📊 Credit Risk Analytics & Credit Scoring Models

Credit risk components, influences, credit risk management processes, instruments (credit approving authority, prudential limits, risk rating), credit risk analytic models (PD, LGD, EAD), Basel framework, software support, credit scoring model stages, and things to keep in mind.

Credit Risk Analytics and Credit Scoring Models

Introduction

- Banks primarily function by accepting deposits and extending loans and investments, which carry credit risk.

- Bank credit is generally considered the most profitable asset.

- Retail and corporate banking contribute significantly to a bank's revenue, with interest income forming the major share.

- Bank exposure is more susceptible to Non-Financial Risk (NFR), while lending practices focus on credit risk using scoring models.

- Risk-based measures are gaining momentum, primarily targeting income-generating assets.

- Risk is a computable metric that helps determine the amount of economic capital necessary to support a bank's exposures.

- Advanced credit risk models use well-known formula attachments/combinations to assist in gauging credit risk.

- The initial interest in credit risk models originated from the need to determine the amount of economic capital necessary to support a bank's exposures.

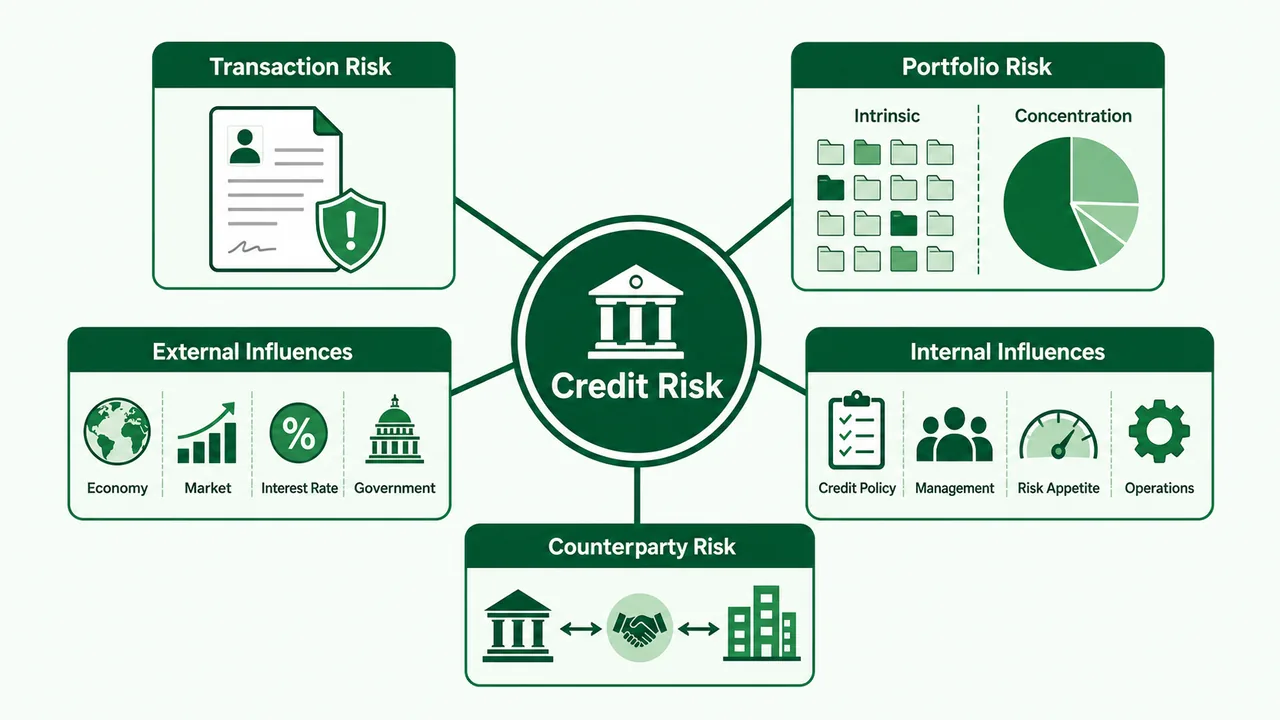

Credit Risk Components

- Transaction risk (or default risk) — risk arising from individual credit transactions.

- Portfolio risk — which consists of intrinsic risk and concentration risk.

Influences on a Bank's Credit Risk

- External factors: Economic conditions, market volatility, exchange and interest rates, trade policies, and government regulations.

- Internal factors: Credit policies, management quality, risk appetite, and operational efficiency.

- Customer satisfaction ratings are NOT typically considered an influence on a bank's credit risk.

