🏠 Retail Loans

Retail banking products, model loan schemes for home, auto, personal, education, gold, pensioner, property, holiday loans, and Reverse Mortgage Loan (RML/RMLeA).

Retail Loans

What is Retail Banking?

Banks cater to various clients — companies, agriculturists, MSMEs, and individuals. While loans to businesses are repaid from cash flows generated by the financed activity, retail banking focuses on serving individual customers rather than businesses.

Individuals may borrow for non-income-generating purposes like buying houses, vehicles, or personal expenses. Repayment for retail loans typically comes from the borrower's regular income, not necessarily from the activity financed.

Characteristics of Retail Banking

- Serves individual customers (not corporates).

- Focuses on the mass market, addressing a large group of individuals.

- Utilizes both physical and virtual channels — ATMs, online banking, and mobile banking.

- Standardization in features and criteria is a common characteristic across retail loan products.

Advantages of Retail Banking

1. Large Customer Base:

- Aids in mass selling and easy recovery of marketing costs.

- Provides opportunities for cross-selling other financial products and services.

2. Increased Net Interest Margin (NIM):

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Retail Loans

What is Retail Banking?

Banks cater to various clients — companies, agriculturists, MSMEs, and individuals. While loans to businesses are repaid from cash flows generated by the financed activity, retail banking focuses on serving individual customers rather than businesses.

Individuals may borrow for non-income-generating purposes like buying houses, vehicles, or personal expenses. Repayment for retail loans typically comes from the borrower's regular income, not necessarily from the activity financed.

Characteristics of Retail Banking

- Serves individual customers (not corporates).

- Focuses on the mass market, addressing a large group of individuals.

- Utilizes both physical and virtual channels — ATMs, online banking, and mobile banking.

- Standardization in features and criteria is a common characteristic across retail loan products.

Advantages of Retail Banking

1. Large Customer Base:

- Aids in mass selling and easy recovery of marketing costs.

- Provides opportunities for cross-selling other financial products and services.

2. Increased Net Interest Margin (NIM):

- Retail loans carry higher interest rates compared to corporate loans.

- Interest rates on retail deposits are lower than corporate deposits.

- Higher spread between interest charged and interest paid leads to a better NIM.

3. Less Volatility:

- Home/personal loans have lower default rates and less volatility during economic downturns, providing a stable portfolio in economic shocks.

4. Dispersed Credit Risk:

- Risks are spread across a stable customer base with consistent incomes (salaried individuals).

- Small loan amounts per customer minimize the impact on the balance sheet.

5. Customer Loyalty:

- Retail customers are less likely to switch banks due to access, familiarity, convenience, and emotional attachment.

6. Facilitates Marketing:

- Large customer base enables effective marketing and cross-selling across various products and services.

Disadvantages of Retail Banking

- High processing costs per unit due to small ticket size.

- Large workforce required for handling retail accounts.

- High competition among banks leading to pressure on margins.

- Increased risk of fraud and defaults in unsecured lending.

- Technological investment needed for digital services and channels.

Retail Banking Products

| Category | Products |

|---|---|

| Liability Products | Savings, Current, and Term Deposit Accounts |

| Credit Products | Personal Loans, Auto Loans, Home Loans, Education Loans, Credit Cards, Gold Loan |

| Other Products/Services | Debit Cards, ATM Cards, Insurance, Mutual Funds, Depository Services, Internet Banking, Mobile Banking |

Salient Features of Retail Asset Products

Loan Types

- Loans for construction or purchase of houses, house plots, renovation.

- Loans for purchase of personal vehicles (two-wheelers and four-wheelers).

- Personal loans for purchase of white goods.

- Loans for personal expenses — family events, medical expenses, leisure travel.

- Education loans.

Target Customers

- Individuals, self-borrowers, employees of proprietorship/partnership firms, companies, government/semi-government employees, professionals.

- Retail loans are volume-driven. Eligibility is determined through scorecard-based assessments.

- Qualifications and scoring sheets, along with KYC norms, apply to personal loans.

How Retail Differs from Corporate Loans

- Corporate loans use detailed credit appraisal; retail loans use scorecard-based assessments and predetermined criteria.

- Assessment involves both quantifiable and non-quantifiable aspects; a scoring sheet is used.

- KYC norms are also applicable in the lending process.

Quantum of Loan

- Related to the product or individual's income.

- Examples: 12 times monthly income for personal expenses, 4 times annual income for housing loans (may vary across banks).

