📋 Project Appraisal & Term Loan Appraisal

Project appraisal process, technical/commercial/managerial/financial/environmental appraisal, term loan appraisal, project cost and finance, DSCR, sensitivity analysis, break-even analysis, capital budgeting (Pay Back Period, ARR, NPV, IRR, BCR).

Project Appraisal / Term Loan Appraisal

Introduction

Project Appraisal

- Process of reviewing and evaluating a project to assess feasibility and potential return.

- Aims to approve or reject the project concept.

- Analyses the projected need and potential benefits, identifying stakeholders.

- Creates a decision package for project approval or rejection.

Term Loans

- Loans used to acquire fixed assets (e.g., buildings, machinery).

- Repaid over an extended period.

- Key classification:

- Beyond 36 months: Term loans.

- Up to 36 months: Demand loans.

- Used for new ventures (green field) or existing units (brown field).

- Can be for expansion, modernisation, or asset replacement.

Why Project Appraisal

Project Basics

- Projects organise resources.

- Appraisal reviews various aspects: technical, managerial, financial, market, etc.

Bank's Role & Appraisal

- Banks evaluate project viability before funding.

- Focus is on the project's return on investment.

- Shift from security-focused to purpose-oriented lending emphasises appraisal techniques.

- Project viability is primary; collateral is secondary.

Project Viability Concerns

- If reliant on collateral, main project security has likely failed.

- Questions arise on the accuracy of viability assessments.

Post-Appraisal Activities

- Proper appraisal isn't the only key to project success.

- Timely and appropriate fund disbursement is crucial.

- Regular supervision ensures on-schedule progress.

- Adherence to implementation schedules in large projects is vital.

Delays & Impact

- Delays cause cost escalations.

- Delays in funding amplify implementation setbacks.

- Any delay can create a cycle of further delays and rising costs, threatening viability.

Aspects of Project Appraisal

Banker's Initial Assessment

- A consulting pitch can be an initial validation for considering financial support.

- Evaluation criteria include:

- Technical Evaluation

- Market Analysis

- Costing & Management Review

- Examination of financial performance (for existing entities)

- Project cost and funding sources

- Key financial ratios

- Determination of breakeven point

- Evaluation using NPV, IRR, BCR, and other financial metrics

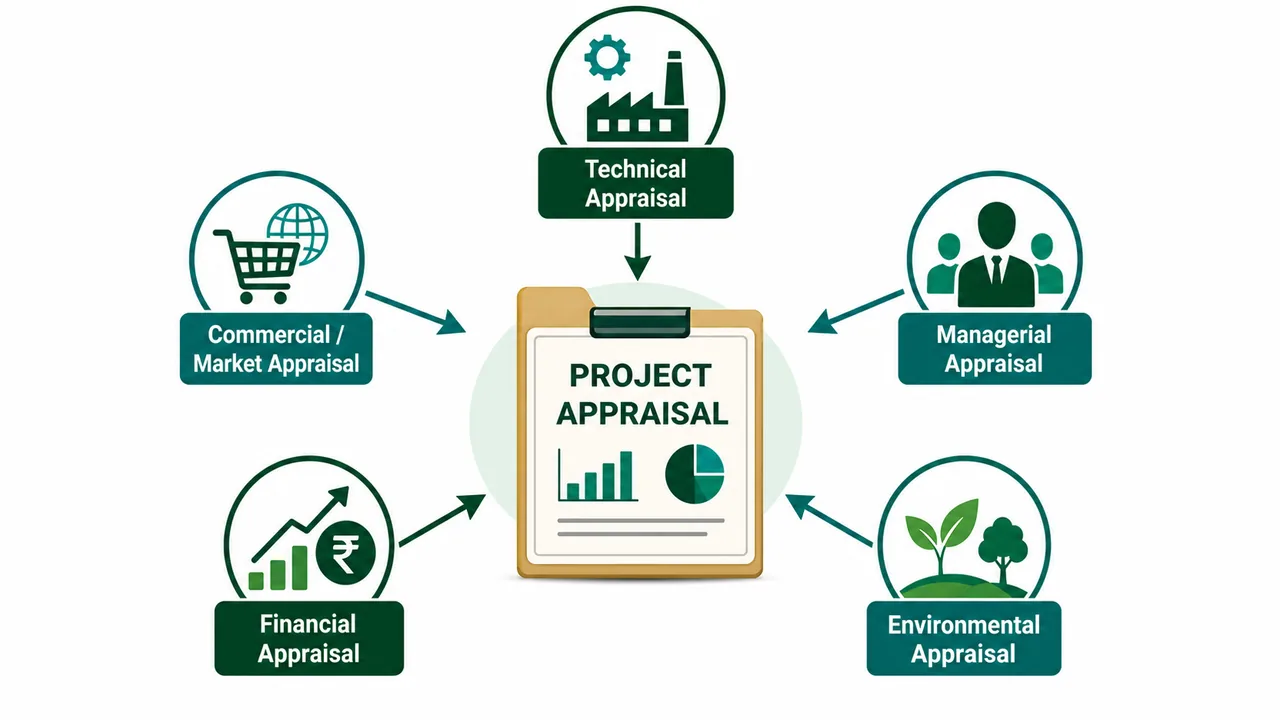

The Five Angles of Evaluation

Evaluating project viability involves the following angles — Historical is NOT an angle for evaluating project viability:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Project Appraisal / Term Loan Appraisal

Introduction

Project Appraisal

- Process of reviewing and evaluating a project to assess feasibility and potential return.

