📜 Non-Fund Based Credit Facilities

Non-fund based (NFB) limits — Letters of Credit (types, parties, process, risks), Bank Guarantees (financial, performance, types, issuance, claims), Buyer's/Supplier's Credit, Bills Purchase/Discounting, and Co-Acceptance facilities.

Non-Fund Based Credit Facilities

Introduction

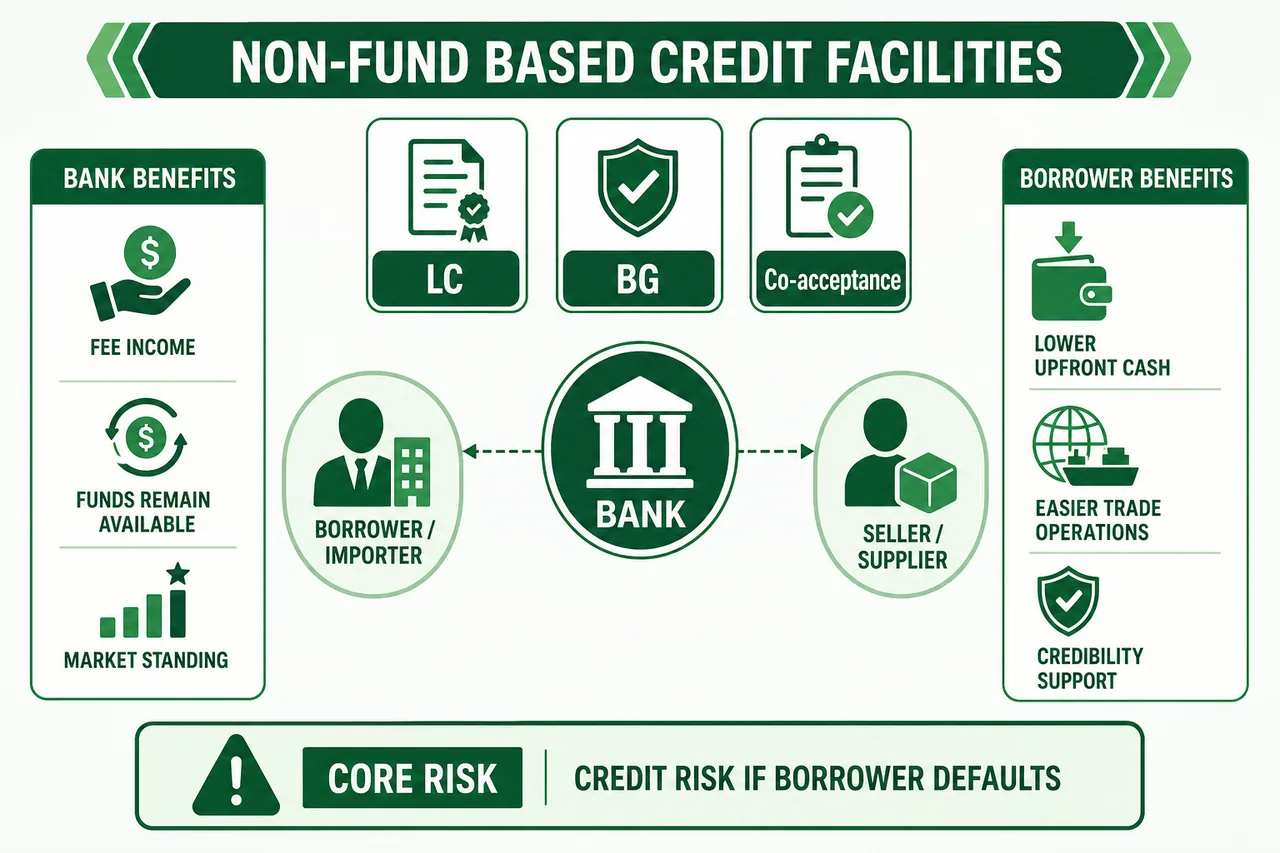

- Banks provide non-fund based (NFB) facilities, which don't involve direct money flow.

- Such facilities are becoming more popular as they boost banks' non-interest income.

- Non-interest income is crucial for bank profits.

- Top-tier clients can often get cheaper funding from markets, bypassing banks.

- The trend of top-paying clients for banks to move to financial disintermediation.

- NFB services are gaining importance due to financial disintermediation.

- Both banks and borrowers benefit from NFB services.

- NFB services are considered a form of indirect credit since no actual money is disbursed.

Non-Fund Based Limits

- Banks offer non-cash facilities like Letters of Credit (LC) and Bank Guarantees to ensure sellers are paid.

- These services confirm the bank will cover payments if the buyer can't, without initial fund transfer.

- Sellers trust bank-backed commitments, reducing the need for advance payments.

- Non-fund based limits replace buyer credit with bank assurance, offering seller confidence.

