📄 Banking Documentation

Legal documentation requirements, stamp duty, and limitation periods for bank loans.

Documentation (General Principles)

The legal foundation for what a "document" is and why it is critical for bank loans.

- Legal Definition: According to the Indian Evidence Act, a document is any matter expressed upon any substance using letters, figures, or marks to record information. This means even a digital file or a handwritten note can be a document.

- Purpose of Loan Documents:

- Identification: To clearly identify the borrower and the collateral (securities).

- Binding Terms: To fix the specific interest rates, repayment schedules, and other conditions of the loan.

- Limitation Period: To set the legal "timer" for how long the bank has the right to sue for recovery (usually 3 years for most loans in India).

- Legal Action: To provide evidence in court if a recovery suit must be filed.

- Legal Framework: Banks must follow multiple laws, including the Indian Contract Act, Companies Act, Partnership Act, and Indian Registration Act.

- Variations:

- Documents are not "one size fits all"; they change based on the type of loan (e.g., Cash Credit vs. Term Loan), the type of security (e.g., a car vs. a house), and the type of borrower (e.g., an individual vs. a company/legal entities).

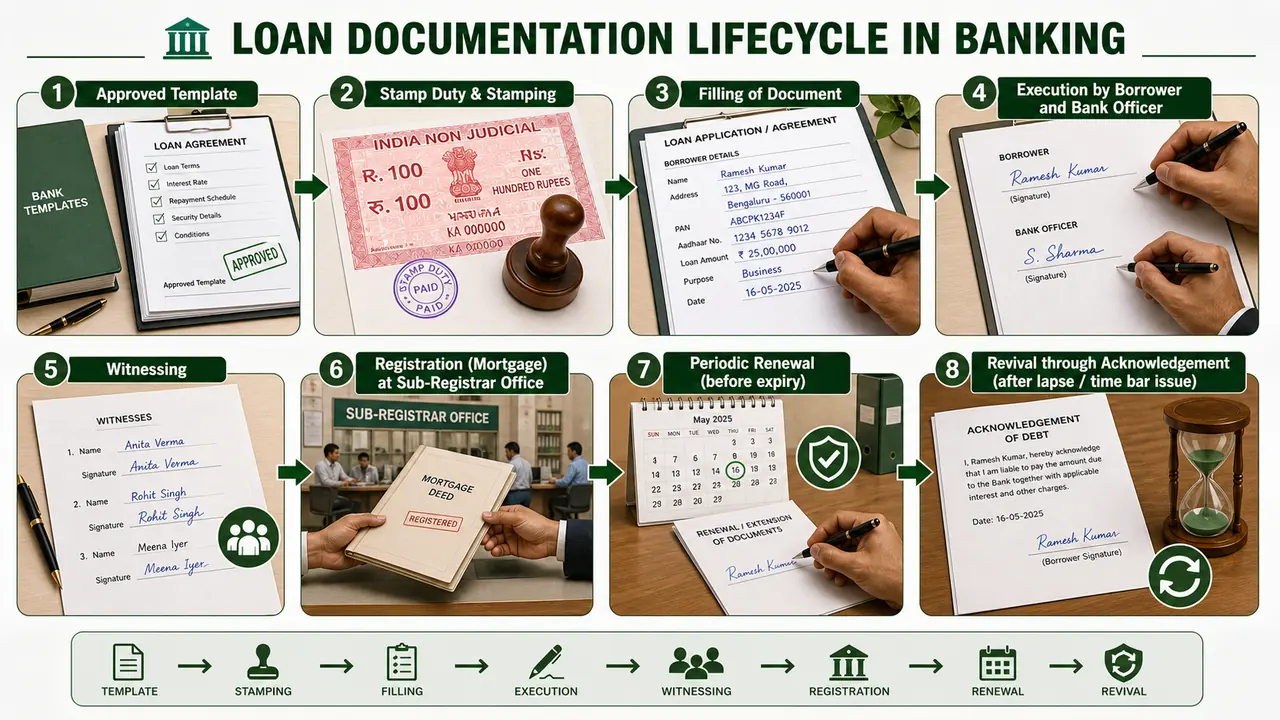

Documentation Process

The lifecycle of a document from creation to legal maintenance.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Documentation (General Principles)

The legal foundation for what a "document" is and why it is critical for bank loans.

