🏦 Opening & Maintenance of Current Accounts and Overdraft Accounts

RBI directions on opening and maintaining current accounts (CA) and overdraft (OD) accounts — exposure-based eligibility, collection accounts, exemptions, compliance monitoring, and escrow accounts (w.e.f. 1st April 2026).

Opening and Maintenance of Current Accounts and Overdraft Accounts

Current Accounts (CA), Overdraft (OD) accounts, and Cash Credit (CC) accounts are used as transaction accounts by borrowers. Since funds flow freely through these accounts, they raise concerns relating to credit monitoring by lenders — a borrower could route funds through a bank that hasn't lent to them, making it harder for lending banks to track end-use of funds.

Objective: These rules are designed to prevent the "diversion of funds" (borrowers using money for unintended purposes) and ensure better credit monitoring.

To address this, the RBI issued revised directions that become operative with effect from 1st April, 2026.

Legal Basis

These directions are issued under two key provisions of the Banking Regulation Act, 1949:

- Section 21 of BR Act — Empowers RBI to issue directions to banks for control over advances (loans, credit facilities, etc.)

- Section 35A of BR Act — Empowers RBI to issue directions to banks in the public interest or to prevent the affairs of the bank from being conducted in a manner detrimental to depositors' interests

Key Point: These restrictions apply only when exposure is ₹10 crore or more. Below ₹10 crore, there are no restrictions.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Opening and Maintenance of Current Accounts and Overdraft Accounts

Current Accounts (CA), Overdraft (OD) accounts, and Cash Credit (CC) accounts are used as transaction accounts by borrowers. Since funds flow freely through these accounts, they raise concerns relating to credit monitoring by lenders — a borrower could route funds through a bank that hasn't lent to them, making it harder for lending banks to track end-use of funds.

Objective: These rules are designed to prevent the "diversion of funds" (borrowers using money for unintended purposes) and ensure better credit monitoring.

To address this, the RBI issued revised directions that become operative with effect from 1st April, 2026.

Legal Basis

These directions are issued under two key provisions of the Banking Regulation Act, 1949:

- Section 21 of BR Act — Empowers RBI to issue directions to banks for control over advances (loans, credit facilities, etc.)

- Section 35A of BR Act — Empowers RBI to issue directions to banks in the public interest or to prevent the affairs of the bank from being conducted in a manner detrimental to depositors' interests

Key Point: These restrictions apply only when exposure is ₹10 crore or more. Below ₹10 crore, there are no restrictions.

Cash Credit (CC) Accounts — Fully Exempt

An important distinction: Cash Credit (CC) accounts are fully exempt from these restrictions. CC is treated as a core working capital product and is not subject to the CA/OD opening restrictions. Banks can freely maintain CC accounts for their borrowers regardless of exposure levels or the 10% eligibility rule.

Key Definitions

Before diving into the rules, understand these terms clearly:

- Banking System: All banks (Public, Private, Co-operative) except Payment Banks. Payment Banks cannot lend, so they are excluded from these directions.

- Exposure: The total of all sanctioned fund-based credit facilities and non-fund-based facilities from the banking system to a borrower. This is the aggregate across all banks — not just one bank's share.

- Fund-based facilities: Cash loans, Overdrafts, Term Loans

- Non-fund-based facilities: Bank Guarantees (BG), Letters of Credit (LC)

Category A — Exposure Less Than ₹10 Crore

When the borrower's total exposure from the banking system is below ₹10 crore, the rules are simple:

- Any bank may open and maintain a current account or OD account for such a borrower without any restrictions.

- Both lending and non-lending banks can freely open and maintain CA/OD accounts.

This recognises that small borrowers pose limited systemic credit-monitoring risk, so banks are given full flexibility. The strict monitoring rules do not apply to them.

