💸 Crop Loans & Kisan Credit Card (KCC)

Complete guide to crop loan schemes, KCC, interest subvention, scale of finance, and DBT for fertilizers -- with exam-focused tips and agricultural examples.

Why Crop Loans Matter

Imagine a wheat farmer in Punjab who needs Rs 50,000 for seeds, fertilizers, and labour before the Rabi season begins. Without timely credit, he borrows from a local moneylender at 36% interest. By harvest, half his profit goes to the lender. Crop loan schemes solve this problem by giving farmers affordable institutional credit, using their standing crop as security instead of their land.

Crop Loan Scheme -- Origin

The Crop Loan Scheme is one of the foundational pillars of agricultural credit in India.

NOTE

Recommended by the All India Rural Credit Survey Committee (Gorwala Committee, 1954). The V.L. Mehra Committee on Co-operative Credit (1960) recommended its adoption in all States.

- The Gorwala Committee found that institutional credit was severely lacking in rural India and recommended a crop-based lending system.

- After a gap of five years, the scheme was introduced nationwide in 1965 and in Andhra Pradesh from Kharif 1966.

- Twin objectives:

- Treat the crop as security instead of landed property.

- Fix the scale of finance based on actual farm expenditure (variable cost).

Agricultural example: A paddy farmer in Tamil Nadu pledges his standing crop (not his ancestral land) to get a loan of Rs 40,000 for seeds, fertilizers, pesticides, and hired labour -- all variable costs that change with the level of production.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Why Crop Loans Matter

Imagine a wheat farmer in Punjab who needs Rs 50,000 for seeds, fertilizers, and labour before the Rabi season begins. Without timely credit, he borrows from a local moneylender at 36% interest. By harvest, half his profit goes to the lender. Crop loan schemes solve this problem by giving farmers affordable institutional credit, using their standing crop as security instead of their land.

Crop Loan Scheme -- Origin

The Crop Loan Scheme is one of the foundational pillars of agricultural credit in India.

NOTE

Recommended by the All India Rural Credit Survey Committee (Gorwala Committee, 1954). The V.L. Mehra Committee on Co-operative Credit (1960) recommended its adoption in all States.

- The Gorwala Committee found that institutional credit was severely lacking in rural India and recommended a crop-based lending system.

- After a gap of five years, the scheme was introduced nationwide in 1965 and in Andhra Pradesh from Kharif 1966.

- Twin objectives:

- Treat the crop as security instead of landed property.

- Fix the scale of finance based on actual farm expenditure (variable cost).

Agricultural example: A paddy farmer in Tamil Nadu pledges his standing crop (not his ancestral land) to get a loan of Rs 40,000 for seeds, fertilizers, pesticides, and hired labour -- all variable costs that change with the level of production.

TIP

Exam mnemonic -- "CroSS": Crop as Security, Scale of finance based on variable cost.

Agricultural Credit -- Overview

Agricultural credit refers to all types of loans and advances given to farmers for agricultural and allied activities. It is the financial fuel that powers farming operations.

| Year | Credit Target (Rs lakh crore) | Actual Achievement |

|---|---|---|

| 2017-18 | 10.00 | 11.69 (exceeded by 17%) |

| 2021-22 | 16.50 | ~18.60 (exceeded by ~13%) |

| 2022-23 | 18.50 | Target set |

| 2023-24 | 20.00 | 25.49 (exceeded significantly) |

Credit flow has consistently exceeded targets. Overall agricultural credit flow rose from ₹7.3 lakh crore in FY 2013-14 to ₹25.49 lakh crore in FY 2023-24.

