📜 Payment of Cheques

Understanding bank's obligations u/s 31 NI Act, conditions for payment, handling insufficient funds, and simultaneous presentation rules.

Bank's Obligation

Obligation of Bank u/s 31 NI Act

Under Section 31 of the Negotiable Instruments Act, a banker has a statutory obligation to pay cheques drawn by a customer, provided certain conditions are met.

- Mandatory Payment: The bank must honor the cheque if the customer has sufficient funds properly applicable to the payment and the cheque is valid.

- Unlawful Dishonour: If the bank wrongly dishonours a valid cheque despite having funds, it is considered unlawful.

- Liability: In such cases, the bank is liable to compensate the drawer for any loss or damage caused by the wrongful dishonour (e.g., injury to credit/reputation).

Dispute on Payment

If a bank makes a payment and the customer later disputes it (claiming it shouldn't have been paid), the burden of proof lies with the bank. The bank must prove that the payment was a payment in due course to be discharged from liability.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Bank's Obligation

Obligation of Bank u/s 31 NI Act

Under Section 31 of the Negotiable Instruments Act, a banker has a statutory obligation to pay cheques drawn by a customer, provided certain conditions are met.

- Mandatory Payment: The bank must honor the cheque if the customer has sufficient funds properly applicable to the payment and the cheque is valid.

- Unlawful Dishonour: If the bank wrongly dishonours a valid cheque despite having funds, it is considered unlawful.

- Liability: In such cases, the bank is liable to compensate the drawer for any loss or damage caused by the wrongful dishonour (e.g., injury to credit/reputation).

Dispute on Payment

If a bank makes a payment and the customer later disputes it (claiming it shouldn't have been paid), the burden of proof lies with the bank. The bank must prove that the payment was a payment in due course to be discharged from liability.

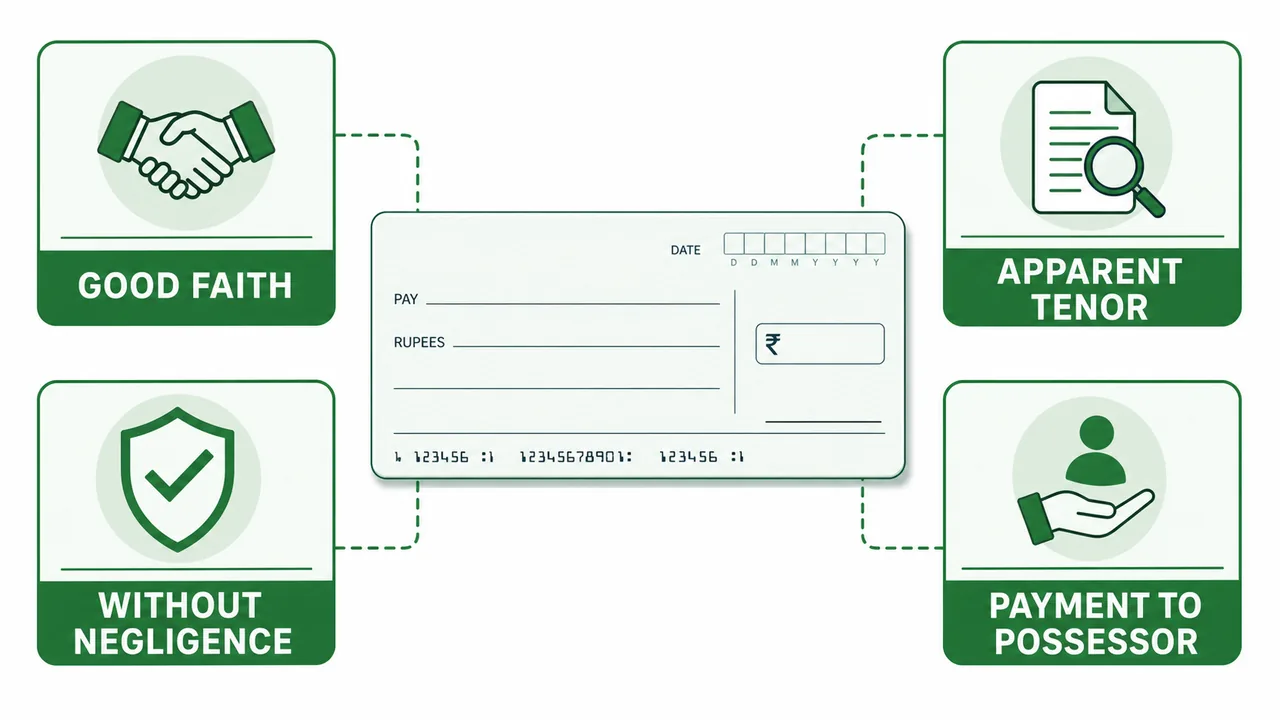

Payment in Due Course

Defined under Section 10 of the NI Act, a payment is considered a payment in due course (valid discharge) only if it meets these criteria:

- Good Faith: The payment was made honestly and without fraudulent intent.

