🔐 Securities and Charges

Types of securities, creation of charges, and legal aspects of collateral management in banking.

Securities and Charges

Overview of Securities in Lending

- The Basic Principle: Fundamental banking principles suggest that banks should always obtain securities to secure their loans. This protects the bank's interests if a borrower fails to repay.

- Types of Securities:

- Primary vs. Collateral: Securities can be classified as either primary (the asset financed by the loan itself) or collateral (additional security provided by the borrower).

- Tangible vs. Intangible: They can also be tangible (physical assets like a car) or intangible (non-physical assets like rights or claims).

- Legal Framework: Banks deal with these securities under the provisions of different Acts depending on the type of asset involved.

- Purpose of Securities in Banking:

- Safeguard banks' loans

- Used as a fallback in case of loan defaults

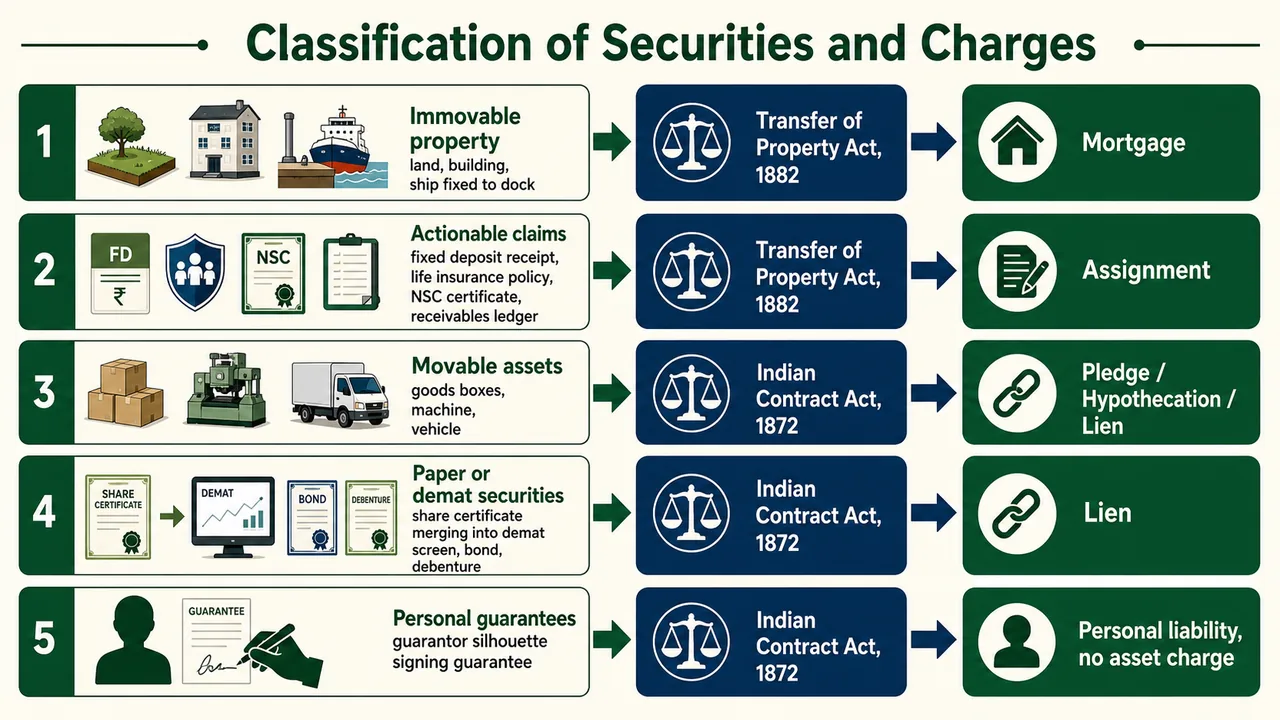

Classification of Securities and Relevant Acts

There are four main groups, each governed by specific laws and legal charges:

1. Immovable Properties

- Assets: This category includes fixed assets like Land, buildings, and ships. (ship, plant and machinery if fixed at one place are considered as immovable)

- Governing Law: These are governed by the Transfer of Properties Act 1882.

- Type of Charge: The legal charge created on immovable property is called a mortgage.

2. Actionable Claims (Unsecured Debts)

- Assets: These are financial claims or unsecured debts such as FDR (Fixed Deposit Receipts), LIP (Life Insurance Policies), NSC (National Savings Certificates), KVP, book-debts, etc.

- Governing Law: Like immovable property, these are also governed by the Transfer of Property Act 1882.

- Type of Charge: The legal charge created here is an assignment (transferring the rights of the claim to the bank).

3. Movable Assets

- Assets: This includes physical items that can be moved, such as Goods, machinery, and vehicles. (you shift from one place to another)

- Governing Law: Dealing with these assets falls under the Indian Contract Act.

- Type of Charge: The charge depends on who holds the asset:

- Pledge: Used when possession is with the bank (e.g., gold loans).

- Hypothecation: Used when possession is with the borrower (e.g., car loans where the borrower drives the car).

- Lien: Another form of charge applicable to movable assets. (e.g. lien on RC of vehicle)

4. Paper or Demat Securities

- Assets: This covers financial instruments like Shares, bonds, and debentures.

- Governing Law: Governed by the Indian Contract Act.

- Type of Charge: The charge created is typically a Lien.

5. Personal Guarantees

- Nature: These are guarantees provided by promoters or 3rd parties.

- Governing Law: Governed by the Indian Contract Act.

- Type of Charge: There is no physical asset charge; instead, there is personal liability of the guarantors to repay if the borrower defaults.

Legal Aspects Summary

| Asset Type | Governing Law | Charge Type |

|---|---|---|

| Immovable Property | Transfer of Property Act, 1882 | Mortgage |

| Actionable Claims | Transfer of Property Act, 1882 | Assignment |

| Movable Assets | Indian Contract Act, 1872 | Pledge / Hypothecation / Lien |

| Paper/Demat Securities | Indian Contract Act, 1872 | Lien |

| Personal Guarantees | Indian Contract Act, 1872 | Personal Liability |

Types of Charges

Charges over securities are legally created by obtaining security and loan documents. The seven types of charges are: Assignment, Lien, Set-off, Hypothecation, Pledge, Mortgage, and Appropriation.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Securities and Charges

Overview of Securities in Lending

- The Basic Principle: Fundamental banking principles suggest that banks should always obtain securities to secure their loans. This protects the bank's interests if a borrower fails to repay.

- Types of Securities:

- Primary vs. Collateral: Securities can be classified as either primary (the asset financed by the loan itself) or collateral (additional security provided by the borrower).

- Tangible vs. Intangible: They can also be tangible (physical assets like a car) or intangible (non-physical assets like rights or claims).

- Legal Framework: Banks deal with these securities under the provisions of different Acts depending on the type of asset involved.

- Purpose of Securities in Banking:

- Safeguard banks' loans

- Used as a fallback in case of loan defaults

Classification of Securities and Relevant Acts

There are four main groups, each governed by specific laws and legal charges:

1. Immovable Properties

- Assets: This category includes fixed assets like Land, buildings, and ships. (ship, plant and machinery if fixed at one place are considered as immovable)

- Governing Law: These are governed by the Transfer of Properties Act 1882.

- Type of Charge: The legal charge created on immovable property is called a mortgage.

2. Actionable Claims (Unsecured Debts)

- Assets: These are financial claims or unsecured debts such as FDR (Fixed Deposit Receipts), LIP (Life Insurance Policies), NSC (National Savings Certificates), KVP, book-debts, etc.

- Governing Law: Like immovable property, these are also governed by the Transfer of Property Act 1882.

- Type of Charge: The legal charge created here is an assignment (transferring the rights of the claim to the bank).

3. Movable Assets

- Assets: This includes physical items that can be moved, such as Goods, machinery, and vehicles. (you shift from one place to another)

- Governing Law: Dealing with these assets falls under the Indian Contract Act.

