📱 NPCI

Comprehensive overview of National Payments Corporation of India (NPCI) and its key products including UPI, BHIM, RuPay, IMPS, AePS, and FASTag.

National Payments Corporation of India (NPCI)

Overview & History

National Payments Corporation of India (NPCI), an umbrella organisation for operating retail payments and settlement systems in India, is an initiative of Reserve Bank of India (RBI) and Indian Banks’ Association (IBA).

- Establishment: Incorporated in December 2008.

- Legal Status: A ”Not for Profit” Company under Section 8 of the Companies Act 2013 (formerly Section 25 of Companies Act 1956).

- Mission: To provide infrastructure to the entire banking system in India for physical as well as electronic payment and settlement systems.

- Promoters: Initially promoted by 10 major banks. The shareholding is now broad-based to include Public Sector Banks, Private Sector Banks, Foreign Banks, Co-operative Banks, and Regional Rural Banks.

NOTE

NPCI was incorporated under Section 8 of the Companies Act 2013 (Not-for-Profit), not directly under the PSS Act. However, it derives its regulatory mandate from the Payment and Settlement Systems (PSS) Act, 2007 — the primary legislation that empowers RBI to authorize and regulate payment systems in India. In other words: Companies Act governs NPCI's existence as a company; PSS Act governs the payment systems it operates.

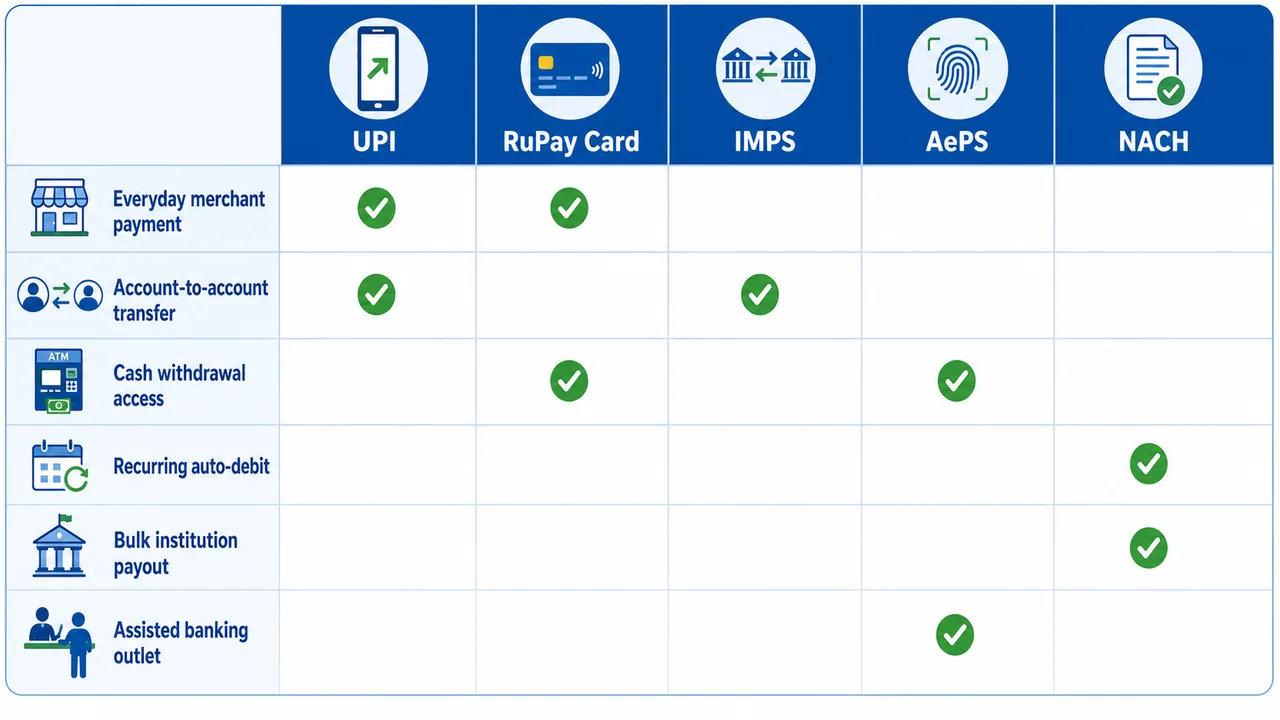

Unified Payment Interface (UPI)

Unified Payments Interface (UPI) is a system that powers multiple bank accounts into a single mobile application (of any participating bank), merging several banking features, seamless fund routing & merchant payments into one hood.

