🛡️ Crop & Livestock Insurance Schemes

Complete guide to CCIS, NAIS, MNAIS, PMFBY, WBCIS, RWBCIS, UPIS, CPIS, and Livestock Insurance -- evolution, premium rates, coverage, and exam-focused comparisons.

Why Crop Insurance Matters

A groundnut farmer in Anantapur (Andhra Pradesh) invests Rs 30,000 per hectare on seeds, fertilizer, and labour. A sudden drought wipes out the entire crop. Without insurance, the farmer falls into a debt trap. Crop insurance ensures that even when nature fails, the farmer receives compensation to survive and sow again next season.

India's journey toward comprehensive agricultural insurance spans over five decades, with each new scheme addressing the shortcomings of its predecessor.

NOTE

Timeline of Crop Insurance in India: GIC Pilot (1973) → Area-based Pilot (1979) → CCIS (1985) → NAIS/RKBY (Rabi 1999-2000) → MNAIS (2010-11) → PMFBY & RWBCIS (Kharif 2016)

Historical Evolution

Early Experiments (1970-1984)

| Year | Event | Significance |

|---|---|---|

| 1970 | Dharamnarain Committee appointed | Concluded India lacked infrastructure for nationwide crop insurance |

| 1970s | Prof. V.M. Dandekar advocated for crop insurance | Kept the idea alive in policy discussions |

| 1973 | GIC (General Insurance Corporation) established | Set up under the General Insurance Business (Nationalisation) Act, 1972, with four subsidiary companies |

| 1973 | GIC launched pilot crop insurance in Gujarat | Only H4 cotton was covered; later extended to West Bengal, Tamil Nadu, and Andhra Pradesh (operational till 1979, except 1977) |

| 1979 | Area-based crop insurance pilot by GIC | If actual average yield fell below guaranteed yield, all insured farmer-borrowers in the area received indemnity |

Agricultural example: In the 1979 area-based pilot, if the average cotton yield in a selected block of Gujarat fell below the guaranteed level, every insured cotton farmer in that block received compensation -- regardless of individual farm performance.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Why Crop Insurance Matters

A groundnut farmer in Anantapur (Andhra Pradesh) invests Rs 30,000 per hectare on seeds, fertilizer, and labour. A sudden drought wipes out the entire crop. Without insurance, the farmer falls into a debt trap. Crop insurance ensures that even when nature fails, the farmer receives compensation to survive and sow again next season.

India's journey toward comprehensive agricultural insurance spans over five decades, with each new scheme addressing the shortcomings of its predecessor.

NOTE

Timeline of Crop Insurance in India: GIC Pilot (1973) → Area-based Pilot (1979) → CCIS (1985) → NAIS/RKBY (Rabi 1999-2000) → MNAIS (2010-11) → PMFBY & RWBCIS (Kharif 2016)

Historical Evolution

Early Experiments (1970-1984)

| Year | Event | Significance |

|---|---|---|

| 1970 | Dharamnarain Committee appointed | Concluded India lacked infrastructure for nationwide crop insurance |

| 1970s | Prof. V.M. Dandekar advocated for crop insurance | Kept the idea alive in policy discussions |

| 1973 | GIC (General Insurance Corporation) established | Set up under the General Insurance Business (Nationalisation) Act, 1972, with four subsidiary companies |

| 1973 | GIC launched pilot crop insurance in Gujarat | Only H4 cotton was covered; later extended to West Bengal, Tamil Nadu, and Andhra Pradesh (operational till 1979, except 1977) |

| 1979 | Area-based crop insurance pilot by GIC | If actual average yield fell below guaranteed yield, all insured farmer-borrowers in the area received indemnity |

Agricultural example: In the 1979 area-based pilot, if the average cotton yield in a selected block of Gujarat fell below the guaranteed level, every insured cotton farmer in that block received compensation -- regardless of individual farm performance.

Key features of the 1979 pilot:

- Sum assured: 100% of crop loan

- Indemnity ceiling: Rs 5,000 (dryland), Rs 10,000 (irrigated)