- Eligibility may also factor in spouse's or co-applicant's income.

Repayment

- Duration varies from 3 to 20 years based on loan purpose.

- Personal/consumer loans: 5 to 7 years; housing loans: 5 to 20 years (sometimes 25/30 years).

- Banks ensure minimum net take-home pay after accounting for all EMIs.

- EMIs can be fixed or floating rate linked.

- Penalties for prepayment should be clearly outlined in the fair practices code.

Processing and Other Charges

- Banks may impose processing fees, documentation fees, inspection charges.

- Transparent disclosure in the scheme and clear explanation to the applicant are mandatory.

Due Diligence

Due diligence is vital due to the high number of retail loan applicants and aggressive marketing:

- KYC verification validated with relevant documents.

- CIBIL report verification.

- Telephonic verification at office/business phone numbers.

- Verification of moveable property offered as security.

- Verification of creditworthiness of guarantor and employment status.

- Valuation of property by a bank-appointed valuer.

- Aim is to authenticate provided particulars and confirm applicant's eligibility.

Loan Application Process

- Applicant approaches the bank or is approached by the sales team.

- Initial step: collecting necessary information for eligibility determination.

- Information used by CACS for scoring, allocating weights to applicant details.

- System generates a credit score for loan qualification.

- Due diligence follows — verifying application details thoroughly.

- Risk management department assesses credit suitability, exposure, documentation.

- Application moves to back office for documentation, security creation, and loan disbursement.

- Loan disbursal is approved and carried out by the branch.

Advantages of the Process:

- Technology simplifies the process (some banks promise home loans within 7 days).

- Score card method speeds up evaluation.

- Recoveries typically through EMI deductions, often facilitated by employers.

Risks and Mitigation:

- Unscrupulous customers may exploit ease of delivery and score card-based approval.

- KYC should not be done by third parties or relaxed.

- Staff should be well-versed in product details.

Model Loan Schemes

Model schemes outline major considerations, terms, and conditions for various retail loans. Terms may vary based on individual bank risk appetite. Loan officers may have leeway within specified conditions, subject to appropriate level approval. The bank's loan/credit policy clarifies deviations and conditions.

A. Home Loan

Home loan is the single largest loan product for an individual. Initially approved only for bank employees, it was later extended to salaried employees, self-employed, and professionals.

Eligibility

- Salaried employees, Professionals, Self-employed persons.

- Requests also considered from NRIs, PIOs, HUF, Proprietorship Firms, and corporates for their employees/quarters.

Purpose

- To purchase/construct house/flat.

- To renovate/extend/repair existing house/flat.

- To purchase a plot of land for construction of house.

- To acquire household articles along with the house/flat for furnishing (15% of Home Loan amount).

Quantum of Loan

- Construction/purchase of a house/flat: ₹500 Lakh / ₹5.00 Lakh in major metros (Mumbai, Kolkata, New Delhi, Chennai).

- Repairs/renovation/extension: ₹5.00 Lakh.

- Purchase of a plot: ₹5.00 Lakh.

- Amount varies from bank to bank.

Eligible Quantum of Loan (EMI-based)

| Borrower Type | Quantum |

|---|---|

| Salaried Employees | 12 times gross monthly salary OR 6 times gross annual income (IT Returns) |

| Self-employed/Professionals | Approx 6 times of Gross annual income |

| HUF/Proprietorship/Partnership/Company | 7 times of cash accruals (last 3 year accounts) |

NOTE

Net take-home pay (net of IT) of proposed loan should not be less than 40% of the gross monthly salary/income of applicant(s). DSCR should be minimum 1.5.