- Type of Charge: The charge depends on who holds the asset:

- Pledge: Used when possession is with the bank (e.g., gold loans).

- Hypothecation: Used when possession is with the borrower (e.g., car loans where the borrower drives the car).

- Lien: Another form of charge applicable to movable assets. (e.g. lien on RC of vehicle)

4. Paper or Demat Securities

- Assets: This covers financial instruments like Shares, bonds, and debentures.

- Governing Law: Governed by the Indian Contract Act.

- Type of Charge: The charge created is typically a Lien.

5. Personal Guarantees

- Nature: These are guarantees provided by promoters or 3rd parties.

- Governing Law: Governed by the Indian Contract Act.

- Type of Charge: There is no physical asset charge; instead, there is personal liability of the guarantors to repay if the borrower defaults.

Legal Aspects Summary

| Asset Type | Governing Law | Charge Type |

|---|---|---|

| Immovable Property | Transfer of Property Act, 1882 | Mortgage |

| Actionable Claims | Transfer of Property Act, 1882 | Assignment |

| Movable Assets | Indian Contract Act, 1872 | Pledge / Hypothecation / Lien |

| Paper/Demat Securities | Indian Contract Act, 1872 | Lien |

| Personal Guarantees | Indian Contract Act, 1872 | Personal Liability |

Types of Charges

Charges over securities are legally created by obtaining security and loan documents. The seven types of charges are: Assignment, Lien, Set-off, Hypothecation, Pledge, Mortgage, and Appropriation.

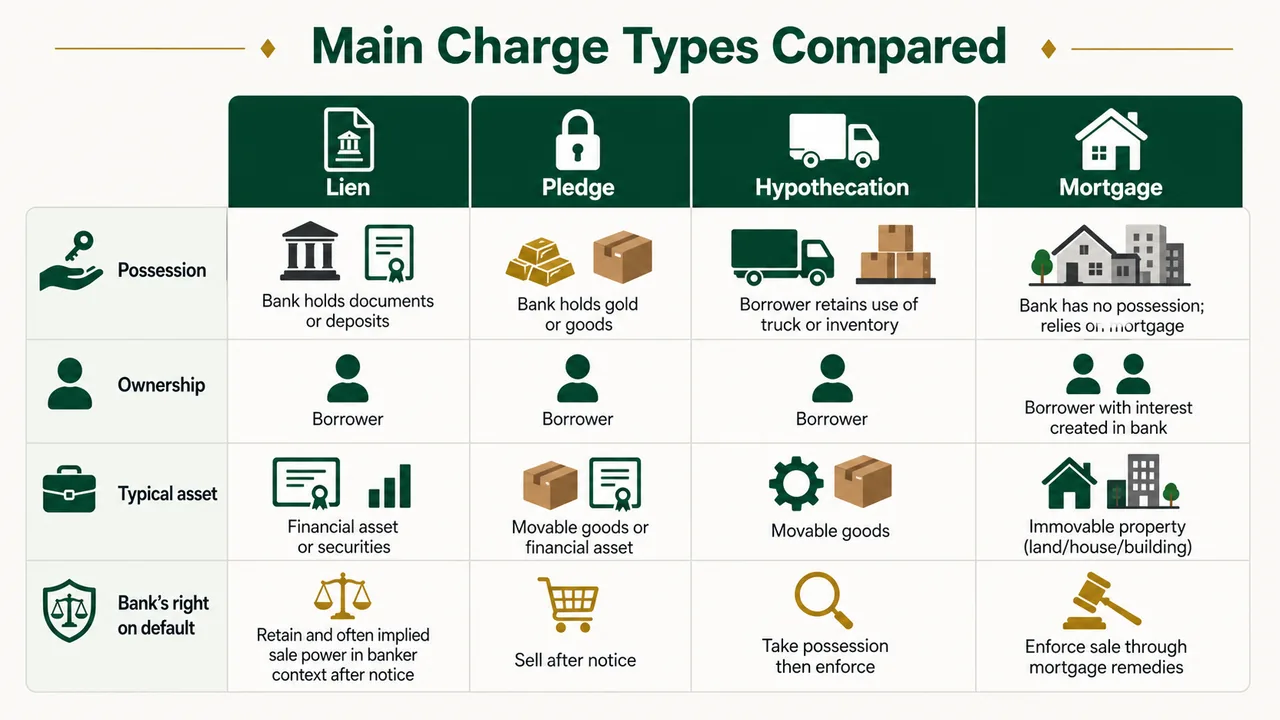

Charges by Borrowers in Favour of Bank — Comparison

| Charge | Security Created On | Possession | Ownership | Governing Act |

|---|---|---|---|---|

| Lien | Financial Asset | Lender | Borrower | Indian Contract Act |

| Pledge | Physical Asset (Movable) & Financial Asset | Lender | Borrower | Indian Contract Act |

| Hypothecation | Physical Asset (Movable) | Borrower | Borrower | SARFAESI Act |

| Mortgage | Physical Asset (Immovable) | Borrower | Borrower | Transfer of Properties Act, 1882 |

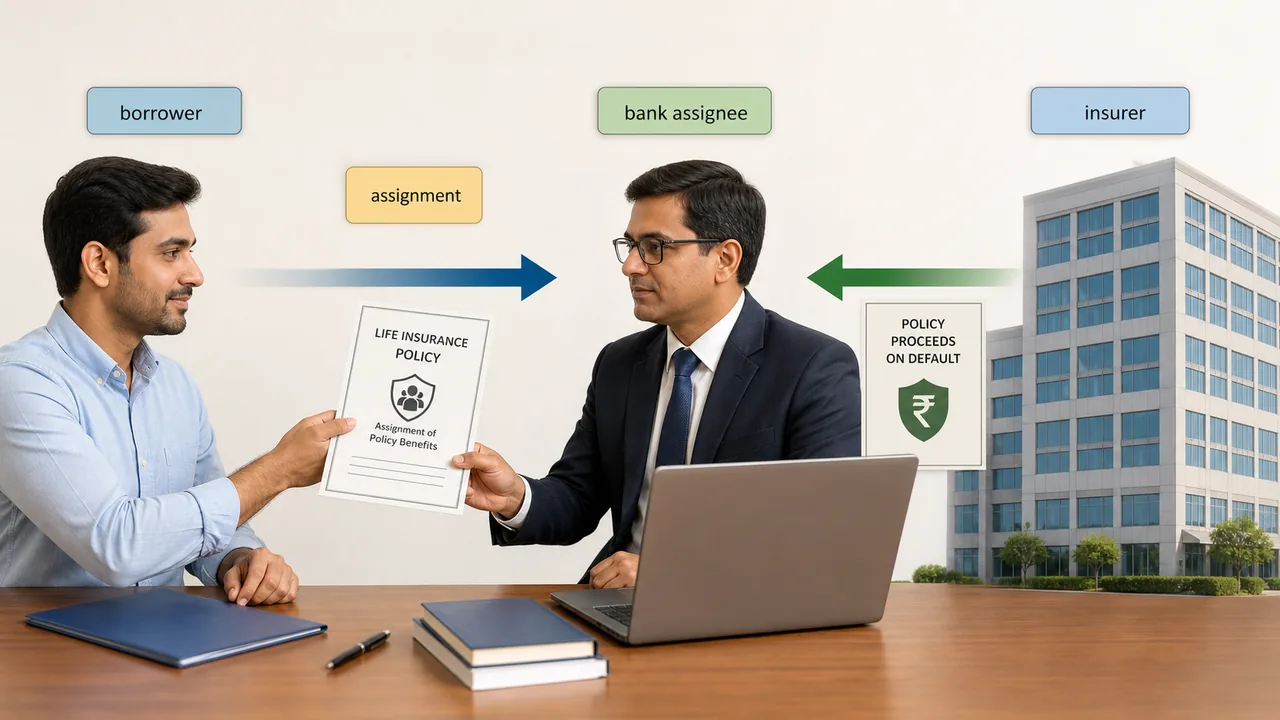

Assignment (Actionable Claims)

Assignment is the method used to secure Actionable Claims (unsecured debts), defined under Section 130 of the Transfer of Property Act 1882.

