📊 Asset Classification

RBI asset classification ladder, SMA buckets, provisioning norms, PCR, MSME revival timelines, and the RBI 2026 ECL transition.

Asset Classification

Overview

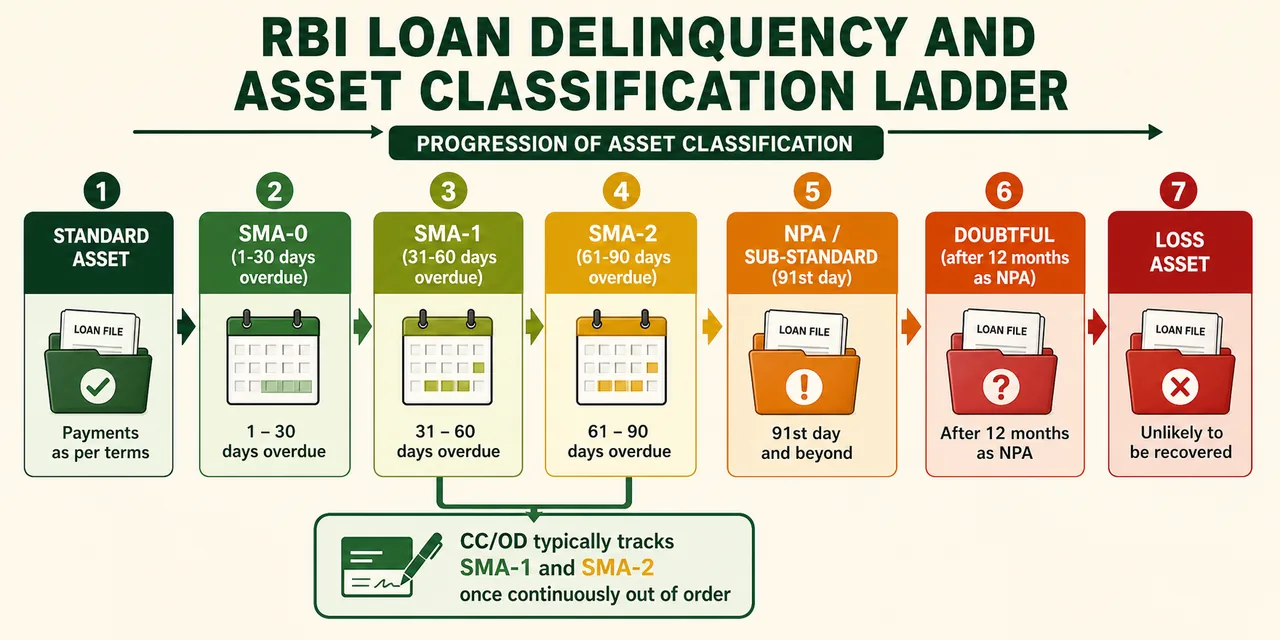

Every loan a bank gives out starts as a Standard Asset — a performing loan that is expected to be repaid on time. But borrowers sometimes miss payments, face financial stress, or default entirely. The moment that happens, the bank needs a structured, objective way to:

- Detect stress early — before a loan becomes a full NPA (Special Mention Account system)

- Classify the damage — how bad is it? Sub-standard? Doubtful? Total loss?

- Provide for it — set aside profit as a buffer (provisioning)

- This entire system is governed by the RBI's Master Circular on Prudential norms on Income Recognition, Asset Classification and Provisioning pertaining to Advances (commonly known as IRAC norms).[2]

- The two key ideas behind the whole system:

