📊 RBI Directions on Credit Information Companies (CICs)

Guidelines, regulations, and reporting requirements for Credit Information Companies under the CICRA Act.

RBI Directions on Credit Information Companies (CICs)

On 28.11.2025, the RBI issued directions under the Credit Information Companies (Regulations) Act, 2005 (CICRA). CICRA provides the legislative framework for the regulation and supervision of Credit Information Companies in India. These directions standardise how borrower data is collected, maintained, shared, and corrected — ensuring a reliable credit ecosystem.

At present, 4 CICs are operational in India:

- CRIF High Mark Credit Information

- Equifax Credit Information Services

- Experian Credit Information Company

- TransUnion CIBIL Limited (established March 05, 2012)

1. Membership and Fee

Every Credit Institution (CI) is required to become a member of each CIC — not just one. This ensures that borrower data is available across all four CICs for a complete credit picture.

Who are Credit Institutions (CIs)? They include:

- All Commercial Banks

- All Co-operative Banks

- All India Financial Institutions regulated by RBI (NABARD, NHB, SIDBI, EXIM Bank)

- All NBFCs (Non-Banking Financial Companies)

- HFCs (Housing Finance Companies)

- ARCs (Asset Reconstruction Companies)

There can also be Special User (SU) entities associated with CICs. To qualify as a Special User, an entity must have a net worth of ₹2 crore and 3 years of experience in processing of information.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

RBI Directions on Credit Information Companies (CICs)

On 28.11.2025, the RBI issued directions under the Credit Information Companies (Regulations) Act, 2005 (CICRA). CICRA provides the legislative framework for the regulation and supervision of Credit Information Companies in India. These directions standardise how borrower data is collected, maintained, shared, and corrected — ensuring a reliable credit ecosystem.

At present, 4 CICs are operational in India:

- CRIF High Mark Credit Information

- Equifax Credit Information Services

- Experian Credit Information Company

- TransUnion CIBIL Limited (established March 05, 2012)

1. Membership and Fee

Every Credit Institution (CI) is required to become a member of each CIC — not just one. This ensures that borrower data is available across all four CICs for a complete credit picture.

Who are Credit Institutions (CIs)? They include:

- All Commercial Banks

- All Co-operative Banks

- All India Financial Institutions regulated by RBI (NABARD, NHB, SIDBI, EXIM Bank)

- All NBFCs (Non-Banking Financial Companies)

- HFCs (Housing Finance Companies)

- ARCs (Asset Reconstruction Companies)

There can also be Special User (SU) entities associated with CICs. To qualify as a Special User, an entity must have a net worth of ₹2 crore and 3 years of experience in processing of information.

Fee Structure:

- One-time membership fee: Maximum ₹10,000 payable to each CIC

- Annual fee: Shall not exceed ₹5,000

These are intentionally kept low to ensure all lending institutions — even small NBFCs and co-operative banks — can afford CIC membership.

2. Submission of Data by CIs

Data submission is the backbone of the credit information system. The RBI has set strict timelines to ensure credit records stay current:

