👶 Economics: Foundations & Core Concepts

Complete guide to economics fundamentals — definitions by Adam Smith, Marshall, Robbins & Keynes, micro vs macro economics, methods of investigation, and economic laws. Essential for ICAR, exams, NABARD, and agricultural competitive exams.

Why Study Economics?

Before diving into definitions, let's understand why economics matters — especially for agriculture students.

Imagine a farmer with 5 acres of land. She can grow wheat, rice, or sugarcane — but not all three on the same land at the same time. She must choose. This simple decision involves economics: allocating scarce resources (land, water, money) among competing wants (different crops).

Economics is not just about money — it is about understanding how individuals, farmers, businesses, and governments make choices when resources are limited.

Core Insight: Economics exists because of one fundamental truth — human wants are unlimited, but resources to satisfy them are limited. This gap creates the need to choose, and economics studies those choices.

What is Economics?

Economics is popularly known as the Queen of Social Sciences. It studies the economic activities of people living in a society.

Economic activities are those activities concerned with the efficient use of scarce means to satisfy human wants. After basic needs (food, shelter, clothing) are met, priorities shift to education, healthcare, entertainment, and so on — the list never ends.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

Charged once for one year · ₹1188 total

Save ₹100/month vs ₹2388/year launch price

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure one-time yearly payment via Razorpay · No hidden fees

Why Study Economics?

Before diving into definitions, let's understand why economics matters — especially for agriculture students.

Imagine a farmer with 5 acres of land. She can grow wheat, rice, or sugarcane — but not all three on the same land at the same time. She must choose. This simple decision involves economics: allocating scarce resources (land, water, money) among competing wants (different crops).

Economics is not just about money — it is about understanding how individuals, farmers, businesses, and governments make choices when resources are limited.

Core Insight: Economics exists because of one fundamental truth — human wants are unlimited, but resources to satisfy them are limited. This gap creates the need to choose, and economics studies those choices.

What is Economics?

Economics is popularly known as the Queen of Social Sciences. It studies the economic activities of people living in a society.

Economic activities are those activities concerned with the efficient use of scarce means to satisfy human wants. After basic needs (food, shelter, clothing) are met, priorities shift to education, healthcare, entertainment, and so on — the list never ends.

The Three Central Problems

Since we cannot have everything, every economy must answer three fundamental questions:

| Problem | Meaning | Agricultural Example |

|---|---|---|

| What to produce? | Which goods and services? | Should India grow more rice or export flowers? |

| How to produce? | Which methods and technology? | Manual harvesting or combine harvester? |

| For whom to produce? | Who gets the output? | Subsidized grain for poor or market-price sales? |

These three problems arise directly from scarcity — the gap between unlimited wants and limited resources.

