📋 Bank Credit Policy

Comprehensive guide to bank credit policy — its framework, contents, objectives, lending authorities, appraisal standards, and portfolio composition.

Bank Credit Policy

Introduction

Credit Policy / Loan Policy Overview

A bank's Credit Policy (also called Loan Policy) is a comprehensive document that serves as the guiding framework for all credit-related functions within the bank. Think of it as the ultimate rulebook that every loan officer must follow to ensure safe and profitable lending.

- Goal: Ensure excellence in customer service, stakeholder satisfaction, and employee contentment. By having a clear policy, customers get transparent service, shareholders see steady returns, and employees have clear guidelines to follow without ambiguity.

- Created by: The bank's Board of Directors. This highlights the strategic importance of the document—it comes directly from the highest level of governance.

- Purpose: Guide all credit functions — from sanctioning loans to collecting repayments and advances. It covers the entire lifecycle of a loan, leaving no room for guesswork.

IMPORTANT

The Credit Policy is the single most important internal document governing a bank's lending operations. It dictates how the bank manages its most critical asset: its loan portfolio.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Bank Credit Policy

Introduction

Credit Policy / Loan Policy Overview

A bank's Credit Policy (also called Loan Policy) is a comprehensive document that serves as the guiding framework for all credit-related functions within the bank. Think of it as the ultimate rulebook that every loan officer must follow to ensure safe and profitable lending.

- Goal: Ensure excellence in customer service, stakeholder satisfaction, and employee contentment. By having a clear policy, customers get transparent service, shareholders see steady returns, and employees have clear guidelines to follow without ambiguity.

- Created by: The bank's Board of Directors. This highlights the strategic importance of the document—it comes directly from the highest level of governance.

- Purpose: Guide all credit functions — from sanctioning loans to collecting repayments and advances. It covers the entire lifecycle of a loan, leaving no room for guesswork.

IMPORTANT

The Credit Policy is the single most important internal document governing a bank's lending operations. It dictates how the bank manages its most critical asset: its loan portfolio.

Types of Credits

Banks extend credit to customers in various forms to suit different financial needs. Understanding these nuances is key to grasping how a bank operates daily:

- Cash Credit — A running account facility where the borrower can withdraw funds up to the sanctioned limit. This is typically used by businesses for working capital, allowing them to draw and repay continuously as their cash flow dictates.

- Overdraft — An arrangement allowing the customer to withdraw more than the account balance, up to a specified limit. Often linked to current accounts, it provides a crucial short-term safety net for immediate operational expenses.

- Demand Loan — A loan repayable on demand by the bank at any time. While less common for long-term needs, it gives the bank ultimate control over liquidity if urgent funds are required.

- Term Loan — A loan with a fixed repayment schedule over a specified period (short, medium, or long term). This is the standard structure for financing significant assets like machinery, vehicles, or real estate, where returns are generated over years.

- Additional services: Beyond direct funding, banks provide crucial non-funded support that facilitates business:

- Letter of Credit (LC) — A guarantee of payment issued by the bank on behalf of a customer. Vital for international trade, it ensures sellers get paid once they meet the shipping conditions, substituting the bank's creditworthiness for the buyer's.

- Bank Guarantees — A promise by the bank to cover a loss if a borrower defaults. Used widely in government contracts and large projects to assure performance or financial capability.

- Co-acceptances — Where a bank adds its commitment to a bill of exchange, guaranteeing its payment on the due date and greatly enhancing its acceptability in the market.

Credit Delivery

- Credit is delivered mainly via bank branches, which remain the primary channel for loan distribution. The local branch manager and their team bring invaluable local knowledge and relationship-building to the lending process.

- Other emerging channels include digital lending platforms, fintech partnerships, and centralised processing centres. Modern banking is rapidly migrating toward these efficient models, using data analytics for faster, standardized loan approvals.

Bank's Customers

- Bank customers can be individuals, partnerships, or companies (corporate entities). From a small personal loan to a massive corporate syndication, the policy must cater to all scales.

- They are located in various regions — urban, semi-urban, and rural areas. This geographic diversity requires a policy that understands varied economic realities, from agricultural cycles to urban industrial demands.

Credit Policy Document

The Credit Policy document is a critical internal reference that keeps the entire massive machinery of a bank aligned. It ensures that every loan officer is singing from the same sheet music:

- Ensures alignment with regulatory standards set by the Reserve Bank of India (RBI) and other regulatory bodies. Ignoring these can lead to massive penalties or even license revocation.

- Adheres to the bank's internal risk profiles and risk appetite framework. Every bank decides how much risk it's willing to take; the policy enforces this boundary.

- Aims for a quality credit portfolio — minimising non-performing assets (NPAs) while maximising healthy loans. A good policy is the first line of defense against bad debts.

- Seeks profitability for the bank through optimal pricing and risk management. Loans must not only be safe but also priced high enough to cover the inherent risks and generate shareholder value.

- Acts as a manual for credit/loan officers to follow while processing, sanctioning, and monitoring loans. It is the daily guidebook that answers "Can we do this deal? And if so, how?"

Objectives of Credit Policy

The primary objectives are strategically designed to keep the bank thriving:

- Balance credit volume, earnings, and asset quality. It's easy to grow a loan book if you ignore quality; the real challenge is growing safely and profitably.

- Follow regulatory guidelines and the bank's corporate goals simultaneously. A dual mandate of compliance and commercial success.

