🏦 Types of Banks in India: Nationalised, Private, RRB, SFB & NBFC

A guide to types of banks in India, including nationalised banks, public sector banks, private banks, RRBs, cooperative banks, small finance banks, payments banks and NBFCs.

Types of Banks and Financial Institutions in India

Legal Definition of "Banking"

As per Section 5(b) of the Banking Regulation Act, 1949, "banking" means the accepting, for the purpose of lending or investment, of deposits of money from the public, repayable on demand or otherwise, and withdrawable by cheque, draft, order or otherwise.

Similarly, Section 5(c) defines a "banking company" as any company which transacts the business of banking in India.

This definition establishes three essential functions of a bank:

- Accepting deposits from the public

- Lending or investing those deposits

- Repayment on demand or otherwise, withdrawable by cheque, draft, or order

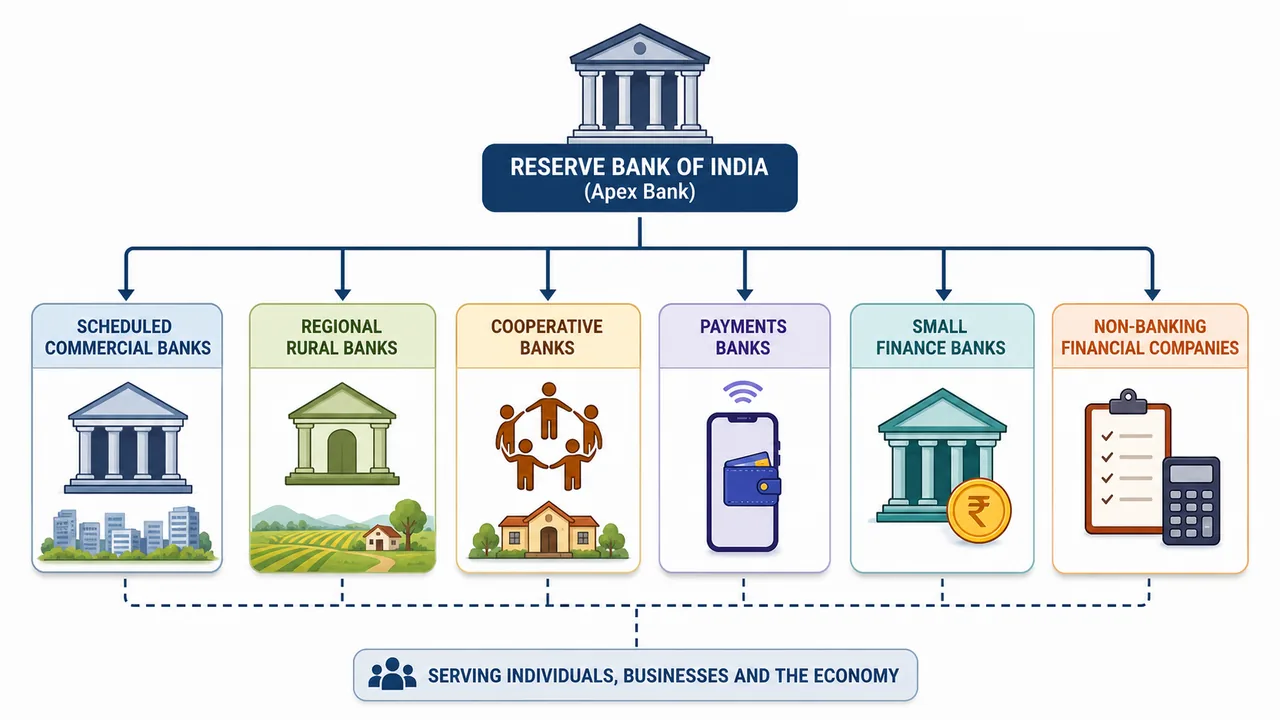

The Indian banking system is incredibly diverse, designed to cater to the financial needs of a vast population ranging from large corporate conglomerates to small marginal farmers. The Reserve Bank of India (RBI) sits at the apex of this structure, regulating and supervising the entire financial system.

Broadly, financial institutions in India can be classified into scheduled/non-scheduled banks, commercial banks, cooperative banks, specialized banks, and non-banking financial companies (NBFCs).

