💸 Consumer Protection

RBI Ombudsman Scheme (BOS) -> Integrated Ombudsman Scheme (RB-IOS)

Banking Ombudsman Scheme 2021

The Integrated Ombudsman Scheme, 2021 streamlines the grievance redressal process for customers of banks, NBFCs, and non-bank payment system participants. It adopts a "One Nation One Ombudsman" approach, making the mechanism neutral to the jurisdiction and liability of the regulated entity.

Legal Framework & Applicability

The RBI notified this scheme under:

- Section 35A of the Banking Regulation Act, 1949

- Section 45L of the RBI Act, 1934

- Section 18 of the Payment and Settlement Systems Act, 2007

Effective Date: It came into effect w.e.f. 12.11.2021.

Repealed Schemes

This new integrated scheme repealed and replaced the three previous distinct schemes:

- Banking Ombudsman Scheme, 2006

- Ombudsman Scheme for NBFCs, 2018

- Ombudsman Scheme for Digital Transactions, 2019

Organizational Structure

Appointment and Tenure

The RBI may appoint its officers as Ombudsman and Deputy Ombudsman.

- Tenure: Appointed for a period not exceeding 3 years at a time.

Centralised Receipt and Processing Centre (CRPC)

To streamline operations, RBI established the CRPC at the RBI Regional Office, Chandigarh.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Banking Ombudsman Scheme 2021

The Integrated Ombudsman Scheme, 2021 streamlines the grievance redressal process for customers of banks, NBFCs, and non-bank payment system participants. It adopts a "One Nation One Ombudsman" approach, making the mechanism neutral to the jurisdiction and liability of the regulated entity.

Legal Framework & Applicability

The RBI notified this scheme under:

- Section 35A of the Banking Regulation Act, 1949

- Section 45L of the RBI Act, 1934

- Section 18 of the Payment and Settlement Systems Act, 2007

Effective Date: It came into effect w.e.f. 12.11.2021.

Repealed Schemes

This new integrated scheme repealed and replaced the three previous distinct schemes:

- Banking Ombudsman Scheme, 2006

- Ombudsman Scheme for NBFCs, 2018

- Ombudsman Scheme for Digital Transactions, 2019

Organizational Structure

Appointment and Tenure

The RBI may appoint its officers as Ombudsman and Deputy Ombudsman.

- Tenure: Appointed for a period not exceeding 3 years at a time.

Centralised Receipt and Processing Centre (CRPC)

To streamline operations, RBI established the CRPC at the RBI Regional Office, Chandigarh.

- Function: To receive physical (paper) complaints from across the country.

- Email Complaints: Can be sent through the portal https://cms.rbi.org.in.

- Cost: The entire cost of the scheme is borne by the RBI.

Powers and Functions

The Ombudsman considers complaints of customers against Regulated Entities (REs). REs serve as the umbrella term for Banks, NBFCs, and System Participants (Digital Wallets/PPIs(Payment Infrastructure Providers)).

Compensation Limits

There is no limit on the amount involved in a dispute that can be referred to the Ombudsman. However, there are caps on the financial awards the Ombudsman can pass:

- Compensation for Loss: Up to ₹20 Lakh (for actual pecuniary loss).

- Compensation for Harassment: Additional up to ₹1 Lakh for loss of complainant’s time, expenses incurred, and harassment/mental anguish suffered.

Filing a Complaint

Grounds of Complaint

A customer aggrieved by an act or omission of an RE resulting in a deficiency in service can file a complaint.

- Definition: Deficiency includes any shortcoming or inadequacy in financial service, which may or may not result in financial loss.

- Representation: The complaint can be filed personally or through an authorized representative.

- Restriction: It cannot be filed through an Advocate.