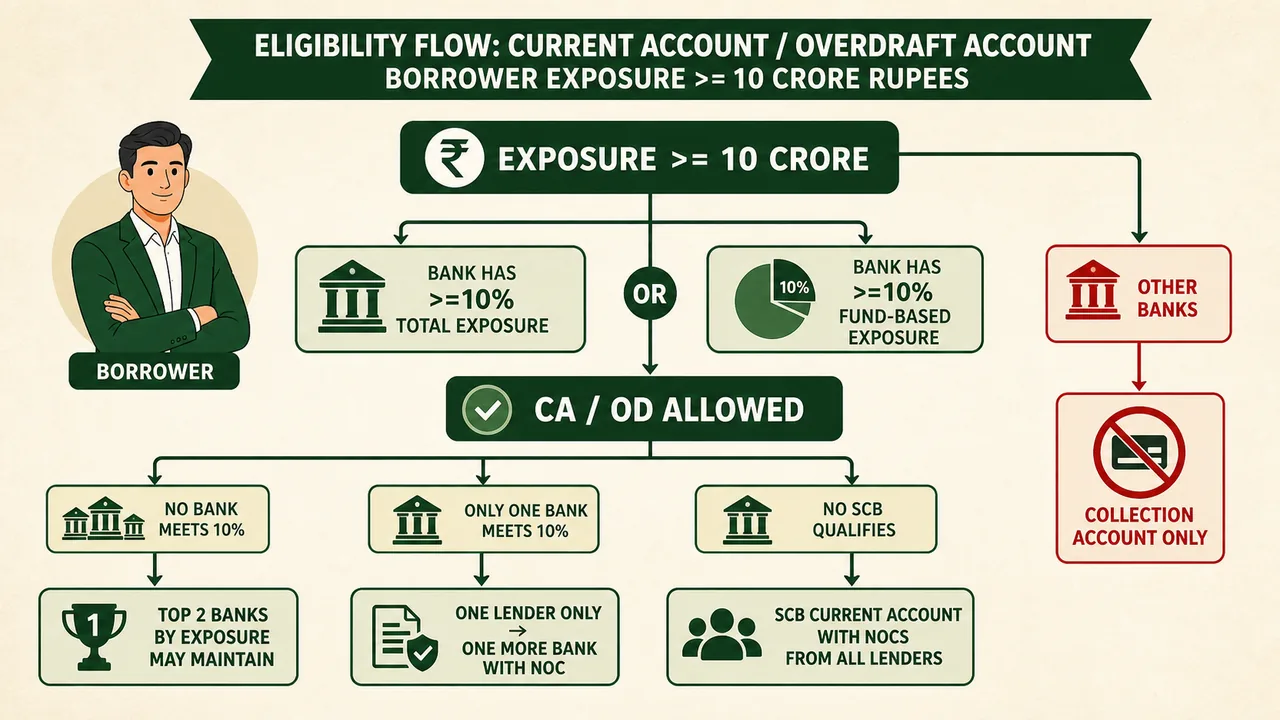

Category B — Exposure of ₹10 Crore or More

When the borrower's aggregate exposure from the banking system is ₹10 crore or more, strict restrictions apply. A borrower cannot just open a current account with any random bank — they must follow the "10% Rule".

The Main Rule (Eligibility Criteria)

A bank may maintain current accounts or OD accounts if it has either:

- (A) A minimum 10% share in the banking system's aggregate exposure to the borrower, OR

- (B) A minimum 10% share in the banking system's aggregate fund-based exposure to the borrower.

Meeting either threshold qualifies the bank.

Logic: If a bank has lent a large chunk of money (10%+), they have "skin in the game" and will monitor the funds properly.

Special Conditions (When Criteria Aren't Met)

The RBI provides fallback rules to ensure borrowers always have access to transaction banking:

(a) No single big lender: If no bank meets the 10% criteria, or only one bank meets it (e.g., the loan is split across 20 small banks) — the 2 banks having the largest exposures to the borrower may maintain such accounts.

(b) Single lender: If only one bank has exposure to the borrower — one more bank may maintain a CA, but only after obtaining a No-Objection Certificate (NOC) from the lender bank.

