📜 Collection and Alterations of Cheques

Understanding the collection process, conversion, and rules regarding material and non-material alterations in cheques under the NI Act.

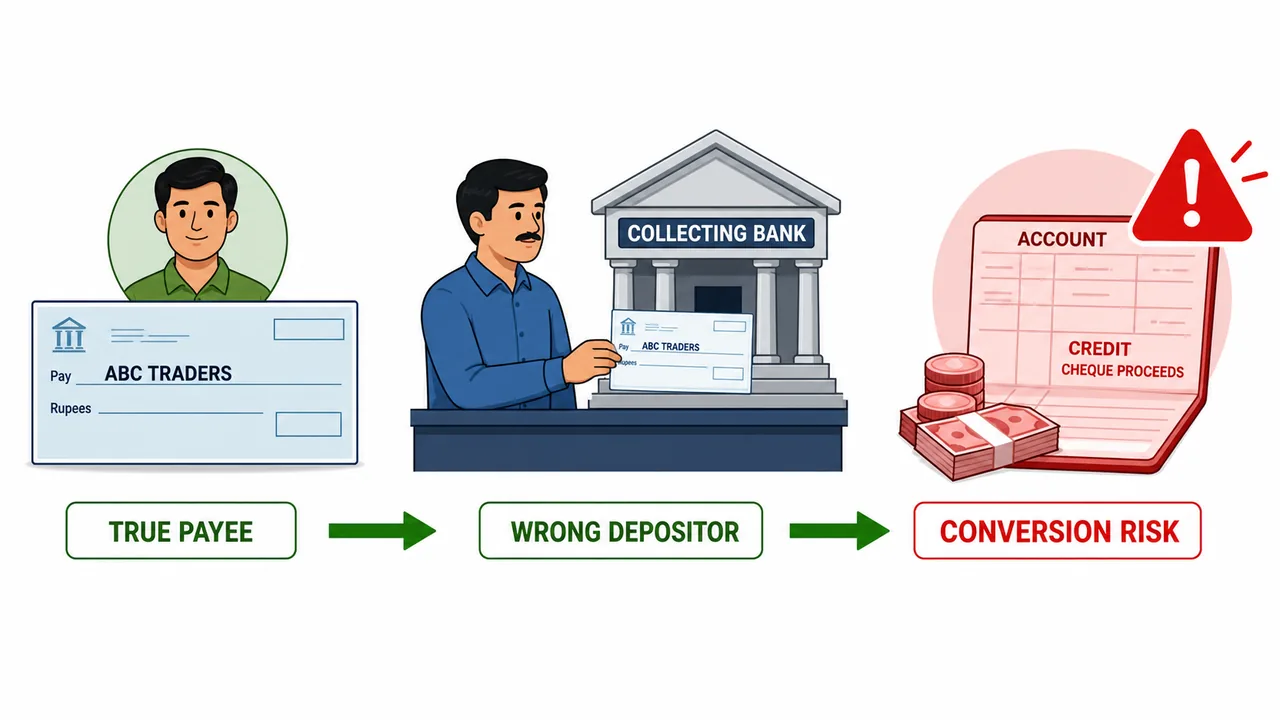

Collection of Cheque

When a bank collects a cheque for a customer, the relationship established is that of Agent and Principal, where the bank acts as the agent and the customer is the principal.

Conversion

If a bank collects a cheque for a customer that does not belong to that customer, it is legally termed as conversion.

Example: Imagine a cheque is issued to Mr. Vijay Kumar (the true owner). Another person, also named Mr. Vijay Kumar (an unlawful holder), gets hold of this cheque and deposits it into his own account. If the bank collects this cheque for the unlawful holder, it constitutes conversion because the bank has dealt with the property (cheque) inconsistent with the rights of the true owner.

As per the Criminal Procedure Code, conversion is an unauthorised act that deprives the true owner of their personal property without their consent. It is potentially a punishable offence.

Interactive Preview

Try the embedded exercise below. Full lesson access still requires Pro.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Collection of Cheque

When a bank collects a cheque for a customer, the relationship established is that of Agent and Principal, where the bank acts as the agent and the customer is the principal.