- Three key non-cash facilities: LCs, Bank Guarantees, Co-acceptances.

Advantages and Risks

| Stakeholder | Details |

|---|---|

| Bank Advantages | Money remains in-house for other uses; Earns non-interest income; Enhances bank's market standing; Simplifies operations |

| Borrower Benefits | Access to credit without major capital; Operational ease; Acts as a financial reliability endorsement by the bank |

| Risks | Banks face credit risks; Requires thorough risk assessment and appraisal |

Letters of Credit (LC)

International Trade Challenges

- Buyers and sellers are geographically distant.

- Different legal systems.

- Uncertainty about each other's financial reliability.

Role of Banks

- Mediate the trade process.

- Handle and route the documents related to goods.

What is a Letter of Credit?

- Issued by a bank at the buyer's request.

- Favors the seller.

- Guarantees the bank will honor documents or drafts from the seller.

- Stipulates specific terms, conditions, and timeframes.

- LC is akin to a bank guarantee ensuring payment on presenting required documents.

- It's not negotiable.

General Consideration

- LC governed by UCPDC 600 (Uniform Customs & Practice for Documentary Credits).

- As of January 1, 2013, banks are required to use SFMS for issuing and managing domestic LCs.

LC Process — Example

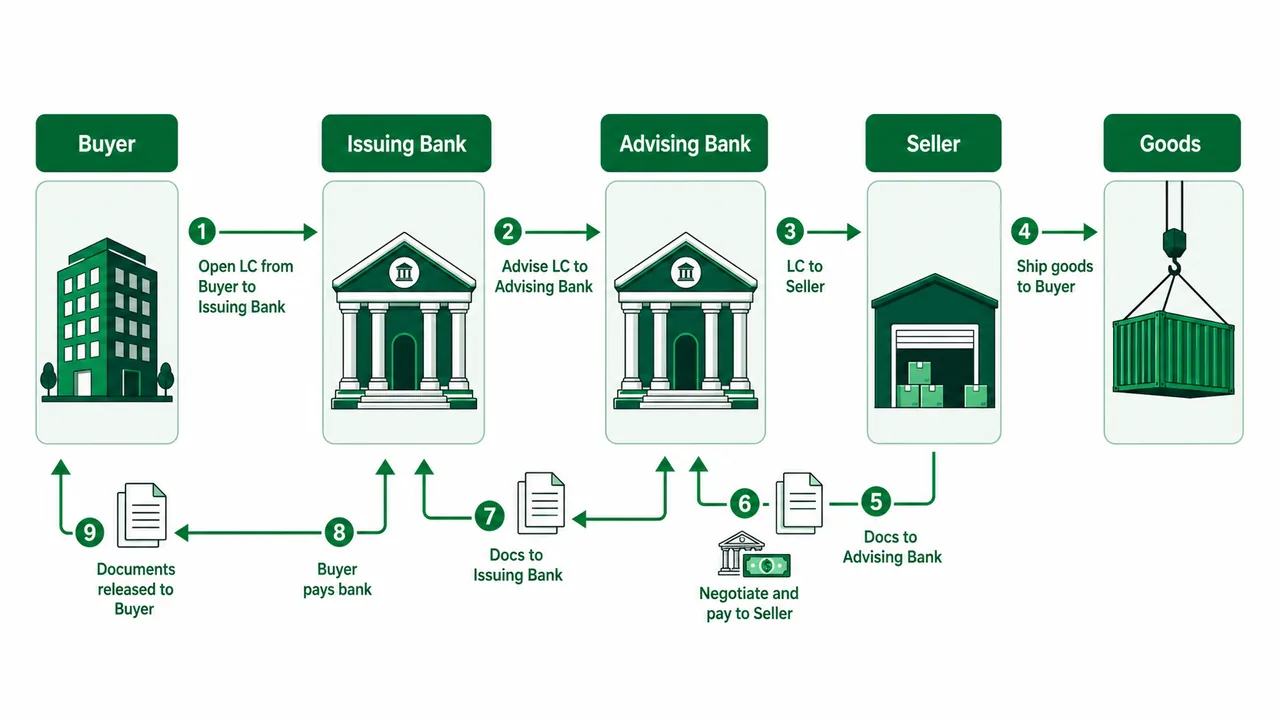

Bharath & Co. (India) — buyer — wants machinery from Edward & Co. — seller (England). They agree on LC payment due to mutual unfamiliarity.

🔐

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

Pro

Popular Save ₹100/mo

₹ 99 /mo

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Non-Fund Based Credit Facilities

Introduction

- Banks provide non-fund based (NFB) facilities, which don't involve direct money flow.

- Such facilities are becoming more popular as they boost banks' non-interest income.

- Non-interest income is crucial for bank profits.

- Top-tier clients can often get cheaper funding from markets, bypassing banks.

