🏦 New Banking Models & Licensing

Universal Banking, TReDS, On-Tap Licensing, Payment Banks, and Small Finance Banks.

Universal Banking vs Narrow Banking

| Feature | Universal Banking | Narrow Banking |

|---|---|---|

| Committee | Khan Committee | Tarapore Committee |

| Operations | Banking operations by using all types of products i.e. low risk (CASA), medium risk (HL) and high risk (such as insurance, credit card, forex etc.) | Banking operations by using low risk products such as CASA deposits, term deposit and safe investments. |

On-Tap Policy on Licensing of New Private Banks

The Reserve Bank of India (RBI)'s "on-tap" licensing policy for new private sector banks allows eligible entities to apply for a banking license at any time, rather than waiting for specific, periodic application windows. This policy aims to foster increased competition and innovation in the banking sector.

Eligible Promoters ("Fit and Proper")

- Residents: Individuals/professionals with 10 years of experience in banking and finance.

- Private Sector Entities: Companies/Groups owned and controlled by residents with a successful track record of 10 years.

- NBFCs: Existing resident-controlled NBFCs with a 10-year track record.

- Excluded: Large industrial houses (where non-financial business > 40% of total assets/income) are not eligible to promote banks but can invest up to 10%.

Corporate Structure (NOFHC)

- Mandatory: If the promoter has other group companies ((e.g., Manufacturing, Real Estate), etc.), setting up a Non-Operative Financial Holding Company (NOFHC) is mandatory. This is to ring-fence (isolate) the bank from other group risks.

- Optional: If the promoter is an individual or a standalone entity with no other group companies, the NOFHC structure is optional (they can own the bank directly).

- Ownership: Promoter/Promoter Group must own at least 51% of the NOFHC.

💡 Concept: What is an NOFHC? A Non-Operative Financial Holding Company is a specific type of company that does not conduct any commercial business itself ("Non-Operative"). Its sole purpose is to hold shares in other financial companies (like the Bank, Insurance arm, etc.). This structure "ring-fences" the bank, ensuring that financial stress in other group companies does not directly affect the bank's depositors.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Universal Banking vs Narrow Banking

| Feature | Universal Banking | Narrow Banking |

|---|---|---|

| Committee | Khan Committee | Tarapore Committee |

| Operations | Banking operations by using all types of products i.e. low risk (CASA), medium risk (HL) and high risk (such as insurance, credit card, forex etc.) | Banking operations by using low risk products such as CASA deposits, term deposit and safe investments. |

On-Tap Policy on Licensing of New Private Banks

The Reserve Bank of India (RBI)'s "on-tap" licensing policy for new private sector banks allows eligible entities to apply for a banking license at any time, rather than waiting for specific, periodic application windows. This policy aims to foster increased competition and innovation in the banking sector.

Eligible Promoters ("Fit and Proper")

- Residents: Individuals/professionals with 10 years of experience in banking and finance.

- Private Sector Entities: Companies/Groups owned and controlled by residents with a successful track record of 10 years.

- NBFCs: Existing resident-controlled NBFCs with a 10-year track record.

- Excluded: Large industrial houses (where non-financial business > 40% of total assets/income) are not eligible to promote banks but can invest up to 10%.

Corporate Structure (NOFHC)

- Mandatory: If the promoter has other group companies ((e.g., Manufacturing, Real Estate), etc.), setting up a Non-Operative Financial Holding Company (NOFHC) is mandatory. This is to ring-fence (isolate) the bank from other group risks.

- Optional: If the promoter is an individual or a standalone entity with no other group companies, the NOFHC structure is optional (they can own the bank directly).

- Ownership: Promoter/Promoter Group must own at least 51% of the NOFHC.

💡 Concept: What is an NOFHC? A Non-Operative Financial Holding Company is a specific type of company that does not conduct any commercial business itself ("Non-Operative"). Its sole purpose is to hold shares in other financial companies (like the Bank, Insurance arm, etc.). This structure "ring-fences" the bank, ensuring that financial stress in other group companies does not directly affect the bank's depositors.