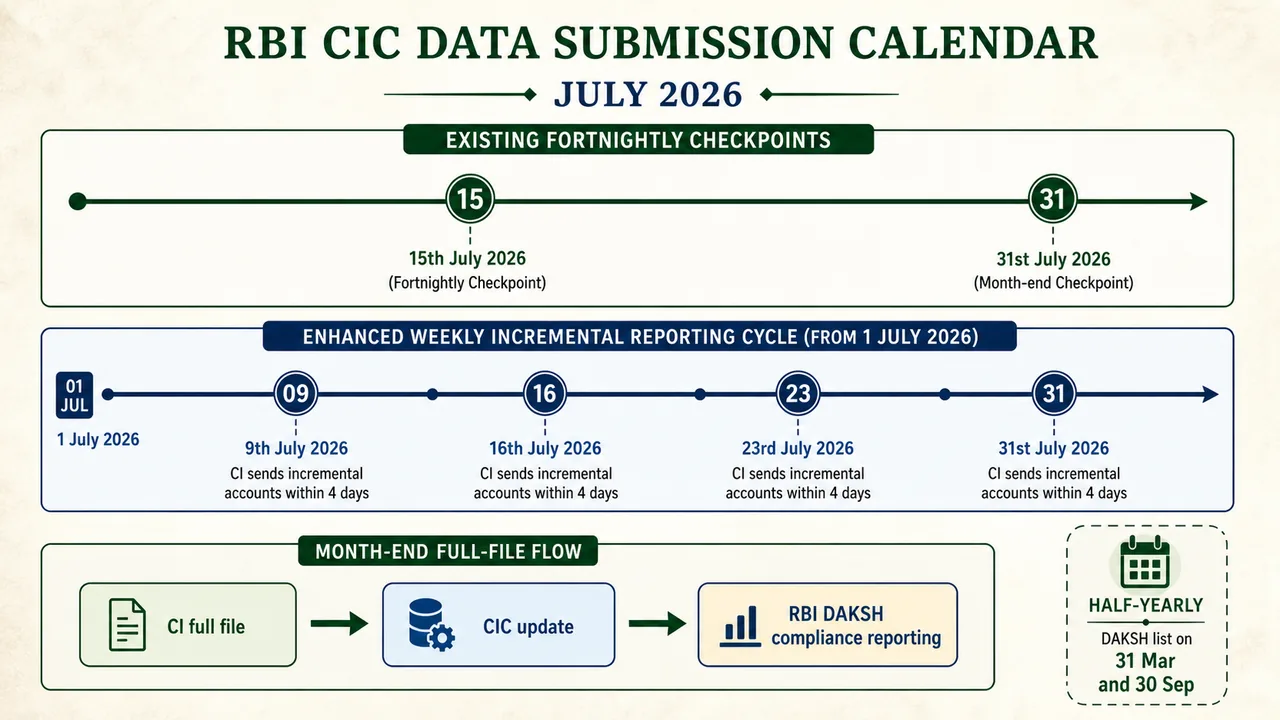

1. Frequency of Data Updates:

A CIC shall collect and maintain credit information and update it on a fortnightly basis (as on the 15th and the last day of the respective month) or at shorter intervals.

- From 1st July 2026 (enhanced frequency): Information for 'incremental accounts' (new or recently modified accounts) is to be submitted by CIs as on the 9th, 16th, 23rd, and last day of each month — effectively a weekly cycle — within 4 calendar days of each reporting date.

- Additionally, CIs shall submit a full file of all credit information records at the end of every month, by the 5th of the next month.

2. DAKSH Portal Reporting:

As on March 31 and September 30 (half-yearly), each CIC shall provide a list of CIs to RBI at the 'DAKSH' portal that are not adhering to the data submission timelines. This acts as a compliance enforcement mechanism — non-compliant CIs are flagged to the regulator.

3. Uniform Credit Reporting Format (UCRF):

CIs shall submit credit information to CICs using the "Uniform Credit Reporting Format" (UCRF). There are 3 separate Forms:

- One for the Consumer segment (individual borrowers)

- One for the Commercial segment (companies/firms)

- One for the Microfinance segment

4. Commercial Papers:

Information on Commercial Papers issued by companies shall be reported on a fortnightly basis by the CI designated as the Issuing and Payment Agent (IPA).

5. Unhedged Foreign Currency Exposure (UFCE):

The information regarding UFCE of individual borrowers shall be reported on a fortnightly basis to the CICs by the lending CI. This helps assess the foreign exchange risk in a borrower's portfolio.

6. Self Help Groups (SHGs):

CIs financing SHGs shall report SHG member-level data. However, this applies only to members of SHGs that take loans exceeding ₹1,00,000. Smaller SHG loans are exempt from individual member-level reporting.

3. Reporting of Defaulters

CICs play a critical role in making defaulter information available to the banking system:

7. A CIC shall provide access to the list of non-suit filed accounts of large defaulters to all CIs. This is an internal-access list — shared among lenders but not publicly displayed.

8. A CIC shall display the list of suit-filed accounts of large defaulters on its website (publicly visible). Cases admitted with the NCLT (National Company Law Tribunal) or NCLAT (National Company Law Appellate Tribunal) shall be reported under the suit-filed cases.

9. Every CIC shall display both suit-filed and non-suit filed accounts of the List of Wilful Defaulters (LWD) on its website. Wilful defaulters get the harshest disclosure treatment — both categories are made public.

4. Data Cleansing and Data Quality Index (DQI)

Maintaining data accuracy is as important as collecting data in the first place.

Data Cleansing:

Each CIC shall undertake data cleansing at least once in a quarter and share the findings with the respective CIs for confirming accuracy. If a CI does not respond within a month, the CIC shall report this non-response to RBI on a half-yearly basis. This ensures CIs cannot ignore data quality issues.

Data Quality Index (DQI):

A CIC shall prepare a DQI for assessing the quality of data submissions and improving it over time. The DQI framework works as follows:

- DQIs shall be in the form of numeric scores calculated on a monthly basis.

- A CIC shall compute industry-level DQIs as a weighted average of the CI-level DQI — giving a sector-wide quality benchmark.

- A half-yearly industry benchmark shall be calculated as a rolling average of the preceding six months' Industry-level DQI score of the respective category of CIs.

