📜 Demand Drafts & Bill of Exchange

Understanding Demand Drafts, their issuance, duplicate issuance rules, cancellation, and Bill of Exchange concepts.

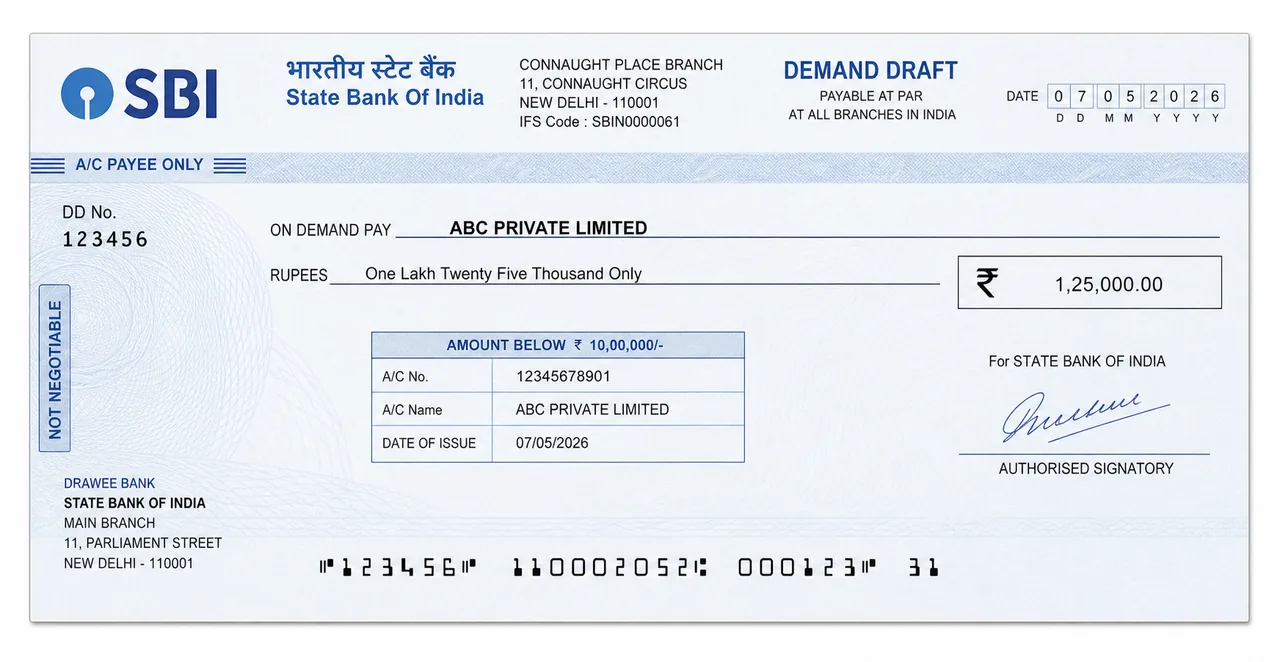

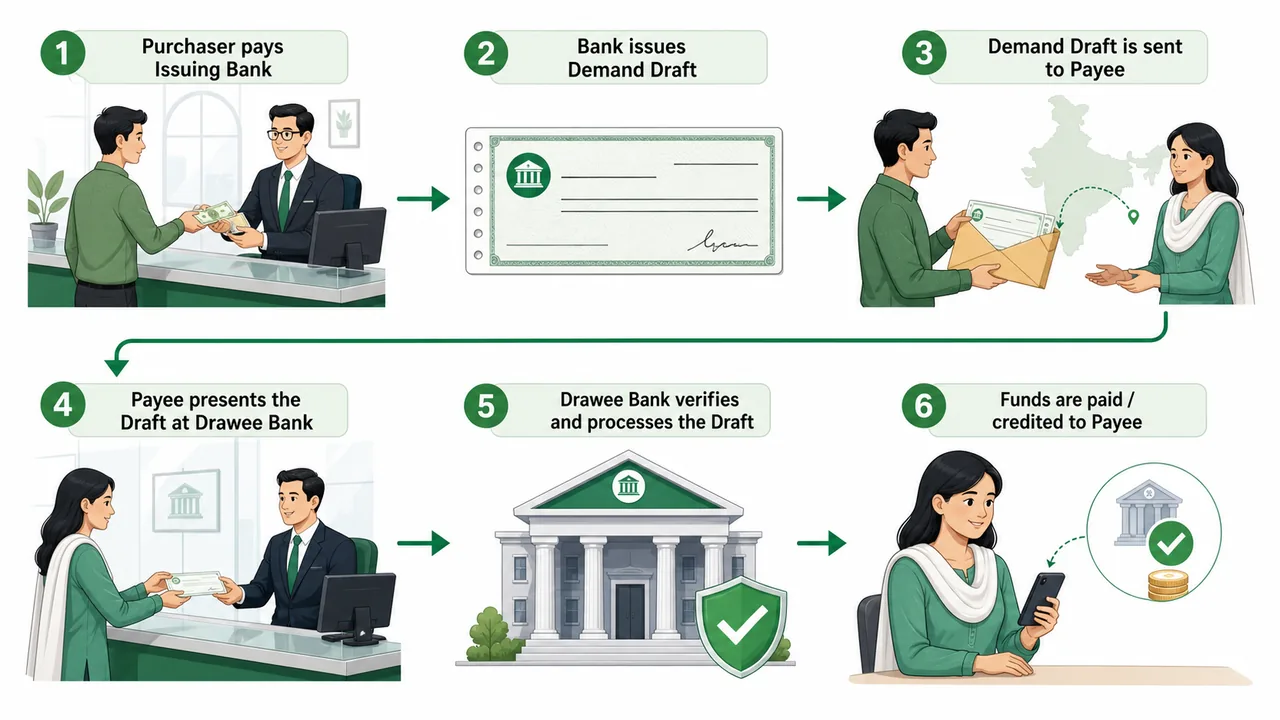

Demand Drafts (DD)

A Demand Draft (DD) is a prepaid negotiable instrument used for effecting transfer of money.

- Definition: A DD is essentially a Bill of Exchange (BOE) drawn by one bank branch on another bank branch, payable on demand. It typically involves three parties: the drawer bank, the drawee bank, and the payee.

- Legal Basis: It is governed by Section 85 of the Negotiable Instruments (NI) Act, 1881.

- Value Paid Instrument: Since the purchaser pays for the draft in advance, it is considered a value paid instrument. Unlike a cheque, its payment cannot be stopped or countermanded by the purchaser once issued, unless there is a court order or loss of instrument.

- Restriction on Bearer Issue: A DD cannot be issued payable to bearer. It must always be payable to order to prevent money laundering and ensure traceability. This restriction comes from Section 31 of the RBI Act.

- Validity: A specific DD is valid for 3 months from the date of issue. This validity period was standardized by RBI directives under Section 35A of the Banking Regulation (BR) Act (effective from 1.4.2012).

- Bank-Purchaser Relationship: When a customer purchases a DD founds are collected, the relationship is that of Debtor and Creditor (Bank is Debtor, Purchaser is Creditor). This was established in the case Sidhnaath Vs PNB AIR 1960.

Issuance Rules

Banks must follow strict Know Your Customer (KYC) norms to prevent formatting of illegal funds:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Demand Drafts (DD)

A Demand Draft (DD) is a prepaid negotiable instrument used for effecting transfer of money.

- Definition: A DD is essentially a Bill of Exchange (BOE) drawn by one bank branch on another bank branch, payable on demand. It typically involves three parties: the drawer bank, the drawee bank, and the payee.

