💸 Monetary Policy

Comprehensive overview of RBI's Monetary Policy, MPC, Policy Rates, and detailed 2026 Directions on CRR and SLR.

Monetary and Credit Policy

The Monetary and Credit Policy is a crucial macroeconomic tool used by the Reserve Bank of India (RBI) to manage the supply of money, interest rates, and credit in the economy. This policy helps maintain price stability while ensuring adequate flow of credit to support continuous economic growth.

- Announcement: RBI announces the policy annually (normally in April). This annual announcement provides the broader roadmap for the financial year, outlining the primary focus areas for the economy.

- Review: Policy review is done on a bi-monthly basis. That means every two months (six times a year), the central bank assesses the current economic conditions and makes necessary adjustments to crucial rates to respond to ongoing changes like inflation shifts or economic slowdowns.

- Types of Policy:

- Expansionary Policy (Easy Money): Used during low economic growth. CRR, SLR, Repo are reduced to increase liquidity. By slashing these reserve requirements and policy rates, the RBI encourages banks to lend more money at cheaper interest rates to the public. This injected cash helps individuals and businesses spend and invest, thereby reviving an economy that is growing slowly.

- Contractionary Policy (Tight/Dear Money): Used during high inflation. CRR, SLR, Repo are increased to suck out liquidity. When inflation (prices of goods and services) gets too high, the RBI takes steps to make borrowing expensive and restricts the amount of money floating in the markets. By restricting cash availability, overall demand decreases, effectively cooling down inflationary pressures.

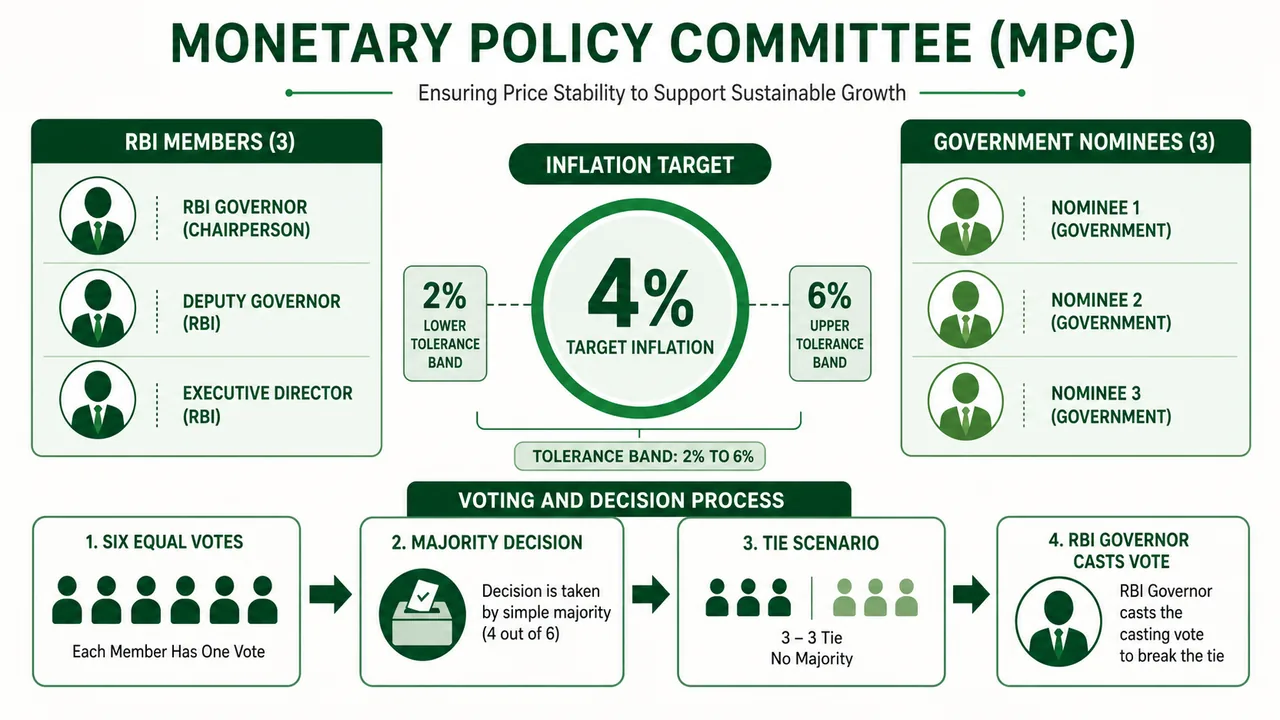

Monetary Policy Committee (MPC)

The Monetary Policy Committee (MPC) is the dedicated, specialized body responsible for setting the benchmark interest rates in India. Before its inception, these decisions relied more heavily on the RBI Governor alone.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Monetary and Credit Policy

The Monetary and Credit Policy is a crucial macroeconomic tool used by the Reserve Bank of India (RBI) to manage the supply of money, interest rates, and credit in the economy. This policy helps maintain price stability while ensuring adequate flow of credit to support continuous economic growth.

- Announcement: RBI announces the policy annually (normally in April). This annual announcement provides the broader roadmap for the financial year, outlining the primary focus areas for the economy.

- Review: Policy review is done on a bi-monthly basis. That means every two months (six times a year), the central bank assesses the current economic conditions and makes necessary adjustments to crucial rates to respond to ongoing changes like inflation shifts or economic slowdowns.