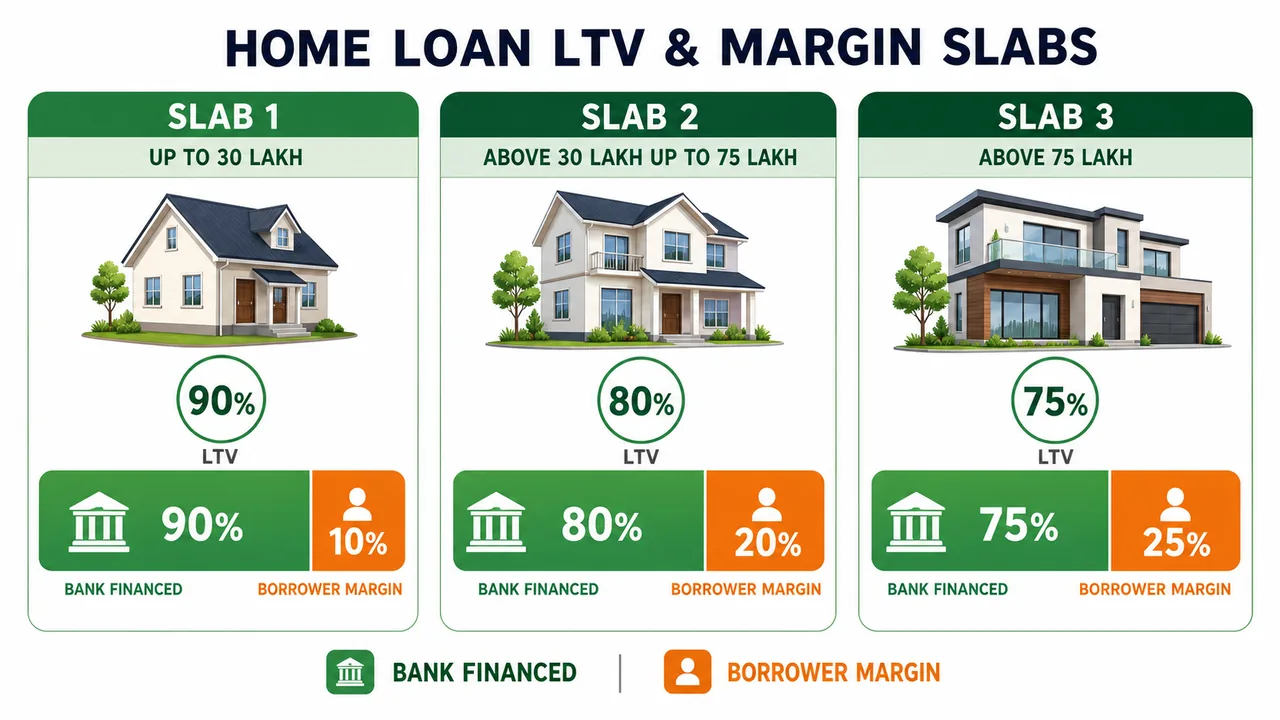

Margin (LTV — Loan to Value)

Margin is subject to RBI stipulated LTV (Loan to Value):

| Loan Amount | Margin | LTV |

|---|---|---|

| Up to ₹30 Lakh | 10% | 90% |

| Above ₹30 Lakh up to ₹75 Lakh | 20% | 80% |

| Above ₹75 Lakh | 25% | 75% |

- Margin is on pure cost of house/flat/plot (excluding stamp duty, registration).

- LTV varies from bank to bank.

- RBI has left ROI at the discretion of individual banks.

Security

- Mortgage/Equitable Mortgage (1st charge) on land/flat/house.

- Third Party guarantee if mortgage could not be created at the time of disbursement.

Disbursement

- Upfront disbursement for ready flat/house, closely linked to stages of construction.

- Upfront disbursal should not be made for incomplete/under-construction/green field housing projects.

Repayment

- Maximum 25 years, including moratorium period of 18 months (max.) in monthly rests.

- Repayment through salary deduction/post-dated cheques.

- Loan to be repaid before retirement (salaried) or before age 65/70 years (others).

Special Features

- Free Personal Accident Insurance cover for borrower and property.

- Tax Benefit under Section 24 & 80C of Income Tax Act.

- CVR Insurance at affordable premium against risk of death during loan tenure (max ₹50 lacs).

- 100% finance for stamp duty and registration expenses.

- Provision of top-up loan for renovation/alteration/addition/extension.

Interest

- Based on Daily Reducing Balance Basis.

- No Pre-Payment Charges on Floating Rate Loan.

- Repayment allowed up to 25 years in select cases.

- Flexible, accelerated, step-up EMI options.

- Inclusion of notional rental income in case of 2nd House.

- No foreclosure charges.

- Tax Benefit under Section 24/80C/80EE/80EEA of Income Tax Act.

Insurance

- Personal Accident Insurance covers accidental death and permanent total disablement.

- In case of accidental death, insurance covers the outstanding loan amount.

- Optional feature; borrowers bear the expenses.

Property Valuation

- Property valued at the bank's approved valuer.

- Bank's lawyer verifies borrower's title to the property.

- Borrower's right to transfer the property must not be restricted.