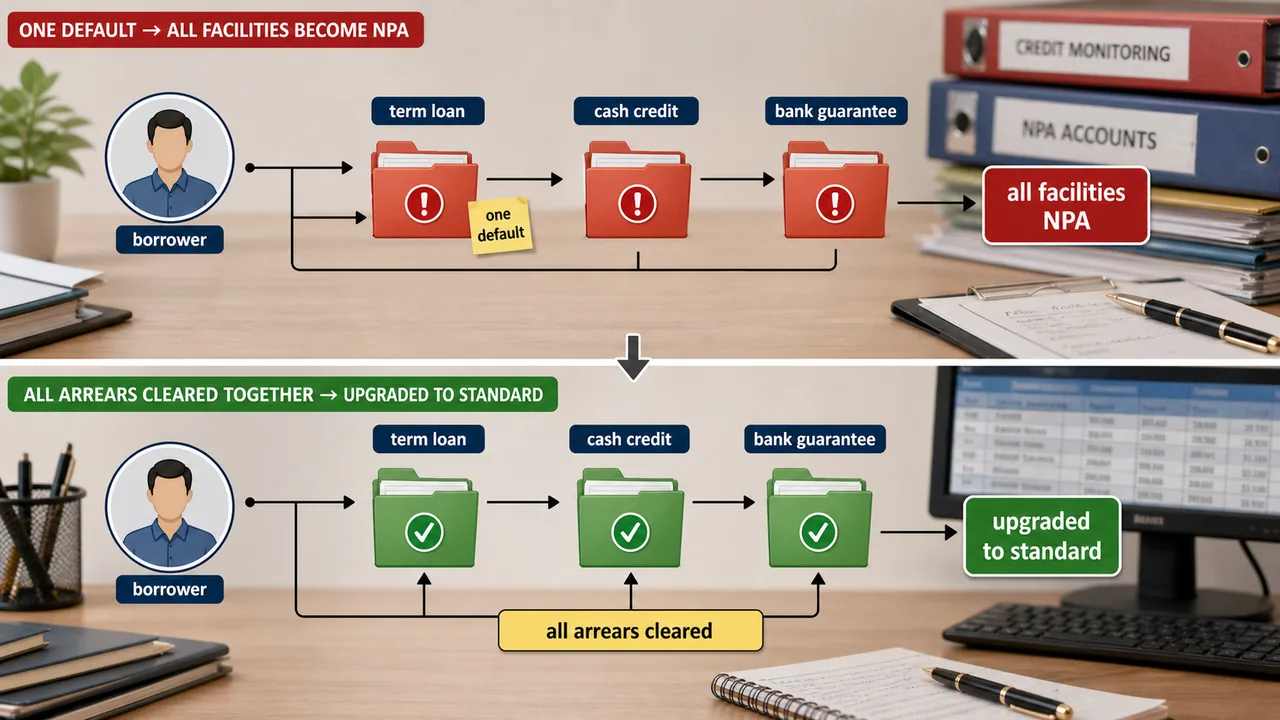

- Borrower-level classification: If one loan account of a borrower goes NPA, all facilities to that borrower are classified NPA. The bank looks at the borrower, not just the facility.

- Objective trigger: Classification is based on days of default — not on management judgment. This prevents banks from hiding bad loans.

Classification Hierarchy

Bank assets are classified into 4 categories, while NPAs specifically falls into 3 categories:

Interactive Preview

Try the embedded exercise below. Full lesson access still requires Pro.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Asset Classification

Overview

Every loan a bank gives out starts as a Standard Asset — a performing loan that is expected to be repaid on time. But borrowers sometimes miss payments, face financial stress, or default entirely. The moment that happens, the bank needs a structured, objective way to:

- Detect stress early — before a loan becomes a full NPA (Special Mention Account system)

- Classify the damage — how bad is it? Sub-standard? Doubtful? Total loss?

- Provide for it — set aside profit as a buffer (provisioning)

- This entire system is governed by the RBI's Master Circular on Prudential norms on Income Recognition, Asset Classification and Provisioning pertaining to Advances (commonly known as IRAC norms).[2]

- The two key ideas behind the whole system:

- Borrower-level classification: If one loan account of a borrower goes NPA, all facilities to that borrower are classified NPA. The bank looks at the borrower, not just the facility.

- Objective trigger: Classification is based on days of default — not on management judgment. This prevents banks from hiding bad loans.

Classification Hierarchy

Bank assets are classified into 4 categories, while NPAs specifically falls into 3 categories:

- Standard Assets (Performing)

- Sub-standard Assets (NPA)

- Doubtful Assets (NPA)

- Loss Assets (NPA)