- Legal Basis: It is governed by Section 85 of the Negotiable Instruments (NI) Act, 1881.

- Value Paid Instrument: Since the purchaser pays for the draft in advance, it is considered a value paid instrument. Unlike a cheque, its payment cannot be stopped or countermanded by the purchaser once issued, unless there is a court order or loss of instrument.

- Restriction on Bearer Issue: A DD cannot be issued payable to bearer. It must always be payable to order to prevent money laundering and ensure traceability. This restriction comes from Section 31 of the RBI Act.

- Validity: A specific DD is valid for 3 months from the date of issue. This validity period was standardized by RBI directives under Section 35A of the Banking Regulation (BR) Act (effective from 1.4.2012).

- Bank-Purchaser Relationship: When a customer purchases a DD founds are collected, the relationship is that of Debtor and Creditor (Bank is Debtor, Purchaser is Creditor). This was established in the case Sidhnaath Vs PNB AIR 1960.

Issuance Rules

Banks must follow strict Know Your Customer (KYC) norms to prevent formatting of illegal funds:

- Cash Limits: A DD can be issued against cash only for amounts less than ₹50,000. If the amount is ₹50,000 or more, it must be debited from the customer's account or against a cheque.

- Account Payee Crossing: Any DD of ₹20,000 or above must be issued with an "Account Payee" crossing (RBI directive, Nov 05, 2011). This ensures the money goes directly into a bank account and cannot be encashed over the counter. Consequently, cash payment of a DD is only possible if the amount is less than ₹20,000.

Loss of DD and Issue of Duplicate

If a DD is lost, the bank can issue a duplicate to protect the purchaser's interest, subject to certain conditions:

- Lost by Purchaser: If the original DD is lost by the purchaser before it was handed over or dispatched to the payee, a duplicate can be issued to the purchaser. The bank will typically require an indemnity bond.

