🏦 What are NABARD Model Bankable Projects? — Concept, Purpose & Techno-Economic Parameters

Understand why NABARD created Model Bankable Projects, what problems they solve for farmers and banks, and the 8 key techno-economic parameters (IRR, DSCR, BCR, margin money, repayment period etc.) that every agricultural financing decision is built on. Essential foundation for exams.

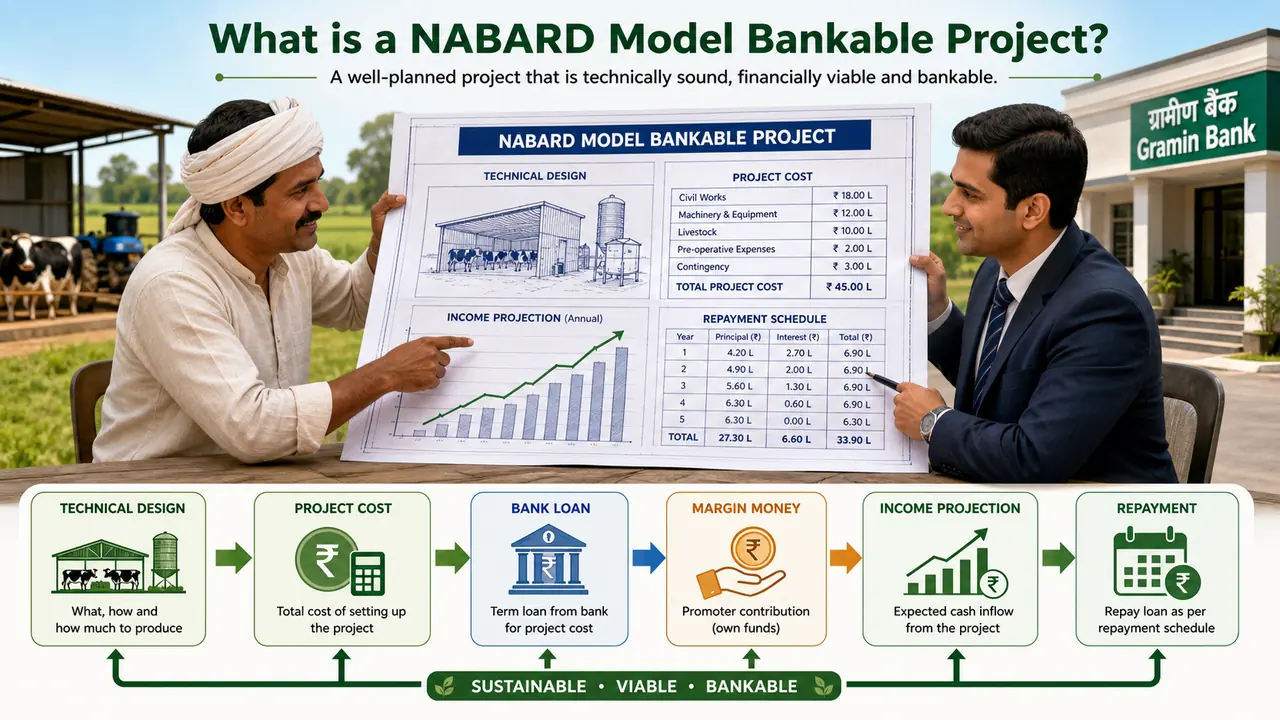

Before a farmer can get a bank loan to set up a dairy, fish farm, or orchard, the bank asks one question: Is this project financially viable? NABARD Model Bankable Projects exist to answer that question — in advance, for every major agricultural activity in India.

What is a Model Bankable Project?

A Model Bankable Project (MBP) is a standardised techno-economic blueprint prepared by NABARD (National Bank for Agriculture and Rural Development) for a specific agricultural enterprise.

It contains:

- The technical design of the activity (unit size, land needed, equipment, breeds/varieties, stocking density)

- The complete financial structure (total project cost, how it is funded, income projections, repayment schedule)

- A viability analysis (IRR, BCR, DSCR, break-even) proving the project can repay a bank loan

Think of it as a standardised business plan template — a farmer does not need to hire a consultant; the bank does not need to analyse from scratch. Both parties work from the same vetted blueprint.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Before a farmer can get a bank loan to set up a dairy, fish farm, or orchard, the bank asks one question: Is this project financially viable? NABARD Model Bankable Projects exist to answer that question — in advance, for every major agricultural activity in India.

What is a Model Bankable Project?