- Types of Policy:

- Expansionary Policy (Easy Money): Used during low economic growth. CRR, SLR, Repo are reduced to increase liquidity. By slashing these reserve requirements and policy rates, the RBI encourages banks to lend more money at cheaper interest rates to the public. This injected cash helps individuals and businesses spend and invest, thereby reviving an economy that is growing slowly.

- Contractionary Policy (Tight/Dear Money): Used during high inflation. CRR, SLR, Repo are increased to suck out liquidity. When inflation (prices of goods and services) gets too high, the RBI takes steps to make borrowing expensive and restricts the amount of money floating in the markets. By restricting cash availability, overall demand decreases, effectively cooling down inflationary pressures.

Monetary Policy Committee (MPC)

The Monetary Policy Committee (MPC) is the dedicated, specialized body responsible for setting the benchmark interest rates in India. Before its inception, these decisions relied more heavily on the RBI Governor alone.

-

Constituted: September 2016 under Section 45ZB of the RBI Act, 1934 (inserted by the Finance Act, 2016). Established to formalise the inflation targeting framework — shifting monetary policy decisions from the sole discretion of the RBI Governor to a structured, committee-based approach with statutory backing.

-

Composition: 6 Members (3 from RBI + 3 nominated by Central Govt). This balanced structure ensures that both monetary experts and government-nominated economists collaborate for effective decision-making.

-

Task: To determine policy rates to achieve the inflation target. The sole primary objective of this committee is to make calculated adjustments to the repo rate and others to keep inflation firmly under control.

-

Inflation Target: 4% with a provision of (+/-) 2%. This means the RBI aims to keep the inflation rate strictly between 2% (minimum) and 6% (maximum). This flexible inflation targeting ensures economic stability without stunting growth.

-

Decision Making: By voting (1 member = 1 vote). RBI Governor has the casting vote (2nd vote) in case of a tie. While decisions are typically made as a majority vote among all members, the casting vote ensures a definitive conclusion can be reached if opinions are evenly split.

-

Meetings: At least 6 times a year. These meetings correspond with the bi-monthly policy reviews, ensuring frequent and timely reactions to economic shifts.

-

Report: Monetary Policy Report published every 6 months. This detailed report transparently explains to the public and the markets the sources of inflation and the forecasts for the short-to-medium-term future.

Policy Rates

These rates Impacting Cost of Money

Policy Rates directly dictate the interest costs associated with the financial system. When these change, they almost immediately impact the interest rates you see on home loans, business loans, and savings accounts.

- Repo Rate: The key policy rate. Also known as the Repurchase Agreement Rate, this is the interest rate at which the RBI strictly lends short-term money to commercial banks against government securities. It acts as the foundational benchmark for all other interest rates in the economy.

- Standing Deposit Facility (SDF): Repo – 0.25% (Floor of the corridor). Introduced as a tool to absorb excess liquidity without the RBI needing to provide collateral to banks. Because it is lower than the Repo, it acts as the baseline (floor) of the interest rate spectrum.

- Marginal Standing Facility (MSF): Repo + 0.25% (Ceiling of the corridor). This is an emergency borrowing window for banks. If a bank faces an acute shortage of funds, it can borrow overnight from the RBI against special securities, but at a slightly higher, penal rate—forming the uppermost limit (ceiling) of the corridor.

- Bank Rate: Repo + 0.25% (Rate for rediscounting bills). Unlike the Repo Rate which deals with short-term secured lending, the Bank Rate acts as the penal rate and the standard rate for long-term lending and rediscounting commercial papers.

- Reverse Repo Rate: Repo - 0.65% (Fixed rate, largely replaced by SDF). Historically, this was the rate at which the RBI borrowed from banks (or banks parked their excess funds with the RBI). Today, the SDF acts as the primary tool for absorbing liquidity due to its collateral-free nature.

Reserve Ratios

These are the rates Impacting Liquidity

While policy rates change the cost of money, Reserve Ratios actively restrict the physical amount (volume) of money a bank is legally allowed to lend out to customers.

- Cash Reserve Ratio (CRR): A highly strict cash buffer all banks must set aside with the RBI to ensure safety.

- Statutory Liquidity Ratio (SLR): A mandatory proportion of a bank's deposits kept in safe, liquid assets like gold or government bonds.

Interest Rate Types

Interest rates in the banking sector can fall broadly into two major categories depending on how strictly they are controlled by external authorities vs market forces.

| Deregulated Rates | Regulated Rates |

|---|---|

| Savings Bank Rate | DRI Lending |

| Term Deposit Rates | NRLM / NULM Schemes |

| Lending Rates (MCLR/EBLR) | Crop Loans (Subvention) |

| Export Credit Rates |

Deregulated Rates are those where commercial banks have the freedom to decide the rates themselves, typically linked to benchmark market rates (like EBLR). Regulated Rates reflect subsidized or targeted lending guided directly by the government and RBI for social welfare and priority sectors (like agriculture and poverty alleviation).

Current Key Rates (as of June 5, 2026)

All monetary policy decisions ultimately result in changes to these key rates. Memorizing these is essential for any banking exam — they form the backbone of questions on monetary policy.

| Rate | Current Value |

|---|---|

| Repo Rate | 5.25% |

| Standing Deposit Facility (SDF) | 5.00% (Repo − 0.25%) |

| Marginal Standing Facility (MSF) | 5.50% (Repo + 0.25%) |

| Bank Rate | 5.50% |

| Reverse Repo Rate | 3.35% (fixed, largely replaced by SDF) |

| Cash Reserve Ratio (CRR) | 3.00% |

| Statutory Liquidity Ratio (SLR) | 18.00% |

TIP

Quick Memory Trick Once you know the Repo Rate, you can derive the entire corridor: SDF = Repo − 0.25% (floor), MSF = Bank Rate = Repo + 0.25% (ceiling). Just remember one number and calculate the rest.

