🚫 Wilful Defaulter

Analysis of Wilful Defaulter guidelines, criteria for identification (diversion vs siphoning), and penal consequences.

RBI (Treatment of Wilful Defaulters and Large Defaulters) Directions, 2024[1]

Occurrences Qualifying as Wilful Default

A. In the Case of a Borrower

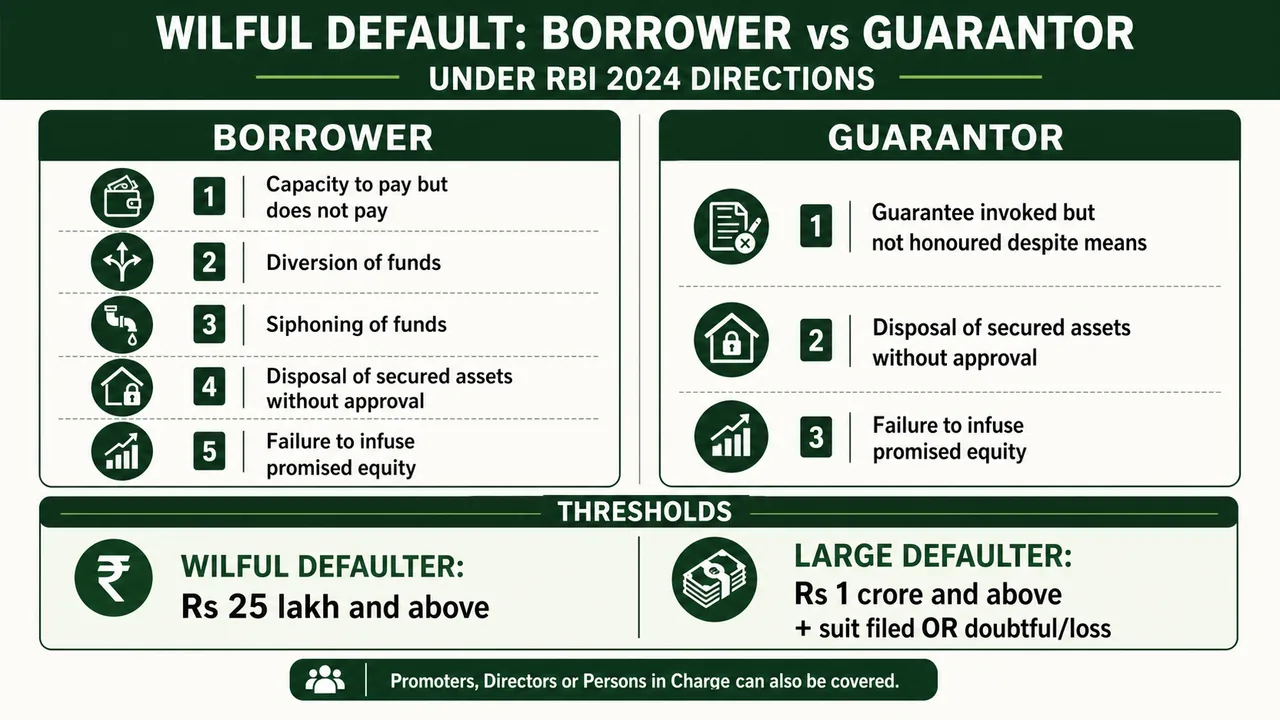

- A wilful default occurs when a borrower defaults on payment obligations to the lender.

- AND any one or more of the following features are present:

- Capacity to Pay (Intentional Default): The borrower holds the financial capacity to honor the obligations but intentionally chooses to hoard the funds rather than pay.

- Diversion of Funds (Misallocation): The borrower took a loan for a specific business purpose but deliberately redirected those funds toward unrelated or unauthorized internal activities.

- Siphoning of Funds (Theft): The borrower secretly extracted the loan funds out of the company entirely, meaning the money is strictly missing and neither contributing to operations nor existing as an asset within the firm.

- Asset Disposal (Undermining Security): To maliciously prevent the bank from recovering losses, the borrower illegally sold or disposed of the collateral assets originally pledged to secure the loan, without seeking the lender's permission.

- Equity Commitment Failure: When a stressed borrower receives lifelines (concessions) from the bank under the strict promise that promoters will inject their own personal equity to save the firm, failing to honor that equity injection despite having the wealth to do so constitutes wilful default.

