📊 Lending Rates

Learn about different lending rates, benchmark rates, and interest rate determination in banking.

The Evolution of Lending Rates

- BPLR (Benchmark Prime Lending Rate) - April 2003: An older system where banks set rates based on their "prime" customers. It lacked transparency.

- Base Rate - 01.10.2010: Introduced to ensure banks didn't lend below a certain cost, but banks were still slow to pass on rate cuts to customers.

- MCLR (Marginal Cost Based Lending Rate) - 01.04.2016: Introduced to make interest rate calculations more scientific and responsive to RBI policy changes.

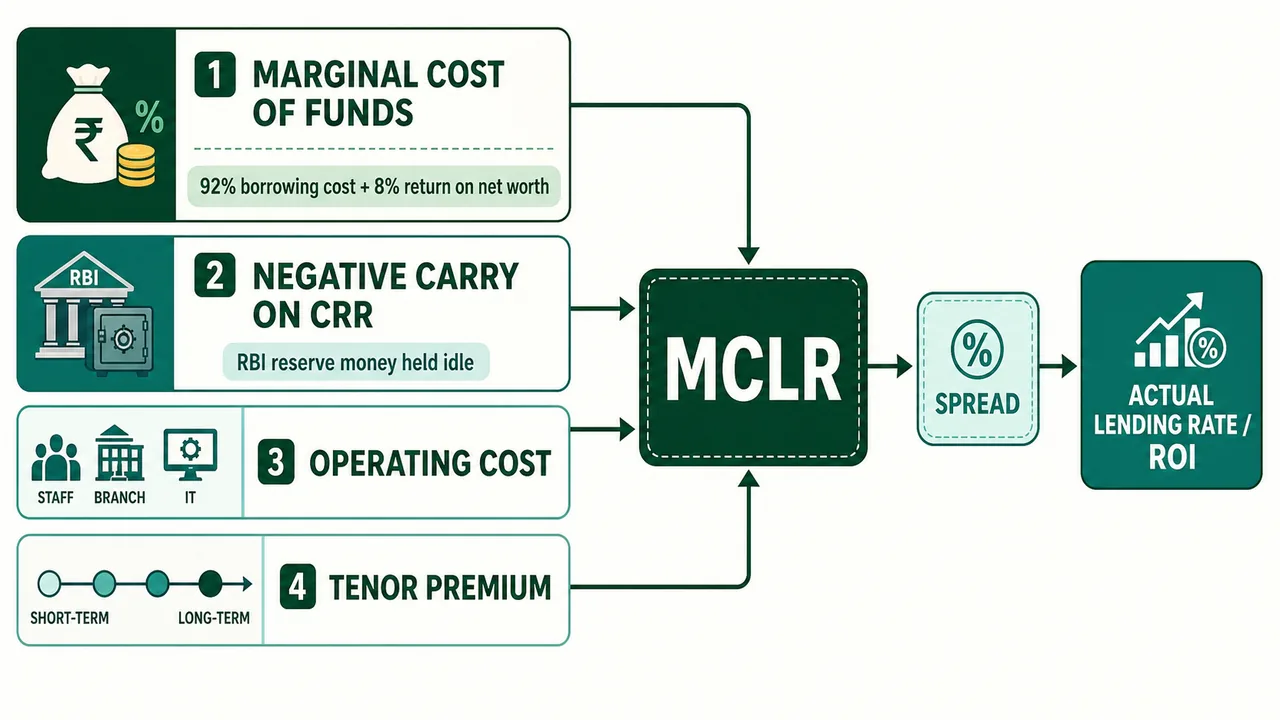

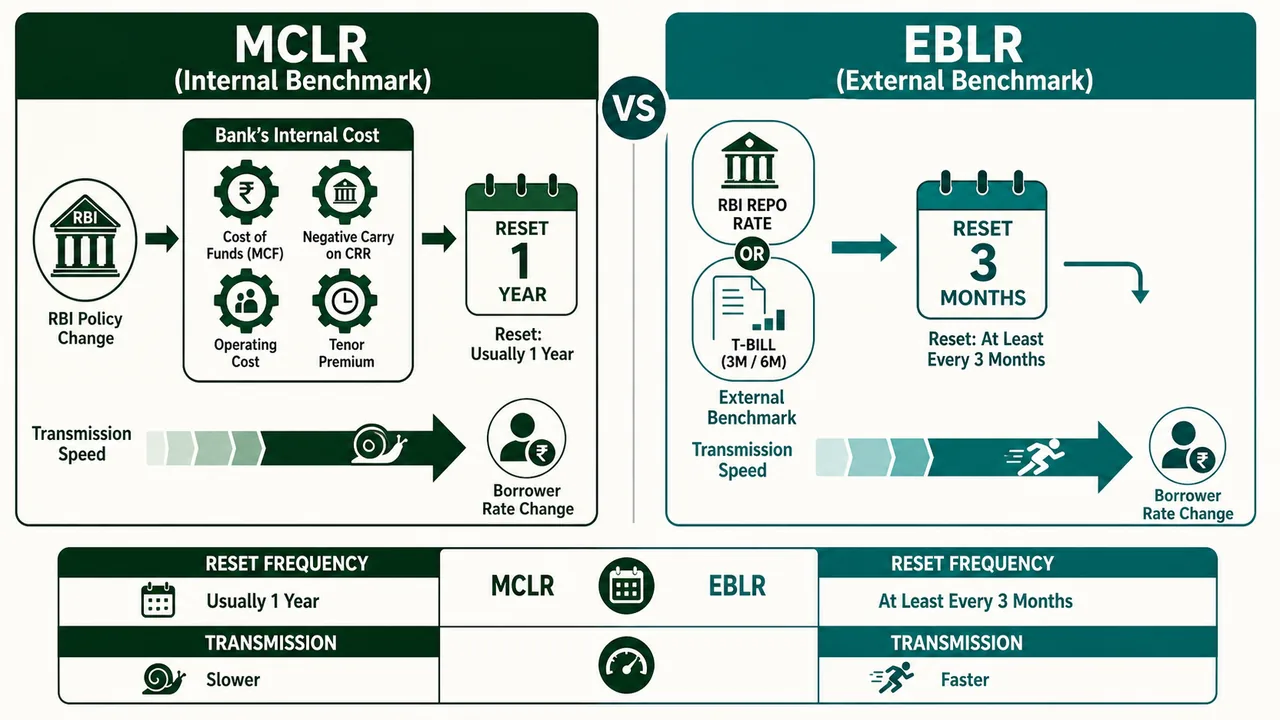

MCLR (Marginal Cost Based Lending Rate)

MCLR is an internal benchmark, meaning the bank calculates it based on its own costs. It has four distinct components.

1. Marginal Cost of Funds (MCF)

This is the most significant component. It represents the cost the bank incurs to get new funds (deposits/borrowings). It is a weighted average:

- Marginal Cost of Borrowing: The interest the bank pays on new deposits (Savings/FDs).

- Return on Net Worth: The profit the bank expects to make on its own capital.

- The Formula: MCF = 92% x Marginal Cost of Borrowing + 8% x Return on Net Worth

2. Negative Carry on CRR

- Context: Banks must keep a certain percentage of their deposits with the RBI as Cash Reserve Ratio (CRR). The RBI pays zero interest on this money.

- The Cost: Since the bank cannot lend this money or earn interest on it, it is a "dead loss" or "negative carry."

- Result: The bank charges this cost to the borrower to recover the loss.

- Negative Carry = Required CRR x Marginal Cost / (1 – CRR)

3. Operating Cost

This covers the bank's day-to-day expenses required to provide loan products. It includes salaries, rent, and IT infrastructure charges.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

The Evolution of Lending Rates

- BPLR (Benchmark Prime Lending Rate) - April 2003: An older system where banks set rates based on their "prime" customers. It lacked transparency.