A Model Bankable Project (MBP) is a standardised techno-economic blueprint prepared by NABARD (National Bank for Agriculture and Rural Development) for a specific agricultural enterprise.

It contains:

- The technical design of the activity (unit size, land needed, equipment, breeds/varieties, stocking density)

- The complete financial structure (total project cost, how it is funded, income projections, repayment schedule)

- A viability analysis (IRR, BCR, DSCR, break-even) proving the project can repay a bank loan

Think of it as a standardised business plan template — a farmer does not need to hire a consultant; the bank does not need to analyse from scratch. Both parties work from the same vetted blueprint.

NOTE

Exam clarity: "Bankable" does not just mean "suitable for a bank loan." It specifically means the project has been assessed to generate sufficient cash flow to service debt — i.e., pay back both principal and interest on time. A project can be profitable yet not bankable if its cash flows are too irregular to meet EMIs.

Why Did NABARD Create MBPs?

The Problem Before MBPs

In the 1970s–80s, agricultural lending in India faced three failures:

- Information asymmetry — Banks lacked expertise to evaluate niche activities like rabbit farming, spirulina production, or beekeeping. This led to over-cautious lending or mispriced loans.

- Inconsistency — Two bank branches would finance the same activity at completely different terms, creating unfairness.

- High transaction cost — Farmers had no access to professional project appraisal; each loan application required expensive consultants.

NABARD's Solution

NABARD, as the apex development bank for agriculture, stepped in to:

- Conduct field-level feasibility studies across India

- Standardise the techno-economic norms for each enterprise

- Publish these as free, publicly available model projects

Result: A small farmer in Bihar and a large entrepreneur in Karnataka both approach their bank with the same NABARD-vetted blueprint. The bank's appraisal time drops from months to days.

NOTE

MBPs are updated periodically as input costs, output prices, and technology change. Many current MBPs were revised post-2015. Always check the revision date when citing figures in exams — older editions had lower cost norms.

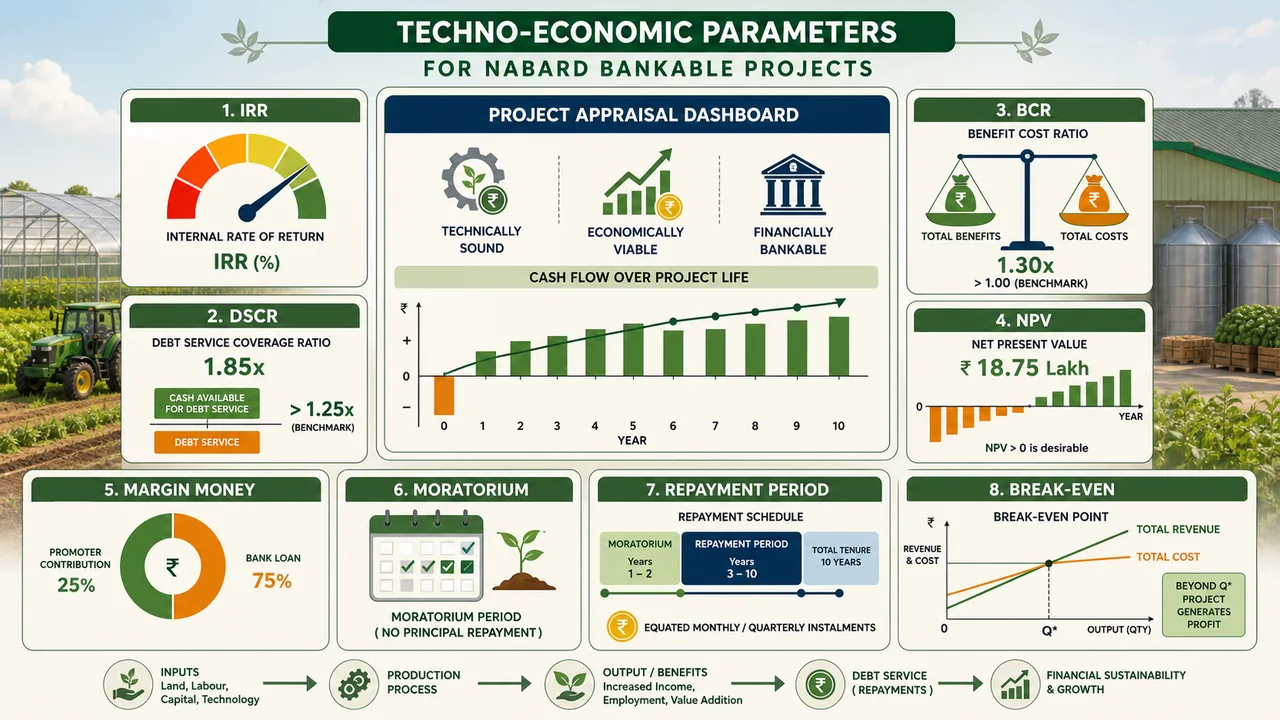

The 8 Techno-Economic Parameters Banks Evaluate

Every MBP presents these parameters. Exams test your ability to interpret them, not just recall them.