B. In the Case of a Guarantor

A guarantor is treated as a wilful defaulter when:

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

RBI (Treatment of Wilful Defaulters and Large Defaulters) Directions, 2024[1]

Occurrences Qualifying as Wilful Default

A. In the Case of a Borrower

- A wilful default occurs when a borrower defaults on payment obligations to the lender.

- AND any one or more of the following features are present:

- Capacity to Pay (Intentional Default): The borrower holds the financial capacity to honor the obligations but intentionally chooses to hoard the funds rather than pay.

- Diversion of Funds (Misallocation): The borrower took a loan for a specific business purpose but deliberately redirected those funds toward unrelated or unauthorized internal activities.

- Siphoning of Funds (Theft): The borrower secretly extracted the loan funds out of the company entirely, meaning the money is strictly missing and neither contributing to operations nor existing as an asset within the firm.

- Asset Disposal (Undermining Security): To maliciously prevent the bank from recovering losses, the borrower illegally sold or disposed of the collateral assets originally pledged to secure the loan, without seeking the lender's permission.

- Equity Commitment Failure: When a stressed borrower receives lifelines (concessions) from the bank under the strict promise that promoters will inject their own personal equity to save the firm, failing to honor that equity injection despite having the wealth to do so constitutes wilful default.

B. In the Case of a Guarantor

A guarantor is treated as a wilful defaulter when:

- They do not honor the guarantee when invoked, despite having sufficient means.

- They dispose of movable or immovable assets securing the credit facility without lender approval.

- They fail to infuse equity despite having the ability, after the lender provided concessions based on that commitment.

Thresholds

A person or entity is classified as a wilful defaulter if:

- They are a borrower or guarantor who has committed a wilful default as per above criteria, AND

- The outstanding amount is ₹25 lakh and above.

- In the case of a company: This includes promoters, directors, and persons in charge of/responsible for the management of the entity's affairs.

Large Defaulter

A defaulter with an outstanding amount of ₹1 crore and above, where:

- A legal suit has been filed; OR

- The account has been classified as doubtful or loss (in terms of RBI rules).

Review and Identification Process

Lenders must follow a specific timeline and criteria for identifying these accounts:

- Mandatory Examination: Lenders must examine the "wilful default" aspect in all Non-Performing Asset (NPA) accounts with an outstanding balance of ₹25 lakh and above.