- Launch: 2016.

- Key Features: Immediate money transfer through mobile device 24x7 and 365 days.

- Identifiers: Virtual Payment Address (VPA), Mobile Number, Account Number + IFSC.

- Limits:

- P2P (Person-to-Person — individual transfers): Rs. 1 Lakh per transaction.

- P2M (Person-to-Merchant — payments to businesses/services): Enhanced limits apply for specific categories — max Rs. 5 Lakh per transaction and Rs. 10 Lakh per day (daily cumulative across all transactions). Categories covered: Capital Markets (Mutual Fund subscriptions, stock investments), Insurance premiums, Collections, Credit Card Bill Payments, Government e-marketplaces, Travel, Hospitals, Educational Institutions, IPO Subscriptions, RBI Retail Direct Scheme. (Effective Sep 15, 2025 — NPCI OC-185-B)

- UPI Lite: A simplified, on-device wallet built into UPI-enabled apps. Money is pre-loaded from the bank account into the UPI Lite balance, and payments are made offline without internet — no PIN, no OTP, instant checkout. Designed for everyday low-value purchases (tea, bus fare, etc.). Regular UPI requires an internet connection and a bank server round-trip for every payment; UPI Lite bypasses this by storing a small balance on the device itself, making it work even in low-signal areas like metro stations or rural markets.

- Transaction Limit: Rs. 1,000 per transaction (no PIN required). PIN protects large losses — RBI determined ₹1,000 is an acceptable risk ceiling in exchange for the friction-free experience. Anything above ₹1,000 falls back to regular UPI with PIN.

- Wallet Balance Limit: Max Rs. 5,000 at any time. Keeps UPI Lite as a petty-cash tool rather than a primary account substitute — limits exposure if the phone is lost or stolen.

- Daily Cap: Max Rs. 10,000 total spending per day. Even if the wallet is reloaded multiple times, the daily ceiling prevents abuse through repeated small transactions and aligns with RBI's guidelines for low-KYC Prepaid Payment Instruments (PPIs).

- UPI 123PAY: UPI for feature phone users without smartphones or internet. Customers can make payments via three modes — IVR call (dial a number), missed call, or proximity sound-based payments (phone emits inaudible ultrasonic sound; merchant device picks it up and initiates payment — no QR scan or NFC needed). Enables financial inclusion for India's non-smartphone population.

- Merchant Limit: Rs. 5,000 per transaction.

- P2P Limit: Rs. 1,000 per transaction.

- e-RUPI: A purpose-specific, one-time digital voucher issued as an SMS string or QR code — cashless and contactless. The key feature: it can only be redeemed at a specific pre-defined merchant for a specific purpose (e.g., government welfare schemes, corporate employee benefits, health vouchers). The beneficiary does not need a bank account or smartphone app to use it.

- Limit: Rs. 1 Lakh per voucher.

Bharat Interface for Money (BHIM)

BHIM is a mobile app developed by NPCI based on the Unified Payment Interface (UPI).

- Purpose: Enables quick, simple, and secure digital payments.

- Modes: App (Smartphones) or *99# (USSD for Feature phones).

- Authentication: Three levels of authentication (App bind with device ID, Mobile number, and UPI PIN).

- Transaction Limit: Rs. 1 Lakh per transaction/day.

RuPay

RuPay is an Indigenously developed card payment network like VISA/Mastercard of America. The name is derived from the words ‘Rupee and ‘Payment’.

- Launch: March 2012.

- RuPay Kisan Card: Used by Public Sector banks to provide credit to farmers.

- PaySecure: An e-commerce solution providing security for online transactions using ATM PIN.

- Insurance Benefit: Personal accident insurance (Death/Permanent Disability) of Rs. 2 Lakh (for RuPay PMJDY cards issued after 28.08.2018).