Conversion

If a bank collects a cheque for a customer that does not belong to that customer, it is legally termed as conversion.

Example: Imagine a cheque is issued to Mr. Vijay Kumar (the true owner). Another person, also named Mr. Vijay Kumar (an unlawful holder), gets hold of this cheque and deposits it into his own account. If the bank collects this cheque for the unlawful holder, it constitutes conversion because the bank has dealt with the property (cheque) inconsistent with the rights of the true owner.

As per the Criminal Procedure Code, conversion is an unauthorised act that deprives the true owner of their personal property without their consent. It is potentially a punishable offence.

Protection against conversion of Cheque

Banks need protection against liability for conversion. Subject to specific conditions, statutory protection is available under:

- Section 131 of the NI Act for cheques.

- Section 131-A of the NI Act for demand drafts.

Condition for protection against conversion

To claim this protection, the bank must ensure:

- The collection is for a customer whose account complies with KYC requirements.

- The cheque is crossed (either generally or specially) in favour of the bank prior to collection. Means the crossing must exist on the cheque before the bank receives it from the customer. If the bank receives an open cheque and then crosses it themselves, protection under Section 131 is not available.

- The collection is performed in good faith (believing the cheque belongs to the customer) and without negligence.

Alterations in Cheque

Alterations to a cheque generally fall into two categories: non-material and material alterations.

Definition

According to Section 62 of the Indian Contract Act, a material alteration is one which significantly varies the rights, liabilities, or legal position of the parties from the original instrument.

In the specific context of cheques, a material alteration:

- Dilutes the basic instructions of the drawer.

- Changes the basic character of the cheque.

Non-material alterations in Cheque

Certain alterations are considered non-material and do not invalidate the cheque. These include:

- Completion of an inchoate (incomplete) cheque by the holder or payee.

- Crossing an uncrossed cheque or converting a general crossing to a special crossing.

- Converting a bearer cheque into an order cheque.

- Cuttings or alterations that are confirmed by the drawer with their full signature.

A cheque containing such non-material alterations can be paid by the bank.

Alteration by drawer

However, under current RBI guidelines for CTS (Cheque Truncation System), a cheque should not be altered even by the drawer. The only exception is the revalidation of the date.

Material Alterations in Cheque

Material alterations render the instrument void. Common examples include:

- Conversion of an order cheque into a bearer cheque.

- Cancellation of a crossing or converting a special crossing into a general crossing.

- Any change in the amount, name of the payee, or date.

- Mutilation of the cheque.

These are classified as material alterations under Section 87 of the NI Act. If a bank pays such a cheque, it is liable for the loss.

Protection for payment of materially altered cheque u/s 89

A bank may be protected under Section 89 if the alteration is not visible even when the cheque is examined with due care and diligence (e.g., a very skillful forgery).

Use of ultra-violet lamp

To mitigate fraud, RBI guidelines mandate that all cheques of Rs. 2 lacs and above must be examined under an ultra-violet (UV) lamp to detect invisible alterations.

Crossing of Cheque

Crossing is a specific instruction from the drawer to the paying or collecting bank. It directs the bank:

- Not to make cash payment across the counter.

- To make payment only to a bank (payee's bank).

Payment to payee's bank can be in cash OR in clearing OR as transfer.

Method of crossing

- Crossing is denoted by drawing two parallel transverse lines on the face of the Cheque or Demand Draft.

- Important Note on Placement: The lines can be drawn in any manner and anywhere on the face of the cheque (e.g., top-left corner, bottom-center, or across the middle). It does not strictly have to be in the top-left corner, as long as the lines are transverse and parallel.

Who can cross?

The following parties can cross a cheque:

- The Drawer himself.

- The Holder (payee or endorsee).

- The Collecting Bank, but they can only add a special crossing to an already crossed cheque or cross it specially to themselves.

Regardless of who effectively marks it, crossing is legally treated as the drawer's direction. Note that a Bill of Exchange or Promissory Note cannot be crossed.