- Legal Definition: According to the Indian Evidence Act, a document is any matter expressed upon any substance using letters, figures, or marks to record information. This means even a digital file or a handwritten note can be a document.

- Purpose of Loan Documents:

- Identification: To clearly identify the borrower and the collateral (securities).

- Binding Terms: To fix the specific interest rates, repayment schedules, and other conditions of the loan.

- Limitation Period: To set the legal "timer" for how long the bank has the right to sue for recovery (usually 3 years for most loans in India).

- Legal Action: To provide evidence in court if a recovery suit must be filed.

- Legal Framework: Banks must follow multiple laws, including the Indian Contract Act, Companies Act, Partnership Act, and Indian Registration Act.

- Variations:

- Documents are not "one size fits all"; they change based on the type of loan (e.g., Cash Credit vs. Term Loan), the type of security (e.g., a car vs. a house), and the type of borrower (e.g., an individual vs. a company/legal entities).

Documentation Process

The lifecycle of a document from creation to legal maintenance.

- Correct Format: Using the bank's approved legal templates.

- Proper Stamp Duty: Paying the required state government tax to make the document legally valid and admissible in court.

- Filling of Document: Ensuring all blanks (names, amounts, dates) are accurately completed before signing.

- Signatures: Must be signed by the borrower, all borrowers in joint loan and, if applicable, witnessed.

- Registration: Certain documents (like property mortgages) must be recorded with a government Sub-Registrar to be legally binding.

- Keeping Valid/Renewal/Revival:

- Renewal: Replacing old documents with new ones (often during loan renewal).

- Revival: Obtaining a "Revival Letter" or "Acknowledgment of Debt" from the borrower before the limitation period expires to "reset" the 3-year clock for legal action.

Documents with Multiple Dates/Places

Specific technicalities often found in legal agreements.

- Multiple Dates: If a document has more than one date (e.g., Jan 22 and Jan 26), the latest date (Jan 26) is the official date used for calculating the limitation period and due dates.

- Multiple Places: A document signed in different locations is still valid, but banks must ensure it has proper stamp duty paid according to the laws of each respective place.

- Competency: Documents must be signed only by persons legally "competent" to do so (e.g., adults of sound mind, or authorized directors for a company).

- Registration as per Indian Registration Act

Summary Table

| Step | Key Requirement |

|---|---|

| Stamping | Must be done before or at the time of execution (signing). |

| Execution | Signing by the borrower and authorized bank officials. |

| Witnessing | Required for specific documents like Mortgage Deeds. |

| Registration | Mandatory for documents involving transfer of immovable property. |

Types of documents

- Agreements

- Promissory notes (PN)

- Forms

Legal Provisions for Stamp Duty

Stamp duty is a mandatory tax governed by the Indian Stamp Act 1899.

Authority and Jurisdiction

| Authority | Scope | Examples of Documents |

|---|---|---|

| Central Govt. | 10 Documents (Uniform duty across India) | Promissory Note, Bill of Exchange, Cheque, LC, Bills of Leading (BL), Money Receipt. |

| State Govt. | 55 Documents (Duty differs from state to state) | Mortgage deed, Partnership deed, Hypothecation deed, Power of Attorney, Acknowledgement of debt letter. |

Specific Stamp Duty Rates (Central Govt.)

- Bills of Exchange: It can be of 2 types.

- Demand bill: Nil (No duty).

- Usance bill: Ad valorem (Based on time and amount).

- Exemptions: (1) Export usance bills and (2) usance up to 90 days where a bank is a party.

- Demand Promissory Note (DPN):

- Up to Rs. 250: 5 P.

- Above Rs. 250 to Rs. 1000: 10 P.

- Above Rs. 1000: 15 P.

- Usance Promissory Note: Ad valorem.

- Money Receipt:

- Up to Rs. 5000: No duty.

- Above Rs. 5000: Re. 1 is payable.

- Letter of Credit (LC): Rs. 1.