- Prioritize steady profit growth alongside continuous asset quality monitoring. Profitability cannot come at the cost of tomorrow's stability.

Overall Essence

- The policy is the bank's method for sanctioning, managing, and overseeing credit risks. It replaces arbitrary decisions with a structured, scientific approach to lending.

- It focuses on building effective systems and controls that ensure loans are safe, profitable, and compliant.

Policy Framework

Credit Policy Overview

- Definition: A formal bank statement on its credit objectives, laying out the bank's lending philosophy. It clearly dictates what kind of lender the bank wants to be.

- Approval: Set and approved by the bank's Board of Directors. It holds the highest executive weight.

- Purpose: Ensure full adherence to regulatory guidelines and proper risk management at every level of the hierarchy, from the front desk to the boardroom.

Primary Role of Credit Policy

The credit policy's primary role is to provide a safe operating environment:

- Ensure operations remain strictly within the set risk limits defined by the Board. If the board decides a maximum default rate is acceptable, the policy ensures loan officers don't exceed that threshold.

- Address the competitive and challenging market environment in which the bank operates. It gives staff the tools to compete safely without lowering standards excessively.

- Prevent deviations that might jeopardise the bank's profitability or long-term viability. A single rogue branch ignoring policy can severely damage a bank's bottom line.

Clarity and Guidelines

A well-drafted credit policy must leave no room for fatal ambiguity:

- Set clear risk tolerances for credit officers at every level of the organization. Everyone must exactly know what they are, and are not, allowed to approve.

- Outline explicit steps for handling requests beyond the set risk levels. If a particularly lucrative but high-risk deal appears, there must be a known path to escalate it safely.

- Define the approval process for exceptions — typically routed via the Credit Risk Committee or another relevant authority. Exceptions are inevitable, but they must be managed collectively by senior experts, not individual officers.

Organizational Structure

- The policy clearly defines roles, responsibilities, and authorities in all credit functions. It answers the critical question: "Who has the power to sign off on this ₹50 Crore loan?"

- It places strong emphasis on the importance of risk management across the organization, making it everyone's responsibility, not just the risk department's.

Policy Adaptation

Credit policies are living documents that must evolve. They need to adapt to the real world, which is constantly changing:

- Address exceptions, new loan products, and any deviations from the standard framework. As new financial instruments are invented, the policy must expand to govern them.

- Require review by Risk/Credit Committee or Board for any major changes. This ensures that adaptations are strategically sound and culturally aligned.

- Be updated to:

- Introduce new products as market demands change (e.g., green energy financing).

- Reflect changes in risk factors (economic shifts, new sectoral risks, geographical issues).

- Incorporate new regulatory requirements issued by the RBI or other regulatory bodies.

Real-World Applicability

- Credit policies should be pragmatic for bank staff handling loans on a daily basis. They must work in the trenches, not just in the boardroom.

- They must avoid setting unrealistic expectations — policies that look good on paper but are impossible to follow in practice are counterproductive and actively encourage staff to find dangerous loopholes.

International Operations

- The Credit Policy may differ for branches located outside the home country. Global operations bring unique challenges.

- International branches operate under different regulatory regimes and may need adapted credit norms to comply with local laws while maintaining the parent bank's standards. A policy working in Mumbai might violate regulations in London or New York.

Contents of a Credit Policy

A comprehensive Credit Policy document typically includes several core components to ensure nothing is missed:

1. Purpose and Contents

- Clearly defines the policy's goals — what the bank aims to achieve through its lending operations, setting the strategic north star.

- Reviews factors like the economy, regulatory concerns, and past bank performance to set the context for lending decisions. Lending does not happen in a vacuum; macroeconomic realities matter.

2. Objectives

The Credit Policy sets out specific, measurable objectives, including:

- Maintain and enhance asset quality — keep NPAs (Non-Performing Assets) low and recovery rates high. This is the bedrock of banking stability.

- Grow assets while managing risks — expand the loan book without compromising on quality. Growth without quality is an illusion.

- Secure a reasonable return on credit — ensure that the interest spread covers the risk undertaken. High risk must mean high reward.

- Achieve or maintain market share — stay competitive in the lending market against fierce modern rivals.

- Prioritize lending to certain sectors — align with national priorities (e.g., agriculture, MSME, infrastructure) as mandated by bodies like the RBI.

- Maintain a balance between fund-based (loans, overdrafts) and non-fund-based assets (LCs, guarantees). Non-fund based facilities earn fees without immediate cash outflow, improving return on equity.

- Highlight focus areas (e.g., Corporate, Retail, MSME) for better risk spread across segments. Diversification is the only free lunch in finance.

- Set targets for different asset terms and fee-based income generation. Pushing for processing fees and LC commissions boosts profitability safely.

- Establish minimum credit scores — borrowers must meet a threshold credit rating before they are even considered.

- Identify banned and restricted assets — certain sectors, like speculative real estate or environmentally harmful industries, may be strictly prohibited.

- Clarify the approach to risk premiums and pricing — precisely outlining how interest rates are dynamically set based on the calculated risk of the borrower.

3. Lending Authority & Responsibilities

- Details the powers of different credit authorities at various levels — from branch managers to regional heads to central committees. This creates a clear hierarchy of financial power.

- These powers can be further detailed in a "Delegation of Authority" document, a critical addendum that quantifies trust.

