🛡️ Anti-Money Laundering (AML) & PMLA

How money laundering works, the PMLA 2026 framework, FATF, FIU-IND, terrorism financing, offences, punishments, and bank obligations explained pedagogically.

A drug trafficker in Mumbai earns ₹5 crore in cash. He cannot deposit it in a bank — that would trigger questions. He cannot spend it openly — that would trigger an income tax investigation. So he needs to make this dirty money look clean. The process he uses is called money laundering, and stopping it is the central mission of every bank's compliance team. While KYC (the previous lesson) verifies who a customer is, AML ensures the bank is not used as a washing machine for criminal money. Together they form India's first line of defence against financial crime.

How Money Laundering Actually Works

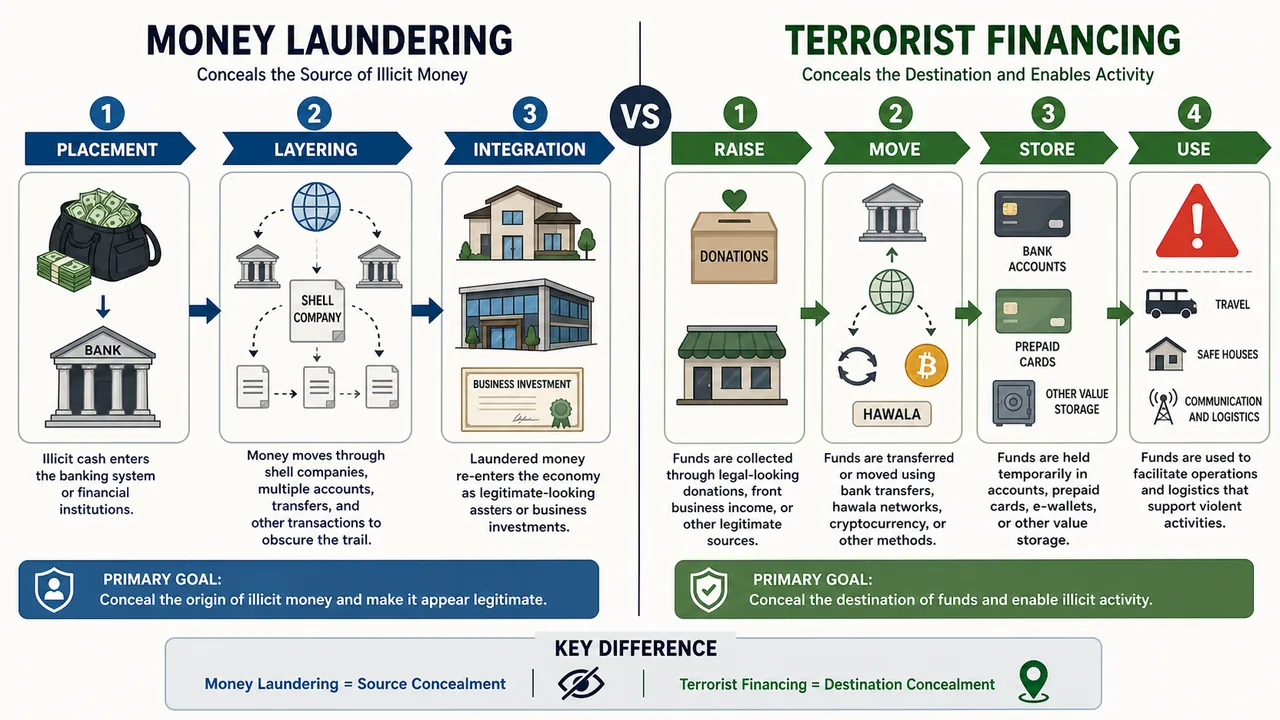

Imagine money laundering as a three-act play. The criminal must move the cash through three carefully designed stages — each stage solving a specific problem.