- Without Negligence: The bank took reasonable care (e.g., checking signatures).

- Apparent Tenor: The payment matches the visible instructions on the instrument.

- To Possessor: The money was paid to a person in possession of the instrument (bearer or endorsee).

Important Conditions for Payment of Cheque

Before honoring a cheque, the bank must ensure specific conditions are met:

Signatures as per Record

- Verification: The drawer's signature on the cheque must match the specimen signature recorded with the bank.

- Forgery: A forged signature gives no mandate to the bank. If the bank pays a forged cheque, it cannot debit the customer's account.

- Different Signatures: If the signature on the cheque differs from the bank's records, the bank has no obligation to pay.

- Example: If 'Suresh Kumar Sharma' instructs the bank to honor cheques signed as 'SK Sharma', the bank should return a cheque signed as 'Suresh K Sharma', even if it is genuinely signed by him. The customer cannot demand reversal later for a signature he authorized, but strictly speaking, the bank follows the recorded mandate.

Sufficient Balance in Account

The cheque must be drawn against sufficient funds in the same account.

- No Right to Combine: A customer cannot expect the bank to combine balances from different accounts without specific arrangement.

- Example: If X has Rs. 2000 in a Savings Account and Rs. 8 Lakhs in a Current Account, a cheque for Rs. 2100 drawn on the Savings Account will be returned. The bank is not obliged to transfer funds from the Current Account to cover it.

Minimum Balance Condition

Banks usually require a minimum balance to be maintained. However, the obligation to pay depends on the actual balance available, not the minimum balance rule.

- Example: Y has Rs. 3000 in his account. The minimum balance requirement is Rs. 1500. A cheque for Rs. 3000 is presented.

- Result: The bank must pay the cheque because there are sufficient funds to cover the amount. The bank may charge a penalty for non-maintenance of minimum balance later, but it cannot dishonour the cheque for this reason.

Presentation after Business Hours

Payment to Payee

- Rule: A cheque presented after official business hours is not a payment in due course.

- Consequence: The bank should not pay. If it does, and the customer suffers a loss (e.g., they stopped payment the next morning), the bank will be liable.

Payment to Drawer

- Discretion: If the drawer themselves presents the cheque after hours, the bank has discretion to pay or refuse.

- Immunity: If the bank pays the drawer after hours, and later a Garnishee Order (court attachment) arrives, the bank is not liable because the payment was made to the customer before the order was received.