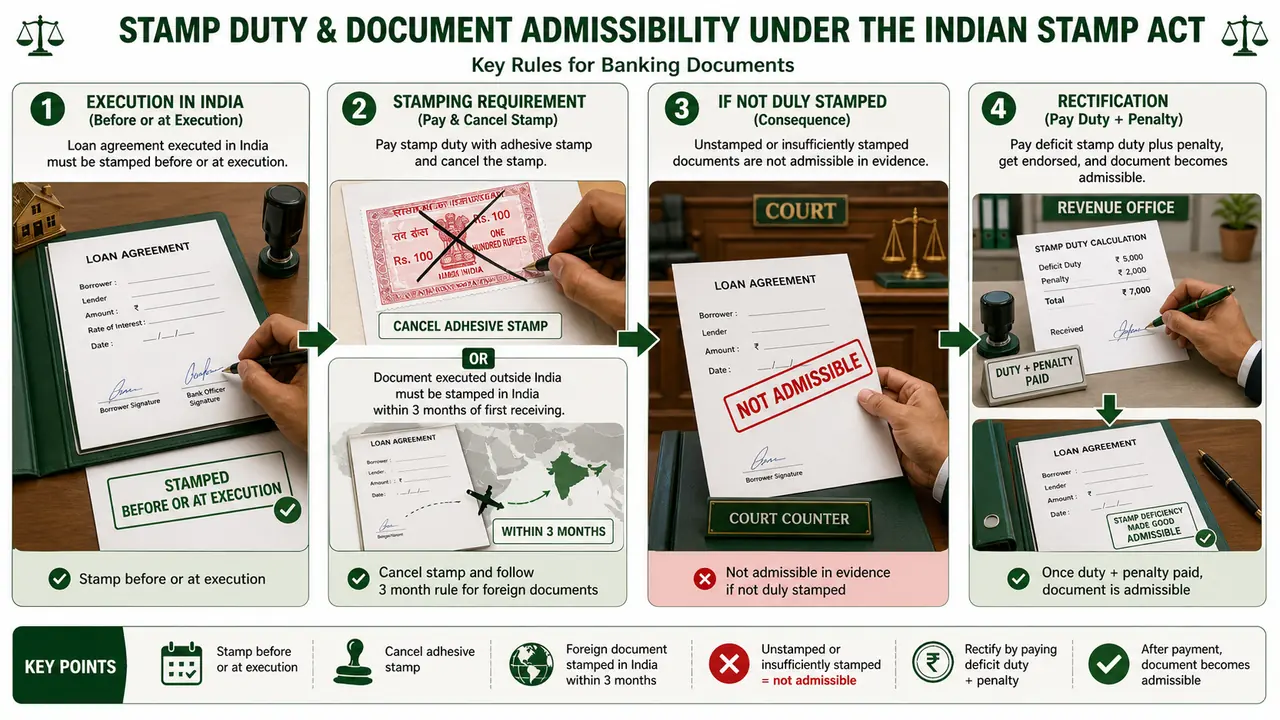

Rules for Payment and Stamping

Strict timelines and methods apply to ensure a document is legally "admissible" in court.

1. Timing and Cancellation

- Time for payment: Duty must be paid either before or at the time of signatures (Section 17, Indian Stamp Act 1899).

- Post-signature payment: If duty is paid after signatures, the document is treated as un-stamped.

- Court Admissibility: Documents without proper stamp duty are not accepted by courts as evidence (Section 35, Indian Stamp Act).

- Adhesive Stamps: Must be cancelled so they cannot be reused.

- If not cancelled, the document is treated as un-stamped.

- Cancellation is done by putting a cross or signing across the stamp.

2. Documents Signed Outside India

- General Documents: If executed abroad but used in India, duty must be paid within 3 months of its first arrival in India (Section 18, Indian Stamp Act 1899).

- Negotiable Instruments: If signed abroad, duty payment must be made before acceptance or negotiation.

3. Rectifying Errors (Unstamped/Under-stamped)

- These can be validated later with the permission of the State Govt..

- The State recovers the difference in duty plus a fine.

- Fine amount: Minimum Rs. 5 and maximum 10 times the difference of the duty.