(c) Non-SCB lenders: If no Scheduled Commercial Bank (SCB) meets the criteria and the borrower desires to have a CA with an SCB (e.g., borrower has loans only from Co-operative banks or NBFCs) — the borrower can do so after obtaining NOCs from all banks that have exposure to them.

(d) Non-eligible banks: Other banks that do not meet the eligibility criteria may maintain only collection accounts — these are restricted to receiving cash inflows on behalf of the borrower.

Treatment of Non-Lending Banks

Non-lending banks (banks that have not lent to the borrower) have different treatment based on the exposure threshold:

| Borrower's Exposure | Non-Lending Bank's Permission |

|---|---|

| Less than ₹10 crore | No restriction — can open and maintain CA/OD freely |

| ₹10 crore or more | Can only open Collection Account — no full CA/OD |

Key Point: A non-lending bank can never qualify for the 10% rule (since it has zero exposure). Therefore, when exposure is ₹10 crore or more, it can only maintain a collection account for the borrower.

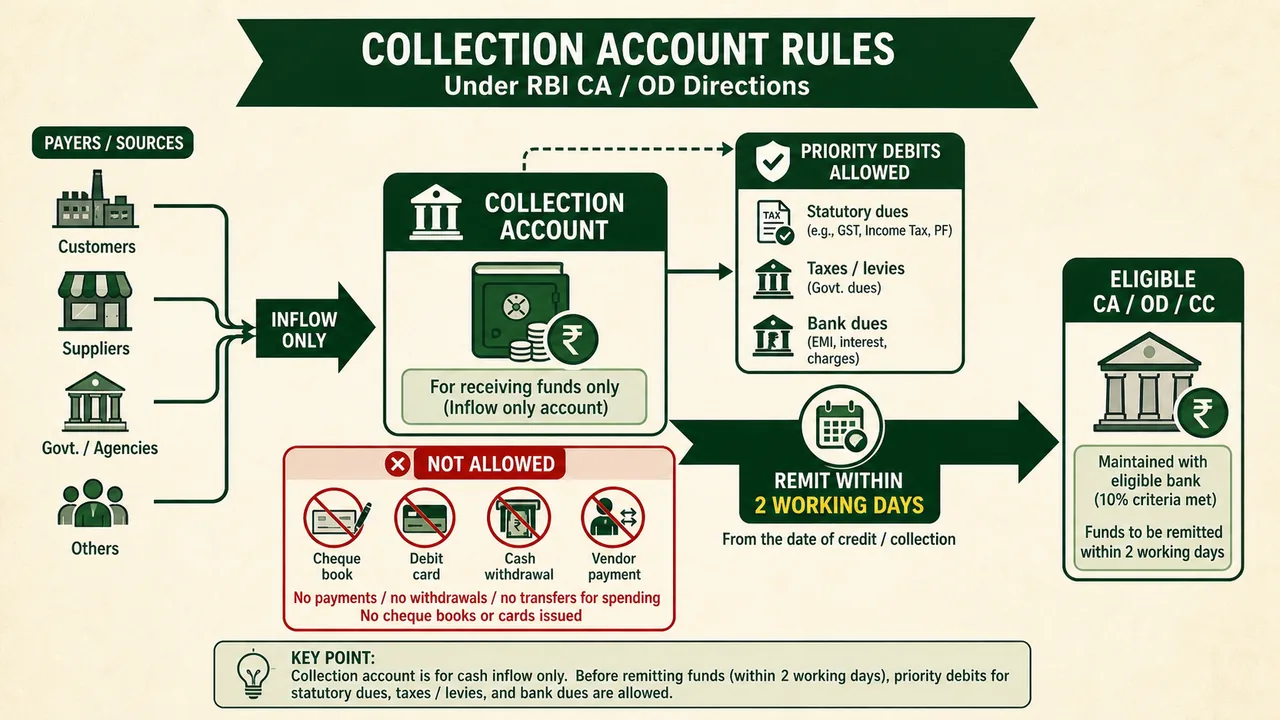

Collection Accounts

What if a bank has lent money to a borrower but holds less than 10% of the exposure? They cannot open a regular transactional Current Account. They can only open a "Collection Account".

