⚖️ Fair Practices Code on Lender's Liability

RBI's Fair Practices Code (2026) covering loan assessment, disbursement, administration, recall, grievance redressal, and time stipulations for credit requests.

Fair Practices Code on Lender's Liability

Introduction

RBI introduced the Fair Practices Code in 2003 to protect bank loan borrowers.

- The code aims to ensure ethical practices by banks and financial institutions.

- Guidelines were finalized and adopted by banks, with the freedom to enhance them while preserving the spirit.

- The code is a framework to prevent unfair lending practices and hold institutions accountable.

To Whom Applicable

- Guidelines apply to all borrowers, excluding:

- Staff loans

- Loans against specific securities

Applicable Customer Types:

-

Individuals

-

Joint Borrowers

-

Proprietary concerns

-

Partnership firms

-

Private and Public Ltd. Companies

-

Trusts

-

PSUs

-

Covers both fund-based and non-fund-based limits for all mentioned borrower categories.

Practices to be Adopted

- Provide prospective borrowers with general information on interest rates, processing fees, charges, penal rates, and other relevant details.

- Priority sector borrowers receive this information in the application form itself.

- Acknowledge filled application forms and specify the time frame for conveying loan decisions after receiving all required details.

- Discuss rules, terms, conditions, margins, security, interest rates, service charges, etc., with borrowers.

- Address queries arising from due diligence within 10 working days of application receipt.

Loan Assessment

- Ensure clients meet eligibility criteria based on applicable norms for their category.

- In retail banking, consider factors like age, income, employment status, and qualifications.

- Assess applications within a reasonable time frame, announcing the timeframe and discussing additional details with clients when needed.

- Proposals should be put up for sanction and communicated within the stipulated time according to bank guidelines.

- The applications will be assessed objectively. RBI has laid down methods of arriving at the need-based requirements of various sections of the borrowers covered in various communications on different subjects. The said methods/procedures, as may be amended from time to time, shall be followed by the bank.

- While assessing the credit needs of the proponents/borrowers, stipulation of margin, security etc. will be based on the guidelines governing the schemes/facilities as approved by the Board of Directors. The collateral security and the margin will be regarded only as an additional comfort for the lender and will not be the sole criteria for deciding a loan request.

- Wherever the applications are rejected, the same should be conveyed in writing. The specific reason for rejection will be indicated in case of all advances including those up to ₹2 lakhs, depending upon the actual reason, but within the timeframe stipulated so that the applicant may be free to go to another institution to raise the loan.

