📉 Resolution of Stressed Assets — Framework & Process

RBI Directions 2026 — Early Recognition, SMA Classification, ICA, Resolution Process, Post-Resolution Monitoring, Kamath Committee Ratios, and MSME Revival.

Resolution of Stressed Assets — RBI Directions 2019

RBI issued the directions on 7th June, 2019.[1]

Status: Still fully operative for commercial banks (2026). The 2026 IRAC Directions (Lesson 09-05) overhaul provisioning and income recognition norms effective April 1, 2027 — but they do not replace this Resolution Framework. The ICA mechanism, SMA classification, 30-day review period, 180-day implementation clock, and delay penalties continue to govern stressed asset resolution for all scheduled commercial banks. Only NBFCs have received separate amendment directions (2025–26); for commercial banks, this 2019 framework remains the primary operative circular.

Why This Framework Exists

Before 2019, India had a fragmented system — banks could independently choose when to act on stressed loans, and a borrower could play lenders against each other (paying one bank while defaulting on another). Lenders in a consortium often disagreed on whether to restructure or recover, causing years of delay while the asset deteriorated.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Resolution of Stressed Assets — RBI Directions 2019

RBI issued the directions on 7th June, 2019.[1]

Status: Still fully operative for commercial banks (2026). The 2026 IRAC Directions (Lesson 09-05) overhaul provisioning and income recognition norms effective April 1, 2027 — but they do not replace this Resolution Framework. The ICA mechanism, SMA classification, 30-day review period, 180-day implementation clock, and delay penalties continue to govern stressed asset resolution for all scheduled commercial banks. Only NBFCs have received separate amendment directions (2025–26); for commercial banks, this 2019 framework remains the primary operative circular.

Why This Framework Exists

Before 2019, India had a fragmented system — banks could independently choose when to act on stressed loans, and a borrower could play lenders against each other (paying one bank while defaulting on another). Lenders in a consortium often disagreed on whether to restructure or recover, causing years of delay while the asset deteriorated.

RBI's 2019 Prudential Framework replaced all previous restructuring schemes (CDR, S4A, SDR, 5:25) with a single, unified approach built on three pillars:

- Early recognition — detect stress via SMA, report to CRILC so all lenders see the same picture

- Time-bound resolution — 30-day review + 180-day implementation clock. No extensions, no excuses

- Penalty for delay — miss the deadline, bear 20–35% additional provision

Objective

To provide a framework for early recognition, reporting and time-bound resolution of stressed assets.