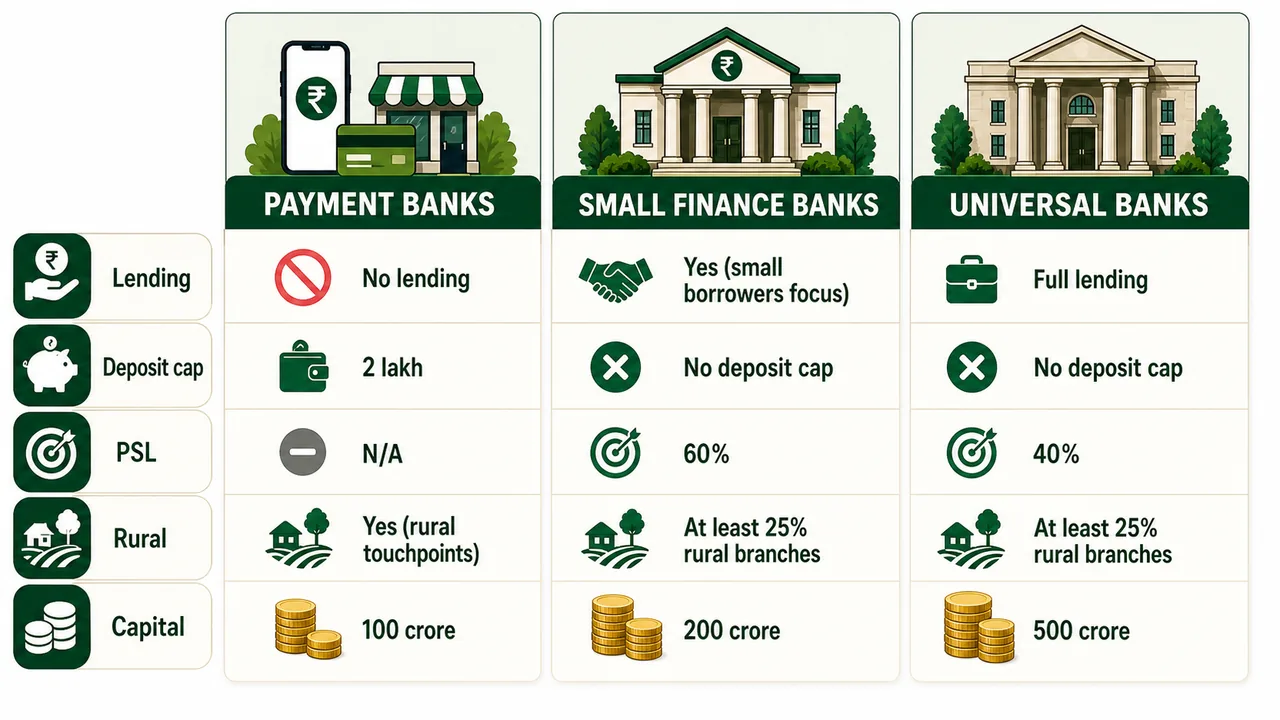

Minimum Capital

- The initial minimum paid-up voting equity capital required is Rs. 500 crore.

- The NOFHC must maintain a minimum net worth of Rs. 500 crore at all times.

- Min CAR - 13% for 3 years.

Shareholding Pattern

- Promoter Stake: Minimum 40% (locked in for 5 years).

- Dilution: A roadmap must be provided at the time of licensing to dilute the holding to the 26% long-term cap within 15 years. (updated in 2021 by RBI)

- Foreign Shareholding: Allowed up to 74% (as per FDI policy).

Regulatory Norms

- Listing: The bank must get listed on stock exchanges within 6 years.

- Branches: Must open at least 25% of branches in unbanked rural centers and follow priority sector lending norms.

