⚠️ Non-Financial Risk Analysis & Macroeconomic Factors

Complete guide to Non-Financial Risk (NFR) — classification, management framework, three circles of defense, facilitating factors, macroeconomic linkages, and loss estimation approaches for banking exams.

Introduction

Non-Financial Risk (NFR) refers to risks that are not directly financial in nature but affect the bank's operations — such as operational risks, cyber risks, and compliance risks.

- Complex modern financial systems rely on technology infrastructure and digital platforms, making NFR increasingly critical.

- NFR encompasses non-traditional financial risks like market, credit, and liquidity risk — which can still significantly impact a bank's operations and reputation.

- NFR can have significant negative implications for a bank's strategy, business operations, economics, and reputation.

Key Facts

- NFR (Non-Financial Risk) encompasses risks not included in traditional categories like operational risk.

- NFR, previously called "unidentified risk", has now been recognised as significant due to its direct impact on banks.

- While Basel considers NFR as part of the self-governing business model, they do not mandate specific frameworks.

- All Operational Risk falls under the category of Financial Risk, but not all Non-Financial Risk is Operational Risk.

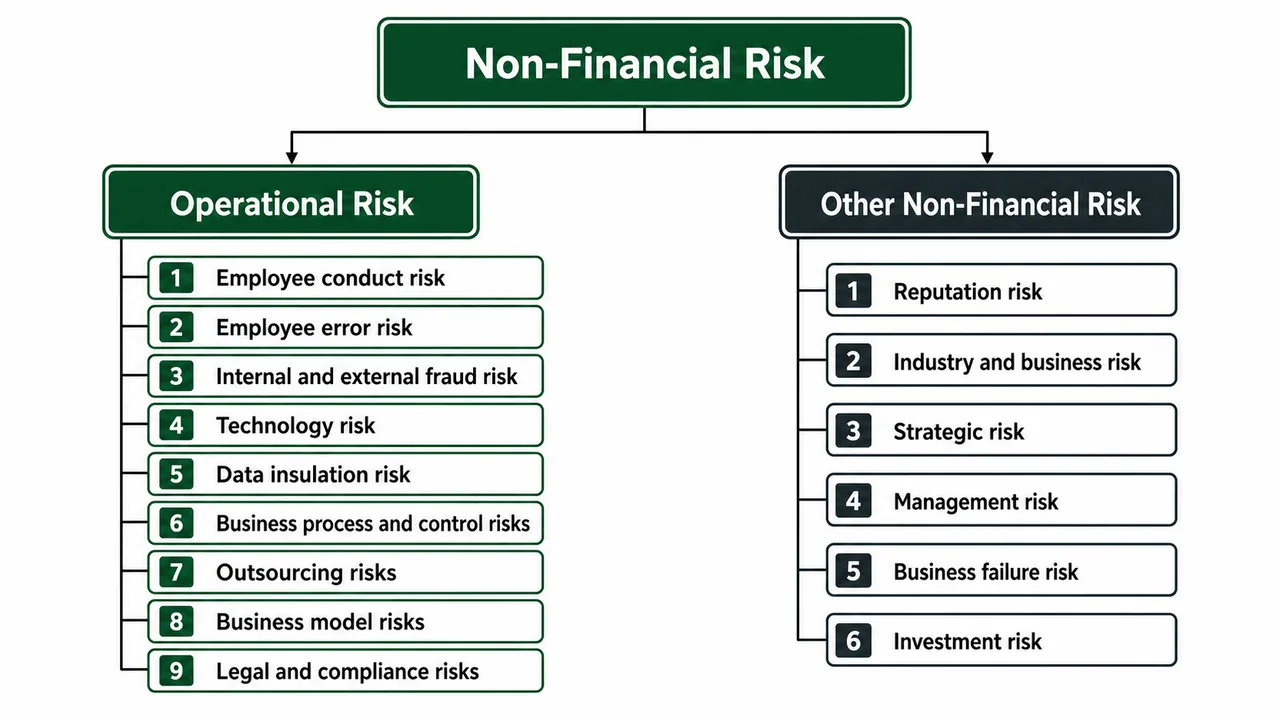

Classification of Non-Financial Risk

NFR is broadly classified into two categories:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Introduction

Non-Financial Risk (NFR) refers to risks that are not directly financial in nature but affect the bank's operations — such as operational risks, cyber risks, and compliance risks.