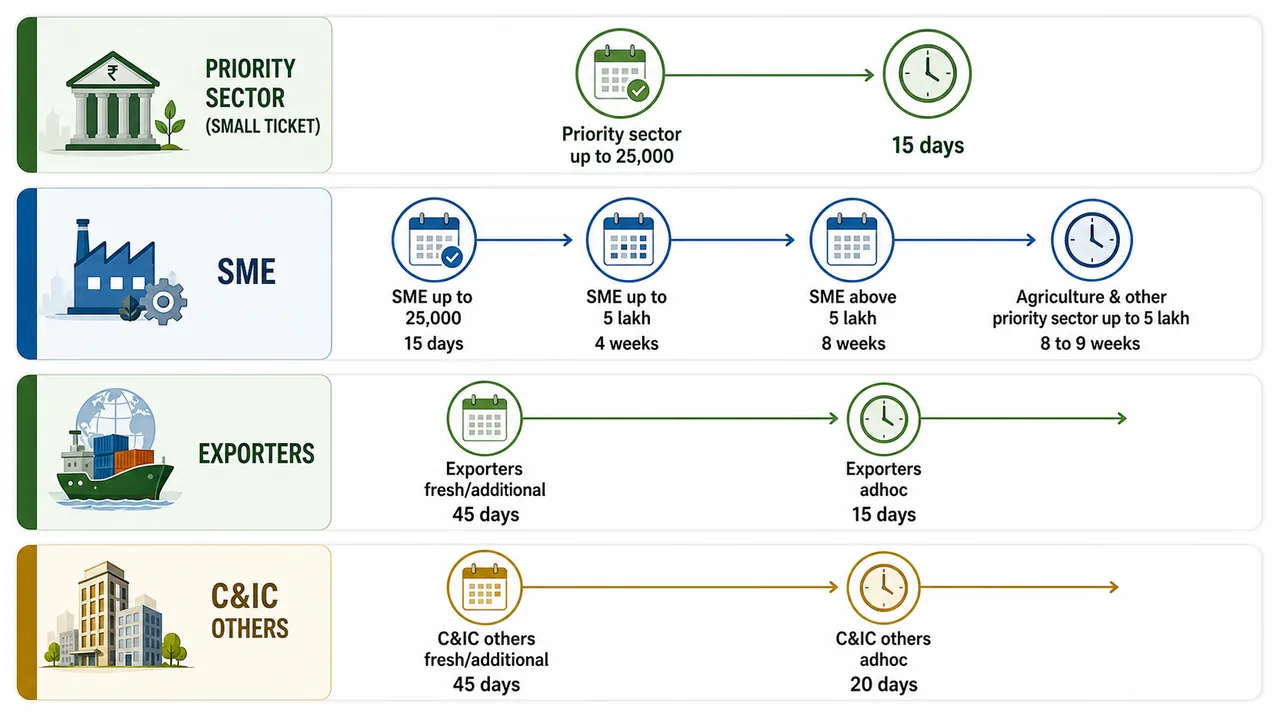

Time Stipulations for Considering Credit Requests

Priority Sector

| Loan Amount | SME Units | Agriculture & Other Priority Sector |

|---|---|---|

| Up to ₹25,000 | 15 days | 15 days |

| Up to ₹5 lakhs | 4 weeks | 8/9 weeks |

| Above ₹5 lakhs | 8 weeks | — |

C & IC Sector

| Request Type | Exporters | Others |

|---|---|---|

| Fresh / Additional | 45 days | 45 days |

| Adhoc | 15 days | 20 days |

Loan Disbursement

- Issue a sanction letter with terms, conditions, and covenants upon loan approval. The sanction letter should be issued by an authorized signatory — Credit Department Head or Branch Manager.

- Clearly outline discretionary guidelines for overdrawing, honoring cheques, cash withdrawals, business growth, non-performing assets, and compliance.

- Disburse loans promptly upon compliance with sanction terms.

- Provide copies of executed documents to borrowers upon request, subject to applicable charges.

- Advise customers on products like FEX derivatives and swaps, emphasizing their responsibility for informed decisions.

- Respond to requests for 'No dues certificate' or transfer of a borrowal account within 21 days of receipt.

Loan Administration

- Keep borrowers informed of account status through periodic statements.

- Notify borrowers in advance (7 working days) of any changes in terms, conditions, interest rates, or service charges, either on the website or through press notification.

- Obtain necessary information from borrowers for monitoring their account conduct during the facility tenure.

- Provide reasonable time for submission of required information and address genuine difficulties or unplanned situations.

- Specify different time limits for information submission in the sanction letter.

- Reserve the right to enforce security for dues recovery in case of default or non-adherence to terms, following normal procedures.

- Refrain from interfering in borrower affairs, except as specified in the terms and conditions, unless new undisclosed information comes to the bank's knowledge.

Recall / Repayment of the Loan

- Communicate any decision to recall the loan or accelerate payment to borrowers in advance, providing a 15-day notice period.

- Initiate further recovery steps only after the expiration of the notice period, unless warranted by a change in circumstances.

- Release all securities upon full repayment of the loan and clearance of dues by the borrower.

- Retain a legitimate right of lien for any other claims the bank may have against the borrower.

- Notify borrowers of outstanding claims, providing full particulars, and retain securities until relevant claims are settled or paid.

Grievance Redressal Mechanism

- Bank has established a procedure for grievance redressal.

- Ensures review and disposal of disputes arising from decisions at the next higher level.

- Board reviews matters through periodic reports.

- Borrowers receive a copy of the charter for grievances, prominently displayed in branch premises.

Conclusion

- Fair Practices Code summarizes existing guidelines with necessary improvements in line with RBI directives.

- Ensures the bank acts in good faith and without negligence in dealings with borrowers.

- Detailed operational guidelines, as amended, will continue to govern specific areas.

- Banks, having adopted the code, should advise borrowers on specific time limits and code of conduct.