On June 5, 2026, the RBI's MPC kept the Repo Rate unchanged at 5.25% and retained the Neutral stance. Reported reasons included the West Asia conflict, trade-route and supply-chain disruption risks, elevated energy prices, market volatility, and uncertainty around the monsoon. The updated FY27 projections reported after the meeting were GDP growth 6.6% and CPI inflation 5.1%.

2025-2026 Rate Cut Timeline

The RBI's easing cycle began in February 2025, with a total of 125 bps in cuts (from 6.50% to 5.25%) before pausing:

| Date | MPC Action | Repo Rate After | Notes |

|---|---|---|---|

| Feb 2025 | −25 bps | 6.25% | First cut of the cycle |

| Apr 2025 | −25 bps | 6.00% | Second consecutive cut |

| Jun 2025 | −50 bps | 5.50% | Aggressive cut + CRR cut by 100 bps (4% → 3%) + stance changed to Neutral |

| Dec 2025 | −25 bps | 5.25% | Fourth cut of the cycle |

| Feb 2026 | Held | 5.25% | First pause in the easing cycle |

| Apr 2026 | Held | 5.25% | Held steady — external risks and volatile crude |

| Jun 2026 | Held | 5.25% | Neutral stance retained; FY27 growth cut to 6.6% and inflation raised to 5.1% |

June 2026 Update: What Changed

This lesson already explains the framework. The June 2026 update is mainly about the latest MPC outcome and the market-access measures announced alongside it.

1. Policy outcome

| Item | June 5, 2026 status |

|---|---|

| Repo Rate | 5.25% |

| SDF | 5.00% |

| MSF / Bank Rate | 5.50% |

| Policy Stance | Neutral |

| FY27 GDP forecast | 6.6% |

| FY27 CPI inflation forecast | 5.1% |

2. Market-access measures announced with the June package

The June 5, 2026 package also added a few important current-affairs points:

- FAR widened: New 15-year, 30-year, and 40-year Government securities were brought under the Fully Accessible Route (FAR). Sovereign Green Bonds (SGrBs) in FAR-eligible tenors were also included.

- FPI limits under General Route relaxed: Three restrictions were removed:

- short-term investment limit

- concentration limit

- security-wise investment limit

- Overall caps retained: Even after these relaxations, the aggregate limits remain 6% of outstanding Central Government securities and 2% of outstanding State Government Securities (SGSs).

- Sub-categories merged: The separate general and long-term sub-limits for G-Sec/SGS investment were merged into a single limit.

- Tax exemption for FPIs in G-Secs: Interest and capital gains on Government securities for FPIs were exempted from income tax with effect from April 1, 2026.

- BIS exemption: The Bank for International Settlements (BIS) also received similar tax exemption on interest and capital gains from G-Sec investments.

- PROI equity access expanded: Individual Persons Resident Outside India (PROIs) were permitted to invest in listed Indian companies through the Portfolio Investment Scheme (PIS), with the per-investor cap raised from 5% to 10% and the overall limit for all individual PROIs raised from 10% to 24%.

IMPORTANT

Short answer line: "June 2026 brought a status quo on rates, but wider access for foreign investors in G-Secs and equities."