- Base Rate - 01.10.2010: Introduced to ensure banks didn't lend below a certain cost, but banks were still slow to pass on rate cuts to customers.

- MCLR (Marginal Cost Based Lending Rate) - 01.04.2016: Introduced to make interest rate calculations more scientific and responsive to RBI policy changes.

MCLR (Marginal Cost Based Lending Rate)

MCLR is an internal benchmark, meaning the bank calculates it based on its own costs. It has four distinct components.

1. Marginal Cost of Funds (MCF)

This is the most significant component. It represents the cost the bank incurs to get new funds (deposits/borrowings). It is a weighted average:

- Marginal Cost of Borrowing: The interest the bank pays on new deposits (Savings/FDs).

- Return on Net Worth: The profit the bank expects to make on its own capital.

- The Formula: MCF = 92% x Marginal Cost of Borrowing + 8% x Return on Net Worth

2. Negative Carry on CRR

- Context: Banks must keep a certain percentage of their deposits with the RBI as Cash Reserve Ratio (CRR). The RBI pays zero interest on this money.

- The Cost: Since the bank cannot lend this money or earn interest on it, it is a "dead loss" or "negative carry."

- Result: The bank charges this cost to the borrower to recover the loss.

- Negative Carry = Required CRR x Marginal Cost / (1 – CRR)

3. Operating Cost

This covers the bank's day-to-day expenses required to provide loan products. It includes salaries, rent, and IT infrastructure charges.

4. Tenor Premium

- Concept: Lending money for a longer time is riskier than lending for a short time.

- Application: A 1-year loan will have a lower interest rate than a 15-year home loan. The "Tenor Premium" adds extra percentage points for longer loan durations.

MCLR Formula: MCLR for a specific maturity = (1) + (2) + (3) + Tenor Premium

MCLR Implementation Rules

- Publishing: Banks must publish MCLR for different durations (Overnight, 1-Month, 3-Month, 6-Month, 1-Year).

- Actual ROI: Actual ROI = MCLR + Spread (The "Spread" is the bank's profit margin based on your credit risk).

- Review: Banks must review and publish their MCLR every month.

- Reset Period: Typically one year. Your rate is locked for that year, regardless of market changes.

- Exemptions: Govt schemes (DIR), Loans against deposits, Staff loans, Fixed-rate loans (> 3 years).

Use of External Benchmarks (EBLR)

Effective 01.10.2019, the RBI introduced External Benchmarks to remove the bank's internal calculation from the equation for certain loans.

Key Rules

- Applicability: Mandatory for all new floating rate Personal/Retail loans (Housing, Auto) and loans to MSMEs.

- The Benchmarks: Banks must link the loan to one of the following:

- RBI Repo Rate (RLLR) - Most common.

- 3-Month or 6-Month GOI Treasury Bill yield (published by FBIL).

- Spread Rules: Banks can add a "Spread" but cannot change it for 3 years unless the borrower's credit score changes.

- Reset Period: Must reset at least once every 3 months (Quarterly).

- Transition: Existing borrowers on MCLR/Base Rate can switch to EBLR (usually for a fee).

- Fixed Rate Loans: Interest rate on fixed rate loans (< 3 years maturity) shall not be less than benchmark rate for similar tenor.

Summary: MCLR vs EBLR

| Feature | MCLR (Internal Benchmark) | External Benchmark (EBLR) |

|---|---|---|

| Basis | Bank's internal costs (MCF + Ops cost) | External Market Rates (Repo Rate/T-Bills) |

| Transparency | Lower (Complex calculation) | High (Publicly available data) |

| Reset Period | Usually 1 Year | At least once every 3 months |

| Transmission | Slow (Bank decides when to change) | Fast (Linked directly to RBI/Market) |

Loan Against Shares and Securities

A. Statutory Restrictions (Banking Regulation Act)

- Holding Limits (Section 19(2) B R Act): A bank cannot hold more than 30% of PAID-UP CAPITAL + RESERVES of the bank OR 30% of PAID-UP CAPITAL of the company (whichever is lower).