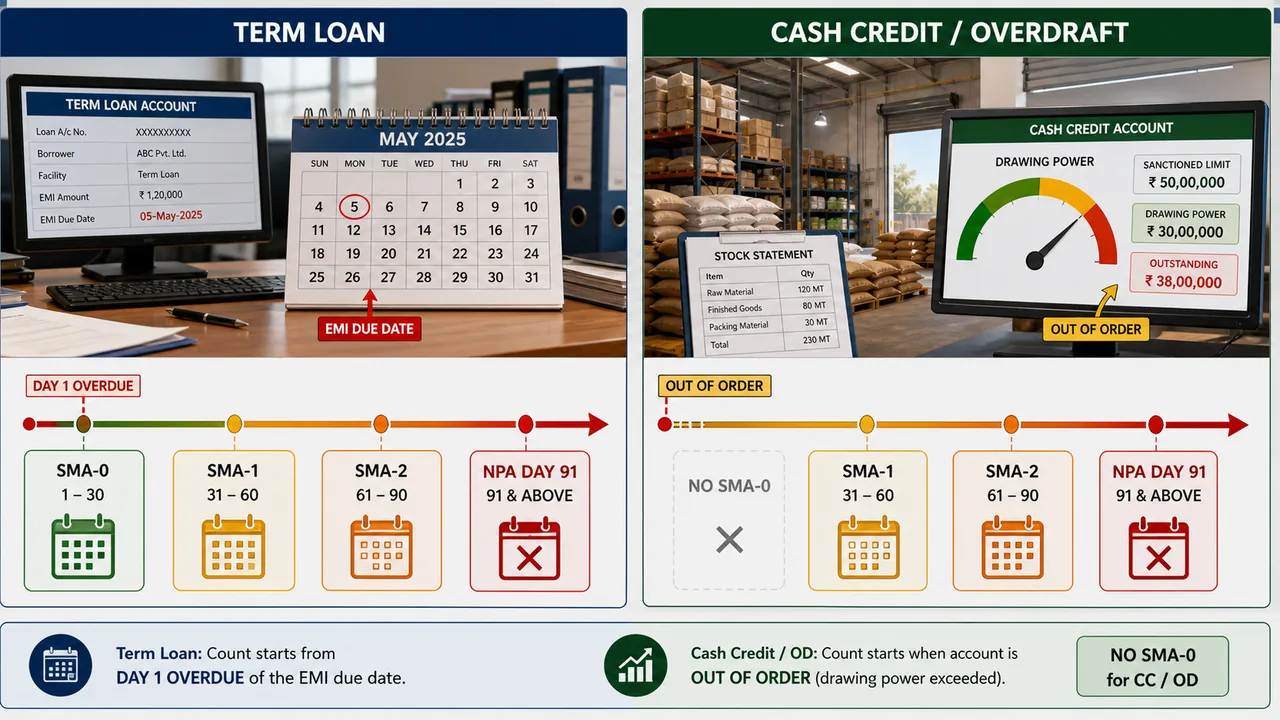

Standard Assets & SMA

Assets carrying normal credit risk where all conditions of sanction are met. If accounts become irregular, they are tracked as Special Mention Accounts (SMA):

- SMA-0: Overdue for 1-30 days

- SMA-1: Overdue for 31-60 days

- SMA-2: Overdue for 61-90 days

Note on Revolving Loans (CC/OD):

- Cash Credit and Overdraft accounts do not have an SMA-0 tier. They are only classified as SMA-1 (31-60 days) and SMA-2 (61-90 days) if their outstanding balance is continuously beyond the sanctioned limit or drawing power.

- A Term Loan has a fixed repayment schedule: EMI on the 5th of every month. The day the 5th passes without payment, the account is "overdue" — Day 1 of default. SMA-0 kicks in from Day 1.

- A Cash Credit / Overdraft works completely differently. There is no EMI. The borrower draws funds and repays freely within the sanctioned limit. The limit is the ceiling; the account fluctuates constantly. Going slightly over the limit on a given day is operationally normal — the borrower may credit funds tomorrow.

- The stress signal for CC/OD is not a missed payment date. It is when the outstanding balance stays continuously above the sanctioned limit or Drawing Power (DP) — meaning the borrower cannot bring the account back within bounds even over time.

- Drawing Power (DP) is the actual limit available to the borrower on any given day, calculated from the value of stock and debtors pledged as security. If the stock value drops, DP drops — and if outstanding exceeds DP, the account is "out of order" even without new drawings.

- Because a 1-30 day breach is too common and not yet a reliable distress signal for revolving facilities, RBI deliberately skips SMA-0 for CC/OD. Stress is only flagged when the breach persists for 31+ days continuously (SMA-1).

Example: The due date for one account is 31.03.2026 on the day end:

| Date | Status | Logical Breakdown |

|---|---|---|

| 31.03.2026 | Overdue / SMA-0 | The moment the day-end process completes without payment, the account is 1 day overdue (Day 1 of default). |

| 30.04.2026 | SMA-1 | The account has remained overdue for more than 30 days (Day 31). |

| 30.05.2026 | SMA-2 | The account has remained overdue for more than 60 days (Day 61). |

| 29.06.2026 | NPA | The account has remained overdue for more than 90 days (Day 91). It is now classified as a Sub-standard Asset. |