- A CIC shall provide a file-level DQI for all segments for all files to the concerned CI within 3 calendar days of their receipt. CI-level DQI shall be provided to the concerned CI on a monthly basis by the 10th day of the next month.

5. Credit Information Report (CIR) & Corrections

The CIR is the end product of the entire credit information system — the report that lenders use to evaluate borrowers.

Standardisation:

A CIC shall use standardised terminology to facilitate comparison between CIRs of two or more CICs. Importantly, information relating to loans declined previously to customers shall not be reported by a CIC — only actual credit relationships are reflected.

Credit Score Calibration:

To facilitate understanding and interpretation, credit scores shall be calibrated from 300 to 900 by a CIC. A higher score indicates better creditworthiness.

Free Report:

Upon request, a CIC shall provide access in an electronic format to one Free Full Credit Report (including credit score), once at any time during a calendar year, to individuals whose credit score is available with them. This empowers borrowers to check their own credit health at no cost.

6. Correction of Credit Information Report

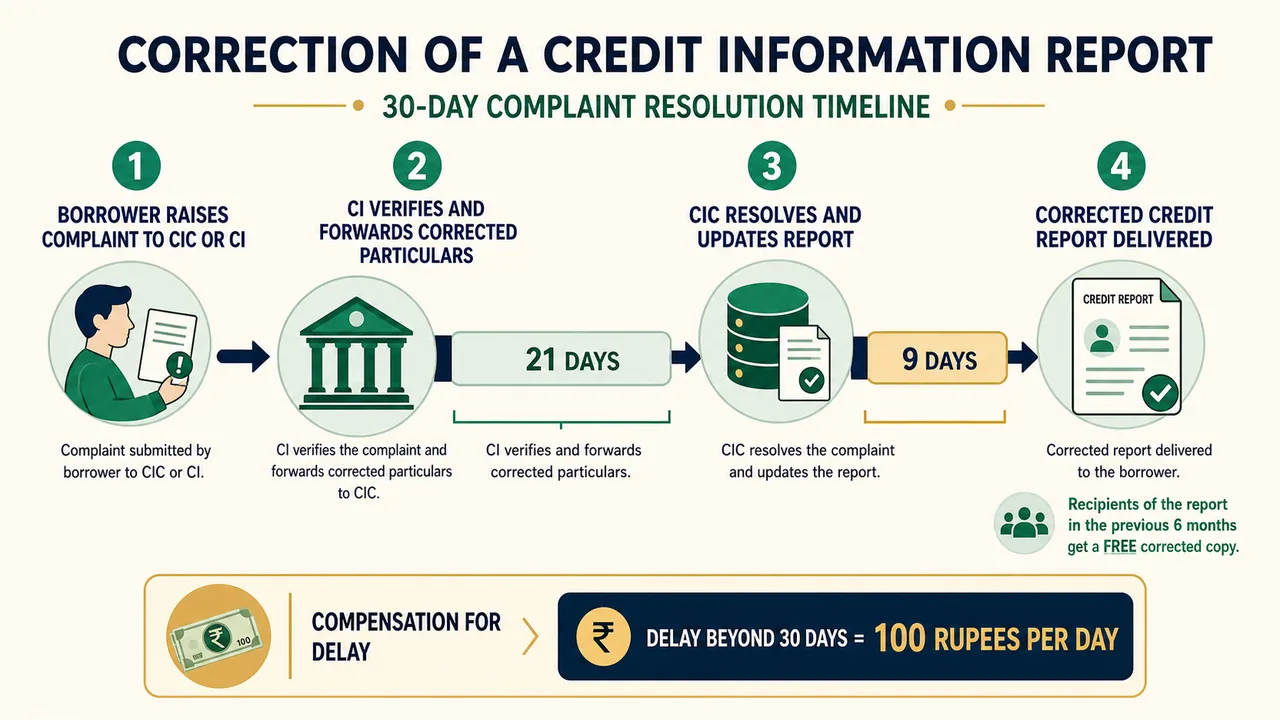

If a borrower finds errors in their CIR, a structured correction process applies:

- A borrower may request a CIC or CI to update the credit information.

- Collectively, the CI and CIC have an overall limit of 30 days to resolve or dispose of the complaint. This breaks down as:

- 21 days for the CI to forward the corrected particulars to the CIC

- 9 days for the CIC to resolve the complaint and update the report

- After correction, the CIC shall provide a free copy of the corrected report to everyone to whom the report had been issued during the previous six months.

Compensation:

If a complaint is not resolved within 30 calendar days from the date of initial filing, the complainant is entitled to compensation of ₹100 per calendar day of delay. This penalty incentivises timely resolution.

7. Investments in CIC

The RBI regulates ownership and investment in CICs to ensure independence and prevent concentration:

- Investments (directly or indirectly) shall not exceed 10% of the equity capital of the investee CIC.