- Own Shares (Section 20(1) B R Act): Banks are strictly prohibited from granting loans against the security of their own shares.

B. Loans to Individuals

Limits for loans against shares/debentures/mutual funds:

| Security Type | Maximum Loan Amount | Minimum Margin |

|---|---|---|

| Demat Shares (Electronic) | ₹ 20 Lakh | 25% |

| Paper Shares (Physical) | ₹ 10 Lakh | 50% |

C. Loans to Brokers

- Bank Guarantees: 50% margin required (IMPORTANT: 25% must be in cash).

- Prohibition on "Badla": Banks cannot finance carry-over transactions.

D. Other RBI Restrictions

Banks are forbidden from financing:

- Loans against Deposits of Other Banks: To prevent fraud using fake receipts.

- Loans against Certificate of Deposit (CD): CDs are tradable liquid instruments; lending creates a "money loop".

- Loans for Buy-back of Shares: Companies must use their own free reserves/securities premium for buy-backs.

Loans to Bank Directors

A. Directors of the Same Bank

- Rule (Section 20(1) B R Act): A bank cannot grant loans to its own directors or firms where they have an interest.

- Exemptions: Loans against Government Securities, Life Insurance Policies, Fixed Deposits, or Staff Loans.

B. Directors of OTHER Banks

- Loans below ₹5 Crore: Sanctioned by appropriate authority; reported to Board.

- Loans ₹5 Crore and above: Must be sanctioned directly by the Board of Directors.

- Major Shareholder: Person holding 10% or more capital OR ₹5 Crore in paid-up shares.

C. Write-offs (Section 20A B R Act)

Loans to directors cannot be written off without explicit RBI permission.

Miscellaneous Policy Issues

- Transfer of Loan Accounts: Existing bank must convey decision (approval/rejection) within 15 days.

- Legal Audit of Title Deeds: Mandatory for loans ₹5 Crore and above.

- Valuation of Property: For property valued ₹50 Crore or above, valuation must be obtained from at least 2 independent valuers.

- Undertaking from Borrower: New borrowers must declare existing loan facilities with other banks.

- Return of Security Documents: Must be returned within 15 days of loan repayment/closure.

- Passport Copies: Mandatory for directors/promoters if exposure > ₹50 Crore.

Loan to Value (LTV) Ratio for Home Loans

LTV Formula: LTV = Loan Amount / Cost of House × 100

Maximum LTV Limits

| Loan Amount Category | Maximum LTV Ratio | Down Payment Required |

|---|---|---|

| Up to ₹30 Lakh | Max 90% | 10% |

| > ₹30 Lakh up to ₹75 Lakh | Max 80% | 20% |

| Above ₹75 Lakh | Max 75% | 25% |

- Stamp Duty Exception: For houses costing up to ₹10 Lakh, stamp duty and registration charges can be included in the "Cost of House".

- Usage: LTV is linked to Risk Weights (RW) for Capital Adequacy Ratio (CAR) purposes.

Reporting to CRILC

CRILC = Central Repository of Information on Large Credits — set up by RBI in 2014 to collect, store, and disseminate credit data on large borrowers. It helps RBI and banks monitor concentration risk and early signs of stress across the banking system.

1. Who Reports to CRILC?

- Scheduled Commercial Banks (SCBs) — all banks must report borrowers with aggregate fund-based and non-fund-based exposure of ₹5 Crore and above

- Primary (Urban) Cooperative Banks (UCBs) — UCBs with total assets of ₹500 Crore and above (as on 31st March of the previous year) must report exposures of ₹5 Crore+. They submit via the XBRL platform, quarterly, within 30 days of quarter-end.

- NBFCs — must also report to CRILC. Failure to report leads to accelerated provisioning and supervisory actions by RBI. Borrowers who refuse to share information can be classified as non-cooperative borrowers.

