🏗️ Reserve Bank of India (Project Finance) Directions

Guidelines and prudential conditions related to sanctioning, disbursing, monitoring, and provisioning of project finance loans.

Reserve Bank of India (Project Finance) Directions, 2025

The RBI issued these directions to standardise and strengthen the framework for project finance lending across all major regulated entities in India. Project finance is a high-stakes lending model — understanding the phases, conditions, and provisioning norms is critical for exam and professional readiness.

1. Overview & Applicability

These directions came into effect from October 01, 2025, and apply uniformly across:

- Commercial Banks (including Small Finance Banks; but excluding Payments Banks, RRBs, and LABs, which have limited lending mandates)

- All NBFCs (including Housing Finance Companies)

- Primary (Urban) Co-operative Banks (UCBs)

- All India Financial Institutions (AIFIs) like NABARD, NHB, EXIM Bank, SIDBI

The broad coverage ensures that project finance risks are managed consistently, regardless of the type of lender.

2. Key Definitions

Understanding these terms is foundational — they appear repeatedly in every rule:

-

Project Finance: A method of funding where the revenues generated by the project itself are the primary source of repayment (at least 51% of cash flows) and the primary security. Unlike corporate loans, there's no direct recourse to the promoter's general assets beyond the project.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Reserve Bank of India (Project Finance) Directions, 2025

The RBI issued these directions to standardise and strengthen the framework for project finance lending across all major regulated entities in India. Project finance is a high-stakes lending model — understanding the phases, conditions, and provisioning norms is critical for exam and professional readiness.

1. Overview & Applicability

These directions came into effect from October 01, 2025, and apply uniformly across:

- Commercial Banks (including Small Finance Banks; but excluding Payments Banks, RRBs, and LABs, which have limited lending mandates)

- All NBFCs (including Housing Finance Companies)

- Primary (Urban) Co-operative Banks (UCBs)

- All India Financial Institutions (AIFIs) like NABARD, NHB, EXIM Bank, SIDBI

The broad coverage ensures that project finance risks are managed consistently, regardless of the type of lender.

2. Key Definitions

Understanding these terms is foundational — they appear repeatedly in every rule:

-

Project Finance: A method of funding where the revenues generated by the project itself are the primary source of repayment (at least 51% of cash flows) and the primary security. Unlike corporate loans, there's no direct recourse to the promoter's general assets beyond the project.

-

Date of Financial Closure: The date on which the capital structure of the project (equity + debt + grants, if any) covering at least 90% of the total project cost, becomes legally binding on all stakeholders. Grants are counted only in infrastructure PPP projects.

-

Original DCCO (Date of Commencement of Commercial Operations): The target date for the project to start generating revenue, as fixed at the time of financial closure. Any extension to this date is called DCCO deferment and has important NPA implications.

-

Standby Credit Facility (SBCF): A contingency credit line sanctioned alongside the main project loan at financial closure. It serves as a pre-approved buffer to fund cost overruns without triggering a restructuring event.