- Implemented by 12 states up to 1984

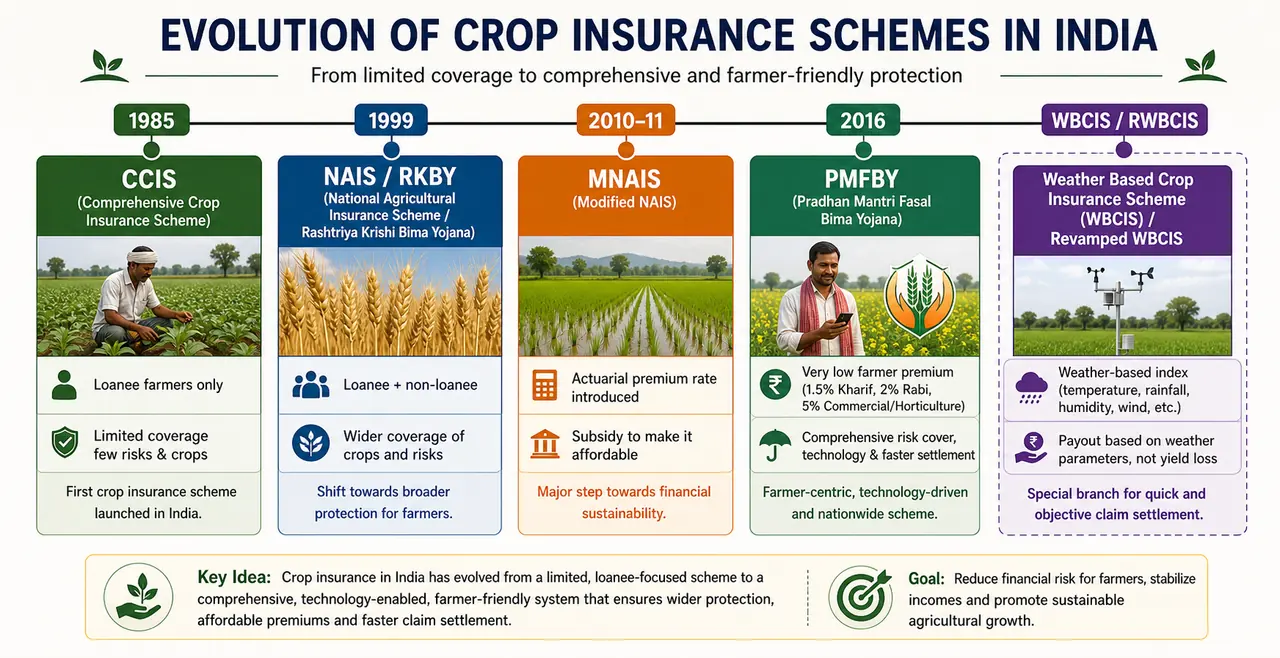

Comprehensive Crop Insurance Scheme (CCIS) -- 1985

India's first nationwide crop insurance scheme, introduced by GIC based on the area approach.

| Feature | Detail |

|---|---|

| Year | 1985 |

| Implementing agency | GIC |

| Approach | Area-based |

| Coverage | Loanee farmers only (farmer-borrowers) |

| Crops covered | Cereals (rice, wheat), millets, oilseeds, pulses |

| Sum insured | 150% of crop loan |

| Premium -- rice, wheat, millets | 2% of sum insured |

| Premium -- oilseeds, pulses | 1% of sum insured |

| Threshold yield | 80% of average annual yield over previous 5 years |

| Yield data method | Crop Cutting Experiments (CCEs) |

Indemnity formula:

Indemnity = (Shortfall in Yield / Threshold Yield) x Sum Insured

Agricultural example: If the threshold yield for wheat in a block is 30 quintals/ha and actual yield is only 15 quintals/ha, the shortfall is 50%. A farmer with sum insured of Rs 45,000 receives Rs 22,500.

Limitations of CCIS:

- Restricted to loanee farmers only -- excluded the majority who did not take institutional loans

- The 80% threshold meant claims triggered only when yields fell significantly below average

TIP

Exam mnemonic -- CCIS "152": Sum insured = 150% of crop loan; Premium = 2% for cereals, 1% for oilseeds/pulses.

National Agricultural Insurance Scheme (NAIS) -- 1999

Also called Rashtriya Krishi Bima Yojana (RKBY). Replaced CCIS with expanded coverage.

| Feature | CCIS (1985) | NAIS (1999) |

|---|---|---|

| First season | 1985 | Rabi 1999-2000 |

| Implementing agency | GIC | GIC → AIC (from 1 April 2003) |

| Crops | Cereals, millets, oilseeds, pulses | Added commercial and horticultural crops |

| Farmer coverage | Loanee only | Compulsory for loanee, optional for non-loanee |

| Sum insured | 150% of crop loan | Up to 150% of average yield value |

| Premium sharing | -- | 50:50 between Centre and State |

| Yield estimation | CCEs | CCEs or Small Area Crop Estimation |

AIC (Agriculture Insurance Company) commenced operations on 1 April 2003, taking over NAIS implementation from GIC as a specialized agricultural insurance company.

Modified NAIS (MNAIS) -- 2010-11

An improved version of NAIS incorporating actuarial premium rates (market-based, calculated by insurance experts) and faster claim settlement. Operated alongside NAIS rather than replacing it.