Counterparty Risk

- Counterparty risk is a subtype of credit risk, stemming from a trading partner's failure to meet obligations due to financial or external constraints.

Credit Risk Management Processes

Credit risk management processes should include:

🔐

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

Pro

Popular Save ₹100/mo

₹ 99 /mo

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Credit Risk Analytics and Credit Scoring Models

Introduction

- Banks primarily function by accepting deposits and extending loans and investments, which carry credit risk.

- Bank credit is generally considered the most profitable asset.

- Retail and corporate banking contribute significantly to a bank's revenue, with interest income forming the major share.

- Bank exposure is more susceptible to Non-Financial Risk (NFR), while lending practices focus on credit risk using scoring models.

- Risk-based measures are gaining momentum, primarily targeting income-generating assets.

- Risk is a computable metric that helps determine the amount of economic capital necessary to support a bank's exposures.

- Advanced credit risk models use well-known formula attachments/combinations to assist in gauging credit risk.

- The initial interest in credit risk models originated from the need to determine the amount of economic capital necessary to support a bank's exposures.

Credit Risk Components

- Transaction risk (or default risk) — risk arising from individual credit transactions.

- Portfolio risk — which consists of intrinsic risk and concentration risk.

Influences on a Bank's Credit Risk

- External factors: Economic conditions, market volatility, exchange and interest rates, trade policies, and government regulations.

- Internal factors: Credit policies, management quality, risk appetite, and operational efficiency.

- Customer satisfaction ratings are NOT typically considered an influence on a bank's credit risk.

Counterparty Risk

- Counterparty risk is a subtype of credit risk, stemming from a trading partner's failure to meet obligations due to financial or external constraints.

Credit Risk Management Processes

Credit risk management processes should include:

- Measurement of risk through credit rating/scoring.

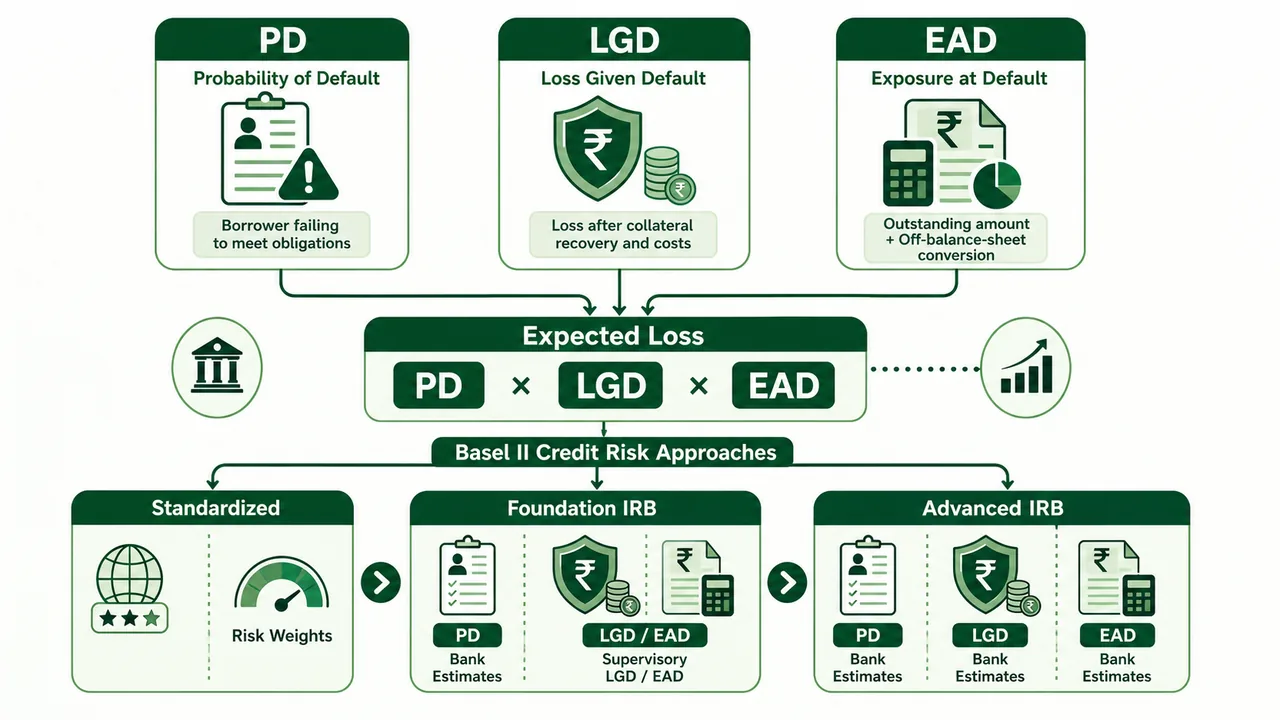

- Quantifying the risk through estimating expected loan losses — the amount of loan losses that a bank would experience over a chosen time horizon (expected losses = Probability of Default × Loss Given Default × Exposure at Default).