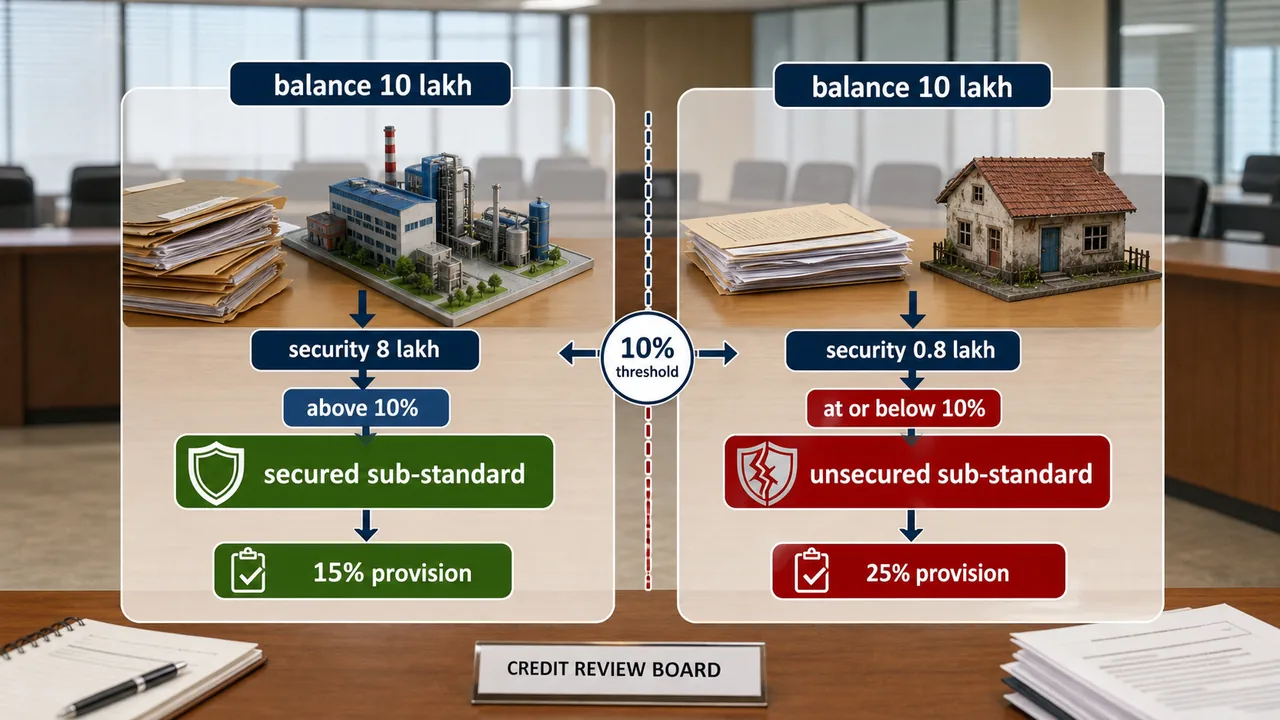

Sub-standard Accounts

- Criteria: Account remains SMA-2 for > 30 days (Total irregularity > 90 days). It becomes Sub-standard on the 91st day.

- Provisioning Categories:

- Unsecured Sub-standard: Security value is ≤ 10% of the outstanding balance.

- Secured Sub-standard: Security value is > 10% of the outstanding balance.

Examples:

| Example | Loan Amount | Security Value (SV) | Classification | Reason |

|---|---|---|---|---|

| 1 | ₹10 Lac | ₹8 Lac (80%) | Secured Sub-standard | SV > 10% |

| 2 | ₹10 Lac | ₹0.8 Lac (8%) | Unsecured Sub-standard | SV ≤ 10% |

Doubtful Loan Accounts

If an account remains Sub-standard for > 12 months, it migrates to Doubtful (DF).

| Category | Description |

|---|---|

| DF-1 | Doubtful up to 1 year |

| DF-2 | Doubtful above 1 year but up to 3 years |

| DF-3 | Doubtful more than 3 years |

Timeline Example:

- Sub-standard Date: 04.04.26

- DF-1 Date: 05.04.27 (1 year later)

- DF-2 Date: 05.04.28 (2 years later)

- DF-3 Date: 05.04.30 (4 years later)

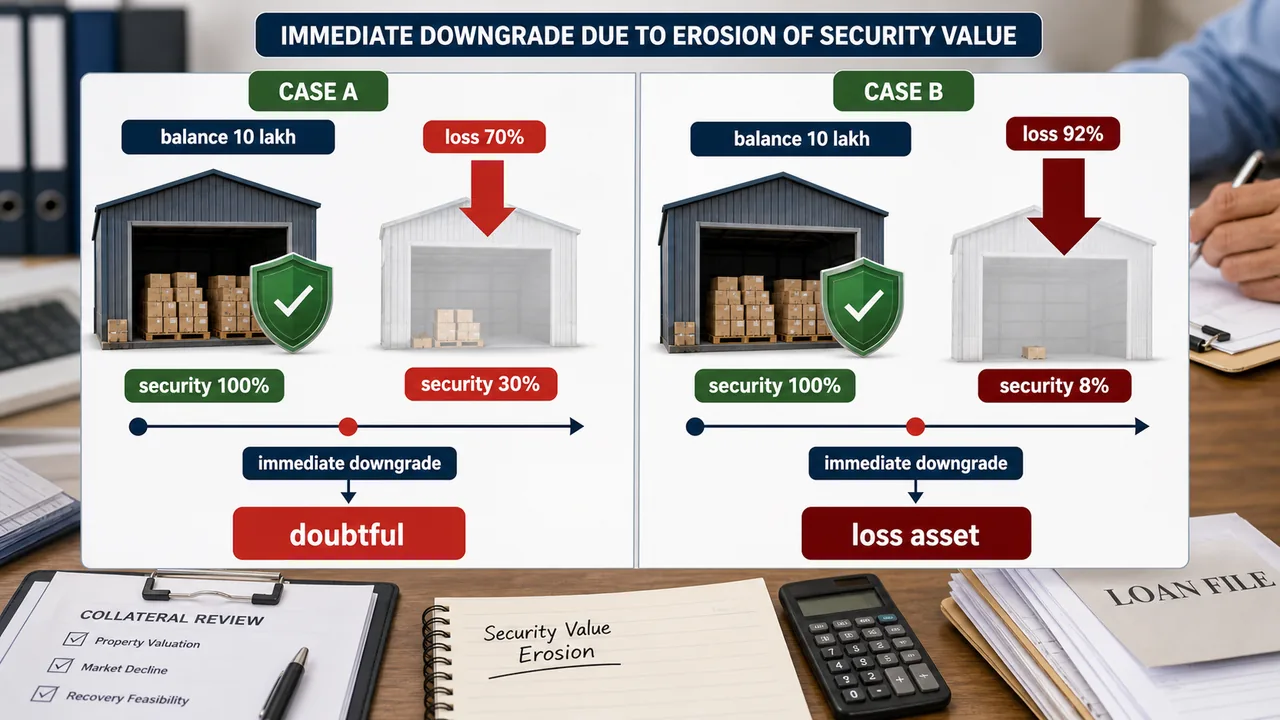

Loss Accounts due to Erosion of Security

In fully secured accounts, if security value erodes significantly, the account can be downgraded immediately without waiting periods.

- Downgrade to Doubtful (DF): If loss is 50% or more (Secured balance < 50%).

- Downgrade to Loss: If loss is 90% or more (Secured balance < 10%).