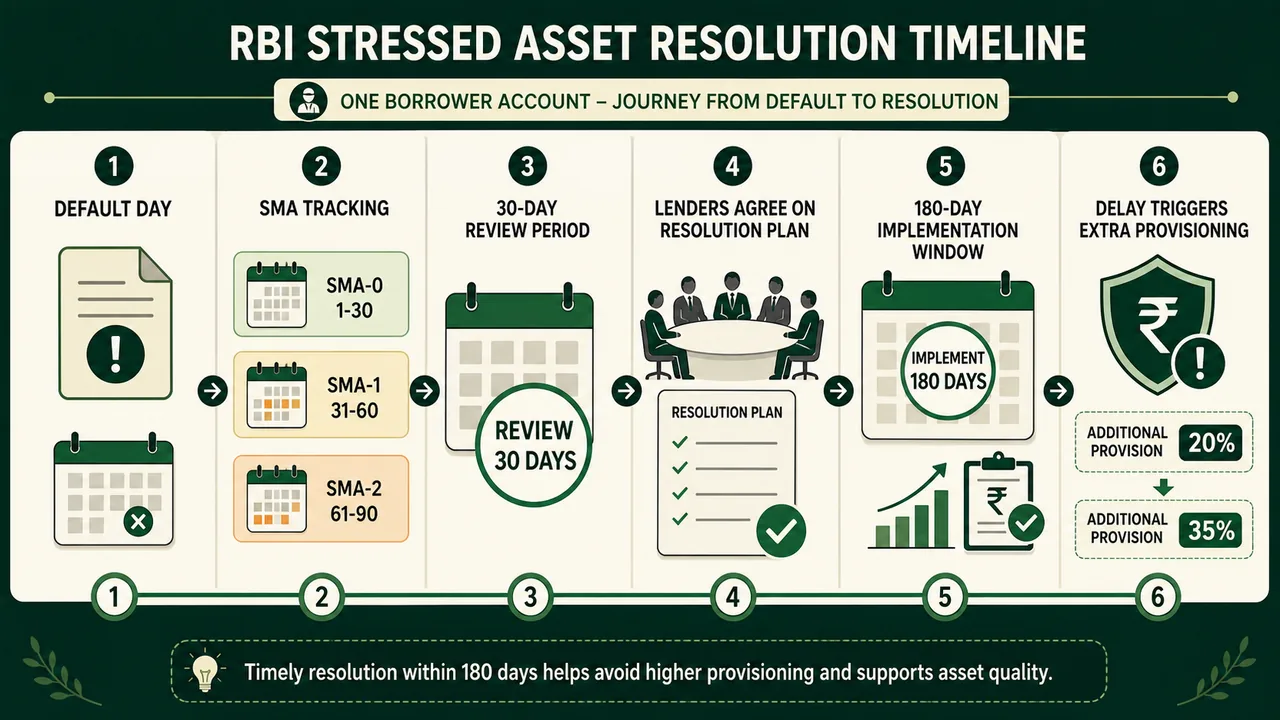

Early Detection — SMA Classification

- Banks must classify accounts as Special Mention Account (SMA) immediately on default. SMA is a pre-NPA early warning system — the account is still standard but is being watched.

- CRILC Reporting: All SMA classifications for borrowers with exposure of ₹5 crore and above must be reported to CRILC (Central Repository of Information on Large Credits) — monthly (CRILC-Main) and weekly on every Friday (Default Report). This ensures every lender in a consortium sees the same stress signal simultaneously.

Key Definitions

Understanding these four terms is critical because they dictate the entire resolution timeline—from the moment a default occurs to the moment the loan is fully rehabilitated.

1. Review Period (The Assessment Phase)

- What it is: A strict 30-day window that starts exactly on the date of default.

- Why it matters: During these 30 days, banks must quickly take a "prima facie" (initial) view of the account. They must decide: Is this borrower's business still viable? Should we restructure the loan, or should we just initiate recovery/insolvency?

- The Rule: The clock starts ticking immediately. Banks cannot sit on a default and pretend they didn't notice. To enforce this, RBI introduced the Reference Date rule (see below).

2. Reference Date (The Unavoidable Starting Gun)

- What it is: An anchor date set by RBI to ensure banks couldn't delay action on massive legacy defaults that were already sitting in the system when the 2019 circular was issued.

- How it was phased:

Loan Size Reference Date ₹2,000 crore and above 07.06.2019 (The exact date the RBI Directions were published) ₹1,500 crore and above 01.01.2020 Below this threshold To be announced separately by RBI - Why it matters: If a ₹2,000 crore loan had defaulted way back in 2018, the bank couldn't claim the 30-day Review Period didn't apply to them. For these legacy accounts, the Review Period officially started on the Reference Date (June 7, 2019). No excuses.

3. Satisfactory Performance (The 10% Trust Marker)

- What it is: When a restructured account successfully repays at least 10% of its outstanding principal and capitalized interest (from the date the Resolution Plan was implemented).

- Why it matters: This is the ultimate "trust marker." Before reaching this 10% threshold, the bank considers the restructuring highly risky. But once the borrower pays back 10%, they prove they are genuinely servicing the new terms. Only at this point can the bank consider upgrading the account from NPA back to a Standard Asset.

4. Specified Period (The 20% Monitoring Window)

- What it is: The time period starting from the implementation of the Resolution Plan and ending only on the exact date the borrower finally clears 20% of the outstanding principal and capitalized interest.

- Why it matters: This is the bank's active "monitoring window." While 10% (Satisfactory Performance) allows for an upgrade, the bank cannot take its eyes off the borrower until the 20% mark is reached. If the borrower defaults again during this Specified Period, they are immediately slapped with a severe penalty (a 15% extra provision for the bank, and an instant downgrade to NPA).

Quick Contrast for Exams:

- 10% = Satisfactory Performance: The minimum threshold required to upgrade the account to a Standard Asset.

- 20% = Specified Period End: The threshold where the intense monitoring window finally closes.

Restructuring — What It Is

Definition

An act where lenders grant concessions to a borrower due to legal or economic reasons — i.e., the borrower cannot meet the original terms, and recovery would destroy more value than a modified repayment plan.

What Restructuring Includes

Modification of terms and conditions of the loan, securities, repayment schedule including interest, rollover of loans, additional funding, or compromise settlement.