- Aims to approve or reject the project concept.

- Analyses the projected need and potential benefits, identifying stakeholders.

- Creates a decision package for project approval or rejection.

Term Loans

- Loans used to acquire fixed assets (e.g., buildings, machinery).

- Repaid over an extended period.

- Key classification:

- Beyond 36 months: Term loans.

- Up to 36 months: Demand loans.

- Used for new ventures (green field) or existing units (brown field).

- Can be for expansion, modernisation, or asset replacement.

Why Project Appraisal

Project Basics

- Projects organise resources.

- Appraisal reviews various aspects: technical, managerial, financial, market, etc.

Bank's Role & Appraisal

- Banks evaluate project viability before funding.

- Focus is on the project's return on investment.

- Shift from security-focused to purpose-oriented lending emphasises appraisal techniques.

- Project viability is primary; collateral is secondary.

Project Viability Concerns

- If reliant on collateral, main project security has likely failed.

- Questions arise on the accuracy of viability assessments.

Post-Appraisal Activities

- Proper appraisal isn't the only key to project success.

- Timely and appropriate fund disbursement is crucial.

- Regular supervision ensures on-schedule progress.

- Adherence to implementation schedules in large projects is vital.

Delays & Impact

- Delays cause cost escalations.

- Delays in funding amplify implementation setbacks.

- Any delay can create a cycle of further delays and rising costs, threatening viability.

Aspects of Project Appraisal

Banker's Initial Assessment

- A consulting pitch can be an initial validation for considering financial support.

- Evaluation criteria include:

- Technical Evaluation

- Market Analysis

- Costing & Management Review

- Examination of financial performance (for existing entities)

- Project cost and funding sources

- Key financial ratios

- Determination of breakeven point

- Evaluation using NPV, IRR, BCR, and other financial metrics

The Five Angles of Evaluation

Evaluating project viability involves the following angles — Historical is NOT an angle for evaluating project viability:

- Technical Appraisal

- Commercial / Market Appraisal

- Managerial Appraisal

- Financial Appraisal

- Environmental Appraisal

Technical Appraisal Overview

Infrastructure & Requirements

- Assess available infrastructure.

- Check licensing and registration needs.

- Choose appropriate technology and technical processes.

- Ensure availability of raw materials and skilled labour.

Production Aspects

- Understand manufacturing process and technical setup.

- Prepare plant cost, product quality, equipment procurement.

- Study project implementation timeline and input availability.

Location Factors

- Analyse factors: land, raw materials, utilities, transportation, labour, infrastructure.

Technology & Manufacturing

- In developing countries, reliance might be on foreign technology.

- Ensure updated and effective technology is adopted.

- Examine supply-chain terms and technology's life cycle.

- Certain processes may require collaboration or may be restricted.

- Different products might require diverse processes (e.g., oleic acid or soap production).

Human Resources

- Ensure qualified staff is available.

- Implement training, especially if know-how is foreign.

- Consider turnkey contracts for smooth project execution and covering initial operations.

Optimal Plant Size

- Ensure plant size is economically viable.

- Plant size can be defined by supply, input, or machinery constraints.

- Consider minimum economic size, market availability, capital needs, and market size.

- Larger units often have economic advantages, but market absorption is key.

- Consider local raw material sourcing for better flexibility (e.g., sugar plant example).

Plant Size and Market

- Determine plant size based on market absorption capacity.

- Avoid plants with excessive capacities that aren't economical.

- High production without market absorption can block funds in inventory.

Product Considerations

- Base product mix/range on market potential.

- Consider size, quality, and market segment differentiation.

- Ensure flexibility to adapt product line to market changes.

Plant & Machinery

- Choose between local and imported machinery.

- For local machinery, gather feedback on the supplier.

- For imports, check overseas supplier's credibility.

- For used machinery, evaluate condition, residual life, and performance guarantees.

- Some suppliers assist with installation and other performance guarantees.

Plant Layout

- Efficient layouts save time and costs.

- Ensure logical flow for materials and processes.

- Plan for storage and future expansion.

- For chemical units, have distant effluent treatment plants.

Raw Materials

- Ensure raw material availability and understand supply regulations.

- Consider multiple vendors for reliable supply and competitive pricing.

- Seek alternative or substitute materials.

Labour

- Ensure the availability of various labour skills.

- Plan for training and housing if needed.