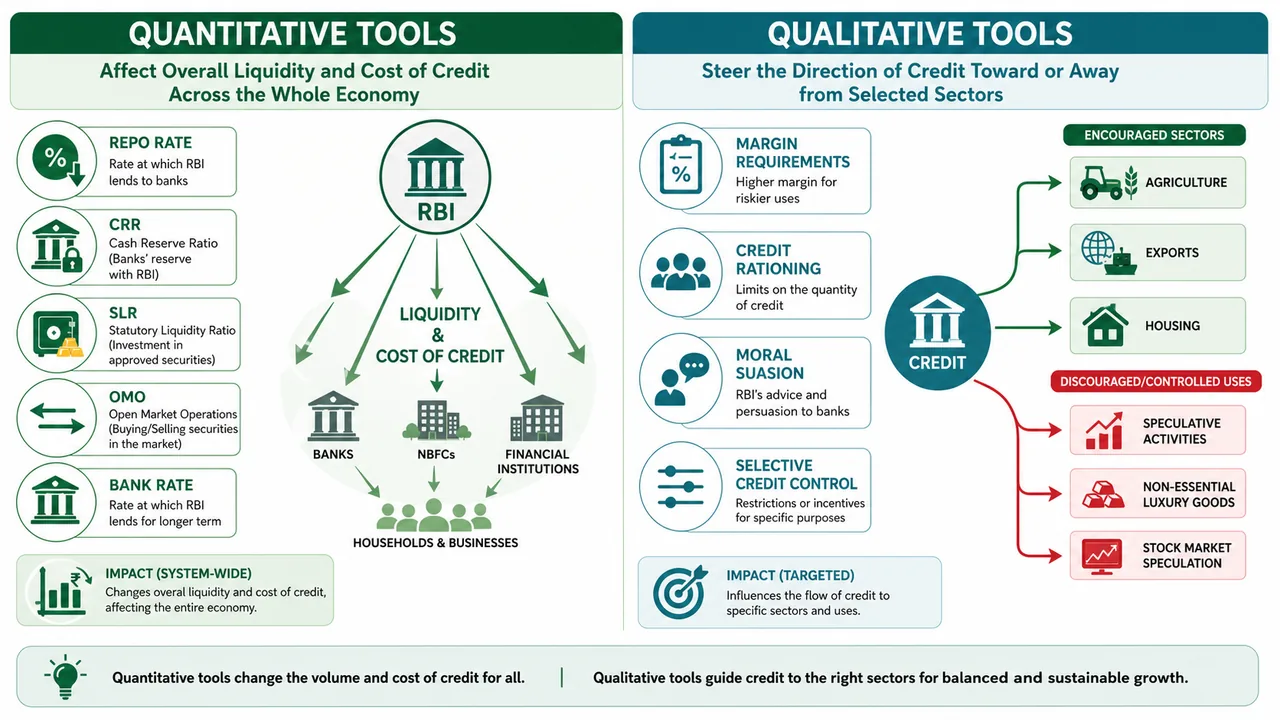

Monetary Policy Instruments

Now that we understand what the rates are, we need to understand how the RBI actually implements its policy decisions. The RBI doesn't simply announce a rate — it uses a toolkit of instruments to actively manage money supply, credit flow, and liquidity in the economy. These instruments fall into two broad categories:

- Quantitative Instruments — control the overall volume and cost of money

- Qualitative Instruments — control the direction and end-use of credit

A. Quantitative Instruments (General Credit Control)

Quantitative instruments are economy-wide tools that affect the total amount of money circulating in the banking system. They do not discriminate between sectors — when the RBI tightens or loosens using these tools, every bank and every borrower feels the impact. Think of them as controlling the size of the tap from which money flows.

1. Liquidity Adjustment Facility (LAF)

The Liquidity Adjustment Facility (LAF) is the RBI's primary framework for managing day-to-day (frictional) liquidity in the banking system. It is the most frequently used monetary policy tool. Every single day, banks either have a surplus of funds (they collected more deposits than they lent out) or a deficit (they lent out more than they received). The LAF helps balance this by providing a corridor system — a structured range within which overnight interest rates move.

| Component | Rate | Function |

|---|---|---|

| MSF (Ceiling) | Repo + 0.25% | Emergency overnight borrowing by banks — penal rate |

| Repo Rate (Middle) | Policy Rate | RBI lends to banks against govt securities (injects liquidity) |

| SDF (Floor) | Repo − 0.25% | Banks park excess funds with RBI — no collateral needed |

IMPORTANT

Why is it called a "corridor"? The SDF sets the floor — no bank will lend in the interbank market at a rate lower than what RBI pays via SDF. The MSF sets the ceiling — no bank needs to borrow in the market at a rate higher than the MSF because RBI always lends at MSF rate. This means the overnight interbank rate (call money rate) always stays within this corridor, keeping interest rates stable and predictable.

How LAF works in practice:

- When banks need funds → they borrow from RBI via Repo (pledging government securities as collateral). The RBI essentially buys those securities temporarily, releasing cash into the system. This injects liquidity.

- When banks have excess funds → they deposit surplus cash with RBI via SDF (earning interest, but without giving any collateral to RBI). This absorbs liquidity.

- The 14-day variable rate repo/reverse repo aligned with the CRR maintenance cycle is the main liquidity management tool. Unlike overnight repos that expire the next day, this 14-day instrument gives banks and the RBI a more stable, predictable window to manage liquidity over a fortnight.

- SDF and MSF operational window: 7:00 PM to 11:59 PM daily (revised from July 2025 to align with extended call money market hours).

Example: How the LAF Corridor Works

Suppose the Repo Rate is 5.25%. Then: - **SDF Rate** = 5.00% (floor) — banks earn 5.00% by parking funds with RBI - **MSF Rate** = 5.50% (ceiling) — banks pay 5.50% for emergency borrowing from RBIIf Bank A has excess ₹500 Cr today, it can either lend in the interbank call money market at ~5.10%-5.20%, or park it with RBI via SDF at 5.00%. The SDF guarantees a minimum return.

If Bank B urgently needs ₹200 Cr, it can borrow in the call money market at ~5.20%-5.30%, or go to RBI's MSF window at 5.50% (costlier, but guaranteed availability). The MSF acts as a safety net.

This ensures interbank rates hover around 5.00%–5.50%, keeping the transmission of monetary policy effective.

2. Open Market Operations (OMOs)

While the LAF handles temporary, day-to-day liquidity fluctuations, Open Market Operations (OMOs) are used to manage durable (structural) liquidity — long-term shifts in the money supply that cannot be fixed by overnight or 14-day operations. OMOs involve the outright purchase or sale of government securities by RBI in the open market.

| Action | RBI Does | Effect on Liquidity | When Used |

|---|---|---|---|

| Expansionary OMO | Buys govt securities from banks | Injects liquidity (increases money supply) | During tight liquidity / low growth |

| Contractionary OMO | Sells govt securities to banks | Absorbs liquidity (reduces money supply) | During excess liquidity / high inflation |

The key difference from LAF is permanence: in a Repo, the RBI buys securities but sells them back the next day (or in 14 days). In an OMO, the purchase or sale is outright and permanent — the money injected or absorbed stays in the system.

TIP

Exam Memory Aid OMO Buy = RBI gives money, takes securities = Liquidity increases. OMO Sell = RBI takes money, gives securities = Liquidity decreases. Think: "Buy = money Buy-lds up in the system."

Recent Example: In December 2025, RBI announced OMO purchases worth ₹2 trillion across four tranches plus a USD 10 billion USD/INR buy-sell forex swap to inject nearly ₹3 trillion of durable liquidity into the banking system. This was done to offset the liquidity drained by RBI's forex market interventions to defend the rupee.