Example: Two loans (A & B) initially fully secured with Balance ₹10 Lac each. Security is damaged.

- Loan-A: Value of security drops to ₹3 Lac (30%). Loss is 70%.

- Result: Classified as Doubtful (DF) immediately.

- Loan-B: Value of security drops to ₹80,000 (8%). Loss is 92%.

- Result: Classified as Loss Asset immediately.

Stock Statement & Renewal Rules

- Stock Statement Age Limit & NPA Trigger: Stock statements should not be older than 3 months to determine Drawing Power (DP). If the DP is calculated based on statements older than 3 months, the outstanding amount is treated as irregular immediately. If this irregularity continues for a continuous period of 90 days, the account is classified as NPA (even if the account is otherwise in order).[1]

- Non-submission Limit: If stock statements are not submitted at all for a continuous period of 6 months, the account is classified as NPA.[2]

- Renewal Rule: An account where regular/ad hoc credit limits have not been reviewed/renewed within 180 days from the due date/date of ad hoc sanction will be treated as NPA.[2]

Stock Audit Rules

For large NPA accounts ₹5 Crore and above, internally generated inventory statements can no longer be blindly trusted as fraud risks multiply. Therefore, an Annual Stock Audit by independent external agencies is strictly mandatory to verify the collateral genuinely exists before initiating major recovery actions.[2]

Bill Financing NPA Classification

- Purchased bills: Because the bank buys a bill payable strictly on demand, the asset becomes an NPA if it remains overdue for 90 days directly from the bill's purchase date.[2]

- Discounted bills: Because the bill has a predetermined future maturity (usance) date, the 90-day NPA clock only starts ticking from that future due date rather than the day it was heavily discounted.[2]

Upgradation of NPA Accounts

For an NPA account to be upgraded back to a Standard Asset, strict RBI guidelines apply:

- No Partial Recovery Upgradation: An NPA account cannot be upgraded to Standard merely by making a partial payment. It can only be upgraded upon the absolute full payment of all arrears of interest and principal.[1]

- Multi-Facility Rule (Borrower-Wise Upgradation): Since asset classification is borrower-wise (not facility-wise), if a borrower has multiple credit facilities with a bank and even one of them is classified as an NPA, all facilities must be fully regularized (clearing all arrears of interest and principal across all facilities) before any of the accounts can be upgraded back to Standard. Paying off arrears for only one account while another remains in default will not allow upgradation.[1]

Provisioning

Provisioning is a conservative accounting practice where banks set aside a portion of their profits to cover potential future losses on loans.

- Process: It is created by debiting the Profit & Loss (P&L) account and maintaining a separate fund.

- Basis: The amount to be provisioned depends on the Asset Classification (Standard, Sub-standard, Doubtful, or Loss).

- Standard Accounts: For healthy (standard) accounts, the provision is calculated based on the Global Balance (the total outstanding amount).

Provisioning Rates: Standard Loans

For standard loans, the provision amount is calculated based on the Global Balance (the total outstanding amount). The rates are strictly defined by the RBI:

| Loan Category | Provisioning Rate |

|---|---|

| Micro & Small Enterprises | 0.25% |

| Home Loans (within RBI stipulated LTV) | 0.25% |

| Farm Credit (Direct Agriculture) | 0.25% |

| Other Loans (General / Allied Agriculture like Food Processing) | 0.40% |

| Commercial Real Estate - Residential Housing | 0.75% |

| Commercial Real Estate (CRE) | 1.00% |

| Teaser Home Loans | 2.00% |

Provision for Agriculture Loans

- Direct advances to Agriculture (e.g. crop loan under KCC) and MSME attract 0.25% provisioning.

- However, loans to allied agriculture activities (e.g., food processing units) attract 0.40% provisioning under "Others".

Commercial Real Estate (CRE) Categories

- CRE (1.00%): Lending to builders/developers for commercial projects like shopping malls, office complexes, or industrial parks. These carry higher risk because repayment depends heavily on commercial leasing and volatile real estate cycles.

- CRE - Residential Housing (0.75%): Lending to builders specifically for Residential Housing projects (like apartment complexes or residential townships). Because housing has steady intrinsic demand and lower systemic risk than pure commercial properties, the RBI created this carve-out to encourage housing development with a slightly lower (0.75%) provision burden.

Teaser Rate Housing Loans:

- A Teaser Home Loan is a type of loan product where a bank offers a significantly lower interest rate during the initial years (typically the first 1–3 years) to attract borrowers.

- These loans lure borrowers with artificially low initial rates that aggressively "reset" to much higher standard floating interest rates later.

- Because this jump causes a massive "payment shock" and a high risk of sudden household default, the RBI forces banks to hold a heavily fortified initial provision of 2.00%. This only drops to the normal 0.40% after the borrower proves their resilience by surviving 1 year at the higher reset rate without defaulting.

Definition of Unsecured Exposure

- Unsecured exposure is defined as an exposure where the realisable value of the security, as assessed by the bank/approved valuers/RBI inspecting officers, is not more than 10%, ab-initio, of the outstanding exposure.

- Rights, licenses, and authorisations charged to banks as collateral for project finance are strictly NOT reckoned as tangible security — such advances are forcefully treated as unsecured.