- Launched in 2010-11

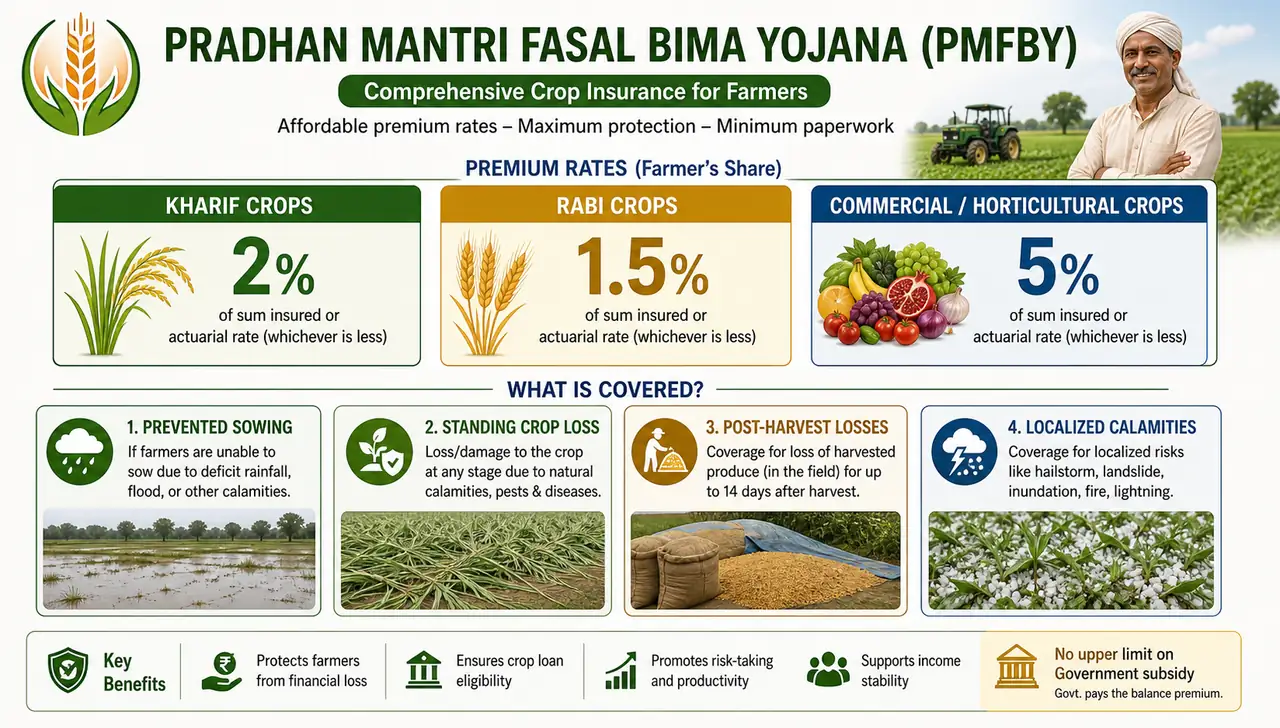

Pradhan Mantri Fasal Bima Yojana (PMFBY) -- 2016

The current flagship crop insurance scheme. Designed under the "One Nation -- One Scheme" principle, replacing both NAIS and MNAIS.

IMPORTANT

PMFBY Key Facts:

- Launched: 13 January 2016; implemented from Kharif 2016

- Premium: Kharif = 2%, Rabi = 1.5%, Annual commercial/horticultural = 5%

- No upper limit on Government subsidy

- Made voluntary from Kharif 2020

- Threshold yield: Best 5 out of 7 years moving average

Objectives

- Provide insurance coverage against crop failure from natural calamities, pests, and diseases

- Stabilize farmer income to ensure continuance in farming

- Encourage adoption of modern agricultural practices (farmers take more risk when insured)

- Ensure continued credit flow to agriculture (banks lend more readily when crops are insured)

Premium Rates

| Season/Crop Type | Farmer's Premium | Balance Premium |

|---|---|---|

| Kharif crops | 2% of sum insured | Borne by Government |

| Rabi crops | 1.5% of sum insured | Borne by Government |

| Annual commercial/horticultural crops | 5% of sum insured | Borne by Government |

- No upper limit on Government subsidy -- even if the balance premium is 90%, the Government bears it fully.

- Premium subsidy is shared 50:50 by Centre and State for most states and 90:10 for North Eastern and Himalayan states.

- Previous schemes had premium capping that reduced farmer payouts. PMFBY removed this cap entirely.

- Estimated 75-80% of the total premium is subsidized by the Government.

Agricultural example: A soybean farmer in Maharashtra insures 2 hectares with a sum insured of Rs 50,000/ha (total Rs 1,00,000). His premium is only Rs 2,000 (2% of Rs 1,00,000). If the actuarial premium is Rs 15,000, the Government pays the remaining Rs 13,000.

TIP

Exam mnemonic -- "2-1.5-5": Kharif 2%, Rabi 1.5%, Commercial 5%. Remember: Kharif is riskier (monsoon), so premium is slightly higher.

Farmers Covered

- All farmers growing notified crops in notified areas with insurable interest

- Voluntary for all farmers from Kharif 2020 (previously compulsory for loanee farmers)

- Target: Covering 50% of gross cropped area; achieved 30% by 2019-20

Unit of Insurance

| Risk Type | Unit of Insurance | Example |

|---|---|---|

| Widespread calamity (yield loss) | Village/Village Panchayat level for major crops | Drought affecting all rice farms in a panchayat |

| Localized calamity | Individual farm level | Hailstorm damaging one farmer's orchard |

| Post-harvest losses | Individual farm level | Unseasonal rain spoiling wheat left to dry in field |

Moving to village/panchayat level (from block/taluka in NAIS) ensures more accurate loss assessment.

- For a crop to be "major" at a given level, its sown area must be at least 25% of Gross Cropped Area in that District/Taluka.