- Definition: It is the transfer of rights, property, or debt from one person (assignor) to another (assignee). These are existing or future rights.

- Note: These assets are not secured by pledge, hypothecation, or mortgage.

- Parties Involved:

- Assignor (Transferor): The Borrower.

- Assignee (Transferee): The Bank.

- Creation Rules: An assignment must be created in writing only, as a written instrument signed by the assignor.

- Actionable claims pertain to debts excluding those secured by mortgages, hypothecation, or pledge of movable assets.

- Transferring actionable claims doesn't mandatorily require notifying the debtor.

- The transferee can sue the debtor directly, inheriting all rights and remedies of the transferor. However, the transferee also inherits liabilities and equities the transferor had at the transfer time.

Illustration: If A owes B money and B transfers the debt to C without informing A, any payment made by A to B remains valid. C can't later claim this debt from A.

Types of Assignment:

- Legal Assignment: When a notice of the assignment is sent to the original debtor (e.g., notifying LIC that a policy has been assigned to the bank). It is an absolute transfer of an actionable claim in writing, with notifications sent to the debtor about the assignee.

- Equitable Assignment: If no notice is given to the original debtor. Occurs when formalities for a legal assignment aren't fulfilled.

Assignment in Banking Practices:

- Borrowers often assign book debts, dues from Government departments, and life insurance policies as security.

- Assignments can be in various forms — absolute or security-based, legal or equitable.

- For life insurance policies, assignments are done either through policy endorsement or a separate deed. However, the insurer must be informed about such an assignment.

Rights of the Bank:

- The bank (transferee) acquires the same rights the borrower had; they cannot acquire a "better" title than the assignor possessed.

- If the loan is not repaid, the bank can approach the original debtor (e.g., the insurance company) directly to recover the money by surrendering the claim.

- No Consent Needed: The bank does not need the borrower's consent to obtain the money from the original debtor once the default occurs.

Assignment of Actionable Claim (Insurance Policies):

- An actionable claim means a claim to any debt or beneficial interest in moveable property.

- If the policy is assigned to the bank, the bank is entitled to receive the proceeds.

- Priority of assignment is fixed based on the date of delivery of notice to the insurance company by the assignee.

- Section 38 of the Insurance Act states Assignment and Transfer of Insurance Policies.

Lien (Financial Assets with Possession)

Lien means the right of the creditor to retain the goods and securities owned by the debtor until the debt is repaid. It confers upon the creditor the right to retain the debtor's security but not the right to sell it.

- It is a form of implied pledge.

- Backed by Sec. 171 of the Indian Contract Act, 1872 granting general lien on all goods/securities, unless a contrary agreement exists.

- Lien doesn't require a separate agreement and is statutory.

- If goods/securities aren't given during normal banking operations (e.g., left behind by accident), no lien right applies.

Types of Lien:

| Type | Description | Section |

|---|---|---|

| Particular Lien | Right to retain possession of goods until charges due in respect of that specific property are paid | Section 170, Indian Contract Act, 1872 |

| General Lien | Right to retain possession for payment of any sum owed, even if not connected with the property in possession | Section 171, Indian Contract Act, 1872 |

Banker's Lien:

- A banker's lien is a General Lien and is an implied pledge. This means it enjoys the characteristics of pledge as well.

- Unlike a regular lien (retain only), a banker's right of lien is more than a general lien — it confers the power to sell the goods and securities in default by the customer.

- Such a right of lien resembles a pledge and is usually called an implied pledge.

- The banker can dispose of the securities after giving proper notice to the customer.

- When a bank holds a customer's property as security against a debt, this is known as Lien.

Negative Lien

Negative Lien means that the borrower gives a written undertaking to the bank that:

- They will not create any further charge on the assets already charged to the bank/lending institution.

- They will not create any other encumbrance on the assets already charged to the bank without the consent of the existing lender.

- Pertains to items not in bank's possession.

- Doesn't require registration with official bodies, like the Registrar of Companies.

NOTE

Negative Lien is not a "charge" in the legal sense — it is a contractual restriction. It does not give the bank any right over the asset but prevents the borrower from diluting the bank's security.

Set-off

Set-off allows a debtor to counterbalance owed amounts using debts owed to them by the creditor. It essentially combines debtor and creditor accounts to determine net balance.

- It is a statutory right but can also arise from mutual agreements.

- Enables banks to balance a customer's debit with their credit balance.

- The right of a debtor to consider his own owed debt when repaying is known as Set-off.

Salient Features of Set-off:

- Both involved debts must be definitive.

- Can't set-off a guarantor's credit balance until their liability is clear.

- A current account's credit balance can't be set against a not-yet-due discounted bill's contingent liability.

- Loans repayable on demand/at a specified date can't be set-off against a current account credit until demand is made or the date arrives.

- Both parties should be mutually indebted in the same capacity.

- Partner's credit balance can counterbalance partnership account's debit, given joint and several liability.

- Set-off is valid between two differently named firms with identical partners.

- A sole proprietor's personal account balance can counterbalance the sole proprietary concern's balance and vice versa.

- Banks can't exercise both lien and set-off rights simultaneously.

Automatic Right of Set-off triggers under circumstances such as:

- Death, insanity, or insolvency of a customer.

- Insolvency of a firm's partner or company winding up.

- Receipt of a garnishee order.

- Notification of a customer's credit balance assignment.

Availability of Right of Set-off in Different Situations:

| Deposit in the name of | Loan in the name of | Right Available? |

|---|---|---|

| Single person | Jointly with others | Available |

| Partner in a firm | Partnership firm | Available |

| Single name | Same name | Available |

| Proprietor | Proprietorship firm | Available |

| Partnership firm | One of the partners | Not available |

| Trust | Trustee | Not available |

| Trustee | Trust | Not available |

| Dividend account of a company | Loan account of a company | Not available |

| Minor operated by guardian | Guardian | Not available |

| Joint account | One of the joint holders | Not available |

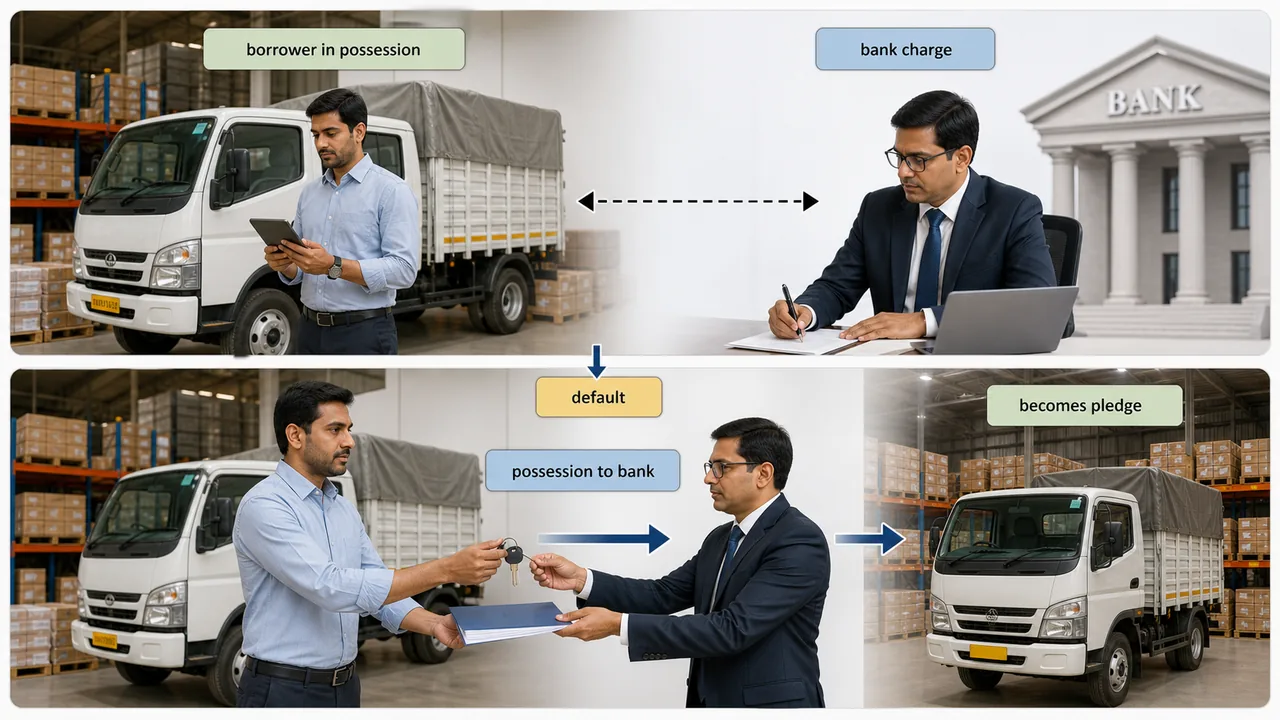

Hypothecation (Movable Assets without Possession)