The Three Stages

| Stage | The Problem It Solves | What Happens |

|---|---|---|

| 1. Placement | "How do I get cash into the banking system without raising alarms?" | The dirty cash is broken into small amounts and deposited across many accounts, often through cooperative shopkeepers, restaurants, or "smurfing" (multiple sub-threshold deposits). This is the riskiest stage for the launderer. |

| 2. Layering | "How do I hide the trail back to the original crime?" | The money is moved through dozens or hundreds of transactions — wire transfers, fake invoices, shell companies in tax havens, cryptocurrency conversions. Each layer makes the audit trail harder to follow. |

| 3. Integration | "How do I bring the cleaned money back into the open economy?" | The funds re-enter the economy as legitimate-looking investments — real estate, businesses, luxury goods. At this point, the money is "clean" on paper. |

TIP

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

A drug trafficker in Mumbai earns ₹5 crore in cash. He cannot deposit it in a bank — that would trigger questions. He cannot spend it openly — that would trigger an income tax investigation. So he needs to make this dirty money look clean. The process he uses is called money laundering, and stopping it is the central mission of every bank's compliance team. While KYC (the previous lesson) verifies who a customer is, AML ensures the bank is not used as a washing machine for criminal money. Together they form India's first line of defence against financial crime.

How Money Laundering Actually Works

Imagine money laundering as a three-act play. The criminal must move the cash through three carefully designed stages — each stage solving a specific problem.

The Three Stages

| Stage | The Problem It Solves | What Happens |

|---|---|---|

| 1. Placement | "How do I get cash into the banking system without raising alarms?" | The dirty cash is broken into small amounts and deposited across many accounts, often through cooperative shopkeepers, restaurants, or "smurfing" (multiple sub-threshold deposits). This is the riskiest stage for the launderer. |

| 2. Layering | "How do I hide the trail back to the original crime?" | The money is moved through dozens or hundreds of transactions — wire transfers, fake invoices, shell companies in tax havens, cryptocurrency conversions. Each layer makes the audit trail harder to follow. |

| 3. Integration | "How do I bring the cleaned money back into the open economy?" | The funds re-enter the economy as legitimate-looking investments — real estate, businesses, luxury goods. At this point, the money is "clean" on paper. |

TIP

Memory aid — PLI: Placement (entry), Layering (concealment), Integration (re-use). The criminal's hardest job is Placement — that's where banks must catch them. Once layering begins, the trail is already going cold.

What "Money Laundering" Really Means

Stripped of jargon, money laundering is the processing of criminal proceeds to disguise their illegal origin. The criminals are usually involved in drug trafficking, gun smuggling, corruption, tax evasion, Ponzi schemes, and increasingly, cybercrimes — which now constitute a significant share of laundered funds globally.

Terrorist Financing — A Related but Distinct Problem

Money laundering and terrorist financing share the same techniques, but they are mirror opposites in one crucial way:

| Money Laundering | Terrorist Financing | |

|---|---|---|

| Source of funds | Illegal (proceeds of crime) | Often legal (donations, charities, businesses) |

| Goal | Hide the origin (make dirty money look clean) | Hide the destination (make clean money fund violence) |

| Tactics | Placement → Layering → Integration | Raise → Move → Store → Use |

This is why AML and CFT (Combating the Financing of Terrorism) are usually treated together in regulations.

The 4 Stages of Terrorism Financing

Where money laundering has 3 stages, terror financing has four:

| Stage | What Happens |

|---|---|

| 1. Raise | Sympathisers, individuals, NGOs, and front businesses contribute funds. Some come from extortion or smuggling, but many come from legal sources (donations, fake charities). |

| 2. Move | Funds are moved across borders to wherever the terror cell is operating. Hawala, wire transfers, and cryptocurrency are common channels. |

| 3. Store | Funds are parked temporarily — bank accounts, prepaid cards, or financial investments — until needed. |

| 4. Use | Final deployment for attacks, recruitment, weapons, or operational expenses. |

IMPORTANT

Because OCGs (Organized Crime Groups) and PMLs (Professional Money Launderers) often work with terror financiers — sharing the same hawala networks and shell companies — modern AML laws treat ML and TF as overlapping threats.

