💳 Cards, ATMs and Wallets

Rules regarding ATM usage, White Label ATMs, POS Transactions, and Prepaid Payment Instruments (PPIs).

Types of ATMs

An ATM (Automated Teller Machine) is an electronic device that allows customers to perform basic banking operations — cash withdrawal, balance inquiry, mini-statement, PIN change — without visiting a branch.

By Location

- On-site ATM: Installed within bank premises (inside or adjacent to branch). Operated directly by the bank.

- Off-site ATM: Installed outside bank premises — malls, airports, petrol stations, etc. May be owned by banks or third parties.

- Mobile ATM: ATM mounted on a vehicle that travels to remote/rural areas or events where fixed ATMs don't exist.

By Ownership

- Bank ATM: Owned and operated by the bank itself (e.g., SBI ATMs, HDFC ATMs).

- White Label ATM (WLA): Owned by non-bank entities (e.g., Tata Communications, Hitachi) incorporated in India — no bank branding visible. Purpose: expand ATM reach into rural/semi-urban areas where banks don't operate. Minimum net worth required: Rs. 100 crore.

- Brown Label ATM: Hardware and ATM location are owned by a third-party service provider, but cash management and banking network are provided by a sponsor bank. A hybrid — not fully bank-owned, not fully independent like WLA.

By Function / Purpose

- Green Label ATM: Exclusively for agricultural transactions (e.g., Kisan Credit Card withdrawals).

- Yellow Label ATM: Set up for e-commerce transactions.

- Pink Label ATM: Dedicated to women customers — separate queue, women-only machines for safety.

- Orange Label ATM: Used for share/securities transactions.

- Biometric ATM: Uses fingerprint or iris scan instead of PIN — designed for rural/semi-literate customers who cannot remember PINs.

- Cash Recycler Machine (CRM): Accepts cash deposits AND dispenses cash — combines the functions of a cash deposit machine and ATM in one unit.

Free ATM Access Policy

Customers can use ATMs of any bank for transactions in Savings Bank (SB) accounts. Rules apply to White Label ATMs as well.[1]

- Single Withdrawal Limit: You can withdraw a maximum of Rs. 10,000 in a single go.

- Free Transactions: You get a minimum of 5 free transactions per month at your own bank's ATM.

- Other Bank ATMs: You get 3 free transactions in Metro cities (Mumbai, New Delhi, Chennai, Kolkata, Bengaluru, Hyderabad) and 5 free in non-metro centers.

- Charges Limits: If you exceed these free limits, the bank charges you. The RBI has capped this charge at Rs. 23 per transaction (effective May 1, 2025).

Understanding "Interchange Fee"[1]

When you use another bank's ATM (e.g., using an HDFC card at an SBI ATM), your bank (HDFC) pays a fee to the ATM operator (SBI). This is called the Interchange Fee.

- Financial Transaction (Cash Withdrawal): Rs. 19 (previously Rs. 17).

- Non-Financial Transaction (Balance Check): Rs. 7 (previously Rs. 6).

- Note: This cost is usually borne by your bank, but if you cross the free limit, they pass it to you (max Rs. 23).

Failed ATM Transactions

If account is debited but cash not dispensed:

- Reporting: Customer to inform bank within 30 days.

- Resolution: Bank to resolve within T + 5 days — here "T" is the date of the failed transaction (not the complaint date).

- Compensation: Rs. 100 per day for delay beyond T+5 (paid automatically, no need to claim).

Cash-out at ATMs

RBI takes strict action if ATMs run dry.

- Penalty: If an ATM is out of cash for more than 10 hours in a month, the bank pays a flat penalty of Rs. 10,000 per ATM.

- Reporting: Banks must submit a "Cash-out Report" to the RBI monthly.

Cardless Cash Withdrawal (ATM)

You can send money to a person who withdraws it at an ATM without a physical card. The mechanism: sender initiates via mobile banking → recipient receives a one-time OTP/code → enters the code at ATM → cash dispensed.

- Limit: Rs. 10,000/txn (Max Rs. 25,000/month).

Point of Sale (POS) and Cards

Withdrawal of Cash at POS (Debit Card)

Did you know you can withdraw cash at a shop's POS machine using your debit card?

- Limit: Rs. 2,000 per transaction (in Tier I & II centers) / Rs. 1,000 in smaller centers.