- Specifies approval limits for officers at different levels — e.g., a branch manager may sanction up to ₹50 lakh, while larger loans explicitly require zonal or head office approval. This prevents massive systemic failure from a single localized error.

4. Controlling Authority

- A higher authority continuously oversees and confirms all sanctions made at lower levels. This "four-eyes principle" is crucial for fraud prevention and error catching.

- Provides feedback or conditions on sanctions to ensure they strictly comply with the policy and broader economic view.

- Ensures adherence to the bank's lending guidelines and stated risk appetite.

5. Sign Off

- A designated credit officer confirms that every single loan proposal aligns perfectly with the credit policy before funds move.

- Verifies regulatory adherence and overall credit quality before final disbursement. They are the final gatekeepers.

- Seeks approvals for any unavoidable deviations from the standard policy norms.

6. Credit Denial and Recording

- Defines the procedure when a credit request is denied — the borrower must be formally informed of the reason, ensuring fair practices.

- Ensures that a record is kept for each refusal, maintaining transparency, building an audit trail, and providing data to refine future marketing and policy adjustments.

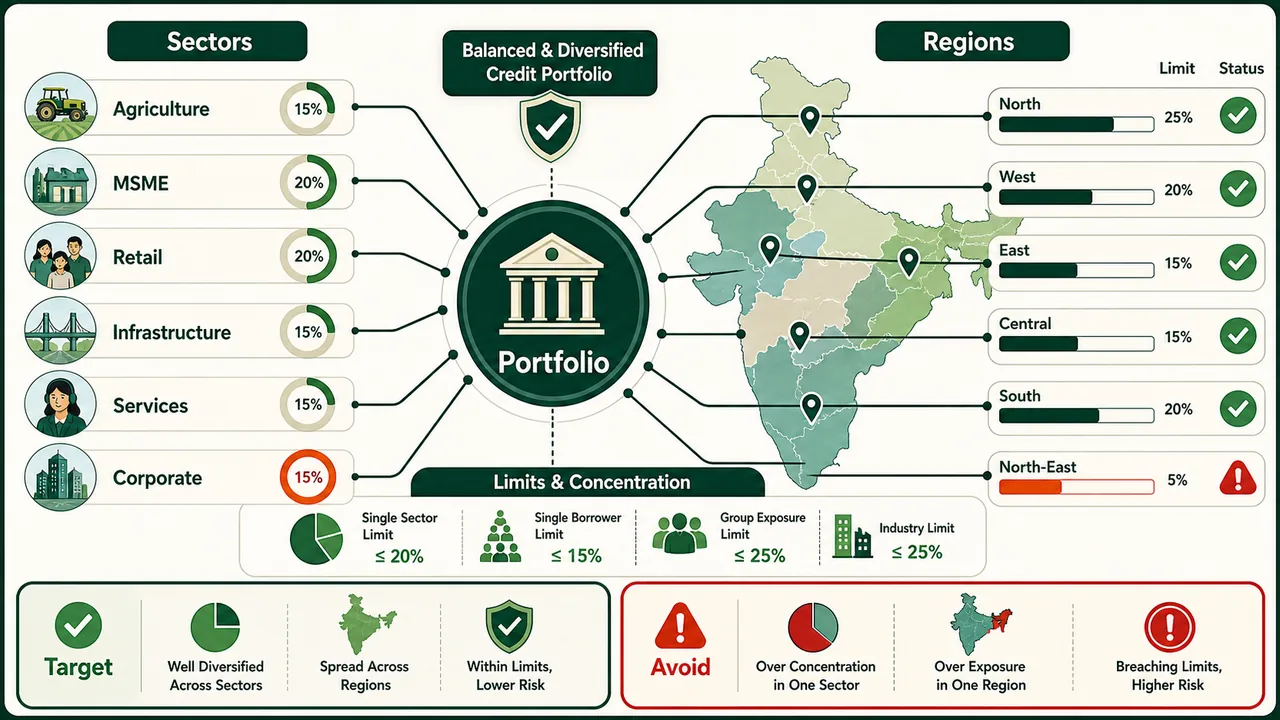

Portfolio Composition

The credit policy provides clear, strategic direction on how the bank's overall loan portfolio should be constructed to survive economic shocks:

- Specifies exposure levels to different sectors — dictating exactly how much lending is directed to agriculture, industry, services, retail, etc.

- Defines risk diversification across sectors and geographies — actively avoiding dangerous concentration in any single area. If one sector crashes, the bank must survive.

- Sets concentration limits based on the bank's capital and sectoral asset levels — no single sector or corporate group should ever dominate the portfolio to the point where their failure brings down the bank.

- Clarifies sectors to target and avoid — prioritizing sectors that align heavily with the bank's long-term strategy versus those currently deemed too risky.

Types of Loans

The credit policy elaborates on the mechanics of what the bank actually sells:

- Different loan forms and limits — defining structures for working capital loans, term loans, project finance, trade finance, retail loans, etc. Every product needs its own specific rules.

- Policy on loans to employees, officers, directors, etc. — outlining special terms, stringent limits, and absolute disclosure requirements for insider lending to prevent devastating conflicts of interest.

Appraisal Standards

Overview

The credit policy rigorously outlines the loan appraisal process — detailing exactly how every credit proposal is systematically evaluated before a single Rupee is sanctioned.

- Highlights the massive importance of evaluating financial strength and credit risk of each unique borrower.