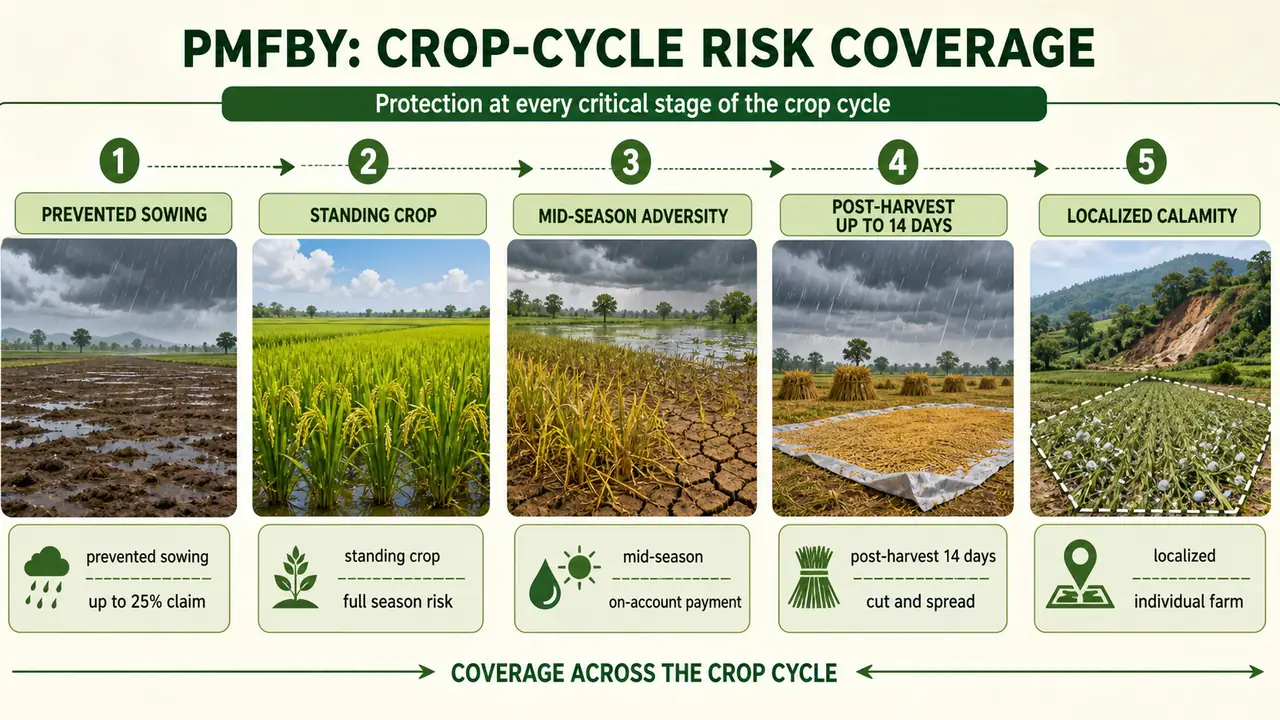

Risks Covered -- Comprehensive Protection

PMFBY covers the entire crop cycle from pre-sowing to post-harvest:

| Risk Category | Coverage | Key Detail |

|---|---|---|

| Prevented sowing | Up to 25% of sum insured | When adverse weather prevents sowing despite expenditure incurred |

| Standing crop losses | Full sum insured | Natural fire, lightning, storm, hailstorm, cyclone, flood, drought, pests, diseases |

| Mid-season adversity | On-account payment up to 25% of likely claims | When expected yield is less than 50% of normal yield |

| Post-harvest losses | Up to 14 days after harvest | For crops kept in "cut and spread" condition to dry |

| Localized calamities | Individual farm assessment | Hailstorm, landslide, inundation affecting isolated farms |

Agricultural example: A paddy farmer in Odisha harvests in November but leaves the cut paddy in the field for 10 days to dry. An unseasonal cyclonic rain on day 12 damages the crop. PMFBY covers this post-harvest loss since it occurred within the 14-day window.

Sum Insured and Claim Formula

The dedicated PMFBY scheme lesson treats the Scale of Finance as the base for insurance coverage:

Sum Insured = Scale of Finance × Area under Cultivation

The scheme claim is calculated using the standard yield shortfall formula:

Claim = (Threshold Yield - Actual Yield) / Threshold Yield × Sum Insured

Where:

- Threshold Yield = moving average of the best 5 out of past 7 years × indemnity level

- Indemnity level depends on risk category:

- 70% for high risk

- 80% for medium risk

- 90% for low risk

Exclusions and Intimation Window

- Excluded risks include war, nuclear risk, malicious damage, and other preventable risks

- For localized calamities and post-harvest losses, the farmer must intimate the loss within 72 hours

- For widespread calamities, settlement is based on Crop Cutting Experiments (CCEs) and notified-area yield data

Implementation

- Implemented by Agricultural Insurance Company (AIC) and other empaneled private general insurance companies (total 18 companies including 5 government)

- Selection of implementing agency by State Government through competitive bidding

- Under overall guidance of Department of Agriculture, Cooperation & Farmers Welfare

- State govt/UT must provide 10 years of historical yield data for threshold yield calculation

Revised Operational Guidelines (from 1 October 2018)

Key improvements addressing implementation challenges:

| Revision | Detail |

|---|---|

| Penalty for delayed claims | Insurance companies pay 12% interest for delays beyond 2 months; States pay 12% for subsidy delays beyond 3 months |

| Threshold yield calculation | Moving average of best 5 out of 7 years (excludes 2 worst/calamity years) |

| Perennial horticultural crops | Included on pilot basis (mango, coconut, apple, citrus) |

| Post-harvest coverage expanded | Now includes hailstorms besides unseasonal/cyclonic rainfall |

| Localized calamities expanded | Added cloud burst and natural fire |

| Wild animal damage | Covered on pilot basis (additional cost borne by State) |

| Mandatory Aadhaar | For de-duplication of beneficiaries |

| Claim intimation time | Increased to 72 hours (from 48 hours) |

| Crop name change | Allowed up to 2 days before cut-off (was 1 month before) |

| Awareness expenditure | 0.5% of gross premium per company per season |

| Remote Sensing Technology | Used for risk classification and clustering |

TIP

Exam Key (NABARD 2020 Mains): Threshold yield = Moving average of best 5 out of 7 years -- average of last 7 years minus two notified calamity years.