Repossession Clause

- Banks rely on the repossession clause to enforce rights in case of default.

- Terms and conditions should be transparent.

- Full details of outstanding amounts to be given before satisfaction.

- Banks may use Recovery Agents, following RBI guidelines.

B. Auto / Vehicle Loan

Nature of the Market

- Private and foreign banks lend heavily for car and personal loans, often collaborating with manufacturers and dealers.

- Non-Banking Finance Companies (NBFCs) typically handle two-wheeler financing (smaller ticket sizes).

- Public sector banks are less aggressive in car loans compared to private and foreign banks.

Eligibility

- Salaried employees, Professionals, Self-employed, NRIs (advance to be granted jointly with Resident Indian).

- Age of individual borrower not to exceed 65 years.

- Also given to HUF, Proprietorship Firms, corporate entities.

Purpose

- Purchase of new four-wheeler vehicles (not requiring heavy duty license).

- Purchase of used/second-hand 2 and 4 wheeler vehicles (age not to exceed 5 years normally).

Permissible Limits

| Category | Limit |

|---|---|

| Individuals — 4 wheelers | ₹50 Lakh |

| Individuals — 2 wheelers | ₹2 Lakh |

| Companies/Corporate (fleet) | ₹100 Lakh |

- Average annual income should be at least ₹3 Lakh p.a.

- Net take-home pay: 40% of Gross income (Net of proposed EMI).

Margin

| Vehicle Type | Margin |

|---|---|

| New cars | 10% |

| 2nd Hand Cars | 25/30% |

| Two-wheelers | 10% |

Security

- Hypothecation of vehicle to be purchased out of bank finance.

- Charge to be registered with RTO.

- Third party guarantee required for:

- Loans to NRIs (Guarantee of Resident Indian required).

- Vehicles not registered with RTO and loans exceeding ₹25.00 Lakh.

Repayment

| Category | Maximum Tenure |

|---|---|

| 4 wheelers (individuals) | 7 years |

| 2 wheelers (individuals) | 5 years |

| Corporates/Firms | 5 years |

- Public sector banks normally do not charge prepayment penalty.

Insurance & Enforcement

- Comprehensive insurance covers 100% of vehicle's value.

- Bank's hypothecation charge noted in insurance policy.

- Disbursement directly to the dealer.

- Banks rely on repossession clause; may use Recovery Agents following RBI guidelines.

C. Personal Loan

Nature

- Primarily unsecured and rely on personal credibility.

- Credit risk and delinquency rates are higher compared to home or vehicle loans.

- Private banks and NBFCs are dominant in this segment.

- Generally provided as an installment repayment or a revolving credit facility.

Eligibility

- Salaried employees, Professionals, individuals with high Net Worth, regular pensioners, retired employees drawing regular monthly pension through Bank, Staff members.

Purpose

Clean/Unsecured Loan:

- Medical expenses for self, spouse, children, dependents.

- Marriage expenses of self, children, dependent relatives.

- Expenses on pilgrimage, tourism.

- Any other personal expenses of bona fide nature.

Secured Loans:

- Repayment of existing housing loan from excess.

- Purchase of consumer durables.

Type of Advance

- Demand/Term Loan/Overdraft (reducible as per repayment schedule).

- Or revolving facility: Flexi/Auto Plough Back.

Quantum of Loan

| Type | Quantum |

|---|---|

| Clean/Unsecured | 12 times net monthly emoluments (salaried) OR 50% of gross annual income (professionals/HNW) |

| Secured | 36 times of Net monthly salary (salaried/pensioners) OR 50% of gross average annual income (self-employed) |

Minimum Loan Size:

- Metro and Urban Centres: ₹10,000.

- Rural and Semi-Urban centres: No minimum.

Security (for Secured Loans)

- Equitable/Legal Mortgage of commercial or residential properties.

- Hypothecation charge on assets acquired.

- Collateral: pledge of gold/gold ornaments, NSC/Indira Vikas Patra, Bonds, Assignment of LIC policies, Mutual Funds.

Repayment

- Clean/Unsecured Loan: Maximum 60 months (exceptional cases up to 84 months).

- Secured Loan: Maximum 60 EMIs. One month after first disbursement.

D. Pensioner Loan Scheme

Eligibility

- Regular pensioners or family pensioners drawing regular monthly pension through the branch.

- Retired employees (other than dismissed/compulsorily retired).

