🛂 Banking Supervision & Operations

RBI Supervision, CAMELS rating, Insurance Business by Banks, and Dividend Payment Rules.

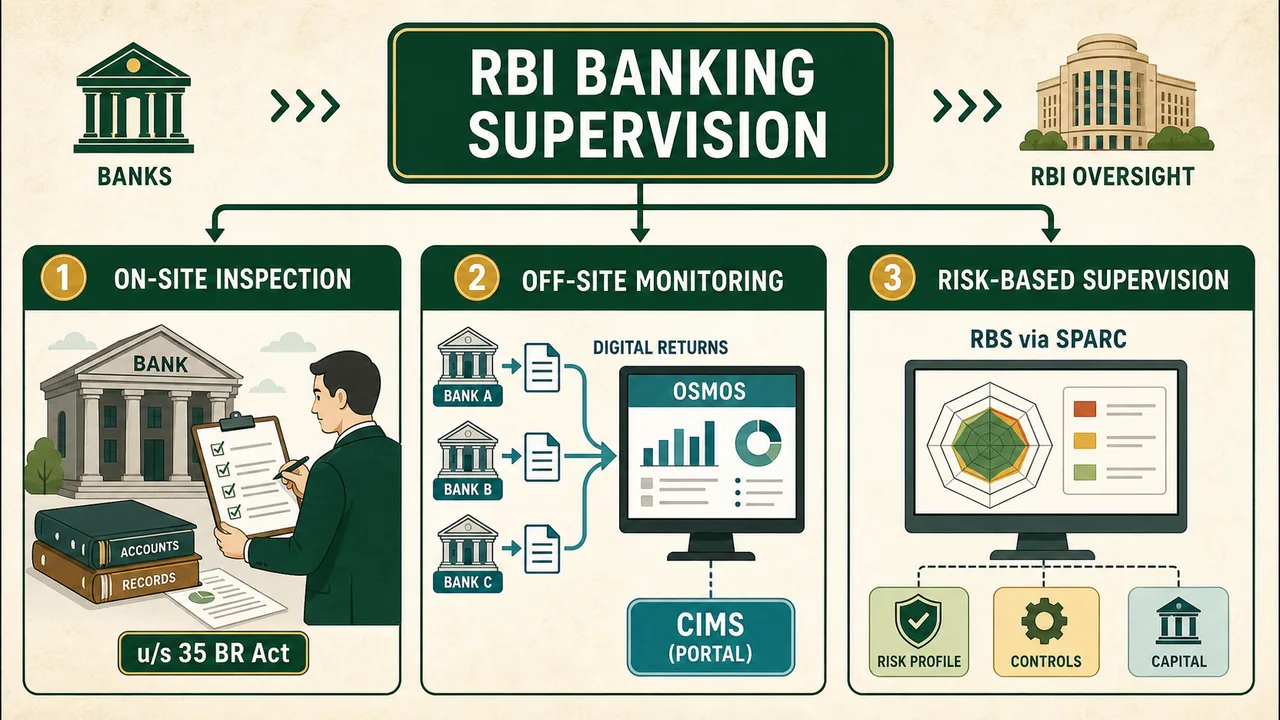

Banking Supervision

- Conducted by: RBI’s Department of Banking Supervision (DBS), primarily through Annual Financial Inspection (AFI).

- Objective: To ensure financial stability, protect depositors' interest, and ensure solvency of banks.

- Types:

- On-site supervision: Physical inspection of books and accounts u/s 35 of B R Act, 1949.

- Off-site supervision (OSMOS): Monitoring through periodic returns submitted by banks.

- OSMOS: Off-site Monitoring and Surveillance System.

- DSB Returns: Banks submit different returns/reports covering capital, assets, earnings, and liquidity. Currently these submissions are done through the new Centralized Information Management System (CIMS) portal.

- Risk Based Supervision (RBS): Implemented w.e.f. 1.4.2013.

- Concept: Using the SPARC (Supervisory Program for Assessment of Risk and Capital) framework. It shifts focus from inspecting individual transactions to evaluating the bank's Risk Management Systems and processes.

Rating of Banks

RBI rates banks annually using specific models to assess their health:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Banking Supervision

- Conducted by: RBI’s Department of Banking Supervision (DBS), primarily through Annual Financial Inspection (AFI).