- Complex modern financial systems rely on technology infrastructure and digital platforms, making NFR increasingly critical.

- NFR encompasses non-traditional financial risks like market, credit, and liquidity risk — which can still significantly impact a bank's operations and reputation.

- NFR can have significant negative implications for a bank's strategy, business operations, economics, and reputation.

Key Facts

- NFR (Non-Financial Risk) encompasses risks not included in traditional categories like operational risk.

- NFR, previously called "unidentified risk", has now been recognised as significant due to its direct impact on banks.

- While Basel considers NFR as part of the self-governing business model, they do not mandate specific frameworks.

- All Operational Risk falls under the category of Financial Risk, but not all Non-Financial Risk is Operational Risk.

Classification of Non-Financial Risk

NFR is broadly classified into two categories:

1. Operational Risk

| Sub-type | Description |

|---|---|

| Employee Conduct Risk | Inappropriate behaviour or misconduct |

| Employee Error Risk | Mistakes due to lack of training or negligence |

| Internal & External Fraud Risk | Deliberate deception from inside or outside |

| Technology Risk | System failures, cyber threats |

| Data Insulation Risk | Data breaches, privacy violations |

| Business Process & Control Risks | Weak internal processes |

| Outsourcing Risks | Third-party service failures |

| Business Model Risks | Flawed business strategy |

| Legal & Compliance Risks | Regulatory non-compliance |

2. Other Non-Financial Risk

| Sub-type | Description |

|---|---|

| Reputation Risk | Damage to public image |

| Industry & Business Risk | Sector-wide challenges |

| Strategic Risk | Poor strategic decisions |

| Management Risk | Leadership failures |

| Business Failure Risk | Complete operational breakdown |

| Investment Risk | Non-financial investment losses |

Characteristics of NFR Management

Management of Non-Financial Risks should align with three main factors:

- Customer Expectations

- Regulatory Objectives

- Shareholder Interests

Ignoring any of these factors in NFR management renders the approach ineffective.

Important Characteristics

- Financial risks and Non-Financial Risks are interconnected — one can lead to the other.

- NFRs often result in reputational damage to banks, which can vary in intensity but is never absent.

- Negative incidents related to NFR can diminish regulator trust and employee morale.

- Reputational damage affects customer and shareholder confidence and may result in personal repercussions for employees due to accountability investigations.

- Banks face significant internal and regulatory pressure to continuously improve NFR management.