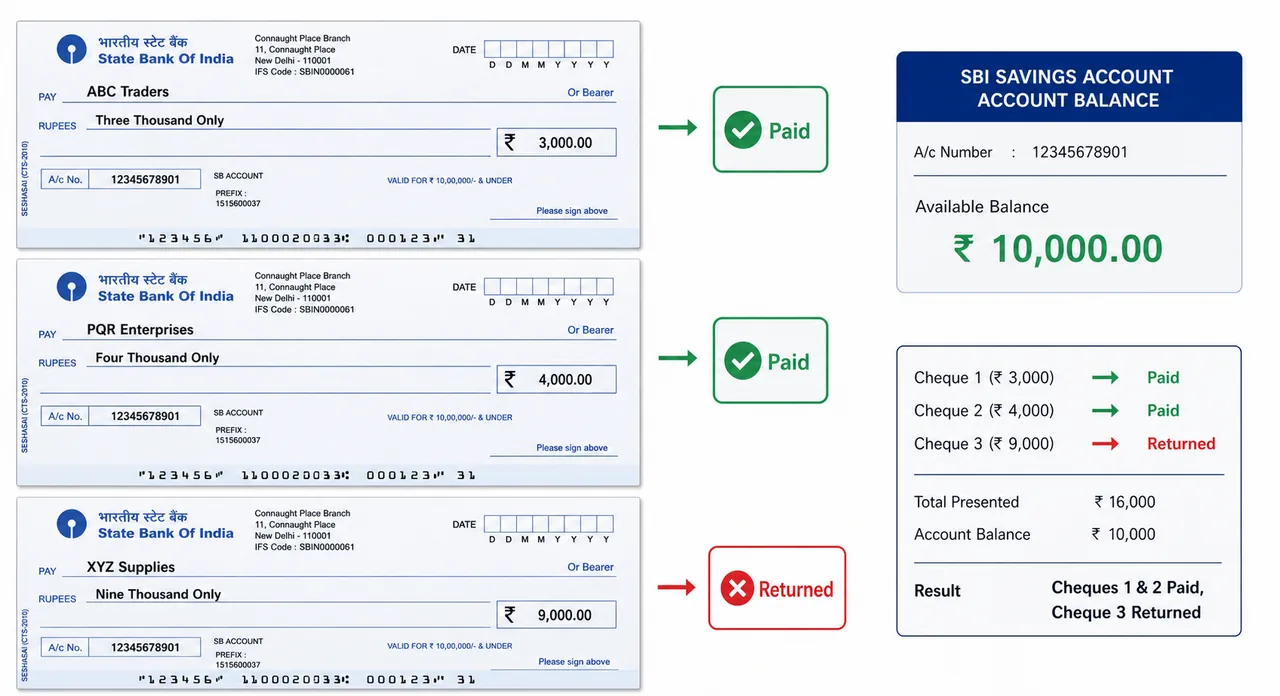

More than one Cheque Presented Simultaneously

If multiple cheques are presented at the same time (e.g., in clearing) and funds are insufficient to pay all, the bank generally follows the Principal of Discharge of Max Liability:

- Priority 1: Cheques for Government dues or utility payments are typically prioritized.

- Priority 2: Maximize the number of cleared cheques. The bank tries to pay the combination of cheques that discharges the maximum number of payments.

- Logic: If the balance is Rs. 10,000, and three cheques are presented for Rs. 3,000, Rs. 4,000, and Rs. 9,000.

- Action: The bank will pay the first two (Total Rs. 7,000) and return the third (Rs. 9,000). This clears 2 cheques instead of just 1, reducing total dishonours.

- Priority 3: Chronological order by date of issue (early date first).

- Priority 4: Serial number order (lower serial number first).

When Not to Pay

Even if there are sufficient funds, a bank must refuse payment in the following circumstances:

- Defective Instrument: If the cheque is post-dated (future date), stale (expired validity), mutilated, or incomplete.

- Countermanding: If the drawer has issued a "Stop Payment" instruction.

- Status of Drawer: On receiving notice of the drawer's death, insolvency, or insanity.

- Legal Orders: On receipt of a Garnishee Order or Attachment Order, if the order amount exceeds the available balance.

- Other Reasons: Insufficient funds, signature mismatch, or presentation outside business hours.

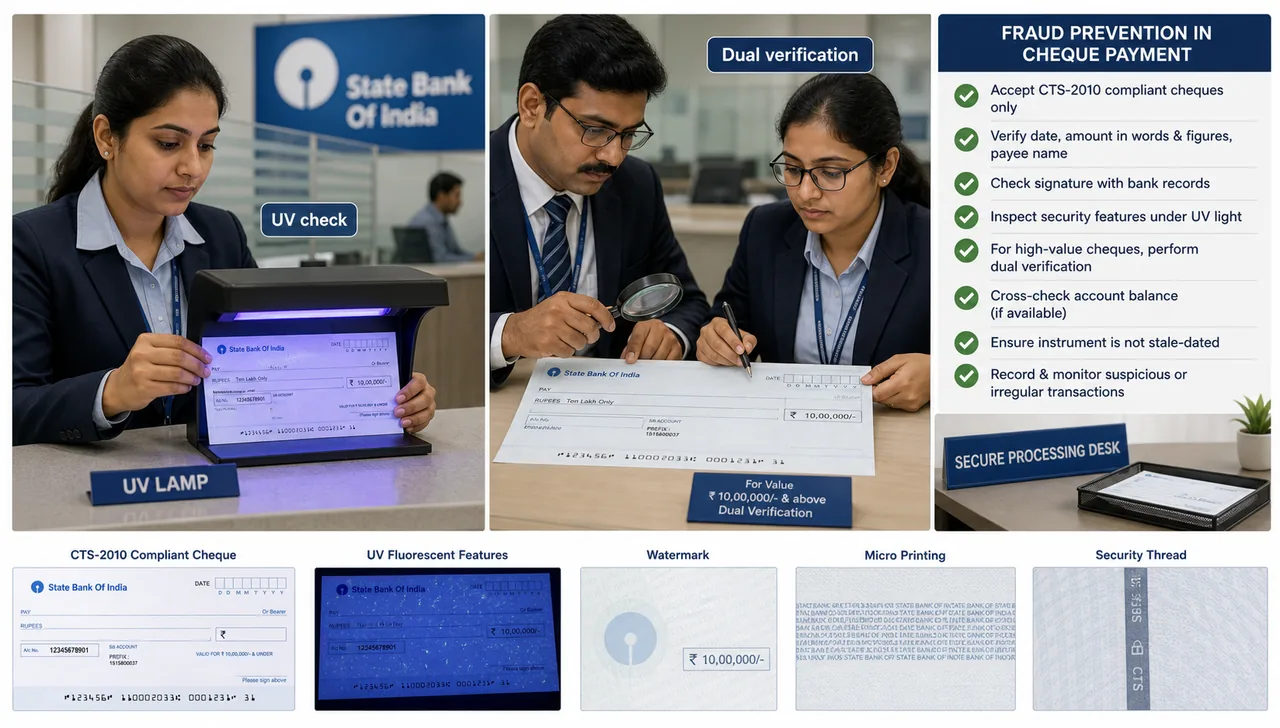

Fraud Prevention Measures

To safeguard against fraud, banks follow strict protocols:

- CTS Standards: Banks should process only CTS-2010 compliant cheques (which have enhanced security features).