India's Legal Framework — PMLA 2002

In response to global pressure (especially from FATF, discussed below), India enacted the Prevention of Money Laundering Act, 2002 (PMLA) — the principal law governing money laundering offences in India.

The Three Key Sections to Remember

| Section | What It Does |

|---|---|

| Sec. 3 | Defines the offence — anyone who "directly or indirectly attempts to indulge or knowingly assists" in any process connected with proceeds of crime, including its concealment, possession, acquisition, or projecting it as untainted, is guilty of money laundering. |

| Sec. 4 | Punishment — Rigorous imprisonment of 3 to 7 years + fine. If the offence is linked to the NDPS Act (drugs), imprisonment can extend to 10 years. |

| Sec. 45 | All PMLA offences are cognizable and non-bailable. This means police can arrest without a warrant, and the accused has no automatic right to bail. |

What is "Proceeds of Crime"?

Under PMLA, "proceeds of crime" means any property derived directly or indirectly by any person as a result of criminal activity relating to a scheduled offence — or the value of any such property.

In simple terms: if the property exists because of a crime listed in the PMLA Schedule, it counts.

The Schedule — What Crimes Trigger PMLA?

The PMLA Schedule lists "predicate offences" — the underlying crimes whose proceeds become subject to PMLA. The schedule has three parts:

| Part | Offences Covered |

|---|---|

| Part A | Offences under IPC, NDPS Act, Explosive Substances Act, Unlawful Activities (Prevention) Act, Arms Act, Wild Life (Protection) Act, Immoral Traffic (Prevention) Act, Prevention of Corruption Act, Antiquities and Art Treasures Act, and others |

| Part B | False declarations and false documents |

| Part C | Trans-border crimes — designed to tackle money laundering across global boundaries |

TIP

Exam shortcut: Part A = "the big list" of criminal acts (drugs, arms, terror, corruption). Part B = paperwork fraud. Part C = international/cross-border laundering.