- Exception: Annuities and toll collection rights can legally be counted as tangible security under highly specific conditions.

Provisioning Rates: Sub-standard Loans

An account is sub-standard if it has been an NPA for 12 months.

- Rule: There is no bifurcation of the balance into secured and unsecured portions here. You first determine if the account is "Secured" or "Unsecured" based on the value of the security relative to the debt.

- Guarantee Note: No relaxation is given for DICGC/ECGC/CGTMSE guarantees in this category.

| Category | Provisioning Rate |

|---|---|

| Secured Sub-standard | 15% |

| Unsecured Sub-standard | 25% |

| Unsecured Sub-standard (Infrastructure loans) | 20% |

- Security Includes: Primary and collateral security, and guarantees from ECGC, DICGC, CGTMSE, or the Government.

- Exclusion: The net worth of the borrower or guarantor is not considered security.

- A general provision of 15% on total outstanding should be made without any allowance for ECGC guarantee cover and securities available.

- 'Unsecured exposures' identified as 'substandard' attract additional provision of 10%, i.e., a total of 25% on outstanding balance.

- Infrastructure loan accounts classified as sub-standard attract a concessional provisioning of 20% instead of 25%. This discount is granted because infrastructure projects utilize an escrow mechanism—meaning all project revenues (like toll collections or user fees) are legally routed directly into a bank-controlled escrow account. This gives the bank strict first rights to the cash flow before the borrower can touch it, heavily mitigating the risk of the unsecured exposure.

Examples for Sub-standard Loans

| Scenario | Total Balance | Security Value | Category | Calculation | Provision Amount |

|---|---|---|---|---|---|

| Example 1 | Rs. 10 lac | Rs. 9 lac | Secured (90% covered) | Rs. 1.50 lac | |

| Example 2 | Rs. 10 lac | Rs. 0.9 lac | Unsecured (only 9% covered) | Rs. 2.50 lac |

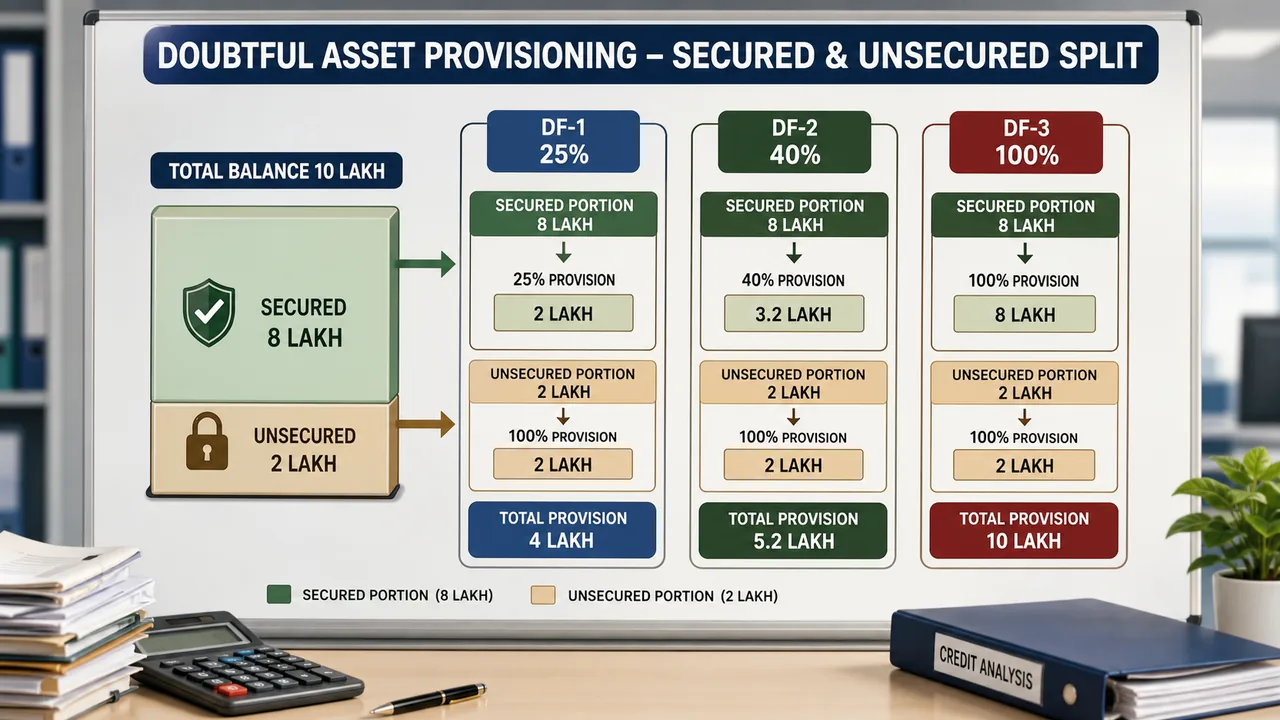

Provisioning Rates: Doubtful Loans (DF)

For Doubtful assets, the balance is bifurcated into a Secured portion and an Unsecured portion.

- Unsecured Portion: Always provided for at 100%.