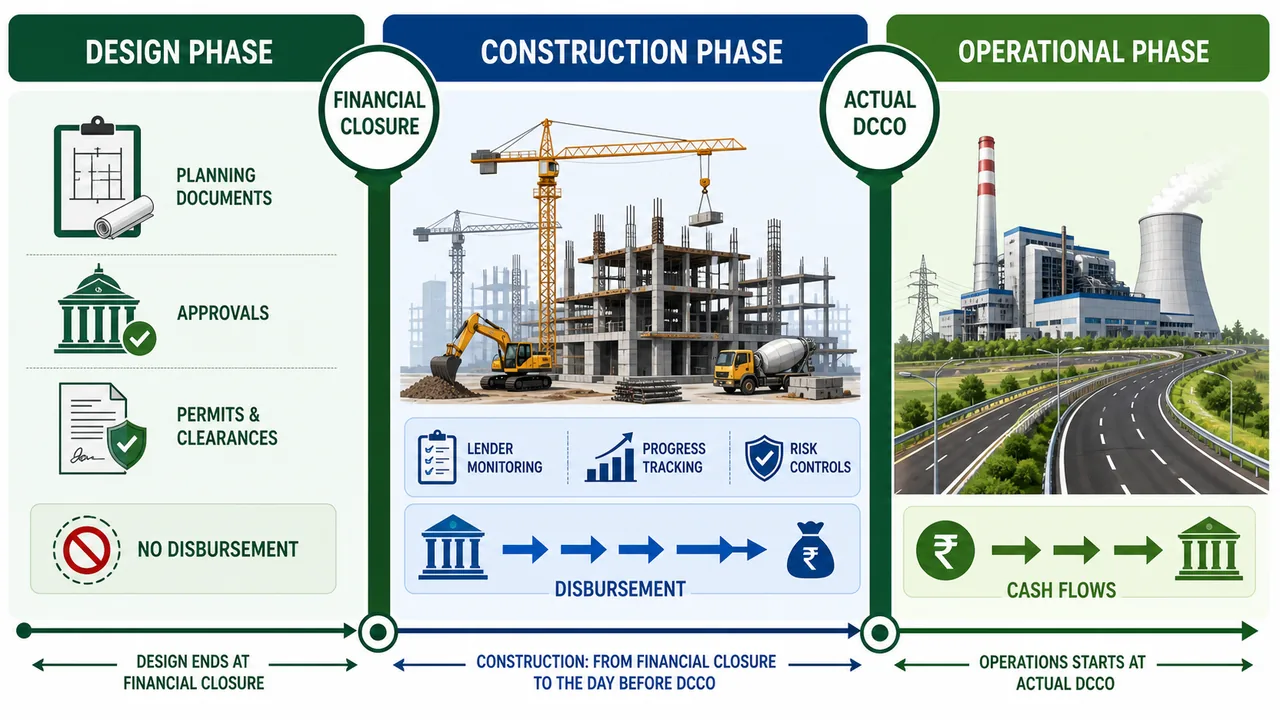

3. A - Phases of Projects

The RBI divides every project into three distinct lifecycle phases, each with its own rules for disbursement, monitoring, and classification:

-

Design Phase — Starts from the genesis of the project and covers designing, planning, and obtaining all applicable clearances/approvals, right up to financial closure. No loan funds are disbursed during this phase.

-

Construction Phase — Begins after financial closure and runs until the day before the actual DCCO. This is the highest-risk phase — money is being spent, but no revenue is being earned yet. Most lender safeguards (land availability, LIE certification) apply during this phase.

-

Operational Phase — Starts on the day of the actual DCCO and ends with the full repayment of the project finance exposure. Lower provisioning norms apply here because cash flows have started.

4. B - Prudential Conditions Related to Sanction of Project Finance Loans

Lenders must satisfy themselves on the following conditions before and during financing to protect against bad loans:

-

Financial closure must have been achieved and the original DCCO clearly documented before any funds are disbursed. Disbursing before financial closure is not permitted.

-

A project-specific disbursement schedule — tied to the actual stage of construction completion — must be part of the loan agreement. This prevents lump-sum disbursements that outpace project progress.

-

The post-DCCO repayment schedule must be realistic, factoring in the initial (often slow) cash flows of a newly operational project.

- The total repayment tenor (including moratorium) shall not exceed 85% of the economic life of the project — ensuring loan repayment happens while the asset is still productive.

-

For projects where aggregate lender exposure ≤ ₹1,500 crore: no single bank can hold less than 10% of that aggregate. This ensures skin-in-the-game and avoids token participation.

-

For projects where aggregate lender exposure > ₹1,500 crore: the minimum floor for any individual lender is 5% or ₹150 crore, whichever is higher.

- Important: These minimum exposure rules cease to apply post-actual DCCO — lenders are free to buy/sell positions in the secondary market once the project is operational.

5. C - Sale or Purchase of Exposure

These rules govern how lenders can trade their project finance positions — a key concern in large syndicated deals:

-

Before DCCO, banks may buy or sell their exposures to other lenders under a syndication arrangement — but only if each lender's resulting share stays within the minimum floors described above.

-

A bank must ensure that all required approvals and clearances for implementing the project are obtained before financial closure. Lending blind — without confirmed regulatory permissions — increases risk significantly.

-

Milestone-contingent approvals (e.g., environmental clearances post land acquisition) are only considered valid once those milestones are actually achieved. Anticipated future approvals cannot be treated as existing clearances.

6. D - Prudential Conditions Related to Disbursement and Monitoring

Disbursement discipline is central to project finance risk management:

-

Before disbursing any funds, the bank must verify that sufficient land and right-of-way is available. The minimum thresholds are:

- PPP Infrastructure Projects — at least 50% of required land must be available

- All other projects (non-PPP infrastructure + non-infrastructure including CRE & CRE-RH) — at least 75% must be available

- Transmission line projects — the bank decides the threshold based on its own assessment

-

For PPP infrastructure projects, disbursement can only begin after the Appointed Date (the date from which the concessionaire's obligations begin under the concession agreement) is declared. Exception: Non-fund-based facilities (like bank guarantees) mandated as a pre-condition for the Appointed Date may be sanctioned earlier.

-

A Techno-Economic Viability (TEV) study is mandatory for all projects where the aggregate lender exposure is ₹100 crore or more. The TEV independently validates that the project is technically feasible and economically viable before any concessions are considered.