Rules for Collection Accounts

- Inflow Only: These accounts are essentially for receiving money (deposits). The borrower cannot use this account to pay vendors or withdraw cash. No cheque books or cards are issued.

- Who Can Open: Banks that do not meet the 10% eligibility rule can only open Collection Accounts. This includes non-lending banks when exposure is ₹10 crore or more.

- The 2-Day Rule: Funds collected in this account must be remitted within two working days to a designated CC, CA, or OD account maintained with an eligible bank.

- Priority Debits (Statutory Dues Exception): Before remitting funds, the following may be debited first:

- Statutory dues — GST, Income Tax, PF contributions

- Taxes and other government levies

- Bank dues — EMIs, interest, or charges owed to the bank

The tight remittance window ensures funds are quickly routed to accounts where lending banks can monitor them.

Exemptions from Restrictions

The above restrictions on opening and maintaining CA/OD accounts are not applicable to the following:

- FEMA Accounts — Accounts opened as per the provisions of the Foreign Exchange Management Act, 1999, for foreign exchange transactions.

- Government/Regulator-directed Accounts — Accounts or transactions under instruction of a financial sector regulator (SEBI, IRDAI, etc.), or the Central Government or a State Government.

- Regulated Entity Accounts — Accounts of entities regulated by a financial sector regulator (Mutual Funds, Insurance companies, etc.), used for carrying out their regulated activities.

- Product-Specific Current Accounts — Sometimes a bank needs to open a current account purely to service a specific product it has sold — for example, a loan repayment account where EMI collections are received, or a trade finance account linked to an LC. These are not general-purpose transaction accounts; they exist only to support that one product. RBI allows these even if the bank doesn't meet the 10% rule, but with strict limits (no cash, no cheque book, no discretionary debits).

Operational Limits on Product-Specific Accounts

When a bank is permitted to maintain a product-specific current account (such as a loan servicing account), the following operational restrictions apply:

- No cash transactions permitted through the account

- No cheque books or debit cards are issued for such accounts

- No discretionary debits — only pre-authorised or product-related debits allowed

- Surplus funds must be transferred to a designated eligible account maintained with a bank that meets the 10% eligibility criteria

These restrictions ensure that product-specific accounts are used strictly for their intended purpose and do not become a backdoor for unrestricted fund movement.

RBI Mandate for Banks

The RBI has laid down clear rules on how banks must use and manage CA/OD accounts:

- Authorised Use Only: Accounts must be used only for the account-holder's own legitimate business activities. Banks must ensure the account is not misused for purposes other than what was declared at the time of opening.

- No Pass-Through Transactions: CA/OD accounts cannot be used to route third-party funds. A borrower cannot use their current account to pass money on behalf of another entity — unless the entity is specifically licensed by a financial sector regulator to do so (e.g., payment aggregators).

- Deposit/Payment Restrictions: Entities not licensed by RBI cannot accept deposits or provide payment services through these accounts. This prevents unregulated entities from using bank accounts to mimic banking functions.

- Mandatory CBS Flagging: Banks must implement system-level identification through their Core Banking Solution (CBS) to flag and track accounts that fall under these CA/OD directions. This enables automated monitoring and compliance.

Compliance Monitoring

Banks cannot just check eligibility once and forget about it:

- Half-Yearly Review: Accounts shall be monitored on a regular basis, and in any case at least once every half-year to verify the bank still meets the 10% criteria.

- If Eligibility is Lost: If a bank is found to be no longer eligible to maintain a CA or OD account — it shall notify the customer within one month, directing them to either:

- Convert the account to a collection account, or

- Close the account: This conversion/closure must be completed within three months of the notification.

Term Loan End-Use Monitoring

This rule prevents borrowers from touching the loan money directly:

- Direct Remittance: Term loans shall preferably be remitted directly to the intended beneficiary's account (e.g., the machinery seller/supplier) or for the specified end-use, where such beneficiary is identifiable, rather than routing funds through the borrower's account.