Comparison with Previous Schemes

PMFBY Coverage & Technology

| Parameter | Detail |

|---|---|

| Farmers covered (2023-24) | 4.19 crore |

| Voluntary status | Made voluntary for loanee farmers from Kharif 2020 |

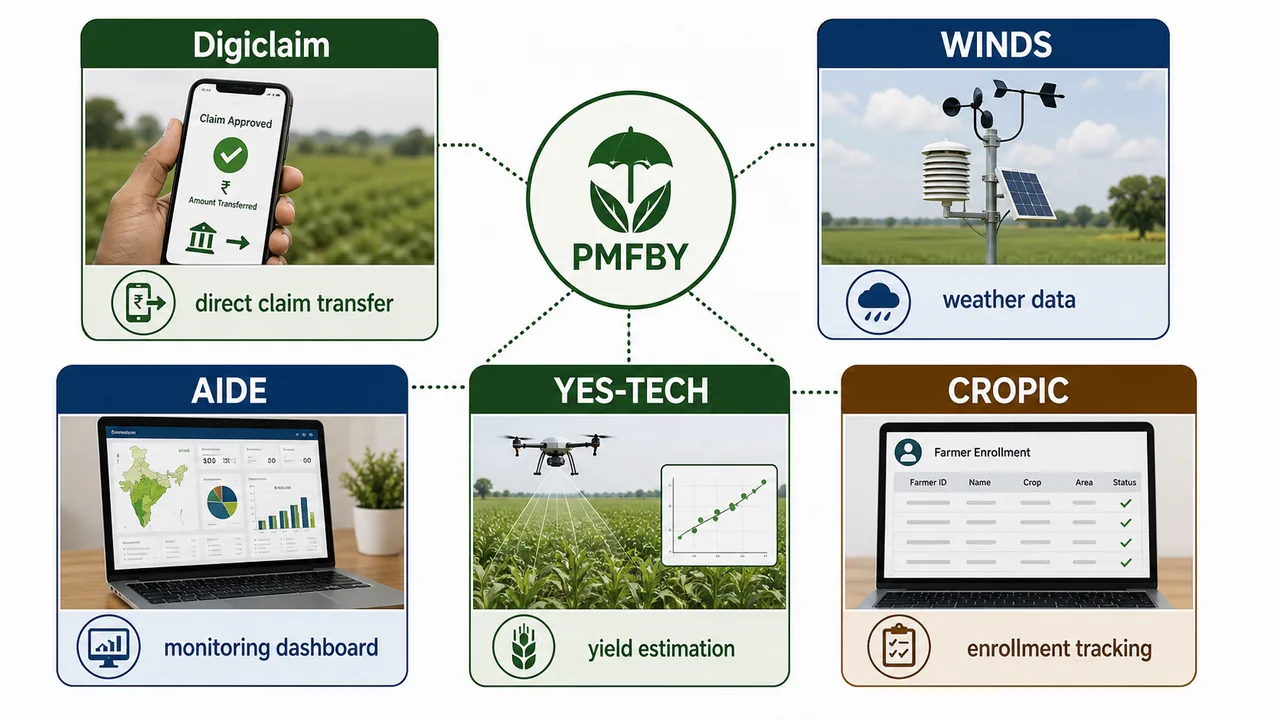

Technology Initiatives under PMFBY

| Technology | Full Form | Purpose |

|---|---|---|

| Digiclaim | Digital Claims Module | Faster claim settlement directly to farmer accounts |

| WINDS | Weather Information Network Data Systems | Real-time weather data for crop loss assessment |

| AIDE | Agriculture Insurance Dashboard for Everyone | Transparent dashboard for monitoring |

| YES-TECH | Yield Estimation System using Technology | Technology-based yield estimation |

| CROPIC | Crop Insurance Portal | Online platform for enrollment & tracking |

TIP

Exam Tip: PMFBY tech acronyms are frequently asked. Remember: D-W-A-Y-C (Digiclaim, WINDS, AIDE, YES-TECH, CROPIC).

Operational Strengthening

- Meri Policy Mere Haath supports doorstep distribution of crop insurance policy documents

- Smartphones, drones, GPS, and remote sensing are increasingly used for better yield estimation and faster settlement