Scheduled Commercial Banks (SCBs)

Section 42(6)(a) of the Reserve Bank of India (RBI) Act, 1934, outlines the conditions under which the RBI can include a bank in the Second Schedule of the Act. Banks included in this schedule are referred to as Scheduled Banks.

Direct Excerpt from Section 42(6)(a) of the Act:

(a) direct the inclusion in the Second Schedule of any bank not already included therein which carries on the business of banking in India and which— (i) has a paid-up capital and reserves of an aggregate value of not less than five lakhs of rupees, and (ii) satisfies the Bank that its affairs are not being conducted in a manner detrimental to the interests of its depositors;

NOTE

Why is it called the "Second Schedule"? In legal drafting, a "Schedule" is simply an appendix attached to the end of an Act. The First Schedule of the RBI Act defines the geographical areas of India used to constitute the RBI's Local Boards. The Second Schedule is the literal second appendix to the Act—it acts as a blank ledger where the RBI maintains the running, official list of all the banks that meet its stringent criteria.

So, when we say a bank is a "Scheduled Bank," we literally just mean: "The RBI has officially written this bank's name into the second appendix of its founding rulebook."

According to this section, the RBI shall direct the inclusion of any bank in the Second Schedule if it satisfies the following two primary criteria:

1. Capital Requirement

The bank must have an aggregate value of paid-up capital and reserves of not less than five lakhs of rupees (₹5,00,000).

- Note: While this remains the statutory figure in the 1934 Act, the RBI effectively requires much higher capital norms for licensing new banks today.

2. Depositor Interest Protection

The bank must satisfy the RBI that its affairs are not being conducted in a manner detrimental to the interests of its depositors. This gives the RBI the authority to inspect the bank's books and governance before granting scheduled status.

Significance of Being a "Scheduled Bank"

When a bank is included in the Second Schedule under Section 42(6)(a), it gains certain rights and obligations:

- Access to Refinance: Scheduled banks are eligible for debts and refinance facilities from the RBI at the Bank Rate.

- Clearing House Membership: They generally obtain membership to currency chests and clearing houses.

- CRR Obligations: They are strictly required to maintain the Cash Reserve Ratio (CRR) with the RBI as per the percentages prescribed.

- Statutory Status: It acts as a "seal of quality," signifying to the public and other financial institutions that the bank meets the RBI's regulatory standards.

TIP

Market Fact: As of 2025-26, there are approximately 135 Scheduled Commercial Banks in India. This number fluctuates due to mergers, consolidations, and new licenses granted by the RBI. The SCB category broadly includes Public Sector Banks, Private Sector Banks, Foreign Banks, Small Finance Banks, and Regional Rural Banks.

Commercial Banks

Commercial banks are the backbone of the Indian financial system. Their primary business is accepting deposits from the public and granting loans to individuals and businesses for profit. Commercial banks operate on a commercial basis and their primary objective is profit maximization (alongside regulatory compliance).

They are broadly classified into three categories:

A. Public Sector Banks (PSBs)

- Ownership: The majority stake (more than 50%) is held by the Government of India.

- Examples: State Bank of India (SBI), Punjab National Bank (PNB), Bank of Baroda (BoB).

- Role: They drive massive government financial inclusion schemes (like PMJDY) and hold the largest share of deposits and advances in the country.

IMPORTANT

Nationalised / public sector banks in India -- quick exam list: Bank of Baroda, Bank of India, Bank of Maharashtra, Canara Bank, Central Bank of India, Indian Bank, Indian Overseas Bank, Punjab & Sind Bank, Punjab National Bank, State Bank of India, UCO Bank, and Union Bank of India. Use the RBI's live bank-list page as the final authority before exams because mergers and classifications can change.

| Query | Exam-safe answer |

|---|---|

| How many nationalised / public sector banks are in India? | 12 public sector banks are listed in the current RBI bank list. |

| Is SBI counted with government banks? | Yes, SBI is listed under public-sector/government-bank references, though its origin is separate from the 1969 and 1980 nationalisation rounds. |

| Which source should be trusted? | RBI's official "Banks in India" list, then the latest exam notification if a recruitment body gives a custom banking list. |

B. Private Sector Banks

- Ownership: The majority of the share capital is held by private individuals and corporations.