- Refunds: If duty is paid but the stamp is not used, a refund can be obtained within 6 months.

- Usage: Once stamp duty is paid, it can be used at any time.

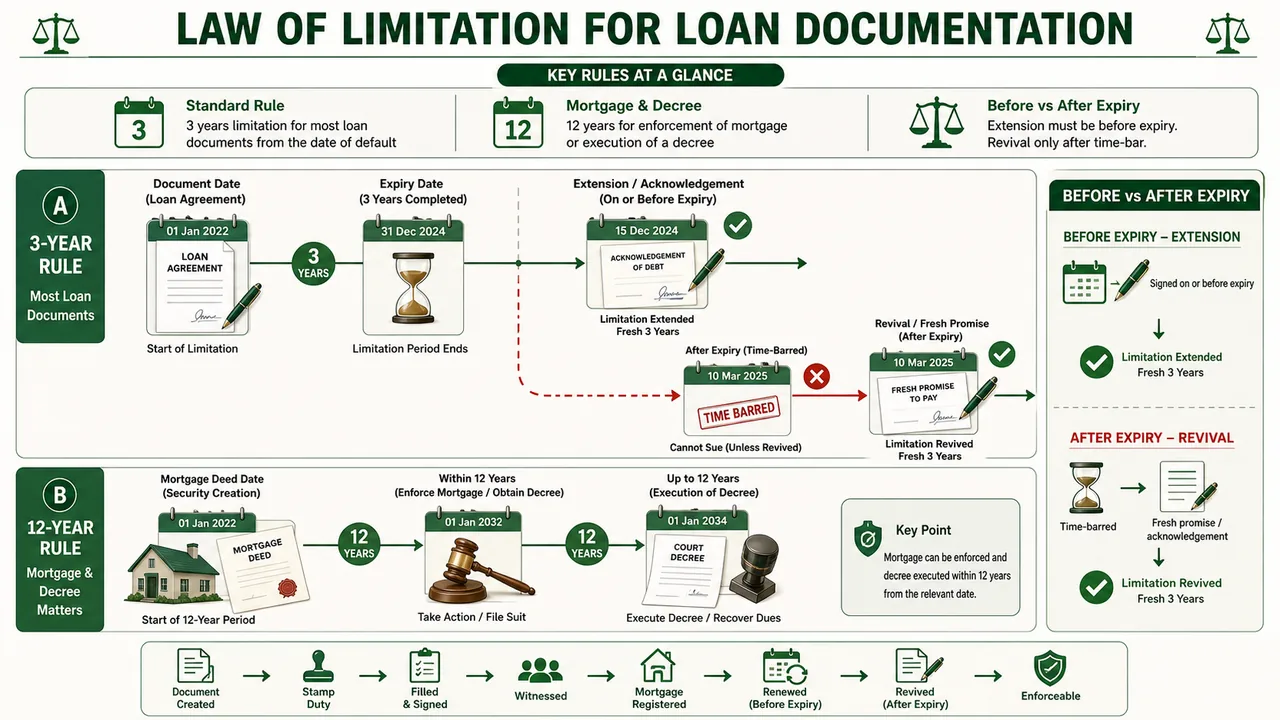

Law of Limitation

The Law of Limitation in India is governed by the Limitation Act, 1963. Fundamentally, this law defines the specific lifespan of a legal claim. For a creditor, such as a bank, the "Limitation Period" is the strictly defined window of time during which they can file a lawsuit in court to recover their money. Once this period expires, the bank loses its legal remedy to sue, and the document is considered "Time Barred."

How the Time Limit Varies

The key principle is that limitation periods are not uniform. They differ depending on the type of loan, the security involved, and the specific starting point (trigger date) for the countdown.

1. The Standard 3-Year Limitation

For most common banking transactions, the limitation period is 3 years. However, the "starting date" for this 3-year countdown changes based on the nature of the facility:

- Immediate Start (Date of Document/Transaction): For Demand Loans, Cash Credit (CC), and Overdrafts (OD), the 3-year clock starts ticking immediately from the date of the document. Similarly, for Bills Purchased, the 3 years begin from the date of purchase.

