📈 Large Exposure Framework

Guidelines on Large Exposure Framework of RBI

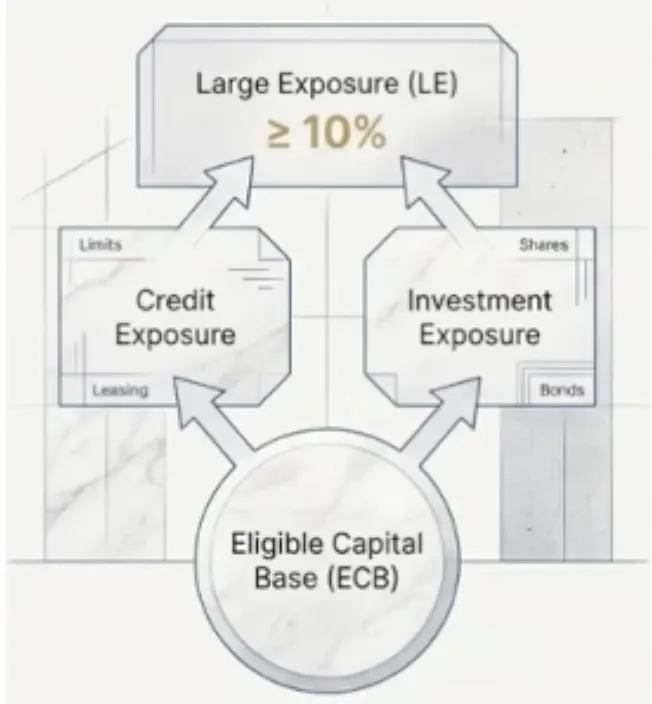

Large Exposure Framework (LEF)

- This framework is crucial for preventing banks from putting "too many eggs in one basket" by lending too much to a single person or group.

- LEF was introduced by RBI with effect from 01.04.2019, by using its powers conferred by Sections 21 and 35A of the Banking Regulation Act, 1949.

What counts as "Large Exposure"?

- Large Exposure (LE) is total value of all exposures (credit exposure and investment exposures) of a bank to a single counterparty or a group of connected counterparties, when it is 10% or above of a bank's Eligible Capital Base.

- Credit Exposure comprises all types of funded and non-funded credit limits, and facilities by way of equipment leasing, hire purchase finance and factoring services.

- Eligible capital base (ECB)

- It is the effective amount of Tier 1 capital as per last audited balance sheet.

- Capital under Tier I introduced after published balance sheet date may also be included but bank should obtain an external auditor's certificate on completion of the augmentation of capital and submit the same to RBI.

- Exclusions: Certain "exempted exposures" are not counted.

Who does this apply to?

- Scope: The framework applies to banks at two levels:

- Consolidated Group Level: The bank including its subsidiaries. So that bank don't use subsidiaries to hide this.

- Solo Level: The bank as a standalone entity.

- Effective Date: This specific framework came into effect on April 1, 2019.

Identifying "Groups" of Borrowers

Banks must identify if different borrowers are actually connected. If they are, they are treated as a single "Group Borrower," and their limits are combined.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Large Exposure Framework (LEF)

- This framework is crucial for preventing banks from putting "too many eggs in one basket" by lending too much to a single person or group.

- LEF was introduced by RBI with effect from 01.04.2019, by using its powers conferred by Sections 21 and 35A of the Banking Regulation Act, 1949.

What counts as "Large Exposure"?

- Large Exposure (LE) is total value of all exposures (credit exposure and investment exposures) of a bank to a single counterparty or a group of connected counterparties, when it is 10% or above of a bank's Eligible Capital Base.

- Credit Exposure comprises all types of funded and non-funded credit limits, and facilities by way of equipment leasing, hire purchase finance and factoring services.

- Eligible capital base (ECB)

- It is the effective amount of Tier 1 capital as per last audited balance sheet.

- Capital under Tier I introduced after published balance sheet date may also be included but bank should obtain an external auditor's certificate on completion of the augmentation of capital and submit the same to RBI.

- Exclusions: Certain "exempted exposures" are not counted.

Who does this apply to?

- Scope: The framework applies to banks at two levels:

- Consolidated Group Level: The bank including its subsidiaries. So that bank don't use subsidiaries to hide this.

- Solo Level: The bank as a standalone entity.

- Effective Date: This specific framework came into effect on April 1, 2019.

Identifying "Groups" of Borrowers

Banks must identify if different borrowers are actually connected. If they are, they are treated as a single "Group Borrower," and their limits are combined.

Criteria for Grouping

Group means an arrangement involving two or more natural or legal persons related to each other being a subsidiary, associate, joint venture or related party, satisfying one of the following criteria:

- A) Control relationship Criteria:

- A counterparty, directly or indirectly, has control over the other (this criterion is satisfied if one entity owns more than 50% of the voting rights of the other entity)

- Explanation: If Company A owns 51% of Company B, Company A controls Company B. They are one group.

- B) Economic Interdependence Criteria:

- A counterparty were to experience financial problems, in particular during or after a funding or repayment difficulties, the other(s), as a result, would also be likely to encounter funding or repayment difficulties.