1. Total Financial Outlay (TFO) / Project Cost

The total capital required to set up the enterprise from scratch. Includes:

- Fixed assets (land development, civil construction, equipment, vehicles)

- Working capital margin (funds needed to run operations for the first cycle before income starts)

| Component | Example (Dairy — 10 animals) |

|---|---|

| Fixed capital | ₹5.54 lakh |

| Working capital margin | ₹1.00 lakh |

| Total Financial Outlay | ₹6.54 lakh |

2. Means of Finance (Funding Structure)

How the TFO is divided between the bank and the borrower:

| Source | Proportion | Who bears it |

|---|---|---|

| Bank Loan | 65–90% of TFO | Commercial bank / RRB / cooperative |

| Margin Money (borrower's equity) | 10–25% of TFO | Farmer / entrepreneur |

| Subsidy (if applicable) | Varies by scheme | Govt. (DEDS, NLM, SMAM, etc.) |

Why margin money matters: Banks insist on borrower equity (skin in the game) to reduce moral hazard. The higher the risk of the enterprise, the higher the margin money required. Margin money for dairy is typically 25%; for low-cost activities like goat farming it can be as low as 10%.

NOTE

Exam trap: Subsidy is not part of the borrower's margin money — it is a separate third source. Total = Bank Loan + Margin Money + Subsidy. When a question gives TFO and two of the three components, you calculate the third.

3. Internal Rate of Return (IRR)

The discount rate at which Net Present Value (NPV) = 0. In plain terms: the actual annual return the project generates on the total investment.

- IRR > prevailing interest rate → project is viable

- IRR < prevailing interest rate → project will not repay the loan

Typical ranges in MBPs:

| Enterprise | IRR Range |

|---|---|

| Dairy farming | 25–35% |

| Poultry (layer) | 35–45% |

| Horticulture (mango, coconut) | 15–20% (long gestation) |

| Custom Hiring Centre | 20–25% |

| Moringa | >100% (high-value crop) |

NOTE

High IRR ≠ better project automatically. Moringa shows 127% IRR partly because the denominator (investment) is small. For exam MCQs, focus on whether IRR > interest rate (viability test), not which is "highest."

4. Benefit-Cost Ratio (BCR)

BCR = Total Discounted Benefits ÷ Total Discounted Costs

- BCR > 1 → project is viable

- BCR = 1.5 means every ₹1 invested returns ₹1.50 in present value terms

Used more for plantation/horticulture projects (mango, coconut) where cash flows are uneven and long-term.

5. Net Present Value (NPV)

NPV = Present value of all future cash inflows − Present value of all cash outflows

- Positive NPV → viable

- Higher NPV → more absolute wealth created

IRR and NPV together give a complete picture: IRR shows rate of return, NPV shows absolute value creation.

6. Debt Service Coverage Ratio (DSCR)

DSCR = Net Cash Accrual ÷ Debt Service (principal + interest due)

- DSCR > 1 → project generates enough cash to repay debt in that year

- Minimum acceptable DSCR: 1.75 (NABARD norm for most projects)

- Average DSCR over repayment period should be ≥ 1.75

Why it matters to the bank: IRR tells you the long-run return. DSCR tells you if the project can make its next EMI. A project with high IRR but low Year-1 DSCR may default even if it is ultimately profitable.

NOTE

Exam trap: DSCR is calculated on net cash accrual (profit after tax + depreciation), not on gross revenue. Depreciation is added back because it is a non-cash charge — it reduces profit on paper but does not consume cash.

7. Repayment Period & Moratorium

Repayment period = number of years to repay the loan principal + interest.