-

Disbursals must be proportionate to construction progress and to the actual infusion of equity and other agreed finance sources. Certification from the Lender's Independent Engineer (LIE) or architect is required to validate each stage of completion before funds are released.

-

A project finance account can become NPA at any point before DCCO based on the record of recovery — meaning delayed interest or principal payments can classify the loan as non-performing even while under construction.

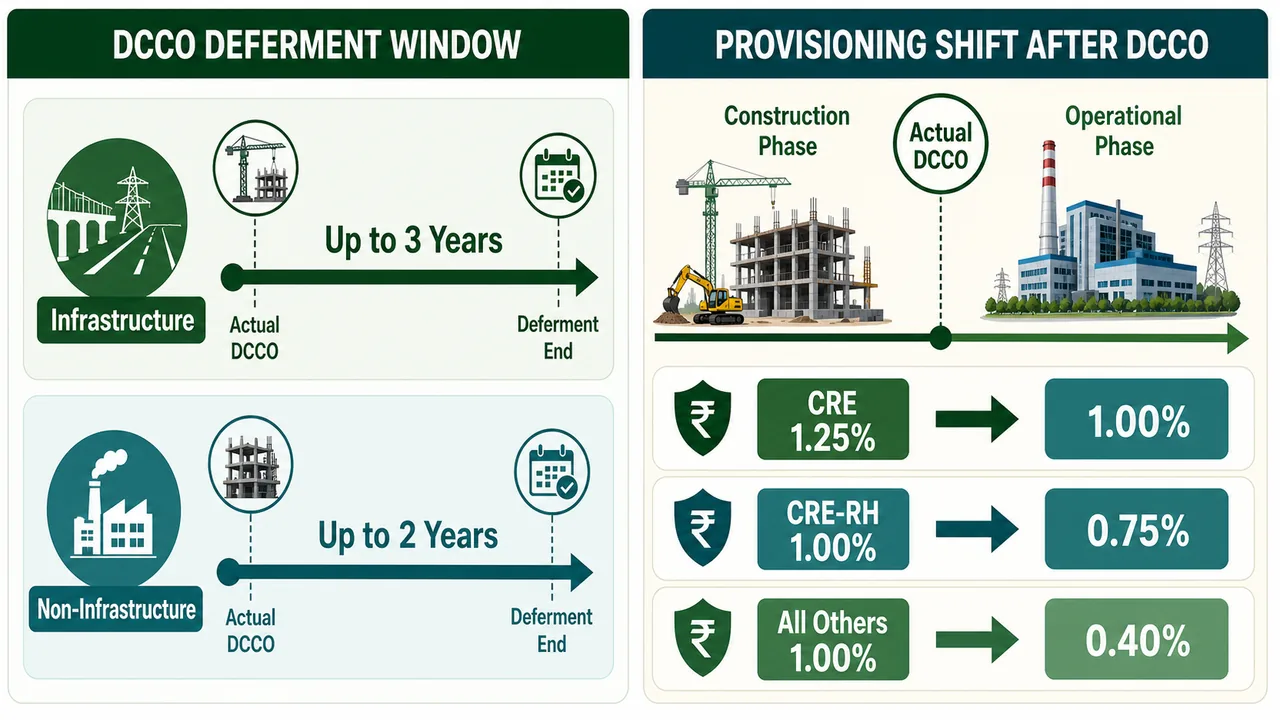

7. Resolution of Stress & DCCO Deferment

When a project faces delays, the RBI provides a structured framework to avoid automatic NPA classification while still maintaining discipline:

- Infrastructure Projects: DCCO can be deferred by up to 3 years without downgrading the account — reflecting the longer gestation of infrastructure.

- Non-Infrastructure Projects (including Commercial Real Estate): Deferment is allowed for up to 2 years.

These windows allow lenders time to resolve genuine project delays without immediately triggering NPA provisioning.

Cost Overrun Support:

- Cost overruns of up to 10% of the original sanctioned project cost can be funded additionally and still classified as 'Standard' assets — provided the extra funding is drawn from the pre-approved Standby Credit Facility (SBCF). This incentivises lenders to pre-plan for contingencies at the time of financial closure itself.

8. Provisioning Norms for Standard Assets

Even for loans that are performing (i.e., Standard assets), lenders must set aside provisions. The required rate depends both on the sector and the phase of the project:

| Sector | Construction Phase Provision | Operational Phase Provision |

|---|---|---|

| CRE (Commercial Real Estate) | 1.25% | 1.00% |

| CRE-RH (Residential Housing) | 1.00% | 0.75% |

| All Others (Infra/Non-Infra) | 1.00% | 0.40% |

Key insight: Provisioning is higher during the Construction Phase (when risk is greatest and no revenue exists) and drops significantly in the Operational Phase (when cash flows provide a natural buffer). For example, a general infrastructure project moves from 1.00% → 0.40% provisioning once it crosses DCCO. This reduction incentivises timely project completion.