Utilities

- Secure essential utilities: power, water, fuel, transportation.

- Have backup plans, such as generators, for power outages.

Implementation

- Create a realistic implementation schedule accounting for all milestones.

- Account for potential delays.

Licenses & Requirements

- Check necessary licences and permissions.

- Register with appropriate authorities depending on the industry and operations.

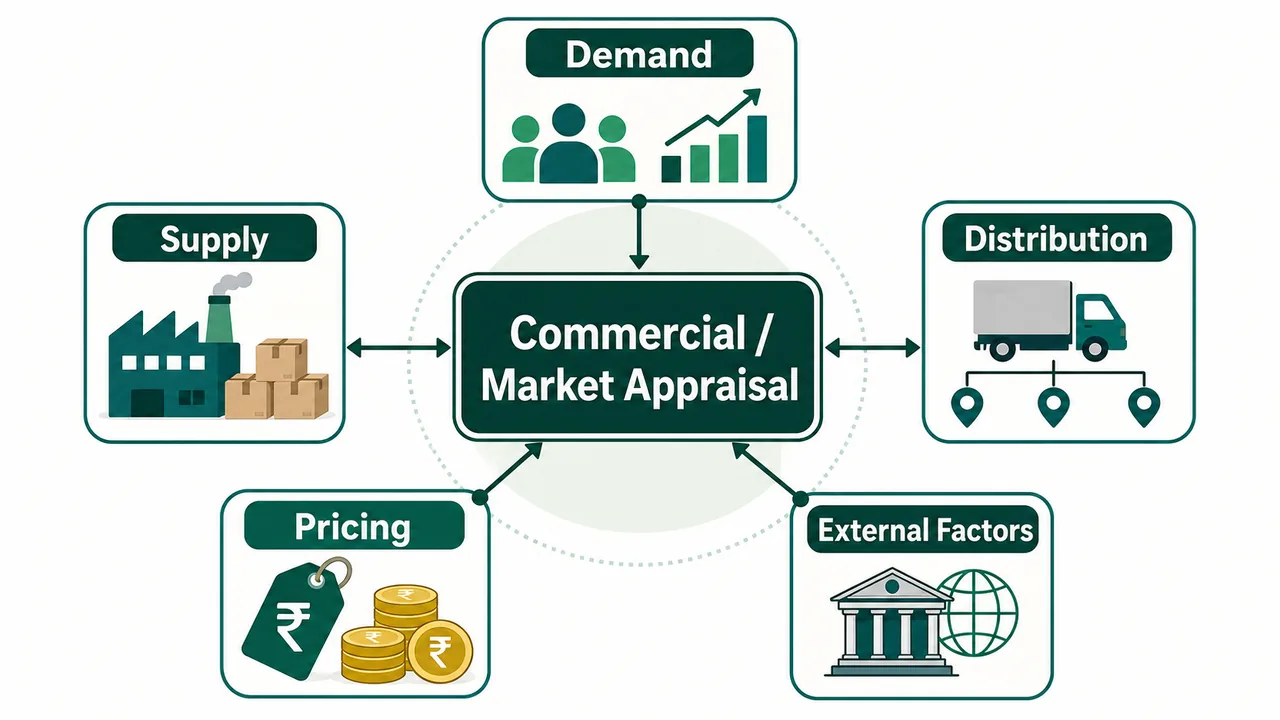

Commercial / Market Appraisal Overview

- Crucial for project evaluation.

- Involves studying demand, supply, distribution, pricing, and external factors.

- Market survey reports can be valuable.

Key Components

| Component | Details |

|---|---|

| Demand | Product details and its uses; current and future consumers; competition trends and export potential |

| Supply | Current production capacity and utilization; imports and future capacity predictions |

| Distribution | Channels used and associated costs; preferred transportation methods |

| Pricing | Local and global pricing trends; impact of duties, taxes, and price controls |

| External Factors | Government regulations on industrialisation, trade, collaborations; relevant economic plans |

Demand Forecasting Techniques

- Import substitution.

- Analysing past trends.

- End-use analysis.

- Correlation and regression studies.

- Evaluating export markets.

Commercial Appraisal Focus Areas

- Market outlook and competitor analysis.

- Market size and projected share of the unit.

- Pricing frameworks.

- Raw material considerations.

- Marketing strategies.

Market Relevance

- Selling capability is as crucial as production.

- A unique product with no competitors eases marketing, unless cheaper imports are available.

- Success factors: leadership, product quality, and effective sales strategy.

Managerial Appraisal Overview

- Focuses on evaluating the individuals or teams behind a business.

- Success heavily influenced by the competency of leaders.

- "The man behind the project" is crucial.

- Confidence in transactions based on:

- 5 C's: Character, Capacity, Capital, Collateral, Conditions.

- Additional factors: Reliability, Responsibility, Resources.