- Deferred Start (Due Dates & Demands):

- Term Loans (TL): The 3-year period does not start at signing. Instead, it applies to each instalment individually, starting from the due date of the unpaid instalment.

- Bills Discounting: The 3-year period begins from the bill's due date.

- Guarantors: The limitation against a guarantor (3 years) only begins when the bank explicitly recalls the loan (demands payment) from the guarantor.

- Deposit Accounts: If a customer sues a bank, the 3 years start from the date the customer demanded the return of the deposit.

2. The 12-Year Exception (Mortgages & Court Orders)

There are specific scenarios where the law grants a much longer period of 12 years:

- Mortgage Property: If the bank wants to enforce its rights against the specific property mortgaged (e.g., selling the house to recover dues), they have 12 years from when the debt became due.

- Important Distinction: If the bank wants to sue the Mortgager personally (for money beyond the property value), the limit is only 3 years, not 12.

- Execution of Decree: Once a bank wins a court case and gets a judgment (decree), they have 12 years to execute it (collect the assets).

3. The Government Exception

The government holds a privileged position. For any suit filed by the Government, the limitation period is extended significantly to 30 years.

Rules for Calculating the Period

The precise rules on how to calculate these dates to avoid a document becoming "Time Barred":

- Exclusion of the First Day: When calculating the period, the actual date of the document is excluded. You technically start counting from the next day.

- The Calculation Example: Despite the exclusion rule, the mathematical deadline usually lands on the same calendar date.

- Example: If a document is dated Jan 22, 2015, and the period is 3 years, the limitation is valid up to Jan 22, 2018.

- On Jan 23, 2018, the document becomes Time Barred, meaning a suit can no longer be filed.

- Court Closure Rule: If the last day of the limitation period falls on a day when the court is closed (e.g., a holiday or Sunday), the bank is granted an extension. The suit can be validly filed on the first day the court reopens.

Extension of Limitation Periods (General Rules)

- Can be extended when available.

- In above example it can be extended on or before Jan 22, 2018.

- The "extension" of a limitation period is only possible while the loan is still active (i.e., within the valid limitation period). Using the previous example, if the deadline is Jan 22, 2018, you must get the extension signed on or before that specific date.

Revival of limitation period

- After it expires (i.e. on Jan 23 onwards) it cannot be extended.

- Once the deadline date has passed (e.g., Jan 23 arrives), the option to simply "extend" the time limit is gone forever. The document is now time-barred.

- It can be revived by obtaining fresh promise to pay (i.e. new documents for the time barred loan)

- If the period has expired, you need a "Revival," not an extension. This is legally harder; it requires the borrower to sign a completely new set of documents promising to pay the old, expired debt.

Extension of Limitation Periods (Methods)

A. Obtaining acknowledgement of debt from the borrower (such letters are obtained annually by banks)

- (called an Acknowledgement of Debt or AOD) every year to keep the limitation period fresh.

- A public acknowledgement (bank shown as creditor, in the balance-sheet by the borrower)

- If the borrower is a company and they publish their annual balance sheet listing the bank as a creditor they owe money to, this counts as a "public acknowledgement." This act automatically extends the limitation period because they have publicly admitted the debt exists.

B. By part payment of the loan.

- If the borrower makes a partial payment toward the loan, the limitation period resets. The 3-year countdown starts over from the date that payment was made.

- This should be done by the borrower or his agent.

- For these methods (acknowledgement or payment) to be legally valid, the action must be taken by the borrower themselves or their legally authorized agent/representative.

Extension of Limitation Periods (Entities)

- For a joint loan account, acknowledgement by one of them, extends the limitation against all joint borrowers.

- In a joint loan (e.g., husband and wife), if only one person signs the acknowledgement letter, it is legally sufficient to extend the time limit for all the borrowers on that account.

- For a partnership firm, acknowledgement can be done by one of them.

- If the borrower is a partnership firm, any single partner has the authority to sign the acknowledgement, and it will bind the entire firm.

- For a company, it is to be done by a person authorised by Board of the Company.

- Explanation: For a corporate borrower, a random employee cannot sign. The acknowledgement must be signed by a specific person (like a Director) who has been explicitly authorized to do so by a resolution from the company's Board of Directors.