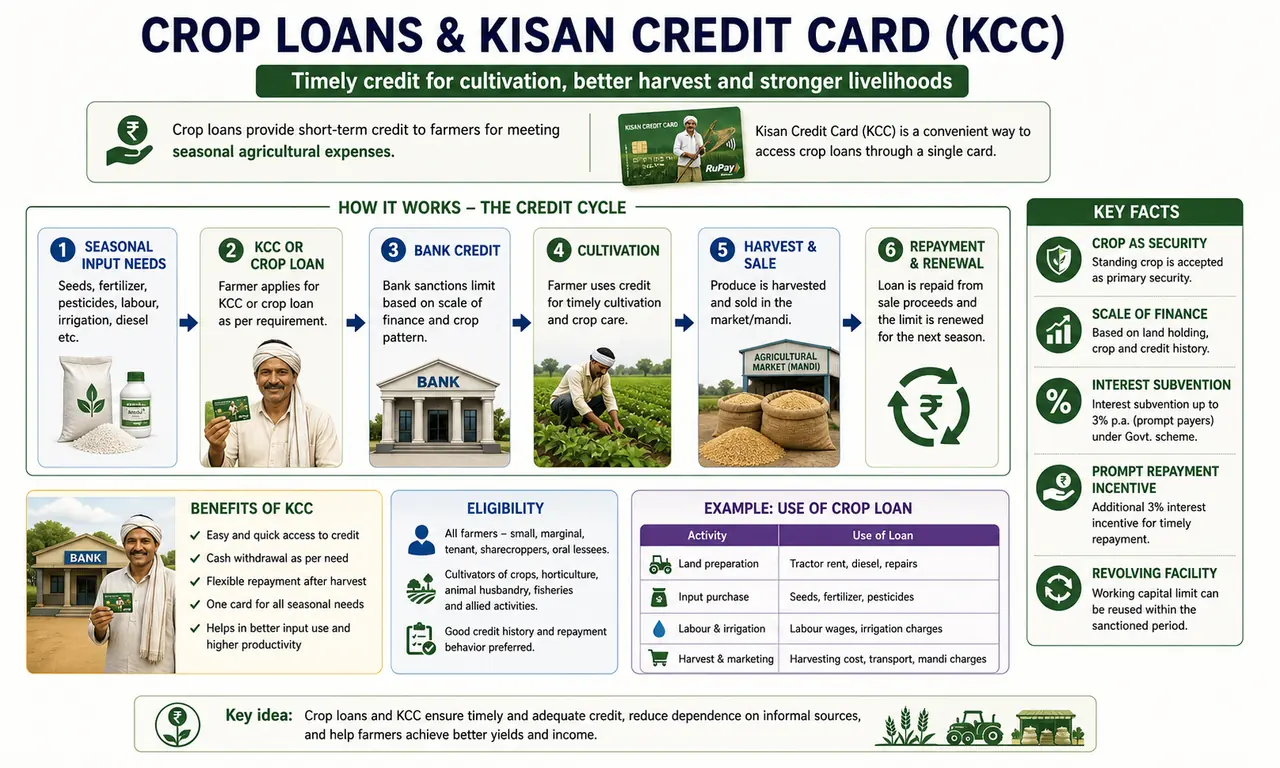

Kisan Credit Card Scheme (KCC)

The Kisan Credit Card (KCC) is one of the most successful agricultural credit delivery mechanisms in India. It works like a revolving credit card for farmers -- draw funds when needed, repay after harvest, and draw again next season.

IMPORTANT

KCC was introduced in 1998 by Finance Minister Yashwant Sinha. Model scheme prepared by NABARD on recommendations of the R.V. Gupta Committee. First bank to launch KCC: SBI.

Agricultural example: A soybean farmer in Madhya Pradesh uses her KCC to buy seeds in June, fertilizer in July, and pesticide in August. After harvest in October, she sells at the mandi and repays the loan -- all through one card.

- As of early 2025, total KCC accounts stood at 7.75 crore, and KCC credit disbursement had risen to ₹10.05 lakh crore by December 2024.

- KCC facility was extended to fisheries and animal husbandry farmers from 2018-19.

Objectives of KCC

KCC is designed as a single-window credit delivery system covering all financial needs of a farmer:

| Credit Need | Example |

|---|---|

| Short-term crop cultivation | Seeds, fertilizers, pesticides for a rice crop |

| Post-harvest expenses | Threshing, cleaning, and drying of harvested wheat |

| Produce marketing loan | Transporting mangoes from Ratnagiri to Mumbai APMC |

| Household consumption | Family expenses during the crop growing period |

| Working capital for allied activities | Feed for dairy cattle, fish pond maintenance |

| Investment credit | Purchasing a pump set, sprayer, or dairy animal |

| Short-term credit for animal rearing | Poultry feed, veterinary medicines |

Eligibility

KCC is designed to be inclusive, covering not just land-owning farmers but also landless cultivators:

- Owner cultivators (individual or joint borrowers)

- Tenant farmers, oral lessees, and sharecroppers (farmers who lease land through verbal agreements)

- SHGs and Joint Liability Groups (JLGs) -- informal groups of 4-10 individuals who borrow without traditional collateral using mutual trust

- Fisheries: Inland fishers, fish farmers, aquaculture operators with pond/tank/hatchery

- Marine fisheries: Owners/lessees of registered fishing vessels with valid fishing licence

- Animal husbandry: Poultry farmers, dairy farmers (individual, JLG, or SHG) with owned/rented/leased sheds

Key stat: As of October-November 2022, 1.0 lakh KCCs sanctioned for fisheries and 9.5 lakh for animal husbandry.

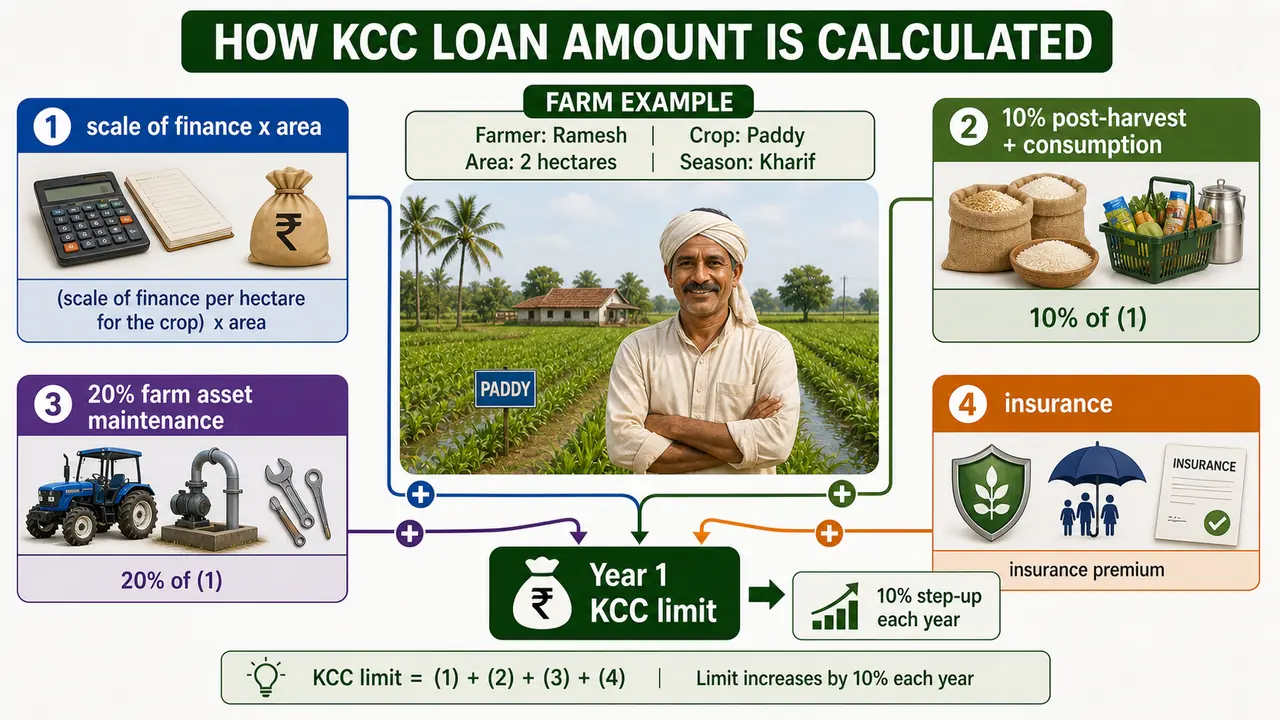

How KCC Loan Amount is Calculated

For Farmers Other Than Marginal Farmers

Single crop per year:

The formula for the first year:

Scale of Finance (per crop) x Area Cultivated + 10% (post-harvest/consumption) + 20% (farm asset maintenance) + crop insurance + PAIS + asset insurance

Agricultural example: A farmer in Haryana grows wheat on 3 hectares. If the Scale of Finance for wheat is Rs 25,000/ha:

- Base: Rs 25,000 x 3 = Rs 75,000

- Post-harvest/consumption (10%): Rs 7,500

- Farm asset maintenance (20%): Rs 15,000

- Insurance: Rs 2,500

- Year 1 limit: Rs 1,00,000

For each successive year (2nd to 5th), the limit is stepped up by 10% to account for inflation in input costs.