- Where 50% or more of one counterparty's gross receipts or gross expenditures (on an annual basis) is derived from transactions with other counterparty;

- Where one counterparty has fully or partly guaranteed exposure of other counterparty;

- Where entities have direct or indirect ownership of 20% or more interest in the voting power of the enterprise.

- Explanation: If Company X makes car parts and sells 90% of them to Car Manufacturer Y, Company X is economically dependent on Y. If Y fails, X fails. They are a group.

Cut-off for Identification

- Banks don't have to check every tiny borrower for connections. They are required to identify connected parties in all cases where the exposure to a single party is > 5% of the bank's capital base.

Large Exposure Ceilings (Limits)

These are the strict maximum percentages of its Tier-1 Capital that a bank can lend.

Single Borrower Limit

- Limit: 20% of Tier-1 Capital.

- Exposure to Single Counter-party≤ 20% (In exceptional cases, Board may allow an additional 5%)

Group Borrower Limit

- Limit: 25% of Tier-1 Capital.

- Note: There was a temporary easing for COVID up to 30% or specific timeline up to June 2021, but the standard regulatory limit has generally been tightened to 25% to align with global standards.

NBFCs (Non-Banking Financial Companies)

- Exposures to NBFCs (other than a gold loan company): 20% of Tier-1 Capital

- Exposures to Gold Loan NBFCs: 7.5%

- Why lower limit? Because gold loan NBFCs are riskier than other NBFCs due to volatile gold prices.

- Ceiling may go up by 5% to 12,5% if additional exposure is on account of funds on-lent by NBCs to infrastructure sector.

- Gold loan NBFC are those NBFCs where their gold loans comprise 50% or more of their financial assets

- Exposure to connected NBFCs: 25% of Tier-1 Capital

- Context: This is strict because NBFCs themselves are financial institutions, so the risk of contagion (domino effect as they borrow from banks) is higher.

Other Exposures

1. Global Systemically Important Banks (G-SIBs) to G-SIBs Exposure

- This is the strictest limit of 15% of Tier-1 Capital, designed to prevent a "domino effect" where the failure of one global giant instantly topples another.

- The ceilings apply to G-SIBs identified by Basel Committee and published annually. When a bank becomes a G-SIB, it shall apply 15% exposure limit within 12 months from the date of becoming G-SIB.

- Explanation: G-SIBs are banks that are "too big to fail" (like JP Morgan, HSBC). To prevent a global domino effect, the limit for one G-SIB lending to another G-SIB is very tight (15%). (finacial crisis of 2008)

2. Non G-SIB to G-SIB Exposure

- This limits how much a smaller or domestic bank can lend to a global giant to 20% of its Tier-1 Capital.

- Explanation: It protects smaller banks from being overly vulnerable to the systemic risks associated with global financial volatility.

3. Indian Branches of Foreign G-SIBs

- These branches are not treated as G-SIBs themselves; they have a 20% limit when dealing with their own Head Office or other G-SIBs.

- When they deal with "regular" (Non G-SIB) banks, they are allowed a higher safety margin of 25%.

4. Indian Branches of Foreign Non-GSIBs

- These banks have more flexibility, allowing up to 25% exposure to their Head Office or other non-systemic banks.

- However, if they lend to a G-SIB, the limit tightens back to 20% to account for the systemic importance of the counterparty.

Exposure Limit Table

| From Bank (In India) | To Bank | Exposure Limit (% of Tier 1 Capital) |

|---|---|---|

| G-SIB | Another G-SIB | 15% |

| Non G-SIB | G-SIB (India or Overseas) | 20% |

| Indian Branch of Foreign G-SIB | Its Head Office / Other G-SIBs | 20% |

| Indian Branch of Foreign G-SIB | Any other (Non G-SIB) bank | 25% |

| Indian Branch of Foreign Non-G-SIB | Its Head Office / Other Non-GSIBs | 25% |

| Indian Branch of Foreign Non-G-SIB | A G-SIB | 20% |

Other Points

Additional Exposure

- Provision: A bank can lend an additional 5% exposure (above the limits mentioned) in individual cases.

- Condition: This requires specific Board Approval. It cannot be done by regular loan officers; the bank's Board of Directors must sign off on it.

On-Balance Sheet Netting

- This allows a bank to reduce its reported "exposure value" by offsetting what it owes to a client (deposits) against what the client owes the bank (loans).

- Requirement: It is only permitted if the bank has a legally enforceable agreement that allows it to "set off" the loan and deposit amounts in the event of default.

- Significance: Instead of calculating exposure based on the full loan amount (gross), the bank only counts the "Net" amount. This lowers the bank's total exposure for regulatory limits, effectively giving them more "room" to lend.

Aggregate Exposure to all NBFCs

- The Reserve Bank of India (RBI) mandates specific caps on how much a bank can lend to a single Non-Banking Financial Company (NBFC), but also expects banks to monitor the total risk across the entire NBFC sector.