Mitigating Non-Financial Risk

Objectives of a Robust NFR Management System

- Eradication of malfunction and prevention of attendant risks

- Fulfilling the responsibilities to the stakeholders

- Curbing expenditures

Essential Elements of a Comprehensive NFR Management Approach

- A harmonized structure

- A collection of facilitating factors

- A paradigm shift in the outlook of operating staff

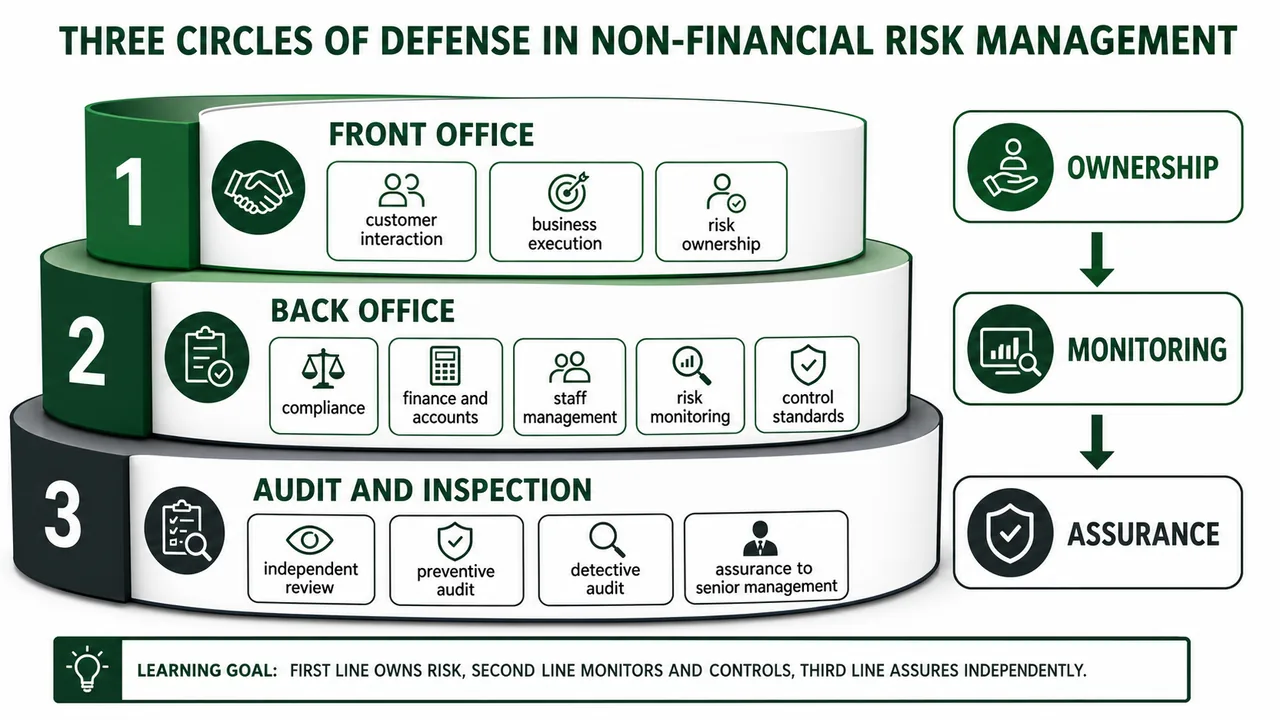

Three Circles of Defense

Global banks are developing a Non-Financial Risk management model with three protective layers:

First Circle (Front Office)

- Comprises the front office which directly manages risks and interacts with customers.

- This circle bears the primary responsibility for preventing NFR while also achieving business and profit targets.

Second Circle (Back Office)

- Encompasses back-office functions like staff management, finance, accounts, compliance, and risk.

- This layer ensures that control standards are met and synchronises with the first circle to prevent NFRs.

Third Circle (Audit & Inspection)

- Conducts checks on the adequacy of the first two circles.

- Focuses on both preventive and detective audit functions to ensure thorough risk mitigation.

Each function independently acts as a consolidated measure for risk mitigation. The first line takes ownership, the second line monitors, and the third line provides independent assurance.

Key Principles

- The back-office function (second circle) is responsible for right-sizing requirements and agile-yet-tight monitoring.

- Bank audit should proactively identify potential NFR risks and aid senior management in prevention efforts.

- Achieving harmony across the three layers of NFR management is crucial for effective risk mitigation.

Facilitating Factors

A. Uniform Understanding of NFR Policy

- Ensure that every member across all levels comprehends the NFR policy uniformly.

- Avoid misinterpretation and inconsistent risk mitigation efforts.

- Maintain a consistent risk taxonomy across the organisation.

B. Preventive Measures in Risk Management

- Develop robust mechanisms and alert systems to notify all levels of any policy breaches or risks.

- Employ tools like auto-verification of KYC data against government databases and security/mobile access gate-locking.

- Identify vulnerable points in products, processes, or personnel, and install circuit breakers preventing any critical areas while utilising built-in error sensors for simpler processes.

C. Strategic Surveillance and Controls

- Conduct thorough evaluations of business processes to determine where advanced surveillance systems are necessary.