- Secured Portion: Provisioned based on the age of the NPA:

- DF-1 (Up to 1 year): 25%

- DF-2 (1 to 3 years): 40%

- DF-3 (Above 3 years): 100%

Example for Doubtful Loans

Scenario: Total Balance = 10 lac; Realizable Security Value (RSV) = 8 lac.

| Asset Category | Secured Portion (lac) | Unsecured Portion (lac) | Total Provision |

|---|---|---|---|

| DF-1 | 8 | 2 | Rs. 4.00 lac |

| DF-2 | 8 | 2 | Rs. 5.20 lac |

| DF-3 | 8 | 2 | Rs. 10.00 lac |

Calculation with CGTMSE Guarantee

When a loan is covered by a CGTMSE guarantee, the guaranteed portion requires 0% provision. The calculation follows a specific hierarchy:

- Apply security value first.

- Calculate the "Uncovered Balance."

- Apply the CGTMSE guarantee % to that uncovered balance.

- The remaining "Net Unsecured" portion is provisioned at 100%.

Scenario: Balance = 10 lac; Security = 4 lac; CGTMSE Cover = 80%.

| Component | If DF-1 | If DF-2 | If DF-3 |

|---|---|---|---|

| Total Balance | 10.00 lac | 10.00 lac | 10.00 lac |

| Security (RSV) | 4.00 (Prov @ 25% = 1.00) | 4.00 (Prov @ 40% = 1.60) | 4.00 (Prov @ 100% = 4.00) |

| Uncovered Balance | 6.00 lac | 6.00 lac | 6.00 lac |

| CGTMSE Cover (80% of 6.00) | 4.80 (Prov @ 0% = 0.00) | 4.80 (Prov @ 0% = 0.00) | 4.80 (Prov @ 0% = 0.00) |

| Net Unsecured (6.00 - 4.80) | 1.20 (Prov @ 100% = 1.20) | 1.20 (Prov @ 100% = 1.20) | 1.20 (Prov @ 100% = 1.20) |

| Total Provision | 2.20 lac (1.00 + 1.20) | 2.80 lac (1.60 + 1.20) | 5.20 lac (4.00 + 1.20) |

Comprehensive Provisioning Reference Table

| Asset Classification | Period of NPA | Loan Type | Provisioning % |

|---|---|---|---|

| Standard | Before NPA | SME/Agri | 0.25% |

| Standard | Before NPA | CRE Residential Housing | 0.75% |

| Standard | Before NPA | Commercial Real Estate | 1.00% |

| Standard | Before NPA | Others | 0.40% |

| Substandard | Up to 12 Months of NPA | Secured Loan | 15.00% |

| Substandard | Up to 12 Months of NPA | Unsecured | 25.00% |

| Doubtful 1 | Substandard for 1 Year | Secured Loan | 25.00% |

| Doubtful 1 | Substandard for 1 Year | Unsecured | 100.00% |

| Doubtful 2 | 2nd to 3rd Year (NPA 3rd-4th Year) | Secured Loan | 40.00% |

| Doubtful 2 | 2nd to 3rd Year | Unsecured | 100.00% |

| Doubtful 3 | 4th Year+ (NPA 5th Year) | Secured & Unsecured | 100.00% |

| Loss Assets | From Date of Classification | Secured & Unsecured | 100.00% |

Ratios and Formulas

Key Provisioning & Netting Terms

Before calculating coverage ratios or Net Advances, it is crucial to understand the different components used to buffer against losses. We can divide provisions logically into two phases: Before NPA and After NPA.

1. Provisions BEFORE NPA (Broad Buffers)

These provisions act as a broad buffer for unexpected future losses rather than covering a specific defaulted loan. Because they cover future unknowns, they both qualify as Tier-2 Capital (up to a combined maximum of 1.25% of total Risk-Weighted Assets).

- General Provisions (Mandatory): These are the strict, mandatory provisions the RBI forces banks to make specifically against performing, healthy loans (Standard Assets) based on predefined rates (e.g., 0.25%, 1.00%). They cannot be used to net out specific NPAs or calculate PCR.

- Floating Provisions (Voluntary Extra): Unlike General Provisions (which are tied to healthy loans), Floating Provisions are a completely unattached, voluntary "rainy-day" fund set aside from profits. Because this massive extra buffer isn't tied to any specific loan, the RBI grants banks a special privilege: they can count it towards their 70% Provision Coverage Ratio (PCR) target to show they have enough total cash to cover their bad loans.

2. Provisions AFTER NPA (For Bad Loans)

These provisions are made only after a loan has defaulted and been classified as an NPA.

- Specific Provisions (Mandatory): Provisions made directly against individual, identified bad loans (NPAs like Sub-standard, Doubtful, or Loss assets) based on strict RBI percentages. These are directly subtracted from Gross Advances to calculate Net Advances.

- Note: Specific provisions do NOT qualify as Tier-2 Capital because they represent already identified losses. The bad event has already happened, the borrower has already defaulted, and the bank already knows it is going to lose money on that exact loan.

3. Other Netting Components

- DICGC/ECGC Claims: Claims received from credit guarantee corporations (like DICGC or ECGC) that are kept pending adjustment. Because this money acts as a safety net against the bad loan, it is subtracted when calculating Net Advances.