- Internal Board Limits: Banks are required to set their own internal limits for their total lending to all NBFCs combined to prevent over-concentration in one industry.

- Gold-Loan NBFC Sub-limit: Because gold-loan NBFCs have unique risks (like fluctuations in gold prices), banks often set a specific sub-limit just for them.

- Significance: This ensures that if the NBFC sector faces a crisis (like a liquidity crunch), the bank isn't so heavily invested that it threatens its own financial stability.

Large Exposure Framework – Reporting

This section focuses on what banks must tell the RBI and which loans are "Exempt" (don't count towards the strict limits).

Reporting Requirements (What to tell RBI)

Banks are required to submit regular reports to the Reserve Bank of India to prove they are following the rules.

The Reporting Threshold

- Rule: Banks must report all large exposures to the RBI.

- Definition: As mentioned in previous notes, a "Large Exposure" is any exposure that is 10% or more of the bank's eligible capital base.

- Important: This includes exempted categories too. Even if a loan is "exempt" from the limit (like a loan to the Govt), if it is huge (>10%), the RBI still wants to know about it.

The "Gross" Calculation (CRM Rule)

- Rule: When calculating the value of the exposure for this report, banks must NOT subtract "Credit Risk Mitigation" (CRM).

- Explanation: CRM refers to things that reduce risk, like collateral or hedges.

- Example: If a bank lends ₹100 Cr but holds ₹40 Cr in gold as security, the "Net Risk" is ₹60 Cr.

- Reporting: However, for this RBI report, the bank must report the full ₹100 Cr (Gross Exposure). The RBI wants to see the total potential risk before safety nets.

The "Top 20" Rule

- Rule: Regardless of percentages, banks must report their 20 largest exposures.

- Why: Even if a bank is huge and its biggest borrower is only 5% of its capital (below the 10% large exposure definition), the RBI still wants to monitor the top 20 biggest borrowers to track systemic risk.

Transition from Old Rules

- Note: The previous guidelines on exposure norms officially ceased to operate on March 31, 2019. The new Large Exposure Framework (LEF) replaced them completely on April 1, 2019.

- Further, any breach of LE limits be reported immediately and be rapidly rectified.

- Review by /reporting to the Board - The bank is put up an annual review of the implementation of exposure management measures before the end of June.

Exempted Exposures (The "Safe List")

These are specific types of loans/investments that do not count towards the 20% or 25% exposure limits. Banks can lend unlimited amounts (theoretically) to these entities because they are considered zero-risk or essential for the economy.

Sovereign & Regulator Entities

- GOI and State Govt: exposures to Govt. of India and State Governments eligible for 0% Risk Weight

- RBI: Money deposited with or lent to the Reserve Bank of India.

- Guaranteed Loans: Any exposures fully guaranteed by Govt. of India;

- Secured by Govt Instruments: exposures secured by financial instruments issued by Govt. of India (like Treasury Bills) as collateral.

Banking Operations

- Intra-day Interbank: (same दिन में) Money lent to other banks for just one day (to manage liquidity).

- Intra-group Exposure: Exposure between entities within the same banking group (often subject to different internal limits).

- Clearing Activities: Money moved essentially for settling checks/payments.

Specific Sectors

- Food Credit: Loans given for the procurement of food grains (usually to agencies like FCI - Food Corporation of India). This is critical for national food security.

- NABARD Deposits: Money deposited with NABARD (National Bank for Agriculture and Rural Development) specifically when banks fail to meet their Priority Sector Lending targets.

- exposures to foreign sovereigns or their central banks with a 0% risk weight

- borrowers, to whom limits are authorised for food credit;

- clearing activities related exposures to Qualifying Central Counterparties (QCCPs). Other types of exposures not directly related to clearing services provided shall be subjected to LE limit of 25%.

- contribution to deposits / funds maintained with NABARD, NHB, SIDBI, MUDRA Ltd., for shortfall in achievement of targets for priority sector lending;

Consortium Lending

This explains how banks handle very large loans by teaming up rather than lending alone. This is critical for risk management and adhering to the exposure limits we discussed earlier.

What is Consortium Lending?

- Definition: It is a formal arrangement where two or more banks come together to provide finance to a single borrower.

- Key Concept: Instead of one bank taking the entire risk of a massive loan, a group (consortium) shares the risk.

- Common Agreement: In a consortium, the banks usually sign a common loan agreement and share the documentation, unlike in "Multiple Banking" where everyone acts separately.

When is it Compulsory?

- The Trigger: Forming a consortium becomes mandatory when the loan amount exceeds the exposure ceiling of a single bank.

- Remember the "Single Borrower Limit" (20% of Capital). If a company needs a loan that is larger than 20% of the bank's capital, the bank simply cannot lend that amount alone. It must find other banks to join in and share the loan amount.

Sharing the Security (Pari-Passu Charge)

- The Rule: How do banks share the collateral (security) if things go wrong? They hold a "Pari-Passu" charge.

- Meaning of Pari-Passu: This is a Latin term meaning "on equal footing."

- Calculation: The rights to the security are shared in the ratio of their loans.

