🏦 SARFAESI

Detailed provisions of SARFAESI Act, Asset Reconstruction Companies (ARC), and the NARCL (Bad Bank) structure.

SARFAESI Act 2002

- SARFAESI Act = Securitization And Reconstruction of Financial Assets and Enforcement of Security Interest Act 2002.

- Passed on December 17, 2002, to lay down processes to help Indian lenders recover their dues efficiently.

- The Act essentially empowers banks and other financial institutions to directly auction residential or commercial properties that have been pledged with them.

- Constitutional validity:

- Upheld (approved) by Supreme Court in Mardia Chemicals vs Union of India and others.

- Section 17, was amended in 2004, as a fallout of this case.

- Act extends to whole of India (including J & K).

- Court jurisdiction for SARFAESI Act case: DRT and DRAT, as created under RDDB Act 1993.

- The major drawback of the Act is that it is not applicable to unsecured creditors. Because the entire premise of SARFAESI is empowering banks to directly auction pledged collateral without court intervention, if there is no collateral (an unsecured loan), there is nothing to auction. Thus, unsecured lenders cannot use SARFAESI.

3 Types of Provisions of SARFAESI Act

- Creation of Asset Reconstruction Companies

- Setting up of Central Registry of Charges

- Enforcement of Security Interest

Asset Reconstruction Company (ARC)

-

ARC (previously Securitization companies (SCs) or Reconstruction Companies) are created under the Act.

Interactive Preview

Try the embedded exercise below. Full lesson access still requires Pro.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

SARFAESI Act 2002

- SARFAESI Act = Securitization And Reconstruction of Financial Assets and Enforcement of Security Interest Act 2002.

- Passed on December 17, 2002, to lay down processes to help Indian lenders recover their dues efficiently.

- The Act essentially empowers banks and other financial institutions to directly auction residential or commercial properties that have been pledged with them.

- Constitutional validity:

- Upheld (approved) by Supreme Court in Mardia Chemicals vs Union of India and others.

- Section 17, was amended in 2004, as a fallout of this case.

- Act extends to whole of India (including J & K).

- Court jurisdiction for SARFAESI Act case: DRT and DRAT, as created under RDDB Act 1993.

- The major drawback of the Act is that it is not applicable to unsecured creditors. Because the entire premise of SARFAESI is empowering banks to directly auction pledged collateral without court intervention, if there is no collateral (an unsecured loan), there is nothing to auction. Thus, unsecured lenders cannot use SARFAESI.

3 Types of Provisions of SARFAESI Act

- Creation of Asset Reconstruction Companies

- Setting up of Central Registry of Charges

- Enforcement of Security Interest

Asset Reconstruction Company (ARC)

-

ARC (previously Securitization companies (SCs) or Reconstruction Companies) are created under the Act.