- Differentiates between loans sourced through marketing (where the bank aggressively approaches the borrower) vs. walk-in customers (who approach the bank directly). The appraisal rigour and initial skepticism may strategically differ.

- Emphasizes absolute thorough credit quality and risk evaluation for every proposal, regardless of how the customer was sourced.

Development of Appraisal Standards

- These standards are rigorously developed based on deep historical experiences and scientific methodologies refined over decades of global banking practice.

- They are broadly divided into two crucial categories:

- Qualitative Standards — evaluating subjective, human, and intangible factors.

- Quantitative Standards — analyzing objective, data-driven financial metrics.

Qualitative Standards

Qualitative appraisal focuses heavily on critical factors that cannot be easily measured with simple numbers on a spreadsheet:

- Evaluate proposal viability and the bank's overall exposure to the borrower/group/sector — essentially asking, is the bank already dangerously overexposed to this entity's success or failure?

- Consider past dealings with the industry and the promoters — have they been reliable, honest, and competent in the past? Past behavior is a strong predictor of future performance.

- For new relationships, thoroughly review opinions from existing bankers, examine all available financial data, and mandatorily check credit bureau reports (like CIBIL).

- For new ventures, heavily weigh subjective impressions formed during discussions with promoters and meticulously evaluate their business network, practical experience, and verifiable track record in related fields. A strong promoter can often save a weak project, but a weak promoter will destroy a strong one.

Quantitative Standards

Quantitative appraisal uses hard financial data and specific ratios to objectively assess creditworthiness and repayment capacity:

1. Liquidity

- General benchmark: The expected Current Ratio (CR) is typically 1.33 (meaning current assets should be at least 1.33 times current liabilities). This provides a 25% margin of safety for short-term creditors.

- Flexibility is key — a CR dipping below the rigid benchmark doesn't immediately negate a good loan proposal.

- The appraiser must critically examine reasons for deviations (e.g., highly efficient inventory management can lower the CR artificially) and assess them in the overall, realistic context of the business operations.

2. Net Working Capital (NWC)

- Observe NWC movements critically over multiple periods — is the borrower's long-term working capital position steadily improving or rapidly deteriorating?

- Proactively suggest corrections for mismatches if NWC trends are severely unfavourable — the borrower may essentially need to bring in additional long-term capital to stabilize their operations before the bank risks its funds.

3. Financial Soundness

- This is evaluated based on the promoter's leverage — the critical ratio between the borrower's own funds (equity risking their own money) and borrowed funds (debt from banks).

- For massive industrial ventures, a standard debt-to-equity ratio of 3.0 is the general benchmark, though this can wildly vary depending heavily on the specific industry's capital intensity.

-

TIP

Note: The bank always calculates the Adjusted Tangible Net Worth (ATNW), cleverly excluding intangible assets (like goodwill) and artificial revaluation reserves, to see a much more realistic, conservative picture of the borrower's true wealth.

4. Turnover

- Analyze trends in turnover — carefully considering both quantity (volume) and value (revenue) over multiple consecutive years.

- Focus primarily on consistent or increasing output (quantity), irrespective of short-term price fluctuations. A fundamentally strong company may show lower revenue simply due to falling market prices, even though its actual production and market share volume has healthily increased.

5. Profits

- Use sustained net profit and real cash accruals as the absolute key indicators of long-term financial health. Profit is an opinion, but cash is a fact.

- Strictly exclude non-operating income (like the sudden sale of land, or one-time speculative gains) to ensure an accurate assessment of the business's actual core operational profitability.

- Monitor companies with consistent losses extremely carefully and immediately consider exit strategies — continued, blind lending to persistently loss-making entities massively increases dangerous NPA risk.

6. Credit Rating

- Always consider the bank's proprietary internal Credit Risk Assessment score for every borrower.

- Also thoroughly review any available external ratings from recognized agencies like CRISIL, ICRA, CARE, etc.

- External credit ratings should be used optimally if already available, but the bank should generally not insist on forcing smaller borrowers to get one solely for the appraisal — the immense cost and time may be entirely unnecessary and anti-competitive for smaller MSME borrowers.

7. Capital Markets

- For publicly listed companies, closely monitor daily share price movements — massive, significant, and sustained price drops often signal deep underlying corporate problems long before the balance sheet shows them.

- Compare with competitors operating in the same sector — is the borrower's stock severely underperforming relative to its direct peers?

- Observe response to public/rights issues — a remarkably poor subscription to equity offerings strongly indicates low general market confidence in the promoters.

- Ultimately, share price movements serve as a relentless, real-time indicator of corporate reputation among institutional investors and the broader financial market.

Specialized Lending Categories

Term Loans / DPGs (Deferred Payment Guarantees)

When comprehensively evaluating long-term loans and DPGs, the credit policy requires highly specific, stringent checks:

- Technical Feasibility: Massive projects must be rigorously vetted for both technical engineering feasibility and long-term economic viability. Sometimes, obtaining a completely independent second opinion from external technical experts is absolutely necessary.

- Promoters' Contribution: The bank typically demands a minimum 20% contribution in equity directly from the promoters, ensuring they have substantial "skin in the game" (though there is no fixed, universal benchmark across all projects).

- Debt Service Ratios: These are critical for long-term survival.

- Net DSCR (Debt Service Coverage Ratio) should ideally be comfortably above 2.

- Gross DSCR should be generally above 1.75.