- Risk pricing on a scientific basis.

- Controlling risk through effective Loan Review Mechanism and portfolio management.

Loan Loss Policy

The bank's Loan Policy, endorsed by the Board, should clearly outline procedures and standards for managing credit risk, including:

- Criteria for credit proposal presentations, financial covenants, rating standards.

- Delegation of credit approval powers and limits on large credit exposures.

- Guidance on collateral standards, portfolio management, loan review, risk monitoring, loan pricing, and regulatory compliance.

Instruments of Credit Risk Management

1. Credit Approving Authority

- Banks should establish a detailed delegation of authority system for loan approval.

- Consideration should be given to setting up credit approval committees at multiple operational levels.

- A robust framework for reporting and assuring the quality of credit decisions by different groups should be implemented.

- All credit proposals should be reviewed within 3 to 6 months using a clearly defined Loan Review Mechanism.

2. Prudential Limits

- Define key financial ratios such as debt-to-equity and debt service coverage to act as limits for the Loan Policy, including aggregate limits and borrower-specific limits.

- Establish limits for single borrowers and groups that are tighter than regulatory norms.

- Set separate exposure limits for single borrowers with credit facilities at a significant level of a bank's capital funds.

- Implement maximum exposure limits by industry or sector, with regular reviews and analytical justifications.

- Restrict exposures to sectors prone to high volatility, such as real estate and capital markets.

- Ensure the maturity profile of the loan book is balanced.

- Assess the maturity profile of the loan book to address market needs, risk appetite, and maturity of liabilities.

- Prudential limits are established to enhance risk filtering and mitigate adverse impacts of credit risk.

3. Risk Rating

- Implement a unified risk scoring/rating system to evaluate counterparty risks comprehensively and support consistent credit decision-making.

- A unified risk scoring/rating system aims to standardize risk ratings across all borrowers.

- Ensure the risk rating system reduces subjectivity and enhances uniformity in the assessment process.

- Risk ratings play a crucial role in determining total lending risk, essential for determining loan pricing and terms.

- Ensure the risk rating includes migration/transition analysis for ongoing insights for loan portfolio review and management.

- The system should accurately represent the inherent credit risk within the loan book.

- Utilize the rating to give credit authorities a reliable understanding of loan quality at any given time.

Credit Risk Analytic Models

Quick Note

- Credit Risk Analytic Models are mathematical models that can be expressed in equation notation using well-known formula attachments/combinations that assist in gauging of credit risk.

- The initial interest in credit risk models originated from the need to determine the amount of economic capital necessary to support a bank's exposures.

Premises of Credit Risk Analytics

- The Bank for International Settlements (BIS) has emphasised the consistent and rigorous assessment of credit risk since the Basel I framework.

- The 2008 financial crisis highlighted the need for more advanced credit risk models due to significant banking sector losses.

- Post-crisis, banks have developed multiple advanced credit risk models, moving from outdated methods to more sophisticated approaches.

- The evolution of credit risk management models since 2008 has emphasized forward-looking elements.

- Contemporary risk management models incorporate forward-looking elements and are based on detailed probability assessments, considering both expected and unexpected losses.

- Over-reliance on historical data is problematic as it may not accurately predict future outcomes, a concept known as "history being a poor predictor".

- Credit risk models now focus on distinguishing borrower risks by estimating Probability of Default (PD), assessing collateral risks through Loss Given Default (LGD), understanding exposure through the concept of Exposure at Default (EAD), and quantifying total risk exposure at the time of default.

- Credit Conversion Factor (CCF) is applied to estimate EAD.

- Risk analytics play a crucial role in refining these models by applying statistical techniques to analyse vast datasets, identifying patterns, and predicting outcomes.

- These models aid in understanding both current and potential future credit exposures.

- These models act in tandem with PD and through the cycle (TTC) risk models, crucial for developing robust calibration procedures that account for evolving macroeconomic conditions.

- The primary role of capital in banks is to absorb unexpected losses, underscoring the importance of maintaining adequate capital against credit risk.