-

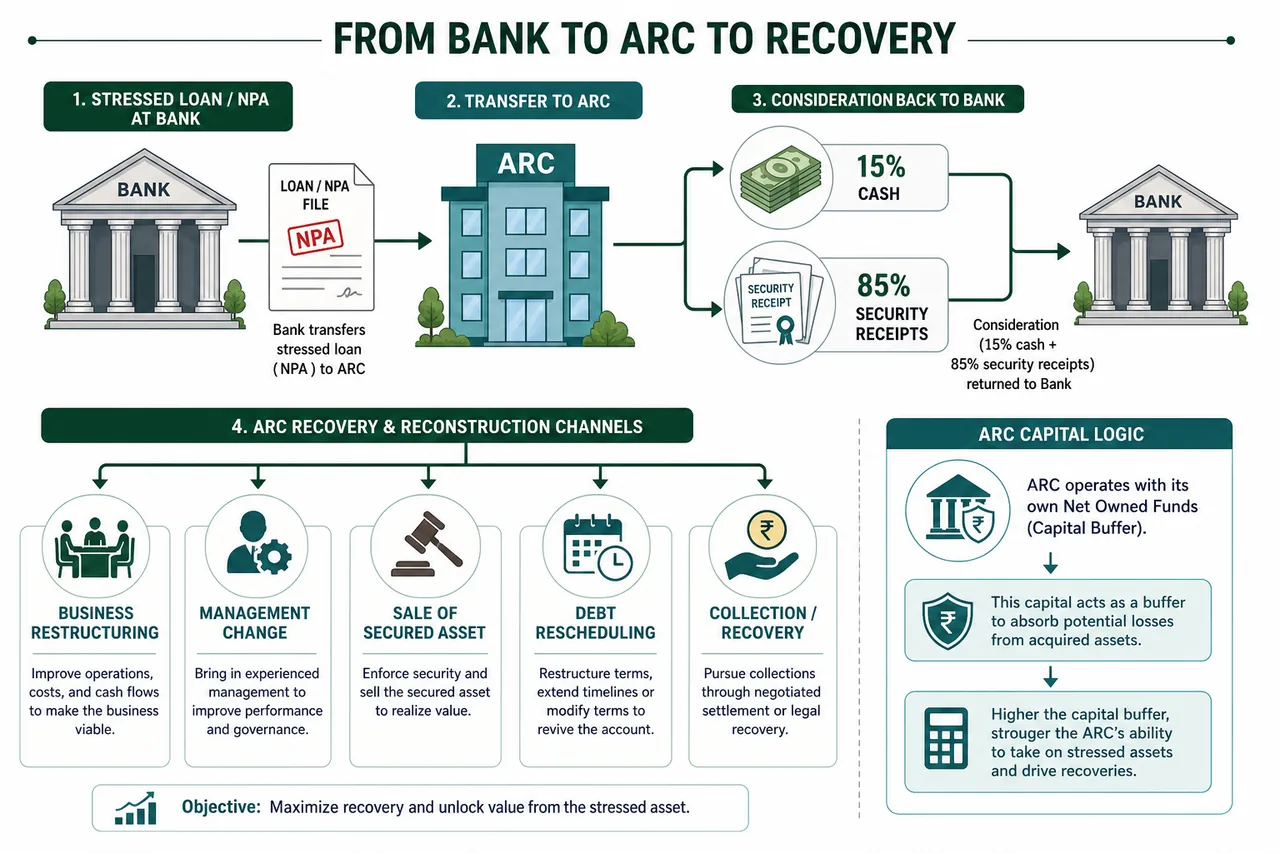

Functions: Purchase stressed assets from banks / FIs to recover through:

- (a) Securitization: Process of converting illiquid assets (loans) into marketable securities (Security Receipts) sold to QIBs.

- (b) Reconstruction: Measures taken to revive the business or realize the debt (e.g., change management, sale of assets, rescheduling debt).

- (c) sale of available securities

- (d) change of management etc.

-

Recovery period: 5 years (can be extended by 3 years by Board of Directors).

-

RBI registration: ARC to have registration with RBI. Can commence business within 6 months of such registration.

-

Minimum Net Owned Funds (NOF) - [Updated 11.10.22]:

- Rs. 300 Crore (Increased from Rs. 100 Crore).

- OR 15% of acquired assets, whichever is lower.

-

Net worth: At least 15% of NPAs acquired, all the time.

-

Capital Adequacy Ratio: Min 15% of Risk Weighted Assets.

-

Investment by ARC in Security Receipts ("Skin in the Game"):

- The RBI wants ARCs to share the risk so they don't just act as middlemen. When an ARC issues Security Receipts (SRs), it must invest its own money in them.

- The Rule: The ARC must invest a minimum of either 15% of the Transferor's (Bank's) investment in those SRs OR 2.5% of the total SRs issued, whichever is higher.

Why the "whichever is higher" rule? Imagine Bank A sells a ₹100 crore NPA to an ARC. The ARC issues ₹100 crore of SRs. Initially, Bank A holds 100% of these SRs. 15% of Bank A's investment = ₹15 crore. But what if Bank A sells most of its SRs to a mutual fund, and now holds only ₹10 crore? If the rule was only "15% of the Bank's holding", the ARC would now only have to invest ₹1.5 crore. To stop the ARC's risk from dropping too low, the RBI put a hard floor: 2.5% of the total SRs issued (i.e., 2.5% of ₹100 crore = ₹2.5 crore). Since ₹2.5 crore > ₹1.5 crore, the ARC is forced to keep at least ₹2.5 crore invested.

NOTE

Security Receipts Instrument issued by ARC to Qualified Institutional Buyers (QIBs) evidencing purchase of joint right in financial asset. Means the invester buy a part, then he and other investors have a "joint" claim. When the ARC successfully recovers money from the borrower, that money is distributed among all receipt holders based on their share.

ARCIL: India's First ARC

Now that we understand the concept of an ARC, let's look at the pioneer.

- ARCIL (Asset Reconstruction Company (India) Limited) was the very first ARC established in India in 2002, right after the SARFAESI Act was passed.

- Sponsors & Owners: It was jointly promoted by four major Indian banks: SBI, IDBI Bank, ICICI Bank, and PNB. These banks remain its principal shareholders.

- Registered with RBI as a securitisation and reconstruction company.

- Primary objective: Acquire NPAs from banks and resolve through recovery, restructuring, sale, and enforcement of security interest. Also provides advisory and consultancy services.

- Operates as a public limited company, listed on BSE and NSE.

- Headquarters: Mumbai; Regional offices: Delhi, Chennai, Kolkata, Bangalore.

- Actively involved in resolution under IBC and other mechanisms.

- Notable cases resolved: Kingfisher Airlines and Bharathi Cements.

National Asset Reconstruction Company Limited (NARCL) BAD BANK

- NARCL has been registered under Companies Act 2013 in July 2021.

- Its authorized capital is Rs.100 cr.

- Its capital has been subscribed by a no. of banks. 51% to remain with public sector banks.

- Functions: It will takeover large sized NPA accounts from banks, with individual size of above Rs.500 cr.