Multiple crops per year: Same calculation applied per crop, with 10% annual step-up. If the cropping pattern changes, the limit is reworked.

For Marginal Farmers (Flexi KCC)

Marginal farmers (landholding less than 1 hectare) constitute the majority of Indian farmers.

- Flexi KCC limit: Rs 10,000 to Rs 50,000

- Based on land holding and crops grown, including post-harvest storage needs and consumption

- Includes small term loans for mini dairy, backyard poultry, or farm equipment

- Assessed by Branch Manager based on practical farming needs (not land value)

- Fixed for a 5-year period

For Animal Husbandry and Fisheries

Scale of finance fixed by the District Level Technical Committee (DLTC) based on local costs per acre/unit/animal/bird.

| Sector | Working Capital Components |

|---|---|

| Aquaculture | Seed, feed, fertilizers, lime, harvesting, marketing, labour, lease rent |

| Capture fisheries | Fuel, ice, labour, mooring/landing charges |

| Animal husbandry | Feed, veterinary care, labour, water, electricity |

Term Loans Under KCC

Term loans cover longer-duration investments that improve farm productivity:

- Land development and minor irrigation

- Purchase of farm equipment

- Allied agricultural activities (dairy shed, poultry unit)

- Quantum fixed based on unit cost of asset, repayment capacity, and existing loan obligations

Maximum Permissible Limit (MPL)

MPL = Short-term loan limit for the 5th year + Estimated long-term loan requirement

The MPL is treated as the total Kisan Credit Card Limit for the farmer.

Disbursement Channels

KCC operates as a revolving cash credit facility with no restriction on the number of debits and credits:

| Channel | Use Case |

|---|---|

| Bank branch | Traditional over-the-counter withdrawal |

| Cheque facility | Payment to input dealers |

| ATM/Debit card | Cash withdrawal from any ATM |

| Business Correspondents | Banking in remote areas without branches |

| PoS at sugar mills/contract farming companies | Tie-up advances |

| PoS at input dealers | Buying seeds, fertilizers at dealer shops |

| Mobile-based transfers | Digital payments at dealers and mandis |

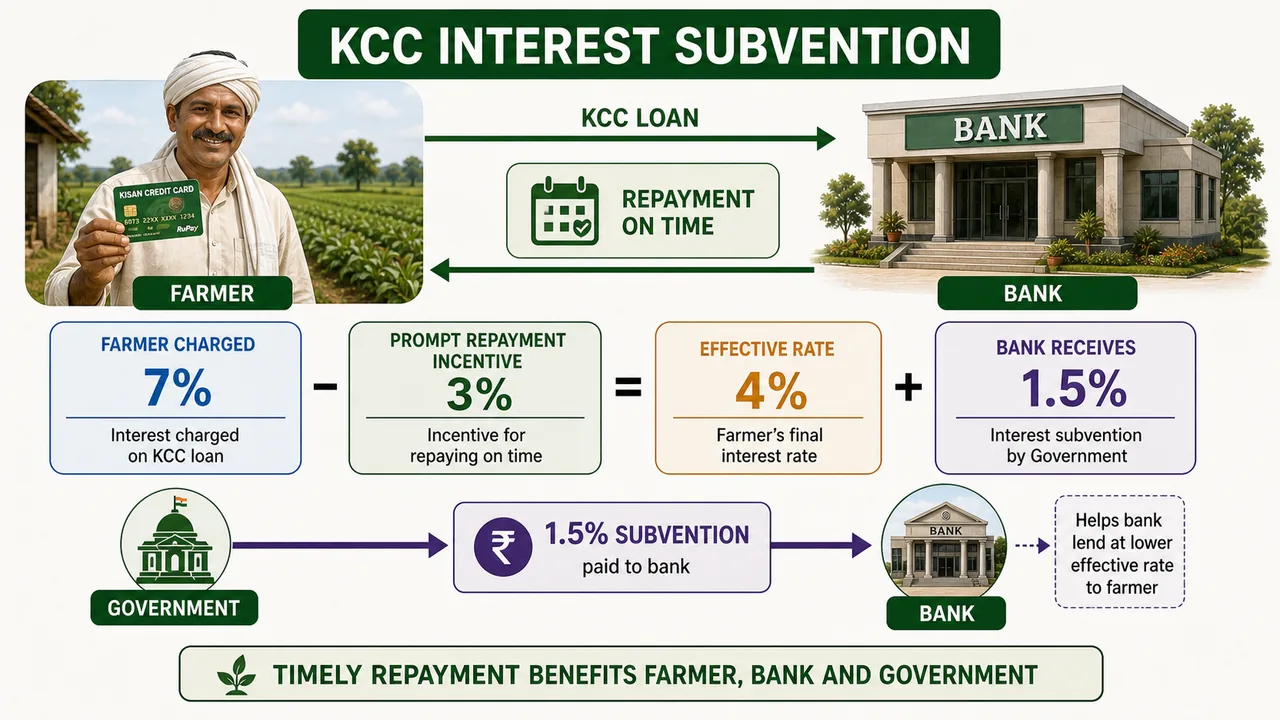

Interest Rate Structure

This is one of the most exam-important topics in agricultural finance.

TIP

Exam Key -- Interest rate breakdown: Farmer is charged 7% interest → Government gives 1.5% interest subvention to banks → Farmer gets additional 3% prompt repayment incentive on timely repayment = effective rate of 4% per annum.

| Parameter | Detail |

|---|---|

| Rate charged to farmer | 7% p.a. |

| Government subvention to bank | 1.5% |

| Prompt repayment incentive | 3% |

| Effective rate for timely repayment | 4% p.a. |

| MISS ceiling for crop loan benefit | Up to ₹3 lakh |

| Allied activity sub-limit under MISS | Up to ₹2 lakh |

| Combined eligible cap | ₹3 lakh per farmer across crop + allied |

| Interest subvention calculation period | From disbursement to repayment, max 1 year |

| Late repayment | Farmer loses PRI benefit; interest charged at applicable card/bank rate |

| MIS/KRP compliance | Aadhaar/e-KYC and claim reporting through Kisan Rin Portal (KRP) |

- For Animal Husbandry & Fisheries farmers: MISS benefit applies on short-term loans up to ₹2 lakh. If the farmer also has crop KCC exposure, the overall benefit cap remains ₹3 lakh per farmer.

- Interest Subvention Scheme (ISS) has been operational since 2006-07.

- Implemented by RBI and NABARD.

Agricultural example: A cotton farmer in Gujarat borrows Rs 2 lakh under KCC. If he repays within the due date, he pays only Rs 8,000 as interest (4% of Rs 2 lakh) for the entire year -- cheaper than any commercial loan.

TIP

Exam mnemonic -- "7 minus 3 = 4": Farmer is charged 7%, and timely repayment earns a 3% prompt repayment incentive, making the effective rate 4%. Separately, banks receive 1.5% MISS subvention from the Government.

Repayment Period

- Short-term loans: Linked to anticipated harvesting and marketing period for the crop. A Rabi wheat farmer repays after April-May harvest; a Kharif paddy farmer repays after October-November.

- Term loans: Normally repayable within 5 years, depending on the type of investment. Banks may allow longer periods at their discretion.