2. CRILC-Main Report

Submitted quarterly, within 21 days of the quarter close, the CRILC-Main return has 4 sections:

| Section | What is Reported |

|---|---|

| Section 1 | Exposure to large borrowers (₹5 Cr+ aggregate) |

| Section 2 | Technically written-off accounts |

| Section 3 | Balance in current account (debit/credit of ₹1 Crore and above) |

| Section 4 | Non-cooperative borrowers |

NOTE

UCB CRILC return has 3 sections (same as above minus Non-cooperative borrowers section).

3. SMA (Special Mention Account) Classification

Banks must report the SMA status of borrowers to CRILC. SMA classification is based on days past due (DPD):

| SMA Category | Days Overdue | Significance |

|---|---|---|

| SMA-0 | 1–30 days | Early stress signal |

| SMA-1 | 31–60 days | Moderate stress |

| SMA-2 | 61–90 days | High stress — triggers resolution framework |

- CRILC-SMA 2 reporting is done on an "as and when" basis — i.e., the moment an account becomes overdue for 61 days (SMA-2), it must be reported immediately.

- Weekly SMA reporting (every Friday) for borrowers with exposure ≥ ₹5 Crore.

- SMA-2 assets can be sold to Securitisation Companies (SCs) / Reconstruction Companies (RCs).

4. LEI (Legal Entity Identifier)

LEI is a 20-digit alphanumeric code that uniquely identifies legal entities participating in financial transactions. It is mandatory for corporate borrowers with aggregate exposure of ₹5 Crore and above. Banks must obtain and report LEI for such borrowers in CRILC submissions.

5. Red Flagged Accounts (RFA)

- Exposure ≥ ₹50 Crore with Early Warning Signals (EWS) of fraud.

- Reported immediately/weekly.

Summary of CRILC Reporting

| Category | Threshold | Reporting Frequency |

|---|---|---|

| CRILC-Main (Large Loans) | ₹5 Cr+ | Quarterly (within 21 days) |

| Current Account Balances | ₹1 Cr+ | Quarterly (in CRILC-Main) |

| SMA-2 (61+ days overdue) | ₹5 Cr+ | As and when basis |

| Weekly SMA | ₹5 Cr+ | Weekly (Fridays) |

| Red Flagged (Fraud Risk) | ₹50 Cr+ | Immediate/Weekly |

| UCBs (assets ≥ ₹500 Cr) | ₹5 Cr+ | Quarterly (within 30 days, via XBRL) |

Summary Questions

- Which loans can be granted to same bank directors?

- Against Govt securities, FD, LIP, Credit Cards.

- Who sanctions loans of ₹30 Lac to a director of another bank?

- Appropriate authority (Credit Committee) with reporting to Board.

- Who permits write-off of director loans?

- RBI.

- Direct Capital Market exposure ceiling?

- 20% of Net Worth (Aggregate ceiling is 40%).

- Bank's max holding in a company?

- 30% of Bank's Paid-up Capital+Reserves OR 30% of Company's Paid-up Capital (whichever is lower).

- Max loan against Physical Shares to individuals?

- ₹10 Lakh (50% margin).

- Margin for Bank Guarantee to stock broker?

- 50% (of which 25% must be Cash Margin).

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Evolution of lending rates | BPLR (April 2003) → Base Rate (01.10.2010) → MCLR (01.04.2016) → EBLR (01.10.2019) |

| MCLR | Marginal Cost Based Lending Rate — an internal benchmark calculated from 4 components |

| MCLR Component 1: MCF | Marginal Cost of Funds (most significant); Formula: 92% x Marginal Cost of Borrowing + 8% x Return on Net Worth |

| MCLR Component 2 | Negative Carry on CRR — RBI pays zero interest on CRR; cost passed to borrower |