- Security Margin: This is evaluated based on the broader Debt-to-Equity ratio. It is ideally targeted around 1.5:1, but generally not exceeding 2:1 for standard safety.

- Other Factors: Extremely careful consideration must be proactively given to the verified end-use of funds, the borrower's external credit rating, and the strategic implementation of automatic interest rate triggers if ratings fall.

Lending to NBFCs (Non-Banking Financial Companies)

Lending to NBFCs involves entirely distinct systemic risks, as they are lenders themselves, and follows highly specific regulatory guidelines:

- RBI Guidelines: Banks must completely and strictly follow all RBI master guidelines for lending to NBFCs to ensure the NBFC sector's orderly functioning and prevent massive systemic contagion risks.

- Registration with RBI:

- NBFCs properly engaged in Equipment Leasing, Hire Purchase, etc., can receive bank credit without a regulatory ceiling provided they are fully, properly registered formally with the RBI.

- Unregistered NBFCs:

- For unregistered entities, banks must carefully decide on lending based heavily on the specific purpose of the credit, the borrower's verifiable repayment capacity, and the bank's stringent internal risk perception.

- Limitations for RNBCs (Residuary Non-Banking Companies):

- Their overall finance access is strictly and legally capped to the absolute extent of their Net Owned Funds (NOF).

- Restricted Activities:

- Crucially, NBFCs should absolutely not be financed for highly speculative activities like investing in capital market shares or dangerously lending to their own corporate subsidiaries.

- Credit Risk for NBFCs:

- Given their remarkably distinct nature (functioning as financial intermediaries themselves), a entirely unique Credit Risk Assessment model is inherently required. Standard corporate models fail here.

- NBFC units rating anywhere below investment grade require strict, mandatory half-yearly reviews due to elevated risks.

Infrastructure Project Financing

Infrastructure projects are critically crucial for national development but carry extraordinarily unique risks due to their massive financial scale and multi-year long gestation periods.

- Specialized Departments: Due to its immense significance to the country's economic development, major banks have purposefully created specialized divisions exclusively dedicated to complex infrastructure financing.

- Infrastructure Sectors Include: Power generation, national roads, highways, major bridges, deep-water ports, international airports, heavy rail systems, massive water and sanitation systems, critical telecommunications, affordable housing, specialized industrial parks, and other core public facilities. (Note: This specific list is constantly updated by the CBDT in the official Gazette as necessary).

- Characteristics of Financing:

- Requires massive, unprecedented large capital requirements.

- Face extended development and extremely complex construction times (long gestation periods before any revenue is generated).

- Typically feature remarkably high debt ratios compared to standard manufacturing.

- RBI Guidelines on Infrastructure:

- To spur development, the RBI strategically removed previous absolute loan limits (which were previously ₹1000 cr. for power projects and ₹500 cr. for others, which proved too restrictive).

- Banks can now aggressively provide massive loans strictly governed under broader prudential exposure norms (dynamically linked to their expanding capital base).

- To facilitate mega-projects, banks may strategically and legally exceed the standard Single Borrower / Group exposure limit by 10% specifically if the funding is exclusively for approved infrastructure projects.

Long Tenor Loan Structuring (as per RBI 2014 & 2015 Guidelines)

To realistically accommodate the multi-decade life span of major infrastructure projects, the RBI introduced highly flexible but safe structuring rules:- Fundamental Viability: The bank must evaluate the project rigorously based on both financial and crucial non-financial metrics, prominently including a sustained, strong interest coverage ratio over decades.

- Amortization Schedule: Significantly allows for a much longer tenor amortization (e.g., stretching up to 25 years), deeply and realistically aligned with the project's actual physical useful life, featuring built-in, mandatory periodic refinancing options.

- Project Viability & Refinancing:

- Forward-looking banks can consider a project ultimately viable based on an average DSCR and other strict parameters mathematically stretched over a much longer period (like 25 years).

- However, the initial hard funding might firmly be sanctioned for a shorter term (such as 5 to 7 years), with distinct, conditional refinancing options made available immediately afterward.

- Refinancing Structure: Typically, every 5 years, strategic refinancing would be methodically executed, strictly based on adhering to the original, long-term 25-year amortization schedule.

Lease Finance Guidelines

If a bank actively engages in large-scale equipment or heavy machinery leasing:

- Typically, comprehensive full payment financial leases fundamentally focus on fully recovering the entire asset's capital cost plus interest within one single, binding lease term.

- Single Unit Lease Exposure: Risk limits are strictly and legally capped to the lesser of 50% of the highly-rated lessee's net worth OR ₹200 cr. specifically for the Public Sector and ₹100 cr. strictly for the Private Sector.

- A specific individual bank's financial contribution is rigidly capped at 25% for single massive projects solely involving complex machinery and heavy equipment leasing.

- Prudent banks aggressively strive for highly diversified lease portfolios widely spread across entirely different cyclic industries and highly varied equipment asset types.

- Banks actively participate in massive lease syndications directly collaborating with specialized organizations like IDBI and IL&FS, especially to fund massively high-value, critical assets like commercial aircraft.

- Overall cumulative lease exposure for any given commercial bank shouldn't broadly and systemically surpass 10% of its total global advances.

Non-Fund Based Limits & Syndication

LCs, Guarantees, & Bill Discounting

- Opening LCs & Issuing Guarantees: Banks actively open Letters of Credit (LCs), aggressively issue performance guarantees, and readily discount trade bills specifically and exclusively for genuine, verified trade transactions of officially sanctioned borrowers.