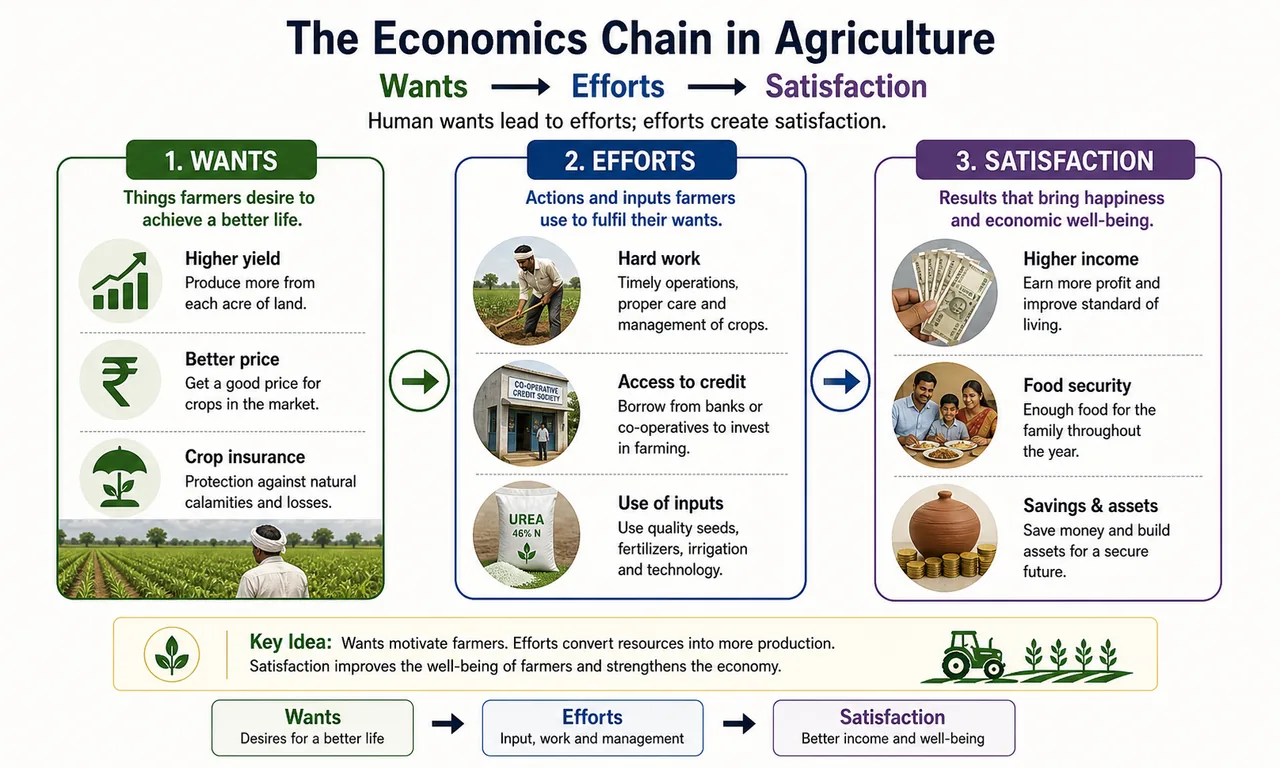

Subject Matter: Wants → Efforts → Satisfaction

The subject matter of economics can be summarized in three words:

- Wants: A farmer wants higher yield, better prices, crop insurance

- Efforts: She works the land, takes loans, uses fertilizers

- Satisfaction: She earns income, feeds her family, saves for the future

In a primitive economy, this chain is direct. In a modern economy, specialization, trade, and money act as intermediaries — a wheat farmer doesn't eat all her wheat; she sells it and buys what she needs.

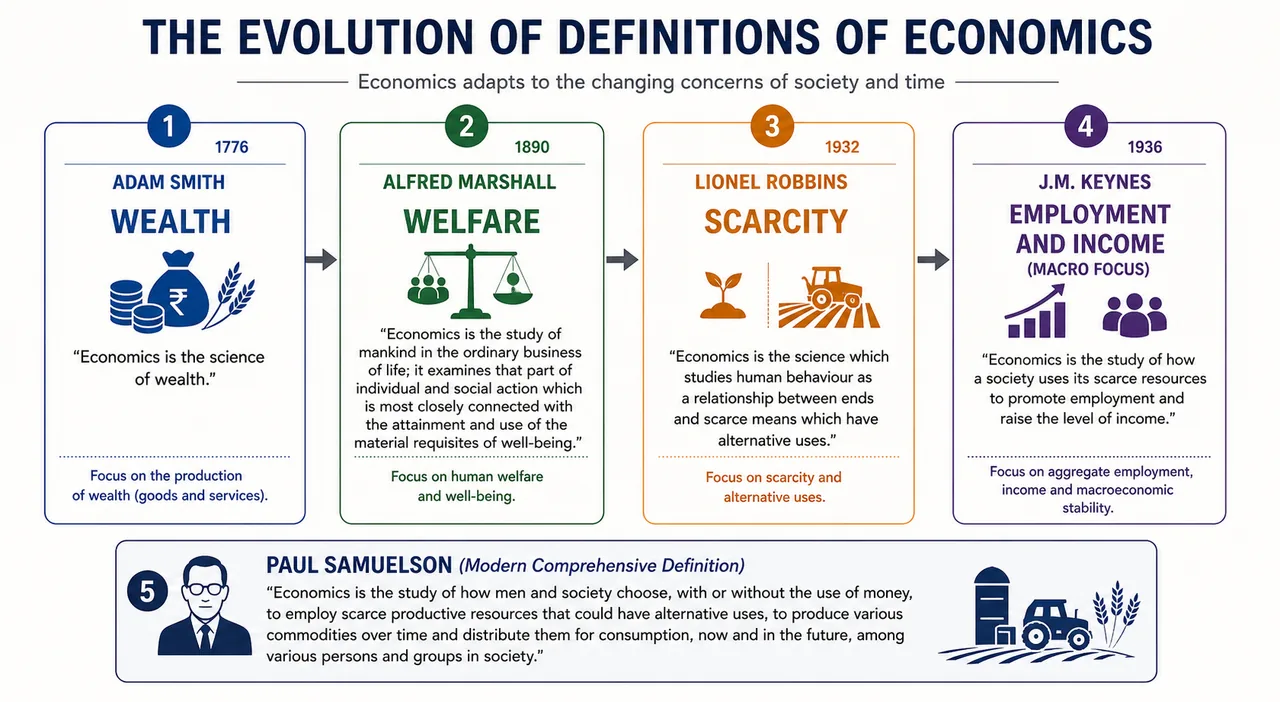

How Economists Define Economics — 4 Key Definitions

The definition of economics has evolved over centuries. Each definition reflects the thinking of its era. All four are exam-important.