Moratorium (grace period) = initial period during which no principal repayment is required (only interest paid, or in some cases interest is also capitalised).

| Enterprise type | Typical repayment | Typical moratorium |

|---|---|---|

| Dairy, poultry | 5–7 years | 6 months–1 year |

| Horticulture (mango, coconut) | 10–13 years | 3–7 years (until first commercial yield) |

| Fisheries | 6–10 years | 1–2 years |

| Solar pumpset | 10 years | 1 year |

Why moratoriums exist: Perennial crops (mango, coconut, citrus) have a gestation period — trees do not bear fruit for 3–7 years. No income = no cash to repay. Banks extend moratoriums to cover this gestation.

8. Break-Even Point (BEP)

The level of output/sales at which total revenue = total cost — neither profit nor loss.

- BEP (units) = Fixed Cost ÷ (Selling Price − Variable Cost per unit)

- BEP (capacity utilisation %) = Fixed Costs ÷ Contribution × 100

Lower BEP % means the project is safer — it becomes profitable even at partial capacity.

Summary: Quick Reference for Exams

| Parameter | What it measures | Pass criterion |

|---|---|---|

| IRR | Rate of return | > lending interest rate |

| BCR | Benefit per ₹1 cost | > 1.0 |

| NPV | Absolute wealth created | > 0 |

| DSCR | Annual debt repayment ability | ≥ 1.75 |

| Margin Money | Borrower's own contribution | 10–25% of TFO |

| Repayment Period | Time to repay loan | Varies by enterprise |

| Moratorium | Grace period before repayment | Matches gestation period |

| BEP | Safety margin | Lower is safer |

NOTE

Most-tested MCQ fact: NABARD was established on 12 July 1982 based on the recommendations of the B. Sivaraman Committee. It took over agricultural credit functions from RBI and ARDC. This context explains why NABARD — not RBI or SIDBI — is the nodal agency for agricultural project financing norms.

Sources & References

Primary source for this lesson is NABARD's official Model Bankable Projects portal.[1]

References

1 source • [1]

References

Used for: Official NABARD portal for model bankable project documents and updates.

The figures in this lesson reflect the cost norms and technical parameters as published in the NABARD document. Actual costs may vary by state, season, and year of implementation. Always refer to the latest NABARD circular for current norms.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Model Bankable Project (MBP) | Standardised techno-economic blueprint by NABARD for a specific agricultural enterprise; contains technical design, financial structure, and viability analysis |

| Purpose of MBPs | Solve information asymmetry, inconsistency in lending terms, and high transaction cost of project appraisal |

| NABARD established | 12 July 1982, on recommendations of the B. Sivaraman Committee; took over agricultural credit from RBI and ARDC |

| "Bankable" definition | Project generates sufficient cash flow to service debt (repay principal + interest on time) — a profitable project can still be non-bankable if cash flows are irregular |

| Total Financial Outlay (TFO) | Total capital required = Fixed assets + Working capital margin |

| Means of Finance | Bank Loan (65–90%) + Margin Money (10–25%) + Subsidy (if any) — subsidy is NOT part of margin money |

| Margin money range | Dairy: 25%; Goat farming (low-risk): 10% |

| IRR (Internal Rate of Return) | Discount rate at which NPV = 0; project is viable if IRR > lending interest rate |

| IRR ranges by enterprise | Dairy: 25–35% · Poultry (layer): 35–45% · Horticulture: 15–20% · Custom Hiring: 20–25% · Moringa: >100% |

| BCR (Benefit-Cost Ratio) | Total Discounted Benefits ÷ Total Discounted Costs; BCR > 1 = viable; used mainly for plantation/horticulture |

| NPV (Net Present Value) | PV of cash inflows − PV of cash outflows; positive = viable; measures absolute wealth created |

| DSCR (Debt Service Coverage Ratio) | Net Cash Accrual ÷ Debt Service; minimum acceptable = ≥ 1.75 (NABARD norm) |

| DSCR calculation note | Based on net cash accrual = profit after tax + depreciation (depreciation added back as it is non-cash) |

| Repayment Period & Moratorium | Dairy/Poultry: 5–7 yrs, moratorium 6 months–1 yr · Horticulture: 10–13 yrs, moratorium 3–7 yrs · Solar pumpset: 10 yrs, moratorium 1 yr |

| Moratorium rationale | Covers gestation period of perennial crops (mango, coconut) — no income during early years so no repayment required |

| Break-Even Point (BEP) | BEP (units) = Fixed Cost ÷ (Selling Price − Variable Cost per unit); lower BEP % = safer project |

| MBP update cycle | Updated periodically — many revised post-2015; always check revision date when citing figures |

Lesson Doubts

Ask questions, get expert answers