Hypothecation is defined under Section 2 of the SARFAESI Act and is used when the borrower needs to use the asset (e.g., a car or factory machinery).

- Definition: A charge on movable assets without delivery of possession. The borrower retains the asset but creates a charge to secure the loan.

- Nature of Ownership: Both ownership and possession remain with the borrower. However, the borrower holds the asset as a Trustee for the bank.

- Parties Involved:

- Hypothecator: The Borrower.

- Hypothecatee: The Bank.

- Equitable Charge: It is considered an equitable charge because the bank does not have physical control.

- Key Difference from Pledge and Mortgage:

- In pledge, goods are in possession of the creditor.

- Mortgage typically involves immovable property and transfers interest to the creditor.

Aspects of Hypothecation:

- Usage: Offered to trustworthy customers, especially companies registered under the Companies Act.

- Ideal for:

- Loan against work-in-progress.

- Goods requiring frequent handling, e.g., in factories.

- Daily business assets like in shops or showrooms.

- Drawbacks:

- No creditor control over the assets.

- Possible fraudulent handling of hypothecated goods.

- Potential for stock erosion or duality in hypothecation.

- Difficult and costly recovery in default cases.

- Precautions:

- Borrower exclusively with one bank.

- Mandatory registration of charge for registered companies.

- Periodic and serialized stock statements.

- Routine checks and supervision of hypothecated goods.

Deed of Hypothecation Highlights:

- Nature: Comprehensive document detailing the hypothecation agreement.

- Contents include:

- Borrower's loan request based on goods as collateral.

- Precise description of the goods and assurance of ownership.

- Commitment to not create further charges on the goods.

- Borrower's obligation to provide goods' details and permit inspections.

- Insurance on goods as mandated by the bank.

- Maintenance of an agreed security margin.

- Commitment to manage all expenses related to the property storing hypothecated goods.

- Bank's right to call in the loan, and procedures in case of default.

- Borrower's acknowledgement of debt accuracy.

- Security continuation clause, emphasizing its ongoing nature regardless of account balances.

Enforcement and Conversion:

- Right to Possession: The bank has the legal right to demand possession of the asset.

- Conversion to Pledge: If the borrower hands over possession upon demand, the hypothecation converts into a pledge. The bank then becomes a "pledgee" and gains the right to sell the asset without court intervention (after notice).

- Refusal to Surrender: If the borrower refuses to give possession:

- The bank must file a suit in court (within the limitation period).

- If applicable, the bank can use the SARFAESI Act provisions to seize the asset.

- Registration:

- Companies: Charges must be registered with the ROC (Registrar of Companies) within 30 days under the Companies Act 2013.

- General: Under the SARFAESI Act 2002, charges must be registered with CERSAI.

Pledge (Movable Assets with Possession)

Pledge is a specific type of charge defined under Section 172 of the Indian Contract Act, 1872.

- Definition: It is a "bailment" of goods, meaning the delivery of goods from the borrower to the bank to secure a loan or fulfil a promise (e.g., Gold Loan, Jewellery Loans, Advances against goods/stock, Advances against National Savings Certificates).

- Parties Involved:

- Pawnor/Pledger/Bailor: The borrower (person giving the goods).

- Pawnee/Pledgee/Bailee: The bank (person receiving the goods as security).

- Ownership vs. Possession: In a pledge, ownership remains with the borrower, but possession transfers to the bank.

- Constructive Pledge: If physical delivery isn't possible, possession can be given to an agent of the bank (e.g., a loan against a warehouse receipt).

- Liability for Loss: If goods are damaged while in the bank's possession, the bank is liable only if it was negligent. If the bank handled the goods carefully, it is not liable.

Requirements for a Valid Pledge:

- A contract regarding a specified item given as security.

- The item must be physically or symbolically handed over.

- The item should be given by the debtor.

- The purpose should be for securing a payment or fulfilling a promise.

Essential Elements of Pledge:

- The security item is delivered to the pawnee, either physically or constructively.

- The pawnee has limited rights over the pledged item, while the pawnor retains the main ownership.

Legal Implications of Pledge:

- Ownership remains with the pawnor, but the pawnee gets a qualified interest.

- Delivery to the pawnee can be actual or constructive.

- Delivery modes:

- Giving the storage key.

- Using attornment (third-party acknowledgement).

- Handing over official documents linked to the goods.

- Pledge aspects:

- Goods can remain with pawnor but acknowledged as for the pawnee.

- Delivery can be symbolic or actual.

- Court case: Co-operative Hindustan Bank Ltd. vs Surendar Nath Dey highlights the importance of delivery in a pledge.

- Pledge can be implicit or explicit.

- Pledging only possible for current, specific items in possession.

- Losing possession means losing the pledge.

- Goods can be released with a trust letter, preserving the rights of the pawnee.

Who Can Create a Pledge:

- The owner of the goods.

- A mercantile agent under specific conditions:

- Possession with owner's consent.

- Goods given in agent's capacity.

- Pledge made in regular business.

- Pawnee acts in good faith, without notice of restrictions.

- Individuals possessing goods under a valid yet voidable contract.

- Before retaking possession after a sale, as long as the new owner's consent. If pawnee can re-pledge, but rights are limited.

Rights of Pawnee:

- Retention: Can hold goods for debt, interest, and necessary preservation expenses.

- Extraordinary Expenses: Can recover, but not lien.

- Debt Restriction: Can't keep goods for unrelated debts unless agreed upon.

- Third-Party Rights: Can seek legal action against those infringing on possession.

- Pawnee Default:

- Can sue pawnor.

- Can retain as security.

- Can sell after notifying pawnor.

- Concurrent/Alternative Rights: Retain or sell, but not both. Right to sue remains.

- Post-Sale Actions: Must settle differences with pawnor based on sale proceeds.

- Loss/Damage Events: Can sue in event of theft or damage, sharing any compensation with bailor.

- Limited Interest Pledge: Valid up to the limited interest.

Rights of Pawnor:

- Sale Notice: Entitled to a notice prior to sale.

- Surplus Proceeds: Receives excess from sale proceeds.

- Redemption: Can retrieve goods if not sold by pawnee.

Duties of Pawnor:

- Disclosure: Must reveal flaws/risks in goods.

- Preservation Expenses: Must cover costs incurred for preservation.

- Sale Deficit: Must cover the difference if sale doesn't cover the debt.

Title & Agreement Details:

- Clear title to goods.

- Covers both present and future debt.

- Return of goods post-repayment.

- Right of sale in case of default.

- Option for bank inspection & pawnee registration.

- Not responsible for third-party sale mishaps.

- Allows bank inspections.

Enforcement and Rights in Pledge:

- Priority over Government Dues: If the government demands possession of goods to recover dues, the bank's loan recovery has priority. Only the surplus after the bank is paid goes to the government.