- The trend of top-paying clients for banks to move to financial disintermediation.

- NFB services are gaining importance due to financial disintermediation.

- Both banks and borrowers benefit from NFB services.

- NFB services are considered a form of indirect credit since no actual money is disbursed.

Non-Fund Based Limits

- Banks offer non-cash facilities like Letters of Credit (LC) and Bank Guarantees to ensure sellers are paid.

- These services confirm the bank will cover payments if the buyer can't, without initial fund transfer.

- Sellers trust bank-backed commitments, reducing the need for advance payments.

- Non-fund based limits replace buyer credit with bank assurance, offering seller confidence.

- Three key non-cash facilities: LCs, Bank Guarantees, Co-acceptances.

Advantages and Risks

| Stakeholder | Details |

|---|---|

| Bank Advantages | Money remains in-house for other uses; Earns non-interest income; Enhances bank's market standing; Simplifies operations |

| Borrower Benefits | Access to credit without major capital; Operational ease; Acts as a financial reliability endorsement by the bank |

| Risks | Banks face credit risks; Requires thorough risk assessment and appraisal |

Letters of Credit (LC)

International Trade Challenges

- Buyers and sellers are geographically distant.

- Different legal systems.

- Uncertainty about each other's financial reliability.

Role of Banks

- Mediate the trade process.

- Handle and route the documents related to goods.

What is a Letter of Credit?

- Issued by a bank at the buyer's request.

- Favors the seller.

- Guarantees the bank will honor documents or drafts from the seller.

- Stipulates specific terms, conditions, and timeframes.

- LC is akin to a bank guarantee ensuring payment on presenting required documents.

- It's not negotiable.

General Consideration

- LC governed by UCPDC 600 (Uniform Customs & Practice for Documentary Credits).

- As of January 1, 2013, banks are required to use SFMS for issuing and managing domestic LCs.

LC Process — Example

Bharath & Co. (India) — buyer — wants machinery from Edward & Co. — seller (England). They agree on LC payment due to mutual unfamiliarity.

- Opening LC: Bharath & Co. asks Bank of India (Issuing Bank) to open an LC favoring Edward & Co.

- Advising LC: Bank of India informs Barclays Bank (England) (Advising Bank), which then sends the LC to Edward & Co.

- Goods & Documents: Edward & Co. ships machinery, collects necessary documents, and presents a bill to Barclays Bank.

- Bill Negotiation: Barclays Bank confirms documents align with LC, pays Edward & Co., then sends documents to Bank of India.

- Bill Payment: Bank of India sends the bill to Bharath & Co., who then pays.

- Document Release: Upon payment, Bank of India releases shipping documents to Bharath & Co.

Advantages of LC

For Buyer:

- No upfront payment needed.

- Can secure credit due to bank guarantee.

- Can set quality checks and conditions to safeguard interests.

For Seller:

- Guaranteed payment upon meeting LC terms.

- Can get immediate payment post-shipment by negotiating bills with a local bank.

Parties to a Letter of Credit

| Party | Role |

|---|---|

| Applicant (Buyer/Importer/Opener) | Initiates the LC process for goods/services payments |

| Issuing Bank (Opening Bank) | Opens the LC upon the applicant's request |

| Beneficiary (Exporter/Seller) | Receives benefits under LC, such as payments |

| Advising Bank (Notifying Bank) | Alerts the beneficiary about the LC, ensuring its authenticity |

| Negotiating Bank | Located in the exporter's country; handles bills and payments. Can be specified (nominated) or any bank if not mentioned in LC |

| Confirming Bank | Provides additional assurance if the seller doubts the issuing bank's credibility. Guarantees payment based on LC terms |

| Reimbursing Bank | Appointed by the issuing bank to handle reimbursements to other involved banks |

| Accepting Bank | Agrees to pay a drafted bill of exchange when it meets LC conditions |

| Nominated Bank | Authorized to pay under the LC; can be any bank if none is specified |

Types of Letters of Credit

Domestic vs. International LCs

- Domestic LCs involve parties all within one country, aiding domestic trade transactions.

- International LCs involve an international party, facilitating import/export activities.

Immediate vs. Deferred Payment LCs

- Sight LCs require immediate payment to the beneficiary upon document presentation.

- Usance LCs allow payment at a future date, offering a credit period to the buyer.

Revocable vs. Irrevocable LCs

- Revocable LCs can be altered or canceled by the issuer at any moment without notice.

- Irrevocable LCs are fixed and can only be changed with all parties' consent, offering security to the beneficiary.

Enhanced Security LCs

- Confirmed LC: Involves a second bank's guarantee, providing double security but at a higher cost.

Intermediate Trade LCs

- Back-to-Back LC: A secondary LC used for intermediary transactions, where one LC is used as collateral for another. Participants include the original buyer, seller/manufacturer, and a sub-contractor. Utilized when confidentiality is needed or when the intermediary lacks funds.