- On acquiring a loan, NARCL shall pay 15% in cash upfront to the bank. The remaining 85% shall be paid in the form of security receipts (which are essentially IOUs promising to pay the bank the rest of the money if and when NARCL successfully liquidates the toxic asset).

- Govt. guarantee: Govt. to provide guarantee of up to value of Rs.30,600 cr (valid for 5 years) to security receipts issued by NARCL.

- Govt. guarantee can be invoked if there is failure in payment of security receipts.

- India Debt Resolution Company Limited (IDRCL) = It is an operational entity that will manage assets of NARCL.

Example: Invoking the Guarantee

1. The Shortfall Scenario When NARCL takes over a bad loan, it pays 15% in cash and 85% in Security Receipts (SRs). These receipts represent the "Face Value" of what NARCL expects to eventually recover from the borrower.

The Problem: If NARCL is unable to recover the full amount (e.g., they expected to recover ₹100 Cr but only got ₹70 Cr), there is a shortfall.

2. Invoking the Guarantee "Invoking" the guarantee means the selling bank officially asks the Government to pay the difference.

- Condition Precedent: The guarantee can only be triggered after the resolution or liquidation process of that specific loan is finished.

- The Payout: The Government pays the gap between the actual amount recovered and the face value of the Security Receipt.

- Ceiling: This payout comes from the ₹30,600 crore fund set aside by the government.

3. Why This Matters

- Protecting Banks: It ensures that even if the "Bad Bank" fails to recover the money, the selling banks do not suffer further losses.

- Regulatory Compliance: RBI allows banks to hold these receipts without extra "provisioning" money, freeing up capital to give new loans.

- Time Limit: Valid for 5 years to encourage NARCL to resolve bad loans quickly.

NOTE

Confused between ARCIL, NARCL, and IDRCL? These three acronyms sound very similar but have distinct roles in the banking system:

- ARCIL (The Pioneer): This was the very first ARC established in India (2002). It is a standard, private ARC that buys bad loans from banks and tries to recover them.

- NARCL (The "Bad Bank"): Set up much later in 2021. It is a special, government-backed ARC created strictly to clear out massive toxic loans (above ₹500 crore). It legally buys and owns the bad loans.

- IDRCL (The Manager): This is the twin sister of NARCL. While NARCL legally owns the loans, it doesn't have the staff to resolve them. IDRCL is the operational agency that actually does the ground work to sell, restructure, or recover the money on behalf of NARCL.

Acquisition of Interest in Financial Assets

- ARC may acquire financial assets of any bank by issuing debt & debenture or by entering into an agreement with the financial institution.

- NPA shall be acquired at a reasonable price.

- Banks and FIs may receive bonds/debentures in exchange for NPAs transferred to ARCs. A part of the value can be paid in the form of Security Receipts (SRs). Latest regulations instruct that ARCs should give 15% of the value of assets in cash.

- The first ARC in India is ARCIL (ARC India Ltd).

- ARCs are currently prohibited from engaging in any business other than securitisation, asset reconstruction, or the activities listed in Section 10(1) of the SARFAESI Act, without RBI's prior clearance.

ARC Governance Norms

- The chair of the board must be an independent director, and at least half of the total board must consist of independent directors. (Additionally, no more than half can be nominee directors). Why so strict? ARCs deal in massive billions of rupees of distressed assets, creating a massive risk for sweetheart deals and corruption. A highly independent board ensures transparent, fair-market auctions rather than ARCs illegally selling assets back to the original defaulting promoters through backdoor deals.

- Tenure of MD, CEO, and Whole Time Directors: cannot be more than 5 years.

- They will be eligible for reappointment and cannot continue beyond the age of 70 years.

- Fit and proper assessment of directors must be carried by banks.

- Company can't be operated by more than 2 whole time directors.

- Audit Committee: ARCs shall constitute an Audit Committee of the Board, which shall comprise of non-executive directors only. The Chair of the Board shall not be a member of the Audit Committee. The Audit Committee shall meet at least once in a quarter with a quorum of 3 members.

ARC Capital & Transition

- Minimum capital requirement for setting up an ARC raised to Rs 300 crore from the existing Rs 100 crore.

- Existing ARCs have been given a glide path to meet the minimum net owned fund (NOF) requirement till March 2026.[2]

- Any ARC obtaining the certificate of registration on or after the date of this circular shall not commence the business of securitisation or asset reconstruction without having minimum NOF of Rs 300 crore.

- Transition Period: ARCs that currently do not comply with the RBI guidelines are required to comply within six months from the date of announcement.

ARCs as Resolution Applicants under IBC

Usually, an ARC's job is just to buy bad loans and recover the money. However, the RBI now allows ARCs to act as Resolution Applicants under the Insolvency and Bankruptcy Code (IBC). This means an ARC can formally bid to take over, own, and run a bankrupt company to turn it around.