- Avoid Front Companies: Banks must strictly and diligently avoid discounting complex bills originating from obscure front finance companies that secretly belong to large, over-leveraged industrial groups attempting to bypass credit limits.

- Service Sector Bills: Ensure that actual, verifiable services have been securely and completely rendered when actively discounting tricky service sector bills. Banks must absolutely and rigorously avoid accommodation bills (which are essentially fraudulent bills drawn without any actual, underlying exchange of goods or services).

Guarantees and Co-Acceptances

- Banks can securely and profitably issue guarantees for large loans prominently provided by other Financial Institutions (FIs) or competing banks.

- Banks can also readily and safely provide immediate credit facilities directly against explicit, strong guarantees formally received from other highly-rated banks or FIs.

WARNING

Crucially, the massive exposure stemming from these guarantees directly and mandatorily counts towards the bank's strict internal exposure limits on those exact other banks or FIs. Continuous, regular board-level reviews explicitly establish and aggressively monitor these critical sub-limits.

Loan Syndication

- There is an expected, ongoing massive global growth in loan syndication, especially structured for colossal, multi-billion dollar infrastructure projects, strategically spreading the massive risk among many participating banks.

- When a single, massive bank can't or prudently won't absolutely finance a massive project fully due to strict internal exposure limits, the remaining necessary massive finance is intelligently syndicated among several other participating lenders.

- The original initiating lead bank can powerfully and profitably manage the entire complex syndication independently (earning massive fee income) or actively collaborate with other specialized investment banking firms.

Risk Management & Administration

Risk Management Policies

- Forex Risk Hedging:

- The RBI rigidly and legally requires all authorized banks to firmly establish a completely separate, comprehensive 'Hedging Policy' that must be officially and annually approved by the bank's board of directors.

- Volatile Forex loans (typically those up to USD 5 Million) should be actively and mandatorily hedged by the borrowing corporation unless they possess proven, highly verifiable uncovered forex receivables (like confirmed export orders) to naturally and safely offset the massive currency risk.

- Fair Practices Code (FPC):

- Modern bank operations boldly aim for absolute, undeniable transparency and total fairness throughout the entire loan processing journey for every customer.

- Requires strict, audited adherence to RBI master guidelines specifically for formally, promptly acknowledging and processing all loan applications without discrimination.

- Risk Policy Specifics:

- The overarching Credit Policy explicitly and clearly must specify the bank's overall accepted systemic risk levels to regulators and shareholders.

- Powerful, mathematical tools utilized for highly sophisticated risk measurement like VAR (Value at Risk) or complex Duration analysis might effectively and prominently be mentioned as standard practice.

- Example: A highly conservative bank may proactively set a strict '3-duration' explicitly for certain critical, highly volatile investment portfolios.

Documentation & Operations

- Documentation & Waivers:

- Massive loans must invariably be disbursed strictly only after all complex documentation and legal security perfection are totally and undeniably complete.

- Rare, unavoidable exceptions are sometimes quietly allowed, provided there is a remarkably proper, extensively detailed official internal record justifying the risk.

- The specific authority empowered for massive waiver approval should invariably be strictly higher than the original loan sanctioning authority to prevent localized corruption.

- Loan Administration:

- Banks must meticulously and flawlessly maintain perfectly detailed, legally binding loan records (or a master loan register).

- The strict policy governing Loan-file requirements/maintenance/administration clearly indicates this specific, absolute need. Many massive larger banks have heavily staffed, dedicated Loan Administration Departments specifically solely for this critical purpose.

- Loan Loss Provision:

- Extremely proper, aggressive provisioning for bad, defaulted loans is usually an integral, mandatory part of formal, audited accounting disclosures.

- It strictly and legally follows RBI master guidelines for swift, honest loan loss recognition and proper, adequate provisioning to protect depositors.

Portfolio Monitoring & Evolution

Ongoing Portfolio Management

- Loan Grading/Credit Scoring: This is universally considered one of the absolute key, fundamental components contained within a modern credit policy.

- All massive loans are heavily, mathematically graded/scored precisely based on firmly set, objective parameters.

- Dynamic Loan Pricing is intrinsically and automatically linked directly to these resulting, evolving scores/ratings. (Better rating = lower interest rate).

- Loan Review & Renewal:

- The policy contains remarkably firm, explicit, and unyielding guidelines on specifically when and exactly how an existing loan must be thoroughly reviewed.

- Strict, unyielding policies are fully in place solely for the safe, conditional renewal of various ongoing, massive credit facilities.

- Highly specific penal instructions must be religiously followed specifically for handling dangerous, unaccepted delays in receiving audited Financial Statements from the major borrower.

- Charged Off Accounts:

- The policy also remarkably contains highly granular, aggressive details specifically for aggressively recovering bank dues from formally accounting written-off accounts.

NOTE

Writing off a loan is an accounting entry that cleanly removes the bad asset from the balance sheet, but it absolutely does not extinguish the borrower's legal liability to pay. Recovery efforts must continue relentlessly.

Credit Policy Evolution

A massive bank's Credit Policy is absolutely not a static, dead document; it constantly and aggressively adapts to the real world:

- It proactively, strategically adjusts with time primarily due to driving, massive macro factors remarkably like sweeping global economic liberalization and rapid globalization.