- Repayment: Once the loan is paid, goods must be returned to the borrower immediately.

- Default and Sale:

- Under Section 176, the bank can sell the pledged goods without filing a lawsuit in court.

- Requirement: The bank must give reasonable notice before selling; selling without notice is illegal.

- Time-Barred Loans: Uniquely, even if the loan is time-barred (limitation expired), the bank can still recover money by selling the pledged goods.

- Shortfall: If the sale doesn't cover the full debt, the bank must file a suit within 3 years to recover the balance from the borrower personally.

Advantages of Pledge:

- Direct Control: Bank has physical possession.

- No Subsequent Charges: Regular inspections prevent further charges.

- Stock Transparency: Difficult for pawnor stock manipulations.

- Insurance Security: Recovery possible via insurance if goods are lost.

- Simplicity: Easier than mortgage processes.

Precautions in Pledging Goods to a Banker:

- Verify pawnor's ownership of the goods.

- Ensure contract completeness and inclusion of standard clauses.

- Maintain strong control over all pledged goods.

- Display a signboard in the storage area indicating banker's interest.

- Treat the goods with the same care as one's own similar goods; compensate pawnor for any loss due to negligence.

- Regularly inspect the goods to ensure quality, quantity, and maintenance of value.

Differences: Pledge vs. Lien vs. Hypothecation:

| Feature | Pledge | Lien | Hypothecation |

|---|---|---|---|

| Sale on default | Allowed | Not allowed (except banker's lien) | Not directly |

| Transfer of interest | No | No, only right to retain | No |

| On losing possession | Pledge ends | Lien ends | Continues |

| Assignability | Can involve sales, is assignable | Not assignable | Borrower retains asset |

Noteworthy Cases on Pledge:

-

Morvi Mercantile Bank Ltd. vs Union of India (AIR 1965 SC 1954):

- Bank was entitled to recover goods' value since valid pledge was created via railway receipts endorsement.

- Constructive delivery suffices for a pledge.

- Endorsement resulted in a valid bank pledge.

-

Lallan Prasad vs Rahmat Ali (AIR 1967 SC 1322):

- A pawnee can sue for debt recovery only if able to return the pledged goods when the pawnor repays.

-

Bank of Bihar vs State of Bihar (AIR 1971 SC 1210):

- Bank's right as a pawnee overrides the government's right, so the government had to repay the bank.

-

Standard Chartered Bank vs Custodian (AIR 2000 SC 1488):

- Any value increase in pledged goods is owed to the pawnee.

- Accretions (like bonuses or dividends) on pledged items form part of the pledge and must be returned or can be sold upon default.

Mortgage (Immovable Property)

Mortgages are the legal method for securing loans against real estate and other fixed assets, governed strictly by the Transfer of Property Act.

1. Definition and Core Concepts

- Legal Definition: According to Section 58 of the Transfer of Property Act, a mortgage is defined as the "transfer of interest in specific immovable property by owner, in bank's favour, to secure a loan, existing or future".

- Nature of Transfer: Crucially, only the interest in the property is transferred to the bank. The actual property itself is not transferred (ownership generally remains with the borrower, except in specific types like English Mortgage where it is like sale of property to the bank).

- What Qualifies as Immovable Property: This category is broad and includes land, building, embedded machinery, ship, and vessel.

- Governing Law: Transfer of Property Act, 1882. Sections 58 to 104 cover mortgages specifically.

Sale of Immovable Property:

- Ownership transfer in exchange for a paid or promised price.

- Sales over Rs. 100 require a registered instrument.

- Ownership transfer happens when the buyer possesses the property.

Mortgage Requirements:

- Transfer of property interest.

- Security for a loan or debt.

Parties:

- Mortgagor (Transferor): The borrower who gives the property as security.

- Mortgagee (Transferee): The bank who receives the property interest.

Eligibility to Transfer Property:

- Anyone competent to contract.

- Can transfer wholly, in part, conditionally or absolutely.

Mortgagor Profile:

- Absolute property owners.

- Co-owners.

- Karta of HUF (Hindu Undivided Family).

- Guardians for minors (with court approval).

- Executors or administrators.

2. Creation of a Mortgage

A mortgage can be established in two ways depending on the type:

- In writing: By way of creation of a formal mortgage deed.

- Orally: This is specific to Equitable Mortgages (where the deed is essentially the deposit of title deeds without a formal written mortgage instrument).

- Requirements for Written Mortgages (Mortgage Deed): For all mortgages other than Equitable Mortgage, a written Mortgage Deed is mandatory. This deed generally needs:

- (1) To be witnessed: Formal attestation by witnesses.

- (2) To be registered: It must be registered with the Registrar of Assurances within 4 months if the loan amount is Rs. 100 or above. The Registrar (ROA) has the power to allow late registration within the next 4 months if missed.

- (3) Stamp Duty: Proper stamp duty payment at rates prescribed by the State Govt. is required.

3. Types of Mortgages

The Transfer of Property Act, 1882 outlines six types of mortgages:

A. Simple Mortgage

- Section: Sec. 58(b)

- Structure: Mortgagor promises to pay and the property is given to the mortgagee. The mortgagor commits to paying the mortgage amount. If the mortgagor defaults, the property can be sold through the court.

- Liability: The Borrower is personally liable to pay the loan.

- Remedy: In case of non-payment, the bank cannot sell the property directly. The Bank can cause sale of property, by filing suit (court intervention is required).

- Key features:

- Mortgagor retains property possession.

- Mortgagor retains property ownership.

- Only courts can sanction property sale.

- Bank can sell the property through court if mortgagor defaults.

- Mortgage doesn't get property income.

- Mortgage doesn't get property possession.

- Registration necessary for amounts Rs 100 and above.

B. Mortgage by Conditional Sale

- Structure: The Mortgagor ostensibly (looks like sell on paper) sells property to the bank on a specific condition:

- If default: The sale will become absolute (the bank becomes the full owner).

- If repayment on time: The sale shall become void (ownership returns fully to the borrower).

- The sale is not real; it becomes absolute if the money isn't repaid by the agreed date.

- The mortgagee can't sell the property but can bar the mortgagor's right to redeem.

- There's no personal promise to repay the debt.

- If the property value doesn't cover the debt, the mortgagee can't claim other properties.

- Bankers usually avoid this due to its limitations.

- Key Right: The Right of foreclosure is available in this mortgage (meaning the bank can cut off the borrower's right to redeem the property).

C. Usufructuary Mortgage

- Possession & Rights: Ownership remains with mortgagor, but possession is with the bank.

- The mortgagor allows the mortgagee to retain possession until the debt is cleared.

- Recovery Method: Sale is not allowed. Instead, the bank recovers the loan from income of property only (e.g., collecting rent or crops from the land).

- The mortgagee can't sue for repayment or for selling.

- No set repayment time; mortgagee holds property till either (a) debt is cleared or (b) after 30 years without redemption, the mortgage owes the property.

- Liability: Uniquely, the Borrower is not liable for loan personally; the debt is satisfied purely through the property's income.

- Bankers avoid this due to slow recovery of money.

D. English Mortgage

- Ownership: Ownership is transferred to bank outright at the start.

- The mortgagor promises to repay by a certain date.

- The property is transferred absolutely to the mortgagee.

- Liability: The Borrower is personally liable to repay.

- Remedy: The mortgagee will return the property once the debt is paid. If not repaid, the mortgagee can sue and get a decree for sale. Bank can sell property in case of default without needing court intervention in many cases.

- Redemption: On payment of loan, ownership to be transferred back to borrower.

E. Equitable Mortgage (Mortgage by Deposit of Title Deeds)

- Originates from Sec. 58(f) of the Transfer of Property Act.

- Exists when title deeds are given as collateral in specific towns.

- Documents proving ownership are handed to the creditor.

- Doesn't require a formal mortgage deed, registration, or stamp duty with ROA.

- Process includes:

- Getting a title clearance certificate.