Because taking over and managing a bankrupt company is highly risky and requires massive capital, the RBI has set strict conditions:

- Massive Capital Required: The ARC must have a minimum Net Owned Fund (NOF) of at least Rs 1,000 crore (remember, normal ARCs only need Rs 300 crore).

- The 5-Year Exit Rule: The RBI does not want ARCs to permanently become steel manufacturers or real estate developers. Their core job is finance. Therefore, if an ARC takes over a company, it must sell its controlling stake and exit within 5 years of the resolution plan's approval. It cannot retain "significant influence or control" after this period.

- Internal Policy: Must have a Board-approved policy specifically for taking up the role of a resolution applicant.

- Transparency: Must make enhanced financial disclosures regarding any companies/assets acquired under the IBC.

CERSAI (Central Registry)

- CERSAI = Central Registry of Securitisation Asset Reconstruction and Security Interest of India.

- Established on 31.03.2011 as a company under Section 8 of the Companies Act, 2013, under sub-section (1) of Section 20 of the SARFAESI Act, 2002.

- The Central Government owns a 51% stake in CERSAI. Remaining shareholding is with Public Sector Banks and National Housing Bank (NHB).

- Registered Office: New Delhi.

- Objective: Prevent loan frauds relating to multiple mortgage of same property. Before CERSAI, a fraudster could physically pledge the same house title to Bank A, Bank B, and Bank C simultaneously. Because there was no central database, the banks didn't know about each other until the fraudster vanished. CERSAI solves this by creating a mandatory, centralized database of every mortgaged property in India.

- Mandatory registration with CERSAI:

- (a) Transaction under SARFAESI Act (securitisation & reconstruction of financial assets and equitable mortgages)

- (b) Charges such as Mortgage, hypothecation, assignment etc.

- Time limit for registration: 30 days time limit has been removed w.e.f. 24.01.20 (Section 19 — omission of Section 27).

- No penalty for default in filing, modifying and satisfaction of security interest.

CERSAI Registration Scope

As per SARFAESI Act 2002, registration of security interest for all movable, immovable and tangible assets charged to the bank in CERSAI is mandatory, EXCEPT:

| Exemption | Where Registered Instead |

|---|---|

| Vehicles | VAHAN Portal (not CERSAI) |

| Agricultural Land | Exempt from CERSAI |

| Loan against Bank Deposit | Exempt |

| Government Security Papers | Exempt |

| Loans below ₹1 Lakh | Exempt |

Satisfaction of Charge

When a company repays its secured loan fully to the lender, or when the property or asset charged has been released from charge, it is known as satisfaction of charge. The charge must be deregistered from CERSAI. (Note: The strict penalty provisions for delay in filing satisfaction within 30 days have been removed to ease compliance).[3]

IMPORTANT

Branches must return securities/documents/title deeds to the borrower within 15 days of repayment of all dues.

KYC Registry (PML Rules 2005)

CERSAI was also entrusted with operating and maintaining a KYC Registry, governed under PML Rules 2005 (Prevention of Money Laundering — Maintenance of Records).

| Parameter | Detail |

|---|---|

| KYC Identifier | 14-digit unique number generated for new customer records |

| Prefix "S" | For Small Accounts |

| Prefix "L" | For Simplified Measures Accounts |

| KYC Upload Timeline | Non-individual customer records must be uploaded within 18 days of account opening |

| Authorizing Section | SARFAESI Section 20(1) |

Forms and Fees

| Form | Purpose |

|---|---|

| Form I | Creation and modification of Charge |

| Form II | Particulars of Satisfaction of Charge |

| Form III | Securitisation or Reconstruction of Financial Assets |

| Form IV | Satisfaction of Securitisation or Reconstruction of Financial Assets |

Fee Structure:

| Service | Fee |

|---|---|

| Creation/Modification — Loan up to ₹5 Lakh | ₹50 |

| Creation/Modification — Loan above ₹5 Lakh | ₹100 |

| Satisfaction of Security Interest | NIL |

| Search for information in CERSAI | ₹10 |

CERSAI 2.0

| Feature | Detail |

|---|---|

| Access | Requires a valid Digital Signature |

| Maker-Checker | No Maker-Checker concept — any authorised user can perform end-to-end transactions |

| Roles | Single User, Multiple Roles — more than one role may be assigned to one user |

Changes in CERSAI After SARFAESI Amendment 2020

| Section | Change |

|---|---|

| Section 19 | Omission of Section 27 — 30-day timeline for secured creditors to register with CERSAI is removed |

| Section 26 B | Attachment orders issued by any Government authority for recovery of Govt. dues may be filed with CERSAI |

| Section 26 C | Security interest or attachment orders filed with CERSAI shall have priority over any subsequent security interest created on such property. Filing with CERSAI shall be deemed to constitute a Public Notice from the date & time of filing |

| Section 26 D | Secured Creditors can enforce securities under SARFAESI Act only if the security interest is filed with CERSAI |

| Section 26 E | After registration with CERSAI by Secured Creditors, their dues will be paid in priority over Govt. dues |

Other authorities (besides secured creditors) that can now register their charge in CERSAI:

- A party having attachment order w.r.t. property from a civil court or any other authority

- Tax authority on issuance of attachment order for recovery of tax dues

- Any other authority of the Central/State Government or local authority on issuance of order for attachment of property for recovery of government dues

WARNING

If charge is not registered with CERSAI, the bank cannot sell the secured asset without intervention of the court. The security interest becomes unenforceable under SARFAESI Act.