- Lost by Payee: If the DD is lost after it is in the possession of the payee, or lost in transit while being sent by the purchaser to the payee, the duplicate can be obtained only by the payee. The purchaser cannot claim it in this scenario.

Rules for Duplicates

- Small Amounts: For a lost DD up to ₹5,000, banks must issue a duplicate without waiting for a 'non-payment advice' from the drawee branch, to avoid inconvenience to small customers.

- Timeline & Interest: A duplicate must be issued within 14 days of the customer completing strict formalities (like indemnity). If the bank delays beyond this period, it must pay interest at the Fixed Deposit (FD) rate for the delay period.

- Original becomes Invalid: Once a duplicate is issued, the original instrument becomes non-operative. The bank acts on the premise that the original is cancelled.

Presentation Scenarios (After Duplicate Issue)

What happens if the original or duplicate is presented for payment?

- Original Presented: It must be returned unpaid (since it is cancelled).

- Duplicate Presented: It must be paid.

- Both Presented: The duplicate is the valid instrument and strictly paid.

- Exceptions: If the duplicate is presented after the original has already been paid (perhaps due to system error), the duplicate must be returned.

Special Scenarios

Unsigned DD

If a bank inadvertently issues a DD without a signature and it is presented for payment:

- It should be paid and not returned. The lack of signature is the bank's internal error, and dishonouring it would damage the bank's reputation and liability.

Cancellation by Purchaser

- If a payee returns a DD to the purchaser without using it, the purchaser can get it cancelled and funds refunded.

- Condition: The bank requires specific authority from the payee (such as a letter or an endorsement on the back of the DD) relinquishing their claim, before refunding the purchaser. This protects the bank from claims by the payee.