- Checking land records history.

- Inspecting property and confirming it's in specified towns.

- Keeping a memorandum of entry.

- Paying stamp duty on the memorandum.

- Benefits: Saves on registration costs. Quick and straightforward. Maintains borrower's privacy.

- Drawbacks: Can be time-consuming and costly to enforce. Risks when borrower is a trustee. Subsequent legal mortgagees can be a challenge.

F. Anomalous Mortgage

- Defined in Sec. 58(g) of the Transfer of Property Act.

- It's not any of the previously mentioned mortgage types.

- It's a combination of two or more types of mortgages.

- Examples:

- Mix of simple and usufructuary mortgage.

- Usufructuary mortgage with a conditional sale.

- Can be shaped by local customs and practices.

G. Reverse Mortgage

- In this case, the lender lends money to the borrower on a monthly basis. The entire loan amount is divided into instalments and the lender gives the borrower money in instalments (opposite of a regular mortgage).

- Typically used by senior citizens who own a property but need regular income.

H. Fixed-Rate Mortgage

- When the lender assures the borrower that the rate of interest will remain the same throughout the loan period, it is called a Fixed-Rate Mortgage.

TIP

All types of mortgages except equitable mortgage must be registered with Sub Registrar of Assurances in the local area where the property is situated within a period of 4 months from the mortgage date.

Distinctive Features of Different Mortgage Types:

- In a simple mortgage, title deeds are deposited but property possession isn't transferred. The mortgagee can sell through court order.

- Usufructuary mortgages and mortgages by conditional sale specifically involve transferring property's possession.

- Both simple mortgages and the power mortgage allow the mortgagee the right of sale.

Priority of Mortgages Created:

- Sec. 48 of the Transfer of Property Act focuses on the principle that rights created earlier have precedence over later ones.

- Details on how it applies and its exceptions follow the original Transfer of Property Act.

(a) Order of Registered Instruments:

- According to Sec. 47 of the Registration Act, 1908, a document's effect begins from its execution date, not its registration.

(b) Ranking Registered vs. Unregistered:

- Registered instruments have preferential standing, incorporating greater principles of justice and equity, though they might modify the original order.

- Sec. 50 of the Registration Act sometimes grants priority to a registered mortgage over an unregistered one.

- Mortgages by title deed deposit are unaffected by the provisions of Sec. 48 of the Indian Registration Act.

Equitable Mortgage (EM) — Detailed

Equitable Mortgage is the most common form of mortgage used in banking because it is cost-effective and involves less paperwork than a registered mortgage.

1. Creation and Documents

- Definition: Equitable mortgage (Sec 58-f Transfer of Property Act) is created by deposit of title deed. This means the mortgage is formed simply by the borrower handing over the property documents to the bank.

- What are Title Deeds? These are the documents establishing ownership, such as sale deed or lease deed or gift deed.

- Original vs. Copy: Ideally, the Title deed should preferably be original to prevent fraud.

- However, creating an EM on the basis of certified copy by ROA (Registrar of Assurances) is also possible, but risky because the original might be misused elsewhere.

2. Location Rules

- Location of Property: The Property can be located at any place; it does not need to be in a specific city.

- Location of Deposit: However, the act of depositing the documents must happen in specific locations. The Place for deposit of title deed can be:

- Presidency town (Kolkata, Mumbai or Chennai).

- Notified towns (by State Govt.).

- Bank Premises: The actual handover Can be within bank or outside bank premises also, as long as it occurs within the notified town limits.

3. Registration Requirements for EM

- ROA Exemption: A key benefit is that EM does not require registration with ROA as per Indian Registration Act. This saves significant stamp duty and registration fees.

- CERSAI Requirement: However, modern laws require that it is to be registered under SARFAESI Act, with CERSAI (Central Registry of Securitisation Asset Reconstruction and Security Interest) to prevent multiple lending against the same property.

Common Mortgage Types for Bankers:

- Mortgage by deposit of title deeds (Equitable Mortgage) — most prevalent.

- Simple mortgage.

- Equitable mortgage is most prevalent.

Difference between Equitable Mortgage and Pledge:

| Feature | Equitable Mortgage | Pledge |

|---|---|---|

| Subject | Immovable property | Movable property |

| Security | Property rights | Physical goods |

| Right of Foreclosure | Available | Not available |

Sale Without Court's Involvement

Some provisions allow lenders to sell mortgaged property without court intervention, as per the Transfer of Property Act.

Sec. 69 conditions for this include:

- Specific scenarios related to English mortgages, government mortgages, or properties in particular cities.

- Execution requires written notice, payment default of three months, or interest arrears of at least ₹500 for three months.

- Sales made under these conditions can't be easily challenged.

- Money from sales must first cover costs, then mortgage dues, with remaining funds going to the rightful property owner.

Under the SARFAESI Act, lenders can enforce the mortgage for debts above ₹1 lac without court intervention and can even seek Magistrate support for property possession.

Enforcement of Mortgages Through Court

Mortgages are usually enforced by filing a suit for property sale, as dictated by the Code of Civil Procedure, 1908.

- Suit must be filed where property is located.

- Order 34 outlines the suit filing process.

Recovery of Debts due to Banks and Financial Institutions Act, 1993 allows debt recovery for debts of ₹20 Lakh and above in the DRT.

- For debts below ₹20 Lakh, a civil suit is filed to recover via mortgage enforcement.

Considerations for the civil suit:

- File in the lowest jurisdiction court possible.

- File where the property is located.

- Include all subsequent mortgagees in the suit.

- If multiple mortgages exist, one of all unless court grants permission otherwise.

- Ensure any claim on the mortgaged personal covenant is within the limitation period.

Mortgage decrees in Civil Courts consist of:

- Preliminary decree: sets a payment deadline.

- Final decree: allows property sale if the mortgagor fails to pay.

Post final decree, the mortgagee can sell the property through the court, without requiring additional attachment orders.

Time Limits in Mortgages

- According to Article 62 of the Indian Limitation Act, 1963, suits for mortgage debt recovery or property sale have a 12-YEAR limitation from when the debt is due.

- As per Article 63(a), foreclosure suits have a 30-YEAR limitation from the debt due date.

Limitation and Registration Summary

1. Limitation Periods

- Enforcing Property Rights: The bank has 12 years to sue for the sale of the property.

- Foreclosure: 30 years from debt due date.

- Personal Suit: Against mortgagor, 3 years is the limit if the bank wants to sue the borrower personally for any shortfall.

2. Registration Mandates

- For Companies: If mortgage is created by a company, details of mortgage to be sent for registration with RoC (Registrar of Companies), within 30 days.

- For Non-Equitable Mortgages: If mortgage is other than EM (e.g., Simple or English Mortgage), registration with RoA to be got done within 4 months as per Indian Registration Act.

- Universal Rule: All mortgages to be registered with CERSAI, as per SARFAESI Act.

3. Jurisdiction

- Where to Sue: Legal action cannot be filed just anywhere. Suit can be filed for sale, in a court having jurisdiction, where property is located.

Leases of Immovable Property

Definition of Lease:

- A lease transfers a right to enjoy property for a specific time or forever.

- Transferor: 'Lessor'; Transferee: 'Lessee'.

- Payments: 'premium' and 'rent'.

Lease vs. Sale:

- Sale transfers property ownership absolutely.

- Lease offers limited rights to enjoy property, separating ownership and possession.

Lease Duration:

- Agricultural/Manufacturing purpose: Yearly leases; terminated with six-month notice.

- Other purposes: Monthly leases; terminated with fifteen-day notice.

Notable Case — Chapsibhai Dhanjibhai Danad vs. Purushottam:

- Involved a deed of lease from 1906 for constructing buildings.

- Court dispute arose over the permanency of the lease.

- The Supreme Court found the lease to be for an indefinite period, implying it lasts for the lessee's lifetime but isn't permanently inheritable.

Principles from the Case:

- Determining if a lease is permanent relies on lease terms.