- Examples: HDFC Bank, ICICI Bank, Axis Bank.

- Role: Known for rapid technology adoption, aggressive lending strategies, and superior customer service. They are further divided into "Old Private Banks" (pre-1990s reforms) and "New Private Banks" (post-1991 liberalization).

Exam Focus: Regulatory Limits for Private Banks

- Minimum Capital: To get a new "Universal Banking" license from the RBI, the minimum paid-up equity capital required is now ₹1,000 crore (updated in recent years from the older ₹500 crore requirement).

- FDI Limit: The aggregate Foreign Direct Investment (FDI) limit is set at 74%. (Investment up to 49% is under the automatic route, but anything between 49% to 74% requires government approval).

- Voting Rights Cap: An extremely popular exam question! Regardless of how much equity a single shareholder owns, voting rights in a private sector bank are strictly capped at 26% under the Banking Regulation Act to prevent monopolization.

- Promoter Shareholding: The initial promoters must hold a minimum of 40% of the paid-up capital locked in for the first 5 years. This must be gradually diluted down over a 15-year span.

C. Foreign Banks

- Ownership: Incorporated outside India but operate branches or wholly-owned subsidiaries (WOS) within India.

- Examples: Citibank, Standard Chartered Bank, HSBC.

- Role: They primarily focus on corporate banking, trade finance, and wealth management for high-net-worth individuals. They bring international banking practices and technology to the Indian market.

Regional Rural Banks (RRBs)

Regional Rural Banks were established significantly on October 2, 1975, under the provisions of the RRB Act, 1976. They were created with a specific vision: to combine the local feel and familiarity of cooperative banks with the professionalism and resource base of commercial banks.

Regulatory & Key Features (Exam Focus)

- Origin Committee: They were established strictly based on the recommendations of the Narasimham Working Group (1975) on rural credit.

- The First RRB: A very common exam trivia question. The first RRB was Prathama Bank, headquartered in Moradabad, Uttar Pradesh. It was specifically sponsored by Syndicate Bank.

- Priority Sector Lending (PSL): Because their core mandate is rural inclusion, they are required to direct 75% of their total credit to the Priority Sector (compared to 40% for typical scheduled commercial banks).

- Ownership Structure: The equity of every RRB is rigidly divided in a fixed 50:35:15 ratio:

- Central Government: 50%

- Sponsor Bank (a Public Sector Bank): 35%

- State Government: 15%

- Dual Regulation: They are strictly regulated by the RBI (sets bank rates, CRR, SLR), but the statutory physical inspections and direct supervision are conducted by NABARD.

- Target Audience: Small and marginal farmers, agricultural laborers, artisans, and small entrepreneurs. They step in to eliminate rural dependence on informal moneylenders.

- Current Status: The government actively merges RRBs to rationalize costs under a "One State, One RRB" strategy. There have been no new RRBs successfully established since the Kelkar Committee (1987) recommended against setting up new ones.

Cooperative Banks

Cooperative banks operate on a cooperative basis ("no profit, no loss" or "mutual help" principle). They are registered under the Cooperative Societies Act and are regulated by both the RBI (for banking functions) and the Registrar of Cooperative Societies (for management functions).

Regulatory & Key Features (Exam Focus)

- Principle of Voting: Operates on the democratic principle of "One Member, One Vote", regardless of the number of shares held by a member. This prevents hostile takeovers by a single wealthy shareholder.

- Dual Control: A highly tested topic. They are dually regulated by:

- The Reserve Bank of India (RBI) - for banking functions (licensing, capital adequacy, PSL) under the Banking Regulation Act.

- The Registrar of Cooperative Societies (RCS) / CRCS - for administrative functions (management, elections, audits) under State/Multi-State Cooperative Acts.

- Priority Sector Lending (PSL): The RBI has strictly increased the PSL target for Urban Cooperative Banks (UCBs) up to 75% of ANBC (Adjusted Net Bank Credit), implemented in a phased manner to align closer to Small Finance Banks.

- Capital Adequacy Ratio (CRAR): They have a distinct tiered minimum capital requirement. Tier-1 UCBs must maintain a minimum CRAR of 9%, while Tier-2 to Tier-4 UCBs must maintain 12%.