Flexible LCs for Middlemen

- Transferable LC: Allows the initial beneficiary to pass on the credit, wholly or partly, to additional beneficiaries. Particularly useful for middlemen with limited credit facilities.

Pre-Financing LCs

- Red Clause LC: Contains a clause enabling the beneficiary to receive an advance payment to finance the production or procurement of goods before shipment. The advance is guaranteed by the issuing bank and is typically repaid once the goods are shipped.

Storage-Supportive LCs

- Green Clause LC: Offers financing for pre-shipment needs including storage costs, with warehouse receipts required as collateral.

Continuous Transaction LCs

- Revolving LC: Facilitates ongoing trade by automatically renewing the credit limit after each use, avoiding the need for separate LCs for each transaction.

Loan Security LCs

- Standby LC: Functions similarly to a bank guarantee to ensure loan repayment, activated if the applicant fails to fulfill contractual obligations.

Multi-Purpose LCs

- Omnibus LC: A single LC covering multiple transactions, offering convenience and less paperwork for buyers.

LC Content Requirements

- Include import license details when applicable.

- Provide complete and accurate beneficiary address.

- Give a clear, brief description of the merchandise.

- State the price of goods both verbally and numerically.

- Specify the goods' origin and chosen mode of transportation.

- Mention the final date for shipment and document negotiation.

- Indicate ports of shipment and destination.

- Clarify if partial or trans-shipments are allowed.

- Detail the value and currency of the goods (CIF/CI/FOB).

- Define payment terms, such as D.P. or D.A., including the bill's tenor.

- Set the LC expiry date.

- Ensure LCs for capital goods are opened as per sanction terms.

- Confirm that regular raw material purchase LCs are not diverted for capital expenditure (CAPEX) or other uses.

- Adhere to policy-defined authority levels for sanctioning and issuing LCs.

D.P. vs D.A.

| Term | Meaning |

|---|---|

| D.P. (Documentary Payment) | "Documents against Payment" — buyer receives documents for taking possession of goods only after making payment to the seller or presenting payment confirmation through their bank |

| D.A. (Documentary Acceptance) | "Documents against Acceptance" — buyer receives documents for taking possession of goods upon accepting a time draft or bill of exchange. Payment is typically made at a later agreed-upon date, often upon maturity of the draft |

Credit Implications of LCs for Bankers

- Issuing banks honor clean LCs based on trust, without needing goods' movement documents.

- Drafts under LCs are drawn on banks, not the applicant, making bank's commitment primary.

- Banks' LC obligations are firm, regardless of buyer-seller disputes, except in fraud cases.

- Banks must carefully assess the applicant's financial capability to fulfill LC payments.

- Banks may require security or a deposit when issuing LCs to new clients or those with no prior dealings.

- For immediate payment LCs, banks may:

- Request a significant deposit of the LC amount upfront.

- Collect a percentage (e.g., 25%) as a margin and verify the applicant can pay the remainder.

- Use hypothecated or pledged goods as collateral for credit facilities.

- Indian banks often favor goods as security for LC-related advances, requiring proper valuation to avoid over-financing.

- Banks should validate the beneficiary's credibility for large LC amounts, sometimes requiring status reports for sums above a certain threshold.

Usance Letter of Credit

- Usance LCs, also called Deferred Payment LCs, provide buying power on credit in Indian businesses.

- This credit tool allows purchase of goods via LC, later transitioning to a buyer's credit backed by a letter of comfort.

- Indian banks equate Usance LCs with traditional loans due to their financial impact.

- For credit assessments, Usance LCs are now treated as fund-based facilities.

- The bank's confidence in a borrower's reliability is critical as goods are released without secured advance.

- DA LC credit limits must align with the buyer's working capital needs and credit terms.

- Monitoring is needed to prevent the misuse of low-cost funds for speculative or non-bankable investments.

Risk Associated with Opening Import LCs

- Issuing banks face risk if an importer's financial status deteriorates, affecting the bank's obligation to pay under the LC.

- Risk of the exporter delivering inferior goods, potentially harming the importer and the financing bank.

- Banks assess an importer's creditworthiness, including obtaining supplier reports from agencies or correspondent banks abroad.

- Country risks involve political and economic uncertainties in the exporter's country, managed by the bank's specialized units.

- Import LCs must be backed by valid import licenses and match the importer's identity and license details.

- Imported goods should comply with import licenses, considering the type and quantity of goods, source country, and special conditions.

- All imports financed under an LC must adhere to guidelines of international bodies like the IBRD.

- Payments through LCs must align with foreign exchange regulations under FEMA.

- For forward contracts, banks require a commitment from the applicant to accept prevailing rates and may require additional margins if the market fluctuates.