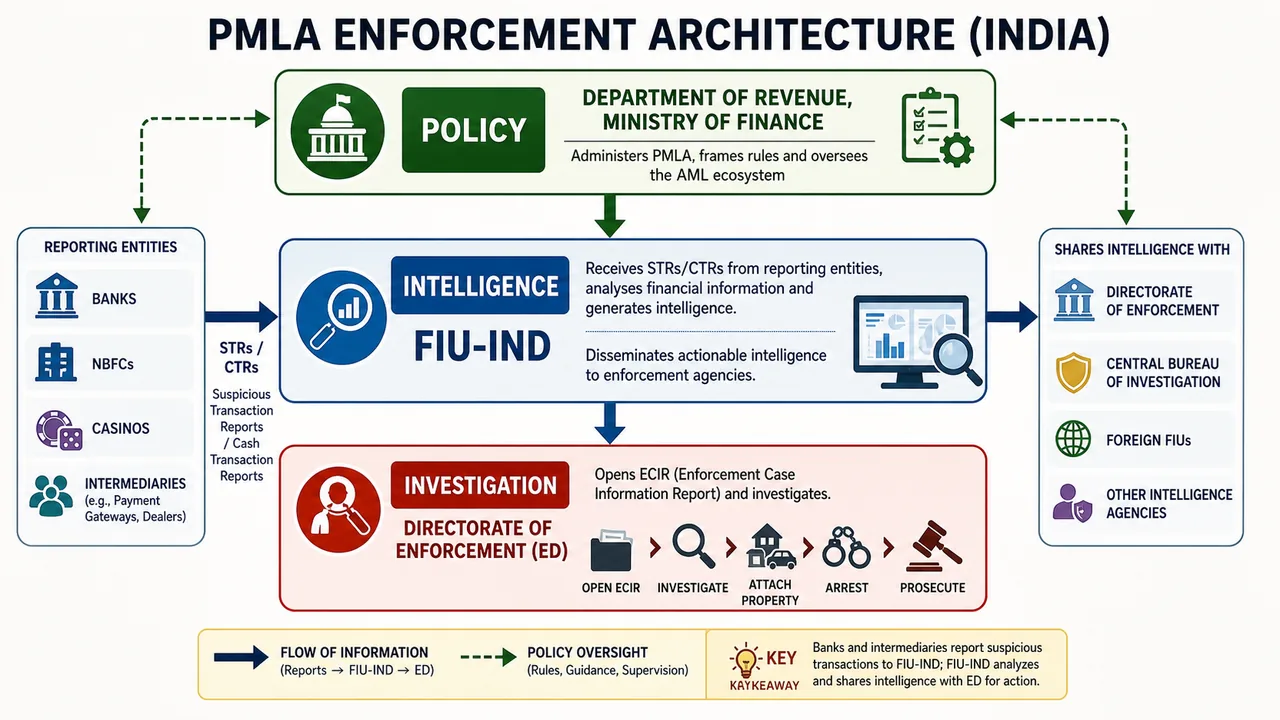

Who Enforces PMLA? The Three-Layer Architecture

PMLA enforcement in India works as a chain of three agencies, each with a distinct role:

| Layer | Agency | What It Does |

|---|---|---|

| Policy | Department of Revenue, Ministry of Finance | Administers the PMLA, frames rules, oversees the entire AML ecosystem |

| Investigation | Directorate of Enforcement (ED) | Files an ECIR (Enforcement Case Information Report) to start an investigation. Has powers to attach property, arrest, and prosecute. |

| Intelligence | Financial Intelligence Unit – India (FIU-IND) | The central national agency for receiving, processing, analysing, and disseminating information about suspect financial transactions. Reports come from banks, NBFCs, casinos, and intermediaries — and FIU-IND shares findings with ED, CBI, foreign FIUs, and intelligence agencies. |

IMPORTANT

Banks file STRs (Suspicious Transaction Reports) and CTRs (Cash Transaction Reports) to FIU-IND. This is the data that triggers most ED investigations — making banks the eyes and ears of the AML system.

The Wolfsberg AML Principles — A Private-Sector Standard

While FATF is the governmental standard, the private banking industry has its own voluntary code: the Wolfsberg Anti-Money Laundering (AML) Principles. These were developed by the Wolfsberg Group — a consortium of thirteen global banks (not the World Bank, not the IMF, not FATF) that meets in the Swiss village of Wolfsberg to agree on common AML standards.

What the Principles Aim To Do

The Wolfsberg Principles provide a unified approach for financial institutions to combat money laundering and terrorist financing. Their primary goal is to promote international trade and commerce through a common baseline of integrity — not to replace FATF or local law, but to promote customer due diligence, risk assessment, reporting of suspicious activities, and international cooperation across member institutions.

The Ten Core Wolfsberg Principles

The principles are broadly organised around the following themes:

- Customer Due Diligence (CDD) — Verify customer identities and assess risk profiles.

- Risk Assessment — Develop a formal risk-assessment framework for customer activity.

- Suspicious Activity Reporting (SAR) — Establish a system to promptly report suspicious transactions.

- Compliance Management — Develop an AML compliance programme aligned with regulations.

- Record Keeping — Maintain accurate records of transactions for prescribed periods.

- International Cooperation — Collaborate with global partners to combat financial crime.

- Training and Awareness — Provide AML training to employees and vendor partners.

- Technology and Innovation — Use advanced tools for AML detection and prevention.

- Continuous Improvement — Regularly assess and enhance AML measures.

- Source of Funds Verification — Ensure transparency in the source of funds for transactions.

Additional themes touched by Wolfsberg include Politically Exposed Persons (PEPs) (enhanced due diligence for PEP relationships), transaction monitoring for unusual patterns, AML officer appointment to oversee compliance efforts, information sharing about customers with regulators while maintaining privacy, and adherence to international standards and guidelines.

IMPORTANT

Exam trap: When asked "Which organization developed the Wolfsberg AML Principles?" — the answer is the Wolfsberg Group (a consortium of global banks), NOT the World Bank, IMF, or FATF. When asked "What is the primary goal of the Wolfsberg Principles?" — the answer is to promote international trade and commerce (not to facilitate tax evasion, increase interest rates, or promote money laundering).