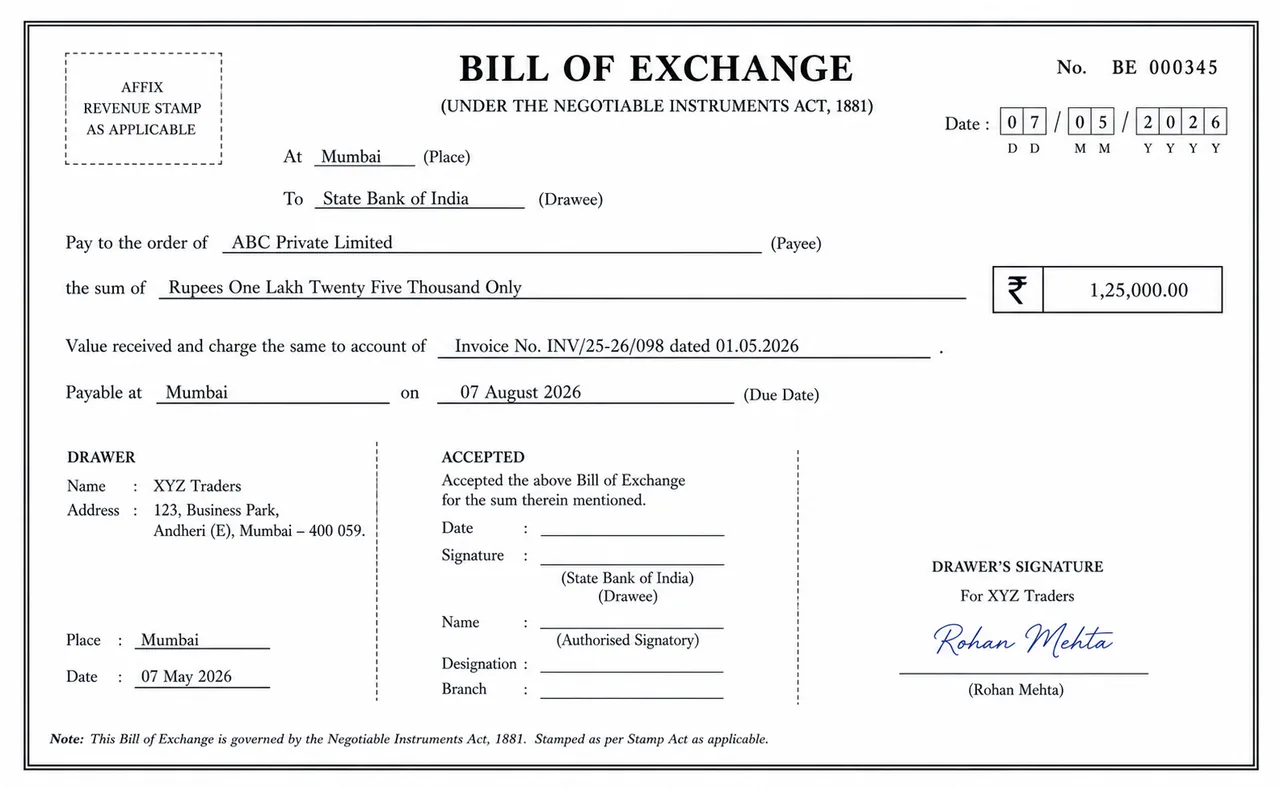

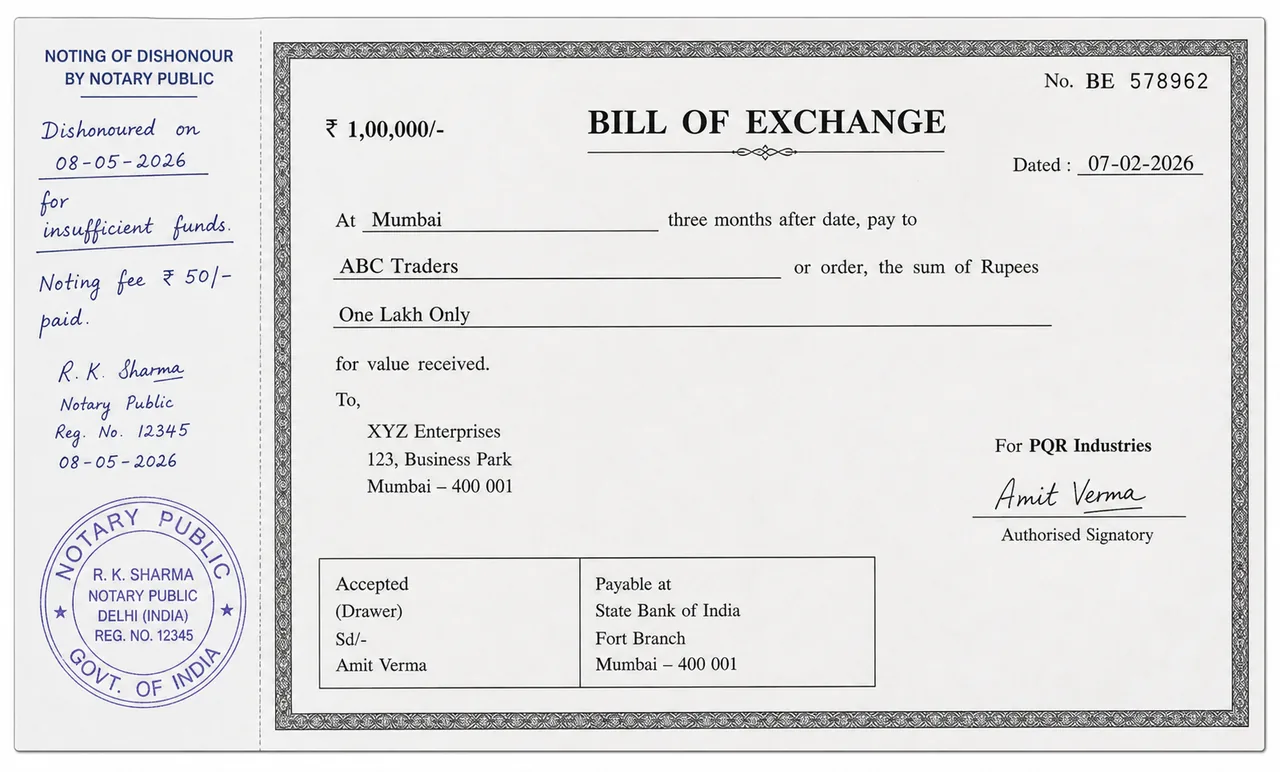

Bill of Exchange (BOE)

Definition (Section 5, NI Act)

A Bill of Exchange is a written instrument containing an unconditional order, signed by the maker (drawer), directing a certain person (drawee) to pay a certain sum of money only to, or to the order of, a certain person (payee) or to the bearer.

- Usage: It is the primary instrument used for sale and purchase transactions in trade and commerce (financing working capital).

- Examples: Both a Demand Draft (DD) and a Cheque are conceptually types of Bills of Exchange payable on demand.

Parties Involved

- Drawer: The person who makes the bill (ordering payment).

- Drawee: The person directed to pay (who must accept the bill).

- Payee: The beneficiary to whom payment is made.

Statutory Restrictions

- No Bearer BOE: A BOE cannot be drawn payable to bearer on demand. This is a monopoly of the central bank (RBI) to issue bearer notes (currency). This restriction is under Section 31 of the RBI Act. It can only be payable to order.

Types of Bill of Exchange

1. Genuine vs. Accommodation Bill

- Genuine Bill: Drawn against an actual sale or purchase transaction of goods. Ideally, it is supported by the movement of goods. There is valid consideration (value).

- Accommodation Bill (Kite Flying): Drawn without any actual trade transaction, simply to accommodate financial help between parties. There is no consideration. Banks are strictly prohibited from purchasing or discounting these "Kite Flying" bills.