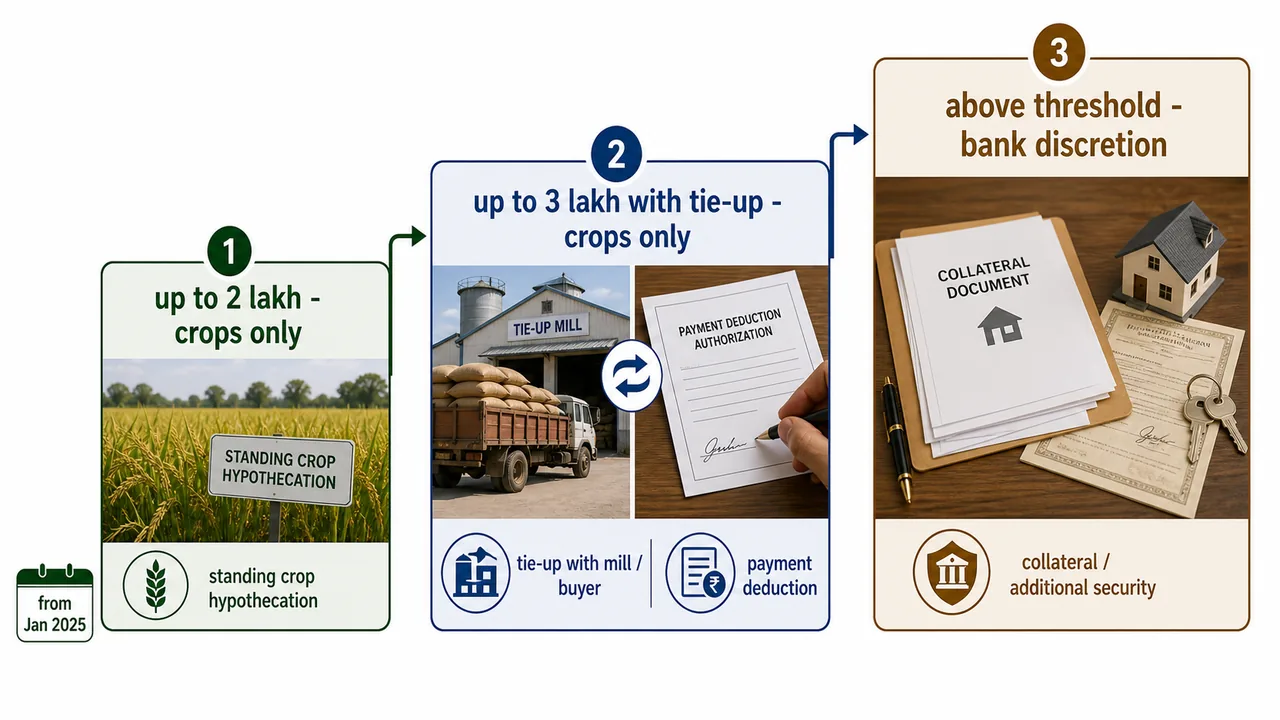

Security Requirements

| Loan Amount | Security Required |

|---|---|

| Up to ₹2.00 lakh | Hypothecation of crops only; no collateral |

| Up to ₹3.00 lakh with tie-up arrangement | Hypothecation of crops only; no collateral |

| Above ₹2.00 lakh without tie-up | Collateral/security at bank's discretion |

| Above ₹3.00 lakh with tie-up | Collateral/security at bank's discretion |

NOTE

The collateral-free KCC limit was updated to ₹2.00 lakh with effect from January 1, 2025. This is a frequently tested current-affairs point in exams interviews.

Hypothecation means pledging the crop as security without transferring ownership. The farmer retains possession and can sell the crop, but the bank has a legal claim on it.

A tie-up arrangement means the bank has an agreement with an agency (like a sugar mill) that deducts loan repayment from payments made to the farmer.

Other Key Features

- Mandatory crop insurance for KCC holders; optional asset, accident (PAIS), and health insurance

- One-time documentation at first availment; only a simple crop declaration from the second year onwards

- No margin required up to ₹2 lakh

- No processing fee up to ₹3 lakh

- Interest subvention/incentive as advised by Central/State Governments

Scale of Finance (SoF)

The Scale of Finance determines the maximum credit per unit of land for each crop. It forms the foundation of KCC credit limit calculation.

| Aspect | Detail |

|---|---|

| Level at which SoF is fixed | District level |

| Fixed by | District Level Technical Committee (DLTC) |

| Meeting convened by | District Central Cooperative Bank (DCCB) |

| Chaired by | CEO of DCCB / senior-most official |

| Approved by | State Level Technical Committee (SLTC) |

| Circulated through | Websites of SLBC, StCB, DCCB, SCBs, and RRBs |

Agricultural example: In Thanjavur district (Tamil Nadu), the DLTC may fix the Scale of Finance for paddy at Rs 30,000/ha based on local costs of seeds, fertilizer, transplanting labour, and irrigation. Every farmer in Thanjavur growing paddy gets credit calculated on this SoF.