- Business Plan: The business plan must address financial inclusion.

Small Finance Banks (SFB)

Concept & Objective

- Goal: To further financial inclusion by providing savings vehicles and supplying credit to small business units, small/marginal farmers, micro/small industries, and unorganized entities.

- Model: High technology, low cost operations.

Eligible Promoters & Capital

- Eligibility: Resident professionals (10 years experience), Companies, Societies, Trusts. Existing NBFCs, MFIs, and Local Area Banks (LABs) can convert.

- Capital: Minimum paid-up equity capital: Rs. 200 crore.

Key Regulations

- Promoter Holding: Minimum 40% (locked for 5 years). Must be reduced to 26% within 15 years (Updated vide 2021 Guidelines; interim targets like 30% withdrawn).

- Prudential Norms:

- Min CAR: 15% (Tier 1: 7.5%, Tier 2: Up to 100% of Tier 1).

- Leverage Ratio: 4.5%

- Forex: Can operate as Category II Authorized Dealer (AD).

- Branching: At least 25% of branches in unbanked rural centers.

- Eligibility for Cat-I: Eligible SFBs can now apply for an AD Category-I license directly after completing two years of operation as an AD Category-II. As of 2026, the SFB must be a Scheduled Bank with a minimum net worth of ₹500 crore and a CRAR of at least 15%.

Business Restrictions (The "Small" Factor)

- Priority Sector Lending (PSL): Adjusted Net Bank Credit (ANBC) target is 60% (vs 40% for universal banks).

- Loan Ticket Size: At least 50% of the Loan Portfolio must constitute loans and advances of up to Rs. 25 lakh. (This ensures focus on "small" borrowers).

Payment Banks

Concept & Objective

- Goal: To further financial inclusion by providing small savings accounts and payments/remittance services to migrant workforce, low income households, small businesses, etc.

- Nature: They are "Differentiated Banks" (focusing on transactions, not credit).

Key Restrictions (What they CANNOT do)

- No Lending: They strictly cannot undertake lending activities (no loans, no credit cards).

- Deposit Limit: Maximum balance of Rs. 2 lakh per customer (end of day).

- No Term Deposits: Can only accept demand deposits (Savings/Current).

Allowed Activities

- Accepting demand deposits (up to Rs. 2 lakh).

- Payments and remittance services methods (ATM/Debit Cards, Net Banking, UPI).

- Distributing third-party products (Mutual Funds, Insurance, Pension products).

Regulatory & Financial Norms

- Capital: Minimum paid-up equity capital Rs. 100 crore.

- Promoter Holding: Minimum 40% for the first 5 years.

- Investments (SLR): Minimum 75% of "Demand Deposit Balances" in Government Securities/T-Bills (maturity up to 1 year).

- Liquidity: Maximum 25% in current/time deposits with other scheduled commercial banks (for operational liquidity).

- Leverage Ratio: Minimum 3.0% (Ratio of Tier 1 Capital to Total Exposure).

- Min CAR: minimum Capital to Risk-Weighted Assets Ratio (CRAR) is 15% (Tier 1: 7.5%, Tier 2: Up to 100% of Tier 1).

Active Payments Banks (January 2026)

- Airtel Payments Bank Limited: The first payments bank launched in India (Jan 2017). It operates as a joint venture between Bharti Airtel and Kotak Mahindra Bank.

- India Post Payments Bank (IPPB): A 100% government-owned entity under the Department of Posts.

- Fino Payments Bank Limited: Focuses on a phygital (physical + digital) model. As of early January 2026, it is undergoing a major digital transformation by migrating to the "Finacle" core banking system.

- Jio Payments Bank Limited: A joint venture between Reliance Industries and the State Bank of India (SBI).

- NSDL Payments Bank Limited: Promoted by the National Securities Depository Limited.