Procedure for Filing

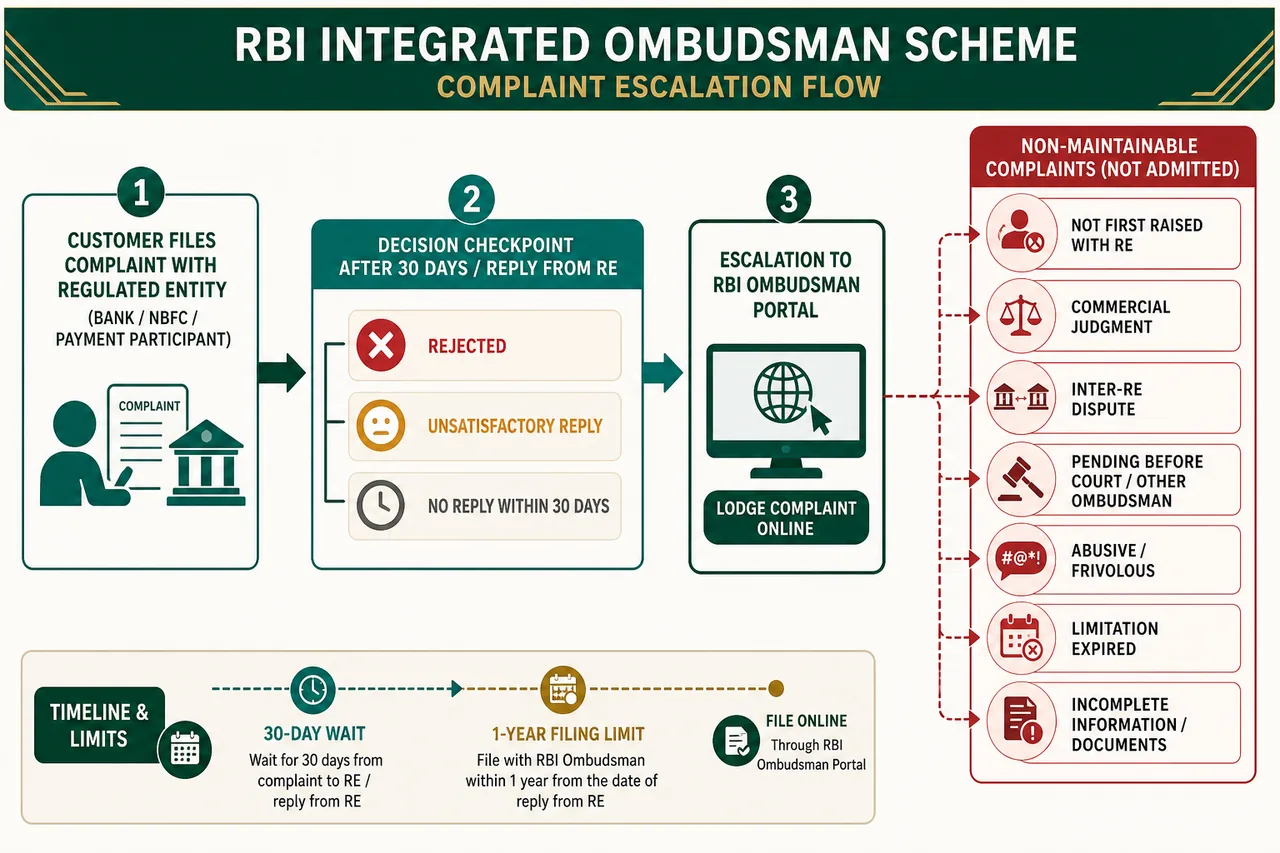

- First Step (Complaint to RE): The complaint must first be made to the Regulated Entity (Bank/NBFC).

- Escalation Condition: You can approach the Ombudsman only if:

- The complaint was rejected by the RE.

- OR the complainant is not satisfied with the reply.

- OR the complainant received no reply within 30 days after the RE received the complaint.

- Limitation: The complaint to the Ombudsman must be made within 1 year after the rejection/reply from the RE (or 1 year + 30 days if no reply).

Grounds for Non-Maintainability

Complaints are not allowed (non-maintainable) if they involve:

- Commercial Judgment: Disputes regarding commercial decisions of the bank (e.g., rejecting a loan based on credit score).

- Not Addressed Directly: Grievances not first addressed to the RE.

- General Grievances: Generic complaints against Management or executives.

- Inter-RE Disputes: Disputes between two banks/REs.

- Employee-Employer: Disputes involving the internal HR relationship of an RE.

- Pending/Settled Cases: Matters already pending before any Court/Ombudsman or already settled/dealt with by them.

- Abusive/Frivolous: Complaints that are vexatious in nature.

- Limitation Expired: Complaints made after the limitation period (as per Limitation Act 1963).

- Incomplete Info: If the complainant provides incomplete information.

Resolution Process

Power to Call for Information

The Ombudsman can seek information or certified documents from the RE.