- Deposit Insurance: Deposits in licensed cooperative banks (urban, state, district central) are insured by the DICGC up to ₹5 lakh per depositor. However, Primary Cooperative Societies (like PACS) are completely excluded from DICGC coverage because they are not strictly licensed/regulated as "banks" by the RBI under the Banking Regulation Act, staying purely under state governance.

They play a crucial role in rural credit. The overall structure of cooperative banking in India is as follows:

A. Urban Cooperative Banks (UCBs)

- Operate in urban and semi-urban areas.

- Primarily lend to small businesses, retail traders, and professionals.

- Classified as Scheduled UCBs and Non-Scheduled UCBs.

- Regulated heavily by the RBI, especially after recent amendments to the Banking Regulation Act.

B. Rural Cooperative Credit Structure

(i) Short-Term Credit Structure

A three-tier federal structure:

- State Cooperative Banks (SCBs) — Apex institution at the state level.

- District Central Cooperative Banks (DCCBs) — Operate at the district level, act as a link between SCBs and PACS.

- Primary Agricultural Credit Societies (PACS) — Operate at the village/grass-root level. They deal directly with rural borrowers.

(ii) Long-Term Credit Structure

A two-tier structure providing medium and long-term credit for agriculture and rural development:

- State Cooperative Agriculture and Rural Development Banks (SCARDBs) — Apex institution at the state level.

- Primary Cooperative Agriculture and Rural Development Banks (PCARDBs) — Operate at the district/taluka level, providing long-term loans directly to farmers for land development, farm mechanization, etc.

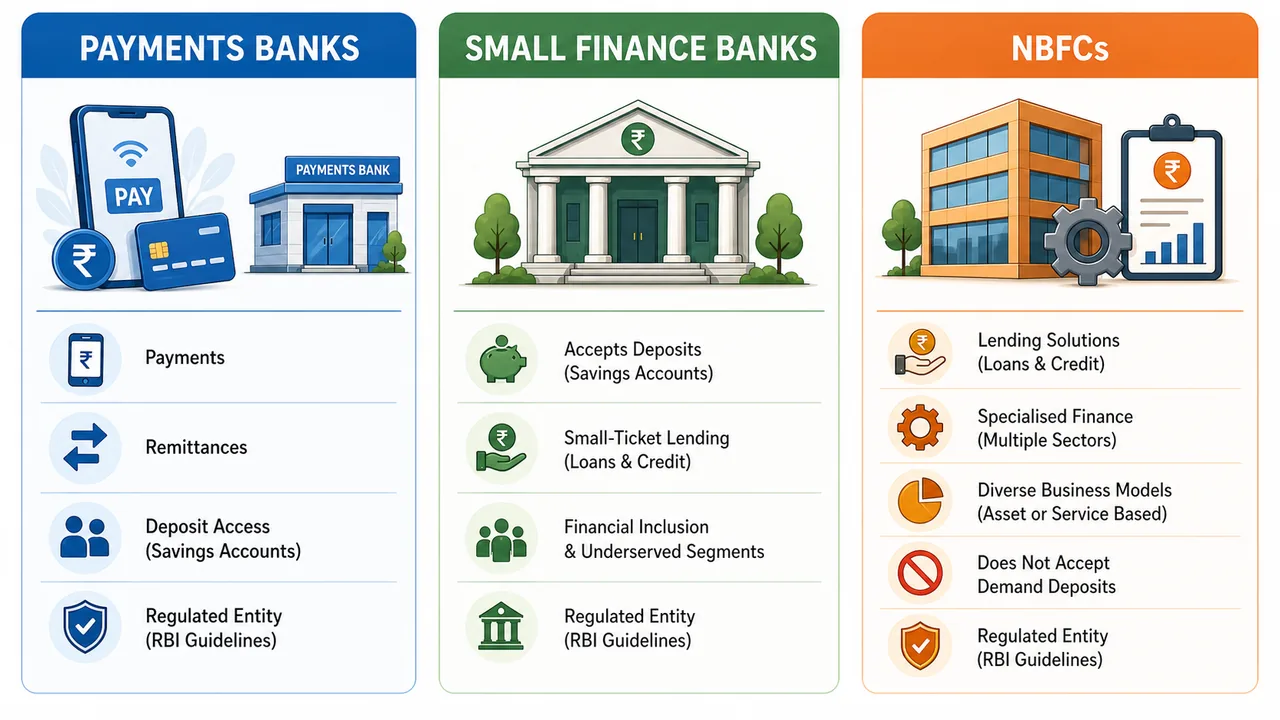

Payments Banks

Payments Banks are a relatively new model of banking introduced by the RBI to push financial inclusion further, especially targeting migrant laborers, low-income households, and small businesses.