1. Wealth Definition — Adam Smith (1776)

"An enquiry into the nature and causes of wealth of nations" — Adam Smith, Wealth of Nations (1776)

- Adam Smith is called the Father of Economics

- His definition placed wealth at the centre of economic study

- Focus: How nations create, accumulate, and distribute wealth

Example: Why is the USA wealthier than many other nations? Smith would analyze their natural resources, labor skills, trade policies, and capital investment.

Limitation: Critics argued this made economics a "dismal science" focused only on wealth, ignoring human welfare.

2. Welfare Definition — Alfred Marshall (1890)

"Political Economy or Economics is a study of mankind in the ordinary business of life" — Alfred Marshall, Principles of Economics (1890)

- Marshall shifted focus from wealth to human welfare

- Economics studies how people earn and use material requisites of well-being

- It is "on one side a study of wealth, and on the other, a study of man"

Example: A government subsidizes cooking gas for rural families. Marshall's approach would evaluate not just the cost (wealth) but whether it improved family health and living standards (welfare).

Advancement: Marshall recognized that wealth is a means, not an end — the ultimate purpose of economics is to improve people's lives.

3. Scarcity Definition — Lionel Robbins (1932)

"Economics is the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses" — Lionel Robbins, Nature and Significance of Economic Science (1932)

- Most widely accepted definition in modern economics

- Introduced three key concepts: scarcity, choice, and alternative uses

- Economics is about choosing between alternatives when resources are limited

Example: A farmer has ₹50,000. She can buy seeds, or a pump, or pay school fees. Each choice means giving up the others — this trade-off is the essence of Robbins' definition.

4. Growth Definition — J.M. Keynes (1936)

"The study of the administration of scarce resources and of the determinants of employment and income" — John Maynard Keynes, General Theory of Employment, Interest and Money (1936)

- Keynes is called the Father of Modern Economics

- Emphasis on employment and income at the national level

- Foundation for modern macroeconomic policy

Paul Samuelson (Nobel laureate) gave the most comprehensive definition:

"Economics is the study of how people and society choose to employ scarce productive resources that could have alternative uses, to produce various commodities and distribute them for consumption among various persons and groups in society."

| Economist | Definition Type | Key Focus | Book/Year |

|---|---|---|---|

| Adam Smith | Wealth | How nations create wealth | Wealth of Nations (1776) |

| Alfred Marshall | Welfare | Human well-being | Principles of Economics (1890) |

| Lionel Robbins | Scarcity | Choice under scarcity | Nature & Significance (1932) |

| J.M. Keynes | Growth | Employment & income | General Theory (1936) |

| Paul Samuelson | Comprehensive | Production + distribution + time | Nobel laureate |

Exam Mnemonic — "SWSG": Smith (Wealth) → MarShall (Welfare) → RobbinS (Scarcity) → KeyneS (Growth)

The Origin of the Word "Economics"

- Derived from Greek word "OIKONOMICAS" — OIKOS (household) + NOMOS (management)

- Literally means "management of a household" — later expanded to nations and the global economy

- Kautilya, the ancient Indian statesman, wrote "Arthashastra" — one of the earliest works on political economy and statecraft

Divisions of Economics

Economics has been divided differently across two approaches:

Traditional Approach (Classical) — 4 Divisions

The classical economists divided economics into four branches, all centered around wealth:

| Division | Meaning | Example |

|---|---|---|

| Production | Creation of utility — transforming inputs into useful goods | A flour mill converts wheat into atta |

| Consumption | Destruction of utility — using goods to satisfy wants | A family eats the roti made from atta |

| Exchange | Transfer of goods between parties | The farmer sells wheat at the mandi |

| Distribution | Sharing of wealth among factors of production | Rent to landowner, wages to workers, interest to bank, profit to entrepreneur |

Distribution has two types:

- Personal distribution: Why some individuals earn more than others (income inequality)

- Functional distribution: How income is shared among land (rent), labour (wages), capital (interest), and enterprise (profit)