- Objective: To ensure financial stability, protect depositors' interest, and ensure solvency of banks.

- Types:

- On-site supervision: Physical inspection of books and accounts u/s 35 of B R Act, 1949.

- Off-site supervision (OSMOS): Monitoring through periodic returns submitted by banks.

- OSMOS: Off-site Monitoring and Surveillance System.

- DSB Returns: Banks submit different returns/reports covering capital, assets, earnings, and liquidity. Currently these submissions are done through the new Centralized Information Management System (CIMS) portal.

- Risk Based Supervision (RBS): Implemented w.e.f. 1.4.2013.

- Concept: Using the SPARC (Supervisory Program for Assessment of Risk and Capital) framework. It shifts focus from inspecting individual transactions to evaluating the bank's Risk Management Systems and processes.

Rating of Banks

RBI rates banks annually using specific models to assess their health:

1. Domestic Banks (CAMELS Model)

Used for Indian Public and Private sector banks.

- C - Capital Adequacy: Does the bank have enough capital to absorb losses? (CRAR).

- A - Asset Quality: Quality of loans (Level of NPAs).

- M - Management Effectiveness: Quality of governance, board oversight, and strategic direction.

- E - Earning Quality: Profitability and sustainability of income (ROA, NIM).

- L - Liquidity Management: Ability to meet short-term obligations (ALM).

- S - Systems and Controls: Robustness of internal audits, IT security, and compliance.

2. Foreign Banks (CALCS Model)

Used for foreign bank branches in India (since they don't have a full domestic board).

- C - Capital Adequacy

- A - Asset Quality

- L - Liquidity

- C - Compliance: Adherence to RBI regulations (replaces Management since governance is overseas).

- S - Systems: Internal controls and systems.

Foreign Investment Limits in Indian Banks

1. Public Sector Banks (PSBs)

- FDI Limit: 20% of paid up capital.

- FII Limit: 20% of paid up capital. (Short term basis on stock market)

- Total Cap: 20% (Composite limit of FII + FDI).

2. Private Sector Banks

- FDI Limit: 74%

- Automatic Route: Up to 49%

- Approval Route: Beyond 49% and up to 74%

- FII Limit: 49% (Aggregate limit).

- Total Cap: 74% (Composite limit of FDI + FII).

- FII beyond 24%: FII beyond 24% requires shareholders' approval.

3. Individual Investment Limits

- Individual FII: Max 10%.

- Individual NRI: Max 5% (repatriable) + 5% (non-repatriable).