IMPORTANT

Exam Insight: The creation of Payments Banks was recommended by the Nachiket Mor Committee (2013). The committee was constituted to explore ways to provide comprehensive financial services to small businesses and low-income households.

Key Features & Restrictions

- Acceptance of Deposits: They can accept demand deposits (Current and Savings Accounts) but cannot accept time deposits (Fixed Deposits or Recurring Deposits) or NRI deposits.

- Deposit Limit: Initially capped at ₹1 lakh, the maximum balance a customer can hold at the end of the day is now ₹2 lakh.

- Lending: They cannot advance loans or issue credit cards.

- Services: They can offer remittance services, mobile payments/transfers/purchases, issue ATM/Debit cards, and act as Business Correspondents (BC) for other banks to sell mutual funds, insurance, etc.

- Deposit Insurance: Deposits up to ₹5 lakh are fully insured by the DICGC, exactly like standard commercial banks.

- Examples: Airtel Payments Bank, India Post Payments Bank (IPPB), Paytm Payments Bank (operations restricted).

Regulatory & Capital Requirements (Exam Focus)

- Minimum Paid-up Capital: Must be at least ₹100 crore.

- Promoter Contribution: Promoters must contribute a minimum of 40% for the first 5 years.

- FDI Limit: Foreign Direct Investment is allowed up to 74%, which is the same cap as private sector banks.

- CAR Requirement: They must maintain a Capital Adequacy Ratio (CAR/CRAR) of at least 15%.

- SLR & CRR Maintenance: They must maintain Cash Reserve Ratio (CRR). For Statutory Liquidity Ratio (SLR), they are required to invest a minimum of 75% of their demand deposit balances in eligible Government securities/Treasury bills. The remaining maximum 25% can be placed as deposits with other scheduled commercial banks for operational liquidity.

Small Finance Banks (SFBs)

Small Finance Banks were established to provide basic banking activities to unserved and underserved sections of the population, including small business units, small and marginal farmers, micro and small industries, and unorganized sector entities.

While the concept to create Small Finance Banks was originally recommended by the Nachiket Mor Committee (2013), the RBI was subsequently flooded with 72 applications. To evaluate these objectively, the RBI formed an External Advisory Committee specifically for SFBs headed by former RBI Deputy Governor Usha Thorat. Therefore, in exams, note that while Nachiket Mor recommended the SFB model, Usha Thorat actually scrutinized the applications to grant the licenses.

Key Features & Operations

- Basic Operations: Unlike Payments Banks, SFBs can carry out all basic banking operations, including accepting all types of deposits (saving, current, FD, RD) and advancing loans.

- Deposit Insurance: Despite the "small" in their name, deposits up to ₹5 lakh are fully secured by the DICGC guarantee.

- Examples: AU Small Finance Bank, Equitas Small Finance Bank, Ujjivan Small Finance Bank.

Exam Focus: Regulatory Targets (SFBs)

- Minimum Capital: The minimum paid-up voting equity capital required to set up a new SFB is ₹200 crore. (For existing UCBs transitioning to SFBs, the initial requirement is ₹100 crore, to be scaled to ₹200 crore within 5 years).

- Priority Sector Lending (PSL): A heavily tested metric! SFBs are mandated to extend 60% of their ANBC to Priority Sector Lending. (Note: This was recently revised downward from their historical 75% requirement, effective April 1, 2025).

- Small Ticket Loans: At least 50% of their loan portfolio must constitute loans and advances of up to ₹25 lakh. This ensures they remain fundamentally true to their "small finance" mandate.

- Rural Branch Network: To guarantee deep rural financial inclusion, at least 25% of their branches must be opened in unbanked rural centers.

- FDI Limit: They follow the private sector commercial bank rules, permitting Foreign Direct Investment up to 74%.