Type of Advance

- Demand Loan/Term Loan/Overdraft (reducible as per repayment schedule/1-2 year overdraft limit).

Quantum

- Regular Pensioner & Family Pensioner: 18 times of monthly pension (maximum loan ₹5 Lakh).

- All Pensioners/Borrowers may be sanctioned more than one loan (e.g., for Personal Needs and Consumer Durables).

Eligible Loan Amount

- Net take-home pension after deduction of loan instalment should be at least 40% of gross pension.

Security

- No security required — pension itself is the security.

- Bank has right to adjust loan against pension credit/family pension credit.

Repayment

- Maximum 60 EMIs w.r.t. one month after first disbursement.

- For Senior Citizens (loans up to ₹5,00,000): @ 0.50% above Base Rate (up to 60 years) and @ 1.00% above Base Rate (above 60 years).

Charges

- Processing charge for Senior Citizens (60 years & above): Waived.

- Stamp Paper Charges: As actual.

E. Property Loan

NOTE

Property loan is a business loan product and not classified under retail loan. It is granted against residential and commercial immovable property.

Eligible Customers

- People engaged in trade, commerce, business, professionals, self-employed, individuals with high net worth, salaried people, proprietary firms, partnership firms, private/public limited companies, HUF, Societies, Staff members, NRIs.

Age Limit

- Permanent service: max. 60 years.

- Others: Maximum 70 years at the end of repayment period.

Type of Advance

- Demand/Term Loan, Overdraft (Reducible/Non-Reducible).

Quantum of Advance

| Category | Eligible | Demand | Overdraft |

|---|---|---|---|

| Individual/Salaried/Self | 1.00 crore | 1.00 crore | 50.00 Lakh |

| Company/Firms | 1.50 crore | 1.00 crore | 1.00 crore |

| Pvt. Ltd, Trust & Others | 1.50 crore | NIL | NIL |

- Take-home pay after proposed instalment should not be less than 40% of gross salary/income.

Rate of Interest

- 1.25% over Base Rate for Directly Reducing Loan.

- Overdraft Non-Reducible: 1.75% over BR.

- Overdraft Reducing: 1.50% above BR.

- DSCR should be more than 1.5.

Repayment

- Overdraft (Non-Reducible): Max 15 years. Reviewed annually.

Processing Charge

- Demand Loan/OD (Reducible): 0.50% of limit. Min ₹5,000, Max ₹25,000.

- Mortgage OD (Reducible): Min ₹5,000, Max ₹10,000.

Insurance & Property

- Mortgaged property must be insured for full value against fire, earthquake, storms, floods, riots, civil commotion.

- Property valued at lower of Realizable/Forced Sale Value OR Registered value of similar property.

- Lawyer's search covers title deeds for current and past 30 years.

F. Holiday Loan Scheme

Eligibility

- Professionals, Business Persons, Self-Employed, Salaried individuals and family members for leisure/tourism/pilgrimage/vacation.

Type of Advance

- Demand Loan (reducible as per repayment schedule).

Quantum

- Clean (unsecured): Max ₹5.00 Lakh.

- With liquid collateral (TRs, NSCs, LIPs, KVPs etc. at least 50% of loan): ₹10 Lakh.

- Pensioners: Max ₹1.25 Lakh.

- No specific margin. Loan amount not to exceed proposed expense/budget.

Repayment

- Maximum 24 EMIs w.e.f. one month after first disbursement.

- Minimum instalment: ₹500.

Processing Charges

- One time @ 2% of loan amount. Min ₹1,000, Max ₹25,000.

- Pensioners: 2% of loan amount. Min ₹500, Max ₹5,000.

- No processing charges for Senior Citizens (60 years & above).

G. Gold Loan Scheme

Target Group

- Resident Indian Citizens, Minors (through natural guardians), Joint borrowers, HUF, Associations of Persons.

- Applicant should get minimum 20 marks under bank's rating exercise.

Type of Advance

- Demand/Term Loan.

Quantum of Advance

- Working/Non-working women: 12 times of monthly net emoluments.

- Professionals: 50% of Gross Annual income (per latest IT Return).

- Minimum ₹5,000/₹10,000. Maximum ₹2 Lakh.

Margin

- 20% of the value of Jewellery/Gold. Valuation as per lender's policy.

Interest Rate

- 3% above Base Rate (~13.50%) (Floating, p.a. at monthly rests).

Repayment

- Maximum 60 EMIs. Repayment period not to exceed age 65 or retirement age (whichever earlier) for salaried employees.