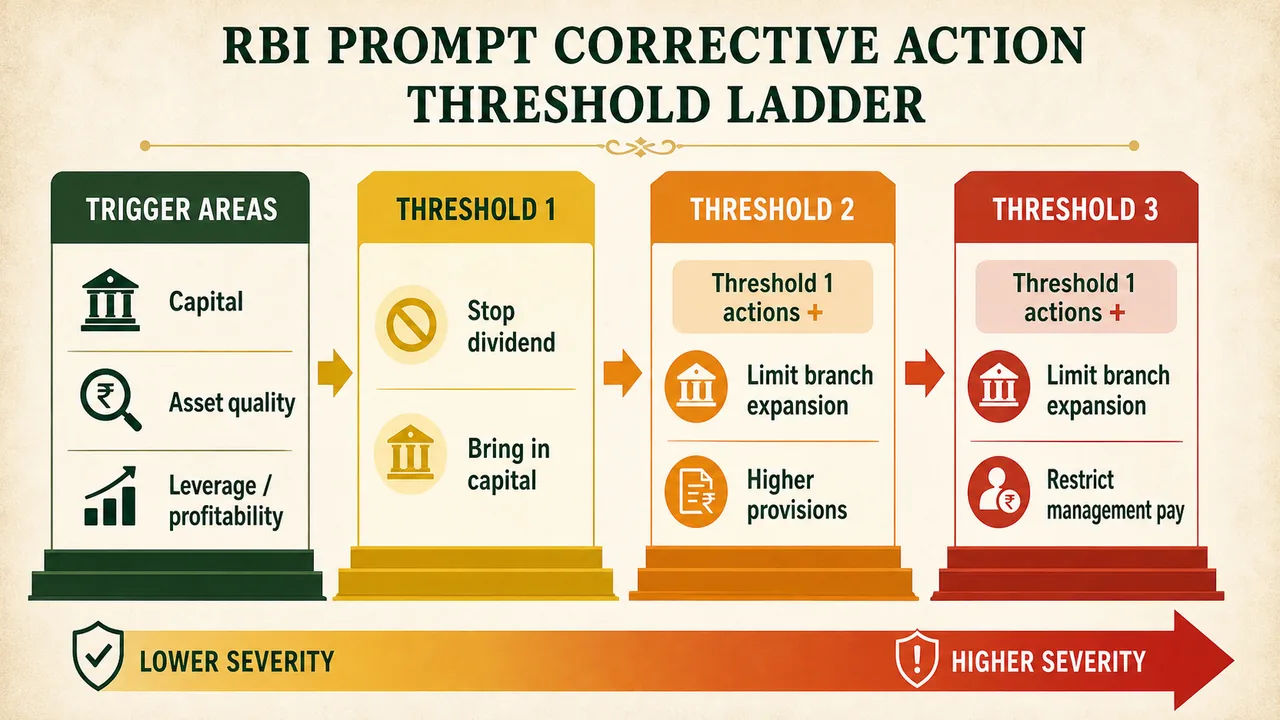

Prompt Corrective Action (PCA)

- The Prompt Corrective Action (PCA) framework is a supervisory tool used by the Reserve Bank of India (RBI) to intervene early in the operations of banks and Non-Banking Financial Companies (NBFCs) that show signs of financial distress.

- Its primary objective is to restore the financial health of weak institutions by imposing mandatory and discretionary restrictions, thereby protecting depositors' interests and maintaining the stability of the overall financial system

- PCA is an RBI framework to initiate structured actions in respect of banks, that show signs of weakness in respect of 3 important areas called Triggers.

- 1. Capital Adequacy: Measured by the Capital to Risk-Weighted Assets Ratio (CRAR) and Common Equity Tier 1 (CET1) ratio.

- 2. Asset Quality: Measured by the Net Non-Performing Assets (NNPA) ratio.

- 3. Profitability/Leverage: Measured by Return on Assets (RoA) (for banks before 2021) and the Tier 1 Leverage Ratio.

- Purpose: Improve financial health of banks.

- PCA applies on all banks in India.

- The type of action is based on degree of the damage, a bank has already suffered.

- A bank is placed under PCA based on (1) Audited Annual Financial Results and (2) Supervisory Assessment of RBI.

- PCA was introduced during 2004 revised in 2017 and then on 02.03.2019.

Risk Thresholds & Mandatory Actions

| Parameter | Risk Threshold 1 | Risk Threshold 2 | Risk Threshold 3 |

|---|---|---|---|

| Min CRAR + CCB | Up to 250 bps (2.5%) below prescribed | > 250 to 400 bps below | > 400 bps below |

| CET-1 + CCB | Up to 162.5 bps below | > 162.5 to 312.5 bps below | > 312.5 bps below |

| Net NPA Ratio | >= 6.0% but < 9.0% | >= 9.0% but < 12.0% | >= 12.0% |

| Tier-1 Leverage Ratio | Up to 50 bps below regulatory min | > 50 to 100 bps below | > 100 bps below |

Mandatory Actions:

- Threshold 1:

- Restriction on dividend distribution/profit remittance.

- Promoters/owners/parent in the case of foreign banks to bring in capital.

- Threshold 2: In addition to T1

- Restriction on Branch Expansion.

- Higher provisions as part of coverage regime

- Threshold 3: In addition to T1

- Restriction on Branch Expansion.

- Restriction on Management Compensation/Directors' fees.

Discretionary Actions:

In addition to mandatory restrictions, the RBI may exercise discretion to initiate several corrective steps to stabilize the institution:

- Special Supervisory Interactions: RBI may conduct frequent special inspections, targeted reviews, and regular meetings with the bank's Board.

- Strategy Related: A comprehensive review of the bank's business model, including restrictions on entering new lines of business or expanding existing ones.