Credit Scoring Models Under Basel II Framework

- A characteristic of credit risk scoring models under Basel II is the estimation of banks' own PDs in Foundation IRB (Internal Ratings-Based approach).

- Under the Foundation IRB approach, banks estimate their own PDs while relying on supervisory estimates for LGD and EAD.

- Under the Advanced IRB approach, banks estimate their own PD, LGD, and EAD.

- Both approaches consider Effective Maturity of exposures.

Advantages of Analytical Models

- Periodic updating of context and parameters of the model — Once data are defined, context and parameter updates enhance the reliability and viability of analytical models, leading to scientifically sound decisions.

- Mathematical tools at hand to analyse — Utilization of mathematical tools such as Probability Theory and Risk-Weighted Functions provides a methodical approach to evaluating credit risk.

- Reasonably easy to run on commonly available platforms — Mathematical models are easily executed on common platforms like spreadsheets, simplifying the construction and application of credit risk models.

- Diverse data and ambiguities — Analytical models expedite the process of drawing conclusions, estimations, and solutions from extensive, conflicting datasets, ensuring swift and effective decision-making.

Software Support for Credit Risk Analytics

- Dedicated software initially designed for physical sciences like mathematics and chemistry is now adapted for complex credit risk analysis, with tools usable for data analysis, modelling, and financial estimations.

- Credit risk solutions encompass a multitude of multidisciplinary, blending finance, economics, and legal principles.

- The historical development of economic theories has seen significant shifts, especially with the 2008 financial crisis, necessitating advanced software tools.

- The rise of big data has transformed traditional inference approaches into more precise algorithmic methods.

- Credit risk analysis involves continuous data refinement, requiring dynamic, evolving models.

- Software tools like SAS, Stata, Eviews, MATLAB are established in the data analysis and modelling space.

- Statistical software has been adapted for complex fields like credit risk analytics.

- Open-source software like Python and R are popular due to accessibility, though this may lack rigorous quality control compared to paid software.

- The adoption and implementation of software for credit risk analysis should align with a sector-specific risk framework, guided by a specialized risk analytics team and robust regulatory standards.

Credit Scoring Models

Three Stages

- Basel I-II modeling can be divided into three stages: Specification, Foundation (SF), and Advanced (A-IRB).

Stage 1: Specification Stage (Problem Definition)

- The Standardized approach in credit risk modeling relies on external credit rating agencies for risk assessment.

- The Standardized approach assigns risk weights to different asset classes based on credit ratings.

- The Foundation IRB uses a bank's own Probability of Default (PD) estimates.

- The Advanced IRB estimates PD, LGD, and EAD independently.

- Risk weighting is applied under the Standardized approach.

- A key stage in the development of credit risk scoring models is defining the problem area.

Stage 2: Data Collection and Preprocessing

- There are multiple perspectives, sources, and dimensions of data sources.

- Financial MIS (payment status to accounts PA, LOS, and CBS, plus account-ID linked to borrower MIS) for transaction data.

- Risk profile data is weighted and re-weighted to achieve metric applicability requirements for modelling.

- End products include a master data containing of PA, LOS, and CBS and different derivations for each segment.

- Credit risk scoring models process data at multiple stages, shifting the problem away from coding to data quality and operational readiness.

- Collect entity's historical and projected data, as well as from peer entities and industry averages.

- Analyze macroeconomic and microeconomic data at local, regional, national, and global levels.

- Integrate ecosystem data from various sources like government agencies, financial institutions, industry associations, etc.

- Compare data vertically over time and horizontally across different spheres.

Stage 3: Model Development and Testing

- Develop analytical models with a clear understanding of the desired outcomes.

- Document the model development process for future adjustments.

- Test the model using known events to ensure it predicts outcomes accurately before full implementation.

Things to Keep in Mind

- Test the model under different stress scenarios to assess its sensitivity to adverse situations.

- Ensure the model can handle both base-case and multiple sensitivity scenarios.

- Calculate regulatory capital required for exposures, adhering to supervisory guidelines and accommodating changes announced by central banks.

- Implement end-to-end automation for seamless risk analytics processes.

- End-to-end automation is essential for credit risk analytics models to decrease efficiency and accuracy issues — i.e., to streamline processes and ensure consistency.

- Maintain a centralized research and development team to stay updated on analytical and regulatory dynamics.

- Insulate the source code while allowing some self-programming capabilities for estimation, simulation, and forecasting.

- Explore new technologies like machine learning for developing credit risk models.

- Invest in Fintech partnerships or in-house resources proficient in analytics-friendly languages like Python to enhance model accuracy and scientific rigor.

