriculture sector.

- v. RIDF Deposits: Outstanding deposits under RIDF and other eligible funds with NABARD on account of priority sector shortfall.

Eligibility criteria for categorization as lending to Small and Marginal Farmers (SMFs)

- i. Farmers with landholding of up to 1 hectare (Marginal Farmers).

- ii. Farmers with a landholding of more than 1 hectare and up to 2 hectares (Small Farmers).

- iii. Landless agricultural labourers, tenant farmers, oral lessees and share-croppers.

- iv. Self Help Groups (SHGs) or Joint Liability Groups (JLGs).

- v. Loans up to ₹2.5 lakh to individuals solely engaged in allied activities without any accompanying land holding criteria.

- vi. Loans to FPOs/FPCs of individual farmers and co-operatives of farmers directly engaged in agriculture and allied activities where the land-holding share of SMFs is not less than 75 per cent.

Lending by banks to NBFCs and MFIs for on-lending in agriculture

- Bank credit extended to registered NBFC-MFIs and other MFIs (Societies, Trusts etc.) for on-lending to individuals and also to members of SHGs/JLGs will be eligible for categorisation as priority sector advance.

- Bank credit to registered NBFCs (other than MFIs) towards on-lending for ‘term lending’ component under agriculture will be eligible for PSL classification up to ₹10 lakh per borrower. Note: The provisions of para 9.5 shall not be applicable to RRBs, UCBs, SFBs and LABs.

Crop Loans

- KCC is included.

Micro, Small and Medium Enterprises (MSMEs)

As per MSME Development Act 2006 (notified on Oct 02, 2006, and modified w.e.f.1.4.2025).

Factoring transactions pertaining to MSMEs taking place through the Trade Receivables Discounting System (TReDS) shall also be eligible for classification under priority sector.

Overdraft to Pradhan Mantri Jan-Dhan Yojana (PMJDY) account holders as per limits and conditions prescribed by Department of Financial Services, Ministry of Finance from time to time, will qualify as achievement of the target for lending to Micro Enterprises.

Definition:

- Micro enterprises: Investment ≤ ₹2.50 Cr, Turnover ≤ ₹10 Cr.

- Small enterprises: Investment ≤ ₹25 Cr, Turnover ≤ ₹100 Cr.

- Medium enterprises: Investment ≤ ₹125 Cr, Turnover ≤ ₹500 Cr. Note: Value of investment excludes pollution control, R&D, industrial safety devices, land & building, furniture & fittings.

Registration: W.e.f. 1.7.2020, all enterprises are required to register online and obtain 'Udyam Registration Certificate'.

Loans to MSMEs:

- Need Based (Working capital, term loan, non-fund based).

- Composite loan under single window: Max amount is restricted to Rs. 100 lac.

- Loans given under KVI sector: To be classified as loans to micro enterprises.

- Loans up to Rs. 50 Cr to Start-up.

- Collateral Free: Loan up to Rs. 10 lac mandatory no collateral. Up to Rs. 10 cr guaranteed by CGT-MSE.

Housing Loans

Bank loans to Housing sector as per limits prescribed below are eligible for priority sector classification:

i. Loans to individuals for purchase/construction of a dwelling unit per family subject to the following limits:

| Category | Loan Limit | Maximum Cost of Dwelling Unit |

|---|---|---|

| Centres with population of 50 lakh and above | 50 | 63 |

| Centres with population of 10 lakh and above but below 50 lakh | 45 | 57 |

| Centres with population below 10 lakh | 35 | 44 |

ii. Housing loans to banks’ own employees will not be eligible for classification under the priority sector. iii. Housing loans which are backed by long term bonds shall not be classified under priority sector. Investments made by UCBs in bonds issued by NHB/HUDCO on or after April 1, 2007 shall not be eligible.

Loans for repairs to damaged dwelling units shall be eligible for priority sector classification subject to the following limits:

- Centres with population of 50 lakh and above: 15 lakh

- Centres with population of 10 lakh and above but below 50 lakh: 12 lakh

- Centres with population below 10 lakh: 10 lakh

Bank loans to any governmental agency for construction of dwelling units or for slum clearance and rehabilitation of slum dwellers subject to dwelling units with carpet area of not more than 60 sq.m.

Bank loans for affordable housing projects using at least 50% of Floor area ratio / Floor Space Index (FAR/FSI) for dwelling units with carpet area of not more than 60 sq.m.