Elements of Managerial Appraisal

- The Entrepreneurs

- Directors/Partners

- The Management Team

- Managerial set-up

- Infrastructure of Liquidity, Integrity, Vision, Ethics & Abuse

- Operational transparency

- External relationships: banks-understanding, Sound micro environment

Key Points

- Competence is essential for each role.

- Evaluate past performance including long-term project consultations during assessment.

Financial Appraisal Overview

- Assesses the project's financial feasibility.

- Important factors: Project cost and execution timelines.

- Delays often lead to increased costs.

- Timely and adequate finance is crucial.

- Reliance on government subsidies should be minimised.

- Key tools: Profitability estimate, Break-even analysis, Debt service coverage ratio.

Environmental Appraisal Overview

- Examines the interplay between the project and the environment.

- Relevant environmental factors: Water, Air, Land, Sound, Conservation policies, Geographical location.

- Essential to secure clearances from pollution control and other relevant authorities.

Term Loan Appraisal

Purpose

- Acquisition of capital assets (Land, Building, Plant & Machinery, Modernisation, etc.).

Duration

- 3 to 10 years.

Feasibility Aspects

- Future earnings of the unit.

- Higher risk than working capital finance due to reliance on future savings.

Appraisal Focuses On

- Feasibility of physical, economic, technical aspects, future trends, cost returns, funds and management.

- Term Loan Appraisal does NOT examine historical loan amounts.

- In term loan appraisal, historical performance is NOT a primary focus — the focus is on technical feasibility, financial feasibility, and future trend analysis.

- The appraisal aspect that examines future trends of a project is the Term Loan appraisal.

Analysis for Existing Concerns

Evaluation Criteria

- Technical, managerial, commercial, financial aspects.

For Functioning Companies

- Review the last 3 years' audited Balance Sheet and Profit & Loss.

- Determine trends: profits/losses and their causes.

- Analyze proportion of borrowings to paid-up capital and reserves.

- Examine current liabilities vs. current assets.

- Check for proper asset depreciation, fund interlocking with associated concerns, profit reinvestment.

Key Principles

- Essential to evaluate if a project is viable.

- Anticipates unforeseen challenges and complexities.

Project Cost & Finance

Cost of the Project

| Cost of the project | Sources of Finance |

|---|---|

| Land, site development, building and other civil works | Share Capital (equity/preference), Reserves and Surplus, Internal accruals from existing cash accruals |

| Plant & Machinery | Term loans from FIs etc. |

| Misc. assets | Term loans, Capital subsidy |

| Electrical fittings | Term loans |

| Preliminary & pre-operative expenses | Debentures |

| Contingencies | Unsecured loans |

| Working capital margin | Own funds |

Technical Appraisal: Financial vs. Technical Angle

Cost & Its Components

- Includes raw materials, utilities, labour costs, and selling expenses.

- Output quality impacts pricing: reject rates and selling prices.

- Proper costing leads to accurate product pricing.

Cost & Its Estimation

- Requires technical expertise.

- Involves estimation of Processing & Manufacturing, Packaging & Despatch, Marketing & Distribution, Administration, Finance & Interest, Depreciation.

- Includes consumables (items that don't form part of product).

Working Assumptions

- Capacity utilization (often 60-75% in Year 1, stabilizing by Year 3).

- Capital outlay includes building, machinery, and net working capital requirement.

Technical Consultants & Fees

- If firm requires technical experts from within or outside the country.

- Sources: Project report creation, technology engineering.

- Costs: Components of the project.

- Royalty payments: Usually a percentage of output/production; considered in profitability projections.

Foreign Expertise

- Foreign expertise might be necessary for project implementation.

- Costs: Part of the project, also treated as operational expenses.

Consumables

- Encompasses goods not directly used in manufacturing.

- Examples: furniture, stationery, lab equipment, firefighting facilities, etc.

Preliminary & Pre-operative Expenses

- Costs incurred/borne before the company's formation in general.

- Examples: company registration "ROC" (initially separated as part of "cost" from preliminary expenses).

- Costs between company formation and the start of commercial production.

- Examples: salaries, insurance, rent, etc.

Escalation

- Price escalation "For" (literally speculated in expected and agreed upon "rate of escalation").

- Covers anticipated increases during construction/pre-commercial period of the project.

Sources of Finance

Share Capital

- Types: Equity (from owners/shareholders) or Preference shares.

Term Loans

- Offered by banks and financial institutions.

- Categories: Rupee loans (for domestic procurement) and Foreign Currency loans.

- Convertible: Can be changed to equity, either partially or fully.

- DFIs (Development Finance Institutions): specialized agencies promoting industrial and economic growth.

Incentive Sources

- Financial boosts from government/agencies.

- Forms: Seed Capital, capital subsidies, tax incentives/concessions.

Miscellaneous Sources

- All resources outside traditional sources.

- Includes: unsecured loans, deposits, fixed deposits, leasing, and hire purchase.

Key Points

- Equity and debt financing determined by debt-equity standards and promoter contributions.

- Require a separate demand-based planning, cost-benefit analysis, and potential GDR approvals.