- Repayment through salary deduction/post-dated cheques.

- Net take-home pay (net of EMI): Min 50% of gross income.

Security

- For loans over ₹50,000: liquid securities (NSC/KVP/Insurance Policies/surrender value) for amount exceeding ₹50,000.

Disbursement

- By DD/Pay Order favouring the seller.

- Stamped Receipt/Invoice for total cost (Loan Amount + Margin).

- Proforma invoice required for loans of ₹1 lakh and over.

Processing

- One time @ 2% of loan amount. Min ₹500, Max ₹2,000.

- Other charges: Stamp charges, Loan Agreement copy charges as applicable.

H. Education Loan (IBA Model)

Objective

- Facilitate meritorious students in pursuing higher education in technical and professional courses.

- Priority given to financially disadvantaged yet academically proficient students.

- Assessment based on the employability and earning potential of the student after completing the course.

- Repayment expected from student's future earnings, not parental income or family wealth.

Government Initiatives

- Government of India's policy ensures no denial of professional education due to financial constraints.

- Indian Banks' Association (IBA) formulates a model educational loan scheme for all banks.

Interest Subsidy Scheme

- Launched by the Department of Education, Ministry of Human Resource Development.

- Supports students from Economically Weaker Sections of Society.

Eligibility

- Student should be an Indian National.

- Secured admission to a higher education course in India or abroad through Entrance Test/Merit Based Selection Process after completing HSC (10+2 or equivalent).

Eligible Courses

Studies in India:

- Graduate/PG degree and PG diplomas by recognized colleges/universities (UGC/Government/AICTE/AIBMS/ICMR).

- CWA, CA, CFA etc.

- Courses by IIMs, IITs, ISC, XLRI, NIFT, NID etc.

- Regular Degree/Diploma courses (Aeronautical, pilot training, shipping, nursing etc.).

- Job-oriented professional/technical courses by reputed universities.

Studies Abroad:

- Post-graduation: MCA, MBA, MS, etc.

- Courses by CIMA-London, CPA in USA etc.

- Degree/diploma courses recognized by competent regulatory bodies.

Quantum of Finance

- Maximum up to ₹20 Lakh (India & Abroad).

- Banks may consider higher quantum on course-to-course basis.

Margin

| Loan Amount | Margin |

|---|---|

| Up to ₹4 Lakh | Nil |

| Above ₹4 Lakh (India) | 5% |

| Up to ₹7.50 Lakh (if eligible for Credit Guarantee) | Nil |

- Scholarship/Assistantship included in margin.

Eligible Expenses

| Expense | Maximum |

|---|---|

| Fee payable to college/school/hostel | Fees as approved. Reasonable lodging/boarding |

| Examination/Library/Lab fee | Actual (Net of margin) |

| Travel expenses (abroad) | One way (outward) |

| Insurance premium for student | Actual (Net of margin) |

| Caution deposit/Building fund | Not to exceed 10% of total tuition fees |

| Books/Equipment/Computer/Study tours | Max. 20% of total tuition fees (all combined) |

Security

| Loan Amount | Security Required |

|---|---|

| Up to ₹4 Lakh | No security. Parents to be joint borrower(s) |

| ₹4 Lakh to ₹7.5 Lakh | Parent(s) as co-borrower + suitable third-party guarantee |

| Above ₹7.5 Lakh | Parent(s) as joint borrower(s) + Tangible collateral security (landed properties/paper securities) + assignment of future income |

Rate of Interest

- Linked to Base rate/MCLR as decided by individual banks.

- Simple interest charged during study period and subsequent moratorium period.

- Servicing of interest during study/moratorium period is optional.

- For EMI fixation, accrued interest added to principal.

Repayment

- Moratorium: Course period + 1 year.

- Moratorium for spells of under-employment/unemployment: max 6 months at a time, two or three times during loan life cycle.

- EMIs or step-up instalments spanning 15 years for all categories.

- No prepayment penalty.

Insurance

- Mandatory life insurance policy on the student availing Education Loan.

Processing Fees

- No processing/upfront charges (except for studies abroad — refunded upon taking up the course).

Other Features

- Start-up enthusiasts: moratorium on principal and interest during incubation period, up to 2 years.

- Maximum 2-year extension for course completion.

- 1% interest concession if interest is serviced during study and moratorium period.

- Banks can issue capability certificates for students going abroad.