Quick Notes for Exam

- Assets of banks are most vulnerable to Credit Risk.

- The primary function of banks in relation to credit risk is providing loans and investments.

- A key component of credit risk management is assessing potential losses, both expected and unexpected.

- Credit Conversion Factor (CCF) is applied to estimate EAD (Exposure at Default).

- Customer satisfaction ratings are NOT considered an influence on a bank's credit risk — but economic conditions, market volatility, and government regulations ARE.

- The purpose of implementing prudential limits in credit risk management is to enhance risk filtering and mitigate adverse impacts.

- The objective of a unified risk scoring/rating system is to standardize risk ratings across all borrowers.

- The evolution of credit risk management models since the 2008 financial crisis has emphasized forward-looking elements.

- Statistical software (not medical, gaming, or graphic design software) has been adapted for credit risk analytics.

- Under Basel II Foundation IRB, banks estimate their own PDs while using supervisory estimates for LGD and EAD. Under Advanced IRB, banks estimate all three independently.

- A key stage in credit risk scoring model development is defining the problem area.

- End-to-end automation is essential to streamline processes and ensure consistency.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Credit Risk | Risk from lending and investment activities; banks' most vulnerable asset |

| Credit Risk Components | Transaction risk (default risk) and Portfolio risk (intrinsic + concentration) |

| External Influences | Economic conditions, market volatility, exchange/interest rates, trade policies, govt regulations |

| Internal Influences | Credit policies, management quality, risk appetite, operational efficiency |

| NOT an Influence | Customer satisfaction ratings |

| Counterparty Risk | Subtype of credit risk; trading partner fails to meet obligations |

| Expected Loss Formula | PD × LGD × EAD |

| PD | Probability of Default |

| LGD | Loss Given Default |

| EAD | Exposure at Default |

| CCF | Credit Conversion Factor — applied to estimate EAD |

| Loan Review | All proposals reviewed within 3 to 6 months |

| Credit Approving Authority | Delegation of authority; committees at multiple levels |

| Prudential Limits | Debt-to-equity, debt service coverage; tighter than regulatory norms |

| Prudential Limits Purpose | Enhance risk filtering and mitigate adverse impacts |

| Risk Rating | Unified system; reduces subjectivity; standardizes across all borrowers |

| Risk Rating Use | Determines total lending risk, loan pricing, and terms |

| Migration Analysis | Included in risk rating for ongoing loan portfolio insights |

| BIS/Basel I | Emphasised consistent and rigorous credit risk assessment |

| 2008 Financial Crisis | Highlighted need for advanced models; emphasized forward-looking elements |

| Historical Data Risk | Over-reliance problematic — "history is a poor predictor" |

| Economic Capital | Primary role: absorb unexpected losses |

| Basel II — Standardized | Relies on external credit rating agencies; assigns risk weights |

| Basel II — Foundation IRB | Banks estimate own PD; supervisory estimates for LGD & EAD |

| Basel II — Advanced IRB | Banks estimate own PD, LGD, and EAD |

| Effective Maturity | Considered in both Foundation and Advanced IRB approaches |

| Analytical Model Advantages | Periodic updates, math tools (Probability Theory, Risk-Weighted Functions), spreadsheet-friendly, handles diverse data |

| Software — Paid | SAS, Stata, Eviews, MATLAB |

| Software — Open Source | Python and R (popular but may lack rigorous quality control) |

| Software Type | Statistical software adapted for credit risk analytics |

| 3 Stages of Scoring Models | Specification, Foundation (SF), Advanced (A-IRB) |

| Stage 1 | Problem definition; Standardized/Foundation IRB/Advanced IRB |

| Stage 2 | Data collection & preprocessing; Financial MIS, peer data, macro/micro data |

| Stage 3 | Model development & testing; test with known events |

| Data Sources | Historical + projected, peer entities, industry averages, macro/micro, ecosystem data |

| Key Stage | Defining the problem area |

| Stress Testing | Test under different stress scenarios; base-case + sensitivity scenarios |

| Regulatory Capital | Calculate per supervisory guidelines; accommodate central bank changes |

| End-to-End Automation | Essential for seamless risk analytics; streamline processes, ensure consistency |

| R&D Team | Centralized team for analytical and regulatory dynamics |

| Source Code | Insulate while allowing self-programming for estimation/simulation |

| New Technologies | Machine learning for credit risk models |

| Fintech/Python | Invest in partnerships or in-house resources for model accuracy |

Lesson Doubts

Ask questions, get expert answers