Non-Banking Financial Companies (NBFCs)

NBFCs are financial institutions that provide banking services without meeting the strict legal definition of a bank. They are originally registered under the Companies Act, 1956/2013, but their financial functions are regulated by the Reserve Bank of India.

Regulatory & Classification Features (Exam Focus)

-

The "50-50" Criteria: This is a classic exam question! To be officially classified as an NBFC and supervised by the RBI, a company must pass the "Principal Business" test:

- Its financial assets must constitute more than 50% of total assets.

- Its income from financial assets must constitute more than 50% of gross income.

-

Minimum Net Owned Fund (NOF): NOF is essentially the core, unencumbered capital of the NBFC (owned capital minus investments in subsidiaries/group companies). Historically, the minimum NOF required to start a basic NBFC was ₹2 crore. However, the RBI has recently updated this to a much stricter ₹10 crore (effective October 2022).

-

Scale Based Regulation (SBR): In October 2022, the RBI replaced the old categorization system with a new four-layered regulatory framework based on size, activity, and systemic risk:

SBR Layer Key Features & Institutional Coverage Base Layer (NBFC-BL) Non-deposit taking NBFCs with asset size < ₹1,000 crore. Exclusively includes P2P Lenders, Account Aggregators (AA), and NBFCs not accessing public funds. Middle Layer (NBFC-ML) All deposit-taking NBFCs (regardless of size), non-deposit NBFCs with asset size ≥ ₹1,000 crore, Housing Finance Cos (HFCs), and Infrastructure Finance Cos (IFCs). Upper Layer (NBFC-UL) Highly systemic NBFCs objectively identified/scored by the RBI. They are strictly supervised and subjected to strict, bank-like regulatory requirements. Top Layer (NBFC-TL) Currently empty. A theoretical layer reserved for Upper Layer NBFCs if the RBI determines they pose an extreme, unsustainable systemic risk requiring immediate intervention.

Key Differences Between Banks and NBFCs (Highly Tested)

- Demand Deposits: NBFCs cannot accept demand deposits (Current and Savings Accounts). Some highly regulated NBFCs can accept term/fixed deposits, but only if explicitly authorized by RBI (Deposit-taking NBFCs / NBFC-D).

- Payment and Settlement System: NBFCs do not form part of the nation's core payment system and therefore cannot issue cheques drawn on themselves.

- Deposit Insurance: The deposit insurance mechanism of DICGC is never available to depositors of NBFCs, unlike SFBs, Payments Banks, and scheduled commercial banks.

Types of NBFCs

NBFCs are highly specialized. Common types include:

- Asset Finance Companies (AFC): Finance physical assets like tractors, equipment, cars.

- Investment Companies (IC): Deal in the acquisition of securities.

- Loan Companies (LC): Provide finance by making loans or advances.

- Infrastructure Finance Companies (IFC): Fund large infrastructure projects.

- Micro Finance Institutions (NBFC-MFI): Provide micro-credit to low-income groups.

- Housing Finance Companies (HFCs): Regulated by the National Housing Bank (NHB), they provide loans for home buying/construction.

Specialized Banks / All India Financial Institutions (AIFIs)

These are institutions set up for specific, specialized economic purposes. The four major AIFIs regulated by the RBI are:

- NABARD (National Bank for Agriculture and Rural Development): Apex body for agriculture and rural development.

- SIDBI (Small Industries Development Bank of India): Principal financial institution for the MSME sector.

- EXIM Bank (Export-Import Bank of India): Focuses on financing, facilitating, and promoting India's foreign trade.

- NHB (National Housing Bank): Apex level institution for housing finance.