- No Routing Through Borrower's Account: The loan proceeds should not be routed through the borrower's CA/OD account and then paid out. This prevents diversion of term loan proceeds through transaction accounts.

- Why? To ensure the money is used exactly for the purpose it was borrowed for.

Escrow Mechanism — Removed

In the previous version of the CA/OD directions, the RBI had prescribed an escrow mechanism — where borrowers' funds were routed through an escrow account to ensure proper credit monitoring. In the revised 2026 directions, the escrow mechanism has been removed completely.

Why removed? The escrow mechanism was operationally complex for both banks and borrowers. The revised framework replaces it with simpler eligibility rules (10% threshold) and collection accounts, achieving the same goal of credit monitoring with less friction.

What is an Escrow Account? (For Reference)

An Escrow Account is a special type of account where funds are held by a third party on behalf of two other parties that are in the process of completing a transaction.

- The funds are held until receiving appropriate instructions or until the fulfilment of predetermined contractual obligations.

- Escrow accounts are commonly used in real estate transactions, M&A deals, and large project payments to ensure both parties meet their obligations before funds are released.

Summary Cheat Sheet

| Concept / Rule | Key Details |

|---|---|

| Effective Date | 1st April, 2026 |

| Legal Basis | Section 21 (control over advances) and Section 35A (public interest directives) of BR Act, 1949 |

| Objective | Prevent diversion of funds and ensure better credit monitoring |

| Banking System (definition) | All banks (Public, Private, Co-operative) except Payment Banks |

| Exposure (definition) | Total of all sanctioned fund-based + non-fund-based facilities |

| Fund-based facilities | Cash loans, Overdrafts, Term Loans |

| Non-fund-based facilities | Bank Guarantees (BG), Letters of Credit (LC) |

| CC accounts | Fully exempt — treated as core working capital product |

| Exposure < ₹10 crore | Any bank may maintain CA/OD without restrictions |

| Exposure ≥ ₹10 crore — Eligibility | Bank must have ≥10% share in aggregate exposure OR ≥10% in aggregate fund-based exposure |

| No bank / only 1 bank meets criteria | 2 banks with largest exposures may maintain CA/OD |

| Only 1 bank has exposure | One more bank may maintain CA after getting NOC from lender bank |

| No SCB meets criteria | Borrower can open CA with SCB after NOCs from all banks |

| Non-eligible banks | May only maintain collection accounts (cash inflow receipts only) |

| Non-lending banks (≥₹10 Cr) | Can only open Collection Account — no full CA/OD |

| Non-lending banks (<₹10 Cr) | No restriction — can open CA/OD freely |

| Collection account — inflow only | No debits for spending; no cheque books/cards; only for receiving money |

| Collection account — remittance | Funds to be remitted within 2 working days to designated CC/CA/OD |

| Collection account — priority debits | Statutory dues, taxes, and bank dues may be debited before remittance |

| Product-specific accounts | Allowed with limits (e.g., loan servicing); no cash, no cheques, no discretionary debits |

| Surplus in product-specific accounts | Must be transferred to designated eligible account |

| Exemption 1 | Accounts under FEMA, 1999 |

| Exemption 2 | Accounts under instruction of regulator / Central / State Government |

| Exemption 3 | Accounts of regulated entities for their regulated activities |

| Exemption 4 | Product-specific current accounts (e.g., loan servicing) allowed with limits |

| Authorised use only | Accounts for account-holder's own legitimate business only |

| No pass-through transactions | Cannot route third-party funds unless licensed by financial regulator |

| Deposit/payment restrictions | Entities not licensed by RBI cannot accept deposits/provide payment services |

| Mandatory CBS flagging | Banks must flag accounts in CBS for system-level identification |

| Monitoring frequency | At least once every half-year |

| Ineligibility — notification | Notify customer within 1 month |

| Ineligibility — conversion/closure | Complete within 3 months |

| Escrow mechanism | Removed completely in the revised 2026 directions |

| Term loan routing | Preferably remit directly to beneficiary — not through borrower's account |

Lesson Doubts

Ask questions, get expert answers