3. Market Stabilisation Scheme (MSS)

Sometimes, the liquidity surplus in the economy is so massive and persistent that even regular OMOs cannot absorb it effectively. This typically happens during periods of large foreign capital inflows — when foreign investors pour dollars into India, RBI buys those dollars (to prevent excessive rupee appreciation), and in the process, releases a flood of rupees into the banking system. To handle such large-scale, enduring liquidity surpluses, the Market Stabilisation Scheme (MSS) was introduced in 2004 (on recommendations of the Deepak Mohanty Working Group, 2003).

How MSS works:

- RBI issues special short-term government securities (T-Bills, dated securities) to absorb excess liquidity. Banks buy these securities, and the cash goes out of the banking system.

- Typical tenor: less than 6 months (can vary based on need)

- Unlike regular government borrowing, MSS proceeds are held in a separate cash balance with RBI — they are not available for government spending. This is crucial — it means MSS is purely a monetary tool, not a way for the government to raise money.

- Used heavily during periods of large foreign capital inflows to sterilise the rupee liquidity created when RBI buys dollars

WARNING

Common Exam Confusion Students often confuse MSS with regular government borrowing. Remember: MSS proceeds are locked with RBI and cannot be used by the government. Regular T-Bills fund government expenditure; MSS T-Bills are purely for liquidity management.

4. Forex Swap Operations

Forex swaps are another powerful tool for managing rupee liquidity, particularly when the RBI's foreign exchange interventions (buying or selling dollars to stabilise the rupee) create unintended liquidity effects. RBI conducts USD/INR Buy-Sell or Sell-Buy swaps to inject or absorb rupee liquidity:

| Swap Type | RBI Action | Effect |

|---|---|---|

| Buy-Sell Swap | RBI buys USD now, agrees to sell later | Injects rupee liquidity (RBI pays rupees to buy dollars today) |

| Sell-Buy Swap | RBI sells USD now, agrees to buy later | Absorbs rupee liquidity (RBI receives rupees by selling dollars today) |

These are particularly useful when liquidity conditions are affected by RBI's forex market interventions (e.g., defending the rupee by selling dollars drains rupee liquidity, so a Buy-Sell swap can replenish it). Unlike OMOs, forex swaps are temporary — the transaction reverses at a future date, making them ideal for managing short-to-medium-term liquidity mismatches.

5. Long Term Repo Operations (LTRO)

While the standard LAF repo is typically overnight or 14 days, sometimes the banking system needs longer-term liquidity assurance. The Long Term Repo Operations (LTRO) address this need:

- RBI conducts repos of 1-year to 3-year tenor at the prevailing Repo Rate. This is significant — banks get long-term funds at the same rate as overnight borrowing, making it a very attractive deal.

- Injects durable liquidity at a lower cost for banks compared to overnight borrowing. This encourages banks to lend more aggressively for longer tenors, boosting credit growth.

- TLTRO (Targeted LTRO): A special variant where banks must deploy the borrowed funds in specific sectors (e.g., corporate bonds, commercial paper, NBFCs). This combines quantitative easing with sectoral targeting — the RBI gives cheap money but dictates where it must go.

NOTE

LTRO was first introduced by RBI in February 2020 during the COVID-19 economic crisis to ensure banks had access to cheap, long-term funds. TLTRO was used specifically to channel funds to stressed sectors like NBFCs and MSMEs.

B. Qualitative Instruments (Selective Credit Control)

While quantitative instruments control the total volume of money in the economy (like adjusting the overall water pressure in a pipe), qualitative instruments control where the money goes (like directing the water to specific taps). These tools target specific sectors or activities to either encourage or discourage lending in those areas. They are also called selective credit control measures.

1. Margin Requirements

Margin is the borrower's own contribution when taking a loan against an asset. RBI prescribes the minimum margin for loans against specific assets to control speculative borrowing:

- Higher margin → borrower must contribute more → less loan available → discourages speculative borrowing

- Lower margin → borrower contributes less → more loan available → encourages borrowing

- Commonly used for loans against commodities, shares, and gold

Example: How Margin Requirements Work

If RBI sets a **40% margin** on gold loans: - A borrower with gold worth **₹1,00,000** can only get a maximum loan of **₹60,000** (100% − 40% margin = 60%) - If RBI raises the margin to **60%**, the same borrower can only get **₹40,000** - This directly reduces speculative demand for gold-backed creditDuring commodity price bubbles, RBI raises margins on commodities to prevent traders from borrowing heavily to hoard essential goods.

2. Selective Credit Control (SCC)

Selective Credit Control (SCC) is a more direct and targeted intervention than margin requirements. Under SCC, RBI can issue specific directives to banks regarding lending against certain sensitive commodities:

- Minimum margins for lending against select commodities (food grains, oilseeds, cotton, sugar, etc.)

- Ceiling on maximum advances against specific commodities — the bank simply cannot lend beyond a certain amount, regardless of the borrower's creditworthiness

- Rate of interest to be charged on such advances — RBI can mandate a higher rate to make speculative borrowing expensive

- Primary purpose: to prevent hoarding and speculation in essential commodities that could lead to artificial price rises and hurt consumers

IMPORTANT

SCC powers are exercised under Sections 21 and 35A of the Banking Regulation Act, 1949. These give RBI the authority to issue binding directives to banks on lending policies.