- Part Payment in Suspense: Sometimes a defaulting borrower pays a partial amount, but the bank cannot immediately figure out how to appropriate it (e.g., towards principal, interest, or penal charges) due to ongoing litigation (especially during ongoing legal settlements or OTS) or technical reasons. This money is temporarily parked in a "Suspense Account". Since the bank actually holds this cash, it is subtracted from Gross Advances when calculating Net Advances.

Provision Coverage Ratio (PCR)

This measures the extent to which a bank has provided against its bad loans.

- The 70% Benchmark: The RBI mandated that the total PCR must not be less than 70%, computed with reference to the gross NPA position as on 30.09.2010. (PCR is calculated using ONLY Specific Provisions and Floating Provisions. General provisions on standard assets are NEVER included in the PCR numerator).

- Countercyclical Buffer: Any surplus provisions that banks had to create to hit this 70% target (over and above the normal prudential requirements) were permanently segregated into a "countercyclical provisioning buffer".

- Buffer Usage: This buffer cannot be used to absorb normal NPA losses. It can only be used during periods of system-wide economic downturn, and strictly with prior approval from the RBI.

Formula:

- Disclosure: Banks must publicly disclose their PCR in the Notes to Accounts section of their Balance Sheet.

Where do Provisions appear on a Bank's Balance Sheet?

A provision is an accounting bookkeeping entry, not a physical stash of cash. When a bank makes a profit, the RBI requires them to "ring-fence" a portion of it to cover potential future loan losses.

- Standard Asset Provisions (Liability Side): For loans that are performing well, the bank debits its Profit & Loss account (reducing reported profit) and credits a Provision Account. Because this money is held as a regulatory buffer and cannot be distributed as dividends, it sits on the Liabilities side under "Other Liabilities and Provisions" (Schedule-5). These standard provisions qualify as Tier-2 Capital for Capital Adequacy Ratio (CAR) purposes.

- NPA Provisions (Asset Side Netting): For bad loans (Sub-standard, Doubtful, Loss), the provisions are used to write down the value of the loan portfolio. The bank reports its Gross Advances, subtracts these NPA specific provisions, and reports the final Net Advances on the Asset side.

Asset Quality Formulas

Gross Advances

The total raw value of all loans given by the bank.

Gross NPA

The total amount of money legally owed by defaulting borrowers.

(Note: This includes the Principal plus any Funded Interest Term Loan linked with the account).

What is a Funded Interest Term Loan (FITL)?

When a borrower cannot pay their interest, the bank may restructure the account by converting the unpaid, accumulated interest into a fresh, separate loan so the main loan balance stops growing. This new loan is the FITL. Because it represents interest that hasn't actually been collected yet from a distressed borrower, its balance must be added to the total Gross NPA.

Net NPA

The actual, unmitigated financial risk or loss the bank is exposed to after accounting for available buffers.

Net Advances

The true active loan portfolio value after removing all buffers set aside for bad loans.

Gross NPA Ratio

This ratio indicates the total proportion of the bank's entire loan portfolio that has turned bad. It is a primary indicator of raw asset quality before any safety buffers are considered.

Net NPA Ratio

This ratio indicates the actual degree of unmitigated risk remaining on the bank's balance sheet. It shows the proportion of bad loans that are not covered by provisions. A high Net NPA ratio implies the bank has insufficient buffers.

References

2 sources • [1] [2]

References

Used for: The primary RBI clarification circular (RBI/2021-2022/125 DOR.STR.REC.68/21.04.048/2021-22) dated November 12, 2021, detailing the day-end process, SMA classification, stock statement irregularities, and borrower-level multi-facility upgradation rules.

Used for: The standard consolidated Master Circular governing the IRAC framework, detailing asset classification categories, stock statement time limits, and provisioning rates for standard, substandard, doubtful, and loss assets.

Summary Cheat Sheet

| Concept | Key Detail |

|---|---|

| Asset Ladder | Standard → SMA-0 / SMA-1 / SMA-2 → Sub-standard → Doubtful → Loss |

| SMA Buckets | 1-30 / 31-60 / 61-90 days overdue |

| Sub-standard | NPA for up to 12 months |

| Doubtful Buckets | DF-1 (up to 1 year), DF-2 (1-3 years), DF-3 (more than 3 years) |

| Loss Asset | Identified as uncollectible or security value effectively below 10% |

| Security Erosion | Loss ≥ 50% → immediate doubtful; loss ≥ 90% → immediate loss asset |

| Stock Statement Rule | CC / OD can become NPA if stock statement is not submitted for more than 6 months |

| Renewal Rule | Credit limit not reviewed / renewed within 180 days can become NPA |

| Standard Provision | 0.25% for MSE / direct agri / eligible housing, 0.40% others, 0.75% CRE-RH, 1.00% CRE, 2.00% teaser loans |

| Sub-standard Provision | 15% secured, 25% unsecured, 20% unsecured infrastructure |

| Doubtful Provision | Secured portion: 25% / 40% / 100% by ageing; unsecured portion: 100% |

| PCR | Provision Coverage Ratio = Total Provisions / Gross NPA, benchmark 70% |

| PCR Surplus | Held in countercyclical buffer (use only in system-wide downturn, with RBI approval) |

| Asset Quality Ratios | Gross Advances = Standard Assets + Gross NPA; Net NPA and Net NPA Ratio are computed after deductions |

Lesson Doubts

Ask questions, get expert answers