Note on Paytm Payments Bank While often listed in historical records, Paytm Payments Bank is no longer fully operational. Following a persistent non-compliance investigation, the RBI barred it from accepting new deposits, credit transactions, or top-ups (including wallets and FASTags) after March 15, 2024. Customers can only withdraw or transfer their existing balances until they are exhausted.

Note: The minimum Leverage Ratio shall be 4% for Domestic Systemically Important Banks (DSIBs) and 3.5% for other banks.

Summary Sheet

| Parameter | Payment Banks | Small Finance Banks (SFB) | On-Tap Universal Banks |

|---|---|---|---|

| Min Paid-up Capital | ₹100 Crore | ₹200 Crore | ₹500 Crore |

| Promoter Holding | Min 40% (5 years lock-in) | 40% (5 yrs) → 26% (15 yrs) | 40% (5 yrs) → 26% (15 yrs) |

| Capital Adequacy (CAR) | 15% | 15% | 13% (for first 3 years) |

| Leverage Ratio | 3% | 4.5% | Standard (3.5% - 4%) |

| Deposit Limit | Max ₹2 Lakh | No Limit | No Limit |

| Lending Activity | Strictly Prohibited | Allowed (Focus on Small Loans) | Allowed |

| PSL Target | N/A | 60% of ANBC | 40% of ANBC |

| Rural Branches | 25% touch points | 25% | 25% |

| FDI Limit | 74% | 74% | 74% |

The Reserve Bank of India (RBI) issued specific Digital Lending Directions on 08.05.2025, which were later included in the RBI (Credit Facilities) Directions 2025.

Digital Lending means a remote and automated lending process, largely by use of seamless digital technologies for customer acquisition, credit assessment, loan approval, disbursement, recovery, and associated customer service.

- Lending Service Provider (LSP): An LSP is a company that functions as an agent of a Regulated Entity (RE) and carries out one or more of the RE’s digital lending functions.

The RE shall remain fully responsible and liable for all acts and omissions of the LSP.

1. Assessing the Borrower’s Creditworthiness

Before approving loans via digital channels, the RE must properly evaluate the risk:

- It is the direct responsibility of the RE to obtain the necessary information relating to the economic profile of the borrower to officially assess the borrower's creditworthiness before extending any loan.

- There should be no automatic increase in the credit limit for the borrower.

2. Disclosures to Borrowers

Transparency is paramount. The RE shall maintain a website in the public domain with:

- Details of all its digital lending products and its Digital Lending Apps (DLAs).

- Details of LSPs and the DLAs of the LSPs, clearly stating the details of the activities for which they have been engaged.

- Direct links to RBI’s Complaint Management System (CMS) and the Sachet Portal.