- It effectively and aggressively aims to swiftly seize new, highly profitable market opportunities while seamlessly and safely meeting necessary, mandated commercial and critical social goals.

- Ultimately, a highly evolved policy securely and decisively protects the bank's top market ranking by ensuring long-term systemic institutional safety and steady, massive profitability.

Role of Credit Policy

- Formal vs. Informal Policy:

- Global regulators now totally insist on the explicit formulation of a highly documented, formal credit policy nowadays primarily to securely maintain overall national asset quality.

- Historically, older banks relied heavily on vague, informal guidelines focusing broadly on asset quality preservation, ensuring some growth and risk-adjusted returns, market share retention/enhancement, and general emphasis on priority sector loans and export credit. This proved disastrously inadequate.

- Not having explicitly laid down, written procedures (or the dangerous absence of formal, binding procedures) directly caused significant, massive systemic banking problems and massive bailouts in the past.

WARNING

Crucially, without a strictly documented credit policy firmly approved by the ultimate Board of Directors, banks faced massively higher, unquantifiable Credit Risk.

- A comprehensive, Written Credit Policy, which the Board of Directors should fully debate and unanimously approve, is the single factor absolutely essential for the proactive, strategic management of future devastating risk events.

MIS and Review Mechanisms

Board's Role in Credit Review

The Board isn't just a rubber stamp; they have active, massive oversight duties:

- Regularly and critically assess the total credit portfolio to ensure ongoing, verifiable financial health.

- Ensure absolute, strict compliance with all major credit policy covenants.

- Continuously and aggressively monitor if the massively disbursed credit actually, factually contributes to expected, high shareholder profits.

- Promptly and thoroughly investigate deep reasons for any major policy violations or dangerous profit shortfalls.

- A highly sophisticated, well-structured MIS (Management Information System) is absolutely legally required for the Board to quickly and review the massive credit portfolio effectively.

Frequency of Review

- The overarching Credit Policy of a massive bank should be periodically, strategically revised to successfully achieve its intended, evolving economic objectives.

- However, a strict requirement for regular, scheduled review absolutely does not imply frequent, chaotic, or capricious changes in major, fundamental policy aspects.

- Core mathematical policy elements like fundamental Risk estimation and rigid accounting standards should absolutely NOT be changed frequently. Banks must actively, aggressively avoid changing them with a dangerous short-term view to hide losses, as this totally undermines long-term systemic stability.

- Review Emphasis: The absolute primary focus of the annual Credit Policy review must be strictly on critically assessing realistic Credit performance and flawlessly ensuring all recent, mandatory Regulatory changes are properly, seamlessly incorporated.

Conclusions

The Credit Policy's Core Function

- The master Credit Policy is the overarching, supreme document that proactively and clearly defines the strategic thrust areas in relation to the bank's entire credit culture and all regulatory directions.

- A deeply key strategic feature of a Credit Policy is aggressively managing the overall, massive Portfolio composition to prevent fatal concentration risk.

- The Credit Policy fundamentally and crucially serves as the massive bank's ultimate, unyielding "Gate Keeping" function, pertaining directly to ensuring absolute adherence to the Credit Policy rules by all staff.

- A strong Credit Policy effortlessly helps maintain a delicate, highly profitable balance between massive Credit volumes, high earnings, and stellar asset quality.

- While it focuses intensely on maximizing earnings, pristine asset quality, and total regulatory compliance, blindly maximizing the sheer number of loans disbursed is explicitly and fundamentally not a main objective. Quality always overrides quantity.

- The Credit Policy is also the primary, audited mechanism that ensures the massive bank actively, provably meets its mandated national social responsibilities.

- The Credit Policy actively, scientifically defines the highly acceptable levels of risk by formally, clearly identifying specific industry segments for massive new exposures.

- The rigorous credit policy actively and automatically prevents fatal risk concentrations through forced diversification by mathematically setting strict exposure limits on sectors and massive single transactions.

- The master Credit Policy directly provides highly strategic, dynamic pricing strategies through the mandatory use of the proprietary Credit Risk Rating framework.

Success Factors

- The ultimate success of any brilliant Credit Policy largely, entirely depends on its deep, practical understanding by every single one of the bank's officials.

- Every single individual remotely involved in lending, specifically including both frontline Credit/Loan Officers and the elite Management of the Bank, must strictly, undyingly adhere to the Credit Policy. The daily, complex job of aggressively marketing and/or rigorously appraising of massive loans specifically and heavily falls to diligent Credit/Loan Officers.

- While strict procedures and rigid rules are massively important, deep, fundamental banking Knowledge serves undoubtedly as the most potent, ultimate real-world risk mitigant.

- Board's Ultimate Responsibility: The Board is the ultimate entity that should strictly, legally ensure the complex Credit Policy is genuinely well understood by all the bank officials globally. To firmly, absolutely avoid dangerous misunderstandings, the written policy must be exceptionally clear, extremely well-articulated, and highly user-friendly, intentionally and actively avoiding useless official bureaucratic language that's dangerously hard to interpret.

- Ideal Policy Traits: An absolutely ideal, world-class credit policy should holistically and relentlessly focus on all of the following critical traits:

- Simultaneously Prioritize massive business growth AND flawlessly maintain pristine asset quality. The Board alone makes absolutely sure that the Credit Policy creates the exact right internal atmosphere to miraculously achieve this massive growth safely.