- Timeline: The RE must file its written reply within 15 days.

- Ex-Parte Award: If the RE omits or fails to file a reply, the Ombudsman may proceed ex-parte to pass an Award. Crucially, the RE has no right of appeal against such an Award passed due to their non-response.

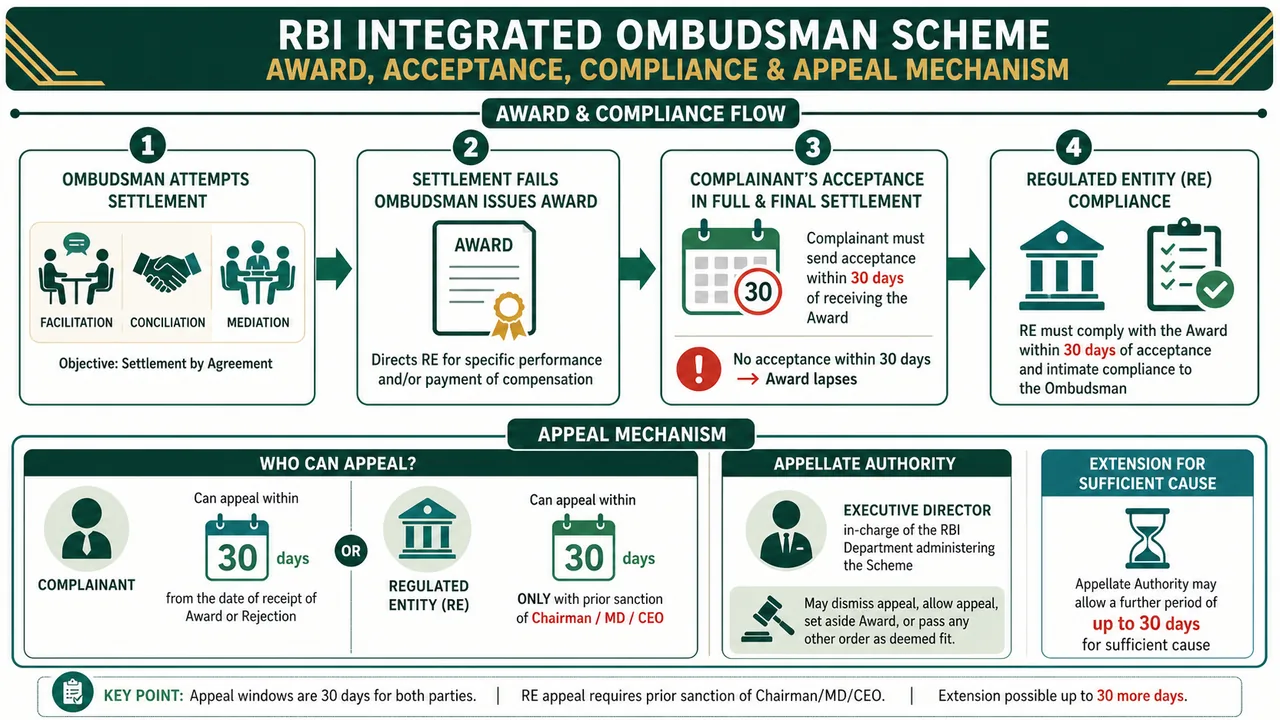

Mode of Resolution

The Ombudsman shall endeavour to promote settlement by agreement through:

- Facilitation

- Conciliation

- Mediation The proceedings shall be summary in nature (quick disposal without elaborate evidence procedures).

The Award

If settlement fails, the Ombudsman passes an Award.

- Scope: Directs the RE for specific performance of obligations and/or pay compensation.

- Lapse: The Award shall lapse if the Complainant does not furnish a letter of acceptance in full and final settlement to the RE within 30 days of receiving the copy of the Award.

- Compliance: Once accepted, the RE must comply with the Award and intimate compliance to the Ombudsman within 30 days of receiving the acceptance.

Appeal Mechanism

The Ombudsman may reject a complaint at any stage. If aggrieved by the decision or Award:

Appellate Authority

The Executive Director in-charge of the RBI Department administering the Scheme is the Appellate Authority.

Who Can Appeal?

- The Complainant: Can appeal within 30 days from date of receipt of Award/Rejection.