PM Awas Yojna:

| Segment | Annual Family Income | Loan Amount Eligible for Subsidy | Interest Subsidy | Carpet Area Limit |

|---|---|---|---|---|

| EWS | Up to ₹3 lakh | ₹6 lakh | 6.5% | 30 sq. m. |

| LIG | ₹3-6 lakh | ₹6 lakh | 6.5% | 60 sq. m. |

| MIG-1 | More than ₹6 lakh up to ₹12 lakh | ₹9 lakh | 4% | 160 sq. m. |

| MIG-2 | More than ₹12 lakh up to ₹18 lakh | ₹12 lakh | 3% | 200 sq. m. |

This old PMAY structure is best remembered as higher subsidy for lower-income segments, with EWS and LIG getting the strongest support.

PM Awas Yojna 2.0:

- Eligibility income criteria: EWS (up to 3 lac), LIG (3-6 lac), MIG (6-9 lac).

- Max house cost = 35 lac. Max house loan = 25 lac.

- Interest subsidy 4% on 1st 8 lac loan up to 12 years tenure.

- Max subsidy amount = Rs. 1.80 lac in 5 yearly instalments.

Education Loan

Loans to individuals for educational purposes, including vocational courses, not exceeding ₹25 lakh will be considered as eligible for priority sector classification.

IBA Model Scheme (15.2.21)

- Loan application through: Vidya Laxmi portal.

- Max amount to be classified as PSL: Rs.25 lac.

- Margin: Loan up to Rs.4 lac: Nil. Beyond Rs.4 lac: 5% (India), 15% (Abroad).

- Repayment: 15 years (EMI).

- Moratorium: Course + 1 year (or 6 months after getting job).

- Collateral:

- Up to Rs.4 lac: No security.

- Above Rs. 4 lac to Rs.7.50 lac: 3rd party guarantee and NCGTC guarantee.

- Above 7.5 lac: Bank discretion.

- NCGTC Guarantee: Eligible loans up to Rs.7.50 lac. Cover 75%. Fee 0.5%.

Education Loans – Interest Subsidy

- Central Sector Interest subsidy scheme: For EWS (Family Income < Rs.4.50 lac). Available for loans up to Rs. 10 lac.

- Ambedkar Interest Subsidy for EBC/OBC: Overseas Masters/PhD. EBC (< 5 lac), OBC (< 8 lac).

Export Credit

Export credit includes pre-shipment and post-shipment export credit (excluding off-balance sheet items).

- Export credit to agriculture and MSME shall be eligible for classification as PSL in the respective categories.

- Export Credit (other than that classified under agriculture and MSME) shall be eligible for classification as PSL as per table:

| Bank Type | Target |

|---|---|

| Domestic banks / WoS of Foreign banks / SFBs / UCBs | Incremental export credit over corresponding date of the preceding year, up to2 per cent of ANBC or CEOBSE whichever is higher, subject to a sanctioned limit of up to ₹50 crore per borrower. |

| Foreign banks with 20 branches and above | Incremental export credit over corresponding date of the preceding year, up to 2 percent of ANBC or CEOBSE whichever is higher. |

| Foreign banks with less than 20 branches | Export credit up to32 per cent of ANBC or CEOBSE whichever is higher. |

Social Infrastructure

Bank loans to social infrastructure sector as per limits prescribed below are eligible for priority sector classification.

- Loan up to Rs. 8 crore per project for building social infrastructure in Tier Il to Tier VI places (school, drinking water, sanitation).

- Health care facilities (Ayushman Bharat): Loans up to a limit of Rs. 12 crore per borrower in Tier II to Tier VI centres.

- In case of UCBs, the above limits are applicable only in centres having a population of less than one lakh.

Renewable Energy

Loans up to Rs. 35 cr per borrower for solar power generators, bio-mass, wind mills, micro-hydel, street lighting etc. For individual household the loan limit is Rs. 10 lac.

Other Priority Sector

- Loans directly to individuals and members of SHG / JLG satisfying micro finance criteria (AFI up to Rs. 3 lac).

- Loans up to Rs.2 lac to SHG/JLG for non-agriculture and non- MSME activities.

- Loans up to Rs. 1,00,000 to distressed poor (other than farmer) for debt swap.

- Loans are eligible for State Sponsored Organizations serving Scheduled Castes/Scheduled Tribes.

- Loans up to 50 crore to Start-ups, engaged in activities other than Agriculture or MSME.

Miscellaneous Aspects

Loan application disposal period

At discretion of banks. Rejection: Reasons in writing to be given to borrower. SC/ST loan application rejection not at branch level but next higher authority.

Data on Priority Sector Lending

Information to be sent to RBI on quarterly and yearly basis within 15 days and one month respectively. (means for quarterly within 15 days after the end of quarter, and year end within one month of year end).