Cost of Production & Profitability Estimation

Data Required for Estimation

| Category | Items |

|---|---|

| Capacity | Installed capacity |

| Working | Daily shifts & working days |

| Product | Product assortment |

| Quantity/Price | Input quantity & pricing; Output quantity & pricing |

| Raw material | Raw material and production mix |

| Labour | Labour expenses |

| Overheads | Plant operational costs, admin costs, packaging expenses, marketing costs, financial charges, depreciation, tax obligations, maintenance charges |

Key Steps

- Determine the project's running potential.

- Determine loan servicing capacity.

- Calculate internal rate of return.

- Ascertain break-even levels.

- Decide on minimum plant capacity.

- Make estimates for future growth.

Debt Service Coverage Ratio (DSCR)

- Represents a company's ability to handle its term liabilities.

Formula

DSCR = (Net Profit + Depreciation + Interest on Term Loan) / (Term Loan Instalment + Interest on Term Loan)

- DSCR above 1.5 indicates the project can comfortably service its debt.

- DSCR measures a company's capability to manage term liabilities.

Key Points

- DSCR and IRR values rely on factors like capacity utilization, raw material prices, and selling prices.

- It's wise to adjust key parameters by ±10%.

- Significant changes in DSCR and IRR due to a ±10% tweak in any factor denotes the project's sensitivity to that factor.

- DSCR is NOT directly used for measuring project profitability — it measures debt servicing capability.

- DSCR is NOT a primary tool for evaluating project profitability.

Sensitivity Analysis

- Sensitivity Analysis checks financial viability under adverse situations.

- It is used to check financial viability under challenges.

- Essential for assessing financial strength in challenging scenarios.

- The ability to check a project's financial health even during tough times is provided by Sensitivity Analysis.

Break-Even Analysis

- A tool for evaluating project profitability.

- Highlights the link between costs, revenue, and profit.

- Break-even analysis focuses on the no-profit-no-loss point.

- The break-even point indicates no-profit-no-loss.

- The level at which a unit neither makes a profit nor a loss is termed the break-even point.

- Break-even Analysis provides insight into a project's profitability without profit or loss.

Two main types

- Fixed Costs: Unchangeable in the short/medium term (e.g., depreciation, loan interest, maintenance).

- Variable Costs: Change with production levels.

Break-even point

Break-even analysis finds the sales volume where total costs equal total revenue.

Tabular Example

| Explanation | Parameters | |

|---|---|---|

| Fixed Cost per unit = ₹ 500 | Fixed Cost per unit = ₹ 500 | |

| Selling Price per unit = ₹ 2 | Selling Price per unit = ₹ 2 | |

| Contribution per unit = Selling Price – Variable Cost = ₹ 1 | Contribution per unit = ₹ 1 | |

| Breakeven Point (units) = Fixed Cost / Contribution per unit = 500 / 1 = 500 units | Contribution = 50% of Sales | |

| Breakeven Point (₹) = Selling Price per unit × 500 units = ₹ 1 × 500 = ₹ 500 | Contribution Value = ₹ 500 |

Examples of High Break-Even Units

| Industry | Characteristics |

|---|---|

| Airline Industry | High fixed costs (e.g., aircraft cost) versus variable costs; must fill seats (high load factor); opportunity cost — last-minute tickets might sell at discount |

| Hotel Industry | High fixed costs for wages, laundry, and cleaning; late-night room profitability — above the costs of laundry, the room is mostly profit; factors affecting discount: hotel's reputation and self-sufficiency; a motel charges for premium rate due to opportunity cost |

Capital Budgeting

- Entrepreneurs must weigh aims and costs of potential investments.

- Relevant for both new and existing businesses raising investment.

Capital Budgeting Techniques

- Pay Back Period

- Average Rate of Return (ARR)

- Net Present Value (NPV)

- Internal Rate of Return (IRR)

- Benefit-Cost Ratio (BCR)

Pay Back Period Method

- Goal: Determine how long it takes to recover the project's initial investment.

- Calculated by accumulating cash inflows until they match the initial cost.

- Cash inflows include: Net Profit (post-tax), depreciation, and other non-cash expenses.

- Decision rule: A shorter payback period signals a more attractive project.

- Pay Back Period Method specifically determines duration for investment recovery.

- Pay Back Period Method measures the period required for a project to recover its entire investment.

Example

A project with ₹ 1000 Lakh initial investment:

| Year | Annual Cash Inflow | Cumulative Cash Inflow |

|---|---|---|

| 1 | 100 | 100 |

| 2 | 150 | 250 |

| 3 | 250 | 500 |

| 4 | 300 | 800 |

| 5 | 300 | 1100 |

Payback period falls between Year 4 and Year 5.

Draw Backs of the Pay Back Period Method

- It considers cash flows only up to the point the original investment is recovered and ignores returns thereafter.

- It does not take into consideration the time value of money.

Average Rate of Return (ARR)

- Computes the average annual profit / total initial investment.