- Condition: At least one successful financial or non-financial transaction at any channel (ATM/POS/e-com) within 45 days (depending on card variant) prior to accident.

- Claim: Intimation within 90 days, Documents within 60 days.

Immediate Mobile Payment Service (IMPS)

IMPS provides robust & real time fund transfer which offers an instant, 24X7, interbank electronic fund transfer service.

- Channels: Mobile, Internet Banking, ATM, Branch.

- Registration: Mandatory for mobile banking channel.

- Identifiers:

- P2P (Person to Person): Mobile Number + MMID (Mobile Money Identifier) (7 digits).

- P2A (Person to Account): Account Number + IFSC.

- Transaction Limit: Rs. 5 Lakh (increased from Rs. 2 Lakh in Oct 2021).

Aadhaar Enabled Payment System (AePS)

AePS serves as a bank-led model which allows online interoperable financial inclusion transaction at PoS (Point of Sale / Micro ATM) through the Business Correspondent (BC)/Bank Mitra of any bank using the Aadhaar authentication.

- Inputs Required:

- IIN (Issuer Identification Number)

- Aadhaar Number

- Fingerprint

- Services: Cash Withdrawal, Cash Deposit, Balance Enquiry, Aadhaar to Aadhaar Fund Transfer, Mini Statement.

National Electronic Toll Collection (NETC) FASTag

NETC offers an interoperable nationwide toll payment solution. FASTag is a device that employs Radio Frequency Identification (RFID) technology for making toll payments directly from the prepaid or savings account linked to it.

- Usage: A tag affixed on the windscreen of the vehicle enables automatic deduction of toll charges.

- Validity: 5 years.

Bharat Bill Payment System (BBPS)

BBPS is an integrated bill payment system offering interoperable and accessible bill payment service to customers through a network of agents (Agent Institutions - AI).

- Scope: Electricity, Telecom, DTH, Gas, Water bills, etc.

- Expansion: Now covers other recurring payments like Insurance Premiums, Municipal Taxes, School Fees, etc.

National Financial Switch (NFS)

NFS is the largest network of shared Automated Teller Machines (ATMs) in India, operated by NPCI. It enables any cardholder to use any bank's ATM regardless of which bank issued their card — this interoperability is made possible through NFS acting as the central switch routing transactions between banks.

National Automated Clearing House (NACH)

NACH (operated by NPCI) has replaced the older ECS (Electronic Clearing Service) system. It is a centralised, web-based system for processing high-volume, repetitive electronic fund transfers in bulk — both credit (push) and debit (pull).

- NACH Credit: Institutions make payments to many beneficiaries at once — e.g., salary disbursement, pension, dividends, subsidy transfers (DBT).

- NACH Debit: Companies recover charges from customer accounts — e.g., loan EMIs, SIP investments, insurance premiums, utility bills.

- e-Mandate: A digital standing instruction authorizing recurring debits (e.g., "debit my account every month for my loan EMI"). Unlike the old paper-based ECS mandate requiring physical signatures, e-Mandates are created and authenticated online — faster to set up, easier to modify or cancel.

- Settlement Cycle: T+1 — transactions initiated on day T are settled by the next business day.

- Amount Limits: No minimum or maximum transaction amount limit.

- TReDS (Trade Receivables Discounting System): NPCI facilitates TReDS settlement — a platform where MSMEs discount their trade receivables (invoices) to get early payment from financiers.

- Per-mandate settlement limit: Enhanced to Rs. 3 Crore (from Rs. 1 Crore).