- No specific age restriction for loan eligibility.

- Joint borrower: usually parent(s)/guardian; for married individuals, spouse or parent(s)/parents-in-law.

- Education loans up to ₹20 Lakh, irrespective of sanctioned amount, considered eligible for priority sector.

Appraisal/Sanction

- Sanction/rejection communicated within 15 days of completed application.

- Future income prospects of student considered during appraisal.

- Rejected applications require concurrence from controlling authority with reasons.

Follow-up/Monitoring

- Banks contact college/university authorities for progress reports.

- Banks encouraged to enter into Memorandum of Understanding (MoU) with educational institutions.

- Annual review of asset quality of educational loans recommended.

I. Reverse Mortgage Loan (RML)

Overview

- Introduced in India in 2007, applicable from April 1, 2008.

- Developed by the National Housing Bank (NHB).

- Enables senior citizens (above 60 years) to receive periodical payments against their mortgaged house.

- Borrowers remain owners and occupants of the house.

- No monthly repayments required during the borrower's lifetime.

Eligibility Criteria

- Indian citizen above 60 years.

- Married couples eligible as joint borrowers.

- Ownership of a residential property in India with clear title.

- Property free from encumbrances.

- Residual life of property: at least 20 years.

- Property used as permanent primary residence.

- Commercial property not eligible.

Salient Features

| Feature | Detail |

|---|---|

| Providers | Primary Lending Institutions (PLIs) — scheduled banks and HFCs registered with NHB |

| Monthly payment cap | ₹50,000 |

| Lump-sum cap | 50% of eligible amount (up to ₹15 lakh) for medical expenses |

| Disbursement | Monthly/quarterly/semi-annually/annually/lump-sum, or line of credit |

| Loan Tenure | Maximum 20 years |

| Tax Exemption | Payments under RML are exempt from income tax |

| Ownership | Borrower remains owner even after loan tenure |

Additional Features

- Settlement: Loan settled from sale proceeds; remaining amount given to borrower/heirs.

- Prepayment: Borrower/heirs can prepay without penalty.

- Existing Mortgage: Borrower can qualify but must be in first lien position.

- Applicability: Nationwide, except areas where agricultural land cannot be mortgaged.

- Property Valuation: Done at least once every five years.

- No Negative Equity Guarantee: Borrower never owes more than property's net realizable value.

- Capital Gains Tax: Only upon property alienation for loan recovery.

Challenges and Limited Success

- Does not ensure regular income beyond fixed tenure of 15-20 years.

- Loan amount is significantly low — determined based on government-set guideline values, not market price.

- Monthly payments comparatively low compared to market interest rates.

- Property assessments are periodic; reduction in market value puts burden on owner.

J. Reverse Mortgage Loan-enabled Annuity (RMLeA)

Enhancement over RML

- NHB, in collaboration with Star Union Daichi Life Insurance Company Ltd. (SUD Life) and Central Bank of India (CBI), introduces an extension of the RML value chain.

- Provides life-time annuity payments to Senior Citizens (key improvement over original RML).

- Borrowers receive assured life-time payments even after the 20-year term.

Eligibility

- Senior Citizens of India above 60 years of age.

- Married couples eligible as joint borrowers.

- Self-acquired, self-occupied residential property with clear and transferable title.

- Property free from encumbrances.

- Residual life at least 20 years.

- Must be permanent primary residence.

Quantum of Loan

- Based on market value of residential property, borrower's age, interest rates, and other factors.

- Minimum property value: ₹5 lakh.

- Revisions based on re-valuation every five years.

Maximum LTV Ratio

| Age | Max. LTV |

|---|---|

| Between 60 and 70 | 60% |

| Between 70 and 80 | 70% |

| 80 and above | 75% |

- Bank has discretion for upper limit (10% or percentage specified by Government).

Other Terms & Conditions

- Source of Annuity: Bank sources Life-time RMLeA from a Life Insurance Company.

- Minimum Purchase Price: ₹2 lakh (no upper limit).

- Irrevocable Nature: RMLeA option cannot be terminated, surrendered, or cancelled.

- Joint Borrowers Option: Can opt to receive annuity separately, proportionately.

- Maximum Lump-sum: 25% of eligible loan amount, capped at ₹15 lakh.

- Loan Disbursement Tenure: Maximum until the demise of the borrower.

- Security: Mortgage of residential property; commercial property ineligible.

- Tax: Periodic annuity payments are subject to income tax (taxable).