- Uses the average of yearly net profits after depreciation.

- ARR compares annual net profits to original and average investments.

- The tool that evaluates average annual net operating profits is the Average Rate of Return.

- The method that assesses the average of annual net profits to investments is the Average Rate of Return.

To determine the average investment

- Calculate yearly average between opening and closing book values of investments.

- Take the average of all yearly averages.

Formula

ARR = (Average investment over the project's life) / Average profit × 100

Key Point

- The payback and average rate of return methods overlook the time value of money.

- Average Rate of Depreciation is NOT a measure used in appraising a project's profitability.

Time Value of Money & Discounting Technique

- Money's value today differs from its future value.

- Immediate cash is more valuable because it can earn interest.

Key Concepts

| Concept | Definition |

|---|---|

| Compounding | Increases the current value over time; transforms today's cash flow to its expected future value |

| Discounting | Determines today's value from future value; converts future cash flow to its present value |

| Discounting Factors | Used to derive present value from future sums; found in tables based on return rates and periods |

For 10% Return

- 1 year's future ₹1 = ₹0.909 today

- 2 years' future ₹1 = ₹0.826 today

- 3 years' future ₹1 = ₹0.751 today

Formulas

- Present Value: PV = Discount Factor × Expected Payment (C1)

- Interest: INT = PV × r/100

- Cash Flow at end of Period 1: C1 = PV × (1 + r)

- For n periods: Cn = PV × (1 + r)^n

Where:

- PV = Present Value

- i = Interest rate per period

- r = Rate expressed as a fraction (i / 100)

- I = Principal plus Interest

- n = Number of periods

Net Present Value (NPV) Method

- Deals with multiple cash flows, including payouts and payins.

- Each cash flow is assigned a present value.

- Payins are marked with +ve signs; payouts with -ve signs.

- The sum of all present values is the Net Present Value (NPV).

- NPV involves discounting future cash flows at a pre-determined cut-off rate.

- If cash flows of all project years are discounted at a fixed rate, the method being used is NPV.

Example

| Amount | |

|---|---|

| Today: Payout | ₹ 10,000 |

| Year 1: Payin | ₹ 6,500 |

| Year 2: Payin | ₹ 9,000 |

| Year 3: Payout | ₹ 1,000 |

Given a 10% annual discount rate:

- Initial payout: PV1 = -10,000

- Year 1 Payin: PV2 = 6,500 ÷ 1.1 = +5,909

- Year 2 Payin: PV3 = 9,000 ÷ 1.21 = +7,438

- Year 3 Payout: PV4 = -1,000 ÷ 1.33 = -752

- NPV = (-10,000) + 5,909 + 7,438 - 752 = +2,595

NPV Decision Rules

| Condition | Interpretation |

|---|---|

| Positive NPV | Project's profit > marginal investment rate/cost of capital. Project can be accepted |

| NPV > 0 | Earnings from project > marginal investment rate |

| Negative NPV | Earnings < marginal investment rate/cost of capital |

NPV Summary Points

- Cut-off rate should be ≥ cost of funds.

- Use Excel's NPV formula: -NPV (rate, range of cash flows).

- Cash flow timing affects NPV.

- When investments are the same, choose project with higher NPV.

- Don't directly compare two projects with different investments using just NPV.

- NPV aids stakeholders in understanding a project's intrinsic financial strength.

- For determining financial viability, the most powerful tools for stakeholders are NPV and IRR.

Comparing Two Projects with Different Investments

Use the Present Value Index (PVI):

PVI = Present value of cash inflows / Present value of cash outflows

- The tool that evaluates the financial health of a project is the Present Value Index.

Pre-set Cut-off Rate or Minimum Return Rate

- Discount rate for NPV is ideally based on the opportunity cost of investment funds.

- Determining the exact opportunity cost is challenging.

- Alternative measures can be the entrepreneur's expected project return or the average capital cost.

- Due to complexities in determining the exact rates, many institutions use the term debt's interest rate as the discounting cut-off rate.

Internal Rate of Return (IRR)

- IRR stands for Internal Rate of Return.

- IRR is the discount rate making the Net Present Value zero.

- The discount rate where the project's NPV is zero is the IRR.

- It represents the annualized effective compounded return rate.

- IRR indicates the profitability of expected cash flows.

- Reflects the Time Value of money and investment risk.

- Banks evaluate a project on whether the minimum return can exceed cost of capital (DSFR) or rate of return (ROR).

- IRR is critical for determining the financial feasibility of a project.

Decision Rules

| Condition | Decision |

|---|---|

| IRR > Cost of Capital | Accept investment |

| IRR < Cost of Capital | Reject |

- IRR is used to determine if the cost of funds is lower than IRR — if yes, the project is viable.

- If a project's IRR exceeds its funding cost, the project is deemed financially viable.

- The gap between IRR and funding cost provides a financial safety margin.

- This safety margin doesn't address technical, commercial, or economic aspects of the project.