- Build automated surveillance tracking for measurable, milestone-based achievements that require milestone achievements which are not automatically verifiable.

D. Comprehensive Analysis of NFR Management Competence

- Develop a uniform culture with standardised risk practices ensuring the company's mission, vision, and values uniformity across all units and locations.

- Ensure a unified approach to payouts and penalties across all staffing levels.

- Incorporating specialised lateral positions only when necessary.

- Ensure each person in risk management at all levels of the organisation is equally accountable for all three circles, enhancing both prevention and detection of NFRs.

E. Paradigm Shift in the Outlook of Operating Staff and their Culture

- Strong risk management demands a robust cultural support, emphasising the importance of mission, vision, and values.

- Job rotations present shared knowledge and spread a comprehensive risk management mindset.

- Partnership from legal and risk management is vital in modelling and presenting NFR awareness, fostering a top-down approach.

Additional Factors

- Middle management often faces negative perceptions as barriers rather than facilitators, changing this outlook is vital.

- Job rotations present shared knowledge and expose staff to various functions, which helps in spreading a comprehensive risk management mindset.

- Mandatory operational roles and geographic relocations should be enforced periodically to prevent complacency and unset roles.

- Enforcing compliance lessons without direct bank access can deter malpractice and promote a culture of risk awareness.

Impact of Macroeconomic Factors on NFR

Key Linkages

- NFR (Non-Financial Risk) events like frauds and errors are more likely and severe during economic downturns, with a noticeable lag between economic decline and detection of NFR incidents.

- Banks tend to ease restrictions during economic booms, which may lead to inadequate systems that fail to prevent NFR events when the economy worsens.

- Historical data shows that banks experienced a spike in frauds following the 2008 financial crisis.

Varying Degrees of Macroeconomic Dependence

| NFR Type | Macroeconomic Correlation |

|---|---|

| Internal and external fraud | Often correlate with economic conditions |

| Client, product, and business practice issues | May relate to macroeconomic circumstances |

| Execution, delivery, and process management | May be influenced by economic conditions |

| Employment practices and workplace safety | Generally show limited dependence |

| Damage to physical assets and business disruptions | Usually do not relate to economic dynamics |

Important Observations

- Banking and risk professionals continuously work to define the connections between NFR events and macroeconomic factors, often focusing on events with proven economic links.

- Developing a strong risk culture is essential for managing NFR across economic cycles.

- Detailed analysis of past NFR events can help identify economic triggers, aiding in classification and preventive measures for future incidents.

- Economic booms can lead to less lending scrutiny and internal fraud as optimism prevails, partly because external auditors and the regulator fail to keep up with risks.

- Frauds often go undetected during prosperous times as long as financial obligations are met, and surface only when conditions worsen and the regulator fails to keep up with fraud.

- Rising unemployment during economic downturns can prompt individuals to commit fraud in an effort to maintain their standard of living or out of desperation when prospects are low.

- Economic upturns result in high credit demand, placing immense pressure on credit processing and delivery, which can inadvertently increase NFR.

Common NFR Loss Estimation Approaches

1. Regression Models

- Banks typically estimate their NFR losses using regression models alone or in combination with other methods.

- These regression models typically calculate two main variables: the expected frequency and the expected severity of NFR losses using macro-economic and bank-specific variables.

- For banks that detected a strong link between macroeconomic factors and NFR losses, regression models may suffice for estimating these parameters in terms of frequency or total losses, with adjustments for macroeconomic variables and bank-specific factors.

- Where regression models applied, NFR losses are typically fitted using log-normal distribution or similar distributions, as suboptimal decisions are often skewed toward extreme outcomes rather than statistical outliers.

- A significant number of banks have not found a substantial correlation between macroeconomic conditions and the severity of NFR losses.

- Often regression models are used primarily for estimating loss frequency, especially referencing the most recent financial crisis.

2. Modified Loss Distribution Approach (LDA)

- Banks utilising the Advanced Measurement Approach (AMA) often employ the Loss Distribution Approach (LDA) for modelling annual NFR loss Value-at-Risk (VaR).