Interest Subvention Scheme -- Detailed Breakdown

| Scenario | Rate Paid by Farmer | Government Support |

|---|---|---|

| Timely repayment (within 1 year) | 4% | Farmer pays 7%; bank gets 1.5% MISS subvention + farmer gets 3% prompt repayment incentive |

| Late repayment | 7% | No prompt repayment incentive |

| Loan amount ceiling | Up to ₹3 lakh | Overall MISS cap for crop KCC benefit |

| Allied activities only | Up to ₹2 lakh | Within the overall MISS framework |

| Natural calamity (restructured loan) | Concessional | 2% subvention on restructured amount for first year |

| DAY-NRLM SHGs | Concessional | 2% subvention for max Rs 3 lakh per SHG |

- Subvention available from: Public Sector Banks, Private Sector Banks, Cooperative Banks, and RRBs

- NABARD provides refinance to RRBs and Cooperative Banks

Kisan Rin Portal (KRP)

The Kisan Rin Portal (KRP) was launched in August 2023 to digitize the interest subvention process for KCC loans, ensuring transparent and timely benefit delivery to farmers.

| Feature | Detail |

|---|---|

| Purpose | Digital tracking of MISS interest subvention claims |

| Ensures | Faster disbursement, transparency, accountability |

| Mandate | Aadhaar authentication, validation of multiple KCC accounts within overall limit |

| Reporting | Banks/PACS must submit certified MISS claims through KRP |

KCC — Key Updated Statistics

| Parameter | Value |

|---|---|

| Total KCC accounts | 7.75 crore |

| KCC credit disbursement (2014) | ₹4.26 lakh crore |

| KCC credit disbursement (Dec 2024) | ₹10.05 lakh crore |

| Overall agri credit (FY 2013-14) | ₹7.3 lakh crore |

| Overall agri credit (FY 2023-24) | ₹25.49 lakh crore |

| Operative MISS cap (FY 2025-26) | ₹3 lakh |

| Budget 2025 announcement | Proposal to raise KCC limit to ₹5 lakh; RBI operational notification awaited |

IMPORTANT

The finance schemes lesson treats ₹3 lakh as the current operative MISS cap for crop loans in FY 2025-26. The Union Budget 2025-26 announced a rise to ₹5 lakh, but until the operational RBI notification takes effect, exam answers should use the currently operative framework: ₹3 lakh overall crop-loan MISS cap, ₹2 lakh allied-only cap, 1.5% bank subvention, and 3% prompt repayment incentive.