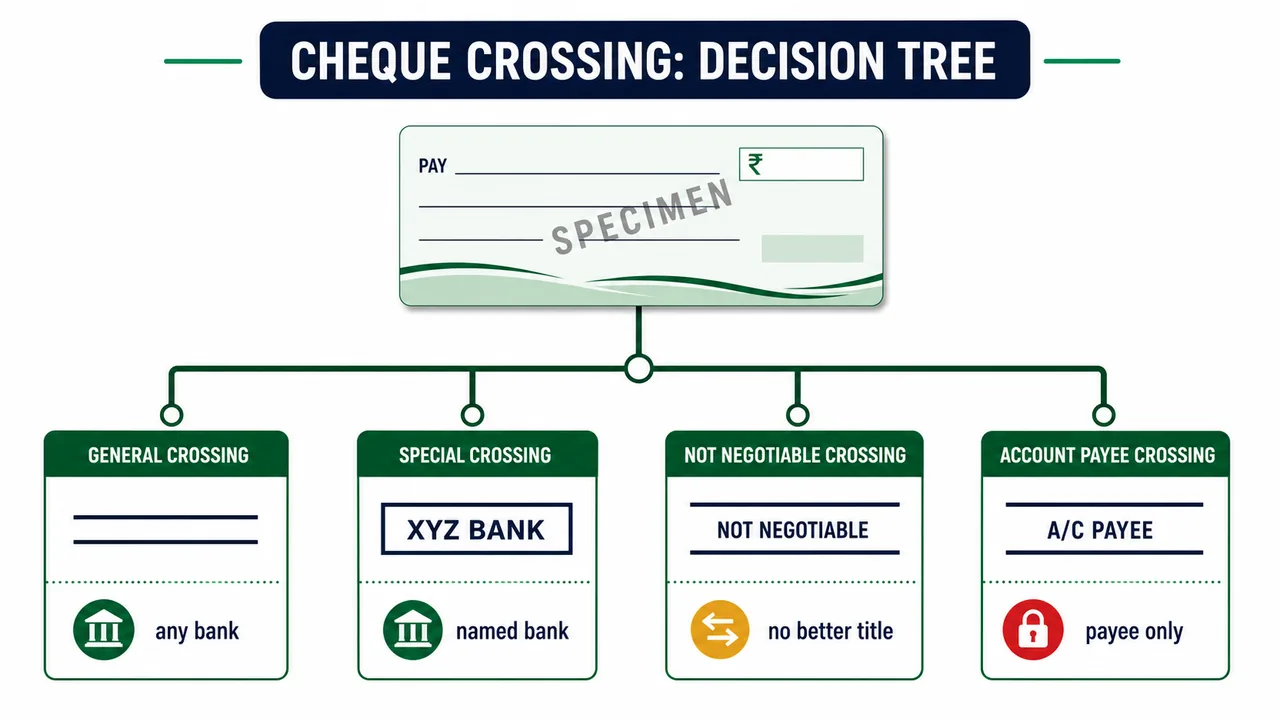

Types of Crossing

The broad categories are General Crossing and Special Crossing.

General Crossing of Cheque

Defined under Section 123 of the NI Act:

- It consists of two parallel transverse lines across the face of the cheque.

- With or without words like "and company" or "not negotiable".

- Essential Element: The two parallel lines are mandatory. Words are optional.

Effect: The paying banker shall not pay cash at the counter. Payment must be made only to a banker (any bank).

Interestingly, words are not strictly bound by location. For instance, if a cheque is presented with 'Mumbai' written between the lines, it is still a valid crossing and will be paid even if presented in Bangalore.