- Emphasizes meticulous implementation of the guidelines for ethical and responsible banking.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Introduced | 2003 by RBI |

| Purpose | Prevent unfair lending, ensure ethical practices |

| Applicability | All borrowers (excluding staff loans & loans vs specific securities) |

| Customer Types | Individuals, Joint, Proprietary, Partnership, Pvt/Pub Ltd, Trusts, PSUs |

| Limits Covered | Both fund-based & non-fund-based |

| Due Diligence Queries | Within 10 working days |

| Rejection Communication | In writing (specific reason for advances up to ₹2 lakhs) |

| Collateral | Additional comfort only, not sole criteria |

| Assessment | Objective, as per Board-approved guidelines |

| SME (Up to ₹25K) | 15 days |

| SME (Up to ₹5L) | 4 weeks |

| SME (Above ₹5L) | 8 weeks |

| Agri/Priority (Up to ₹25K) | 15 days |

| Agri/Priority (Above ₹25K) | 8/9 weeks |

| C&IC Fresh/Additional | 45 days (Exporters & Others) |

| C&IC Adhoc (Exporters) | 15 days |

| C&IC Adhoc (Others) | 20 days |

| Sanction Letter Signatory | Credit Dept Head / Branch Manager |

| No Dues Certificate | Within 21 days of request |

| Executed Docs Copy | On request, subject to charges |

| FEX Derivatives | Customer advised to make informed decisions |

| Change Notification | 7 working days advance notice |

| Loan Recall Notice | 15 days advance notice |

| Security Release | On full repayment & clearance of dues |

| Right of Lien | Retained for other claims |

| Grievance Redressal | Procedure established, charter displayed in branches |

| Board Role | Periodic review of grievance reports |

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Fair Practices Code on Lender's Liability

Introduction

RBI introduced the Fair Practices Code in 2003 to protect bank loan borrowers.

- The code aims to ensure ethical practices by banks and financial institutions.

- Guidelines were finalized and adopted by banks, with the freedom to enhance them while preserving the spirit.

- The code is a framework to prevent unfair lending practices and hold institutions accountable.

To Whom Applicable

- Guidelines apply to all borrowers, excluding:

- Staff loans

- Loans against specific securities

Applicable Customer Types:

-

Individuals

-

Joint Borrowers

-

Proprietary concerns

-

Partnership firms

-

Private and Public Ltd. Companies

-

Trusts

-

PSUs

-

Covers both fund-based and non-fund-based limits for all mentioned borrower categories.

Practices to be Adopted

- Provide prospective borrowers with general information on interest rates, processing fees, charges, penal rates, and other relevant details.

- Priority sector borrowers receive this information in the application form itself.

- Acknowledge filled application forms and specify the time frame for conveying loan decisions after receiving all required details.

- Discuss rules, terms, conditions, margins, security, interest rates, service charges, etc., with borrowers.

- Address queries arising from due diligence within 10 working days of application receipt.

Loan Assessment

- Ensure clients meet eligibility criteria based on applicable norms for their category.

- In retail banking, consider factors like age, income, employment status, and qualifications.

- Assess applications within a reasonable time frame, announcing the timeframe and discussing additional details with clients when needed.

- Proposals should be put up for sanction and communicated within the stipulated time according to bank guidelines.

- The applications will be assessed objectively. RBI has laid down methods of arriving at the need-based requirements of various sections of the borrowers covered in various communications on different subjects. The said methods/procedures, as may be amended from time to time, shall be followed by the bank.

- While assessing the credit needs of the proponents/borrowers, stipulation of margin, security etc. will be based on the guidelines governing the schemes/facilities as approved by the Board of Directors. The collateral security and the margin will be regarded only as an additional comfort for the lender and will not be the sole criteria for deciding a loan request.

- Wherever the applications are rejected, the same should be conveyed in writing. The specific reason for rejection will be indicated in case of all advances including those up to ₹2 lakhs, depending upon the actual reason, but within the timeframe stipulated so that the applicant may be free to go to another institution to raise the loan.

Time Stipulations for Considering Credit Requests

Priority Sector

| Loan Amount | SME Units | Agriculture & Other Priority Sector |

|---|---|---|

| Up to ₹25,000 | 15 days | 15 days |

| Up to ₹5 lakhs | 4 weeks | 8/9 weeks |

| Above ₹5 lakhs | 8 weeks | — |

C & IC Sector

| Request Type | Exporters | Others |

|---|---|---|

| Fresh / Additional | 45 days | 45 days |

| Adhoc | 15 days | 20 days |

Loan Disbursement

- Issue a sanction letter with terms, conditions, and covenants upon loan approval. The sanction letter should be issued by an authorized signatory — Credit Department Head or Branch Manager.