- Example: If Bank A lends ₹60 Cr and Bank B lends ₹40 Cr against a factory worth ₹100 Cr:

- Bank A owns 60% of the rights to the factory.

- Bank B owns 40% of the rights.

- If the borrower defaults and the factory is sold, the money is split 60:40. Bank A doesn't get priority just because they are bigger.

- Example: If Bank A lends ₹60 Cr and Bank B lends ₹40 Cr against a factory worth ₹100 Cr:

RBI Requirement: Certification

- The Risk: In large accounts involving multiple banks, fraud can happen if the borrower hides information from one bank while dealing with another.

- The Solution: The RBI has made it mandatory to obtain a compliance certificate on a regular basis.

- Who can certify? This certificate must come from a qualified professional:

- CA: Chartered Accountant

- CS: Company Secretary

- CWA: Cost and Works Accountant

- What do they certify? That the borrower is strictly complying with all banking guidelines, rules, and regulations. This adds a layer of third-party verification.

Related Concepts

Difference between:

Multiple Banking

- Definition: Banks extend credit facilities to the borrower independently.

- Difference from Consortium: In Multiple Banking, there is no formal common agreement between the banks. Bank A might give a car loan, and Bank B might give a factory loan. They might not even know the details of each other's loans. This is generally considered riskier than Consortium Lending because of the lack of coordination.

Credit Syndication

- Definition: A setup where a "Mandated Bank" (Lead Arranger) arranges the funds from other banks.

- Role of Lead Bank: The lead bank does the hard work of assessing the project and finding other banks willing to lend.

- Fee: For this service, the lead bank charges a commission (essentially a finder's fee or arrangement fee). This is common for massive infrastructure projects (e.g., building an airport).

Co-Lending Model (CLM)

The Reserve Bank of India (RBI) initially released guidelines on co-origination of loans by banks and NBFCs for lending to the priority sector in September 2018. A subsequent circular from November 2020 introduced the "Co-Lending Model" (CLM) to improve credit flow to underserved sectors and offer affordable credit leveraging the banks' lower cost of funds and NBFCs' wider reach.

Why Co-lending?

- Improve priority sector lending portfolio

- Utilize NBFC partnerships for non-priority sector credit expansion

- Deploy resources profitably

- Reach underserved sectors and offer affordable credit

- Combine strengths of banks (lower cost of funds) and NBFCs (wider reach)

- Enhance the bank's customer base

- Jointly share risks and rewards with NBFCs

Key Rules (RBI 06.08.25)

- Eligible Partners: Banks can co-lend with all registered NBFCs (including HFCs).

- Criteria for Partner Institutions (NBFCs/HFCs):

- Registered with RBI/NHB

- Minimum 3 years of operation

- Profits for the last two years

- Credit rating: BBB or above, not more than a year old, from an RBI-approved agency

- Maintain the CRAR as mandated by RBI

- Net NPA should not exceed 6%

- Presence can be in one or two states

- Sharing of Risk and Rewards:

- Each RE (Regulated Entity) shall retain a minimum of 10 per cent share (Updated 28.08.25 from 20%). The bank holds the remaining share.

- Originating RE to provide default loss guarantee up to 5% of loans outstanding.

- The NBFC/HFC must retain its share of the loan exposure on its books until the loan matures.

- Reporting: Co-lending banks will take their share of individual loans on a back-to-back basis in their books. Respective shares of REs should be reflected in books max within 15 calendar days.

- Funding Source: The NBFC/HFC should assure the bank that its share of the loan is not financed by borrowing from the co-originating bank or any other group company of the partner bank.

- Interest Rate:

- NBFC/HFC can decide on the interest rate for their portion of the exposure.

- The bank sets the interest rate for its portion according to its risk profile and existing RBI regulations.

- The interest rate charged to the borrower shall be a blended interest rate.

- Flow of Funds: All transactions pass through an escrow account with the bank to ensure transparency.

- Master Agreement: The bank and NBFC/HFC must create a Master Agreement detailing terms and conditions under which loans will be originated under the Co-Lending Model (CLM).

Legal Entity Identifier (LEI)

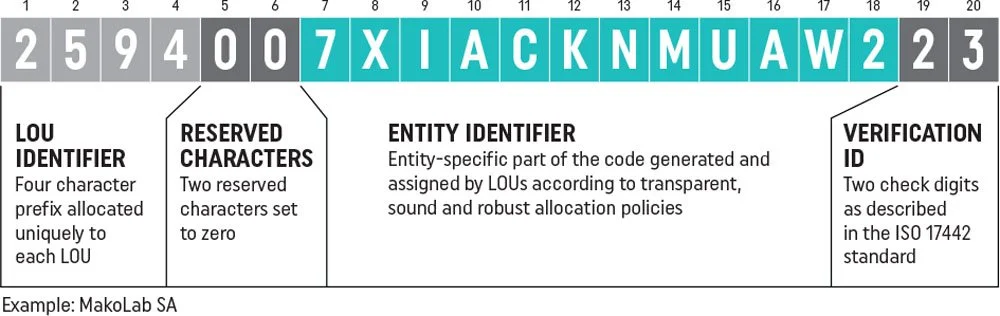

- LEl, a 20-character alphanumeric code, is a global reference number that uniquely identifies every legal entity involved in financial transactions.

