🏆 Directions on Gold Loan

RBI guidelines and regulations governing gold loans, LTV ratios, and compliance requirements.

RBI Lending Against Gold and Silver Collateral Directions 2025

These directions were issued on June 06, 2025, and all lenders must fully implement them by April 1, 2026.

I. Loan Eligibility and Restrictions

1) Detailed Credit Assessment

- Threshold: For any loan amount exceeding ₹2.5 lakh, a detailed credit assessment is now mandatory.

- Requirement: The lender must formally assess the borrower's repayment capacity (income vs. obligations) rather than just relying on the value of the gold/silver pledged.

2) Collateral:

- Accepts Collateral: Against pledge of gold jewellery /ornaments.

- Prohibited Collateral:

- Lenders are not allowed to grant loans against "paper gold" or financial instruments backed by gold/silver.

- Specifically, loans cannot be given against primary gold/silver units of Exchange-traded funds (ETFs) or units of Mutual Funds.

- Against gold bars, gold bullion, unit of Gold.

3) Maximum Tenor

- For "consumption bullet repayment loans" (loans where the entire principal and interest are paid at the end of the term), the maximum duration is 12 months.

4) Maximum Total Weight Limits

There are strict limits on the weight of ornaments and coins a single borrower can pledge for all loans combined:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

RBI Lending Against Gold and Silver Collateral Directions 2025

These directions were issued on June 06, 2025, and all lenders must fully implement them by April 1, 2026.

I. Loan Eligibility and Restrictions

1) Detailed Credit Assessment

- Threshold: For any loan amount exceeding ₹2.5 lakh, a detailed credit assessment is now mandatory.

- Requirement: The lender must formally assess the borrower's repayment capacity (income vs. obligations) rather than just relying on the value of the gold/silver pledged.

2) Collateral:

- Accepts Collateral: Against pledge of gold jewellery /ornaments.

- Prohibited Collateral:

- Lenders are not allowed to grant loans against "paper gold" or financial instruments backed by gold/silver.

- Specifically, loans cannot be given against primary gold/silver units of Exchange-traded funds (ETFs) or units of Mutual Funds.

- Against gold bars, gold bullion, unit of Gold.

3) Maximum Tenor

- For "consumption bullet repayment loans" (loans where the entire principal and interest are paid at the end of the term), the maximum duration is 12 months.

4) Maximum Total Weight Limits

There are strict limits on the weight of ornaments and coins a single borrower can pledge for all loans combined:

| Category | Gold | Silver |

|---|---|---|

| Ornaments | Maximum 1 Kg | Maximum 10 Kg |

| Coins | Maximum 50 grams | Maximum 500 grams |

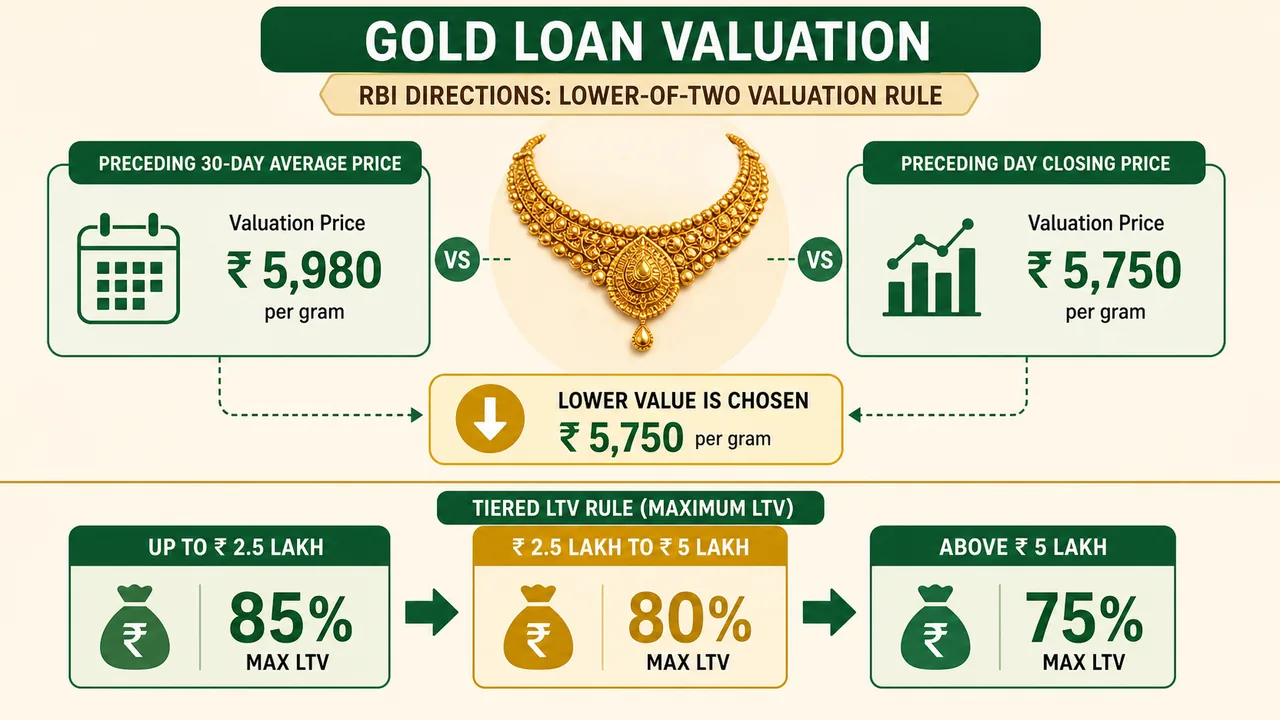

Valuation and Loan-to-Value (LTV)

5) Valuation of Collateral

To determine the value of the gold/silver, lenders must use the lower of the following two rates: a) The average closing price of the specific purity over the preceding 30 days. b) The closing price of that specific purity on the preceding day.

- Source: Rates must be taken from the India Bullion and Jewellers Association Ltd. (IBJA) or a commodity exchange regulated by SEBI.

6) Maximum Loan to Value Ratio (LTV)

The LTV ratio determines how much money you can borrow against the value of your gold. The new rules introduce a tiered structure based on the loan amount:

| Loan Amount Category | Maximum LTV Ratio |

|---|---|

| Less than or equal to ₹2.5 lakh | 85% |

| More than ₹2.5 lakh to ₹5 lakh | 80% |

| More than ₹5 lakh | 75% |

(Example: If your gold is valued at ₹10 lakh, you can only get a loan of ₹7.5 lakh, which is 75%).