Detailed Rules: Enforcement of Security Interest

Important Sections at a Glance

| Section | Provision |

|---|---|

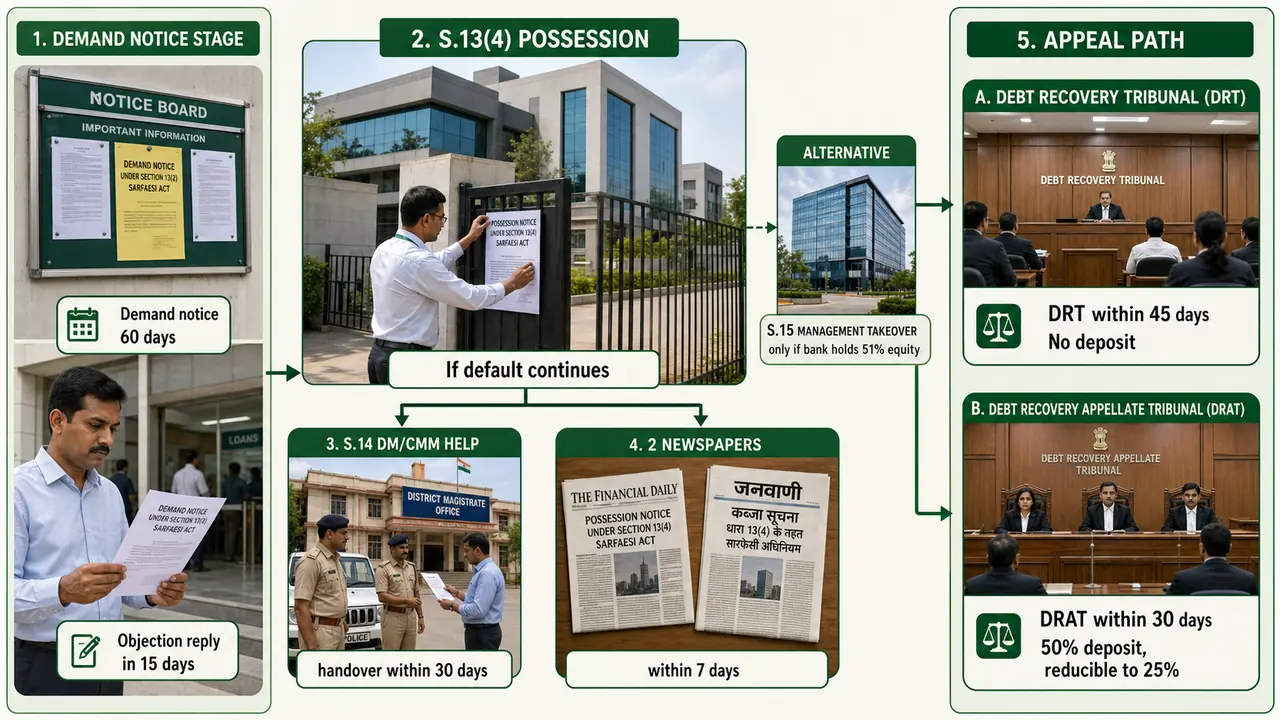

| S. 13(2) | Demand notice to borrower to repay the loan within 60 days |

| S. 13(4) | Possession notice to the borrower if he has not cleared his dues within 60 days |

| S. 17 | Borrower's Right by appeal against the authorized officer |

| S. 18 | Appeal to DRAT against DRT order |

| S. 19 | Right of borrower to receive compensation and costs in certain cases |

Enforcement of Security Interest — Steps

Upon a secured loan becoming NPA, the bank can take the following actions:

- Possession of secured assets

- Take over of the management

- Appoint person to manage the secured asset that is already taken over

- Notice to debtors who has dues to the borrower to pay directly to the bank as recovery of the secured assets

1. Possession of Security (Section 13)

The process involves two main stages: (1) Possession and (2) Sale.

A. The Chronological Process of Possession

Step 1: Demand Notice (Section 13(2)) The Bank serves a formal notice giving the borrower a strict 60 days to repay the entire due amount.

- Nature of the Notice (Case Law): In D. Ravichandran vs Indian Overseas Bank, the court clarified that this initial 60-day notice is merely a "show cause notice" (a preliminary warning). Therefore, courts generally refuse to interfere or block banks at this early stage.