Signs of Financial Difficulty

The RBI defines a borrower as being in financial difficulty if any of these apply:

- Default or possibility of default on a material obligation

- Cash inflows insufficient to service all loans

- Loans classified or likely to be declared SMA or NPA

Why this definition matters: Restructuring is only allowed for borrowers in genuine financial difficulty. Restructuring a healthy borrower to avoid classification is prohibited — that would be evergreening (giving new loans to repay old ones, hiding the real NPA).

Who Cannot Be Restructured

- Fraud / Willful Defaulters — not eligible for restructuring under any route.

The Resolution Process — Step by Step

Step 1: Initiation (30-Day Review)

Lenders initiate the Resolution Plan (RP) process by taking a prima facie review of the account within 30 days of default. This review period cannot begin later than the Reference Date.

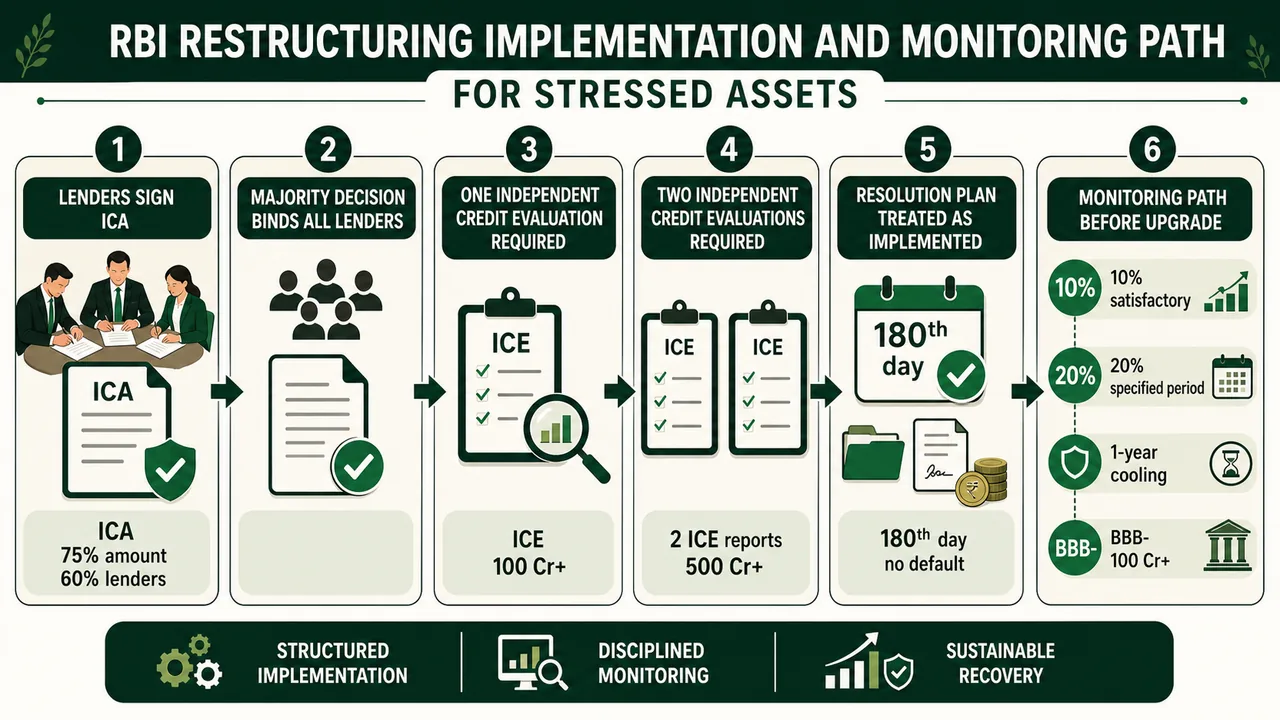

Step 2: Inter-Creditor Agreement (ICA)

Where an RP is to be implemented, all lenders must enter into an ICA. The ICA provides that decisions made by a majority of lenders — 75% by loan amount and 60% by number of lenders — are binding on all lenders, including dissenters.

This solves the old problem: one holdout lender could block resolution indefinitely. Under the ICA, the majority rules.

Step 3: Implementing the Resolution Plan (180-Day Clock)

The RP must be fully implemented within 180 days from the end of the review period. There are no extensions.