2. Documentary vs. Clean Bill

- Documentary Bill: Accompanied by documents of title to goods (like Lorry Receipt, Railway Receipt, Invoice). The bank handles the goods' release.

- Clean Bill: No documents attached; reliant solely on the creditworthiness of the parties.

3. Demand vs. Usance Bill

The key distinction between these two types of bills lies in when payment is due:

Demand Bill (Sight Bill)

A Demand Bill is payable immediately on demand or at sight — meaning as soon as it is presented to the drawee, payment must be made.

- Default Rule: If no specific time for payment is mentioned in the bill, it is automatically treated as a demand bill.

- Stamp Duty: Currently exempted. This exemption is why everyday instruments like cheques and Demand Drafts (DDs) carry no stamp duty — they are essentially demand bills.

- No Acceptance Required: Since payment is immediate, there is no waiting period and hence no formal "acceptance" step by the drawee.

Usance Bill (Time Bill)

A Usance Bill is payable at a future date specified in the instrument (e.g., "30 days after sight", "2 months after date").

- Stamp Duty: Payable ad valorem — meaning the duty amount depends on both the value of the bill and the time period until maturity.

- Exemptions: Stamp duty is waived in two scenarios:

- Export bills (to promote international trade)

- Bills up to 90 days where a bank is a party

- Acceptance is Mandatory: Unlike a demand bill, a usance bill requires formal acceptance by the drawee. By signing (accepting) the bill, the drawee acknowledges their obligation and becomes legally bound to pay on the due date.

Liability in Usance Bills

Understanding who is responsible for payment is critical. In a usance bill, liability shifts based on whether the bill has been accepted or not:

- Before Acceptance: The Drawer (the person who created the bill) is primarily liable. If the bill is dishonoured, the holder looks to the drawer for payment.

- After Acceptance: Once the drawee signs and accepts, they become the Acceptor and assume primary liability. The drawer's liability now becomes secondary — they act as a surety (guarantor) in case the acceptor fails to pay.

| Stage | Primary Liability | Secondary Liability |

|---|---|---|

| Before Acceptance | Drawer | — |

| After Acceptance | Drawee (Acceptor) | Drawer (becomes surety) |

Time for Acceptance (Section 25, NI Act)

The drawee is legally allowed 48 hours (excluding public holidays) to decide whether to accept or refuse the bill.

- If the drawee refuses to accept (or fails to respond within 48 hours), the bill is treated as dishonoured by non-acceptance.

- The holder can then immediately take legal action against the drawer (who remains liable since acceptance never occurred).

Note: The authority to declare public holidays under Section 25 lies with the Central Government, usually delegated to State Governments.

Practical Example

Suppose you are a trader who sold goods worth ₹1,00,000 on credit to a buyer:

- You (Drawer) create a usance bill: "Pay ₹1,00,000 to my order, 30 days after sight."

- You present this bill to the Buyer (Drawee).

- The buyer has 48 hours to accept or refuse.

- If buyer accepts (signs): They become the "Acceptor" and are now primarily liable. You become a secondary surety.

- If buyer refuses/ignores: The bill is dishonoured. You (Drawer) remain liable, and legal action can proceed.