- The Regulated Entity (RE): Can appeal within 30 days, ONLY with the previous sanction of the Chairman, MD, or CEO of the RE. This ensures frivolous appeals by lower-level bank officials are curbed.

Extension: The Appellate Authority may allow a further period of up to 30 days if there is sufficient cause.

Powers: The Appellate Authority may dismiss the appeal, allow it, set aside the Award, or pass any other order as it deems fit.

Other Administrative Matters

Principal Nodal Officer (PNO)

Every RE shall appoint a Principal Nodal Officer (PNO) at their Head Office.

- Rank: Not less than the rank of a General Manager.

- Role: The PNO represents the RE and furnishes information to the Ombudsman.

- Display: The RE must prominently display the Name, Contact Details (Phone/Mobile/Email) of the PNO in all their branches.

IOS 2026: Key Changes

IMPORTANT

The RBI has notified the Integrated Ombudsman Scheme, 2026 (IOS 2026) which will replace RB-IOS 2021 from 1st July 2026. Complaints filed before this date will continue under the 2021 scheme.

Comparison: RB-IOS 2021 vs IOS 2026

| Parameter | RB-IOS 2021 | IOS 2026 (New) |

|---|---|---|

| Effective Date | 12th November 2021 | 1st July 2026 |

| Compensation for Loss | Up to ₹20 Lakh | Up to ₹30 Lakh |

| Compensation for Harassment | Up to ₹1 Lakh | Up to ₹3 Lakh |

| Time to File with Ombudsman | 1 Year from RE last response/expiry | 90 Days from RE last response/expiry |

| Definition of "Customer" | Account-based relationship | Any person engaging in financial service with RE |

| Scope of "Deficiency" | Financial services | All services provided by REs |

| Entities Covered | Banks, NBFCs, PPIs | + State Co-op Banks, DCCBs, CICs |

| Internal Ombudsman | Advisory role only | Compensation powers, direct access to complainants |

| Grievance Structure | Single-tier at RE | Two-tiered within RE before IO escalation |

| Annual Report | Not mandated | RBI must publish annual scheme report |

Key Enhancements in IOS 2026

- Widened Customer Definition: Covers any person engaging with an RE, not just account holders.

- Expanded Deficiency Scope: Now covers all services, not just financial services.

- Higher Compensation: ₹30L for loss (up from ₹20L) + ₹3L for harassment (up from ₹1L).

- Reduced Filing Timeline: Time limit to escalate to RBI Ombudsman reduced from 1 year to 90 days from the date of RE's last response or expiry of response period. Customers must act faster!

- Cooperative Banks Included: State Co-operative Banks and District Central Cooperative Banks (DCCBs) now covered.

- Strengthened Internal Ombudsman: IOs will have compensation-awarding powers and direct complainant access.

- Two-Tiered Grievance Structure: Under IOS 2026, REs must implement a two-level internal process before complaints reach the Internal Ombudsman. This means:

- Tier 1: Initial complaint handling at branch/customer service level.

- Tier 2: Escalation to a senior nodal officer or grievance cell.

- Then: If still unresolved, escalation to the Internal Ombudsman (who now has compensation powers).

- This ensures thorough internal resolution attempts before RBI Ombudsman involvement.

- Multilingual Access: Scheme details must be published on bank websites in multiple languages.

Consumer Protection Act 2019

Notified on: 09.08.19. Repealed: CPA-1986. Operative: w.e.f 20.7.20

Core Concepts

Consumer Definition

A Consumer is a person who buys goods or services for consideration or a person who uses goods or avails services with consent of a person, who purchased goods.

- Exclusion: Person who purchases for resale is not a consumer.

When complaint can be made?

Consumer can seek remedy when there is defect or deficiency.

Administration of CP Act

It is through 3 entities:

- Consumer Protection Councils (Advisory)

- Central Consumer Protection Authority (Regulator)

- Consumer Dispute Redressal Commissions (Courts)

CPA Administration - Redressal Commissions

| Feature | District Commission | State Commission | National Commission |

|---|---|---|---|

| Set-up by | State Govt. | State Govt. | Central Govt. |

| Claim amount | Up to Rs. 50 lac (Earlier Rs. 1 cr) |

> Rs. 50 lac up to Rs. 2 cr (Earlier max Rs. 10 cr) |

> Rs. 2 cr (Earlier > Rs. 10 cr) |

| Composed of | President + min 2 members | President + min 4 members | President + min 4 members |

| Age criteria | 65 Y | 65 Y | Max in years President: 70 Member: 67 |

| Eligibility & Term | Distt. Judge 4 Y |

HC Judge 4 Y |

SC Judge 5 years |

Cases related to Unfair Contracts

- State Commission can entertain cases against unfair contracts up to Rs. 10 cr.