- NaBFID (National Bank for Financing Infrastructure and Development): Established 2021 as a Development Financial Institution (DFI) to support infrastructure funding.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Legal Definition of Banking | Section 5(b) of Banking Regulation Act, 1949: accepting deposits for lending/investment, repayable on demand, withdrawable by cheque/draft/order |

| Banking Company | Defined under Section 5(c): any company transacting the business of banking in India |

| Scheduled Bank Definition | Listed in the Second Schedule of the RBI Act, 1934 (as per Section 42(6)(a)). Must have paid-up capital & reserves ≥ ₹5 Lakh. |

| Quick Comparison | Commercial Banks: all deposits + all loans · RRBs: rural, 50:35:15 equity · Cooperative: dual regulation · Payments Banks: cannot lend, ₹2L cap · SFBs: 60% PSL · NBFCs: no demand deposits, no DICGC · AIFIs: sector-specific apex bodies |

| Indian Banking Regulator | Reserve Bank of India (RBI) sits at the apex, regulating and supervising the entire financial system |

| Commercial Banks — Public Sector (PSBs) | Government holds >50% stake; examples: SBI, PNB, BoB; drive financial inclusion schemes like PMJDY |

| Commercial Banks — Private Sector | Majority stake held by private individuals/corporations; Old (pre-1990s) and New (post-1991); examples: HDFC Bank, ICICI Bank, Axis Bank |

| Commercial Banks — Foreign | Incorporated outside India, operate branches/WOS in India; focus on corporate banking, trade finance, wealth management; examples: Citibank, HSBC |

| Regional Rural Banks (RRBs) | Established 1975 under RRB Act 1976; equity: 50% Central Govt, 35% Sponsor Bank, 15% State Govt; regulated by RBI, supervised by NABARD |

| RRB Objective | Provide credit for agriculture and rural sectors; target: small/marginal farmers, agricultural laborers, artisans |

| Cooperative Banks — Principle | Operate on "no profit, no loss" / mutual help principle; dual regulation by RBI (banking) and Registrar of Cooperative Societies (management) |

| Rural Cooperative Credit Structure (Short-term) | Three-tier: State Cooperative Banks (SCBs) → District Central Cooperative Banks (DCCBs) → Primary Agricultural Credit Societies (PACS) at village level |

| Payments Banks — Recommended by | Nachiket Mor Committee (2013) |

| Payments Banks — Deposits | Can accept demand deposits only (Savings/Current); cannot accept time deposits (FD/RD); max end-of-day balance ₹2 lakh |

| Payments Banks — Lending | Cannot advance loans or issue credit cards; invest in Government Securities |

| Payments Banks — Metrics | Min paid-up capital ₹100 Crore; FDI limit 74%; Deposits insured by DICGC up to ₹5 lakh |

| Payments Banks — Examples | Airtel Payments Bank, India Post Payments Bank (IPPB), Paytm Payments Bank |

| Small Finance Banks (SFBs) | Provide basic banking to unserved/underserved sections; can accept all deposits and lend; Recommended by Nachiket Mor, evaluated by Usha Thorat |

| SFB — PSL Target | Must extend 60% of ANBC to Priority Sector Lending (revised from 75%, w.e.f. April 1, 2025; RBI Circular dated July 18, 2024) |

| SFB — Small Ticket Loans | At least 50% of loan portfolio must be loans up to ₹25 lakh |

| SFB — Metrics | Min paid-up capital ₹200 Crore; FDI limit 74%; Deposits fully insured by DICGC up to ₹5 lakh |

| NBFCs — Criteria & NOF | Must pass the "50-50 Criteria" (financial assets & income >50%). Minimum Net Owned Fund (NOF) recently increased to ₹10 Crore. |

| NBFCs — SBR Framework | RBI regulates them in 4 layers: Base (BL), Middle (ML), Upper (UL), and Top (TL) based on size and systemic risk. |

| NBFCs — Cannot do | Cannot accept demand deposits (Savings/Current); cannot issue cheques; No DICGC deposit insurance available |

| NBFC Types | Asset Finance Co. (AFC), Investment Co. (IC), Loan Co. (LC), Infrastructure Finance Co. (IFC), NBFC-MFI (micro-credit), Housing Finance Co. (HFC, regulated by NHB) |

| DICGC Insurance summary | Covers Scheduled Commercial Banks, SFBs, and Payments Banks (₹5 lakh cap). Never covers NBFCs or primary cooperative societies. |

| NABARD | Apex body for agriculture and rural development |

| SIDBI | Principal institution for MSME sector |

| EXIM Bank | Financing and promoting India's foreign trade |

| NHB | Apex institution for housing finance |

| NaBFID | Established 2021 as a Development Financial Institution (DFI) for infrastructure funding |

Lesson Doubts

Ask questions, get expert answers