- Clearly outline discretionary guidelines for overdrawing, honoring cheques, cash withdrawals, business growth, non-performing assets, and compliance.

- Disburse loans promptly upon compliance with sanction terms.

- Provide copies of executed documents to borrowers upon request, subject to applicable charges.

- Advise customers on products like FEX derivatives and swaps, emphasizing their responsibility for informed decisions.

- Respond to requests for 'No dues certificate' or transfer of a borrowal account within 21 days of receipt.

Loan Administration

- Keep borrowers informed of account status through periodic statements.

- Notify borrowers in advance (7 working days) of any changes in terms, conditions, interest rates, or service charges, either on the website or through press notification.

- Obtain necessary information from borrowers for monitoring their account conduct during the facility tenure.

- Provide reasonable time for submission of required information and address genuine difficulties or unplanned situations.

- Specify different time limits for information submission in the sanction letter.

- Reserve the right to enforce security for dues recovery in case of default or non-adherence to terms, following normal procedures.

- Refrain from interfering in borrower affairs, except as specified in the terms and conditions, unless new undisclosed information comes to the bank's knowledge.

Recall / Repayment of the Loan

- Communicate any decision to recall the loan or accelerate payment to borrowers in advance, providing a 15-day notice period.

- Initiate further recovery steps only after the expiration of the notice period, unless warranted by a change in circumstances.

- Release all securities upon full repayment of the loan and clearance of dues by the borrower.

- Retain a legitimate right of lien for any other claims the bank may have against the borrower.

- Notify borrowers of outstanding claims, providing full particulars, and retain securities until relevant claims are settled or paid.

Grievance Redressal Mechanism

- Bank has established a procedure for grievance redressal.

- Ensures review and disposal of disputes arising from decisions at the next higher level.

- Board reviews matters through periodic reports.

- Borrowers receive a copy of the charter for grievances, prominently displayed in branch premises.

Conclusion

- Fair Practices Code summarizes existing guidelines with necessary improvements in line with RBI directives.

- Ensures the bank acts in good faith and without negligence in dealings with borrowers.

- Detailed operational guidelines, as amended, will continue to govern specific areas.

- Banks, having adopted the code, should advise borrowers on specific time limits and code of conduct.

- Emphasizes meticulous implementation of the guidelines for ethical and responsible banking.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Introduced | 2003 by RBI |

| Purpose | Prevent unfair lending, ensure ethical practices |

| Applicability | All borrowers (excluding staff loans & loans vs specific securities) |

| Customer Types | Individuals, Joint, Proprietary, Partnership, Pvt/Pub Ltd, Trusts, PSUs |

| Limits Covered | Both fund-based & non-fund-based |

| Due Diligence Queries | Within 10 working days |

| Rejection Communication | In writing (specific reason for advances up to ₹2 lakhs) |

| Collateral | Additional comfort only, not sole criteria |

| Assessment | Objective, as per Board-approved guidelines |

| SME (Up to ₹25K) | 15 days |

| SME (Up to ₹5L) | 4 weeks |

| SME (Above ₹5L) | 8 weeks |

| Agri/Priority (Up to ₹25K) | 15 days |

| Agri/Priority (Above ₹25K) | 8/9 weeks |

| C&IC Fresh/Additional | 45 days (Exporters & Others) |

| C&IC Adhoc (Exporters) | 15 days |

| C&IC Adhoc (Others) | 20 days |

| Sanction Letter Signatory | Credit Dept Head / Branch Manager |

| No Dues Certificate | Within 21 days of request |

| Executed Docs Copy | On request, subject to charges |

| FEX Derivatives | Customer advised to make informed decisions |

| Change Notification | 7 working days advance notice |

| Loan Recall Notice | 15 days advance notice |

| Security Release | On full repayment & clearance of dues |

| Right of Lien | Retained for other claims |

| Grievance Redressal | Procedure established, charter displayed in branches |

| Board Role | Periodic review of grievance reports |

Lesson Doubts

Ask questions, get expert answers