- Break-up of 20 characters:

- Characters 1-4: Prefix used to ensure uniqueness among codes from LEI issuers

- Characters 5-18: Entity-specific part of the code generated and assigned

- Characters 19-20: Two check digits as described in the ISO 17442 standard.

- Objective of LEI - Better financial reporting

- Validity period: One year. Requires renewal for continuity.

- Issuing Authority:

- At global level, Global Legal Entity Identifier Foundation (GLEIF) is the regulatory authority.

- In India, Legal Entity Identifier India Ltd. (LEIL), a wholly owned by the Clearing Corporation of India Ltd, is accredited by GLEIF as a Local Operating Unit (LOU) and manages framework of LEI.

- LEIL is recognized by RBI under the Payment and Settlement Systems Act, 2007.

- Primary Objective: The main goal of implementing LEI is to ensure better financial reporting and transparency across the global financial system. It helps regulators identify "who is who" and "who owns whom" in complex transactions.

Applicability

1. Credit Exposure

- Non-individual borrowers with an aggregate exposure of ₹5 crore and above were mandated to obtain an LEI.

- Definition of Exposure: For this purpose, exposure includes all fund-based (loans) and non-fund-based (guarantees, letters of credit) credit and investment exposure from banks and financial institutions.

2. RTGS and NEFT Transactions

- Threshold: Mandatory for all single payment transactions of ₹50 crore and above undertaken by non-individuals.

- Requirement: The bank must obtain and record the LEI for both the remitter (sender) and the beneficiary (receiver).

- Bank Responsibility: Banks are required to maintain a detailed record of these transactions. This rule has been in effect since January 5, 2021.

3. Current & Capital Account Transactions (Remittances)

- Threshold: Mandatory for remittances of ₹50 crore and above.

- Effective Date: This rule became effective on October 1, 2022.

- Authorized Dealer (AD) Banks: Banks authorized to handle foreign exchange (AD-Banks) must ensure the borrower has a valid LEI before processing such high-value international remittances.

4. OTC Derivatives

- All participants in Over-the-Counter (OTC) markets for Rupee Interest Rate derivatives, foreign currency derivatives and credit derivatives in India.

Phased Implementation Timeline (RBI 21.04.22)

The RBI provided a clear roadmap for smaller borrowers to comply with the LEI requirement in stages. This timeline is critical for exams:

| Aggregate Exposure Amount | Deadline to obtain LEI |

|---|---|

| Above ₹25 crore | April 30, 2023 |

| Above ₹10 crore up to ₹25 crore | April 30, 2024 |

| Above ₹5 crore up to ₹10 crore | April 30, 2025 |

Important Consequences of Non-Compliance

The impact of missing these deadlines:

- No New Loans: Borrowers who fail to obtain an LEI code by their respective deadline will not be sanctioned any new credit exposure.

- No Renewals: Banks are prohibited from granting renewals or enhancements of existing credit facilities to non-compliant borrowers.

Loan System of Credit Delivery

This system was introduced to shift large borrowers away from unpredictable "Cash Credit" (overdrafts) toward more disciplined "Working Capital Loans".

- Objective: To enhance credit discipline among large borrowers. By fixing a portion of the credit, banks can better manage their own liquidity and ensure borrowers use funds more efficiently.

- Eligible Accounts: This applies to borrowers with Fund-based Working Capital limits of ₹150 crore and above from the banking system.

- Note: The threshold was significantly increased to ₹150 crore effective April 1, 2019; it was previously only ₹10 crore.

- The limit is calculated based on MPBF (Maximum Permissible Bank Finance) or similar assessment methods.

- Two Components: The total working capital limit is split into:

- Fixed Component: Working Capital Loan (WCL).

- Fluctuating Component: Cash Credit (CC).

- Working Capital Loan (WCL) Percentage:

- Since July 1, 2019, the mandatory WCL component must be at least 60% of the total sanctioned limit.

- Bifurcation Rules:

- The 60% calculation is done after excluding export credit limits (pre and post-shipment) and bills limits for inland sales.

- If a bank invests in Commercial Paper (CP) issued by the borrower, this investment is considered part of the WCDL (Working Capital Demand Loan) portion.

- Cash Credit (CC) Component: Any amount drawn beyond the WCL portion is treated as the Cash Credit component.

- Maturity and Repayment:

- Minimum Maturity: The WCL must have a minimum tenor of 7 days.

- Repayment Style: WCL can be repaid in installments or as a 'bullet' payment (one lump sum at the end).

- Capital Adequacy (CAR) Requirement:

- The undrawn portion of the Cash Credit component attracts a Credit Conversion Factor (CCF) of 20% for calculating Capital Adequacy Ratio (CAR). This forces banks to hold capital even against money the borrower hasn't used yet.