- Strict 60-Day Rule (Case Law): In Sri Lakshmi Saraswathi Finance vs Govt. of India, the Madras High Court ruled that a bank absolutely cannot jump the gun. The secured creditor is strictly prohibited from taking possession or selling the asset even a single day before the full 60-day notice period expires.

Step 2: Borrower's Objection (Section 13-3A) If the borrower feels the NPA classification or amount is wrong, they can raise a formal representation/objection.

- The Bank is legally bound to consider it and reply with reasons for non-acceptance within 15 days.

- Note: The bank's reply does not give the borrower the right to immediately file a DRT application under section 17. However, the borrower can challenge the original notice in a Civil Court or High Court via a writ petition.

Step 3: Taking Possession (Section 13(4)) If the 60 days expire without repayment, the bank officially takes possession of the secured asset.

- District Magistrate (DM) Help (Section 14): If the borrower physically resists, the bank can submit a written request to the Chief Metropolitan Magistrate or District Magistrate. The DM must arrange police help to hand over possession within 30 days. The DM's actions during this process cannot be questioned in any court.

- Public Notice: For immovable property, the bank must publish a possession notice in 2 newspapers (one in local language) within 7 days of taking possession.

- Alternative - Management Takeover (Section 15): Instead of just taking the physical asset, the bank can completely take over the management of the borrower's business. This is only possible if the loan has been converted into equity and the bank holds at least 51% of the paid-up capital.

Step 4: First Appeal to DRT (Section 17(1)) If the borrower feels the bank's possession was illegal, they can appeal to the Debt Recovery Tribunal (DRT) within 45 days of the bank's action.

- No Deposit Required: Because the Constitution guarantees the fundamental right to be heard by a judge at least once, there is no prohibitive deposit barrier for this first appeal. Just standard court fees apply.

- DRT's Massive Power (Case Law): In the landmark Supreme Court case Mardia Chemical Ltd. vs. Union of India, the SC declared that an appeal to the DRT is an "original proceeding". This means the DRT has full power to review the bank's initial 60-day demand notice, and the borrower can legally challenge the exact amount the bank claims they owe.

- Bank's Rights During Appeal (Case Law): In M/s Lakshmi Mills Pvt Ltd. vs Indian Bank, the Madras HC made rules heavily favoring banks during DRT appeals:

- Just filing an appeal in the DRT does not automatically pause the bank's right to sell the asset. The bank can proceed unless the DRT specifically issues a stay order.

- The DRT has no legal power to force the borrower to deposit money as a condition to hear the case.

- The DRT cannot force the bank to hand the property back to the borrower as a temporary measure before the final verdict is reached.

Step 5: Second Appeal to DRAT (Section 18(1)) If either party is unhappy with the DRT's verdict, they can appeal to the Debt Recovery Appellate Tribunal (DRAT) within 30 days.

- Deposit Condition: To prevent frivolous delays, the borrower must deposit 50% of the due amount to file this appeal (the DRAT judge can reduce this to a minimum of 25%, but no lower).

2. Sale of Security Rules (Post-Possession)

How is Sale related to Possession? Under the SARFAESI Act, the Sale stage comes strictly AFTER the Possession stage. First, the bank must successfully take legal/physical possession of the property (Step 3 above). Only once the bank holds the asset can they proceed to auction or sell it to recover their money.

The most powerful feature of the SARFAESI Act is that it vests authority in creditors to both take possession AND sell these loan securities without ever filing a suit in court.

A. The Process of Selling the Asset

Step 1: The Pre-Sale Warning & Valuation Before selling the property, the bank must complete two critical steps:

- Notice to Borrower: Serve a final 30-day notice to the borrower, giving them one last chance to clear the dues before the asset is sold.

- Reserve Price: The bank sets a minimum acceptable sale price. The bank cannot sell the property below this reserve price unless the borrower explicitly gives their consent.

Step 2: Conducting the Sale The sale process must be managed by an Authorized Officer (who must hold the rank of Scale IV or above, or be specially authorized by the Board).

- Methods: It can be sold via Private Treaty or Public Auction.

- Public Notice: If selling via auction, a 30-day notice must be published in 2 newspapers.

Step 3: Auction Rules & Payment To prevent fake or non-serious buyers from delaying the recovery process, the RBI enforces strict payment rules:

- Immediate Deposit: The winning bidder must immediately pay 25% of the final sale amount on the spot.

- Final Settlement: The remaining 75% must be paid within 15 days.

- Penalty for Default: If the buyer fails to pay the 75% balance in time, the bank instantly forfeits their 25% deposit and the property goes back to auction.

B. Special Cases & Exceptions

- Consortium Accounts: Action requires consent of lenders holding at least 60% share by value.

- Simultaneous Proceedings (Case Law): The Supreme Court ruled in Transcore vs Union of India that a bank does not have to pause its recovery efforts just because a borrower filed a case in the DRT. The bank can proceed with the sale of the security simultaneously while the DRT proceedings are still ongoing.

C. Applicability & Scope

- Eligible Lenders: Applicable to Scheduled Commercial Banks, Co-operative Banks, Small Finance Banks, IFC, Asian Development Bank, and identified Housing Finance Companies.