9. E - Other Provisions

1. Creation and Maintenance of Database

Banks must maintain project-specific data in an electronic, easily accessible format on an ongoing basis. This enables real-time monitoring and supervisory oversight by the RBI.

The database must capture, at a minimum:

- Debtor profile — who the borrower is and their financial standing

- Original project profile — sanctioned cost, timeline, sector

- Change in DCCO — any revisions to the commercial operations date

- Credit event other than DCCO deferment — restructuring, default, rating downgrades, etc.

- Current specification of the project — updated technical and financial parameters

2. Updating Database

Any change in the parameters of a project finance exposure must be updated in the system within 15 days of such a change occurring. The necessary infrastructure for maintaining this database must be put in place within three months of the effective date (i.e., by January 1, 2026).

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Effective Date | October 01, 2025 |

| Applicability | Commercial Banks (incl. SFBs; excl. Payments Banks, RRBs, LABs), All NBFCs (incl. HFCs), UCBs, AIFIs |

| Project Finance (definition) | Funding where ≥51% of cash flows from the project are the primary repayment source and primary security |

| Date of Financial Closure | Capital structure (equity + debt + grants) covering ≥90% of project cost becomes legally binding; grants counted only for infrastructure PPP projects |

| Original DCCO | Date of Commencement of Commercial Operations — fixed at financial closure; extensions = DCCO deferment |

| Standby Credit Facility (SBCF) | Contingency credit line pre-sanctioned at financial closure to fund cost overruns without triggering restructuring |

| Phase 1 — Design Phase | Genesis to financial closure; planning, clearances; no disbursement during this phase |

| Phase 2 — Construction Phase | After financial closure to day before actual DCCO; highest-risk phase; most lender safeguards apply |

| Phase 3 — Operational Phase | Day of actual DCCO to full repayment; lower provisioning (cash flows active) |

| Sanction condition — DCCO | Financial closure achieved + original DCCO documented before first disbursement |

| Sanction condition — Repayment tenor | Post-DCCO repayment (incl. moratorium) must not exceed 85% of economic life of the project |

| Exposure floor — ≤₹1,500 cr aggregate | No individual bank can hold less than 10% of aggregate exposure |

| Exposure floor — >₹1,500 cr aggregate | Individual bank floor = 5% or ₹150 crore, whichever is higher |

| Exposure floors post-DCCO | Do NOT apply after actual DCCO — banks may freely buy/sell exposures |

| Sale/Purchase before DCCO | Allowed under syndication, but resulting share must respect the minimum exposure floors |

| Approvals before financial closure | All regulatory clearances must be confirmed; milestone-contingent approvals valid only when milestone is met |

| Land availability — PPP Infra | At least 50% land/right-of-way available before any disbursement |

| Land availability — All other projects | At least 75% land/right-of-way available before disbursement (non-PPP infra, CRE, CRE-RH) |

| Land availability — Transmission lines | Decided by the bank |

| PPP Disbursement — Appointed Date | Disbursement begins only after Appointed Date is declared; exception for non-fund-based pre-conditions |

| TEV Study | Techno-Economic Viability study mandatory where aggregate lender exposure ≥ ₹100 crore |

| Disbursement certification | LIE (Lender's Independent Engineer) / architect must certify each stage of completion |

| NPA before DCCO | Account can be classified NPA at any time before DCCO based on record of recovery |

| DCCO Deferment — Infrastructure | Up to 3 years without NPA downgrade |

| DCCO Deferment — Non-Infrastructure (incl. CRE) | Up to 2 years without NPA downgrade |

| Cost overrun — Standard treatment | Overruns up to 10% of original cost funded via SBCF remain classified as 'Standard' |

| Provisioning — CRE (Construction) | 1.25% |

| Provisioning — CRE (Operational) | 1.00% |

| Provisioning — CRE-RH (Construction) | 1.00% |

| Provisioning — CRE-RH (Operational) | 0.75% |

| Provisioning — All Others Infra/Non-Infra (Construction) | 1.00% |

| Provisioning — All Others Infra/Non-Infra (Operational) | 0.40% |

| Provisioning logic | Higher in construction (no revenue); drops in operational phase — incentivises timely DCCO |

| Project Database | Banks must maintain electronic project data on an ongoing basis — debtor profile, project profile, DCCO changes, credit events, current specs |

| Database update timeline | Changes must be updated within 15 days; system to be in place within 3 months of effective date (by Jan 1, 2026) |

Lesson Doubts

Ask questions, get expert answers