- Compliance Responsibility:

- Consortium Lending: All lenders must jointly ensure the 60% WCL requirement is met at the aggregate level.

- Multiple Banking: Each bank must ensure compliance at their individual bank level.

Selective Credit

Selective Credit Controls (SCC) are qualitative tools used by the RBI to prevent bank funds from being used for hoarding or price speculation of essential goods.

- Legal Provisions: These directions are issued under Section 21 and Section 35A of the Banking Regulation (BR) Act, 1949.

- Meaning & Restrictions: The RBI places specific restrictions on lending against sensitive commodities like wheat, rice, cotton, pulses, oils, and sugar.

- Restrictions can include fixing a maximum loan amount, a specific rate of interest, or a higher margin (the percentage of value the borrower must pay themselves).

- Purpose: To prevent speculative holding (hoarding) of goods using bank finance, which would otherwise drive up market prices for consumers.

- Current Status: Today, most commodities have been deregulated, and banks generally have the discretion to lend against them. However, two specific exceptions remain strictly controlled (means these still have restrictions):

- Buffer stock of sugar held with sugar mills.

- Unreleased stock of sugar with sugar mills (this includes both levy sugar and free sale sugar).

For Selective Credit Controls (SCC), remember that "Buffer stock" usually has a Nil margin (meaning banks can fund 100% of it) because it's maintained for the government, while RBI has prescribed margin of 10% on unreleased stock of sugar with sugar mills representing levy sugar.

Capital Market Exposure

This policy defines how much of a bank's own money (Net Worth) can be tied up in the stock and bond markets.

Forms of Exposure

A bank's total exposure to the capital market is divided into two categories:

- (1) Direct Exposure (Investment): When the bank uses its own funds to buy shares, bonds, or debentures in the market. include investment in equity shares, convertible bonds, convertible debentures and units of equity-oriented mutual funds;

- (2) Indirect Exposure (Loans): When the bank gives loans to others (individuals or companies) and takes shares or debentures as security/collateral.

- advances against shares / bonds / debentures or other securities;

- advances for any other purposes where above instruments are taken as primary security;

- others

- (3) Aggregate Exposure: The sum of (1) + (2) represents the bank's total risk in the capital market.

Ceilings on Exposure (The Limits)

Statutory limit on shareholding in companies

- In terms of Section 19(2) of Banking Regulation Act, 1949, banks cannot hold shares in any company, whether as pledgee, mortgagee or absolute owner, of an amount exceeding:

- 30% of paid-up share capital of the company or

- 30% of its own paid-up share capital and reserves, whichever is lower.

- For example, if a bank has a Net Worth of ₹1000 crore, and company A has a paid-up share capital of ₹100 crore, the bank can hold shares in company A of ₹30 crore (30% of ₹100 crore).

Regulatory Limits

- The aggregate exposure to capital markets in all forms (both fund based, and non-fund based) shall not exceed 40% of its net worth, as on March 31 of previous year.

- Within this overall ceiling, direct investment in shares, convertible bonds / debentures, units of equity-oriented mutual funds and all exposures to Alternate Investment Funds (AlFs) shall not exceed 20% of its net worth.

- A bank exposure to Indian Joint Ventures, Wholly-owned Subsidiaries abroad and step-down subsidiaries is subject to a limit of 20% of the bank's unimpaired capital funds (Tier and Tier II capital).

- The 20% ceiling applies to the aggregate exposure (total amount invested or lent) to the following entities:

- Indian Joint Ventures (JV): A foreign entity where the Indian bank has a stake along with other partners (Indian or foreign).

- Wholly-Owned Subsidiaries (WOS): A foreign entity where the Indian bank owns 100% of the share capital.

- Step-Down Subsidiaries: These are subsidiaries of the JV or WOS (essentially "grandchild" companies of the Indian bank).

- The limit is calculated as a percentage of the bank’s Unimpaired Capital, which is the total "hard cash" and reserves available to absorb losses after deducting any existing losses or bad debts.

- By capping the exposure at 20% of the total capital funds, the Reserve Bank of India (RBI) ensures:

- Risk Diversification: The bank does not put too many "eggs in one basket" abroad.

- Solvency Protection: Even if an overseas subsidiary fails completely, the parent bank still has 80% of its capital intact to cover domestic obligations.

- The 20% ceiling applies to the aggregate exposure (total amount invested or lent) to the following entities:

- The limits are calculated based on the bank's Net Worth (NW) as of March 31st of the previous year.

Prudential Limits on Intra-Group Transactions and Exposure

The following table summarizes the limits a bank must adhere to regarding its exposure to entities within its own corporate group.

1. Single Group Entity Exposure

- This section defines how much a bank can lend to or invest in just one specific company within its group.

- Non-financial/Unregulated (5%): Companies like IT services, back-office support, etc. Because these entities are not under financial regulation, the limit is stricter (5%) to prevent excessive risk.

- Regulated Financial Services (10%): If the group entity is already a regulated financial company (like an insurance arm), the bank is allowed a higher exposure of 10%.