- Due and Payable: When last surviving borrower dies, sells the home, or permanently moves out.

- Settlement: Through proceeds from sale of residential property.

- No Prepayment Charges.

- Foreclosure: Liable for foreclosure due to events of default.

Formula for Periodic Payments

Instalment Amount = (PV × LVTR × {(1+i)^n - 1}) / (i)

Where:

- PV = Property Value

- LVTR = LTV Ratio

- n = Number of Instalment Payments

- i = Value depending on Disbursement Frequency selected

Hypothetical Example

| Parameter | Scenario 1 | Scenario 2 |

|---|---|---|

| Property Value | ₹50,00,000 | ₹50,00,000 |

| LTV | 80% | 90% |

| Loan Tenor | 15 years | 15 years |

| Rate of Interest | 10% | 10.50% |

| Monthly Instalment | ₹9,651 | ₹10,368 |

| Quarterly Instalment | ₹29,414 | ₹31,638 |

| Yearly Instalment | ₹1,25,895 | ₹1,36,116 |

Summary Cheat Sheet

| Topic | Key Details |

|---|---|

| Retail banking focus | Mass market individuals, not corporates |

| Retail banking products | Liability (Savings/Current/TD), Credit (Home/Auto/Personal/Education/Gold), Other (Cards/Insurance/MF) |

| Advantage: NIM | Higher spread due to higher lending rate, lower deposit rate |

| Advantage: Risk | Dispersed credit risk across stable salaried customer base |

| Retail vs Corporate | Scorecard-based assessment vs detailed credit appraisal |

| Home Loan | Single largest individual loan; LTV 75-90% based on amount; max 25 yrs; Tax benefit Sec 24/80C |

| Home Loan margin | ≤₹30L: 10%, ₹30-75L: 20%, >₹75L: 25% |

| Home Loan quantum | Salaried: 12x monthly salary; Self-employed: 6x annual income; Net take-home ≥40% |

| Auto Loan | Hypothecation of vehicle; new car margin 10%; max 7 yrs (4W), 5 yrs (2W) |

| Auto Loan limits | Individual 4W: ₹50L, 2W: ₹2L, Corporate fleet: ₹100L |

| NBFCs | Typically handle two-wheeler financing |

| Personal Loan | Primarily unsecured; higher delinquency; max 60 months (clean), 84 months exceptional |

| Personal Loan quantum | Clean: 12x net monthly; Secured: 36x net monthly salary |

| Pensioner Loan | 18x monthly pension (max ₹5L); pension is security; max 60 EMIs |

| Property Loan | Business loan (not retail); max 15 yrs; DSCR ≥1.5; 1.25% over BR |

| Holiday Loan | Max ₹5L (clean), ₹10L (secured); max 24 EMIs; no processing for Sr. Citizens |

| Gold Loan | 20% margin; 3% above BR; max 60 EMIs; min 50% net take-home |

| Education Loan (IBA) | Max ₹20L; moratorium = course + 1 yr; repayment 15 yrs; no prepayment penalty |

| Education Loan margin | ≤₹4L: Nil; >₹4L India: 5% |

| Education Loan security | ≤₹4L: Nil; ₹4-7.5L: third-party guarantee; >₹7.5L: tangible collateral |

| Education Loan priority | Up to ₹20 Lakh eligible for priority sector |

| Education Loan features | 1% interest concession for servicing during study; mandatory life insurance; no processing fees |

| RML | Introduced 2007 (NHB); for senior citizens ≥60 yrs; max 20 yrs; payments exempt from income tax |

| RML eligibility | ≥60 yrs; residential property; clear title; residual life ≥20 yrs; primary residence |

| RML caps | Monthly: ₹50,000; Lump-sum: 50% (up to ₹15L) |

| RML challenge | No income beyond 15-20 yr tenure; low loan amount vs market value |

| RMLeA | Extension of RML with life-time annuity via insurance company (SUD Life + CBI) |

| RMLeA LTV | 60-70 yrs: 60%, 70-80: 70%, 80+: 75% |

| RMLeA key terms | Min property ₹5L; min annuity purchase ₹2L; irrevocable; taxable annuity; lump-sum max ₹15L |

| RMLeA tenure | Until demise of borrower (lifetime); property revaluation every 5 yrs |

| RMLeA due & payable | When last surviving borrower dies, sells home, or moves out permanently |

Lesson Doubts

Ask questions, get expert answers