Step 4: Independent Credit Evaluation (ICE)

If the RP involves restructuring or change in ownership, an ICE from an RBI-approved Credit Rating Agency (CRA) is required:

- Exposure ₹100 crore and above → 1 ICE required

- Exposure ₹500 crore and above → 2 ICEs required

The CRA rates the resolution plan on a scale of RP1–RP6. The minimum acceptable rating is RP4 — the plan must be assessed as at least minimally viable before lenders can proceed.

| Rating | Viability Assessment |

|---|---|

| RP1 | Highest viability — strong repayment prospects |

| RP2 | Good viability |

| RP3 | Adequate viability |

| RP4 | Minimum acceptable — borderline viable |

| RP5 | Poor — not viable |

| RP6 | Weakest — recovery / IBC is the appropriate route |

"RP4 or better" means the CRA must rate the plan at RP4, RP3, RP2, or RP1 — i.e., borderline viable or better before lenders can proceed.

When is the RP Considered Implemented?

- If the borrower is not in default on the 180th day from the end of the review period; and

- All documentation and/or new capital by new promoter is completed.

Step 5: Penalty for Delay

If lenders fail to implement the RP within 180 days, RBI penalises them by forcing additional provisioning on top of normal NPA provisions. The logic: if banks delay resolution, they must hold more capital as a buffer — creating a financial incentive to act.

| Delay Timeline | Additional Provision Required |

|---|---|

| RP not implemented within 180 days | 20% additional provision |

| RP still not implemented by 365 days | 35% additional provision |

These are on top of the standard NPA provisioning (15% substandard, 25–100% doubtful). A bank sitting on a delayed restructuring could be provisioning 50%+ in total.

Step 6: Reversal of Additional Provision

Once the situation resolves, banks can reverse the extra provision — but only under strict conditions:

-

Normal resolution: Borrower is not in default for 6 months from the date dues are cleared or RP is implemented. The 6-month clean track record is proof the resolution is working.

-

IBC route (Insolvency & Bankruptcy Code): If the account goes to NCLT, reversal is in two tranches:

- 50% reversed when the insolvency application is filed with NCLT

- Remaining 50% reversed when NCLT admits the borrower into insolvency

-

Pre-direction provisions locked: Any provision that existed as on 02.04.2019 cannot be reversed unless the account is actually upgraded — old provisions cannot be quietly unwound without genuine recovery.

Post-Resolution Monitoring & Upgrade

Asset Classification During Resolution

- A standard account must be classified as NPA immediately upon default (if NPA norms are met).

- An NPA account continues as NPA.

Conditions for Upgrade Back to Standard

For a restructured NPA to be upgraded back to Standard, all conditions must be met:

- Account shows satisfactory performance — at least 10% of outstanding principal repaid from date of RP implementation

- Cooling period: Account cannot be upgraded before 1 year from commencement of first payment of interest or principal (whichever is later) on the loan with the longest moratorium

- Rating requirement: For loans of ₹100 crore or above, the loan must be rated at least Investment Grade (BBB−) by a CRA before upgrade

If the borrower fails satisfactory performance, a fresh RP is required.

After Change in Ownership — The 26% Rule

One resolution route is bringing in new promoters — fresh ownership that takes over the stressed company and commits to running it properly. The idea: the old promoter may have caused the stress; a new capable promoter with skin in the game can turn it around.

For the bank to upgrade the loan back to Standard under this route, the new promoters must have acquired at least 26% of the paid-up capital and voting rights of the company.

Why 26%? Under Indian company law, 26% is the threshold for a special resolution block — it gives the holder veto power over major corporate decisions (mergers, winding up, charter amendments). RBI uses this as the minimum "meaningful control" threshold. A promoter holding less than 26% is just a minority investor with no real authority to turn the company around.

So the logic: new promoter must have real control, not just a token stake, before the bank can treat the loan as standard again.

Additional Loans During the Monitoring Period

- Additional loans disbursed during the monitoring period are classified as Standard Asset.

- If the restructured loan does not show satisfactory performance at the end of the monitoring period, the additional loan is classified in the same category as the restructured loan.

Interest Suspense Account

This account holds unpaid interest on bad loans. It is not counted as part of provisions. You must deduct amounts in this suspense account from the relevant advances before applying standard provisioning norms.

Takeout Finance

Relates to long-term infrastructure project funding. Take-out financing resolves the mismatch between a bank's short-term deposits and 15–20 year infrastructure loans by having a long-term investor take over the debt obligation after a predetermined period (e.g., a sovereign pension fund).