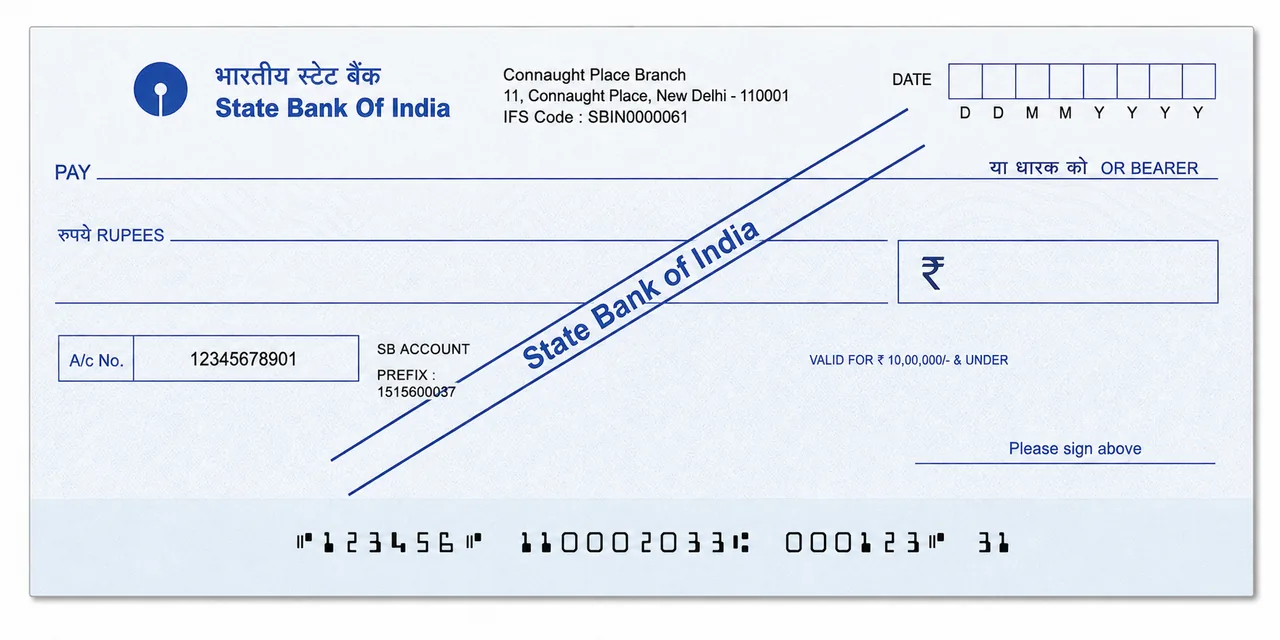

Special Crossing of Cheque

Defined under Section 124 of the NI Act:

- The name of a banker is written across the face of the cheque.

- With or without the two parallel transverse lines.

- Essential Element: The Name of the Banker is mandatory. Parallel lines are optional.

Effect: The paying banker must pay the amount only to the banker to whom it is crossed (or their agent for collection).

This type of crossing is generally done by banks during the collection process.

- Two Branches: A special crossing favouring two or more branches of the same bank is valid and the cheque can be paid.

- Two Banks: A special crossing favouring two independent banks means the cheque strictly should not be paid unless one bank is acting as the agent for the other for collection.

Not-negotiable Crossing of Cheque

Defined under Section 130, this crossing includes the words "not negotiable" between the crossing lines.

- Transferability: The cheque remains transferable. It can be endorsed and delivered to another person just like a normal cheque.

- Clarification: The words 'Not Negotiable' do NOT mean 'not transferable'. They only restrict the negotiability (quality of title), not the transferability (ability to pass it on).

- Title: The key feature is that "Nemo dat quod non habet" (nobody can give what he does not have) applies. The transferee cannot get a better title than the transferor.

- Normal Cheque: If A steals a bearer cheque and gives it to B (who takes it in good faith for value), B becomes a Holder in Due Course and gets a good title. B can claim the money.

- Not Negotiable Cheque: If A steals a 'Not Negotiable' cheque and gives it to B (even if B is innocent), B gets NO title because A had no title (thief). B cannot claim the money and must return it to the true owner.

- Consequently, the payee or endorsee is merely a holder, and can never become a holder in due course if there is a defect in the chain.

- Security Advantage: This crossing is mainly for the protection of the drawer and true owner.

- If the cheque is lost or stolen, the wrong holder cannot pass a clean title to someone else.

- It closes the usual Holder in Due Course escape route that may otherwise protect an innocent transferee.

- This makes recovery easier, because the legal right to the money stays tied to the rightful owner.