- National Commission up to > Rs. 10 cr.

Procedure & Timelines

Important Time Lines

- Complaint filing: 2 years from date of cause of action.

- Admission of complaint by DC: 21 days (additional 45 days in case of testing or inspection).

- Decision on complaint: 3 months (5 months in case of testing or inspection).

- Appeal by parties: 45 days to State Commission (SC). 30 days to National Commission (NC) or Supreme Court.

- Decision on appeal: 90 days.

- Review of order by any commission: 30 days.

Filing Details

- Place to make complaint: Place of residence or business of opposite party or complainant or cause of action.

- Who can?: Consumer, recognized consumer association, one or more consumers, Govt.

- Procedure: Notice to opposite party within 21 days to submit reply within 30 days + extended 15 days.

Appeal Mechanisms

- Appeal against order: Can be made to State Commission. Appeal by liable party only after depositing 50% amount.

Mediation

- Settlement by mediation: If possibility by mediation exists, can give notice to parties to give consent within 5 days. If consent received, shall send consent within 5 days, to Consumer Mediation Cell.

Non-compliance of Order

- Penalty: Imprison min 1 month max 3 years. Fine min Rs. 25,000 max Rs. 1 lac.

Offences and Penalties

Regulatory Violations

- Non-compliance of direction of Central Authority: Imprisonment up to 6 months. Fine up to Rs. 20 lac.

- False or misleading advertisement: Imprisonment up to 2 years. Fine up to Rs. 10 lac. For every subsequent offence, imprisonment up to 5 years and fine up to Rs. 50 lac.

Product Liability (Adulterants)

Penalties for Sale, storing, distribution or imports of product containing an adulterant:

a) Does not result in any injury to consumer:

- Imprisonment up to 6 months.

- Fine up to Rs. 1 lac.

b) Causing injury not amounting to grievous hurt to the consumer:

- Imprisonment up to 1 year.

- Fine up to Rs. 3 lac.

c) Causing injury resulting in grievous hurt to the consumer:

- Imprisonment up to 7 years.

- Fine up to Rs. 5 lac.

d) Results in the death of a consumer:

- Imprisonment min 7 years (may extend to imprisonment for life).

- Fine min Rs. 10 lac.

Licence Cancellation

- In case of first conviction, licence issued to the person can be cancelled up to 2 years.

- In case of subsequent conviction, licence can be cancelled permanently.

Deposit Insurance and Credit Guarantee Corporation (DICGC)

- Subsidiary: Wholly owned subsidiary of RBI.

- Insurance Cover: Rs. 5,00,000 per depositor per bank (principal + interest). Enhanced from Rs. 1 lakh.

- Premium: Paid by banks (not depositors).

- Rate: Max 15 paise per Rs. 100 per annum. (Current 12 paise).

- Insured Banks: All commercial banks (including branches of foreign banks functioning in India, local area banks, RRBs), Co-operative Banks.

- Excluded Deposits:

- Inter-bank deposits.

- Deposits of foreign govts, Central/State Govt.

- Amount due on account of India and outside India.

CICs, CRAs, and Financial Benchmarks (FB)

| Credit Information Companies (CICs) | Credit Rating Agencies (CRAs) | Financial Benchmarks |

|---|---|---|

| 1. CIBIL TransUnion | 1. CRISIL | FBIL (Financial Benchmarks India Pvt Ltd) is an independent benchmark administrator promoted by FIMMDA (Fixed Income Money Market and Derivatives Association of India), FEDAI (FEDAI (Foreign Exchange Dealers' Association of India), IBA (Indian Bank Association) |

| 2. Experian CIC | 2. ICRA | |

| 3. Equifax CIC | 3. CARE | |

| 4. CRIF High Mark CIC | 4. Fitch Rating | |

| 5. Brickwork | ||

| 6. SMERA | ||

| 7. Infomerics Valuations and Rating |

Note: Recently RBI has removed Fitch CRA from the list of CRAs.