Trade Based Money Laundering (TBML)

TBML stands for Trade Based Money Laundering — not "Layering," not "Lifting," not "Lending." It is the process of disguising the proceeds of crime and moving value through trade transactions to legitimise their illicit origins. Common TBML techniques include over-invoicing, under-invoicing, multiple invoicing, over- or under-shipment, and falsely described goods.

Prevention: TBML can be prevented by adopting the basic principles of Customer Due Diligence (CDD), Customer Identification Procedure (CIP), and Customer Relationship Procedure (CRP) — i.e., all three pillars of the KYC framework, not any single one in isolation.

The Global Standard — FATF

PMLA was not invented in isolation. It exists because India is part of an international standard-setting body called the Financial Action Task Force (FATF).

| FATF — At a Glance | |

|---|---|

| Founded | July 1989 |

| Founder | G7 (Group of Seven industrialised nations) |

| Headquarters | Paris, France |

| What it does | Sets global standards for AML and CFT (Combating Financing of Terrorism) |

| Standards | 40 Recommendations — known as the FATF Standards 2012 — followed by 200+ jurisdictions worldwide |

Countries that fail to comply with FATF recommendations risk being grey-listed or black-listed, which can cripple foreign investment. India's PMLA, KYC norms, and bank reporting obligations are all designed to keep India FATF-compliant.

Banks at the Frontline — Obligations under PMLA

Banks are not passive observers — PMLA imposes active duties on every reporting entity (banks, NBFCs, payment gateways, crypto exchanges, etc.).

The Five Core Obligations

| Obligation | What It Requires |

|---|---|

| Transaction Records | Maintain records so that individual transactions can be reconstructed — date, parties, amount, purpose. |

| Confidentiality | Information collected must remain confidential, except when disclosed under legal compulsion. |

| Record Retention | Keep transaction records for at least 5 years from the date of the transaction. |

| Post-Relationship Retention | After an account closes, keep records for 5 more years (whichever is later). |

| Legal Protection (Sec 12(1)(b)) | Banks, directors, and employees who furnish required information cannot be sued for civil or criminal proceedings — protected under Section 13. |

The Web of Record-Retention Laws

Banks aren't governed by PMLA alone. Five different laws collectively determine how long they must keep what:

| Law | What It Mandates |

|---|---|

| PML Amendment Act, 2012 | Domestic & international transaction records → minimum 5 years for criminal-prosecution evidence |

| Bankers' Books Evidence Act, 1891 | Certified copies of bankers' books are accepted as prima facie evidence in court — no need to produce the original ledger |

| Banking Regulation Act, 1949 (Sec 45Y) | Authorises the Central Government (in consultation with RBI) to prescribe minimum record retention periods |

| Banking Companies (Period of Preservation of Records) Rules, 1985 | Cheque book registers, vault registers, and similar records → 5 years preceding the current calendar year |

| Information Technology Act, 2000 | Governs retention and authenticity of electronic records — covers digital ledgers, server logs, and online banking trails |

The Practical Retention Schedule

In practice, most major bank records must be retained for 10 years — the longest period mandated under any of the above laws. Here's the actual retention table banks follow:

| Document Type | Retention Period |

|---|---|

| Customer & third-party transaction records | 10 years from transaction date / payment / account closure |

| Savings/Current/Cash Credit/Overdraft accounts | 10 years; inoperative accounts retained permanently until reactivated |

| KYC, FATCA, CRS, Account Opening Forms | 10 years from cessation of business |

| Loan account files & related papers | 10 years from final settlement / loan closure |

| Litigation, fraud, court case records | 10 years from settlement / closure |

| Staff disciplinary action files | 10 years |

TIP

Exam shortcut: When in doubt, the answer is 10 years. Inoperative accounts are the exception — they are kept permanently until the customer reactivates them.

Penalties — Who Gets Punished, How Much?