- Income should not be recognized on accrual, but strictly when physically paid by the borrower.

- If the account defaulted before handover, the taking-over institution must treat the account as an NPA from the actual historical date of default.

Exchange Rate Impacts

- Foreign currency-denominated loans are not revalued due to exchange rate changes.

- If revalued, losses must be booked in the bank's P&L.

- Any revaluation gains must be fully provisioned against the assets.

Kamath Committee — COVID-19 Resolution Framework

Status: The KV Kamath Committee (formed by RBI, August 2020) prescribed financial benchmarks for the COVID-19 one-time restructuring window — deadline was March 31, 2022. That window is closed. No ongoing legal force. Examined as static banking awareness only.

- RBI formed the committee in August 2020; report submitted September 2020.

- Thresholds prescribed for 26 sectors.

- Five ratios prescribed: TOL/ATNW, Total Debt/EBITDA, Current Ratio, DSCR, ADSCR.

- Current Ratio and DSCR both set at 1.0 for almost all sectors.

Why 1.0? Both thresholds at 1.0 represent the bare minimum survivability level:

-

Current Ratio = 1.0 — current assets exactly cover current liabilities. The business can just pay its short-term obligations without a cash crisis. Below 1.0 means already illiquid — liabilities exceed assets on hand.

-

DSCR = 1.0 — cash generated from operations exactly equals debt repayment obligations. Every rupee owed is matched by exactly one rupee earned. Below 1.0 means the business cannot even service its loans from operations — restructuring would be pointless.

Setting both at 1.0 was deliberate: the committee wasn't asking COVID-hit businesses to be profitable — just to prove they were alive enough to survive restructuring rather than needing liquidation under IBC.

Revival and Rehabilitation of MSME Accounts

Status: Still Operative (2026). RBI issued this framework in March 2016 (circular RBI/2015-16/400).[3] The 2019 Prudential Framework did not supersede it — the 2019 framework governs large-exposure accounts, while this MSME-specific framework remains the operative mechanism for stressed MSMEs with exposure up to ₹25 crore. RBI's Master Direction on lending to MSMEs (FIDD.MSME) has been updated as recently as February 2026. Banks continue to maintain board-approved MSME Revival & Rehabilitation policies under this framework.

Eligibility and Identification

The framework applies to both fund-based and non-fund-based exposures up to ₹25 crore, including single bank, multiple banking, and consortium cases.

- Incipient Sickness: Identified based on Special Mention Account (SMA) status reflected by early warning signals (EWS). SMA status acts as the initial identification of Incipient Sickness.

- MSME Sick Unit: Defined as a unit where the previous year's net worth has eroded by 50% or more due to accumulated losses.

- Corrective Action Plan (CAP): Can take three forms:

- Rectification

- Restructuring

- Recovery

Committee Responsibilities by Loan Size

| Account Status | Amount | Action/Authority |

|---|---|---|

| SMA-2 Accounts | Up to ₹10 lac | CAP decided by Branch level committee but for recovery action consent of ZO/RO committee is required. |

| Stressed Accounts | Above ₹10 lac | Branch must forward details to Standing Committee at RO/ZO within 5 working days for a suitable CAP. |

The Rehabilitation Process Timeline

- Initiation by Borrower: A borrower identified as sick can apply to banks for rehabilitation; the committee must convene within 5 working days.

- Reference by Bank: If a bank makes a reference for an SMA-2 account above ₹10 lac, the committee must notify the borrower within 5 banking days.

- Information Gathering: The committee obtains information regarding statutory creditors and their dues within 15 days.

- The Decision: Within 30 days of the first meeting, the committee decides on the option and notifies the borrower within 5 banking days.

- Techno-Economic Viability (TEV): If restructuring is chosen, the committee must finalize the TEV and restructuring terms within 20–30 working days.

Implementation and Finalization

- Rectification only: Within 30 days.

- Restructuring: Within 90 days.

- Decision Rule (Majority): In consortium or multiple banking cases — 75% by value and 50% by number.