- UV Scanning: Cheques above Rs. 2 Lakhs should be examined under an Ultra-Violet (UV) lamp to detect chemical alterations.

- Multiple Checks: Cheques above Rs. 5 Lakhs undergo multiple levels of checking (passed by at least two officers) to ensure scrutiny.

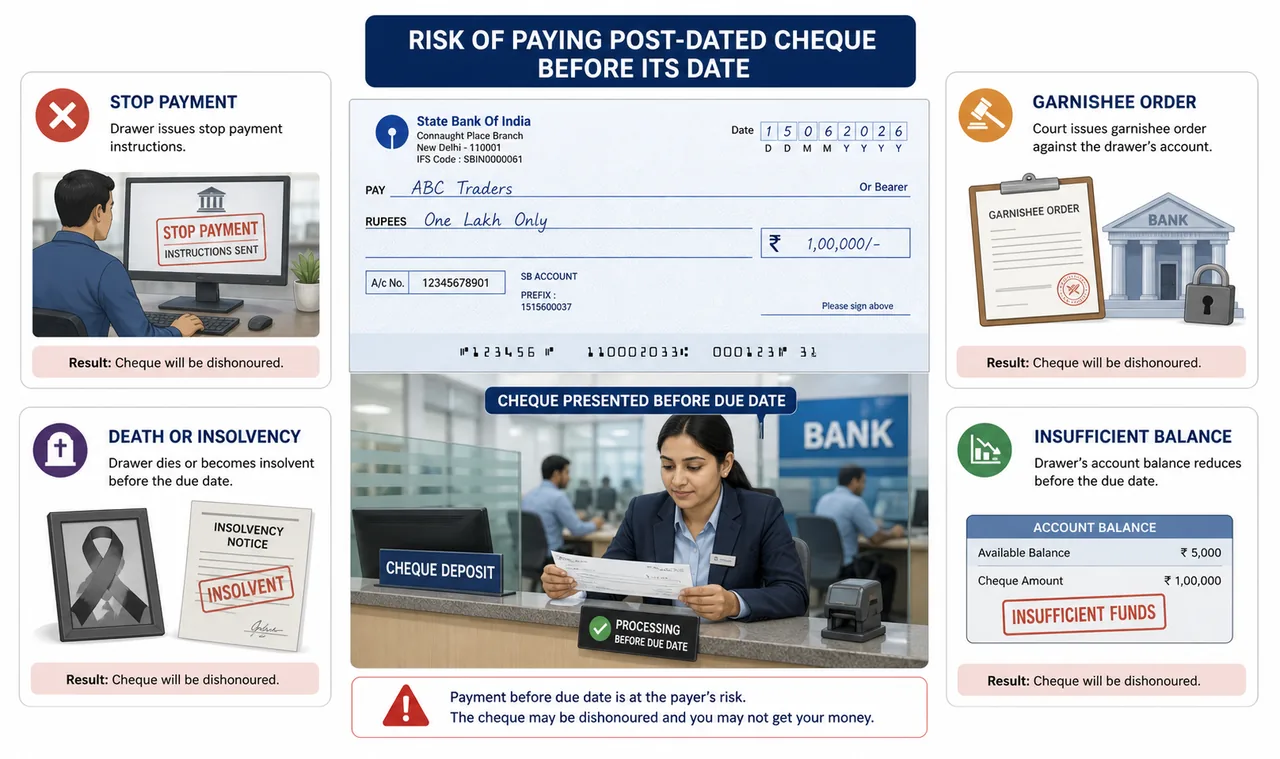

Risk in Payment of Post-Dated Cheques

Paying a post-dated cheque before its date carries significant risk for the bank. If a bank pays it early, it may face liability if:

- The customer dies or becomes insolvent before the actual date of the cheque.

- The customer issues a "Stop Payment" order before the date arrives.

- A Garnishee Order is received before the date.

- Another valid cheque is dishonoured due to the depletion of funds caused by the early payment.