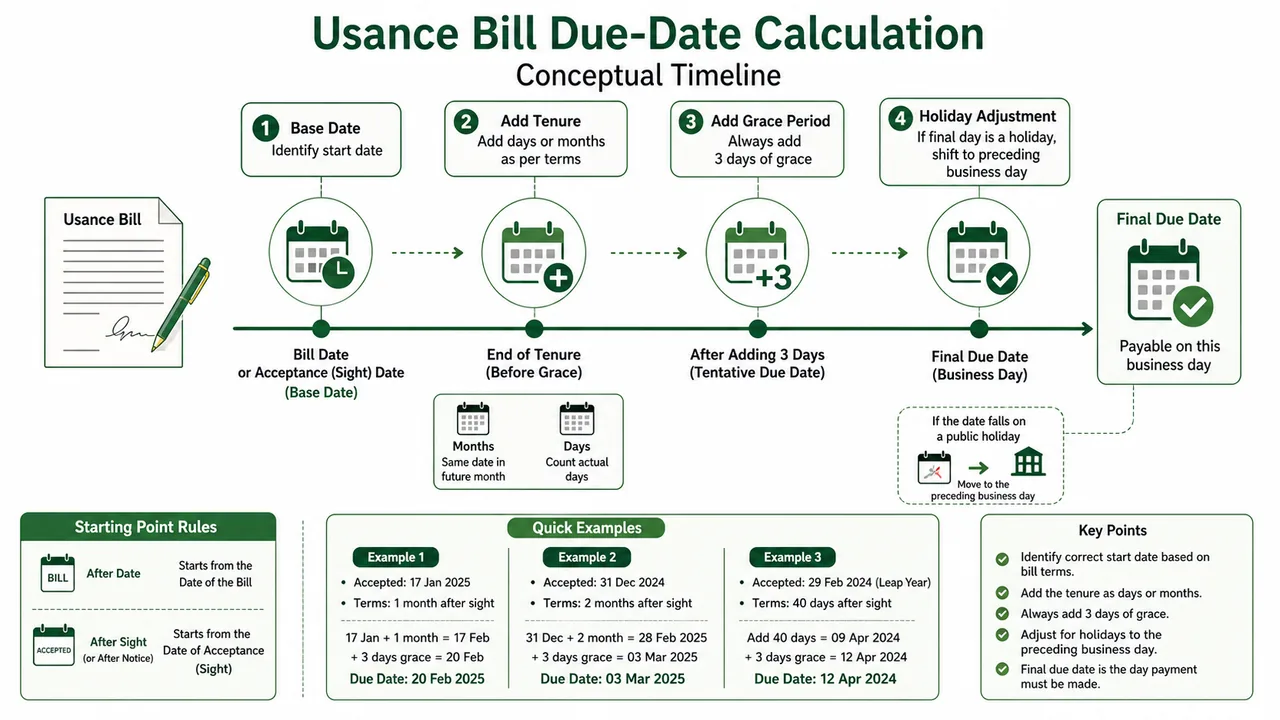

Due Date Calculation

Knowing when a bill is legally due is critical for claiming interest or noting dishonour.

| Payment Term | Starts From... | What It Means |

|---|---|---|

| "After Date" | Date of the Bill | Drawer controls this; due date fixed at creation. |

| "After Sight" | Date of Acceptance | Drawee can delay maturity by delaying acceptance (within 48 hrs). |

| "After Notice" | Date of Acceptance | Same as "after sight" — starts when drawee accepts. |

| Unspecified | Date of the Bill | Law defaults to "after date" behaviour. |

Calculation Steps

- Base Date: Identify start date (Date of Bill or Date of Acceptance/Sight).

- Add Tenure: Add the specified months or days.

- Months: Corresponds to the same date in the future month (e.g., Jan 15 + 1 month = Feb 15).

- Days: Count actual days.

- Grace Period: Always add 3 days of grace to the calculated date.

- Holiday Rule: If the final due date is a public holiday, the due date shifts to the preceding business day.

Examples

-

Scenario 1 (After Sight):

- Bill Dated: Jan 12, 2016

- Terms: 1 month after acceptance

- Accepted: Jan 17

- Calc: Jan 17 + 1 month = Feb 17.

- Grace: Feb 17 + 3 days = Feb 20 (Due Date).

-

Scenario 2 (Month End Logic):

- Bill Dated: Dec 28, 2015

- Terms: 2 months after presentation

- Accepted: Dec 31

- Calc: Dec 31 + 2 months = Feb 28 or 29 (end of Feb). In 2016 (leap year), it is Feb 29. If not leap year, payments due on "Feb 30" or "31" fall on the last day of Feb.

- Grace: Feb 29 + 3 days = Mar 03 (Due Date).

-

Scenario 3 (Days Calculation):

- Accepted: Feb 29, 2016 (Leap year)

- Terms: 40 days after presentation

- Calc: Remaining Feb (0) + Mar (31) + Apr (9) = 40 days. Corresponding date is Apr 9.

- Grace: Apr 9 + 3 days = Apr 12 (Due Date).

Dishonour & Legal Proof

A bill is dishonoured when the drawee either:

- Refuses to accept the bill (dishonour by non-acceptance), or

- Refuses to pay on the due date (dishonour by non-payment)

When a bill is dishonoured, the holder needs formal proof to take legal action against the drawer or endorsers. This is especially critical for foreign bills where courts require authenticated evidence.

Noting (Section 99, NI Act)

Noting is the first step in documenting dishonour:

- The holder takes the dishonoured bill to a Notary Public (a legally authorized officer).

- The Notary records the fact of dishonour directly on the instrument itself.

- The note includes: date of dishonour, reason given (if any), and Notary's fees.

- Purpose: Creates an initial record that dishonour occurred.