- LDA estimates the probability distributions for both the frequency and severity of NFR losses within specific units, such as business lines or event types.

- These distributions of frequency and severity are integrated, typically through a Monte Carlo simulation, to predict the annual probability distribution of NFR losses for each measurement unit.

3. Scenario Analysis

- Involves gathering insights from business managers and risk experts to evaluate the potential impact of severe but plausible NFR events.

- Banks use this analysis to add a management overlay to model-based loss estimations, accommodating unique risks or unprecedented loss scenarios.

- Helps to supplement historical data and standard models, allowing banks to address a broader spectrum of risks.

- Frequency–severity grids paired with expert-supplied scenarios provide a structured approach for quantifying risk.

4. Historical Averages

- Banks sometimes utilise historical averages alongside other methodologies to estimate NFR losses in stress scenarios.

- Historical averages are primarily used for estimating losses from event types with limited data or those that don't correlate strongly with macroeconomic factors — regression models are applied when such correlations exist.

- Key risks: using only recent data or assuming a business-as-usual outlook, which may produce skewed loss estimates, though this approach can be limited as it is retrospective and may overlook unprecedented risks.

- Banks should critically assess factors like sample size, select and justify the time periods and thresholds used, make necessary adjustments, and explain the use of simple averages over alternatives like estimates, single worst, or expected outcomes in stress scenarios.

5. Legal Exposures

- Legal exposure is a major component of NFR losses for many banks, leading them to analyse and forecast legal losses distinctly from non-legal NFR losses.

- Banks are encouraged to include all legal reserves and settled legal issues in their comprehensive NFR loss estimations.

- Approaches include add-on provisions for significant events, leveraging legal reserves, or utilising separate analytical models for specific event types like client, product, and business practices.

- For litigation losses related to reputational and securities law in lending, some banks use portfolio-level analysis with historical performance data to calculate default and repurchase claim rates.

Dealing with Recoveries

- Banks typically expect recoveries through the allowed insurance claims within a predefined period usually from one to three years.

- The net financial damage after accounting for these expected recoveries constitutes the NFR projection base.

- It is crucial that the NFR projection still factors in additional regulatory capital reserves.

- A detailed evaluation of the likelihood and timing of claims, especially under deteriorating economic conditions, is necessary to ensure recovery expectations are realistic.

Quick Notes for Exam

- NFR stands for Non-Financial Risk — risks not directly financial but affecting bank operations (operational, cyber, compliance risks).

- Technology risk is an example of NFR — includes cyber security threats and system failures. Credit risk and market risk are NOT NFR.

- Scenario analysis in NFR is used to assess the impact of potential severe NFR events — NOT to predict exact future profits.

- Customer expectations is a key factor for managing NFR (along with regulatory objectives and shareholder interests).

- The First Circle deals with customer interactions and manages direct risks (front office).

- The Second Circle focuses on back-office functions and maintaining control standards.

- Regression models help banks estimate NFR losses under stress scenarios using historical data.

- A common challenge in NFR management is integrating business growth with regulatory compliance.

- Preventive measures mitigate risks before they materialise — this is why they are important in NFR management.

- Reputational damage from NFR affects customer and shareholder confidence.

- Implementing awareness programs in banks primarily aims to reinforce the bank's values.

- Job rotations spread a comprehensive risk management mindset and prevent knowledge silos.

- Economic downturns make NFR events like frauds and errors more likely and more severe.

- Modified LDA uses Monte Carlo simulation for estimating NFR loss distributions.

- Scenario analysis in NFR management assesses potential severity of NFR events and helps incorporate unique risks.

- Banks estimate NFR losses under stress using historical loss data combined with management insights.

- Banks apply historical averages when no substantial correlation with macroeconomic conditions is detected.

- Operational risk is often analysed separately due to its significant impact on banks.

- During economic upturns, banks may ease restrictions, leading to inadequate systems for preventing NFR events when economy worsens.

