⚖️ DRT & Lok Adalat

Comprehensive guide on Debt Recovery Tribunals (DRT), DRAT, and Lok Adalats for loan recovery, including eligibility, jurisdiction, and procedures.

Debt Recovery Tribunals (DRT)

Introduction

Debt Recovery Tribunals (DRTs) are a special type of civil court dealing exclusively with loan recovery cases. They were created under the Recovery of Debt and Bankruptcy Act 1993 (RDB Act).[1] This Act was enacted on the recommendations of the Narasimham Committee-I to provide dedicated tribunals for expeditious adjudication and recovery of bank debts.

Historical Context: The Path to SARFAESI

- Following the DRTs, RBI notified the One Time Settlement (OTS) Scheme in 1997 & Corporate Debt Restructuring (CDR) Scheme in 2001.

- Later, a committee under Mr. Andhyarujina was appointed to address loopholes in these previous recovery acts, which ultimately recommended the creation of the powerful SARFAESI Act.

- Jurisdiction: Applicable to the whole of India (now including J & K).

- Objective: To expedite recovery in big loan accounts.

- Exclusivity: Eligible cases can be filed only in DRT and not in other civil courts.

Eligibility Checklist

| Criteria | Requirement |

|---|---|

| Minimum Amount | ₹20 Lakh (current operative threshold by Central Government notification) |

| Place for Suit | Where the defendant resides/conducts business OR where the cause of action arises. |

NOTE

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Debt Recovery Tribunals (DRT)

Introduction

Debt Recovery Tribunals (DRTs) are a special type of civil court dealing exclusively with loan recovery cases. They were created under the Recovery of Debt and Bankruptcy Act 1993 (RDB Act).[1] This Act was enacted on the recommendations of the Narasimham Committee-I to provide dedicated tribunals for expeditious adjudication and recovery of bank debts.

Historical Context: The Path to SARFAESI

- Following the DRTs, RBI notified the One Time Settlement (OTS) Scheme in 1997 & Corporate Debt Restructuring (CDR) Scheme in 2001.

- Later, a committee under Mr. Andhyarujina was appointed to address loopholes in these previous recovery acts, which ultimately recommended the creation of the powerful SARFAESI Act.

- Jurisdiction: Applicable to the whole of India (now including J & K).

- Objective: To expedite recovery in big loan accounts.

- Exclusivity: Eligible cases can be filed only in DRT and not in other civil courts.

Eligibility Checklist

| Criteria | Requirement |

|---|---|

| Minimum Amount | ₹20 Lakh (current operative threshold by Central Government notification) |

| Place for Suit | Where the defendant resides/conducts business OR where the cause of action arises. |

NOTE

Why DRTs? Before 1993, banks had to file suits in normal civil courts, which took years. DRTs were established to create a dedicated fast-track channel for banks to recover bad loans.