- Co-operative Banks: Established under a State law or multi-State level societies come within the ambit of SARFAESI Act (SC order, May 2020).

- NBFCs: To be an eligible lender under SARFAESI, the NBFC must have a massive asset size of ₹100 crore and above.[1]

- Bond Market: Benefits of SARFAESI have been extended to the listed bond market in India. They are included as 'secured creditors'.

- NOT applicable to any Self Help Group (SHG).

NOTE

Minimum Loan Thresholds (Exam Critical) The law sets different minimum limits to protect smaller borrowers from brutal asset seizure:

- General Rule (Banks): Can invoke SARFAESI if outstanding is above ₹1 Lakh.

- MSE Protection Rule: If the borrower is a Micro or Small Enterprise (MSE), SARFAESI cannot be invoked if the due is below ₹10 Lakh.

- NBFC Rule: NBFCs can only invoke SARFAESI if the outstanding loan is ₹20 Lakh and above.

- The 20% Rule: No lender can invoke SARFAESI if the remaining debt is less than 20% of the original principal + interest (i.e., the borrower has already paid off 80%+ of the loan).

D. Agricultural Land Controversy

- The Exemption: Under Section 31(i), the SARFAESI Act is not applicable to agricultural land. Banks cannot auction it.

- The "Actual Use" Test (Supreme Court): The Supreme Court has ruled that just because land is listed as "agricultural" in government revenue records does not automatically exempt it. The courts look at the actual use of the land. If the land is being used for commercial purposes (like constructing residential apartments or a resort), the SARFAESI Act WILL apply, and the bank can auction it.

- The Plantation Crop Controversy: Is a massive commercial coffee or tea estate considered "agricultural land"?

- Karnataka High Court (2021): Ruled that plantation crops (like coffee, rubber, pepper) are NOT agricultural land for SARFAESI purposes, meaning banks can auction coffee estates.

- Kerala & Madras High Courts: Have previously taken the opposite view, stating they are agricultural and thus exempt from bank seizure.

- The Supreme Court has yet to make a final, unified ruling specifically on plantation crops, leaving it a highly debated legal grey area.

E. Ineligible Accounts (SARFAESI Actions NOT allowed)

- Small Loans & Paid-Off Loans: As explained in the thresholds above (below ₹1 Lakh, below ₹10 Lakh for MSEs, below ₹20 Lakh for NBFCs, or remaining debt < 20%).

- Unregistered Security: Security interest not registered with CERSAI.

- Agricultural Land: Cannot be sold under SARFAESI.

- Other Exclusions:

- Loans which are against Lien, Pledge, or Deposit (where CPC 1908 action not available).

- Limitation period expired (as per Limitation Act 1963).

- Vessels/Aircrafts.

- Hire purchase or lease arrangements.

G. What Types of Loan Charges are Permitted?

A fundamental concept for exams is knowing which types of security charges SARFAESI applies to:

- Permissible (Hypothecation, Mortgage, Assignment): SARFAESI is specifically designed for loans where the borrower currently holds physical possession of the asset (like a car loan or home loan), and the bank needs the legal power to go seize it.

- NOT Permissible (Pledge): You cannot use SARFAESI for pledged assets (like Gold Loans or Warehouse Receipts). Why? Because in a pledge, the bank already has physical possession of the gold/receipt in their vault. They don't need a special law to seize something they already hold!

- NOT Permissible (Time-Barred Debts): If the legal limitation period to recover the loan has expired (usually 3 years), SARFAESI cannot magically revive it.

Final Exam Review: The Complete SARFAESI Timeline

If you memorize one thing, memorize these deadlines:

- 7 Days: After seizing a property, the bank has 7 days to publish a "Possession Notice" in 2 leading newspapers (one must be in the local vernacular language).

- 15 Days: The bank's deadline to reply if the borrower submits a formal objection to the initial demand notice.

- 15 Days: The "Re-Auction" Notice. If the first property auction fails, the bank only has to give a shorter 15-day notice for the second attempt (not the full 30).

- 30 Days: The "Pre-Sale" Notice. After taking possession, the bank must give the borrower a 30-day warning before they officially auction the asset.

- 45 Days: The strict deadline for the borrower to appeal to the DRT after their asset is seized.

- 60 Days: The initial "Demand Notice" timeline (the bank's first warning: "Pay up within 60 days, or we seize the asset").

References

3 sources • [1] [2] [3]

References

Used for: Official gazette notification reducing the SARFAESI applicability threshold for NBFCs to Rs 100 crore asset size and Rs 20 lakh loan size.

Used for: RBI circular setting the Rs 300 Crore NOF target for ARCs with the March 2026 glide path deadline.

Used for: The legislative amendment that omitted Section 27 of the SARFAESI Act, effectively removing the statutory penalty fees for delayed CERSAI filings (enforced Jan 2020).