- The margin of safety for the viability of a project from a financial angle is the difference between IRR and the cost of funds.

- IRR isn't typically used to compare different projects.

- Viability from a financial angle is indicated when the cost of funds is lower than IRR.

How to Calculate IRR

- IRR is found by discovering the discount rate at which NPV = 0.

- Try an initial rate, observe if NPV is positive or negative, then adjust.

- Use interpolation between the two rates where NPV changes sign.

Data Required for NPV & IRR Calculation

General Requirements

- Project lifespan

- Cash outflow details (investment for capital & working capital)

- Cash inflow projections (project benefits)

- Net cash receipts and IRR computation

- Set cut-off rate or minimum return rate

Project Lifespan

- Defined by the period it remains economically productive.

- Determined by the shortest of: a. Physical lifespan, b. Technological lifespan (equipment aging), c. Market lifespan (product obsolescence).

- Not solely based on depreciation rates in accounting books.

- The life of a project should NOT be based on rate of depreciation in books.

- Industrial projects typically have a 12-year life; exceptions based on industry specifics.

Cash Outflow

- Used for obtaining fixed and current assets.

- Fixed assets = project cost – working capital margin; interest during construction.

- Cash for additions to fixed assets are logged in the year they occur.

- Working capital (current assets) = non-bank-borrowed liabilities with production.

- Project's "year zero" is its implementation or construction start. Subsequent years with production.

- Cash outflow includes all EXCEPT profit from operations.

- Cash outflow includes: requirement of working capital, cost of fixed assets, expenditure on fixed assets addition.

Cash Inflow

- Consists of operational profits and project's end-of-life residual value.

- Profits are considered before interest, lease, depreciation, and tax.

- For the lending bank's perspective, use profit before interest and after tax.

- For equity holders' perspective, use profit after tax but add back interest, lease, and depreciation.

- IRR from the equity holders' perspective should consider benefits after the deduction of tax.

- An essential aspect of the IRR from the equity holder's viewpoint is tax benefits post deductions.

- For broader economic analysis, adjust cash flow for societal impacts using shadow prices.

- Cash inflow includes all EXCEPT initial investment cost.

- Cash inflows include: operating profits, residual value of assets, profit after tax — but NOT initial investments.

Residual or Terminal Value

- This is the value of assets at the end of the project's lifespan.

- Include it in the final year's cash inflow.

- The residual value of assets should be added to the cash inflow of the last year of the project life.

- Land remains at its initial cost (non-depreciating), while other assets take their salvage value.

- Land does not undergo depreciation.

- Assets have a value even at the end of the estimated project life.

Net Cash Receipt & IRR Calculation

- Net receipt is the difference between cash inflow and outflow.

- Initial stages might show negative values due to high investments, but will turn positive with increased production and profitability.

- Use tools like Excel to determine IRR from net cash receipts.

Benefit-Cost Ratio (BCR) Overview

Calculation

BCR = Total Benefits / Total Costs

Example

- Project costs ₹ 100,000 and provides total benefits of ₹ 150,000.

- BCR = 150,000 / 100,000 = 1.5

Interpretation

| Condition | Meaning |

|---|---|

| BCR > 1 | Benefits outweigh costs — for every rupee spent, ₹ 1.50 of benefits gained |

| BCR = 1 | Benefits equal costs |

| BCR < 1 | Costs exceed benefits |

Banker's Point of View

- When BCR > 1: Accept

- When BCR = 1: Indifferent

- When BCR < 1: Reject

Quick Notes for Exam

- The shift from security-oriented to purpose-oriented lending emphasises appraisal techniques.

- Historical is NOT an angle for evaluating project viability — the valid angles are Technical, Commercial, Managerial, Financial, Environmental.

- Term Loan Appraisal does NOT examine historical loan amounts.

- DSCR measures a company's capability to manage term liabilities.

- The break-even point indicates no-profit-no-loss.

- The Pay Back Period Method determines the time needed to recover the initial project investment.

- ARR compares annual net profits to original and average investments.

- The discount rate where the project's NPV is zero is the IRR (Internal Rate of Return).

- Pay Back Period Method measures the period required to recover the entire investment.

- Sensitivity Analysis checks financial viability in adverse situations.

- IRR is used to determine if the cost of funds is lower than IRR.

- The life of a project should NOT be based on rate of depreciation in books — but on physical life, technological life, or product market life.

- Depreciation remains within a unit and does not involve cash flow.

- The residual value of assets should be added to the cash inflow of the last year of the project life.

- Land does not undergo depreciation.

- The margin of safety for financial viability is the difference between IRR and cost of funds.

- A project's technical feasibility is determined during Term Loan Appraisal.

- The NPV Method involves discounting future cash flows at a pre-determined cut-off rate.

- Sensitivity Analysis is essential for assessing financial strength in challenging scenarios.

- Cash inflow includes all EXCEPT initial investment cost.

- Cash outflow includes all EXCEPT profit from operations.