3. Moral Suasion

Moral suasion is the gentlest tool in RBI's arsenal. It involves no legal mandate or binding regulation:

- RBI persuades, requests, or advises banks (without legally binding orders) to follow certain lending practices

- Example: RBI may request banks to restrict lending for speculative activities or to increase lending to priority sectors during an economic slowdown

- Works through RBI's authority, reputation, and influence rather than regulation — banks typically comply because maintaining a good relationship with the central bank is in their long-term interest

- Communicated through meetings, speeches, press conferences, and informal channels

TIP

Think of moral suasion as a "suggestion with weight." The RBI Governor's speech asking banks to pass on rate cuts to borrowers is moral suasion — not legally binding, but banks usually comply.

4. Direct Action

When moral suasion fails and banks refuse to comply with RBI's directives, RBI can escalate to direct action — the strictest qualitative measure:

- Refuse to rediscount bills of exchange of the non-compliant bank — cutting off a key source of short-term funding

- Charge penal interest rates on borrowings — making it expensive for the bank to operate

- Refuse lending facilities under LAF — effectively shutting the bank out of the daily liquidity window

- Cancel banking license in extreme cases (under Section 22 of BR Act) — the ultimate penalty, used only for severe violations

WARNING

Direct action is rare but powerful. Recent examples include RBI restricting certain banks from issuing new credit cards, imposing business restrictions on specific NBFCs, and even superseding the boards of troubled banks.

5. Credit Rationing

Credit rationing is a blunt but effective tool for controlling credit expansion:

- RBI sets a maximum limit on the total loans that banks can grant to any specific sector or borrower

- Controls excessive credit flow to specific sectors to prevent asset bubbles (e.g., excessive lending to real estate can inflate property prices dangerously)

- RBI can also prescribe the maximum loan amount per borrower for certain categories of loans

6. Priority Sector Lending (PSL)

Priority Sector Lending (PSL) is one of the most important qualitative tools because it mandates where a significant portion of bank credit must flow. RBI requires banks to lend a specified portion of their total credit to sectors that are considered vital for the economy but may not receive adequate credit otherwise:

| Bank Type | PSL Target (% of ANBC) |

|---|---|

| Domestic SCBs & Foreign Banks (≥20 branches) | 40% |

| Foreign Banks (<20 branches) | 40% |

Key priority sectors include: Agriculture (18% of ANBC), MSMEs, Education, Housing, Social Infrastructure, Renewable Energy, and Export Credit.

NOTE

What is ANBC? ANBC (Adjusted Net Bank Credit) is the base figure used to calculate PSL targets. It equals Net Bank Credit plus certain investments but excludes specific items like inter-bank participations. Banks that fail to meet PSL targets must deposit the shortfall amount with NABARD/NHB/SIDBI at lower interest rates — this acts as an implicit penalty.

Summary: Quantitative vs Qualitative Instruments

| Feature | Quantitative | Qualitative |

|---|---|---|

| Target | Overall money supply & credit | Specific sectors/activities |

| Tools | LAF, OMO, CRR, SLR, MSS, Forex Swaps, LTRO | Margin, SCC, Moral Suasion, Direct Action, PSL |

| Nature | Indirect, market-based | Direct, administrative |

| Scope | Economy-wide | Sector-specific |

| Effect | Changes cost/volume of money for everyone | Channels credit to/away from specific areas |

RBI Directions on CRR and SLR 2025

Consequent upon the Banking Laws (Amendment) Act 2025, RBI issued consolidated Master Directions. These updated rules tighten reporting and compliance structures for the Indian banking system.

1. Cash Reserve Ratio (CRR)

The Cash Reserve Ratio represents the exact percentage of total bank deposits that commercial banks must park strictly as cash with the RBI. It prevents over-lending and safeguards depositors' money.

- Legal Provision: Section 42(1) of RBI Act, 1934 (Scheduled Banks). This foundational law grants the RBI the ultimate authority to command these cash reserves.

- Rate: Specified by RBI. No floor (minimum) and No ceiling (maximum) as per provisions of Section 42 of RBI Act. The RBI maintains immense flexibility and can effectively drop the CRR to 0% or raise it indefinitely based on real-time economic emergencies.

- Wait Period (Lag): Banks maintain CRR based on NDTL of the Second Preceding Fortnight. Instead of calculating on today's deposits dynamically, banks look at their deposit base as it was logically positioned one month (two fortnights) ago, giving them proper time to prepare cash reserves accurately.

- Daily Maintenance: Minimum CRR balance on a daily basis cannot be less than 90% of the average fortnightly balance required. Even on days with massive cash withdrawals by customers, a Scheduled Commercial Bank (SCB) cannot allow its CRR parked with the RBI to drop below this strict 90% threshold.

- Interest: RBI pays Zero Interest on CRR balances. This is a crucial point—banks earn absolutely nothing on the massive funds locked up as CRR, meaning an increase in CRR actively hurts a bank's profitability and lending capacity.

- Current CRR is 3%.

Calculation of Demand & Time Liabilities (Savings Deposits)

For calculating both CRR and SLR properly, a standard Savings Bank deposit account needs to be mathematically split because customers use them as both long-term savings and short-term spending tools:

- Time Liability (Stable): Average of Minimum Monthly Balances (Fixed ratio calculated Half-Yearly). This logically represents the core, unmoving cash that customers rarely withdraw, acting like a fixed deposit.

- Demand Liability (Volatile): Average Actual Balance minus Time Liability. This mathematically captures the fluctuating funds that customers withdraw and deposit regularly for their daily needs.