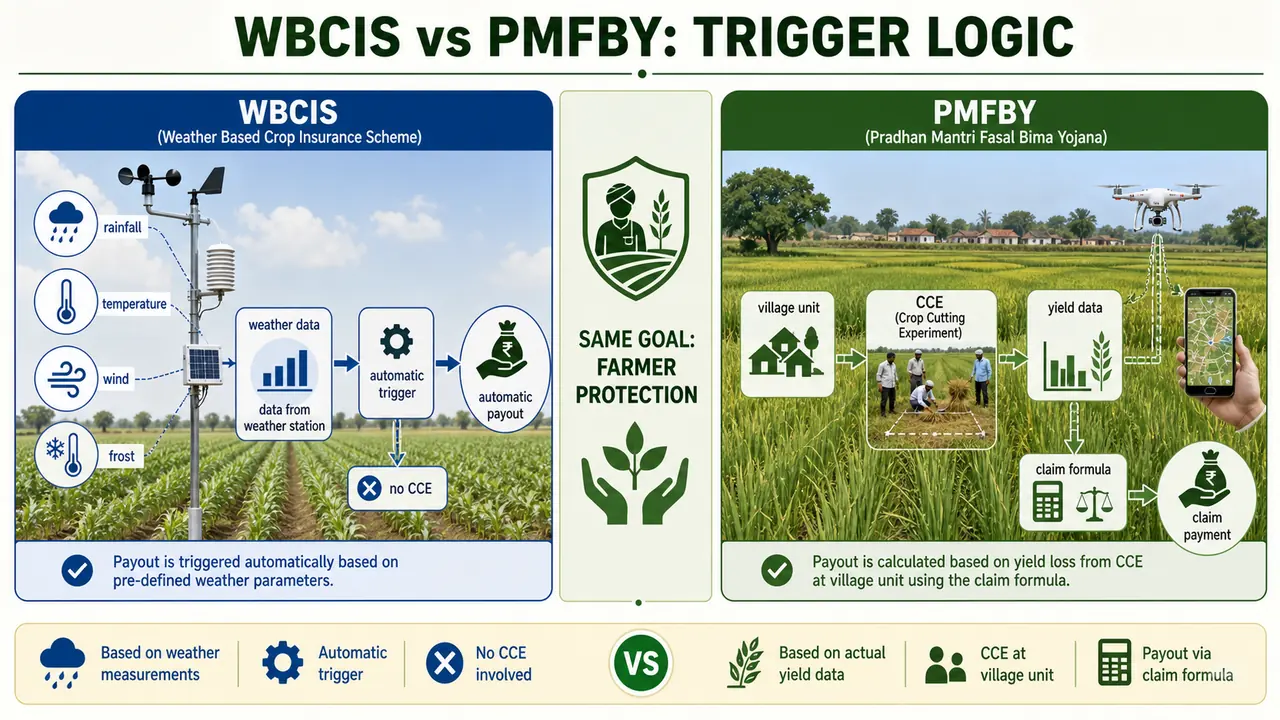

Weather Based Crop Insurance Scheme (WBCIS) -- 2007

WBCIS takes a fundamentally different approach: instead of measuring actual crop yields (time-consuming), it uses weather parameters as proxies for crop loss. If weather deviates from thresholds, payouts are automatic.

| Feature | Detail |

|---|---|

| Started | 2007 |

| Type | Parametric insurance (based on weather data, not yield data) |

| Crops | Major food crops (cereals, millets, pulses), oilseeds, commercial/horticultural crops |

| Farmer coverage | Compulsory for loanee (SAO loan holders), optional for non-loanee |

| Risk period | Sowing to maturity |

| Choice | Non-loanee farmers can choose between WBCIS and PMFBY |

Weather Perils Covered

- Rainfall: Deficit, excess, unseasonal, dry spells, dry days

- Temperature: High (heat waves), low (frost)

- Relative humidity

- Wind speed

- Combinations of the above

- Add-on: Hailstorms, cloud-burst (for farmers with normal WBCIS coverage)

Agricultural example: A mustard farmer in Rajasthan does not insure under PMFBY. A severe frost destroys 60% of the crop. Under WBCIS, the weather station records temperatures below the frost threshold, and the payout is automatically triggered -- no crop cutting experiment needed.

TIP

WBCIS vs PMFBY: WBCIS pays based on weather data (fast, automatic). PMFBY pays based on yield data (accurate but slow, requires CCEs).

Restructured WBCIS (RWBCIS) -- 2016

Updated version of WBCIS, aligned with PMFBY's premium structure for uniformity.