- Present Value Index evaluates the financial health of a project.

- DSCR is NOT a primary tool for evaluating project profitability — NPV, IRR, and Break-even Analysis are.

- The most powerful tools for determining financial viability for stakeholders are NPV and IRR.

- Average Rate of Return evaluates average annual net operating profits.

- In term loan appraisal, historical performance is NOT a primary focus.

- Net Present Value aids stakeholders in understanding a project's intrinsic financial strength.

- Break-even Analysis focuses on the no-profit-no-loss point.

- IRR is critical for determining the financial feasibility of a project.

- Industrial projects typically have a 12-year life.

- IRR from the equity holders' perspective considers benefits after deduction of tax.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Project Appraisal | Review and evaluate project feasibility and return |

| Term Loan | For fixed assets; repaid over 3–10 years |

| Term Loan vs Demand Loan | Term: >36 months; Demand: ≤36 months |

| Green Field | New venture |

| Brown Field | Existing unit (expansion/modernisation) |

| Lending Shift | Security-oriented → purpose-oriented (appraisal techniques) |

| 5 Appraisal Angles | Technical, Commercial, Managerial, Financial, Environmental |

| NOT an Appraisal Angle | Historical |

| 5 C's (Managerial) | Character, Capacity, Capital, Collateral, Conditions |

| Technical Appraisal | Infrastructure, production, location, technology, HR, plant size, machinery |

| Commercial Appraisal | Demand, supply, distribution, pricing, external factors |

| Demand Forecasting | Import substitution, past trends, end-use analysis, regression, export markets |

| Financial Appraisal | Project cost, execution timelines, profitability, break-even, DSCR |

| Environmental Appraisal | Water, Air, Land, Sound, Conservation, Geography; pollution clearances |

| Term Loan NOT Focus | Historical performance / historical loan amounts |

| Term Loan Focus | Future trends, technical feasibility, financial feasibility |

| Existing Concern Analysis | Last 3 years audited BS and P&L |

| Sources of Finance | Share capital, term loans, DFIs, incentives (seed capital, subsidies), misc (unsecured, deposits, leasing) |

| Capacity Utilization | Often 60–75% in Year 1, stabilizing by Year 3 |

| Project Lifespan | Shortest of: physical, technological, or market life; industrial = 12 years |

| NOT Lifespan Basis | Rate of depreciation in books |

| DSCR Formula | (Net Profit + Depreciation + Interest on TL) / (TL Instalment + Interest on TL) |

| DSCR Benchmark | Above 1.5 = comfortable debt servicing |

| DSCR Measures | Company's capability to manage term liabilities |

| DSCR NOT For | Measuring project profitability |

| Sensitivity Analysis | Tests financial viability under adverse situations; adjust parameters by ±10% |

| Break-even Point | No-profit-no-loss level; Fixed Cost / Contribution per unit |

| Break-even Focus | No-profit-no-loss point |

| Capital Budgeting Tools | Pay Back Period, ARR, NPV, IRR, BCR |

| Pay Back Period | Time to recover initial investment; shorter = better |

| PBP Drawback | Ignores returns after recovery; ignores time value of money |

| ARR | Average annual profit / total initial investment × 100 |

| ARR Drawback | Overlooks time value of money |

| ARR NOT a Measure | Average Rate of Depreciation |

| Compounding | Today's value → future value |

| Discounting | Future value → today's value |

| NPV | Sum of present values of all cash flows (payins +ve, payouts -ve) |

| NPV Discount Rate | Pre-determined cut-off rate (≥ cost of funds) |

| NPV > 0 | Project can be accepted |

| NPV < 0 | Project earnings < cost of capital |

| Present Value Index | PV of inflows / PV of outflows; evaluates financial health |

| IRR | Discount rate where NPV = 0 |

| IRR Full Form | Internal Rate of Return |

| IRR > Cost of Capital | Accept investment |

| IRR < Cost of Capital | Reject |

| IRR Determines | If cost of funds < IRR → project viable |

| Margin of Safety | IRR minus cost of funds |

| IRR NOT For | Comparing different projects |

| IRR Critical For | Determining financial feasibility |

| BCR > 1 | Accept (benefits outweigh costs) |

| BCR = 1 | Indifferent |

| BCR < 1 | Reject |

| Cash Inflow Includes | Operating profits, residual value, profit after tax |

| Cash Inflow EXCLUDES | Initial investment cost |

| Cash Outflow Includes | Working capital, fixed assets, fixed asset additions |

| Cash Outflow EXCLUDES | Profit from operations |

| Residual Value | Added to cash inflow of last year of project life |

| Land | Does NOT undergo depreciation |

| Depreciation | Remains within unit; no cash flow involved |

| Equity Holder IRR | Consider benefits after deduction of tax |

| Powerful Tools | NPV and IRR for financial viability |

| Net Receipt | Difference between cash inflow and outflow |

Lesson Doubts

Ask questions, get expert answers