- Monthly Cap: Rs. 10,000.

- Charges: Banks can charge up to 1% of the amount for this facility.

Card Transactions in Contactless Mode (NFC)

For faster checkout, you can just "Tap and Pay" without a PIN.

AFA (Additional Factor of Authentication): Any second layer of verification beyond the card itself — typically a PIN, OTP, or biometric. RBI mandates AFA for digital transactions to prevent fraud. Some low-value scenarios are exempted for convenience.

- No PIN Limit: Transactions up to Rs. 5,000 do not require AFA (PIN). Just tap and go.

- Security: Any transaction above Rs. 5,000 still mandatorily requires a PIN.

Card-on-File (CoF) Tokenization[2]

- The Rule: To improve security, the RBI mandated that merchants cannot store actual card numbers. Only the Card Issuer and Card Networks (Visa/Mastercard) can. So, websites like Amazon/Netflix cannot save your card details for future payments.

- Tokenization: The actual card details are replaced with a unique alternate code called a "Token". This token is unique to the device and the merchant. Even if the merchant is hacked, your actual card details are safe.

Credit Card Billing & Conduct (New Rules 2024)[2]

- Billing Cycle: Cardholders must be given the option to choose their billing cycle.

- Closure: Request for closure must be honored within 7 working days. Failure attracts penalty of Rs. 500 per day.

- Billing Statement: Issued immediately after the billing cycle ends; the cardholder must be given a minimum 15-day grace period before the payment due date (so you have at least 15 days to pay after receiving the bill).

Processing of E-Mandates (Recurring Payments)[2]

For auto-debits like Netflix, Utility Bills, or SIPs:

- General Limit: Recurring payments up to Rs. 15,000 do not need an OTP for every transaction.

- Enhanced Limit: For critical financial payments — Mutual Fund subscriptions, Insurance premiums, and Credit Card bill payments — the limit is Rs. 1 Lakh.

- Notification: The bank must send you a notification 24 hours before the money is cut, giving you a chance to stop it if needed.