- Deposits for 100% margin in LCs are only guarantees, with actual bill payments subject to exchange rates at the time of negotiation or as per forward contracts.

- LCs for importing machinery should be opened only for reputable beneficiaries as per project reports or financial institutions' approvals.

- Banks must secure a clear authorization letter from financial institutions before opening an LC, ensuring payment for the documents under the LC.

Buyer's Credit

- Buyer's Credit is a loan from a foreign bank to pay for imports on behalf of an importer.

- Overseas banks fund these loans by crediting the Indian bank's Nostro account for payment to the exporter.

- The arrangement is typically initiated by the supplier, with the loan paying the supplier directly.

- Indian banks, especially those with foreign branches, are major providers of Buyer's Credit to Indian importers.

- Buyer's Credit is linked to a DA-based LC issued by the importer's bank and settled upon credit period expiry with the loan.

- A letter of comfort from the importer's Indian bank is often required by the financing foreign bank.

- Benefits include timely payment for exporters and extended payment time for importers aligned with their cash flows.

- Importers can negotiate better deals by paying exporters on a sight basis and then financing through Buyer's Credit.

- Buyer's Credit can be in various foreign currencies, offering flexibility and potential currency exchange advantages to the importer.

Supplier's Credit

- Supplier's Credit is a financing option for Indian importers through overseas suppliers.

- It involves the discounting of Usance Bills under LCs issued by Indian banks, done by overseas branches or correspondents.

- Payment to supplier is spread over an agreed period and made in the specified currency.

- Suppliers may finance deferred payments independently, impacting their pricing of the transaction.

- The importer is indebted to the supplier until the full payment is made.

Advantages for Importers

- Access to cost-effective funding for importing raw materials and capital goods.

- Relieves short-term financial stress by providing credit for purchases.

- Leverages credit to negotiate better pricing with suppliers.

- Fulfills supplier demands for immediate payment while enjoying deferred payment benefits.

- Benefits from at-sight payment terms without the risks associated with the importer's credit history, secured by the LC arrangement.

Bills Purchase / Discounting Under LC

- Financing against bills of exchange is favored by banks due to their short-term, self-liquidating nature and protection from the Negotiable Instruments Act.

- While CC/OD is a primary loan type, Indian banks predominantly rely on Cash Credit/Overdraft for working capital.

- The bill culture in India still exists, materially, but has not extensively covered central sector transactions.

- The sector's growth necessitates that banks accommodate to financing needs.

- Banks are autonomous in setting working capital limits, provided they adhere to their loan policies.

Key Rules

- Non-constituent borrowers or those outside consortium/multiple banking arrangements should not receive fund-based or non-fund-based facilities from banks.

- Banks can negotiate LCs if the proceeds are directed to the beneficiary's regular bank.

- Negotiation of unrestricted LCs for non-constituents is generally prohibited.

- Scheduled banks may issue BG/LCs against counter-bank guarantees from co-operative bank counter guarantees, ensuring the co-operative bank examines the request's commercial viability.

- Discounting of bills under LCs is permissible if the beneficiary has credit facilities elsewhere, preserving the LC issuing bank's cash flow.

Exposure Rules

- Genuine bills under LCs are considered an exposure of the issuing bank unless negotiated 'under reserve', which then counts as exposure to the borrower.

- When LC issuing and bill discounting banks are the same, exposure is assigned to the borrower.

- Banks should verify the authenticity of transactions when handling bills, avoiding 'without recourse' clauses unless assessing the LC issuing bank's creditworthiness.

- Banks should steer clear of accommodation bills and maintain records of trade transactions tied to bill financing.

- Caution is advised for banks when discounting bills involving finance companies connected to large industrial groups.

Non-Fund Based Facility to Non-Constituent Borrowers

Restriction on Non-Fund Facilities

- Banks were initially restricted from offering non-fund based facilities to non-constituent borrowers to avoid fraud and misuse.

- Non-constituent borrowers refer to individuals or entities that are not part of the main group or structure of borrowers in a particular lending arrangement.

Revision of Guidelines

- The regulation has been reassessed, allowing banks to offer non-fund based facilities like LCs and bank guarantees to customers who do not have fund-based facilities with any bank.

Conditions for Non-Fund Facilities

- Banks must have a Board-approved policy in place for offering such facilities.

- Customers must verify that they have not received fund-based facilities from any Indian bank.

- Banks need to perform thorough credit checks equivalent to those for fund-based facilities.

- Compliance with KYC, AML, CFT standards, and the Prevention of Money Laundering Act (PMLA) 2002 is mandatory.

- Credit details must be reported to Credit Information Companies as per RBI's authorization.

- Banks must adhere to RBI-prescribed exposure limits.

Negotiation of LCs

- Banks can't negotiate unrestricted LCs from non-constituent borrowers.