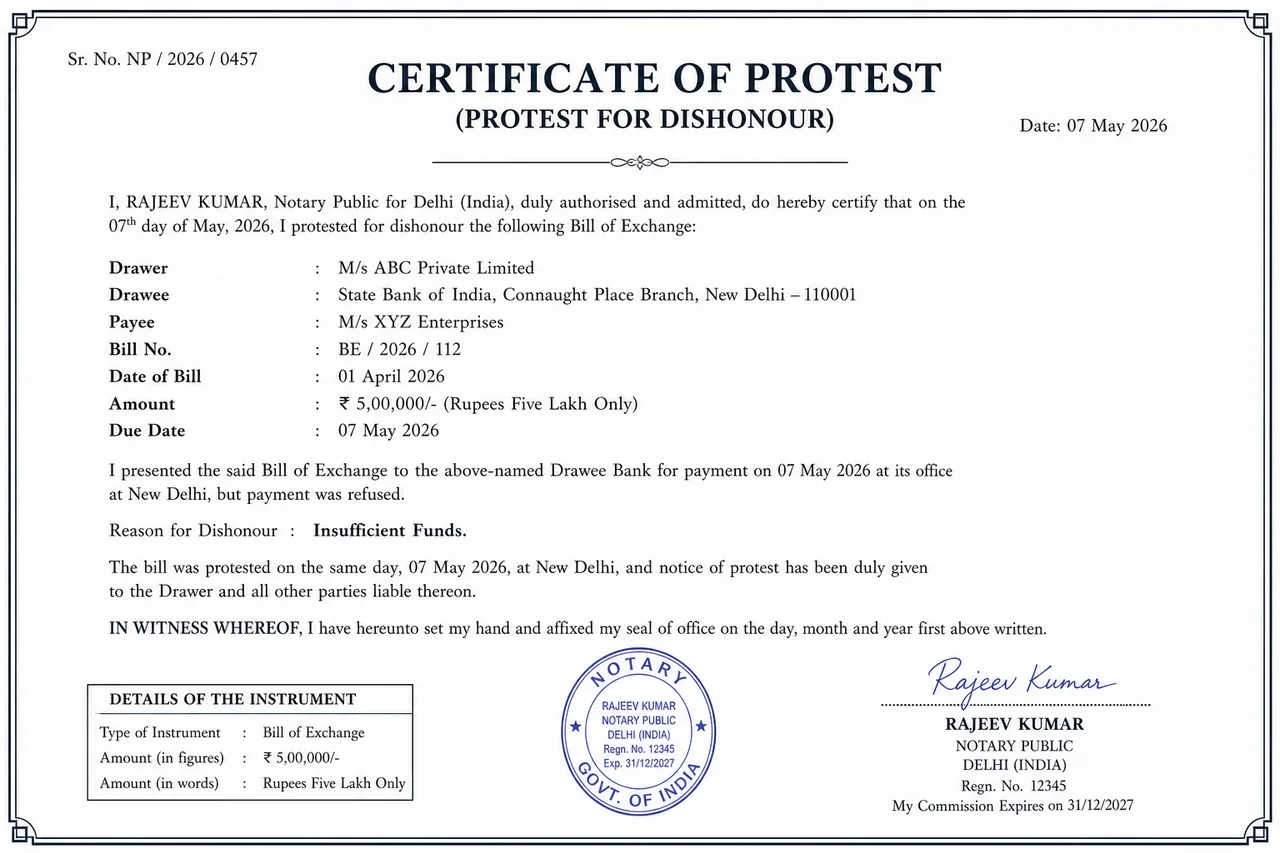

Protesting (Section 100, NI Act)

Protesting is a more formal step that follows noting:

- The Notary Public issues a formal certificate (called a "Protest") attesting to the dishonour.

- This certificate is based on the noting and serves as legally admissible evidence in court.

- Purpose: Provides stronger legal proof than noting alone.

Noting vs. Protesting: Key Differences

| Aspect | Noting | Protesting |

|---|---|---|

| What is it? | Recording dishonour on the bill itself | Formal certificate issued separately |

| Done by | Notary Public | Notary Public |

| Legal strength | Preliminary record | Stronger, admissible as evidence |

| Required for | Optional for inland bills | Mandatory for foreign bills |

When is Protesting Mandatory?

- Foreign Bills: Protesting is compulsory for foreign bills (Section 104). Without it, the holder loses the right to sue prior parties (drawer, endorsers).

- Inland Bills: Protesting is optional. The holder can sue without protest, but noting is still advisable as evidence.

Interest Rules

When a negotiable instrument is dishonoured, the holder is entitled to claim interest in addition to the principal amount. The NI Act specifies how interest is calculated:

Stated Rate (Section 79)

If the instrument explicitly mentions a Rate of Interest (ROI):

- Interest is payable at that specified rate.

- Interest starts from the date of execution of the instrument (i.e., the date the bill was drawn).

Example: A bill for ₹1,00,000 mentions "interest at 12% p.a." → If dishonoured, the holder can claim interest at 12% from the date the bill was created.

Unstated Rate (Section 80)

If the instrument does not mention any interest rate:

- The statutory default rate of 18% per annum applies.

- This acts as a penalty rate to compensate the holder for delayed payment.