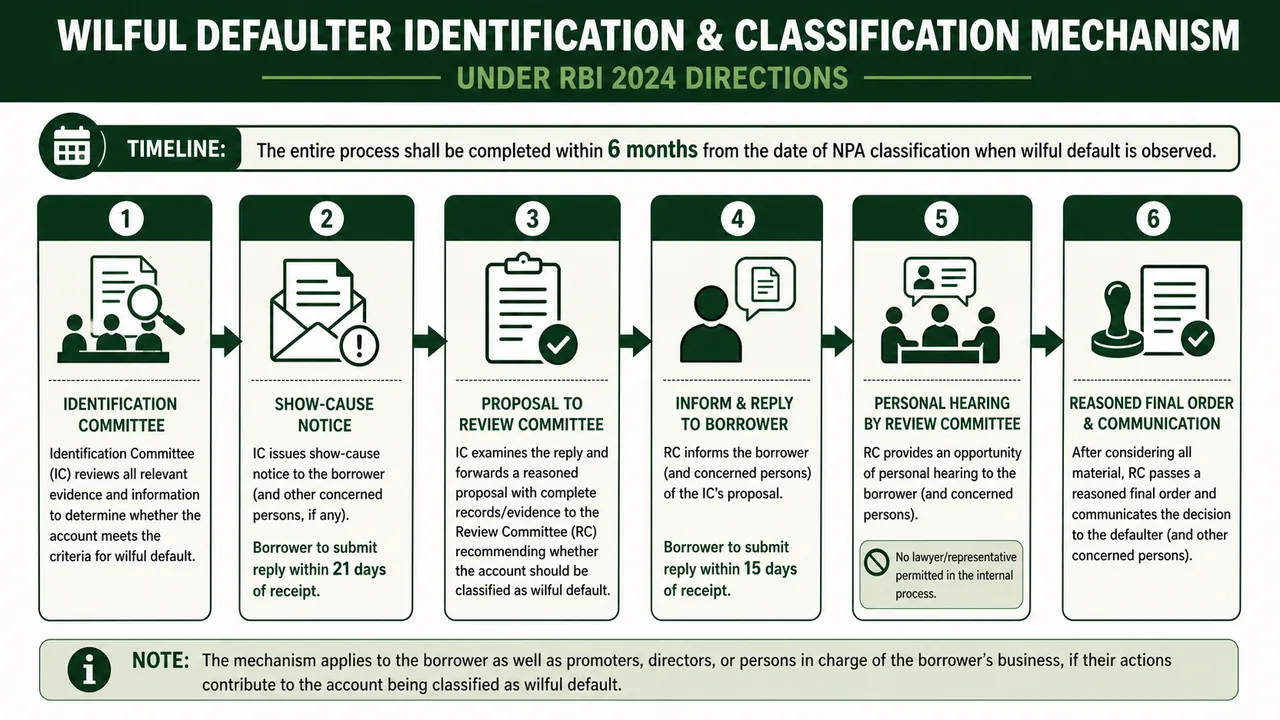

- Timeline: If a wilful default is observed during preliminary screening, the lender must complete the process of declaring/classifying the borrower as a wilful defaulter within 6 months of the account being classified as an NPA.

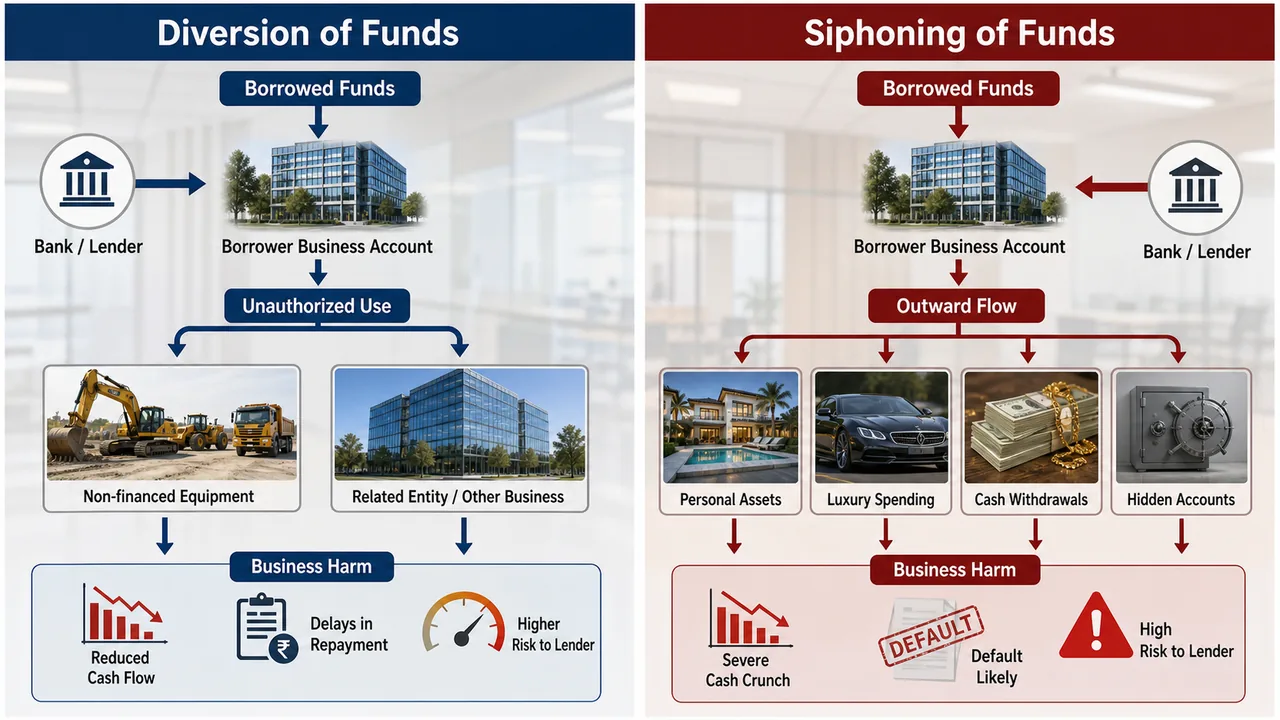

Definitions: Diversion vs. Siphoning

The RBI provides specific criteria for these actions:

| Diversion of Funds | Siphoning of Funds |

|---|---|

| Using short-term working capital for long-term purposes. | If any funds availed using credit facility from lenders are utilised for purposes unrelated to the operations of the borrower. |

| Creating assets other than those for which the credit was sanctioned. | |

| Transferring funds to subsidiaries/group companies without approval. | |

| Routing funds through a lender other than the consortium leader. | |

| Investing in equities/debt instruments of other entities without approval. |

The Core Difference: Diversion means the money stayed within the company's ecosystem but was managed improperly against the rules (e.g., using daily operational funds to buy a factory). The money isn't physically "lost," just misallocated. Siphoning is outright malicious extraction—the funds were drained completely out of the company for personal or totally unrelated use, vanishing from the firm's balance sheet entirely.

Guarding Against Diversion and Siphoning of Funds

- RBI advises banks/FIs to verify the end use of funds, especially in project financing, by requiring certifications from Chartered Accountants.

- For short-term and clean loans, banks should conduct their own due diligence and limit loans to reliable borrowers with proven integrity.

- Banks and FIs should not rely only on external certifications; they should strengthen internal controls and credit risk management to improve loan quality.

- Loan policy documents should include specific measures to ensure proper end use of funds.

Recommended end-use monitoring measures include:

- detailed review of borrowers' quarterly reports and financial statements

- regular inspections of assets pledged as security

- periodic examination of borrowers' accounting records and no-lien accounts with other banks

- frequent visits to sites or business units that received funding

- regular stock audits for working capital loans

- comprehensive management audits of the lending function

Identification & Classification Mechanism

The RBI mandates a two-tier committee process to ensure fairness:

| Stage | Process Description |

|---|---|

| Step 1: IC Review | The Identification Committee (IC) examines evidence of wilful default. |

| Step 2: SCN | If satisfied, the IC issues a Show-Cause Notice (SCN); the borrower has 21 days to reply. |

| Step 3: Proposal | The IC reviews the reply and makes a proposal for classification to the Review Committee (RC) with reasons. |

| Step 4: RC Reply | The borrower is advised of the proposal and has 15 days to reply to the RC. |

| Step 5: Hearing | RC shall provide an opportunity for a personal hearing. Borrowers and guarantors cannot use the services of a lawyer during this internal committee process, as this is a rapid banking fact-finding procedure, not a formal judicial courtroom trial. |

| Step 6: Final Order | The RC passes a reasoned order, which is communicated to the wilful defaulter. |

Note: Who can issue SCN: Lenders to have board-approved policy, designating rank of the official, to issue SCN and serve written order on behalf of IC or RC.

Composition of Identification Committee

| Bank Type | Chairman | Two Members |

|---|---|---|

| Commercial Banks | WTD (Whole Time Director) other than MD&CEO/CEO | Senior Officials (Max 2 ranks below Chairman) |

| Commercial Bank (One WTD or Vacant MD) | Official one rank below WTD | Senior Officials (Max 1 rank below Chairman) |

| Foreign Banks | Officer (Max 1 rank below Country Head/CEO) | Senior Officials (Max 2 ranks below Chairman) |

| UCBs / NBFCs | Officer (Max 1 rank below MD/CEO) | Senior Officials (Max 2 ranks below Chairman) |

| RRBs | Officer (Max 1 rank below Bank Chairman) | Senior Officials (Max 2 ranks below Chairman) |

Composition of Review Committee

| Bank Type | Chairman | Two Members |

|---|---|---|

| Commercial Banks | WTD (Whole Time Director) (MD&CEO / CEO or equivalent) | Independent / Non-Executive Directors |

| Commercial Bank (MD/CEO Vacant) | WTD in place of MD/CEO | Independent / Non-Executive Directors |

| Foreign Banks | Country Head / CEO | Senior Officials (Max 1 rank below Chairman) |

| UCBs | Chairperson | Professional Directors |

| RRBs | Bank Chairman | Nominated Directors |

Penal Measures

Once classified as a wilful defaulter, several penal measures apply:

- Legal Action: Lenders shall aggressively initiate expeditious legal action, including immediate foreclosure, to recover all blocked dues.

- Publicity (Naming & Shaming): To destroy the social and market credibility of fraudulent actors, lenders are legally permitted to publish photographs of declared wilful defaulters under a strict, non-discriminatory board policy.

- Only borrowers declared as wilful defaulters through the RBI-prescribed mechanism should have their photographs published.