2. Aggregate Group Exposure

- This represents the "total cap" for the bank's entire corporate family, ensuring they don't circumvent the 5% or 10% rules by creating many small companies.

- Unregulated Sub-total (10%): The bank cannot have more than 10% exposure to all its non-financial and unregulated companies combined.

- Total Group Cap (20%): No matter how large or diverse the corporate group is, the bank's total exposure to all group entities (financial and non-financial combined) cannot exceed 20% of its paid-up capital and reserves.

| Exposure Type | To Entity Type | Limit (% of Paid-up Capital & Reserves) |

|---|---|---|

| Single Group Entity | Non-financial and unregulated financial services companies | 5% |

| Single Group Entity | Regulated financial services companies | 10% |

| Aggregate Group | All non-financial and unregulated financial services companies taken together | 10% |

| Aggregate Group | The entire group (all financial and non-financial entities) taken together | 20% |

Investment in Unlisted non-SLR Securities

- Limit: Max 10% of total investments in non-SLR securities.

- Context: Non-SLR (Statutory Liquidity Ratio) securities are commercial bonds or shares (not government bonds). "Unlisted" means they aren't traded on a stock exchange and are harder to sell (illiquid). To prevent banks from holding too many "un-sellable" assets, the RBI caps them at 10%.

Loan against Shares

This section outlines the specific "Do's and Don'ts" when a bank lends money against stock market securities.

Prohibited Loans

- Partly Paid Shares: Banks cannot grant loans against shares that are not fully paid up. (If a share is worth ₹100 but only ₹50 is paid, the bank cannot accept it).

- Partnerships/Proprietorships: Banks cannot grant loans to a partnership firm or a sole proprietorship if the only security offered is shares.

- Own Shares to Own Employees: Banks cannot lend money to their own employees to help them buy the bank's own shares. This prevents the bank from artificially inflating its own stock price.

Loans under ESOP (Employee Stock Option Plans)

- Definition: Loans given to employees of other companies to help them buy their company's shares.

- Limit: Banks can lend up to 90% of the purchase price.

- Max Amount: The maximum loan per employee for ESOP is ₹20 lakh.

Transfer of Shares and Voting Rights

- Threshold: If the loan amount against shares exceeds ₹10 lakh, a special rule applies.

- Requirement: The shares must be transferred into the bank's name.

- Purpose: By holding the shares in its own name, the bank gets exclusive voting rights in the company whose shares it holds as collateral. This gives the bank power to protect its interests if the company is mismanaged.

Summary Table

| Item | Limit / Rule |

|---|---|

| Direct Capital Market Exposure | 20% of NW (Prev. Year) |

| Aggregate Capital Market Exposure | 40% of NW (Prev. Year) |

| Unlisted non-SLR Securities | 10% of total non-SLR investments |

| ESOP Loan Max Amount | ₹20 Lakh |

| ESOP Loan Margin | 10% (can fund up to 90%) |

| Mandatory Share Transfer | Loans > ₹10 Lakh |

Misc. Policy Issues

- Loan for Cost Over-runs: If a project's cost increases beyond the original estimate, banks can provide additional funding for these "over-runs," but it is capped at 10% of the project cost.

- Takeover Takeout Financing: This is a method where a new set of lenders takes over a loan from the original lenders after a certain period. This is allowed only if the total exposure is at least Rs. 1000 crore and the new lenders take over at least 30% of the outstanding amount.

- Without Recourse Letters of Credit (LC): A "without recourse" LC means the bank cannot go back to the beneficiary and ask for money back if things go wrong. Regulations state that:

- Banks cannot issue them.

- Banks can negotiate bills under them.

- Banks cannot purchase or discount bills on a without-recourse basis unless they are under an LC.

- Bank Guarantees for Other Banks/FIs: A bank can provide a guarantee for loans sanctioned by other institutions, provided the guaranteeing bank has its own skin in the game: a minimum 10% exposure in that project (reduced to 5% for infrastructure projects).

Unsecured Exposure

- Definition: An exposure is considered "unsecured" if the value of the security (collateral) at the time the loan is sanctioned is 10% or less of the total loan amount.

- Bank Discretion: The Reserve Bank usually allows individual banks the freedom to set their own internal limits (ceilings) on how much unsecured lending they are willing to take on.

Summary Questopms

-

In consortium or multiple banking loans certification regarding compliance of rules / regulations by companies is obtained from