Repayment, Release, and Delays

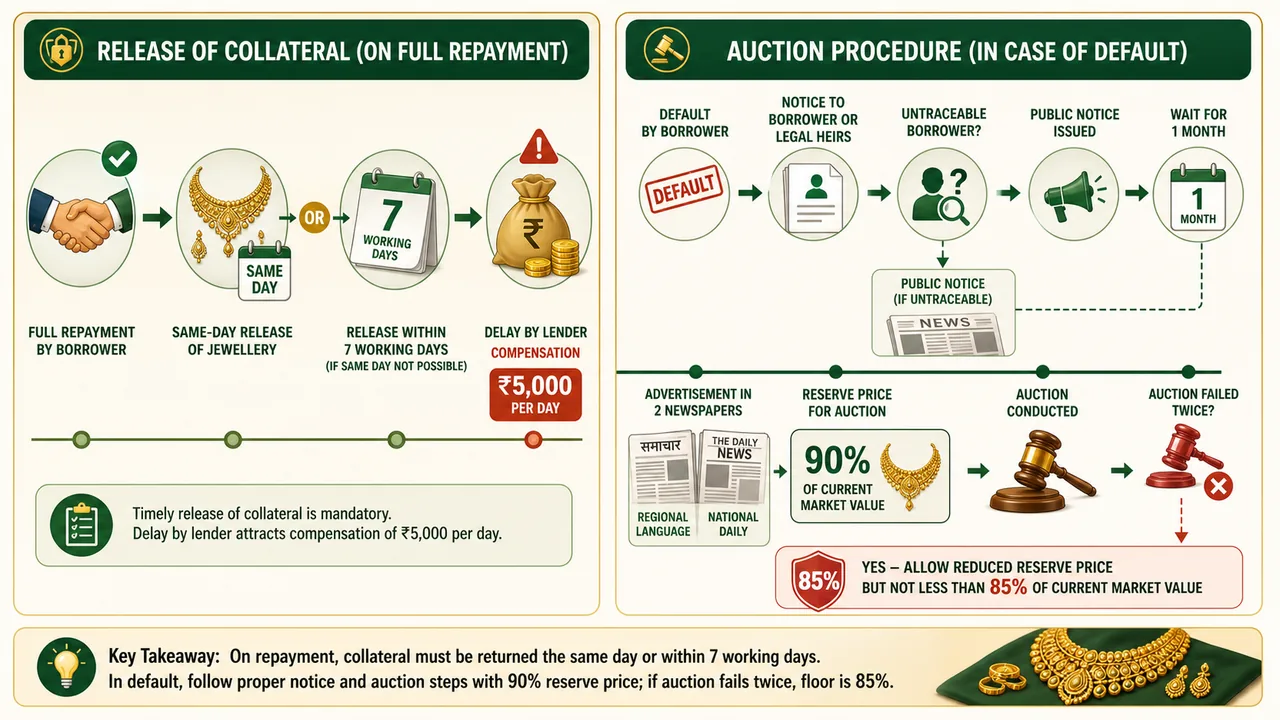

7) Release of Collateral

- Once the loan is fully repaid, the lender must release the jewelry/collateral on the same day.

- If same-day release is not possible, it must be done within a maximum of seven working days.

11) Compensation for Delay

- If the lender fails to release the collateral within the timeline mentioned above (and the delay is the lender's fault), they must pay the borrower compensation.

- Penalty Amount: ₹5,000 for each day of delay.

12) Unclaimed Collateral

- If collateral remains with the lender for more than two years from the date of full repayment or settlement, it is legally treated as "Unclaimed".

- Reporting: A report on such unclaimed collateral must be submitted to the Customer Service Committee or the Board for review at half-yearly intervals.

Auction Procedures (In case of Default)

8) Transparency in Auction

- Lenders must give adequate notice to the borrower (or legal heirs) before auctioning the gold.

- Untraceable Borrowers: If the borrower or legal heirs cannot be found, the bank must issue a public notice. The auction can only proceed one month after the date of this public notice.

9) Auction Announcement

- The auction must be advertised in at least two newspapers:

- One in the regional language (local to the area).

- One in a national daily newspaper.

10) Reserve Price for Auction

- The minimum starting bid (reserve price) for the gold/silver must not be less than 90% of its current market value.

- Failed Auctions: If the auction fails twice (no buyers at that price), the reserve price can be lowered, but it must not be less than 85% of the current value.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| RBI Gold Loan Directions 2025 | Issued June 06, 2025; full implementation by April 1, 2026 |

| Detailed credit assessment threshold | Mandatory for loan amount exceeding ₹2.5 lakh (assess repayment capacity, not just gold value) |

| Accepted collateral | Pledge of gold jewellery / ornaments only |

| Prohibited collateral | Paper gold, ETF units, mutual fund units backed by gold/silver, gold bars, gold bullion |

| Maximum tenor (bullet repayment) | 12 months for consumption bullet repayment loans |

| Max weight — gold ornaments | 1 Kg per borrower (all loans combined) |

| Max weight — gold coins | 50 grams per borrower |

| Max weight — silver ornaments | 10 Kg per borrower |

| Max weight — silver coins | 500 grams per borrower |

| Valuation method | Lower of: (a) average closing price of past 30 days, or (b) closing price of preceding day |

| Valuation source | IBJA (India Bullion and Jewellers Association) or a SEBI-regulated commodity exchange |

| LTV — up to ₹2.5 lakh | Maximum 85% |

| LTV — > ₹2.5 lakh to ₹5 lakh | Maximum 80% |

| LTV — above ₹5 lakh | Maximum 75% |

| Release of collateral | On full repayment: same day; if not possible, within 7 working days |

| Compensation for delayed release | ₹5,000 per day of delay (if lender's fault) |

| Unclaimed collateral | Treated as "unclaimed" if unreturned for > 2 years from full repayment; report to Customer Service Committee / Board half-yearly |

| Auction — notice to borrower | Adequate notice required; if untraceable, public notice must be issued; auction only 1 month after public notice |

| Auction — newspaper requirement | Advertised in 2 newspapers: one regional language, one national daily |

| Reserve price for auction | Not less than 90% of current market value |

| Failed auction (twice) | Reserve price can be lowered but not less than 85% of current market value |

Lesson Doubts

Ask questions, get expert answers