- Publication of photographs of education loan defaulters is not permitted.

- Credit Quarantine (Post-Removal): Even after a defaulter repays their dues and gets removed from the List of Wilful Defaulters (LWD), they face a strict quarantine: lenders are legally barred from granting them any additional general credit facilities for one full year.

- New Venture Ban: To completely block serial fraudsters from abandoning a crashed company and immediately starting afresh with bank money, no credit can be granted to them for floating new ventures for a massive five years after their removal from the LWD.

- Restructuring Ban: Wilful defaulters are fundamentally untrustworthy and therefore strictly excluded from any compassionate loan restructuring lifelines while on the LWD. Subsequent to their removal, normal restructuring rules slowly apply.

- Management Change: Lenders may consider changing the management of persistently defaulting borrower units.

- Loan agreements must include a clause stating that the borrowing company cannot have any person on its Board of Directors whose name appears on the wilful defaulters list.

Reporting

Reporting and Dissemination of Credit Information on Large Defaulters

- All entities regulated by RBI, shall submit following information to all Credit Information Companies (CICs) of the large defaulters (threshold Rs. 1 crore and above) at monthly intervals.

- a list of suit filed accounts

- a list of non-suit filed accounts where classified as doubtful or loss account

- For calculating threshold amount, unapplied interest, shall also be included. In the case of suit-filed accounts, threshold shall relate to amount for which the suits have been filed.

- CICs shall

- provide access to the list of non-suit filed accounts of large defaulters to all credit institutions and

- display the list of suit-filed accounts of large defaulters on their website.

Reporting and Dissemination of Credit Information on Wilful Defaulters

- All lenders or ARCs to which the account has been transferred, shall submit the following information at monthly intervals including for the overseas loans:

- (a) List of wilful defaulters (LWD) in respect of suit filed accounts

- (b) LWD in respect of non-suit filed accounts

- Lender / ARC shall inform all CICs, the removal of the name of the wilful defaulter from the LWD, within 30 days, when the outstanding amount falls below the threshold of Rs. 25 lakh.

- Every CIC shall display the suit-filed and non-suit filed accounts of LWD on its website.

Related Borrower-Control Topics

Non-Cooperative Borrowers

- Non-cooperative borrowers are those who default on repayments and obstruct lenders' efforts for recovery.

- Borrowers with aggregate facilities exceeding Rs. 5 crore may be classified as non-cooperative.

- Classification should be done transparently by a committee of senior officials.

- A show cause notice must be issued to the borrower, followed by review by a higher committee.

- Information on non-cooperative borrowers must be reported to CRILC within 21 days.

- Boards of banks/financial institutions should review the status of non-cooperative borrowers every six months.

- Fresh exposure to non-cooperative borrowers requires higher provisioning.

- Loans to entities related to non-cooperative borrowers also attract increased provisioning.