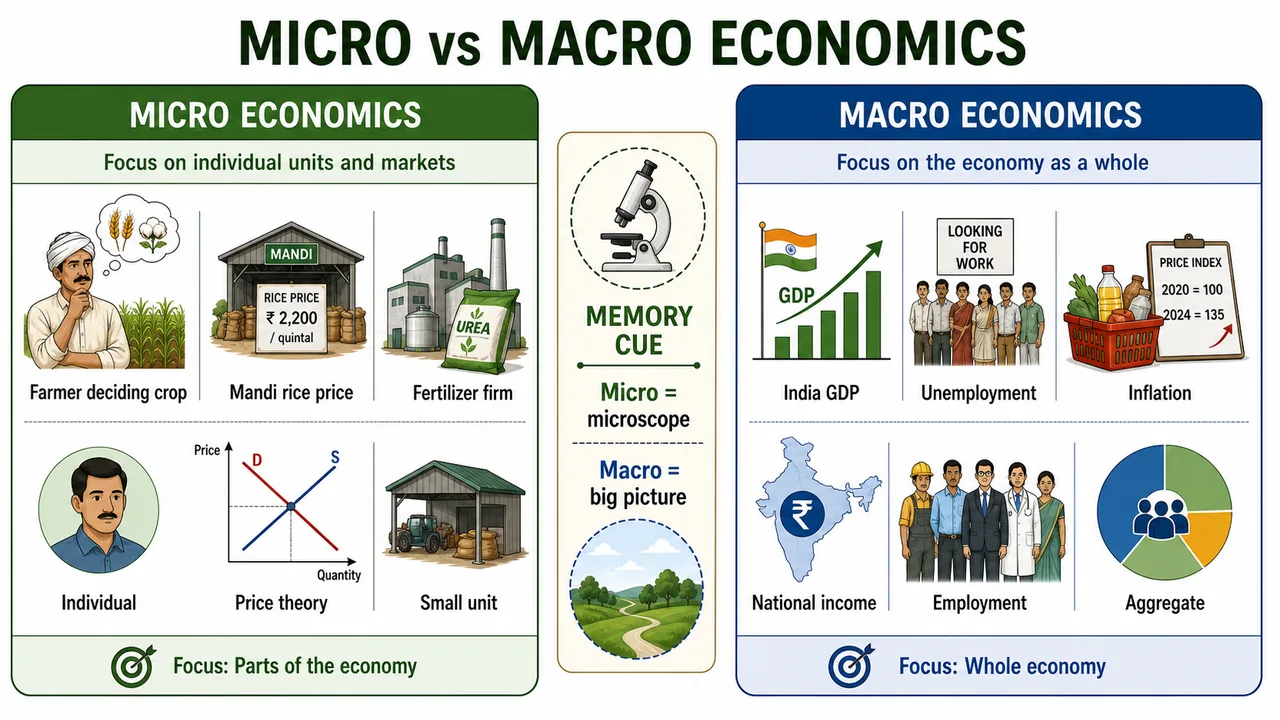

Modern Approach — 2 Divisions

The modern approach, introduced by Ragnar Frisch in 1933, divides economics into Micro and Macro economics.

Memory Aid: Micro = Microscope (small, individual) | Macro = Magnifying the whole economy

Micro Economics (Price Theory)

- From Greek "mikros" = small

- Studies behaviour of individual economic units — a consumer, a firm, an industry

- Also called Price Theory — explains how prices of goods and services are determined

- Assumes full employment in the economy as a whole

What Micro Economics studies:

- How a farmer decides what crop to grow (individual decision)

- How the price of wheat is determined in a local mandi (price formation)

- How a fertilizer company decides production quantity (firm behaviour)

| Importance | Limitation |

|---|---|

| Explains functioning of free enterprise economy | Cannot explain economy-wide problems |

| Shows how prices are determined | Ignores aggregate employment, GDP, inflation |

| Helps formulate policies for efficiency | Assumes full employment (unrealistic) |

| Explains resource allocation | Cannot address recessions or booms |

Macro Economics (Theory of Income & Employment)

- From Greek "makros" = large

- Studies aggregates: national income, GDP, total employment, inflation, aggregate demand/supply

- Also called Theory of Income and Employment

- Looks at the entire economy to guide policy

What Macro Economics studies:

- Why India's GDP grew by 7% this year (national output)

- Why unemployment increased after COVID (aggregate employment)

- Why onion prices rose across all states (general price level)

| Importance | Limitation |

|---|---|

| Understand complex economic systems | Ignores individual differences |

| Formulate policies for unemployment, inflation | General price stability may hide sector-specific crises |

| Estimate national income, living standards | Policies beneficial in aggregate may burden specific groups |

| Essential for global trade and WTO analysis | Overlooks distributional effects |

Exam Tip: A question about "price of rice in a market" is Micro. A question about "India's food grain production" is Macro. If it says "individual" or "firm" — Micro. If it says "national" or "aggregate" — Macro.