Important Reporting Rules (New 2025)

The 2025 amendment fundamentally simplified how and when banks report their status.

- Reporting Fortnight: Now aligned with calendar month. This provides cleaner accounting periods compared to older, rolling fortnights:

- 1st Fortnight: 1st to 15th of the month.

- 2nd Fortnight: 16th to Last Day of the month.

- CRR Reporting Form: Form A — submitted fortnightly (within 5 days of fortnight end). No Provisional/Special returns—only one Final Form A. The RBI has strictly removed provisional reporting to cut down on paperwork. Banks simply submit their finalized data right away.

Penalties for Default

Failing to meet exactly the CRR mandate is considered a critical error. The RBI enforces strict monetary disciplines:

- Shortfall: If a bank fails to keep the mandated cash reserves:

- Day 1: Bank Rate + 3%. A heavy penal interest is immediately charged to the bank.

- Subsequent Days: Bank Rate + 5%. The penalty steepens significantly for every day the bank remains in default.

- Officer Penalty: Fine up to ₹7,500 + ₹500/day for persistent default. In severe cases, the individual executives responsible for bank compliance are personally fined as well.

- Impact of Change: Reduction in CRR increases bank liquidity (more funds available to lend), while an increase decreases liquidity.

Example: If a bank's and the , the required average fortnightly balance to maintain with RBI is .

2. Statutory Liquidity Ratio (SLR)

Unlike CRR which is purely locked cash, Statutory Liquidity Ratio (SLR) allows a bank to earn some interest. SLR is maintained as specified liquid assets — Cash, Gold, or Unencumbered Approved Securities. It is the mandatory percentage of deposits that banks must invest in highly safe, easily sellable liquid assets.

- Legal Provision: Section 24 of Banking Regulation Act, 1949. Note that this is governed by the BR Act (which regulates banking operations), unlike CRR which falls directly under the RBI Act (Section 42(1)).

- Rate: RBI can fix up to 40% (maximum) of NDTL, with no minimum limit. The 40% ceiling legally prevents the RBI from forcing a bank to invest all of its money into government holding schemes, leaving sufficient room for actual customer credit.

- Current SLR is 18%.

- Eligible Assets: To fulfill the SLR mandate, banks can hold onto:

- Cash balances.

- Balances with other banks and excess CRR balance with RBI.

- Investment in Gold/Gold Bonds (subject to conditions).

- Unencumbered Approved Securities (Govt Bonds, T-Bills, State Dev Loans, including purchase under LAF). "Unencumbered" is the key word here: the bank must actually own these securities outright, and they cannot be pledged elsewhere as collateral for other loans.

- Default in maintaining SLR: Interest payment penalty structure is the same as in CRR (Bank Rate + 3% for day 1, Bank Rate + 5% for subsequent days).

- SLR Reporting: Form VIII — submitted electronically on CIMS portal by 20th of every month.

- Impact of change: Reduction in SLR frees up funds from mandatory investment, which can then be used for core lending purposes (and vice versa).

Summary Cheat Sheet: CRR vs SLR

Here is a quick comparison to master the nuances between the two primary liquidity tools:

| Feature | CRR | SLR |

|---|---|---|

| Current Rate | 3.00% | 18.00% |

| Maintained With | RBI (Cash) | Self (Cash/Gold/Securities) |

| Legal Section | Sec 42(1) RBI Act | Sec 24 BR Act |

| Reporting Value | Total Investments (Inc. Encumbered) | Only Unencumbered Securities |

| Reporting Form | Form A (Fortnightly) | Form VIII (Monthly) |

| Wait Period | Lag of 1 Fortnight | Lag of 1 Fortnight |

Net Demand and Time Liabilities (NDTL)

Net Demand and Time Liabilities (NDTL) is effectively the total net deposits held by a bank. NDTL includes liabilities towards the banking system and others (Deposits, Borrowings). Since banks use the NDTL as the base number to calculate how much CRR and SLR they must maintain, getting this calculation right is strictly monitored.

Exempted from NDTL Calculation:

Certain funds are securely excluded so that banks are not unfairly penalized on cash they hold for structural or promotional reasons:

- Paid-up Capital, Reserves, Refinance from RBI/NABARD. These represent the bank's own core capital and official support funds, not public deposits.

- Inter-bank term deposits up to 1 year maturity. When banks lend to each other short-term, this liquidity runs within the system safely without adding systemic risk.

- Credit balance in ACU accounts. Accounts dealing with the specific Asian Clearing Union are given a pass.

- Incentivised Credit: Incremental Auto/Home/MSME loans (Feb-July 2020) exempted for 5 years. This was a special relief measure to aggressively promote lending during a tough economic phase by exempting the matching deposits from reserve cuts.

Liabilities Excluded from CRR:

Additionally, some assets do not require CRR cash buffering:

- Liabilities to the banking system. What a bank owes another bank is generally protected by separate systemic regulations.

- DTL of Offshore Banking Units (OBUs). International banking branches face different regulatory standards and thus are excluded from domestic CRR equations.

- Credit balance in ACU account.

- Inter-bank term deposit up to 1 year maturity.

- Incremental Auto & Home, MSME Loans given wef 14.2.20 to 31.7.20, exempted for 5 years.

- New MSME borrowers who did not avail any loan till 1.1.2021, shall be excluded for loans up Rs.25 lac disbursed till 31.12.21, for 1 year.

Liabilities exempted from provisions of both CRR & SLR: Paid-up Capital & Reserves, Borrowing/Refinance from RBI/NABARD/NHB, Inter-bank term deposits (up to 1 year maturity), and Liabilities to the banking system.