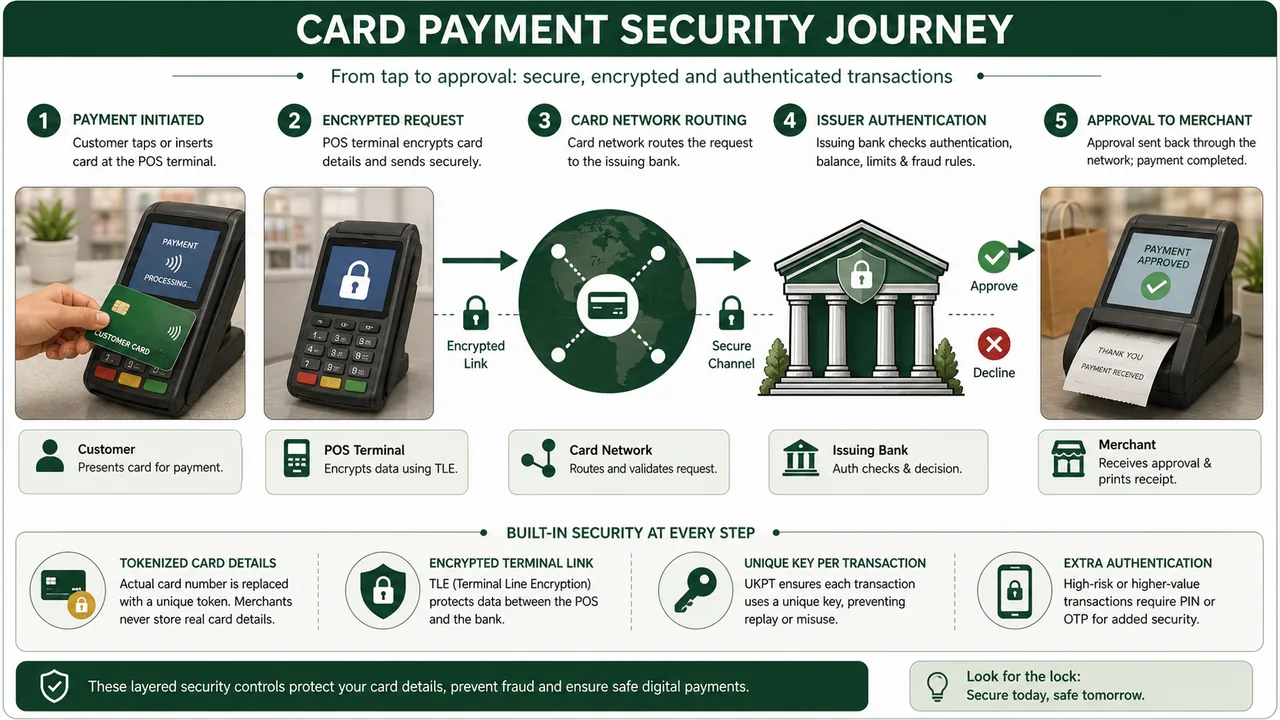

Fraudulent POS Transactions

POS terminals must meet RBI security standards to protect card data:

- TLE (Terminal Line Encryption): Encrypts data transmitted between the POS terminal and the bank's server so it cannot be intercepted.

- UKPT (Unique Key Per Transaction): Each transaction uses a unique encryption key, so capturing one transaction's data cannot be used to replicate another.

If a customer reports fraud at POS:

- Issuing Bank: Ascertains if POS was TLE/UKPT compliant within 3 days.

- Non-compliant POS: Bank pays the disputed amount within 3 days. Delay compensation Rs. 100/day.

- Acquiring Bank: Must reimburse the issuing bank within 3 days of claim if POS was non-compliant.

Pre-Paid Instruments (PPIs)

PPIs are wallets and cards (like Paytm Wallet, Amazon Pay, Gift Cards) issued under the PSS Act 2007.[3] Unlike a bank account where your money is held by the bank, a PPI works on a preloaded model — you first deposit money into the PPI, and can only spend what you've loaded. This is why RBI imposes balance and loading limits — the risk is capped to what's already inside.

Types of PPIs:

-

Small PPIs (Minimum Detail):

- Purpose: Quick onboarding for small payments.

- Restrictions: You can only buy goods/services. No fund transfer or cash withdrawal.

- Limits: Max Rs. 10,000 loaded/month. Must convert to Full KYC within 24 months.

-

Full KYC PPIs:

- Purpose: Full-featured wallet after submitting ID proof.

- Features: Allows Funds Transfer (to bank/wallet) and Cash Withdrawal.

- Limits: Max balance Rs. 2 Lakh. Fund transfer limit Rs. 2 Lakh/month.

- Cash Withdrawal: Rs. 2,000/txn, Rs. 10,000/month.

General PPI Rules:

-

Net Worth: Non-bank issuers need Rs. 5 cr net worth at entry, increasing to Rs. 15 cr within 3 years.

-

Validity: Minimum validity is 1 year (usually issued for 3 years).

-

Cross Border: You can use PPIs for outbound payments (goods/services) up to Rs. 10,000/txn and Rs. 50,000/month.

-

Interoperability: It is now mandatory for Full KYC PPIs to work across different networks. In practice this means: a customer with a Paytm wallet can scan a PhonePe QR code and pay — they are not locked into one platform's ecosystem. This is enforced via UPI and NPCI infrastructure.

-

Gift PPIs:

- Purpose: Non-reloadable instruments issued for gifting purposes.

- Limits: Maximum value of Rs. 10,000.

- Restrictions: No cash withdrawal or fund transfer is permitted.

-

PPIs for Mass Transit Systems (PPI-MTS):

- Purpose: Issued by transit operators (Metro, Bus, Rail) for fare collection.

- Limits: Maximum outstanding balance of Rs. 2,000.

- Features: These do not require a PIN/OTP (AFA) to ensure fast movement at transit gates.

References

5 sources • [1] [2] [3] [4] [5]

References

Used for: Covers free transaction limits, Rs.23 charge cap (w.e.f. May 2025), interchange fees (Rs.19/Rs.7), cash-out penalty, WLA net worth, failed transaction T+5 rules.

Used for: Governs card-on-file tokenization, credit card billing cycle, 7-day closure rule, 15-day grace period, e-mandate limits (Rs.15,000 / Rs.1 lakh), 24-hour pre-debit notification.

Used for: Covers Small PPI and Full KYC PPI limits, issuer net worth (Rs.5cr/Rs.15cr), validity, cross-border limits, interoperability mandate, Gift PPIs, PPI-MTS.