Economics: Science, Art, or Social Science?

| Question | Answer | Reasoning |

|---|---|---|

| Is economics a science? | Yes | It uses systematic methods of observation, analysis, and theory-building |

| Is economics an art? | Yes | It prescribes practical solutions — "what should be done" to achieve goals |

| Is it a social science? | Yes | It studies human behaviour in society, not natural phenomena |

Economics is both a science and an art — as a science it explains "what is", as an art it prescribes "what should be done."

Unlike natural sciences (physics, chemistry), economics studies human behaviour, making its laws less exact but equally important.

Positive vs. Normative Economics

This is one of the most frequently tested distinctions:

| Positive Economics | Normative Economics |

|---|---|

| Concerned with "what is" | Concerned with "what ought to be" |

| Objective — based on facts | Subjective — based on values |

| No value judgment | Involves moral judgment |

| Can be tested with data | Cannot be proven right/wrong |

| "Price rises when demand increases" | "Rising prices are a social evil" |

| "MSP of wheat is ₹2,275/quintal" | "Government should increase MSP further" |

Quick Test: If a statement can be verified with data → Positive. If it uses "should", "ought to", or "must" → Normative.

Methods of Economic Investigation

Economists use two complementary methods to build knowledge:

1. Deductive Method (General → Particular)

- Also called abstract, analytical, hypothetical, or a priori method

- Starts with a general principle → derives specific conclusions

Four Steps: Select problem → Formulate assumptions → Build hypothesis through logical reasoning → Verify with data

Example: General principle: "Consumers prefer lower prices." Deduction: "A decrease in wheat price will increase its demand."

2. Inductive Method (Particular → General)

- Also called concrete, historical, or realistic method

- Starts with specific observations → derives general principles

Example: Observing that farmers in Punjab, UP, and MP all reduce wheat sowing when prices fall → General law: "Supply is directly related to price" (Law of Supply).

Both methods are complementary: deductive builds theoretical frameworks, inductive validates them with real-world data.

Economic Laws — Nature & Characteristics

Economic laws are principles that govern human economic behaviour.

"Economic laws are statements of uniformities which govern human behaviour concerning the utilization of limited resources for the achievement of unlimited ends" — Robbins

7 Key Characteristics

| Characteristic | Meaning | Example |

|---|---|---|

| Not government laws | No punishment for violation; describe tendencies | You won't be jailed for buying expensive goods |

| Statements of tendencies | Indicate what is likely to happen, not what must happen | "Demand usually falls when price rises" — not always |

| Hypothetical | Valid only under certain conditions (ceteris paribus) | Law of demand holds when income, taste, etc. are constant |

| Positive, not normative | Describe phenomena, don't prescribe actions | "Inflation reduces purchasing power" (not "inflation is bad") |

| Some are axiomatic | Self-evident truths needing no proof | Law of diminishing marginal utility |

| Lack exactness | Less precise than laws of physics | Marshall compared them to laws of tides, not gravitation |

| Based on human behaviour | Subject to change as behaviour changes | Consumer preferences shift with culture and technology |

Marshall's Analogy: Economic laws are like laws of tides — influenced by many factors, not perfectly predictable, but still powerful and useful for navigation. Just as a sailor uses tidal patterns despite their complexity, economists use economic laws to guide policy despite their imperfections.

Importance of Economics — Why It Matters

- Analyses economic problems and proposes optimum allocation of resources

- Essential for understanding national and international events — trade wars, inflation, agricultural policy

- Amartya Sen (Bharat Ratna) won the Nobel Prize in Economics for his work on welfare economics, famine, and human development

- Economics provides the analytical tools to understand poverty, inequality, and development — issues central to Indian agriculture

Summary Cheat Sheet

| Fact | Detail |

|---|---|

| Queen of Social Sciences | Economics |

| Father of Economics | Adam Smith |

| Father of Modern Economics | J.M. Keynes |

| Micro & Macro terms coined by | Ragnar Frisch (1933) |

| Most accepted definition | Lionel Robbins (Scarcity) |

| Arthashastra written by | Kautilya |

| Greek root of Economics | Oikonomicas (household management) |

| Micro Economics also called | Price Theory |

| Macro Economics also called | Theory of Income & Employment |

| Nobel Prize (Welfare Economics) | Amartya Sen |

| Ceteris Paribus means | "Other things being equal" |

| Economic laws compared to | Laws of tides (Marshall) |

Lesson Doubts

Ask questions, get expert answers