- Right to Review: If the committee decides on recovery, the borrower has the right to make a review application within 10 working days.

| Event / Action | Deadline | Key Requirement / Authority |

|---|---|---|

| Meeting Initiation (by Borrower) | Within 5 working days | Borrower identifies unit as sick and applies to the bank. |

| Branch Referral to Standing Committee | Within 5 working days | For stressed accounts above ₹10 lac. |

| Notification to Borrower (by Bank) | Within 5 banking days | If the bank initiates reference for SMA-2 accounts above ₹10 lac. |

| Gathering Information | Within 15 days | Regarding statutory creditors and their dues. |

| Final Decision on CAP Option | Within 30 days | Decided from the date of the first meeting. |

| Notify Borrower of CAP Decision | Within 5 banking days | Post-decision on the chosen option (Rectification/Restructuring/Recovery). |

| Finalizing Restructuring Terms/TEV | Within 20–30 working days | Techno-Economic Viability (TEV) study required for restructuring. |

| Implementation: Rectification | Within 30 days | Once the CAP is finalized. |

| Implementation: Restructuring | Within 90 days | Once the CAP is finalized. |

| Borrower Review Application | Within 10 working days | Applicable if the committee decides on the Recovery option. |

References

3 sources • [1] [2] [3]

References

Used for: The fundamental RBI framework (DBR.No.BP.BC.45/21.04.048/2018-19) dated June 7, 2019, outlining the 30-day review period, ICA requirements, 180-day implementation clock, and additional provisioning penalties.

Used for: The RBI clarification circular (RBI/2021-2022/125 DOR.STR.REC.68/21.04.048/2021-22) dated November 12, 2021, defining the CC/OD SMA criteria based on limit or DP, whichever is lower.

Used for: The MSME rehabilitation framework (FIDD.MSME & NFS.BC.No.21/06.02.31/2015-16) dated March 17, 2016, detailing the Standing Committee structure and CAP timelines.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Framework | RBI Prudential Framework — issued 7 June 2019 |

| Replaced | CDR, S4A, SDR, 5:25 schemes |

| SMA-0 | 1–30 Days Overdue (term loans only) |

| SMA-1 | 31–60 Days Overdue |

| SMA-2 | 61–90 Days Overdue |

| CC/OD SMA | No SMA-0 — only SMA-1 (31–60 days) and SMA-2 (61–90 days) beyond limit/DP |

| CRILC Scope | ≥ ₹5 Crore exposure |

| CRILC-Main | Monthly report |

| CRILC-Default | Weekly (every Friday) |

| Reference Date (₹2,000 Cr+) | 07.06.2019 |

| Reference Date (₹1,500 Cr+) | 01.01.2020 |

| Review Period | 30 days from default |

| ICA Majority | 75% (Value) & 60% (Number) |

| RP Implementation | Within 180 days of Review Period end |

| ICE Requirement | ₹100 Cr+ (1 ICE), ₹500 Cr+ (2 ICEs) |

| Min RP Rating | RP4 |

| Add. Provision (Delay) | 20% at 180 days; 35% at 365 days |

| Reversal (Normal) | Borrower not in default for 6 months from dues cleared / RP implemented |

| Reversal (IBC) | 50% on NCLT filing / 50% on NCLT admission |

| Pre-2019 Provisions | Cannot be reversed unless account is upgraded |

| Satisfactory Performance | 10% of outstanding principal repaid from RP date |

| Specified Period | Until 20% of outstanding principal repaid |

| Upgrade Cooling Period | Min 1 year from first payment (longest moratorium) |

| Upgrade Rating (≥₹100 Cr) | Min BBB− (Investment Grade) |

| New Promoter Ownership | Min 26% paid-up capital & voting rights |

| Kamath Committee | RBI Aug 2020; 26 sectors; COVID-19 one-time window (closed Mar 2022) |

| Kamath: CR & DSCR | Both at 1.0 — bare minimum survivability; below 1.0 = liquidation, not restructuring |

| MSME Scope | Fund-based + non-fund-based, up to ₹25 crore |

| MSME Sick Unit | Net worth eroded by ≥ 50% due to accumulated losses |

| MSME CAP | Rectification / Restructuring / Recovery |

| MSME ≤ ₹10 lac (SMA-2) | Branch-level committee |

| MSME > ₹10 lac | Standing Committee at RO/ZO within 5 working days |

| MSME Majority Rule | 75% by value and 50% by number |

| MSME Rectification | Within 30 days of CAP decision |

| MSME Restructuring | Within 90 days of CAP decision |

| MSME Review Right | Borrower can appeal recovery decision within 10 working days |

Lesson Doubts

Ask questions, get expert answers