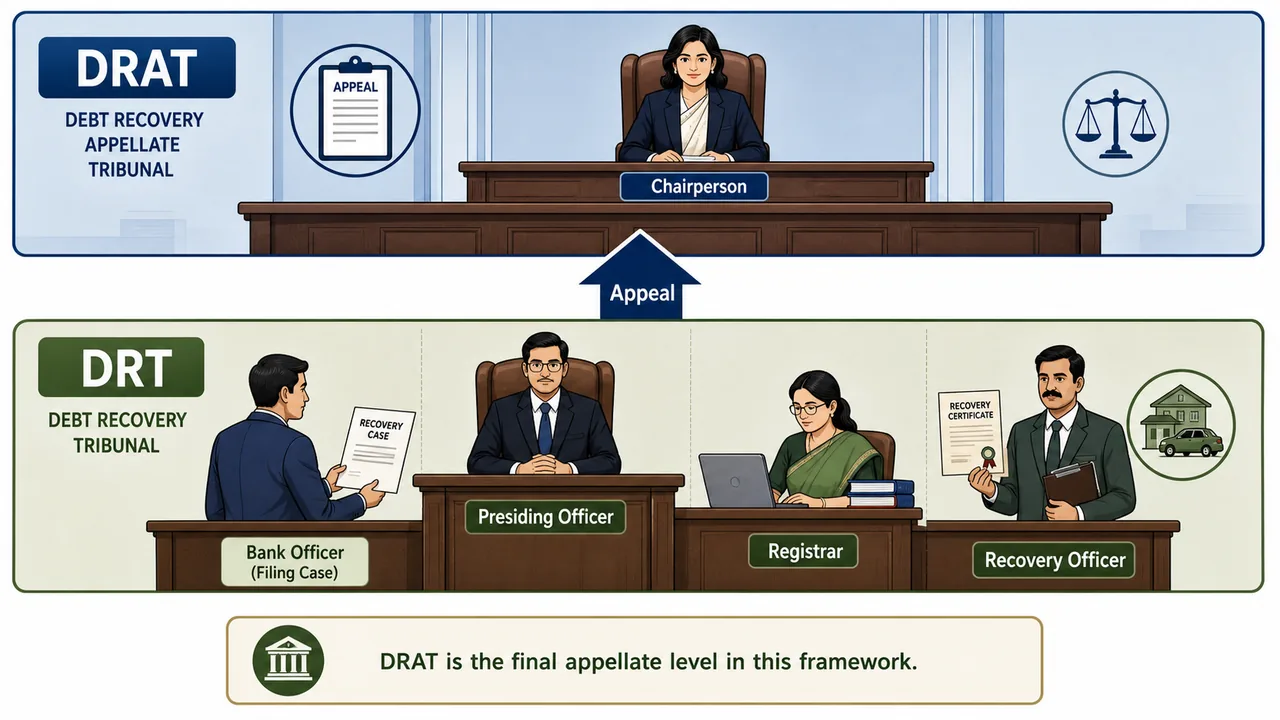

2-Level DRT Structure

The system is organized into two tiers:

- DRT (Debt Recovery Tribunal): The first level for filing suits.

- DRAT (Debt Recovery Appellate Tribunal): The appellate, second level for appeals against DRT decisions.

IMPORTANT

Under the RDB Act, the statutory appeal chain is DRT → DRAT.[1] The Act does not create a regular further appeal from DRAT in the same manner. However, DRAT orders may still be challenged before the Supreme Court under Article 136 and before the High Courts under Articles 226/227.[1]

Officials

| Role | DRT (Tribunal) | DRAT (Appellate Tribunal) |

|---|---|---|

| Head | Presiding Officer | Chairperson |

| Qualification | As prescribed under the governing tribunal appointment framework | As prescribed under the governing tribunal appointment framework |

| Tenure | 4 Years (Till age 70, Min age for appointment: 50 years)[4] | 4 Years (Till age 70, Min age for appointment: 50 years)[4] |

Other Key Staff (DRT)

- Registrar: Handles the filing of suits.

- Recovery Officer: Executes recovery based on the Recovery Certificate issued by the Presiding Officer.