- For an HUF, it can be done by Karta.

- Explanation: In a Hindu Undivided Family (HUF) account, the "Karta" (the head of the family) is the person authorized to sign the acknowledgement to extend the limitation.

- For club or society, it can be by authorised persons.

- Explanation: For organizations like clubs or societies, the bylaws usually designate specific office bearers (like the Secretary or President) who are authorized to sign such legal documents.

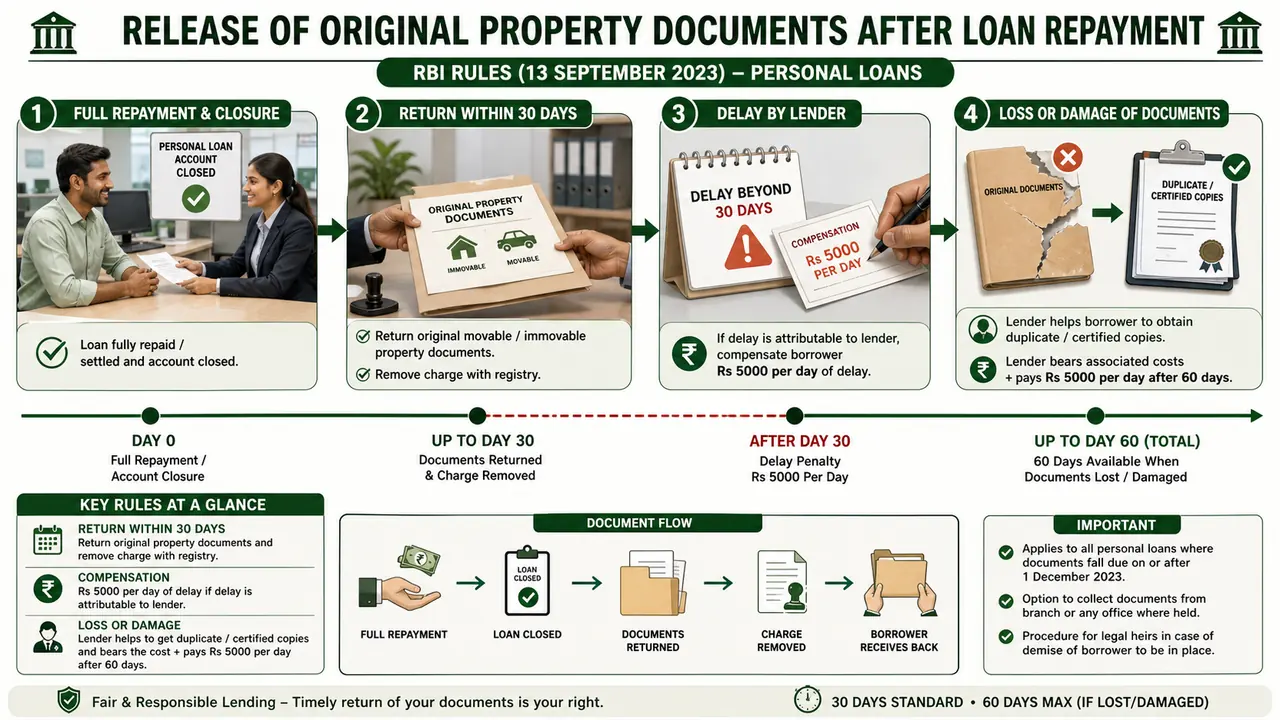

Release on Security Documents

On full payment of loans (RBI 13.09.23)

- RBI's guidelines will be applicable for personal loans, where release falls due on or after 01.12.2023

- Time limit for release - within 30 days from date of full repayment of loan.

- In case of delay beyond 30 days - Compensation of Rs. 5000 per day, of delay period.

- Loss or damage to documents - Bank will bear the cost and assist in getting duplicate, within 60 days.

- In case of delay beyond 60 days, Compensation of Rs. 5000 per day, of delay period.

Summary Questopms

-

Which date is date of document if 2 dates..

Latest date

-

Stamp duty on demand PN of Rs.600..

10 P

-

Stamp duty exempted on which usance BoE..