Loans up to Rs. 50,000-Relaxation

- No service fee.

- No processing fee.

- No inspection charges.

- No penal interest.

- No margin and no Collateral security.

Restriction on loans for on-lending purpose

Bank credit to registered NBFC-MFls and other MFIs and NBFCs for on-lending:

- Agriculture: On-lending by NBFCs for 'Term lending' component under Agriculture will be allowed up to 10 lakh per borrower.

- Micro & Small enterprises: On-lending by NBFC will be allowed up to Rs 20 lakh per borrower.

- HFC approved by NHB: On lending by HFC up to Rs.20 lac per borrower.

- Overall ceiling: Bank credit to NBFCs (including HFCs) for on-lending will be allowed up to an overall limit of 5% of individual bank's total PS lending.

Investments - Part of PS

- Investments made by a bank in securitised assets representing priority sector advances.

- Purchase of priority sector advances from other banks (Direct Assignment).

- Investments in inter-bank participation certificates (IBPCs).

- Investment in PS Lending Certificates (PSLCs). Min size 25 lac. Trading through E-Kuber.

Targets for Minority Communities

15% of priority sector loans should be given to Minority Community. Minority Communities include:

- Muslims

- Sikhs

- Christians

- Buddhist

- Jains

- Zoroastrians (Parsi)

Adjustments for weights in PSL Achievement

- To address regional disparities, it was decided to rank districts on the basis of per capita credit flow.

- 125% Weight: For districts with low per capita PSL (< ₹9,000).

- 90% Weight: For districts with high per capita PSL (> ₹42,000).

- Valid up to FY 2026-27.

Non-Achievement of Priority Sector Targets

- Banks not meeting priority sector lending targets contribute to the Rural Infrastructure Development Fund (RIDF) and other related funds.

- These funds are managed by institutions like NABARD, NHB, SIDBI, and MUDRA Ltd.

- RBI sets the interest rates, deposit tenure, and other terms for these deposits.

- The method to determine the shortfall is detailed in the RBI's Master Direction on Priority Sector Lending.

Common Guidelines for Priority Sector Loans

| Guideline | Detail |

|---|---|

| Rate of Interest | At discretion; guidelines for priority sector applicable |

| Service Charges | As applicable; the third-party charges to be reasonable |

| Insurance | Fire, theft, etc.; all insurance costs at bank's cost unless specified |

| Security | As per approved guidelines/scheme |

| Documentation | Must be available for inspection; maintain records |

| Receipt for applications | Bank should provide a receipt for loan application; acknowledgement within 1 week in rural areas |

| No duplicate receipt | For gold/silver articles pledged |

Other Modes of Lending to Priority Sectors

Investments in Securitised Notes (RBI 21.05.12)

- Banks can classify investments in certain securitized assets under the priority sector.

- Banks classified as originators are not permitted to classify their securitized assets back as priority sector loans.

- Interest charged to borrowers should not surpass the bank's EBLR/MCLR plus appropriate spread.

- Loans against gold jewellery and gold coins do not qualify as priority sector advances.

- Guidelines similar to those for securitized assets apply.

- Reporting about loans should be on disbursement basis, not sanction basis.

Inter Bank Participation Certificates (IBPCs)

- Eligible for classification under priority sectors if they meet RBI guidelines.

- 'Export Credit' related IBPCs have specific classification rules.

- RRBs can issue IBPCs under specific conditions.

- Not applicable to UCBs.

Priority Sector Lending Certificates (PSLCs)

- Banks can classify purchased PSLCs under the priority sector if they align with RBI guidelines.

- Minimum size: ₹25 lakh. Trading through E-Kuber platform.

Co-ordination Between Banks and NBFCs

Two approved methods for priority sector lending via NBFCs:

- Credit to NBFCs for on-lending: Max 5% of total quarterly average PSL.

- Co-origination of loans: Combined credit contribution by bank and NBFC.

Interest Subvention Schemes

Interest Subvention Scheme for Crop Loans

- Farmers can access short-term credit at 7% interest.

- The principal amount has an upper cap of ₹3 lakh.

- The government provides subvention to banks to bridge the gap between commercial lending rate and 7%.

Interest Subvention Under NRLM Scheme

- The scheme offers a subvention on the difference between the charged rate and 7%.

- Specifically targeted at women SHGs.

- Aims to provide affordable credit to women self-help groups under the National Rural Livelihood Mission.