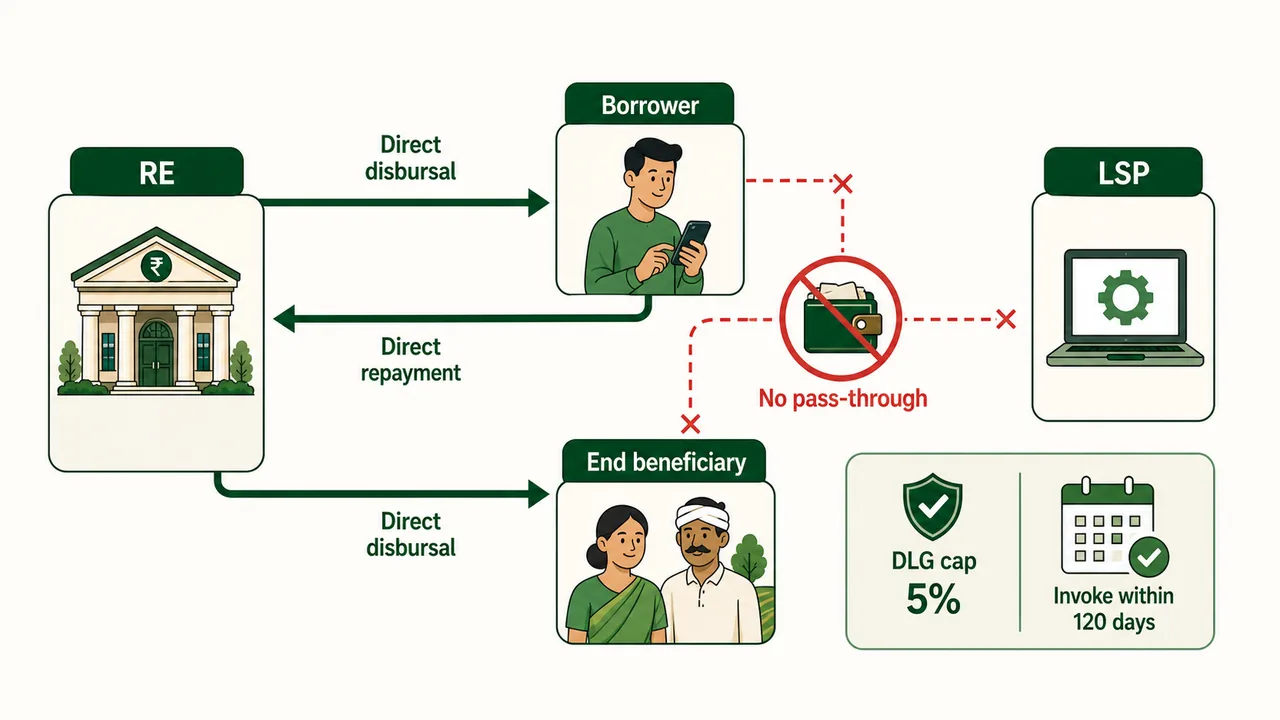

3. Loan Disbursal, Servicing and Repayment

The flow of funds must be completely direct to avoid intermediary fraud:

- Disbursement: Disbursement of the loan by the RE shall always be made into the bank account of the borrower or directly into the bank account of the end-beneficiary ONLY.

- Repayment: The RE shall ensure that all loan servicing and repayment by the borrower are directly deposited in the RE’s bank account without any pass-through account or pool account of any third party, explicitly including the accounts of the LSP.

4. Cooling-off Period & Grievances

- Cooling-off Period: The borrower can exit a digital loan by simply paying the principal and the proportionate APR without any penalty during an initial "cooling-off period". Such a period should not be less than one day.

- Grievance Redressal: If any complaint lodged by the borrower is rejected, or the borrower is not satisfied with the reply, or the borrower has not received any reply within 30 days of receipt of the complaint by the RE, the borrower has escalation rights. They can lodge a complaint over the Complaint Management System (CMS) portal of RBI or send a physical complaint to the RBI.

5. Data Privacy

Collection, usage and sharing of data with third parties: The RE shall ensure that all data is stored only in servers located within India. If data is processed outside India, it shall be immediately deleted from servers outside India and brought back to India within 24 hours of processing.

6. Default Loss Guarantee (DLG) Provider

A Default Loss Guarantee (DLG) is a contract where a third party promises to compensate the Regulated Entity (RE) up to a certain percentage of default losses in a loan portfolio.

- Eligible Providers: The RE may enter into DLG arrangements only with an LSP or another RE engaged as an LSP.

- Maximum DLG Cover: The RE shall ensure that the total amount of DLG cover on any outstanding portfolio shall strictly not exceed 5% of the total amount disbursed out of that specific loan portfolio at any given time.

- Invocation and Tenor: The RE shall officially invoke the DLG within a maximum overdue period of 120 days.