- In short, it gives better safety for high-value or sensitive payments without completely stopping transfer.

Account Payee Crossing of Cheque

- Legal Status: Unlike General or Special crossings, this is not defined in the NI Act. It evolved through judicial practice and usage, and is now enforced via RBI instructions.

- Method: It contains the words 'account payee' or 'payee's account only' between the crossing lines.

- Effect: It acts as a direction to the collecting banker. The bank must collect the amount and credit it only to the account of the named payee. It cannot be credited to any other person's account.

- Transferability: This is the most restrictive crossing. It renders the cheque non-transferable.

- Unlike 'Not Negotiable' (which allows transfer with risk), 'Account Payee' prohibits further negotiation entirely. It cannot be endorsed to a third party.

- Exception (RBI Rule): To help rural/small depositors, a cheque up to Rs. 50,000 drawn in the name of a member of a Primary Credit Cooperative Society can be collected by the society's bank account on behalf of the member.

- Example: Mr. A (a farmer) receives a cheque for Rs. 40,000. He has no commercial bank account but is a member of 'Village Coop Society'. He can deposit the cheque with the Society. The Society collects it through its own bank account. The collecting bank is permitted to credit the Society's account, even though the cheque is 'Account Payee' to Mr. A.

Cancellation of Crossing of Cheque

If a drawer wishes to revoke a crossing ("opening the cheque"), it can be done only by the drawer by signing with their full signature (initials are not sufficient) and writing "Pay Cash".

- Once cancelled, it becomes an open cheque and can be paid in cash.

- Joint Accounts: In "Either or Survivor" accounts, any one account holder can cancel the crossing.

Liability for payment of crossed cheque

If a bank pays a crossed cheque contrary to the crossing instructions (e.g., pays cash over the counter for a general crossing), it faces liability under Section 129.

- Why? It is a breach of mandate. The customer's instruction (via crossing) was to pay only through a bank account.

- Consequence: The paying banker shall be liable to the true owner of the cheque for any loss they may sustain.

- Scenario: A writes a crossed cheque to B. The cheque is stolen by C. C goes to the bank and somehow convinces the teller to pay cash. The bank pays C.

- Result: The bank is liable to B (the true owner) and must compensate B for the full amount, because it ignored the safety instruction of the crossing.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Collection Relationship | In the collection of a cheque, the bank acts as the Agent and the customer as the Principal. |

| Conversion | An unauthorized act of collecting a cheque for someone who is not the true owner, depriving the owner of their property. It is a punishable offense under the Criminal Procedure Code. |

| Protection against Conversion | Available to banks under Sec 131 (Cheques) and Sec 131-A (Demand Drafts) of the NI Act, provided collection is for a KYC-compliant customer, in good faith, without negligence, and the instrument is crossed. |

| Material Alteration | An alteration that changes the rights/liabilities or basic character (e.g., date, amount, payee name, crossing cancellation). It makes the cheque void u/s 87. Defined under Sec 62 of Indian Contract Act. |

| Fraud Prevention (UV Lamp) | Cheques of Rs. 2 lac and above must be examined under an Ultra-Violet (UV) lamp. |

| Alterations by Drawer | Under CTS, no alterations are allowed even by the drawer, except for revalidation of date. (If drawer makes a cutting, he cannot simply confirm by full signature for other details under CTS rules). |

| Crossing | Drawer's direction to pay only to a bank (not cash). Can be done by Drawer, Holder, or Collecting Bank. BOE and Promissory Notes cannot be crossed. |

| General Crossing | Two parallel transverse lines. Lines are essential; words are secondary. |

| Special Crossing | Name of the bank is written. Name is essential. Payment only to that bank. |

| Not Negotiable Crossing | Contains words "Not Negotiable". Defined u/s 130. Transferee gets no better title than transferor. Standard "holder in due course" protection does not apply. |

| Account Payee Crossing | Recognized by practice (not NI Act). Funds must go to payee's account only. Not transferable/endorsable. Exception: Coop Society members up to Rs. 50,000. |

Lesson Doubts

Ask questions, get expert answers