- A lease mentioning heirs doesn't always mean it's permanent.

- Additions to leased property during the lease are considered part of the lease. If the lessee encroaches and gains the title, they must return it at the lease's end.

Creation of Leases:

- Yearly leases or leases over a year require registered documents.

- Shorter leases can be oral but need possession delivery.

Procedure for Mortgage of Lease Rights:

- Original lease agreements serve as title deeds for perpetual leases.

- Lease agreements should be stamped and registered.

- Lease duration should cover bank's repayment period.

- Tripartite agreements can involve the bank, lessor, and lessee.

- Lease deeds should either have mortgage permission or the lessor provides a no-objection letter.

Right of Appropriation

- Deals with how payments by a debtor are applied towards multiple debts.

- Governed by Sec. 59, 60, and 61 of the Indian Contract Act, 1872.

- Applicable to bank loans as well.

- Different from the right of set-off.

Key Points:

- Fixed deposit appropriated before maturity uses right of appropriation.

- Appropriation after maturity exercises right of set-off.

Case Example:

- Mr. A, a bank customer, has a delinquent housing loan.

- He deposits ₹15,000 in his account for an electricity bill.

- Informs bank the deposit is specifically for that bill and not for the housing loan.

- Based on Sec. 59, if the bank accepts the money, they must respect Mr. A's request. The bank can't use it for the housing loan if deposited for a specific reason.

Registration of Charges (Companies Act 2013)

"Charge" is defined under Section 2(16) of the Companies Act, 2013 as an interest or lien created on the property or assets of a company or any of its undertakings or both as security, and includes a mortgage.

Section 77 of the Companies Act, 2013 clarifies charges can include:

- Securing debentures.

- Uncalled company capital.

- Immovable property anywhere.

- Company's book debts.

- Movable property (not a pledge).

- Intangible assets like patents, copyrights, franchises.

- Under-construction residential or commercial assets (excluding mortgages).

Under Section 100 of the Transfer of Property Act, 1882, where an immovable property is made security for payment of money and the transaction does not amount to a mortgage, it is called a charge, and all provisions of a simple mortgage apply to it.

Sections 77 to 87 of the Companies Act, 2013 provide the procedure for registration of charges.

Exemptions from Registration:

- Guarantees.

- Charges arising from law.

- Hundi (a negotiable instrument).

How to Register a Charge

- The particulars of the charge in the prescribed form, together with a copy of the instrument creating the charge, duly signed by the company and charge holder, shall be filed with the Registrar within 30 days of creation of charge along with prescribed fee.

- This can be extended by 30 days with extra fees, and another 60 days with advalorem fees.

- The property charged may be tangible (land, building, plant & machinery), financial (shares, debentures), or intangible (patents, copyrights, trademarks).

- A charge created by deposit of title deeds is also registrable as per Section 54(f) of the Transfer of Property Act, 1882.

Procedure:

- Companies (Registration of Charges) Rules, 2014 guide the process.

- Use Form No.CHG-1 (general) or Form No.CHG-9 (debentures) for creation or modification.

- Satisfaction reported in Form CHG-5.

- Every instrument showing a charge must be filed, verified, and certified.

- Applicable fees to be paid.

- If the company fails to register, a bank can register and charge the company.

Types of Charges (Fixed vs. Floating):

- Fixed Charge:

- Specific to a particular property.

- If compliant with Sec. 77 of Companies Act, 1956, allows creditor to sell property for repayment.

- Floating Charge:

- General charge, not attached to specific assets.

- Allows company to deal with property in regular business.

- Crystallizes into a fixed charge under certain events.

Crystallization of Floating Charge:

-

Transforms when:

- Company stops business.

- Goes into liquidation.

- A specified event in the charge deed occurs.

-

Once crystallized, it has priority over some other types of charges.

-

Pari-passu Charge:

- This is created when 2 or more banks provide a loan together, typically by way of a formal agreement between them known as a consortium. The Latin term means "On equal footing".

- In this arrangement, their share in the security is in the ratio of their outstanding loans within the agreed limit. Effectively, all involved banks share the rights to the assets proportionally.

- The prior consent of the existing charge holder is required by the company for creating Pari-passu.

Constructive Notice (Section 80, Companies Act)

All charges registered with the Registrar are public documents. Section 80 states that where any charge is registered under Section 77, any person acquiring such property, assets, or undertakings shall be deemed to have notice of the charge from the date of registration. This means anyone can check the MCA Portal to verify if a charge exists on an asset.

Consequences of Non-Registration of Charge

- At the time of winding up, the creditor whose charge has not been registered will be reduced to the level of an unsecured creditor.

- Neither the liquidator nor any other creditor will give legal recognition to an unregistered charge.

- However, the debt remains valid and may be enforced against the company through the courts by filing a suit — but the security is lost.

- Sec. 78 states unregistered charges can still be registered within 60 days with extra fees.

- Unregistered charges aren't automatically void. However, they can't be used against a liquidator or other creditors if the company is wound up. They remain valid against the company itself unless in liquidation.

NOTE

The Companies (Registration of Charges) Rules were amended in 2019.

Agency in Banking

- An 'agent' in the context of banking is a representative doing transactions for another.

- When a bank collects financial instruments for its customers, this falls under the concept of Agency.

- An agent's primary role is to represent another in dealings with third parties.

- If a bank collects a cheque for a customer, this activity falls under Agency.

- If a bank collects financial instruments for its customers, the law primarily involved is the Law of Agency.

Guarantors & Guarantees

A guarantee acts as a secondary layer of security where a third party promises to fulfil the borrower's obligation if they default.

1. Definition and Parties

- Legal Definition: A Guarantee is a contract between a creditor and surety where the surety promises to perform the promise or discharge the liability of borrower, if borrower fails to pay (U/s 126 of Indian Contract Act).

- Nature of Liability: In a guarantee, the guarantor has personal liability to pay. This means their personal assets can be attached if the loan is not repaid.

- The Three Parties Involved:

- Surety: The Person giving guarantee (the Guarantor).

- Creditor: The Person getting guarantee (the Bank/Lender).

- Principal Debtor: The Person on whose behalf guarantee is given (the Borrower).

2. Key Legal Concepts

- Consideration (Section 127): A guarantee is a contract, and every contract needs "consideration" (something in return). However, for a guarantee, the guarantor does not need to receive money directly. Anything done for the benefit of principal debtor, is sufficient consideration, for guarantee.

- Co-extensive Liability (Section 128): Guarantor's liability : It is co-extensive with principal debtor. This means the guarantor is liable to the exact same extent as the borrower. The bank can theoretically sue the guarantor directly without even suing the borrower first.

3. Types of Guarantees

- Specific Guarantee: Typically used in Term Loans (TL). Here, the guarantee is specific and liability declines with repayment of instalments. Once the specific debt is cleared, the guarantee ends.

- Continuing Guarantee: Used in Cash Credit (working capital) accounts. It continues for sanctioned limit. Actual liability shall be limited to o/s (outstanding) balance, within this limit. It covers a series of transactions over time.

Withdrawal of Guarantee

A guarantor has the right to exit a "Continuing Guarantee" (like for a Cash Credit account), but this action has specific consequences governed by Section 130.

1. Revocation Rules (Section 130)

- Right to Withdraw: A Guarantor can withdraw continuing guarantee any time, for future transactions, by giving notice of withdrawal.

- Effect of Withdrawal Notice:

- Freezing Liability: The Guarantor's liability is fixed for balance at the time of receipt of withdrawal notice. They cannot escape the debt that already exists, but they stop accumulating new debt.

- Stop on New Debits: If further debit is allowed, guarantor not liable.

- Reduction by Credits (Clayton's Rule): With credit to account, the guarantor's liability is reduced (Rule in Clayton case). Any money the borrower puts into the account after the notice goes toward paying off the old debt (the part the guarantor owes) first.