CA, CS, CWA

-

Objective of loan delivery system is

To maintain credit discipline

-

In loan system of credit delivery, WCDL and CC component ratio is

60:40

-

Loan system of credit delivery is applicable where the amount of is

≥ ₹150 crores

-

Selective credit control is still applicable on

Buffer stock of sugar

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Large Exposure Framework (LEF) | RBI framework effective 01.04.2019; issued under Sections 21 and 35A of Banking Regulation Act, 1949 |

| Large Exposure definition | Total exposure to single/group counterparty ≥ 10% of Eligible Capital Base (ECB) |

| Eligible Capital Base (ECB) | Effective amount of Tier 1 capital as per last audited balance sheet |

| Scope | Applies at both consolidated group level and solo level |

| Group identification — control | One entity owns > 50% voting rights of another |

| Group identification — economic interdependence | 50%+ of gross receipts/expenditure from transactions with counterparty; full/partial guarantee; 20%+ ownership in voting power |

| Cut-off for identification | Required when exposure to single party > 5% of capital base |

| Single Borrower Limit | 20% of Tier-1 Capital (Board may allow additional 5% in exceptional cases) |

| Group Borrower Limit | 25% of Tier-1 Capital |

| Exposure to NBFCs (non-gold loan) | 20% of Tier-1 Capital |

| Exposure to Gold Loan NBFCs | 7.5% of Tier-1 (may go up to 12.5% if additional exposure on-lent to infrastructure) |

| Gold Loan NBFC definition | NBFCs where gold loans comprise 50%+ of financial assets |

| Connected NBFCs | 25% of Tier-1 Capital |

| G-SIB to G-SIB | Strictest limit: 15% of Tier-1 (applied within 12 months of becoming G-SIB) |

| Non G-SIB to G-SIB | 20% of Tier-1 |

| Indian branch of foreign G-SIB | To HO/other G-SIBs: 20%; to non G-SIB: 25% |

| Indian branch of foreign non-G-SIB | To HO/other non-G-SIBs: 25%; to G-SIB: 20% |

| Additional 5% exposure | Requires specific Board approval |

| On-Balance Sheet Netting | Offset deposits against loans if legally enforceable agreement exists; reports net exposure |

| Reporting threshold | All large exposures (≥ 10% ECB) reported to RBI; Top 20 largest exposures always reported |

| Reporting — gross calculation | Must NOT subtract Credit Risk Mitigation (CRM); report full gross exposure |

| Exempted exposures | GOI/State Govt (0% RW), RBI, fully govt-guaranteed loans, intra-day interbank, food credit, NABARD deposits (PSL shortfall), QCCPs clearing |

| Consortium lending | Mandatory when loan exceeds single bank's exposure ceiling; banks share pari-passu charge in ratio of loans |

| Consortium certification | Mandatory compliance certificate from CA, CS, or CWA |

| Multiple banking | Banks extend credit independently; no common agreement; riskier than consortium |

| Credit syndication | Lead Arranger (Mandated Bank) arranges funds from others; earns commission/arrangement fee |

| LEI | 20-character alphanumeric code uniquely identifying legal entities; validity 1 year; issued in India by LEIL (subsidiary of CCIL), accredited by GLEIF |

| LEI — credit exposure | Mandatory for non-individual borrowers with aggregate exposure ₹5 Cr+ |

| LEI — RTGS/NEFT | Mandatory for single payments ₹50 Cr+ by non-individuals (since 05.01.2021) |

| LEI — remittances | Mandatory for ₹50 Cr+ (since 01.10.2022) |

| LEI phased timeline | Above ₹25 Cr: 30.04.2023; ₹10-25 Cr: 30.04.2024; ₹5-10 Cr: 30.04.2025 |

| LEI non-compliance | No new loans, no renewals/enhancements for non-compliant borrowers |

| Loan System of Credit Delivery | For borrowers with WC limits ₹150 Cr+; WCL (fixed) must be ≥ 60%, CC (fluctuating) = balance |

| WCL minimum maturity | 7 days; repayable in instalments or bullet payment |

| CC undrawn portion | Attracts 20% Credit Conversion Factor for CAR calculation |

| Selective Credit Controls (SCC) | RBI tool to prevent hoarding/speculation of essential commodities; issued under Sec 21 & 35A of BR Act |

| SCC current applicability | Only buffer stock of sugar (nil margin) and unreleased stock of sugar (10% margin) with sugar mills |

| Capital market — direct exposure | Max 20% of Net Worth |

| Capital market — aggregate exposure | Max 40% of Net Worth |

| Statutory shareholding limit (Sec 19(2)) | 30% of company's paid-up capital OR 30% of bank's paid-up capital + reserves (whichever lower) |

| Intra-group single entity | Non-financial: 5%; regulated financial: 10% of paid-up capital & reserves |

| Intra-group aggregate | Unregulated total: 10%; entire group total: 20% of paid-up capital & reserves |

| Unlisted non-SLR securities | Max 10% of total non-SLR investments |

| ESOP loans | Up to 90% of purchase price; max ₹20 Lakh per employee |

| Share transfer to bank's name | Mandatory when loan against shares > ₹10 Lakh (bank gets voting rights) |

| Loan for cost over-runs | Capped at 10% of project cost |

| Takeover/takeout financing | Total exposure ≥ ₹1000 Cr; new lenders take over ≥ 30% of outstanding |

| Bank guarantees for other banks | Guaranteeing bank must have minimum 10% exposure in project (5% for infrastructure) |

| Unsecured exposure | Security value ≤ 10% of loan amount at sanction = considered unsecured; banks set own internal limits |

| Infrastructure — exposure limit | Banks may exceed single/group limit by 10% for approved infra projects |

Lesson Doubts

Ask questions, get expert answers