Customer Service in Banks

Customer service is the backbone of banking. Over the years, several high-level committees have shaped how banks treat their customers.

-

Committees: Two major committees laid the foundation for modern customer service standards:

- Talwar Committee: Focused on Customer Service and recommended the time norms for transactions.

- Goiporia Committee: Further refined these norms and introduced the concept of customer compensation for delays.

-

Mandatory Board-Approved Policies: Every bank must have specific policies approved by its Board of Directors to ensure fair treatment:

- Customer Compensation Policy: Defines how and when the bank will compensate a customer (e.g., for delayed credit of dividends or failed ATM transactions).

- Cheque Collection Policy: Sets the timeframe for clearing cheques and penalties for delays.

- Grievance Redressal Policy: Outlines the formal mechanism for solving customer complaints.

-

BCSBI (Banking Codes and Standards Board of India):

- This was an independent body set up to police the "Codes of Commitment".

- Status: It was Dissolved in 2021.

- Current Rule: Despite dissolution, the RBI has mandated that banks must continue to adhere to the "Code of Bank's Commitment to Customers". This Code spells out the minimum standards of banking practices banks are committed to follow.

-

Senior Citizens: Banks must provide special treatment to the elderly. This includes a separate counter or priority handling in the branch to minimize their waiting time.

-

Time Norms (Indicative): Banks are expected to complete transactions within reasonable limits. While these vary by bank, general guidelines are:

- SB Account Opening: Should take approximately 22-25 minutes.

- Demand Draft Issue: Should be completed within 10-15 minutes.

Right to Information (RTI) Act

The RTI Act is a powerful tool for transparency, empowering citizens to question public authorities.

-

Right to Citizens: The Act grants the Right to Information exclusively to Indian citizens (individuals). It allows them to request information from any "public authority" (government bodies and instrumentalities of the state).

- No Reason Needed: Crucially, the applicant is not required to give any reason for requesting the information or any other personal details except those necessary for contacting them.

-

Process & Fees:

- Public Information Officer (PIO): Every public authority appoints a PIO. This officer is responsible for receiving requests and providing the information.

- Fee: The application fee to seek information is nominal: Rs. 10 (typically via IPO, Draft, or Cash).

-

Time Limits for Response:

- General Rule: The PIO must provide the information within 30 days of receiving the request.

- Life and Liberty: If the information concerns the life or liberty of a person, it must be provided within just 48 hours.

-

Third Party Information:

- If a citizen asks for information that relates to a third party (someone other than the government or applicant), the PIO cannot just release it.

- Procedure: The PIO must give notice to the 3rd party within 5 days. The 3rd party is then given 10 days to make a representation (respond/object) before a decision is made.

-

Appeals Mechanism: If the information is denied or not provided in time, the citizen can appeal:

- 1st Appeal: Made to the senior authority (First Appellate Authority) within the department. Must be filed within 30 days of the decision/expiry of the deadline.

- 2nd Appeal: If still unsatisfied, a second appeal lies with the Central Information Commission (CIC). This must be filed within 90 days.

-

Penalties: To ensure officials take this seriously, there is a strict penalty for delay without reasonable cause. The fine is Rs. 250 per day of delay, up to a maximum of Rs. 25,000.

-

Record Preservation: Banks and public authorities typically preserve these records for 5-8 years depending on their internal retention policies.

Summary Cheat Sheet

| Feature | Details |

|---|---|

| Applicability | Banks, NBFCs, Digital Payment Participants. 12.11.2021. |

| Integrated Scheme | Repealed 2006 (Banks), 2018 (NBFCs), 2019 (Digital) schemes. |

| CRPC | Central Receipt & Processing Centre @ Chandigarh |

| Compensation Cap | ₹20 Lakh (Loss) + ₹1 Lakh (Harassment). |

| Timelines | 30 Days wait after complaining to Bank. 1 Year to approach Ombudsman. 15 Days for Bank to reply to Ombudsman. 30 Days to accept Award. 30 Days to Appeal. |

| Maintainability | Allowed: Deficiency in Service. Not Allowed: Commercial decisions, Court cases, Advocate representation. |

| Appellate Authority | Executive Director (RBI). |

| RE Appeal | Requires Sanction of Chairman/MD/CEO. |

Lesson Doubts

Ask questions, get expert answers