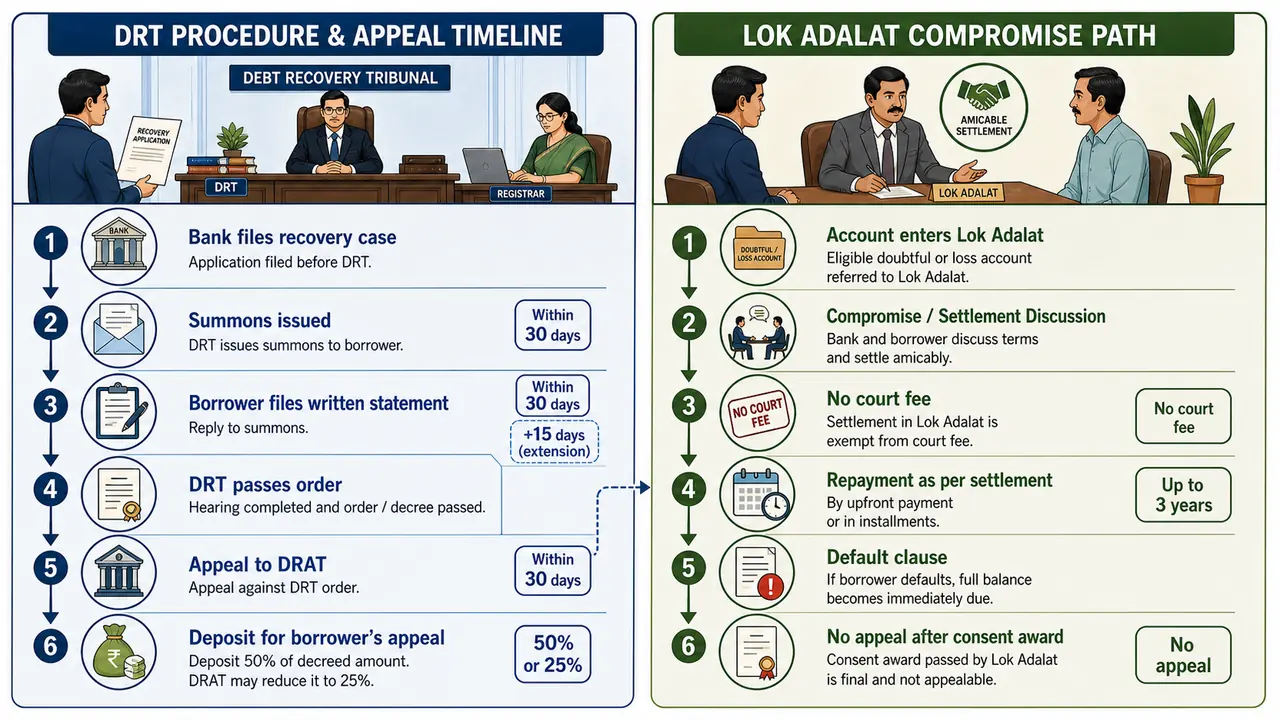

Procedure & Timelines

- Place for suit: Where defendant resides/ conducts business or where cause of action arises.

- Issue of Summons: DRT issues summons to the defendant (borrower/guarantor) within 30 days to submit a reply explaining why relief should not be granted to the bank.

- Written Statement: The defendant is given 30 days to send a written statement (can be extended by 15 days).

- Time limit for DRT Presiding Officer to decide: The DRT Presiding Officer should ideally decide the case within max two hearings.

Appeal Process

-

Appeal to Presiding Officer: Grievances against the Registrar or Recovery Officer can be appealed to the DRT Presiding Officer within:

- 15 days for Registrar orders.

- 30 days for Recovery Officer orders. The Presiding Officer must pass an order on this appeal within 60 days of receiving notice.

-

Appeal to DRAT: An appeal against a DRT decision can be made to the DRAT by the bank or borrower within 30 days from the date of receipt of the order.

-

Time limit for DRAT to decide an appeal: max 180 days.

-

Deposit Rule for Borrowers (Anti-Stalling): Historically, borrowers would automatically appeal every single DRT loss to DRAT simply as a free stalling tactic. To stop this, if a borrower wants to appeal, they are forced to immediately deposit 50% of the decreed amount. This proves they have genuine grievances and aren't just buying time to hide assets. This requirement can be reduced by DRAT up to 25%, but no lower.

-

After DRAT: The Act provides the ordinary statutory appeal to DRAT. It does not create a regular further tribunal-style appeal on the same pattern. But DRAT orders may still be challenged before the Supreme Court under Article 136 and before the High Courts under Articles 226/227.[1]

-

DRAT does not have a separate lower-value threshold of its own in this chapter. It hears appeals from DRT orders, and the current operative DRT filing threshold is ₹20 lakh.

Powers & Legal Status

- The tribunal/appellate tribunal shall be deemed to be a Civil Court.

- The proceedings before the Tribunal/Appellate Tribunal are deemed to be judicial proceedings.

- Both DRT & DRAT can issue summons and enforce the attendance of any person to examine him.

- Tribunal may pass an order of attachment or sale of property of the defendant.

DRT as Adjudicating Authority under IBC

- Presiding Officer of DRT also functions as Adjudicating Authority under IBC 2016 for individual insolvency cases.

- Chairperson of DRAT also functions as Appellate Authority under IBC for individual insolvency cases.

Fees Structure

- Fee for DRT: Min ₹12,000 and Max ₹1.50 Lakh.

- Fee for DRAT: Min ₹12,000 and Max ₹30,000.

Lok Adalat

Concept & Jurisdiction

Lok Adalats are forums for dispute resolution established as per the Legal Services Authority Act 1987.

- Organizers: Organized by District Authority, State Authority, Taluka, or High Court/Supreme Court Legal Services Committee.

- Core Principle: Derives jurisdiction out of compromise between parties to a dispute. It has not legal jurisdiction rather it is out of compromise between parties to a dispute.

- Scope:

- The dispute could be pending in a court.

- Non-compoundable offences cannot be entertained by Lok Adalat.[5]

- If compromise is not possible, the case is referred back to the appropriate court.

Key Features

- No Court Fee is charged.

- Legal Status: The award of a Lok Adalat is deemed to be a Decree of a civil court.

- Finality: These are consent decrees, because they are based on compromise between parties to a dispute, they are final and binding.

- No Appeal: No appeal is absolutely allowed against the Award of Lok Adalat. Why? Because a Lok Adalat isn't a judge imposing a forced ruling—it's a mutual "consent decree." Both the bank and the borrower actively agreed to the compromise, and legally, you cannot appeal an outcome you voluntarily consented to.

RBI Guidelines for Banks

Banks use Lok Adalats as a tool for recovery in smaller NPA accounts.

1. Monetary Limits

- Civil Liability: Up to ₹20 Lakh.

- Above ₹20 Lakh: Can be handled by Lok Adalats organised by DRT.

2. Loan Types

- Eligible Accounts: Doubtful and Loss accounts only.