Used for: IMPS per transaction limit: Rs. 5 lakh (all channels except SMS/IVR). 24x7 availability including holidays.

Used for: UPI transaction limits: standard P2P Rs.1 lakh. Enhanced P2M (w.e.f. Sep 15, 2025): Rs.5 lakh/txn, Rs.10 lakh/day for Capital Markets, Insurance, Collections, Credit Card Bills, Government e-marketplaces, Travel, Hospitals, Educational Institutions, IPO, RBI Retail Direct. UPI Lite (Rs.500/txn, Rs.2,000 wallet) and UPI 123Pay (Rs.5,000 merchant, Rs.1,000 P2P).

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| ATM Single Withdrawal Limit | Max ₹10,000 per transaction |

| Free ATM Transactions — Own Bank | Minimum 5 free per month |

| Free ATM Transactions — Other Bank (Metro) | 3 free per month (Mumbai, New Delhi, Chennai, Kolkata, Bengaluru, Hyderabad) |

| Free ATM Transactions — Other Bank (Non-Metro) | 5 free per month |

| ATM Charge Cap | Max ₹23 per transaction (effective May 1, 2025) |

| Interchange Fee — Financial (Cash) | ₹19 per transaction |

| Interchange Fee — Non-Financial (Balance) | ₹7 per transaction |

| Failed ATM Transaction — Reporting | Customer must inform bank within 30 days of failed transaction |

| Failed ATM Transaction — Resolution | Bank must resolve within T + 5 days; compensation ₹100/day for delay beyond T+5 |

| White Label ATMs (WLAs) | Owned by non-bank entities (incorporated in India); purpose: expand ATM reach in rural/semi-urban areas; min net worth ₹100 crore |

| ATM Cash-out Penalty | Out of cash >10 hours/month: flat penalty ₹10,000 per ATM |

| Cardless Cash (ATM) | ₹10,000/txn, max ₹25,000/month |

| POS Cash Withdrawal (Debit Card) | ₹2,000/txn (Tier I & II); ₹1,000 (smaller centers); monthly cap ₹10,000; charge up to 1% |

| Contactless (NFC) — No PIN Limit | Transactions up to ₹5,000 — no PIN required; above ₹5,000 PIN mandatory |

| Card-on-File Tokenization | Merchants cannot store actual card numbers; only Card Issuer and Card Networks (Visa/Mastercard) can; card replaced by a unique Token |

| Credit Card Billing Cycle | Cardholder must be given option to choose billing cycle |

| Credit Card Closure | Must be honored within 7 working days; delay penalty ₹500/day |

| Credit Card — Grace Period | Minimum 15 days between billing statement and payment due date |

| E-Mandate (Recurring) — General Limit | Up to ₹15,000 — no OTP needed per transaction |

| E-Mandate — Enhanced Limit | Up to ₹1 lakh for Mutual Funds, Insurance premiums, Credit Card bills |

| E-Mandate — Notification | Bank must notify customer 24 hours before auto-debit |

| Small PPIs (Min Detail) | Max load ₹10,000/month; goods/services only; no fund transfer or cash withdrawal; must convert to Full KYC within 24 months |

| Full KYC PPIs | Max balance ₹2 lakh; fund transfer ₹2 lakh/month; cash withdrawal ₹2,000/txn, ₹10,000/month |

| PPI Issuer Net Worth | Non-bank: ₹5 crore at entry, ₹15 crore within 3 years |

| PPI Minimum Validity | 1 year |

| PPI Cross-Border | Outbound: ₹10,000/txn, ₹50,000/month |

| PPI Interoperability | Mandatory for Full KYC PPIs across networks |

| Gift PPIs | Non-reloadable; max ₹10,000; no cash withdrawal/fund transfer |

| PPI-MTS (Mass Transit) | Max balance ₹2,000; no PIN/OTP required |

| Fraudulent POS — Compliance | POS must be TLE (Terminal Line Encryption) + UKPT (Unique Key Per Transaction) compliant |

| Fraudulent POS — Resolution | Issuing bank ascertains compliance within 3 days; non-compliant POS → bank pays disputed amount in 3 days; delay penalty ₹100/day |

Lesson Doubts

Ask questions, get expert answers