PMLA carries severe penalties, but it also penalises misuse of investigation powers. Here is the full picture:

Penalties for the Offender

| Offence | Punishment |

|---|---|

| Money laundering (Sec 4) | Rigorous imprisonment 3 to 7 years + fine (no upper cap on fine — depends on gravity) |

| ML linked to NDPS Act (drugs) | Rigorous imprisonment up to 10 years + fine |

| Cognizability | Police can arrest without a warrant (Sec 45) |

| Bail | Non-bailable — bail is not a right, must be applied for and justified |

Penalties for Officials Misusing Powers

PMLA balances enforcement with safeguards. Investigators who abuse their powers also face punishment:

| Offence | Punishment |

|---|---|

| Giving false information that causes a wrongful arrest/search | Up to 2 years imprisonment + fine up to ₹50,000 |

| Vexatious search (no valid reasons recorded) | Up to 2 years imprisonment + fine up to ₹50,000 |

| Malicious false information causing harm | Same penalty as above |

| Unjustified arrest/search by an officer | Same penalty as above |

This dual structure — harsh on launderers, equally harsh on rogue investigators — is what gives PMLA its constitutional teeth.

The Big Picture — Why This Matters

When you finish reading this lesson, you should be able to answer one core question: why do banks spend so much on AML compliance?

The answer is a chain:

- Criminals generate dirty money → they need to launder it.

- Without banks, laundering would collapse — that's why launderers target the banking system.

- PMLA holds banks legally accountable (with 3-7 years for individuals and unlimited fines for institutions) if they fail to prevent it.

- FATF holds India accountable — non-compliance leads to grey-listing and capital flight.

- The cost of compliance is high, but the cost of non-compliance is systemic.

This is why your bank asks for KYC documents, monitors transactions above ₹10 lakh, files STRs, and retains records for 10 years. It is not bureaucracy for its own sake — it is the price of being trusted with public money.

Exam Tips

TIP

High-frequency facts:

- PMLA = Prevention of Money Laundering Act, 2002

- Sec. 3 = defines the offence | Sec. 4 = punishment (3-7 years RI, up to 10 yrs NDPS) | Sec. 45 = cognizable & non-bailable

- 3 ML stages: Placement → Layering → Integration (PLI)

- 4 TF stages: Raise → Move → Store → Use

- FATF: Founded 1989 by G7 | HQ Paris | 40 Recommendations (FATF Standards 2012)

- FIU-IND: Central national agency under Department of Revenue, MoF

- ED: Investigates via ECIR (Enforcement Case Information Report)

- PMLA Schedule: Part A (IPC/NDPS/Arms/Corruption), Part B (false declarations), Part C (trans-border)

- Bank record retention: 10 years — inoperative accounts retained permanently

- Bankers' Books Evidence Act: 1891 — certified copies = prima facie evidence

- STRs/CTRs filed by banks → FIU-IND → ED/intelligence agencies

- Vexatious search punishment: 2 years + ₹50,000 fine

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| PMLA | Prevention of Money Laundering Act, 2002 — India's principal law against money laundering |

| Money Laundering | Processing criminal proceeds to disguise their illegal origin |

| "Proceeds of crime" | Property derived directly/indirectly from a scheduled offence under PMLA |

| Sec. 3 of PMLA | Defines the offence — knowingly assisting in concealment, possession, acquisition or projecting proceeds as untainted |

| Sec. 4 of PMLA | Punishment: rigorous imprisonment 3-7 years + fine; up to 10 years if linked to NDPS Act |

| Sec. 45 of PMLA | All PMLA offences are cognizable and non-bailable |

| PMLA Schedule — Part A | Predicate offences under IPC, NDPS, Explosive Substances, UAPA, Arms Act, Wild Life, Immoral Traffic, Prevention of Corruption, Antiquities Act |

| PMLA Schedule — Part B | False declaration and false documents offences |

| PMLA Schedule — Part C | Trans-border crimes to tackle ML across global boundaries |

| 3 Stages of ML | Placement → Layering → Integration (PLI) |

| Placement | Dirty cash enters banking system; riskiest stage for launderer |

| Layering | Multiple transactions across accounts/borders to obscure the trail |