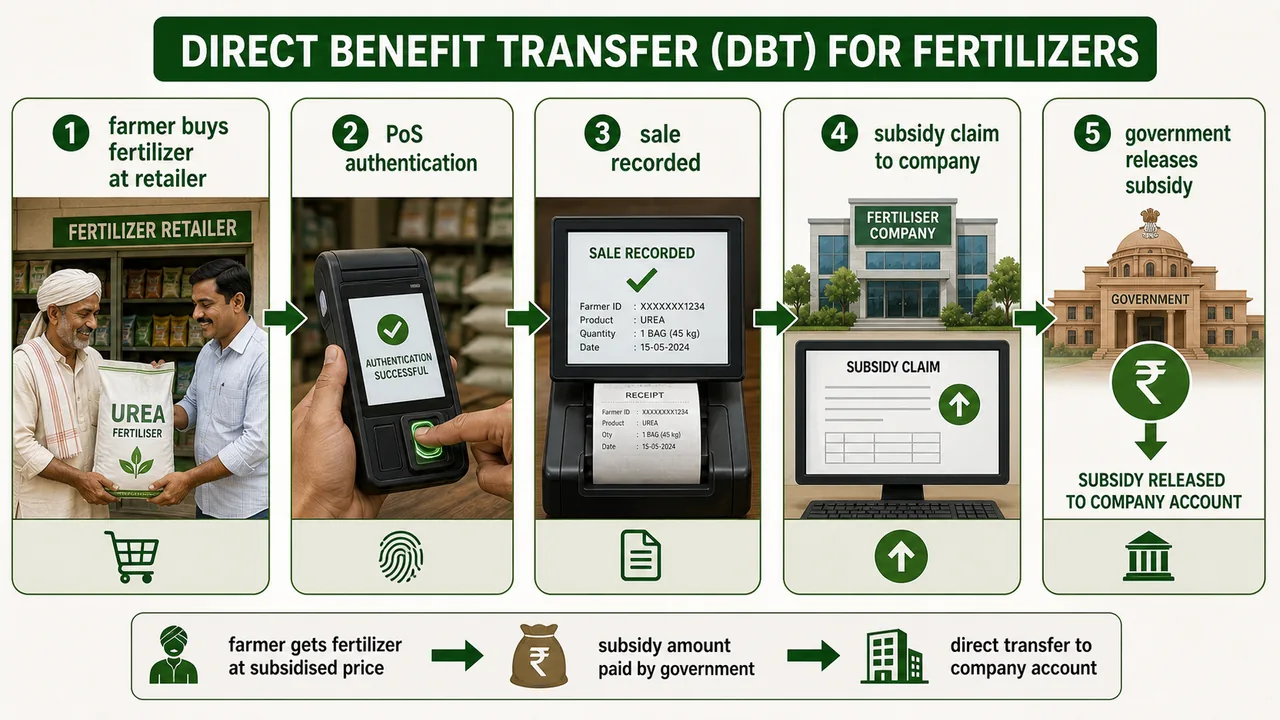

Direct Benefit Transfer (DBT) for Fertilizers

DBT transforms how government subsidies reach farmers. Instead of subsidizing the product (which causes leakages), the subsidy is linked to actual sales at the retail level.

- Introduced on pilot basis from October 2016.

- Under fertilizer DBT, 100% subsidy is released to fertilizer companies based on actual sales made by retailers to beneficiaries.

- Sales are verified through Point-of-Sale (PoS) machines, ensuring genuine farmers receive the benefit and eliminating diversion and black-marketing.

Agricultural example: When a farmer in Bihar buys a bag of DAP fertilizer from a local dealer, the PoS machine records the sale against the farmer's Aadhaar. The farmer pays only the subsidized MRP, and the government transfers the subsidy amount directly to the fertilizer company.

Summary Cheat Sheet

| Topic | Key Fact | Exam Tag |

|---|---|---|

| Crop Loan Scheme | Recommended by Gorwala Committee (1954); V.L. Mehra Committee (1960) | -- |

| KCC launch year | 1998 | IBPS 2018 |

| KCC model scheme by | NABARD (R.V. Gupta Committee) | -- |

| First bank to launch KCC | SBI | -- |

| KCC interest logic | 7% to farmer; 1.5% MISS to bank; 4% effective with prompt repayment | Current |

| Interest Subvention Scheme since | 2006-07 | -- |

| Loan ceiling for MISS benefit | ₹3 lakh overall; ₹2 lakh for allied-only | FY 2025-26 |

| Collateral-free loan limit | ₹2 lakh (from Jan 1, 2025) | Current |

| Scale of Finance fixed by | DLTC (convened by DCCB) | NABARD 2019 |

| SoF approved by | SLTC | -- |

| Flexi KCC (marginal farmers) | Rs 10,000 to Rs 50,000 | -- |

| KCC extended to AH & fisheries | 2018-19 | -- |

| Agri credit target 2023-24 | Rs 20 lakh crore | -- |

| Total KCC accounts | 7.75 crore | PIB 2025 |

| KCC disbursement (Dec 2024) | ₹10.05 lakh crore (up from ₹4.26L Cr in 2014) | -- |

| Operative KCC/MISS cap | ₹3 lakh | Current norms |

| Budget 2025-26 KCC proposal | ₹5 lakh announced; operational notification awaited | Union Budget |

| Kisan Rin Portal (KRP) | Launched August 2023; digitizes MISS claims | -- |

| MISS FY 2025-26 | Continued with 1.5% interest subvention | Cabinet May 2025 |

| DBT for fertilizers | Pilot from October 2016 | -- |

References

3 sources • [1] [2] [3]

References

Used for: 7.75 crore KCC accounts, credit disbursement growth, MISS continuation, Kisan Rin Portal launch date

Used for: KCC short-term crop loan limit raised from ₹3 lakh to ₹5 lakh

Used for: Detailed operational requirements, Aadhaar authentication, digital tracking via KRP