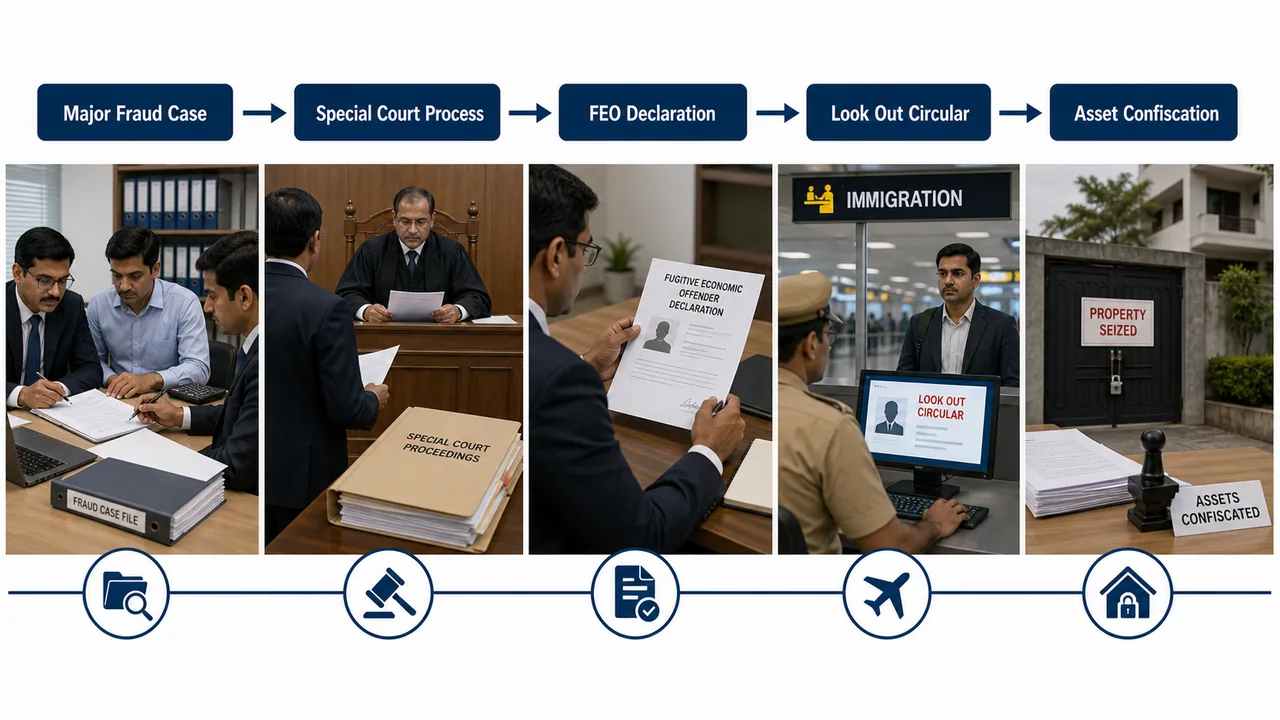

Fugitive Economic Offender

- The Fugitive Economic Offenders Act, 2018 targets economic offenders who leave India or refuse to return to avoid prosecution in major scheduled offences.[2]

- Scheduled offences must involve Rs. 100 crore or more, and 55 offences are currently listed.

- The Director or Deputy Director under the Prevention of Money Laundering Act can apply to a Special Court to declare someone a fugitive economic offender.

- The Special Court may order confiscation of proceeds of crime and other properties owned by the offender.

- Once declared a fugitive economic offender, the individual may be disallowed from participating in civil claims, and associated companies may also be restricted from defending claims.

Look Out Circular (LOC)

- A Look Out Circular (LOC) is a notice circulated to immigration officials to prevent wanted persons from leaving or entering the country undetected.[3]

- LOCs are issued by authorized government agencies to stop absconding fraud accused from evading prosecution.

- The Ministry of Home Affairs specifies the ranks of officers who can issue LOCs.

- Banks may request LOCs against borrowers, guarantors, or company officials involved in fraud.

- Requests are submitted to the Bureau of Immigration and should be signed by the bank's chairman, managing director, or CEO.

- When an LOC is issued, it should be reported to the Central Economic Intelligence Bureau for database updating.

- LOCs are valid for one year and can be renewed or withdrawn depending on case status.

- FEO Process: The LOC acts as a critical travel checkpoint. Once a Major Fraud Case triggers the Special Court Process resulting in an FEO (Fugitive Economic Offender) Declaration, the LOC ensures the offender cannot escape the country.

- Asset Confiscation: The final step in this process is the confiscation of properties and assets. The Special Court is empowered to seize the fugitive's proceeds of crime and other properties (including benami and overseas assets) to recover the bank's massive losses.

Criminal Offences and Investigation Agencies

- Borrowers engaging in wilful default along with criminal misconduct should be declared as wilful defaulters and reported to Credit Information Companies.

- Criminal offences include overstating assets, income, and profits, submitting false financial statements, and misappropriating funds.

- Other offences include submitting bogus bills for discounting, offering forged securities for loans, and disposing of pledged assets without consent.

- Borrowers may also borrow through impersonation, falsify books of accounts, or dishonour cheques.

- Banks must immediately lodge complaints with law enforcement once fraud is detected to prevent document loss, witness unavailability, borrower absconding, and asset stripping.

Guidelines for Reporting Frauds to Police/CBI

- RBI's fraud framework emphasizes that banks should prioritise public interest and ensure guilty parties are held accountable.

- Recovery of money should not be the sole objective; preventing impunity is equally important.

Engaging Private Investigative Agencies

- Lenders often hire private investigative agencies to uncover uncharged assets, gather information on borrowers' and guarantors' other businesses, and locate missing individuals.

- These agencies supplement bank officials' efforts in recovering losses from fraud rather than replacing them.