- Detailed analysis of past NFR events helps banks identify economic triggers and improve preventive measures.

Cheat Sheet

| # | Topic | Key Point |

|---|---|---|

| 1 | NFR Full Form | Non-Financial Risk |

| 2 | NFR Nature | Risks not directly financial but affecting operations |

| 3 | NFR Examples | Operational risk, cyber risk, compliance risk |

| 4 | NOT NFR | Credit risk, market risk, interest rate risk |

| 5 | Operational Risk Types | Employee conduct, error, fraud, technology, data insulation, business process, outsourcing, business model, legal/compliance |

| 6 | Other NFR Types | Reputation, industry/business, strategic, management, business failure, investment |

| 7 | NFR Management Factors | Customer expectations, regulatory objectives, shareholder interests |

| 8 | NFR & Financial Risk | Interconnected — one can lead to the other |

| 9 | Reputational Damage | Always present in NFR incidents, varies in intensity |

| 10 | NFR Objectives | Eradication of malfunction, fulfilling responsibilities, curbing expenditures |

| 11 | Essential Elements | Harmonized structure, facilitating factors, paradigm shift |

| 12 | First Circle | Front office — customer interactions, primary NFR responsibility |

| 13 | Second Circle | Back office — control standards, staff management, compliance |

| 14 | Third Circle | Audit & inspection — preventive and detective audit |

| 15 | Three Circles Purpose | Harmony across all three layers is crucial |

| 16 | Facilitating Factor A | Uniform understanding of NFR policy |

| 17 | Facilitating Factor B | Preventive measures — alert systems, KYC auto-verification |

| 18 | Facilitating Factor C | Strategic surveillance and controls |

| 19 | Facilitating Factor D | Comprehensive analysis of NFR competence |

| 20 | Facilitating Factor E | Paradigm shift in staff outlook and culture |

| 21 | Job Rotations | Spread risk management mindset, prevent knowledge silos |

| 22 | Geographic Relocations | Enforced periodically to prevent complacency |

| 23 | Macro-NFR Link | Frauds and errors more likely in economic downturns |

| 24 | 2008 Crisis Impact | Spike in frauds following the financial crisis |

| 25 | Economic Booms Risk | Banks ease restrictions → inadequate systems |

| 26 | Fraud Detection Gap | Frauds go undetected during prosperous times |

| 27 | Unemployment Effect | Drives individuals to commit fraud |

| 28 | Credit Demand in Upturns | High pressure on processing increases NFR |

| 29 | Internal/External Fraud | Correlates with economic conditions |

| 30 | Employment Practices NFR | Limited dependence on macroeconomic factors |

| 31 | Physical Asset Damage | Usually NOT related to economic dynamics |

| 32 | Estimation: Regression | Two variables — expected frequency and expected severity |

| 33 | Regression Distribution | Log-normal distribution typically used |

| 34 | Loss Frequency | Regression models used primarily for this |

| 35 | Modified LDA | Uses Loss Distribution Approach for annual VaR |

| 36 | LDA Simulation | Monte Carlo simulation to predict annual NFR loss |

| 37 | Scenario Analysis | Expert insights on severe but plausible events |

| 38 | Frequency–Severity Grids | Paired with expert scenarios for quantifying risk |

| 39 | Historical Averages | Used when limited data or weak macro correlation |

| 40 | Historical Average Risk | Retrospective, may overlook unprecedented risks |

| 41 | Legal Exposures | Major NFR component, analysed distinctly |

| 42 | Recovery Period | Typically 1–3 years for insurance claims |

| 43 | Net Financial Damage | After accounting for expected recoveries |

| 44 | Capital Reserves | NFR projection must still factor in regulatory capital |

| 45 | Basel & NFR | Does not mandate specific NFR frameworks |

| 46 | All OpRisk is Financial | But not all NFR is Operational Risk |

| 47 | Risk Culture | Essential for managing NFR across economic cycles |

| 48 | Awareness Programs | Aim to reinforce the bank's values |

Lesson Doubts

Ask questions, get expert answers