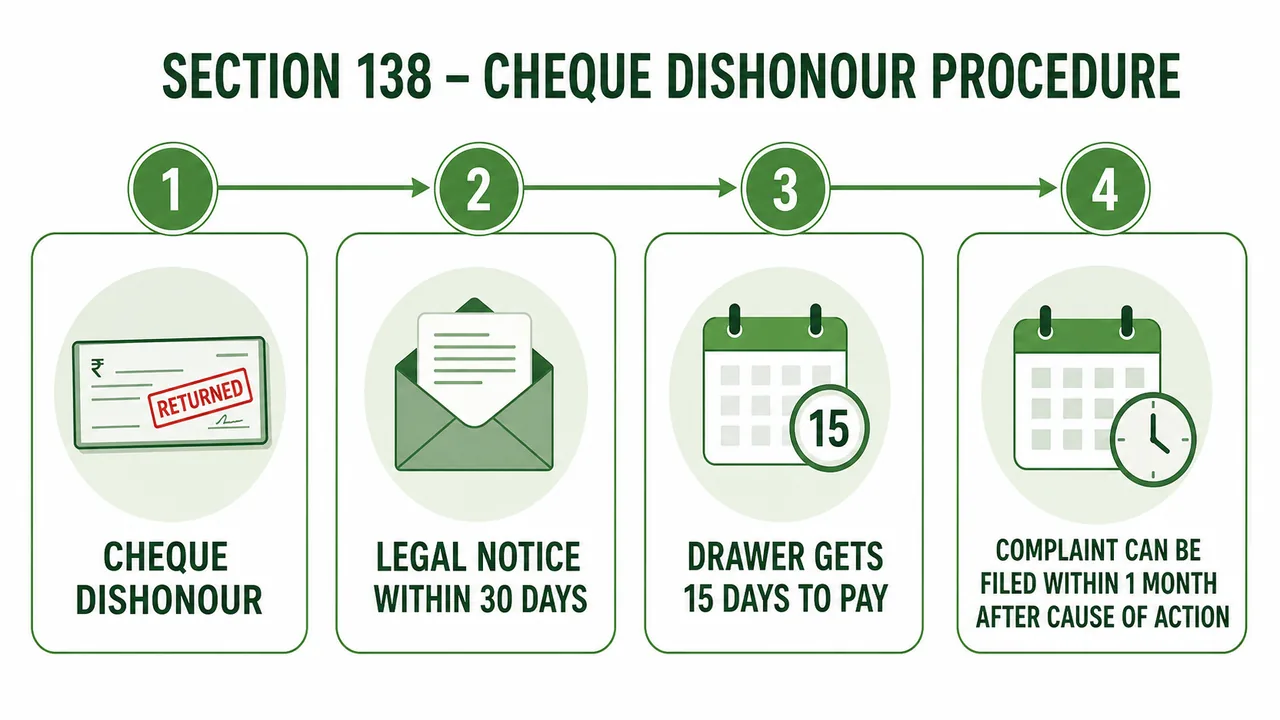

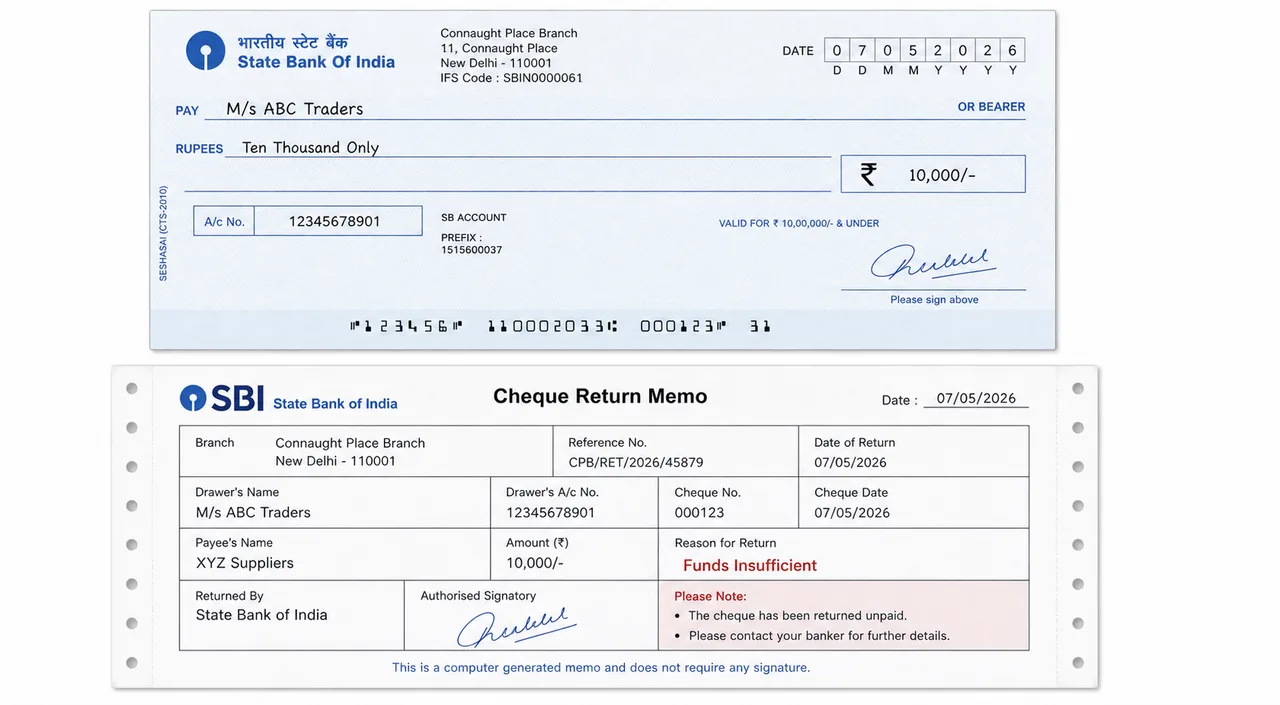

Dishonour of Cheques (Section 138 NI Act)

Dishonour of a cheque for insufficiency of funds is a criminal offence under Section 138 of the NI Act.

- The Offence: If a cheque issued to discharge a debt/liability is returned unpaid due to "Insufficient Funds" (or exceeds arrangement), the drawer is deemed to have committed an offence.

- Right to Sue: The holder (payee/endorsee) gets the right to file a criminal suit against the drawer.

- Jurisdiction: The suit can be filed before a First Class Judicial Magistrate or Metropolitan Magistrate.

- Venue for Filing Complaint (Jurisdiction):

- Standard Case (Collection): If the payee deposits the cheque in their own account, the complaint must be filed in the court having jurisdiction over the Payee's Bank Branch.

- Benefit: This allows the payee to file the case in their own city/locality (2015 Amendment).

- Rare Case (Over the Counter): If the payee presents the cheque personally at the drawer's bank, the jurisdiction is the court covering the Drawer's Bank Branch.

- Standard Case (Collection): If the payee deposits the cheque in their own account, the complaint must be filed in the court having jurisdiction over the Payee's Bank Branch.

- Venue for Filing Complaint (Jurisdiction):

Prerequisites for Filing Suit

To legally proceed under Section 138, these conditions must be met:

- Debt/Liability: The cheque must have been issued to discharge a legally enforceable debt or liability (not a gift).

- Timely Presentation: The cheque must be presented within its validity period (3 months).

- Return Reason: The core offence is insufficiency of funds, but courts interpret this broadly to catch evaders.

- Extended Scope: Approaches like "Stop Payment", "Account Closed", or "Refer to Drawer" are treated effectively as insufficient funds if the underlying cause was lack of money.

- Logic: You cannot escape the law by simply closing your account or ordering a stop payment just before the cheque hits the bank.