- Legally and flawlessly guaranteeing absolute, strict Regulatory compliances and total statutory adherence at all times.

- Offering a remarkably solid, virtually immovable robust foundation for highly comprehensive, proactive Credit Risk Management with very clear, established, unyielding procedures.

Summary

The Bank Credit Policy is a massive, comprehensive, Board-approved master document that totally governs absolutely every single aspect of a massive bank's entire lending operations. It covers:

| Component | Purpose |

|---|---|

| Policy Framework | Systematically sets clear objectives, roles, strict risk tolerances, and vital adaptability mechanisms |

| Contents | Clearly defines core objectives, strict lending authority, mandatory sign-offs, and rigorous denial recording |

| Portfolio Composition | Strategically manages massive sector exposure, forced diversification, and strict, mathematical concentration limits |

| Appraisal Standards | Unyieldingly establishes both subjective qualitative and mathematical quantitative assessment criteria |

| Qualitative Standards | Subjectively evaluates promoter background, deep industry experience, and powerful business network strength |

| Quantitative Standards | Mathematically analyses absolute liquidity, NWC, leverage ratios, turnover trends, real cash profits, credit ratings, and live market signals |

IMPORTANT

Key Takeaway: The Credit Policy is absolutely not merely a dead compliance document — it is the massive bank's ultimate, living operational blueprint for safe, highly profitable, and eternally sustainable lending. Every single credit officer must understand it deeply and follow it meticulously without fail.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Credit Policy (Loan Policy) | Comprehensive Board-approved document governing all credit functions — sanctioning, monitoring, collecting |

| Created by | Bank's Board of Directors; highest level of governance |

| Goal | Customer service excellence, stakeholder satisfaction, employee clarity, regulatory compliance |

| Types of credit | Cash Credit (running a/c), Overdraft (beyond balance), Demand Loan (repayable on demand), Term Loan (fixed schedule); Non-fund: LC, Bank Guarantee, Co-acceptance |

| Credit delivery | Primarily via bank branches; also digital platforms and centralized processing centres |

| Key objectives | Balance credit volume + earnings + asset quality; follow RBI guidelines; prioritize profit growth with asset quality |

| Policy framework | Formal statement of credit objectives; sets clear risk tolerances at every level; defines approval process for exceptions via Credit Risk Committee |

| Policy adaptation | Living document; reviewed by Board/Risk Committee; updated for new products, risk factors, regulatory changes |

| Contents of Credit Policy | Purpose, objectives, lending authority, controlling authority, sign-off process, credit denial recording |

| Lending authority | Branch manager may sanction up to a limit (e.g., ₹50 lakh); larger loans need zonal/head office approval; detailed in Delegation of Authority document |

| Portfolio composition | Defines sector exposure levels, geographic diversification, concentration limits based on capital |

| Qualitative appraisal | Promoter background, past dealings, business network, CIBIL/credit bureau checks for new relationships |

| Quantitative standards | Current Ratio benchmark: 1.33; NWC trends; Debt-to-Equity ratio: 3.0 (industrial); turnover trends; net profit & cash accruals; internal + external credit ratings |

| Adjusted Tangible Net Worth (ATNW) | Excludes intangibles (goodwill) and revaluation reserves for a realistic picture of borrower's true wealth |

| Capital market signals | Monitor share price movements of listed borrowers; compare with peers; poor rights issue subscription = low confidence |

| Term Loan appraisal | Promoter contribution typically ≥ 20% equity; Net DSCR > 2, Gross DSCR > 1.75; Debt-to-Equity ideally 1.5:1, max 2:1 |

| Lending to NBFCs | RBI-registered NBFCs: no regulatory ceiling; unregistered: based on purpose, repayment capacity, risk perception; RNBCs capped at Net Owned Funds |

| NBFC restrictions | Cannot finance NBFCs for capital market investment or lending to their own subsidiaries; below investment-grade NBFCs need half-yearly reviews |

| Infrastructure financing | No absolute loan limits (previously ₹1000 Cr power / ₹500 Cr others); banks may exceed single/group exposure limit by 10% for approved infra projects |

| Lease finance | Single unit capped at lesser of 50% of lessee's net worth or ₹200 Cr (public) / ₹100 Cr (private); bank's contribution max 25% per project; total lease exposure max 10% of global advances |

| Non-fund based (LCs, guarantees) | Only for genuine trade transactions; avoid front companies; avoid accommodation bills; exposure counts toward limits |

| Risk management | Forex loans (up to USD 5M) must be hedged; Fair Practices Code for transparency; VAR/Duration analysis |

| Documentation | Disburse only after full documentation; waiver authority must be higher than sanctioning authority |

| Loan grading / pricing | All loans graded/scored on objective parameters; pricing linked to credit rating (better rating = lower rate) |

| Review frequency | Periodic review; core risk estimation and accounting standards should NOT change frequently; focus on credit performance + regulatory changes |

| Board's role | Assess portfolio health, ensure compliance, investigate violations, review via MIS; ensure policy is clear and well-understood by all officials |

| Gate-keeping function | Credit Policy prevents concentration risk, ensures diversification, sets sector exposure limits, defines pricing strategies |

| Success factors | Deep understanding by all officials (credit officers + management); knowledge is the most potent risk mitigant; policy must be clear, avoiding bureaucratic language |

Lesson Doubts

Ask questions, get expert answers