References

11 sources • [1] [2] [3] [4] [5] [6] [7] [8] [9] [10] [11]

References

RBI — Monetary Policy Framework

OfficialUsed for: Official RBI page explaining the monetary policy framework, MPC composition, and inflation targeting mandate

Used for: Overview of LAF operations including repo, reverse repo, SDF, and MSF

Used for: Consolidated master directions on reserve requirements issued under the Banking Laws (Amendment) Act 2025

Used for: Coverage of RBI's December 2025 liquidity injection measures

Used for: Comprehensive analysis of current key rates and MPC decisions as of 2026

Used for: Classification and explanation of quantitative and qualitative monetary policy instruments

Used for: Press Information Bureau release on MPC decisions from April 2025 — 25 bps cut to 6.00%

Used for: Official RBI page with monetary policy statements, resolutions, and MPC minutes

Used for: Primary source for the June 5, 2026 FAR expansion, FPI rule relaxations, PROI limits, and G-Sec tax exemptions

Used for: Used for the June 2026 policy outcome, FY27 growth forecast of 6.6%, and FY27 inflation forecast of 5.1%

Used for: Secondary confirmation that the RBI held the repo rate at 5.25% and retained the neutral stance on June 5, 2026

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Monetary and Credit Policy | RBI tool to manage money supply and interest rates. Announced annually (April) and reviewed bi-monthly (6 times a year). |

| Expansionary vs Contractionary Policy | Expansionary: Reduces rates to increase liquidity (low growth). Contractionary: Increases rates to suck out liquidity (high inflation). |

| Monetary Policy Committee (MPC) | 6-member body (3 RBI + 3 Govt) that controls policy rates. Meets at least 6 times a year. RBI Governor has the casting vote. |

| Inflation Target | Aimed at 4% with a flexible tolerance of (+/-) 2%. |

| Current Rates (Jun 5, 2026) | Repo: 5.25%, SDF: 5.00%, MSF: 5.50%, Bank Rate: 5.50%, CRR: 3.00%, SLR: 18.00%. Stance: Neutral. Governor: Sanjay Malhotra. |

| June 2026 policy message | Rate unchanged, stance neutral, but FY27 forecast updated to GDP 6.6% and CPI inflation 5.1% because of elevated external risks. |

| June 2026 market measures | FAR expanded to new 15/30/40-year G-Secs and SGrBs; FPI G-Sec restrictions eased; tax exemption on FPI G-Sec interest/capital gains from April 1, 2026; PROI equity limit raised to 10% per investor and 24% overall. |

| Policy Rates: The Corridor | Repo Rate (Key lending rate), SDF (Repo − 0.25%, Floor, collateral-free), MSF (Repo + 0.25%, Ceiling, emergency borrowing). |

| Bank Rate | Repo + 0.25%. Used for long-term lending and penal charges. |

| 2025-26 Easing Cycle | Total 125 bps cut (6.50% → 5.25%): Feb 2025 (−25), Apr 2025 (−25), Jun 2025 (−50 + CRR cut 100 bps), Dec 2025 (−25). Paused Feb & Apr 2026. |

| LAF (Liquidity Adjustment Facility) | RBI's primary framework for day-to-day liquidity management. Corridor: SDF (floor) → Repo (middle) → MSF (ceiling). 14-day variable rate repo is the main tool. |

| OMO (Open Market Operations) | Outright buy/sell of govt securities for durable liquidity. Buy = inject liquidity, Sell = absorb liquidity. |

| MSS (Market Stabilisation Scheme) | Special short-term securities to absorb large-scale excess liquidity (e.g., from forex inflows). Proceeds held separately, not for govt spending. |

| Forex Swaps | USD/INR Buy-Sell swap injects rupee liquidity; Sell-Buy absorbs it. |

| Qualitative Tools | Margin requirements, Selective Credit Control, Moral Suasion, Direct Action, Credit Rationing, Priority Sector Lending (40% of ANBC for SCBs). |

| Reserve Ratios | Impact liquidity. Include CRR (Cash Reserve Ratio) and SLR (Statutory Liquidity Ratio). |

| Cash Reserve Ratio (CRR) | Percentage of deposits (NDTL) kept strictly as cash with RBI (Sec 42(1) RBI Act). RBI pays Zero Interest. |

| CRR Limits and Maintenance | There is No Minimum, No Maximum rate limit (Floor/Ceiling removed). Banks must maintain a daily balance of at least 90% of required CRR. Calculated with a lag of Second Preceding Fortnight. |

| CRR Reporting Fortnights | The New Reporting Fortnights align with the calendar month: 1st-15th and 16th-End of Month. Submitted via Form A (Fortnightly). |

| Statutory Liquidity Ratio (SLR) | Percentage of deposits kept in self-maintained safe assets: Cash, Gold, or Unencumbered Approved Securities (Sec 24 BR Act). |

| SLR Limits and Reporting | The Max SLR can be legally set up to 40% of NDTL. Banks report this using Form VIII (Monthly, by 20th) on the CIMS portal. |

| NDTL (Net Demand & Time Liabilities) | The base deposit figure used to calculate CRR and SLR. Savings deposits are split into Time (Stable) and Demand (Volatile) liabilities. |

| NDTL Exemptions | Capital, reserves, inter-bank term deposits (up to 1 year), and RBI/NABARD refinance are excluded from NDTL calculations. |

Lesson Doubts

Ask questions, get expert answers