Legal Procedure

Step 1: Legal Notice

- Upon dishonour, the holder must send a legal notice to the drawer within 30 days of receiving the "Cheque Return Memo" from the bank.

- The notice demands payment of the cheque amount.

Step 2: Waiting Period

- The drawer is given 15 days from the receipt of the notice to make the payment.

Step 3: Cause of Action

- If the drawer fails to pay within those 15 days, the cause of action arises (i.e., the crime is complete).

- The holder can then file a complaint in court within one month from the date the cause of action arose.

- Condonation of Delay: If you miss this 1-month deadline, the court has the power to "condone" (excuse) the delay if you can prove you had "sufficient cause" (e.g., severe illness, lockdown, etc.) for not filing on time.

Punishments

- Imprisonment: Up to 2 years.

- Fine: Up to twice the amount of the cheque.

- Compounding: If the parties compromise (settle), the court may impose a smaller fine (e.g., up to Rs. 5000) for wasting court time.

Interim Compensation (Section 143A)

To prevent delay tactics, the court can order the drawer to pay Interim Compensation:

- Amount: Up to 20% of the cheque amount.

- Timeline: Must be paid within 60 days (court can extend by 30 days).

- Acquittal: If the drawer is eventually found innocent, the complainant must return this money with interest (at the bank rate) within 60 days.

Appeal by Drawer (Section 148)

If the drawer is convicted and wants to appeal to a higher court, they must deposit min. 20% of the compensation/fine amount with the appellate court.

Other Liability Issues

Companies and Partnerships

- Partnerships: All partners actively involved are liable. sleeping partners may be exempt.

- Companies: All persons in charge of the business (e.g., Managing Directors, Signatories) are liable. Unconnected directors (like Independent Directors) may be exempt.

Duty of Bank on Dishonour

- Timeliness: As per the Goiporia Committee, dishonoured cheques must be returned/dispatched to the customer within 24 hours.