Example: A bill for ₹1,00,000 with no interest clause is dishonoured → The holder can claim interest at 18% p.a.

| Scenario | Interest Rate | Starts From |

|---|---|---|

| ROI mentioned in instrument | As stated | Date of instrument |

| ROI not mentioned | 18% p.a. (statutory) | Date of instrument |

What is a Holder for Value?

When a bank purchases or discounts a bill or cheque, it pays the holder upfront and takes ownership of the instrument. At this point:

- The bank becomes a Holder for Value — meaning it has given valuable consideration (money) in exchange for the instrument.

- This is different from a regular "holder" who may have received the instrument as a gift or without paying for it.

Why Does This Matter?

Being a Holder for Value gives the bank stronger legal rights:

| Right | Explanation |

|---|---|

| Sue in own name | The bank can directly sue the drawer or endorsers for the full amount — it doesn't need to involve the original payee. |

| Full recovery rights | The bank can recover the entire face value of the instrument, not just what it paid for it. |

| Priority over later parties | If multiple claims exist, a Holder for Value has priority. |

Practical Example

- A trader holds a bill for ₹1,00,000 payable in 60 days.

- The trader needs cash now, so they approach a bank to discount the bill.

- The bank pays the trader ₹98,000 (deducting discount/interest) and takes the bill.

- The bank is now the Holder for Value.

- If the drawee dishonours the bill on the due date, the bank can sue the drawer directly for the full ₹1,00,000.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| DD Definition | A Bill of Exchange drawn by one bank on another, payable on demand. Governed by Section 85 of NI Act. |

| DD Bearer Restriction | DD cannot be issued as Bearer — must be payable to order only (under Section 31 RBI Act). |

| DD as Value Paid Instrument | Payment cannot be stopped by purchaser once issued (unlike cheques). Court order or loss required for stop. |

| DD Validity | Valid for 3 months from date of issue (Section 35A, BR Act). |

| DD Cash Issuance Limit | DD can be issued against cash only up to ₹49,999 (less than ₹50,000). |

| DD Account Payee Crossing | DDs of ₹20,000 or above must have "Account Payee" crossing. Cash payment restricted to less than ₹20,000. |

| Duplicate DD – Who Can Obtain | Lost before dispatch → Purchaser can get duplicate. Lost in transit to payee → Only Payee can obtain duplicate. |

| Duplicate DD – Small Amounts | For amounts up to ₹5,000, duplicate issued without waiting for non-payment advice. |

| Duplicate DD – Timeline | Must be issued within 14 days. Delay → Bank pays interest at FD rate. |

| Unsigned DD | If presented, it should be paid (not returned) — bank's internal error. |

| Bill of Exchange (BOE) | Unconditional written order to pay. Defined in Section 5, NI Act. Primary instrument for trade finance. |

| BOE Parties | Drawer (maker), Drawee (payer), Payee (beneficiary). |

| Genuine vs Accommodation Bill | Genuine = actual trade transaction with consideration. Accommodation Bill (Kite Flying) = no consideration, banks prohibited from discounting. |

| Documentary vs Clean Bill | Documentary = with documents of title. Clean = no documents, based on creditworthiness. |

| Demand Bill | Payable immediately on demand/sight. No stamp duty (exempted). No acceptance required. |

| Usance Bill | Payable at future date. Stamp duty ad valorem. Exemptions: export bills, bills up to 90 days with bank as party. |

| Usance Bill – Acceptance | Formal acceptance by drawee is mandatory to become legally liable. |

| Usance Bill – Liability | Before acceptance → Drawer liable. After acceptance → Drawee (Acceptor) is primarily liable, Drawer becomes surety. |

| Time for Acceptance | Drawee gets 48 hours (excl. holidays) to accept — Section 25, NI Act. |

| Due Date – "After Date" | Countdown starts from date of bill. Drawer controls. |

| Due Date – "After Sight" | Countdown starts from date of acceptance. Drawee can delay maturity. |

| Grace Period | Always add 3 days of grace to calculated due date. |

| Holiday Rule | If due date falls on public holiday, payment due on preceding business day. |

| Dishonour | Refusal to accept (non-acceptance) or refusal to pay (non-payment). |

| Noting (Section 99) | Notary Public records dishonour on the instrument. First step for legal proof. |

| Protesting (Section 100) | Formal certificate from Notary Public. Legally admissible evidence. Mandatory for foreign bills (Section 104). |

| Interest – Stated Rate | If ROI mentioned in instrument → pay at that rate from date of instrument (Section 79). |

| Interest – Unstated Rate | If ROI not mentioned → statutory rate of 18% p.a. applies (Section 80). |

| Holder for Value | Bank that purchases/discounts a bill. Can sue drawer directly for full amount in own name. |

Lesson Doubts

Ask questions, get expert answers