- Launched 18 February 2016

- 12 states implemented in Kharif 2016; 9 states in Rabi 2016-17

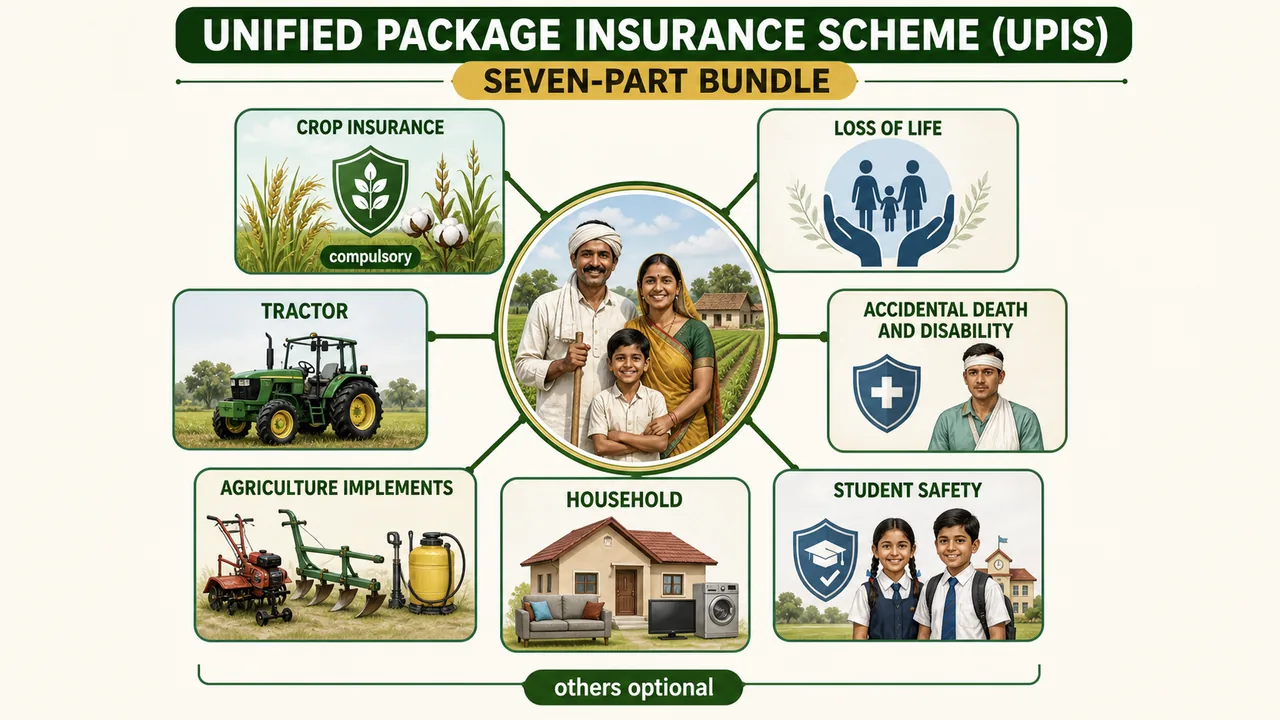

Unified Package Insurance Scheme (UPIS) -- 2016

An innovative approach bundling seven types of insurance into one comprehensive package:

| Section | Coverage | Related Scheme |

|---|---|---|

| 1. Crop insurance | Crop loss | PMFBY/WBCIS (compulsory) |

| 2. Loss of life | Death | PMJJBY (Rs 330/year) |

| 3. Accidental death & disability | Accident | PMSBY (Rs 12/year) |

| 4. Student safety | Student accidents | -- |

| 5. Household | House damage | -- |

| 6. Agriculture implements | Equipment damage | -- |

| 7. Tractor | Tractor damage/theft | -- |

- Approved for 45 districts on pilot basis from Kharif 2016

- Crop insurance section is compulsory; others are optional

Agricultural example: A farmer in Odisha enrolls in UPIS. During a cyclone, his paddy crop is destroyed, his tractor is damaged, and his house roof is blown off. Instead of filing with three different insurers, UPIS covers all three losses under one policy.

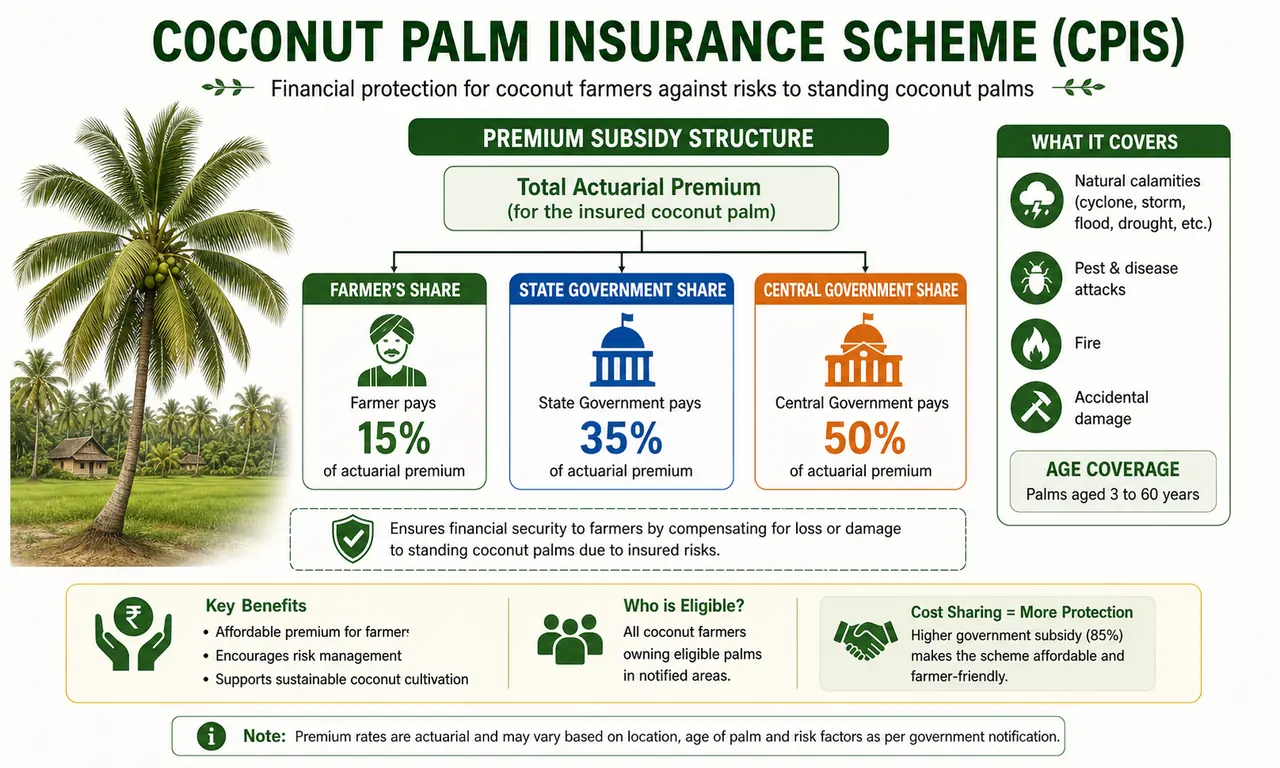

Coconut Palm Insurance Scheme (CPIS) -- 2009-10

A specialized scheme for coconut palms, a major commercial crop in coastal states.