- Return Memo: The bank must attach a "Cheque Return Memo" stating the specific reason (e.g., "Funds Insufficient").

- Reporting: Dishonour of cheques of Rs. 1 Crore and above must be reported to the bank's controlling office for MIS purposes.

- Penalty: Banks typically withdraw the cheque book facility if cheques valued at Rs. 1 Crore+ are repeatedly dishonoured for insufficient funds.

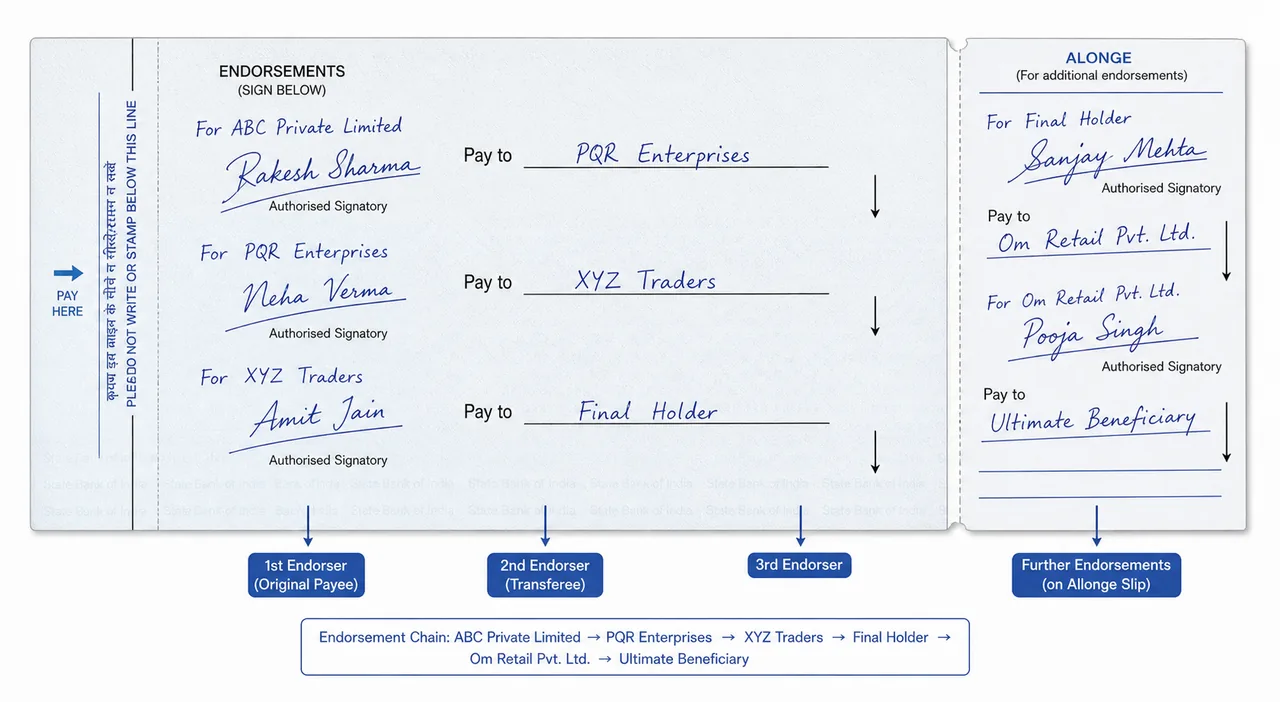

Endorsements

Endorsement is the act of signing a cheque (usually on the back) for the purpose of negotiation (transferring title).

-

Parties involved in Endorsement:

- Endorser: The person who signs the back of the cheque to transfer it. By signing, they promise that if the cheque bounces, they will pay the amount to the new holder.

- Endorsee: The person to whom the cheque is transferred (the new owner).

-

Applicability (When is it needed?):

- Order Cheques: MUST be endorsed to be transferred. If I write "Pay to Rahul", Rahul must sign (endorse) it to transfer it to someone else.

- Bearer Cheques: Do NOT need endorsement negotiation. They can be transferred by mere delivery (handing it over).

- Note: If a bearer cheque is signed on the back (endorsed in blank), it remains a bearer cheque (Section 85-2).

-

Rules:

- Unlimited Transfers: A cheque can be endorsed any number of times until the space runs out.

- Allonge: If the back of the cheque is full of signatures, a separate slip of paper called an "Allonge" can be pasted to the cheque to continue endorsements. It is legally treated as part of the cheque.

-

Condition: The endorsement must be regular (technically correct chain).

-

Forgery Protection: The bank is not responsible for verifying the genuineness of the signatures. If the endorsement appears regular but is actually forged, the bank is still discharged from liability (it is a payment in due course).