2. Rights and Protection of Surety

- Right of Subrogation (Section 140): If the guarantor ends up paying the bank, they step into the bank's shoes. Surety gets right of subrogation i.e. right to receive all securities available with bank for recovery of loan, whether known to surety or not. The guarantor can then use these securities to recover their money from the borrower.

- Protection Against Changes (Section 141): The bank must not alter the loan terms without asking the guarantor. Change in terms and conditions without consent of guarantor absolve (free from) him of his liability. If the contract changes, the guarantee is voided.

Example Illustration: Withdrawal of Guarantee

1. The Scenario Table

| Date | Debit | Credit | Balance |

|---|---|---|---|

| Feb 12 | 10,75,000 | ||

| Feb 13 | 2,00,000 | 8,75,000 | |

| Feb 13 | 1,50,000 | 10,25,000 | |

| Limit | 15 Lac |

2. Application of the Rules (Clayton's Case)

If we assume the Guarantor gives the notice of withdrawal on Feb 12, the following rules apply:

- Step 1 (Freezing Liability): On Feb 12, the balance is 10,75,000. The guarantor's liability is initially "fixed" at this amount.

- Step 2 (Credit Adjustment): On Feb 13, a credit of 2,00,000 comes into the account. According to the Rule in Clayton's Case, credits reduce the oldest liability first. Therefore, the guarantor's liability drops from 10.75L to 8.75L.

- Step 3 (New Debits): On Feb 13, a new debit of 1,50,000 is allowed. Since this is a "future transaction" after the notice was given, the guarantor is NOT liable for this amount.

Conclusion: Even though the final account balance is 10,25,000, the guarantor is only liable to pay 8,75,000. The bank cannot recover the fresh debit of 1.50L from the guarantor.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Securities classification | Primary (asset financed) vs Collateral (additional); Tangible (physical) vs Intangible (rights/claims) |

| Immovable property | Land, buildings, ships; governed by Transfer of Properties Act 1882; charge = Mortgage |

| Actionable claims | FDR, LIP, NSC, KVP, book-debts; governed by Transfer of Property Act 1882; charge = Assignment |

| Movable assets | Goods, machinery, vehicles; governed by Indian Contract Act; charge = Pledge (bank has possession) or Hypothecation (borrower has possession) |

| Paper/Demat securities | Shares, bonds, debentures; governed by Indian Contract Act; charge = Lien |

| Seven types of charges | Assignment, Lien, Set-off, Hypothecation, Pledge, Mortgage, Appropriation |

| Set-off | Statutory right to counterbalance mutual debts; both debts must be definitive; can't exercise lien and set-off simultaneously |

| Right of Appropriation | Governed by Sec. 59, 60, 61 of Indian Contract Act; debtor can direct which debt payment applies to |

| Registration of charges | Defined under Section 2(16), Companies Act 2013; filed with Registrar within 30 days of creation |

| Constructive notice (Section 80) | Registered charges are public documents; anyone acquiring property is deemed to have notice from date of registration (checkable on MCA Portal) |

| Non-registration consequence | Creditor becomes unsecured creditor at winding up; debt remains valid but security is lost |

| Pari-passu charge | Two or more banks share security on equal footing in ratio of outstanding loans; requires prior consent of existing charge holder |

| Floating charge | On changing assets (e.g., inventory in CC); becomes fixed charge on crystallization (default/liquidation) |

| Fixed charge | On specific, identifiable assets (e.g., vehicle, house); assets remain same during loan period |

| Lien | Right to retain goods/securities until debt is repaid; cannot sell (except banker's lien) |

| Particular lien (Sec 170) | Retain goods until charges for that specific property are paid |

| General lien (Sec 171) | Retain possession for any sum owed, even if unconnected to the property |

| Banker's lien | A general lien + implied pledge; bank can sell goods/securities after giving proper notice |

| Pledge (Sec 172, Indian Contract Act) | Bailment of goods; possession with bank (pawnee); ownership with borrower (pawnor) |

| Pledge — sale on default (Sec 176) | Bank can sell without court intervention after giving reasonable notice; even for time-barred loans |

| Pledge — priority | Bank's loan recovery has priority over government dues; surplus goes to government |

| Hypothecation (Sec 2, SARFAESI Act) | Charge on movable assets without delivery of possession; borrower holds as Trustee for bank |

| Hypothecation → Pledge conversion | If borrower hands over possession on demand, it converts to pledge; if refused, bank must file suit or use SARFAESI Act |

| Hypothecation registration | Companies: with ROC within 30 days; General: with CERSAI under SARFAESI Act |

| Negative lien | Written undertaking by borrower not to create further charge on assets without lender's consent; not a legal charge — contractual restriction only |

| Assignment (Sec 130, TPA 1882) | Transfer of right/debt; Legal assignment = notice given to original debtor; Equitable = no notice |

| Assignment — bank's rights | Bank acquires same rights as borrower; can approach original debtor directly on default; no consent needed from borrower |

| Insurance policy assignment | Priority fixed by date of delivery of notice to insurance company; Sec 38 of Insurance Act governs |

| Mortgage (Sec 58, TPA) | Transfer of interest (not property itself) in immovable property to secure a loan |

| Six types of mortgages (TPA) | Simple, Conditional Sale, Usufructuary, English, Equitable (Deposit of Title Deeds), Anomalous |

| Simple mortgage | Borrower personally liable; bank must file suit in court to sell property |

| Mortgage by conditional sale | Ostensible sale; default = sale becomes absolute; repayment = sale void; foreclosure right available |

| Usufructuary mortgage | Possession with bank; recovery from property income only; borrower not personally liable |

| English mortgage | Ownership transferred to bank; borrower personally liable; bank can sell without court in many cases |

| Equitable mortgage (EM) | Created by deposit of title deeds; does not require ROA registration; must register with CERSAI |

| EM — location of deposit | Property can be anywhere; deposit must be in Presidency town (Kolkata, Mumbai, Chennai) or State Govt notified towns |

| Anomalous mortgage | Not a standard type; combination of two or more types; shaped by local customs |

| All mortgages except EM | Must be registered with Sub Registrar of Assurances within 4 months |

| Priority of mortgages | Determined by date of mortgage creation, not date of registration |

| Sale without court (Sec 69) | English mortgage, govt mortgage, or in particular cities; needs written notice + 3-month default or ₹500 interest arrears |

| SARFAESI enforcement | For debts above ₹1 lac without court; DRT for debts ₹20 Lakh+ |

| Limitation: mortgage property | 12 years to sue for sale of property; 30 years for foreclosure; 3 years for personal suit |

| Leases | Lessor/Lessee; Agricultural = yearly lease (6-month notice); Others = monthly (15-day notice) |

| Agency | Bank as agent when collecting cheques/instruments; governed by Law of Agency |

| Registration: companies | Details sent to ROC within 30 days; all mortgages registered with CERSAI |

| Reverse mortgage | Lender pays borrower in monthly instalments; typically for senior citizens owning property |

| Guarantee (Sec 126, Indian Contract Act) | Contract between Surety (guarantor), Creditor (bank), Principal Debtor (borrower) |

| Co-extensive liability (Sec 128) | Guarantor liable to same extent as borrower; bank can sue guarantor directly |

| Specific vs Continuing guarantee | Specific: for Term Loans, liability declines with repayment; Continuing: for Cash Credit, covers sanctioned limit |

| Withdrawal of guarantee (Sec 130) | Guarantor can withdraw for future transactions by giving notice; liability fixed at balance on notice date |

| Clayton's Rule | After withdrawal notice, credits reduce guarantor's liability first; new debits are not guarantor's responsibility |

| Subrogation (Sec 140) | If guarantor pays, they get all bank's securities for recovery from borrower |

| Protection (Sec 141) | Change in loan terms without guarantor's consent absolves guarantor of liability |

| Noteworthy pledge cases | Morvi Mercantile (constructive delivery valid), Bank of Bihar (pawnee > govt), Standard Chartered (accretions part of pledge) |

Lesson Doubts

Ask questions, get expert answers