- Why? Standard borrowers are legally bound to pay 100%. If banks allowed healthy or mildly stressed borrowers to settle in Lok Adalats, everyone would strategically default just to get a discount. Lok Adalats are reserved strictly for cases where the bank has practically given up hope and prefers recovering a smaller, compromised sum rather than nothing at all.

3. Repayment Terms

- Preference for one-time upfront payment.

- If installments are necessary, repayment can be agreed upon for up to 3 years.

- The negotiated agreement MUST contain a default clause. The bank's massive discount is conditional. If the borrower breaks the new, easier payment plan, the compromise is instantly voided, and the original, full, massive pre-compromise debt will fall due for immediate repayment.

4. Procedures

- Lok Adalat is not an ordinary civil court trial forum, but the Act gives it specific civil-court powers for summoning, receiving evidence on affidavit, requisitioning public records, and related procedural acts.[5][6]

- FIs are required to get in touch with the state/district/taluk level legal service authorities for organising the Lok Adalats.

- If no settlement is arrived at through the Adalats, the parties can continue with the court proceedings.

- A decree/certificate from the Lok Adalat for the principal amount and interest claimed — after full repayment, a discharge certificate should be issued by the bank/FI.

- The representing officers should have sufficient authority to accept compromises within bank policy framework and should respond pro-actively to the suggestions of the Presiding Officer.

4. Reporting

- Banks must send a quarterly progress report about cases in Lok Adalat to RBI within 15 days.

Supreme Court Direction Personal loan cases with an amount less than ₹10 Lakh should preferably be settled through Lok Adalat. So that civil courts can focus on large cases and save time.

References

6 sources • [1] [2] [3] [4] [5] [6]

References

Used for: Primary source for DRT jurisdiction, DRT-to-DRAT appeals, the 50% deposit rule reducible to 25%, and the ordinary statutory tribunal appeal structure.

Used for: Official notification trail showing the operative DRT pecuniary threshold increase from ₹10 lakh to ₹20 lakh.

Department of Financial Services — Debts Recovery Tribunals / Debts Recovery Appellate Tribunals

OfficialUsed for: Official DFS page used for current DRT/DRAT institutional count and overview.

Used for: Primary source for the current tenure structure of tribunal chairpersons, including the applicable DRT/DRAT tenure and age framework used in this lesson.

Used for: Primary source for Lok Adalat jurisdiction, finality of awards, non-compoundable-offence exclusion, and statutory powers.

Used for: Official NALSA explainer used for current Lok Adalat process framing and institutional practice.

Summary Cheat Sheet

| Concept | Key Detail |

|---|---|

| DRT Act (Legal Basis) | Recovery of Debt and Bankruptcy Act 1993 |

| DRT Eligible Amount | Min ₹20 Lakh |

| Number of DRTs / DRATs | 39 DRTs and 5 DRATs (Allahabad, Chennai, Delhi, Kolkata, Mumbai) |

| DRT Presiding Officer | Term 4 years, till age 70, min age 50 |

| DRAT Chairperson | Term 4 years, till age 70, min age 50 |

| Appeal: DRT → DRAT | Within 30 Days of receipt of order |

| After DRAT | Ordinary statutory appeal ends at DRAT; DRAT orders may still be challenged before the Supreme Court under Article 136 and High Courts under Articles 226/227 |

| DRT / DRAT Threshold Link | DRT filing threshold currently ₹20 Lakh; DRAT hears appeals from those DRT matters |

| Appeal Deposit (% of Decree) | 50% (Reducible to 25% by DRAT) |

| Heads of Tribunals | DRT: Presiding Officer / DRAT: Chairperson |

| Time Limits | DRT: Max 2 Hearings / DRAT: Max 180 Days |

| Legal Status | Deemed Civil Court, proceedings are judicial |

| DRT under IBC | Presiding Officer = Adjudicating Authority for individuals |

| Lok Adalat Act | Legal Services Authority Act 1987 |

| Lok Adalat Appeal | None (Award is Final / Consent Decree) |

| Lok Adalat Eligibility | Doubtful & Loss Assets |

| Lok Adalat Amount Limit | Up to ₹20 Lakh (Civil Liability) |

| Lok Adalat Offence Rule | Non-compoundable offences cannot be taken up |

| Lok Adalat Personal Loans | < ₹10 Lakh (Supreme Court Direction) |

| Lok Adalat Nature | Dispute Resolution via Compromise |

| Lok Adalat Repayment | Within 3 years, must have default clause |

| Lok Adalat Powers | Has specified civil-court powers for summons, evidence, records, etc., but is not a normal civil-court trial forum |

Lesson Doubts

Ask questions, get expert answers