-

Irregularity: However, if the endorsement is genuine but irregular (e.g., wrong spelling or break in chain), the bank gets no protection.

Example - The Endorsement Chain:

- Cheque Issued: "Pay to Amit".

- 1st Endorsement: Amit signs the back: "Pay to Bob" (Signature: Amit).

- 2nd Endorsement: Bob signs below it: "Pay to Charlie" (Signature: Bob).

- Presentation: Charlie presents it to the bank.

Scenario A (Forgery Protection): If a thief stole the cheque from Amit and forged Amit's signature to transfer it to Bob, the Bank is PROTECTED (discharged) because the chain looks regular. The bank cannot be expected to know Amit's signature.

Scenario B (Irregularity - No Protection): If the cheque was "Pay to Amit" but the endorsement signature says "Amita" (spelling mismatch), the bank is NOT PROTECTED if they pay. This is an apparent irregularity.

Types of Endorsements

| Type of Endorsement | Example / Action | Effect |

|---|---|---|

| Blank Endorsement | Signature only (no name added). | The cheque becomes payable to Bearer. |

| Endorsement in Full | Signing "Pay to A". | Transfers specific ownership to A. Requires logical chain. |

| Restrictive | "Pay to A only". | Prohibits further negotiation. A cannot transfer it to B. |

| Sans Recourse | "Pay to A without recourse to me". | The endorser excludes their own liability if the cheque bounces. |

| Facultative | "Pay to A. Notice of dishonour waived". | The endorser waives their right to receive notice, accepting liability directly. |

| Partial | "Pay Rs. 5000 to A" (on Rs. 10k cheque). | Invalid. Negotiation must be for the full amount. |

| Forged | B signs as A. | A forged endorsement passes no title. The holder has no right to the money. |

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Bank's Obligation (Sec 31) | Bank must pay valid cheques if funds are sufficient. Wrongful dishonour makes the bank liable for damages to the drawer. |

| Payment in Due Course (Sec 10) | Valid discharge if paid in good faith, without negligence, according to apparent tenor, to the possessor. |

| Signature Verification | Must match specimen. Forged signature = No mandate (Bank cannot debit). Slight variations (e.g. S.K. vs Suresh K.) justify return. |

| Sufficient Funds | Must be in the same account. Bank has no right to combine accounts without arrangement. Must pay even if paying breaches minimum balance rules (penalty applicable later). |

| Presentation Time | Payment after business hours is not in due course (liable if stop payment comes next morning). Payment to drawer after hours is allowed (saves bank from Garnishee Order received later). |

| Simultaneous Presentation | Priority Order: 1. Govt/Utility dues → 2. Maximize number of cleared cheques → 3. Date → 4. Serial Number. |

| Mandatory Refusal | Stop Payment, Post-dated, Stale, Mutilated, Death/Insolvency/Insanity (on notice), Garnishee Order (> balance). |

| Fraud Prevention | UV Scan for > Rs. 2 Lakhs. Multiple Checking for > Rs. 5 Lakhs. CTS-2010 standards. |

| Post-Dated Cheque Risk | Early payment is risky. Bank liable if drawer dies, stops payment, or funds deplete before the actual date. |

| Dishonour Offence (Sec 138) | Criminal offence for "Insufficient Funds". Includes "Stop Payment" or "Account Closed" if used to evade payment. |

| Sec 138 Penalties | Imprisonment up to 2 years and/or Fine up to 2x cheque amount. |

| Jurisdiction (Venue) | Collection: Court at Payee's Branch (Standard). OTC: Court at Drawer's Bank (Rare). |

| Legal Timelines | Legal Notice: Within 30 days of return. Payment Time: 15 days for drawer. Filing Complaint: Within 1 month of failure to pay. (Court can condone delay for sufficient cause). |

| Interim Compensation (Sec 143A) | Court may order drawer to pay up to 20% of cheque amount within 60 days (extendable by 30). |

| Appeal Deposit (Sec 148) | Drawer must deposit min. 20% of fine/compensation to appeal conviction. |

| Endorsement Parties | Endorser (Signer/Transferor - Liable if bounced). Endorsee (Receiver/New Owner). |

| Endorsement Rules | Order Cheques: Require Endorsement + Delivery. Bearer Cheques: Delivery only (Signing does not change bearer status). Allonge: Slip for extra signatures. |

| Forgery Protection (Sec 85(1)) | Bank IS Protected if endorsement chain is regular but forged (hidden). Bank NOT Protected if endorsement is irregular (visible mismatch). |

| Endorsement Types | Blank (becomes Bearer), Full (Specific person), Restrictive (No further transfer), Sans Recourse (No liability), Facultative (Waives notice). |

Lesson Doubts

Ask questions, get expert answers