References

3 sources • [1] [2] [3]

References

Used for: The primary RBI Master Direction (DOR.AML.REC.24/14.01.001/2024-25) dated July 30, 2024, outlining the classification criteria, IC/RC committee structures, 21-day show-cause window, 15-day review appeal, and penal consequences.

Used for: The central legislation targeting economic offenders evading prosecution, establishing the ₹100 crore threshold and Special Court confiscation powers.

Used for: MHA instructions and Bureau of Immigration procedures governing the issue, validity (1 year), and executive authority signatures for Look Out Circulars.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Governing Direction | RBI (Treatment of Wilful Defaulters and Large Defaulters) Directions, 2024 |

| Wilful Default — Borrower | Default on payment AND any of: capacity to pay but chooses not to, diversion of funds, siphoning of funds, disposal of secured assets without approval, or failure to infuse equity despite ability |

| Wilful Default — Guarantor | Does not honour guarantee despite sufficient means; disposes secured assets without approval; fails to infuse committed equity |

| Threshold for Wilful Defaulter | Outstanding amount Rs. 25 lakh and above |

| Who is covered (company) | Promoters, directors, and persons in charge of management |

| Large Defaulter | Outstanding Rs. 1 crore and above where suit filed OR account classified as doubtful or loss |

| Mandatory NPA Examination | Lenders must examine wilful default aspect in all NPA accounts with outstanding Rs. 25 lakh+ |

| Timeline for Classification | Must be completed within 6 months of NPA classification |

| Diversion of Funds | Using WC for long-term purposes; creating unauthorized assets; transferring to subsidiaries without approval; routing via non-consortium banks; unauthorized equity/debt investments |

| Siphoning of Funds | Funds used for purposes unrelated to borrower's operations (funds not available as other assets) |

| End-Use Monitoring | Use CA certification, quarterly statement review, no-lien account checks, stock audits, site visits, and management audit to guard against diversion and siphoning |

| Non-Cooperative Borrowers | Obstructs lender monitoring/recovery; aggregate facilities above Rs. 5 crore. 5% provision on existing standard accounts; 15%+ provision on fresh loans. Report to CRILC within 21 days, board review every 6 months |

| FEO / LOC | Major absconding offenders may face Fugitive Economic Offender action under the 2018 Act; LOC is the travel-control alert, typically valid for 1 year unless renewed or withdrawn |

| Identification Committee (IC) | Examines evidence; issues Show-Cause Notice (SCN) with 21 days to reply |

| Review Committee (RC) | Receives IC proposal; gives borrower 15 days to reply; provides personal hearing; passes reasoned order |

| Lawyers in Committee Process | Borrowers/guarantors cannot use lawyers during internal committee hearings |

| IC Chairman — Commercial Banks | WTD (Whole Time Director) other than MD&CEO/CEO |

| RC Chairman — Commercial Banks | MD&CEO / CEO (or equivalent WTD) |

| RC Chairman — UCBs | Chairperson |

| RC Chairman — Foreign Banks | Country Head / CEO |

| RC Chairman — RRBs | Bank Chairman |

| Penal: Legal Action | Lenders initiate expeditious foreclosure and recovery |

| Penal: Publicity | Lenders can publish photographs per board-approved policy, but only after RBI-process declaration as wilful defaulter |

| Photo Disclosure Restriction | Publication of photographs of education loan defaulters is not permitted |

| Credit Restriction | No additional facilities for 1 year after removal from LWD |

| New Venture Restriction | No credit for floating new ventures for 5 years after removal from LWD |

| Restructuring | Not eligible while on LWD; eligible after removal subject to conditions |

| Management / Board Safeguard | Lenders may consider management change and should keep a clause barring wilful-defaulter-listed persons from board positions |

| Large Defaulter Reporting | Monthly to all CICs; threshold Rs. 1 crore+; includes unapplied interest |

| Wilful Defaulter Reporting | Monthly by lenders/ARCs to CICs (suit-filed and non-suit filed lists); includes overseas loans |

| Removal from LWD — CIC Intimation | Within 30 days when outstanding falls below Rs. 25 lakh |

| CIC Display | Suit-filed and non-suit filed LWD accounts displayed on CIC website |

| Criminal Escalation | On fraud signs, banks should move quickly to law enforcement; detailed Police / SFIO / CBI routing thresholds are covered in the Loan Fraud Management lesson |

Lesson Doubts

Ask questions, get expert answers