- Banks may negotiate LCs restricted to specific banks, ensuring funds go to the beneficiary's regular banker.

Bank Guarantees

Definition and Legal Basis

- Contract of Guarantee — defined under Sec. 126, Indian Contract Act, 1872.

- Ensures a third party's promise or liability is fulfilled in case of default.

- Like other guarantees, a bank guarantee involves three parties.

- A bank guarantee is a bank's promise to a third party to cover its customer's financial obligations.

- Activates when the customer doesn't meet contractual or legal duties.

Parties Involved

| Party | Role |

|---|---|

| Applicant / Borrower | Individual or entity that initiates the guarantee |

| Beneficiary | Receiver of the guarantee who can claim in case of default |

| Guarantor / Bank | The bank that promises to cover the applicant's obligations if they default |

- The bank guarantee is a secondary agreement, resulting from the primary contract between the applicant and beneficiary.

- A customer must have a prior commitment to a third party.

- The bank steps in to cover the costs if the customer defaults.

- Banks should secure their position and understand their rights before offering guarantees.

Types of Bank Guarantees

Financial Guarantee

- Replaces customer's need to deposit cash security or earnest money.

- Acts as a direct credit substitute; bank assures payment if the customer defaults.

- Risk equates to the customer's creditworthiness.

- Common for contractors dealing with Government departments.

- If the contractor reneges on the contract, the government can claim money via the guarantee.

Deferred Payment Guarantee

- Banks assure payment to suppliers if the buyer can't pay on time.

- Used for purchases like plant and machinery on a payment-over-time basis.

- While the bank pays only if the borrower defaults, it still counts as a potential liability.

Performance Guarantee

- Assures a third party of the customer's performance of a non-financial contractual obligation.

- Risk isn't solely based on creditworthiness but on the event or transaction specifics.

- If the customer doesn't meet contract conditions, the bank compensates the third party.

- Banks often pay on a default notice without diving into contract specifics.

- Most guarantees don't require proof of default; a claim from the beneficiary often suffices.

Types of Bank-Issued Performance Guarantees

| Type | Purpose |

|---|---|

| Bid Bonds | Ensures the bidder's commitment to a project; if the bid wins, it converts to a performance guarantee |

| Performance Bonds | Secures around 10-15% of the contract's value; compels the contractor to adhere to the agreement |

| Advance Payment Guarantees | Protects advances paid to contractors for initial costs; reduces bank's liability as the project advances |

| Retention Money Guarantees | Replaces cash withheld by the employer to ensure contract fulfillment; bank guarantees the withheld amount |

| Maintenance Bonds | Guarantees the contractor's work post-completion for a period, usually 1-2 years |

| Guarantees on behalf of Travel Agents/Businesses | Secures transactions where travel agents receive tickets from airlines or businessmen ship goods and defer the payment |

Broad Classification of Bank Guarantees

| Performance Guarantee | Financial Guarantee |

|---|---|

| Bid Bond Guarantee in lieu of Earnest Money Deposit | Guarantees for credit facilities |

| Guarantees on behalf of contractors for due completion of work, performance of product | Guarantees in lieu of repayment of financial securities |

| Performance bonds and export performance guarantees | Guarantees in lieu of margin requirements of exchanges |

| Guarantees in lieu of security deposits / Earnest Money Deposits (EMD) for participating in tenders | Guarantees for mobilization advance, advance money before commencement of a project and for money to be received in various stages of project implementation |

| Guarantees for the mobilization of advance | Guarantees towards revenue dues, taxes, duties, levies etc. in favour of Tax/Customs/Port/Excise Authorities and for disputed liabilities for litigation pending at courts |

| Retention money guarantees | Credit enhancements |

| Warranties, indemnities and stand-by letters of credit related to particular transactions | Liquidity facilities for securitization transactions |

| Acceptances (including endorsements with the character of acceptance), Deferred payment guarantees |

Assessment of Guarantee Limit

- Banks primarily provide financial guarantees, cautiously handling performance guarantees.

- Financial guarantees confirm a customer's financial stability and creditworthiness.

- Performance guarantees are tied to the customer's ability to fulfill contractual duties.

- Normally, bank guarantees shouldn't exceed a ten-year duration.

- When setting limits, banks consider the guarantee's purpose, frequency of need, customer's financial health, track record, and required collateral.

- Following Basel II Guidelines, banks differentiate guarantees into financial or performance categories, benefiting from lower capital charges for performance guarantees.

- Customers may require bank guarantee limits, similar to credit lines, reviewed annually.

- Guarantee limits depend on the borrower's activities, guarantee purpose, and duration.