- RBI may consider allowing FDI up to 49% in CICs.

- If ownership of a CIC is not well diversified, governance safeguards apply:

- At least one-third of directors shall be Indian nationals residing in India

- 50% of directors should be Indian nationals / Non-Resident Indians (NRIs) / Persons of Indian Origin (PIOs)

- Foreign Institutional Investment (FII) or Foreign Portfolio Investment (FPI) can directly or indirectly hold below 10% equity, and any acquisition in excess of 1% shall have to be reported to RBI.

8. Related Market Participants and Benchmarks

Credit Information Companies (CICs)

As detailed above, there are currently four functional CICs in India:

- TransUnion CIBIL

- Experian

- Equifax

- CRIF High Mark

Credit Rating Agencies (CRAs)

CRAs are responsible for assessing the creditworthiness of debt instruments and entities. Unlike CICs (which track individual/commercial borrower history), CRAs rate bonds, debentures, and company credit profiles. The major CRAs in India include:

- CRISIL

- ICRA

- CARE

- Brickwork

- SMERA

- Infomerics Valuations and Rating

IMPORTANT

Fitch CRA was recently removed by RBI from the list of accredited Credit Rating Agencies.

Financial Benchmarks

Financial benchmarks are indices or rates used as a reference to determine the price of financial contracts (e.g., loan interest rates, derivative pricing).

- FBIL (Financial Benchmarks India Pvt Ltd): This is the independent benchmark administrator in India, responsible for administering key financial benchmarks.

- Promoted by:

- FIMMDA (Fixed Income Money Market and Derivatives Association of India)

- FEDAI (Foreign Exchange Dealers' Association of India)

- IBA (Indian Banks' Association)

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| CICRA | Credit Information Companies (Regulations) Act, 2005 — legislative framework for CICs |

| RBI Directions issued on | 28.11.2025 |

| 4 CICs in India | CRIF High Mark, Equifax, Experian, TransUnion CIBIL |

| Credit Institutions (CIs) | All Commercial Banks, Co-operative Banks, AIFIs, NBFCs, HFCs, ARCs |

| Special User (SU) eligibility | Net worth ₹2 crore + 3 years experience in information processing |

| One-time membership fee | Maximum ₹10,000 per CIC |

| Annual fee | Not exceeding ₹5,000 |

| Data update frequency | Fortnightly (15th and last day of month) |

| From 1st July 2026 — incremental accounts | Submit on 9th, 16th, 23rd, last day of month; within 4 calendar days |

| Full file submission | End of every month, by 5th of next month |

| Non-compliant CIs reported via | DAKSH portal (half-yearly: March 31 & Sept 30) |

| UCRF — 3 Forms | Consumer, Commercial, Microfinance segments |

| Commercial Papers reporting | Fortnightly by Issuing and Payment Agent (IPA) |

| UFCE reporting | Fortnightly by lending CI |

| SHG member-level data | Only for SHG loans exceeding ₹1,00,000 |

| Non-suit filed defaulters | List provided to all CIs (internal access) |

| Suit-filed defaulters | Displayed on CIC website (public); includes NCLT/NCLAT cases |

| Wilful Defaulters (LWD) | Both suit-filed & non-suit filed displayed on CIC website |

| Data Cleansing | At least once a quarter; non-responsive CIs reported to RBI half-yearly |

| DQI scores | Numeric, computed monthly |

| Industry-level DQI | Weighted average of CI-level DQIs |

| Half-yearly industry benchmark | Rolling average of preceding 6 months' industry DQI |

| File-level DQI delivery | Within 3 calendar days of receipt |

| CI-level DQI delivery | By 10th day of next month |

| CIR Standardisation | Standardised terminology; declined loans not reported |

| Credit Score range | 300 to 900 |

| Free Credit Report | 1 free report per calendar year (electronic, includes score) |

| Complaint resolution | Total 30 days — CI: 21 days + CIC: 9 days |

| Free corrected report | Sent to all recipients of last 6 months |

| Compensation for delay | ₹100 per calendar day beyond 30 days |

| Investment cap in CIC | ≤10% of equity capital |

| FDI in CIC | RBI may allow up to 49% |

| Board composition (non-diversified) | ⅓ directors = Indian nationals in India; 50% = Indian nationals/NRIs/PIOs |

| FII/FPI equity cap | Below 10%; acquisition >1% must be reported to RBI |

| CRAs in India | CRISIL, ICRA, CARE, Brickwork, SMERA, Infomerics (Fitch removed by RBI) |

| FBIL | Independent benchmark administrator; promoted by FIMMDA + FEDAI + IBA |

Lesson Doubts

Ask questions, get expert answers