- Disclosure Requirements: LSPs with whom REs have a DLG arrangement shall prominently publish on their website the total number of portfolios on a monthly basis within 7 working days following the conclusion of that month.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Universal Banking | Recommended by Khan Committee; banks use all types of products — low, medium, and high risk (CASA, home loans, insurance, forex, credit cards) |

| Narrow Banking | Recommended by Tarapore Committee; banks use only low-risk products (CASA deposits, term deposits, safe investments) |

| On-Tap Licensing | RBI policy allowing eligible entities to apply for a private bank license at any time (no periodic windows) |

| Eligible Promoters (On-Tap) | Residents/professionals with 10 years experience; private companies/NBFCs with 10-year track record; large industrial houses excluded (can invest up to 10%) |

| NOFHC | Non-Operative Financial Holding Company — mandatory if promoter has other group companies; optional for standalone/individual promoters; promoter must own ≥ 51% |

| On-Tap: Min Capital | ₹500 crore paid-up voting equity capital |

| On-Tap: Promoter Stake | Min 40% (locked 5 years) → dilute to 26% within 15 years |

| On-Tap: CAR | 13% for the first 3 years |

| On-Tap: Listing | Must list on stock exchanges within 6 years |

| On-Tap: Rural Branches | At least 25% in unbanked rural centres |

| On-Tap: FDI Limit | Up to 74% foreign shareholding allowed |

| Small Finance Banks (SFB) — Goal | Financial inclusion for small businesses, small/marginal farmers, micro industries; high tech, low cost model |

| SFB: Min Capital | ₹200 crore |

| SFB: Promoter Holding | Min 40% (5-year lock-in) → 26% within 15 years |

| SFB: CAR | 15% (Tier 1: 7.5%) |

| SFB: Leverage Ratio | 4.5% |

| SFB: PSL Target | 60% of ANBC (vs 40% for universal banks) |

| SFB: Loan Size Rule | At least 50% of loan portfolio must be loans up to ₹25 lakh |

| SFB: AD Category | Operates as Category II AD; eligible for Cat-I after 2 years + min net worth ₹500 crore + CRAR ≥ 15% |

| Payment Banks — Goal | Financial inclusion for migrant workers, low-income households; differentiated banks focused on transactions, not credit |

| Payment Banks: Cannot Do | No lending (no loans, no credit cards); no term deposits; max deposit ₹2 lakh per customer |

| Payment Banks: Can Do | Accept demand deposits (up to ₹2 lakh); payments/remittances (ATM, debit cards, UPI); distribute MFs, insurance, pension |

| Payment Banks: Min Capital | ₹100 crore |

| Payment Banks: CAR | 15% (Tier 1: 7.5%) |

| Payment Banks: SLR | Min 75% of demand deposits in Govt Securities/T-Bills (maturity ≤ 1 year) |

| Payment Banks: Leverage | Minimum 3.0% |

| Active Payment Banks (Jan 2026) | Airtel (first, Jan 2017), India Post (IPPB) (100% govt-owned), Fino, Jio (Reliance + SBI JV), NSDL |

| Paytm Payments Bank | Barred by RBI from new deposits/top-ups after March 15, 2024; only withdrawals allowed |

| Digital Lending | RBI Directions dated 08.05.2025; automated remote lending via digital tech |

| Lending Service Provider (LSP) | Agent of a Regulated Entity (RE) for digital lending; RE remains fully responsible for LSP's acts |

| Loan Disbursement Rule | Must go directly into borrower's or end-beneficiary's bank account only; repayments must go to RE's account (no pass-through/pool accounts) |

| Cooling-off Period | Borrower can exit digital loan by paying principal + proportionate APR, no penalty; minimum 1 day |

| Grievance Escalation | If no reply within 30 days, borrower can escalate to RBI's CMS portal |

| Data Storage | All data on servers within India; if processed abroad, must return within 24 hours |

| Default Loss Guarantee (DLG) | Max cover: 5% of outstanding portfolio; eligible providers: LSP or another RE; invocation within 120 days overdue; LSP publishes portfolio data monthly within 7 working days |

Lesson Doubts

Ask questions, get expert answers