Computation of Guarantee Limit

| S.No | Particulars | Amount (₹ lakh) |

|---|---|---|

| i | Outstanding BGs | 600 |

| ii | Cancellation envisaged | 100 |

| iii | Requirement incidental to regular operations | 500 |

| iv | Requirement pertaining to contingent events | 200 |

| v | Requirement of BG (i-ii) + iii + iv | 1200 |

Issuance of Bank Guarantee — Precautions

Key Criteria for Bank Liability

- The amount guaranteed.

- The duration of the guarantee.

- Absence of these details might make bank's liability limitless in terms of amount or time.

Amount Guaranteed

- Precise amount should be mentioned in both words and numbers.

- Clearly specify if the amount includes interests, charges, taxes, etc.

- Banks are liable up to the full guaranteed amount when invoked.

Duration of Guarantee

- Clearly define:

- Validity period: Timeframe during which debtor's default leads to a claim.

- Claim period: Additional time for beneficiary to make a claim after a default.

- Defaults must happen within the validity period; claims are made within the claim period.

- For clarity, exact dates should be provided (e.g., valid up to 11 December 2027).

Claim Period

- Beneficiary gets additional time post-validity to claim.

- Typically extends 15 to 30 days past the validity period.

Indian Contract Act — Sec. 28 Amendment

- Before amendment, guarantees often had a clause limiting claim enforcement to 3-6 months.

- Pre-amendment, government bodies had up to 30 years to claim against bank guarantees.

- Post 1 January 1997 amendment, such clauses were deemed illegal.

- New timeframes for suing banks after a valid claim: 30 years for government entities, 3 years for others.

Protection for Banks

- Ensure guarantees are returned post-claim period or get a no-claim certificate from the beneficiary.

- Keep the customer's cash margin and security until either of the above happens.

Counter Guarantee & Security

- Though contingent, banks should obtain counter guarantees to safeguard against potential enforcement.

- Counter guarantees should:

- Cover bank payments, associated costs, attorney fees, interest, taxes, etc.

- Stay active until the bank's guarantee is formally discharged.

- The worth of counter guarantees depends on the financial health of the guarantor.

- Ideally, secure with tangible assets or extend existing charges to cover the guarantee.

Payment Under Bank Guarantee — Precautions

Proper Invocation

- Banks must ensure that a bank guarantee is properly invoked. If not, recourse against the debtor might be challenging.

Court Rulings on Invocation

- Delhi High Court: Likened invoking to a plaintiff disclosing the cause of action. If conditions aren't met, the bank can reject the demand.

- Calcutta High Court: A bank guarantee isn't like a legal pleading. It should be invoked in a commercial manner; it need not be detailed like a cause of action.

Banker's Considerations for Proper Invocation

- Invocation should occur within the guarantee's validity period.

- Invocation amount should not exceed the guaranteed amount. If it does, only pay the maximum stipulated amount.

- Only authorized individuals should invoke the guarantee. For government-related guarantees, roles are typically specified to avoid confusion due to personnel changes.

- The Supreme Court held that invocation by an unauthorized person invalidates the request.

No Injunctions Against Payment

- Even though courts usually don't meddle with bank guarantees, there have been instances where they've issued injunctions preventing payments.

- If there's an existing injunction and the bank pays anyway, it can be held in contempt of court.

Security for Bank Guarantees

- Banks may not have direct security for guarantees due to remote locations of construction sites.

- Instead, banks often take collateral security to cover guarantee limits.

- Credit officials should monitor contract progress after issuing a performance guarantee, either on-site or through financial statements.

- Contractors are expected to provide quarterly audited cash inflow and outflow statements.

- All bank guarantees must be backed by a charge on the borrower's assets, both current and fixed.

- In exceptional cases, unsecured bank guarantees are issued for short terms (one year) and smaller amounts (below ₹5 crores).

Period of Expiry of Guarantee

- Bank guarantees must have a clear expiry date, limiting the bank's liability.

- Banks are bound to pay only if a claim is made before the guarantee expires.

- Banks should keep track of expired guarantees to manage their capital requirements efficiently.

- It's important for banks to clear liabilities of expired guarantees promptly to avoid unnecessary capital charge.

- If the original guarantee documents are delayed, banks should notify beneficiaries about the expiry and consequent termination of liability.

Period of Claim Under the Guarantee

- Beneficiaries can invoke a bank guarantee up until the final expiry date.

- A reasonable time, typically 15 days to 3 months, is given to assess the contract and invoke the guarantee.

- Guarantees contain clauses specifying the deadline for claims.

- A bank's obligation to pay under a guarantee is unconditional and unaffected by other agreements.

- Payment on a guarantee is only deferred if a court issues a restraining order.

- The bank's liability persists until a court decision, even if the guarantee's period has ended.

Due Diligence for Guarantees from Other Banks

- Before granting credit based on another bank's guarantee, thorough due diligence is required.

- Investigate why the guaranteeing bank isn't providing the credit itself.

- Confirm that the officials from the other bank are authorized to issue the guarantee.