| MCLR Component 3 | Operating Cost — salaries, rent, IT infrastructure |

| MCLR Component 4 | Tenor Premium — extra charge for longer loan durations (higher risk) |

| MCLR formula | MCLR = MCF + Negative Carry on CRR + Operating Cost + Tenor Premium |

| Actual ROI | MCLR + Spread (Spread = bank's profit margin based on credit risk) |

| MCLR review | Published every month; reset period typically 1 year |

| MCLR exemptions | Govt scheme loans (DIR), loans against deposits, staff loans, fixed-rate loans (> 3 years) |

| EBLR (External Benchmark) | Effective 01.10.2019; linked to RBI Repo Rate (most common) or GOI T-Bill yield (FBIL) |

| EBLR applicability | Mandatory for new floating rate personal/retail loans (housing, auto) and MSME loans |

| EBLR spread rules | Spread cannot change for 3 years unless borrower's credit score changes |

| EBLR reset period | At least once every 3 months (quarterly) |

| MCLR vs EBLR transparency | MCLR: lower (complex internal calc); EBLR: high (publicly available data) |

| MCLR vs EBLR transmission | MCLR: slow; EBLR: fast (linked directly to RBI/market) |

| Fixed-rate loans (< 3 years) | Interest rate shall not be less than benchmark rate for similar tenor |

| Loan against demat shares (individuals) | Max ₹20 Lakh, minimum margin 25% |

| Loan against physical shares (individuals) | Max ₹10 Lakh, minimum margin 50% |

| Bank guarantee margin for brokers | 50% margin required; 25% must be in cash |

| Prohibited financing | Badla/carry-over transactions; loans against deposits of other banks; loans against CDs; loans for share buy-back |

| Section 19(2) B R Act | Bank cannot hold shares > 30% of bank's paid-up capital + reserves OR 30% of company's paid-up capital (whichever lower) |

| Section 20(1) B R Act | Banks cannot lend against own shares; cannot grant loans to own directors (except against govt securities, LIP, FD, staff loans) |

| Loans to directors of other banks | Below ₹5 Cr: appropriate authority + report to Board; ₹5 Cr and above: sanctioned by Board of Directors |

| Write-off of director loans | Requires explicit RBI permission (Section 20A B R Act) |

| Transfer of loan accounts | Existing bank must convey decision within 15 days |

| Legal audit of title deeds | Mandatory for loans ₹5 Cr and above |

| Valuation of property | For property valued ₹50 Cr or above: valuation from at least 2 independent valuers |

| Return of security documents | Within 15 days of loan repayment/closure |

| Passport copies | Mandatory for directors/promoters if exposure > ₹50 Cr |

| LTV for home loans | Up to ₹30L: max 90%; > ₹30L to ₹75L: max 80%; above ₹75L: max 75% |

| CRILC | Central Repository of Information on Large Credits; set up by RBI in 2014 |

| CRILC reporting threshold | Borrowers with aggregate exposure ₹5 Cr and above |

| CRILC-Main report | Submitted quarterly within 21 days; has 4 sections (large borrowers, technically written-off, current a/c balances ₹1 Cr+, non-cooperative borrowers) |

| UCB CRILC return | 3 sections (no non-cooperative borrowers); UCBs with assets ₹500 Cr+; submitted quarterly within 30 days via XBRL |

| SMA-0 / SMA-1 / SMA-2 | 1-30 days / 31-60 days / 61-90 days overdue |

| SMA-2 reporting | As and when basis (immediately on 61 days overdue); weekly SMA reporting every Friday for ₹5 Cr+ |

| LEI | 20-digit alphanumeric code uniquely identifying legal entities; mandatory for corporate borrowers with exposure ₹5 Cr+ |

| Red Flagged Accounts (RFA) | Exposure ≥ ₹50 Cr with Early Warning Signals of fraud; reported immediately/weekly |

| Direct capital market exposure | 20% of Net Worth; aggregate ceiling 40% of Net Worth |

Lesson Doubts

Ask questions, get expert answers