NOTE

CPIS (exams 2017): Economic life of coconut palm = 60 years. Dwarf/Hybrid covered from 4-60 years, Tall variety from 7-60 years. Minimum 5 palms required.

| Feature | Detail |

|---|---|

| Implemented since | 2009-10 |

| Dwarf & Hybrid coverage | 4-60 years (yield from 4th year) |

| Tall variety coverage | 7-60 years (yield from 7th year) |

| Economic life | 60 years |

| Minimum palms | 5 healthy nut-bearing palms in contiguous plot |

| Exclusions | Unhealthy and senile palms |

Premium Subsidy Structure

| Payer | Share (Normal) | Share (if State does not participate) |

|---|---|---|

| Coconut Development Board (CDB) | 50% | 50% |

| State Government | 25% | 0% |

| Farmer | 25% | 50% |

| Minimum farmer contribution | 10% (even if a planters' association pays on behalf) | 10% |

Livestock Insurance Scheme -- 2008-09

Livestock represents both a productive asset and a store of wealth for rural households. A single dairy animal can be a significant portion of a family's total assets.

| Feature | Detail |

|---|---|

| Pilot phase | 2005-06, 2006-07 (10th Plan), 2007-08 (11th Plan) in 100 districts |

| Regular implementation | From 2008-09 in 100 newly selected districts |

| Premium subsidy | 50% |

| Maximum animals per beneficiary | 2 animals |

| Maximum policy period | 3 years |

Agricultural example: A dairy farmer in Karnataka insures her 2 crossbred cows valued at Rs 60,000 each. She pays only 50% of the premium. When one cow dies due to disease, she receives the insured value, enabling her to buy a replacement animal and continue her dairy business.

ACABC (Agri-Clinics and Agri-Business Centres)

ACABC provides self-employment to agriculture graduates while extending expert advisory services to farmers.

| Feature | Detail |

|---|---|

| Nodal agency | MANAGE (National Institute of Agricultural Extension Management), Hyderabad |

| Training duration | 60 days (45 days classroom + 15 days field) |

| Eligible | Agriculture graduates, diploma holders |

| Individual loan | Up to Rs 20 lakh (Rs 25 lakh for hilly/tribal areas) |

| Group loan | Group of 5 graduates → up to Rs 100 lakh |

| Subsidy | 36% of project cost (44% for SC/ST/women/NE/hilly areas) |

TIP

Exam trigger: ACABC = MANAGE + 60 days + Rs 100 lakh (group of 5). Nodal agency is always MANAGE, Hyderabad.

Master Comparison -- All Insurance Schemes

| Feature | CCIS (1985) | NAIS (1999) | PMFBY (2016) | WBCIS (2007) |

|---|---|---|---|---|

| Approach | Area-based | Area-based | Area-based (village level) | Weather-parameter based |

| Farmer coverage | Loanee only | Compulsory loanee, optional non-loanee | Voluntary from Kharif 2020 | Compulsory loanee, optional non-loanee |

| Premium (Kharif) | 2% | Actuarial | 2% | Actuarial |

| Premium (Rabi) | 1% | Actuarial | 1.5% | Actuarial |

| Govt subsidy cap | Yes | Yes | No cap | Aligned with PMFBY |

| Crops | Cereals, millets, oilseeds, pulses | Added commercial/horticultural | All notified crops | All notified crops |

| Post-harvest coverage | No | No | Yes (14 days) | No |

| Prevented sowing | No | No | Yes (25% of SI) | No |

| Technology use | CCEs only | CCEs | CCEs + drones, satellites, smartphones | Automatic weather stations |

| Claim settlement | Slow | Slow | 12% penalty for delays | Fast (automatic) |

Summary Cheat Sheet

| Topic | Key Fact | Exam Tag |

|---|---|---|

| Dharamnarain Committee | 1970, ruled out crop insurance feasibility | -- |

| GIC established | 1973 | -- |

| CCIS launched | 1985, area approach, loanee farmers only | -- |

| CCIS threshold yield | 80% of 5-year average | -- |

| NAIS/RKBY launched | Rabi 1999-2000 | -- |

| AIC commenced operations | 1 April 2003 | -- |

| MNAIS launched | 2010-11 | -- |

| WBCIS started | 2007, parametric/weather-based | -- |

| PMFBY launched | Kharif 2016 | Exams |

| PMFBY premium | K: 2%, R: 1.5%, Commercial: 5% | Exams |

| PMFBY made voluntary | Kharif 2020 | -- |

| Threshold yield (revised) | Best 5 out of 7 years | NABARD 2020 Mains |

| Post-harvest coverage | 14 days | -- |

| Penalty for delayed claims | 12% interest | -- |

| RWBCIS launched | 18 February 2016 | -- |

| UPIS pilot | 45 districts, Kharif 2016, 7 sections | -- |

| CPIS since | 2009-10, economic life 60 years | exams 2017 |

| CPIS palm age (Dwarf/Hybrid) | 4-60 years | exams 2017 |

| CPIS palm age (Tall) | 7-60 years | exams 2017 |

| Livestock Insurance | From 2008-09, 50% subsidy, max 2 animals, 3 years | -- |

| PMFBY coverage (2023-24) | 4.19 crore farmers | -- |

| PMFBY tech tools | D-W-A-Y-C: Digiclaim, WINDS, AIDE, YES-TECH, CROPIC | -- |

| ACABC nodal agency | MANAGE, Hyderabad | -- |

| ACABC training | 60 days (45+15); group of 5 → Rs 100 lakh loan | -- |

| ACABC subsidy | 36% (44% for SC/ST/women/NE/hilly) | -- |