Summary Cheat Sheet

| Concept | Key Detail |

|---|---|

| SARFAESI Act Passed | December 17, 2002 |

| Legal Validity | Mardia Chemicals Case (Supreme Court) |

| Jurisdiction | Whole of India (Incl. J&K); Courts: DRT / DRAT |

| RDDBFI Act | 1993, Narasimham Committee-I, for debts ≥ Rs 20 lakh |

| DRTs / DRATs | 39 DRTs, 5 DRATs (Allahabad, Chennai, Delhi, Kolkata, Mumbai) |

| DRT Presiding Officer | Qualified as district judge, term 5 years, age 65 |

| DRAT Chairperson | HC judge qualification, term 5 years, age 65 |

| DRT under IBC | Adjudicating Authority; DRAT = Appellate (individual insolvency) |

| OTS Scheme | 1997; CDR Scheme: 2001 |

| ARC Minimum NOF | ₹300 Crore (glide path till March 2026) |

| ARC Capital Adequacy | 15% |

| ARC Investment | Min 15% in each Security Receipt issue |

| ARC Recovery Period | 5 Years (Extendable by 3 years) |

| ARC Chair | Must be independent director |

| ARC MD/CEO Tenure | Max 5 years, cannot continue beyond age 70 |

| ARC Audit Committee | Non-exec directors only, quarterly, quorum 3 |

| First ARC in India | ARCIL (ARC India Ltd) |

| ARC Acquisition | By issuing debt & debenture or agreement with FI |

| NPA Cash Payment | ARC gives 15% of value in cash |

| NARCL (Bad Bank) | 51% Public Sector Bank ownership |

| IDRCL | The operational debt management agency for NARCL |

| NARCL Structure | 15% Cash / 85% Security Receipts |

| Govt Guarantee | ₹30,600 Crore (Valid for 5 years) |

| CERSAI Established | 31.03.2011, under Sec 20(1) SARFAESI Act |

| CERSAI Ownership | Central Govt owns 51% |

| CERSAI Objective | Prevent multiple mortgage frauds |

| CERSAI Fees | ₹50 (≤5L) / ₹100 (>5L) / NIL (satisfaction) / ₹10 (search) |

| CERSAI Forms | Form I (Create/Modify), Form II (Satisfaction), Form III/IV (Securitisation) |

| CERSAI KYC Registry | 14-digit identifier; prefix "S" (small), "L" (simplified) |

| KYC Upload | Non-individual: within 18 days of opening |

| CERSAI Exemptions | Vehicles (→VAHAN), Agri Land, Bank Deposit, Govt Securities, Loans <₹1L |

| CERSAI 2.0 | Digital Signature required, No Maker-Checker |

| Sec 26D (2020) | SARFAESI enforcement only if filed with CERSAI |

| Sec 26E (2020) | Secured creditor dues paid priority over Govt dues |

| NBFC Asset Size | ≥ Rs 100 crore for SARFAESI eligibility |

| Bond Market | Listed bond market included as secured creditors |

| Co-op Banks | SC order May 2020 — included under SARFAESI |

| Agri Land (not used) | If not used for agriculture → SARFAESI applicable |

| Agri Land (plantation) | Karnataka HC: plantation crops (coffee) = NOT agricultural land |

| S. 13(2) Objection | Reply changed from 1 week → 15 days (Amendment) |

| S. 13(2) Challenge | Can challenge in Civil Court and High Court (writ) |

| Possession Notice | 60 Days (Reply to objection: 15 days) |

| DRT Appeal Period | 45 Days (No deposit required) |

| DRAT Appeal Period | 30 Days (Deposit 50%) |

| Sale Notice | 30 Days |

| Sale Payment Terms | 25% Immediate, 75% in 15 days |

| Consortium Consent | Min 60% by value |

| Auth. Officer | Scale IV or above |

| Transcore Case | Bank can sell asset simultaneously with DRT proceedings |

| Mardia Chemicals | DRT appeal is an "original proceeding", gives DRT full power |

| Ravichandran Case | Notice u/s 13(2) is a show cause notice |

| Lakshmi Mills Case | Bank right not auto-suspended on filing u/s 17 |

| CERSAI Penalty | No penalty for default in filing/modifying |

| Recovery Officer Appeal | Within 30 days, Tribunal order within 60 days |

| Applicability | All banks incl. Co-operative Banks & SFBs; NOT SHGs |

| NBFC Threshold | Outstanding dues ≥ ₹20 Lakh |

| MSE Threshold | Not applicable below ₹10 Lakh |

| Subsequent Sale | Notice of 15 days if auction fails |

| Possession Publish | 2 newspapers (1 vernacular) within 7 days |

| ARC Governance | Max ½ nominee directors, IDs ≥ half of board |

| ARC as Res. Applicant | Min NOF ₹1,000 Cr, max control 5 years |

| ARCIL | Est. 2002, HQ Mumbai, listed on BSE/NSE |

Lesson Doubts

Ask questions, get expert answers