Summary Cheat Sheet

Target Summary (by Bank Type)

| Categories | Domestic Commercial Banks (excl. RRBs & SFBs) & Foreign Banks (≥20 branches) | Foreign Banks (<20 branches) | Regional Rural Banks (RRBs) | Small Finance Banks (SFBs) |

|---|---|---|---|---|

| Total Priority Sector | 40% of ANBC or CEOBSE | 40% of ANBC or CEOBSE (Max 32% Export, Min 8% Others) | 75% of ANBC or CEOBSE (Max 15% to Med/Soc Infra/RE) | 60% of ANBC + CEOBSE |

| Agriculture | 18% (14% NCF, 10% SMF) | Not applicable | 18% (14% NCF, 10% SMF) | 18% (14% NCF, 10% SMF) |

| Micro Enterprises | 7.5% | Not applicable | 7.5% | 7.5% |

| Weaker Sections | 12% | Not applicable | 15% | 12% |

Quick Reference: New Limits & Criteria

| Particulars | New Limit / Criteria (from April 1, 2025) |

|---|---|

| Overall PSL Target | Domestic/Foreign (≥20): 40% | RRBs: 75% | SFBs/UCBs: 60% |

| Agriculture Credit Limits | Individual: ₹90 lakh (NWR/eNWR) / ₹60 lakh (Others) | Corporate: ₹4 crore (NWR/eNWR) / ₹2.5 crore (Others) |

| FPO / FPC Loans | ₹10 crore per entity (farming with assured marketing) |

| Agro & Food Processing | ₹100 crore per borrower |

| Start-up Loans | Agri/MSME: ₹50 crore | Other: ₹50 crore |

| Housing (Metros) | Loan: ₹50 lakh (Cost ₹63L) | Repairs: ₹15 lakh |

| Housing (Other centres) | Loan: ₹35 lakh (Cost ₹45L) | Repairs: ₹10 lakh |

| Education Loans | ₹25 lakh (Standard application: Vidya Laxmi portal) |

| Social Infrastructure | Schools/Sanitation: ₹8 crore | Health Care: ₹12 crore |

| Renewable Energy | Projects: ₹35 crore | Individual households: ₹10 lakh |

| Small Finance Banks (SFBs) | Total PSL: 60% (Sub-targets: Agri 18%, Micro 7.5%, Weaker 12%) |

| Urban Co-operative Banks | Total PSL: 60% (Sub-targets: Micro 7.5%, Weaker 12%) |

Detailed Concept Breakdown

| Concept / Topic | Key Details / Explanation |

|---|---|

| Applicability | Applies to Commercial Banks (RRB, SFB, LAB) and Primary (Urban) Co-operative Banks (UCB). |

| Target Base | PSL targets are calculated as a percentage of ANBC (Adjusted Net Bank Credit) or CEOBE (Credit Equivalent of Off-Balance Sheet Exposure), whichever is higher. |

| Small and Marginal Farmers | Marginal: Land up to 1 hectare. Small: Above 1 hectare up to 2 hectares. |

| Micro Enterprises | Definition: Investment ≤ ₹2.50 crore AND Turnover ≤ ₹10 crore. |

| Weaker Sections | Includes SMFs, SC/ST, Women (up to ₹2L), Transgenders, SHGs/JLGs, and Jan Dhan OD (up to ₹10,000). |

| Regional Weighting | High weight (125%) for low-credit districts (< ₹9,000 per capita); Low weight (90%) for high-credit districts (> ₹42,000). |

| UCBs PS Target (Phased) | 40% (FY19-20) → 75% (FY25-26) in phases |

| Non-Achievement | Shortfall deposited in RIDF; managed by NABARD, NHB, SIDBI, MUDRA Ltd |

| TReDS | Factoring via TReDS eligible for MSME PSL classification |

| PMJDY Overdraft | Qualifies as Micro Enterprise target achievement |

| Gold Jewellery Loans | Do NOT qualify as priority sector advances |

| Interest Cap (Securitised) | Should not surpass EBLR/MCLR + spread |

| Reporting Basis | Disbursement-based, not sanction-based |

| IBPCs | Eligible for PSL; Export Credit IBPCs have specific rules; not for UCBs |

| PSLCs | Min ₹25 lakh; traded on E-Kuber |

| NBFC Co-ordination | On-lending: max 5% of quarterly avg PSL; or co-origination |

| Crop Loan Subvention | Short-term credit at 7%; max ₹3 lakh principal |

| NRLM Subvention | Difference between charged rate & 7%; for women SHGs |

| State Sponsored Orgs | Loans eligible for SC/ST serving organizations under "Others" |

| UCBs Social Infra | Limits applicable only in centres with population < 1 lakh |

Lesson Doubts

Ask questions, get expert answers