- Guarantees should align with the customer's regular business and location.

- Ensure timely redemption of expired guarantees.

- Guaranteeing banks should have a minimum funded exposure linked to the guarantee, varying with the sector.

Co-Acceptance Facilities

- For deferred payment purchases, sellers often request a Deferred Payment Guarantee or co-accepted usance Bills of Exchange.

- Banks should rigorously evaluate such requests as they would for any Guarantee or Letter of Credit.

- Co-acceptance by banks adds their assurance to commercial usance bills, allowing buyers to obtain credit.

RBI Guidelines for Co-Acceptance

- It's reserved for borrowers with verified needs for genuine trade transactions.

- Banks must check receipt and valuation of goods associated with the bills.

- Co-acceptance shouldn't be provided for house or accommodation bills within group companies.

- Banks shouldn't co-accept bills under Buyer's Line of Credit Schemes or those drawn by NBFCs under SIDBI Schemes.

- They are allowed to co-accept bills under Seller's Line of Credit Schemes, with no limit, ensuring buyer's payment capacity and adherence to exposure norms.

- A bank's co-acceptance of a bill under its own LC is not advised as it becomes a separate instrument governed by the Negotiable Instruments Act, not by the terms of the LC.

Co-Acceptance of Bills Covering Supply of Goods (RM)

- Co-acceptance facilities should be integrated into the working capital limits, with a corresponding reduction in the overall cap.

- Banks should co-accept only legitimate trade-related bills.

- Items listed on bills must be pledged to the bank without granting advances to prevent dual financing.

- Clients are expected to clear bills using their funds or pre-arranged credit facilities.

- Banks must avoid co-accepting internal company bills (house bills).

- Tracking due dates is crucial to ensure timely payment.

- When supplying machinery under a deferred payment guarantee:

- Process it as if assessing a Term Loan application.

- Conduct viability studies to confirm the unit's capacity for cash generation and timely payments.

- Seek additional security, possibly by charging other fixed assets.

- Avoid short-term usance periods (like 90/180 days) for machinery supply to new units, which require import LCs.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| NFB Facilities | No direct money flow; bank earns non-interest income |

| 3 Key NFB Types | LCs, Bank Guarantees, Co-acceptances |

| LC Definition | Bank guarantee ensuring payment on presenting required documents |

| LC Governed By | UCPDC 600 (Uniform Customs & Practice for Documentary Credits) |

| SFMS Mandate | From January 1, 2013 for domestic LCs |

| LC Parties | Applicant, Issuing Bank, Beneficiary, Advising Bank, Negotiating Bank, Confirming Bank, Reimbursing Bank |

| Sight LC | Immediate payment on document presentation |

| Usance LC | Deferred payment; credit period to buyer; treated as fund-based |

| Irrevocable LC | Cannot be changed without all parties' consent |

| Confirmed LC | Second bank's guarantee; double security |

| Back-to-Back LC | Secondary LC used as collateral for another |

| Red Clause LC | Advance payment to beneficiary before shipment |

| Green Clause LC | Pre-shipment financing including storage costs |

| Revolving LC | Auto-renews credit limit after each use |

| Standby LC | Functions like a bank guarantee for loan repayment |

| D.P. | Documents against Payment |

| D.A. | Documents against Acceptance (time draft) |

| Buyer's Credit | Loan from foreign bank for imports; via Nostro account |

| Supplier's Credit | Financing via discounting Usance Bills under LCs |

| BG — Legal Basis | Sec. 126, Indian Contract Act, 1872 |

| BG Parties | Applicant, Beneficiary, Guarantor (Bank) |

| Financial Guarantee | Covers financial obligations; direct credit substitute |

| Performance Guarantee | Covers non-financial contractual obligations |

| Deferred Payment Guarantee | Payment assurance for plant & machinery on installment |

| Bid Bond | Bidder's commitment; converts to performance guarantee on winning |

| Performance Bond | 10-15% of contract value |

| Maintenance Bond | Post-completion guarantee, usually 1-2 years |

| BG Max Duration | Normally ≤ 10 years |

| BG Classification | Financial vs Performance; Basel II — lower capital for performance |

| Claim Period | 15-30 days post validity period |

| Sec. 28 Amendment | Post 1 Jan 1997; govt: 30 years, others: 3 years to sue |

| Unsecured BG | Short term (1 year), below ₹5 crore |

| Co-Acceptance | Bank adds assurance to usance bills; for genuine trade only |

| Co-Acceptance Ban | No house bills, no Buyer's LoC Scheme, no SIDBI Scheme bills |

| Co-Acceptance — LC | Bank co-accepting bill under own LC is not advised |

| Non-Constituent NFB | Allowed with Board-approved policy, KYC/AML/PMLA compliance |

Lesson Doubts

Ask questions, get expert answers