National Common Mobility Card (NCMC)

NCMC is India's "One Nation One Card" initiative — a single RuPay-based card that works across all forms of public transport (Metro, Bus, Suburban Rail, Toll, Parking) as well as for retail purchases. It uses an offline contactless chip so transit gates can process payments instantly without internet. Launched under the Ministry of Housing and Urban Affairs.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| NPCI — Full Form | National Payments Corporation of India; umbrella org for retail payments & settlement |

| NPCI — Established | Incorporated December 2008 |

| NPCI — Legal Status | Not-for-Profit company under Section 8 of Companies Act 2013 |

| NPCI — Incorporated under | Section 8, Companies Act 2013 (Not-for-Profit) |

| NPCI — Regulatory mandate from | Payment and Settlement Systems Act, 2007 — gives RBI authority to set up & regulate payment systems; initiative of RBI and IBA |

| UPI — Full Form | Unified Payments Interface; launched 2016 |

| UPI — P2P Limit | ₹1 lakh per transaction (individual transfers) |

| UPI — P2M Enhanced Limit | ₹5 lakh/txn, ₹10 lakh/day for: Capital Markets, Insurance, Collections, Credit Card Bills, Govt e-marketplaces, Travel, Hospitals, Educational Institutions, IPO, RBI Retail Direct (w.e.f. Sep 15, 2025) |

| UPI Lite | On-device offline wallet; txn limit ₹1,000 (no PIN); wallet limit ₹5,000; daily cap ₹10,000 |

| UPI 123PAY | UPI for feature phones (no internet); via IVR call, missed call, or sound-based; merchant ₹5,000/txn; P2P ₹1,000/txn |

| e-RUPI | Purpose-specific one-time digital voucher (SMS/QR); redeemable only at pre-defined merchant for pre-defined purpose; no bank account needed; limit ₹1 lakh |

| BHIM — Full Form | Bharat Interface for Money; mobile app by NPCI based on UPI |

| BHIM — Authentication | Three levels: device ID bind, mobile number, UPI PIN |

| BHIM — Limit | ₹1 lakh per transaction/day |

| BHIM — Feature Phone | Access via *99# (USSD) |

| RuPay | Indigenous card payment network; name from Rupee + Payment; launched March 2012 |

| RuPay Kisan Card | Used by PSBs to provide credit to farmers |

| RuPay — Insurance | Personal accident insurance ₹2 lakh (death/permanent disability) for PMJDY cards issued after 28.08.2018 |

| RuPay Insurance — Condition | At least one successful transaction within 45 days prior to accident |

| RuPay Insurance — Claim | Intimation within 90 days; documents within 60 days |

| IMPS — Full Form | Immediate Mobile Payment Service; real-time, 24x7 interbank transfer |

| IMPS — Channels | Mobile, Internet Banking, ATM, Branch |

| IMPS — P2P Identifiers | Mobile Number + MMID (7 digits) |

| IMPS — P2A Identifiers | Account Number + IFSC |

| IMPS — Limit | ₹5 lakh (increased from ₹2 lakh, Oct 2021) |

| AePS — Full Form | Aadhaar Enabled Payment System; bank-led model using Aadhaar authentication |

| AePS — Inputs Required | IIN, Aadhaar Number, Fingerprint |

| AePS — Services | Cash Withdrawal, Cash Deposit, Balance Enquiry, Aadhaar-to-Aadhaar transfer, Mini Statement |

| FASTag — Technology | RFID (Radio Frequency Identification); tag on vehicle windscreen |

| FASTag — Validity | 5 years |

| BBPS | Bharat Bill Payment System; interoperable bill payment (electricity, telecom, DTH, gas, water, insurance, taxes, fees) |

| NFS | National Financial Switch; largest shared ATM network in India; enables any card at any bank's ATM via central routing |

| NACH — Operated by | NPCI; replaced older ECS system; web-based bulk transfer platform |

| NACH — Settlement Cycle | T+1 (next business day) |

| NACH — Amount Limits | No minimum or maximum |

| NACH Credit | Institution pays many beneficiaries — salaries, pensions, dividends, DBT subsidies |

| NACH Debit | Companies recover charges — loan EMIs, SIPs, insurance premiums, utility bills |

| NACH — e-Mandate | Digital standing instruction for recurring debits; replaces paper ECS mandate; set up and modified online |

| NACH — TReDS Limit | Per-mandate settlement limit ₹3 crore (enhanced from ₹1 crore) |

| NCMC | National Common Mobility Card — "One Nation One Card"; RuPay-based; works for Metro, Bus, Rail, Toll, Parking + retail; offline contactless chip |

Lesson Doubts

Ask questions, get expert answers