- Governance Related: The RBI may remove managerial personnel, appoint observers to the Board, or supersede the Board entirely.

- Capital Related: Imposing restrictions on capital expenditure (except for technological upgrades) and requiring the bank to raise fresh capital or sell non-core assets.

- Credit Risk Related: Setting lower exposure limits for individuals and groups, and restricting lending to specific high-risk sectors.

- HR Related: Restrictions on staff recruitment, freezing of performance-linked bonuses, and limits on staff compensation.

- Profitability Related: Measures to reduce operating expenses and improve the cost-to-income ratio.

- Operations Related: Restrictions on high-cost deposits, inter-bank borrowings, and expansion into new geographical areas.

- Others: Any other action deemed fit by the RBI, such as recommending the bank for amalgamation, reconstruction, or winding up.

Insurance Business By Banks

- Recommendations: RN Malhotra Committee.

- Regulation: IRDAI (regulatory authority) license required.

- RBI Permission:

- Not required for bancassurance business.

- Required for underwriting business and broking business.

Types of Business

- Bancassurance business: It relates to selling 3rd party products. Hence without risk (only operational risk).

- Underwriting and Broking business: It is with risk. This involves the bank taking on financial liability for insurance claims (underwriting) or professional liability as an intermediary (broking).

Conditions for RBI Permission

| Condition | Underwriting Business | Broking Business |

|---|---|---|

| Min Net Worth | Rs. 1000 cr | Rs. 500 cr |

| Track Record | 3 year profit record | 3 year profit record |

| Net NPAs | Max 3% | Max 3% |

| CAR | Min 10% | Min 10% |

| Subsidiary | Through subsidiary (Bank investment max 50%) | - |

Dividend Payment Rules

As per RBI directions (28.11.2025), banks can pay dividend without RBI permission only if following conditions are satisfied:

- CRAR is min 9% for previous 2 years and the year for which dividend is to be paid. (means for total 3 years CRAR should be min 9%)

- Net NPA< 7%

- If a bank does not meet above norm, but has CRAR of at least 9% for current financial year for which it proposes to declare dividend, it shall be eligible to declare dividend provided its NNPA ratio is less than 5%;

- Dividend Payout Ratio (DPR): Max 40% as per Matrix.

- DPR = Total dividend / Net profit after tax and provisions.

- Max Permissible Dividend Payout Ratio Matrix:

| Category | CRAR Requirement | Net NPA = 0 | NNPA > 0 to < 3% | NNPA 3-5% | NNPA 5-7% |

|---|---|---|---|---|---|

| A | 11% or more (last 3 yrs) | Up to 40 | Up to 35 | Up to 25 | Up to 15 |

| B | 10% or more (last 3 yrs) | Up to 35 | Up to 30 | Up to 20 | Up to 10 |

| C | 9% or more (last 3 yrs) | Up to 30 | Up to 25 | Up to 15 | Up to 5 |

| D | 9% or more (current yr) | Up to 10 | Up to 5 | NIL | NIL |

Summary Cheat Sheet

| Topic | Key Points |

|---|---|

| Supervision Model | RBS (Risk Based Supervision) uses SPARC framework to check Systems & Controls. |

| Ratings | Domestic: CAMELS (C, A, M, E, L, S); Foreign: CALCS (C, A, L, Compliance, Systems). |

| PCA Triggers | 1. CRAR/CET-1 + CCE, 2. Net NPA, 3. Tier-1 Leverage. (3 Thresholds of severity). |

| PCA Actions | Threshold 1: Div Restriction. Threshold 2: Branch Restriction. Threshold 3: Mgmt/Comp Restriction. |

| FDI Limits | PSB: 20% (Govt Route). Private: 74% (Auto < 49%, App > 49%). FII: Agg 49%. |

| Insurance Biz | Comm: RN Malhotra. Bancassurance: No Risk (Agent). Underwriting: Risk (Subsidiary). |

| Ins. Eligibility | Underwriting: Net Worth ₹1000 Cr, NPA < 3%. Broking: Net Worth ₹500 Cr. |

| Dividend Rules | Eligible if CRAR > 9% (Last 3 yrs) & Net NPA < 7%. Max Payout Ratio: 40%. |

Lesson Doubts

Ask questions, get expert answers