| Integration | Cleaned funds re-enter as legitimate investments/assets |

| 4 Stages of Terrorism Financing | Raise → Move → Store → Use |

| ML vs TF — Key difference | ML hides the origin of illicit funds; TF often hides the destination of legal funds |

| OCGs / PMLs | Organised Crime Groups and Professional Money Launderers — often work together |

| Department of Revenue, MoF | Administers the PMLA, 2002 |

| Directorate of Enforcement (ED) | Investigates ML offences via ECIR (Enforcement Case Information Report) |

| FIU-IND | Financial Intelligence Unit – India; central national agency for suspect financial transactions; receives, processes, analyses, and disseminates information |

| STRs / CTRs | Suspicious Transaction Reports and Cash Transaction Reports — filed by banks to FIU-IND |

| FATF | Financial Action Task Force — international standard-setter for AML/CFT |

| FATF — Founded | July 1989 by G7 |

| FATF — Headquarters | Paris, France |

| FATF Standards | 40 Recommendations — known as FATF Standards 2012 |

| FATF non-compliance risk | Grey-listing or black-listing of countries — leads to capital flight |

| Objectives of PML measures | Prevent criminals from misusing the financial system; prevent spread of criminal activity; safeguard the economy; deny terrorists access to financial resources |

| Bank Obligation: Transaction Records | Maintain so that individual transactions can be reconstructed |

| Bank Obligation: Confidentiality | Information must remain confidential unless required by law |

| Bank Obligation: Record Retention | Minimum 5 years under PMLA; in practice 10 years under combined laws |

| Post-Relationship Retention | 5 years after account closure (whichever is later) |

| Sec 12(1)(b) Protection | Banks, directors, and employees protected from civil/criminal proceedings for furnishing required information |

| PML Amendment Act 2012 | Mandates minimum 5 years retention of domestic & international transaction records |

| Bankers' Books Evidence Act, 1891 | Certified copies of bankers' books = prima facie evidence in court |

| Banking Regulation Act, 1949 (Sec 45Y) | Empowers Central Government (with RBI) to prescribe record retention periods |

| Banking Companies (Preservation of Records) Rules, 1985 | Cheque book/vault registers preserved for 5 years preceding current calendar year |

| IT Act, 2000 | Governs retention of electronic records by banks |

| Customer/third-party transaction records | 10 years from transaction/payment/account closure |

| Inoperative accounts | Records retained permanently until reactivated |

| KYC/FATCA/CRS records | 10 years from cessation of business |

| Loan account documents | 10 years from final settlement/closure |

| Litigation/fraud records | 10 years from settlement/closure |

| False information / vexatious search punishment | Up to 2 years imprisonment + fine up to ₹50,000 |

| Why AML matters | Banks are the gateway — without them, laundering collapses. PMLA + FATF make non-compliance institutionally and internationally costly. |

| Wolfsberg Group | Consortium of 13 global banks (private sector) — developer of the Wolfsberg AML Principles. NOT the World Bank, IMF, or FATF. |

| Wolfsberg — Primary Goal | To promote international trade and commerce by providing a unified AML framework for financial institutions. |

| Wolfsberg — Core Themes | CDD, risk assessment, SAR, compliance mgmt, record keeping, international cooperation, training, technology, continuous improvement, source-of-funds verification, PEP scrutiny. |

| TBML | Trade Based Money Laundering — disguising illicit funds through trade (over/under-invoicing, multiple invoicing, false descriptions). |

| TBML Prevention | Combined application of CDD + CIP + CRP (Customer Relationship Procedure) — not any one in isolation. |

| FATF Recommendation 12 | Defines and mandates enhanced due diligence on PEPs — domestic and foreign. |

| Objectives of PML measures | Prevent criminal acts, facilitate investigation, prevent funds access to criminals, avoid concealing the origin of funds from criminal activities. |

| ED's Supervisory Role | Investigates PMLA offences via ECIR. The agency with supervisory powers over business entities subject to PMLA in India is the Financial Intelligence Unit – India (FIU-IND), which receives reports from banks and refers them to ED for prosecution. |

Lesson Doubts

Ask questions, get expert answers