(1) Export usance bills and (2) usance up to 90 days where a bank is a party.

-

Which document cannot be validated by paying difference amount and fine..

All documents can be revalidated irrespective of type.

-

Document date Jul 12, 2008. Limitation 3 years. Suit can be filed up to..

Jul 12, 2011

-

A will is signed in US and to be used in India. Stamp duty payment time limit..

Within 3 months from date of arrival.

-

Limitation against guarantor begins..

When bank recall finance from them.

-

Example public acknowledgement of debt..

Including in liability side of Balance sheet.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Document (legal definition) | Any matter expressed on any substance using letters, figures, or marks (Indian Evidence Act) |

| Purpose of loan documents | Identification of borrower/collateral, binding terms (interest/repayment), setting limitation period, evidence in court |

| Document types | Agreements, Promissory Notes (PN), Forms; vary by loan type, security type, and borrower type |

| Documentation process | Correct format → stamp duty → fill blanks → signatures → registration (if required) → renewal/revival |

| Multiple dates on document | Official date = latest date (used for limitation period and due dates) |

| Multiple places | Valid; must ensure proper stamp duty paid per each location's laws |

| Stamp duty authority | Central Govt: 10 documents (uniform across India — PN, BoE, cheque, LC, BL, money receipt); State Govt: 55 documents (varies by state — mortgage deed, hypothecation deed, etc.) |

| Demand Promissory Note duty | Up to ₹250: 5 P; ₹250-₹1000: 10 P; above ₹1000: 15 P |

| Demand Bill of Exchange | Nil duty |

| Usance BoE exemptions | (1) Export usance bills and (2) usance up to 90 days where bank is a party |

| Money receipt duty | Up to ₹5000: nil; above ₹5000: Re. 1 |

| Letter of Credit duty | Rs. 1 |

| Timing of stamp duty | Must be paid before or at the time of signing (Sec 17, Indian Stamp Act 1899); post-signature = treated as un-stamped |

| Un-stamped documents | Not accepted by courts as evidence (Sec 35, Indian Stamp Act) |

| Documents signed abroad | General: duty within 3 months of first arrival in India (Sec 18); Negotiable instruments: before acceptance/negotiation |

| Rectifying un-stamped/under-stamped | Permission of State Govt; fine: minimum ₹5, maximum 10 times the duty difference |

| Stamp refund | If stamp not used, refund obtainable within 6 months |

| All documents can be revalidated | Irrespective of type, by paying difference and fine |

| Limitation Act, 1963 | Defines the lifespan of a legal claim; after expiry, document is "Time Barred" |

| Standard limitation: 3 years | Applies to Demand Loans, CC, OD (from date of document); Term Loans (from due date of each instalment); Bills Discounting (from bill's due date); Guarantors (from date bank recalls finance) |

| 12-year limitation | Mortgage property (for sale of property); Execution of court decree |

| Government suits | Extended limitation of 30 years |

| Calculating limitation | First day excluded; e.g., document dated Jul 12, 2008 with 3-year limit → suit valid up to Jul 12, 2011; time-barred from Jul 13 |

| Court closure rule | If last day falls on holiday, suit can be filed on first day court reopens |

| Extension of limitation | Must be done before expiry; via (A) Acknowledgement of Debt (AOD) annually, or (B) part payment of loan |

| Public acknowledgement | Borrower listing bank as creditor in balance sheet = automatic extension |

| Revival (after expiry) | Requires fresh promise to pay (new documents for time-barred loan); cannot simply extend |

| Joint loan | Acknowledgement by one borrower extends limitation for all joint borrowers |

| Partnership firm | Acknowledgement by any one partner binds the entire firm |

| Company | Must be signed by person authorized by Board (e.g., Director with Board resolution) |

| HUF | Acknowledgement by Karta (head of family) |

| Release of security documents (RBI) | Within 30 days of full repayment; delay penalty: ₹5,000 per day |

| Loss/damage to documents | Bank bears cost; duplicate within 60 days; delay penalty: ₹5,000 per day |

| Applicability | Personal loans where release falls due on or after 01.12.2023 |

Lesson Doubts

Ask questions, get expert answers