⚖️ IBC

Comprehensive guide to Insolvency & Bankruptcy Code (IBC 2026), Institutional Infrastructure, Resolution Process, and Liquidation Waterfall.

Insolvency & Bankruptcy Code (IBC) 2016

Before 2016, India's recovery system was a fragmented mess. If a company went bankrupt, banks had to navigate a maze of overlapping laws (like SARFAESI, RDDBFI, and SICA) and multiple different courts. Promoters would use these legal loopholes to drag cases on for decades while continuing to run the dying company into the ground.

The IBC 2016 changed everything by introducing a single, unified law for all companies, partnerships, and individuals (excluding financial firms like banks).

But the biggest revolution of the IBC was its shift to a Creditor-In-Control model. Under the old laws, the defaulting promoters stayed in charge (Debtor-In-Control). Under the IBC, the moment a company defaults, the promoters are immediately kicked out, and the creditors take over the steering wheel to decide the company's fate.

4 Parts of the IBC

To keep things organized, the massive rulebook is split into four distinct parts:

Interactive Preview

Try the embedded exercise below. Full lesson access still requires Pro.

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

Insolvency & Bankruptcy Code (IBC) 2016

Before 2016, India's recovery system was a fragmented mess. If a company went bankrupt, banks had to navigate a maze of overlapping laws (like SARFAESI, RDDBFI, and SICA) and multiple different courts. Promoters would use these legal loopholes to drag cases on for decades while continuing to run the dying company into the ground.

The IBC 2016 changed everything by introducing a single, unified law for all companies, partnerships, and individuals (excluding financial firms like banks).

But the biggest revolution of the IBC was its shift to a Creditor-In-Control model. Under the old laws, the defaulting promoters stayed in charge (Debtor-In-Control). Under the IBC, the moment a company defaults, the promoters are immediately kicked out, and the creditors take over the steering wheel to decide the company's fate.

4 Parts of the IBC

To keep things organized, the massive rulebook is split into four distinct parts:

| Part | Subject |

|---|---|

| 1st Part | Definitions |

| 2nd Part | Process for Corporate Debtors (Companies & LLPs) |

| 3rd Part | Process for Individuals & Partnerships |

| 4th Part | Adjudicating Authorities (The Judges) |

The Two Possible Outcomes

When a case is admitted under the IBC, the clock starts ticking. The process always follows two strict stages:

- Resolution (Plan A): The creditors take over and try to rescue the company. They look for new buyers or restructuring plans to keep the business alive as a "going concern."

- Liquidation (Plan B): If the rescue fails, or if the statutory time limit expires, the company is forcefully dissolved. Its assets are stripped and sold off to pay back the creditors.

The Graveyard of Old Laws

The IBC didn't just add new rules; it completely killed off several obsolete laws to clean up the system.

Acts Completely Repealed (Killed) by IBC:

- Sick Industrial Companies Act (SICA) 1985 — The old, failed framework for reviving sick companies.

- Presidency Towns Insolvency Act 1909

- Provincial Insolvency Act 1920

Acts Overridden (Still exist, but IBC takes priority):

- SARFAESI Act 2002

- RDDBFI Act 1993 (The DRT Act)

- Companies Act 2013

Applicability & Statutory Thresholds

The IBC's jurisdiction encompasses a wide spectrum of legal entities, but applies different monetary thresholds for triggering insolvency proceedings.

Entities Covered (Section 2)

The Code extends to:

- Companies incorporated under the Companies Act (2013 or previous)

- Companies governed by any Special Act

- Limited Liability Partnerships (LLP Act 2008)

- Other corporate bodies notified by the Central Government

- Partnership Firms, Proprietorships, and Individuals

Minimum Default Thresholds for Initiation

| Entity Type | Adjudicating Authority | Minimum Default Threshold | Statutory Notes |

|---|---|---|---|

| Companies & LLPs | NCLT | ₹1 Crore (₹100 Lakh) | Increased from ₹1 Lakh on 24.03.2020 to prevent frivolous CIRP filings. The Govt retains power to raise this up to ₹10 Crore. |

| MSMEs (under PPIRP) | NCLT | ₹10 Lakh | Specialized Pre-Packaged Insolvency Resolution Process threshold. |

| Individuals & Partnerships | DRT | ₹1,000 | Applies to unlimited partnerships and proprietorship firms. |

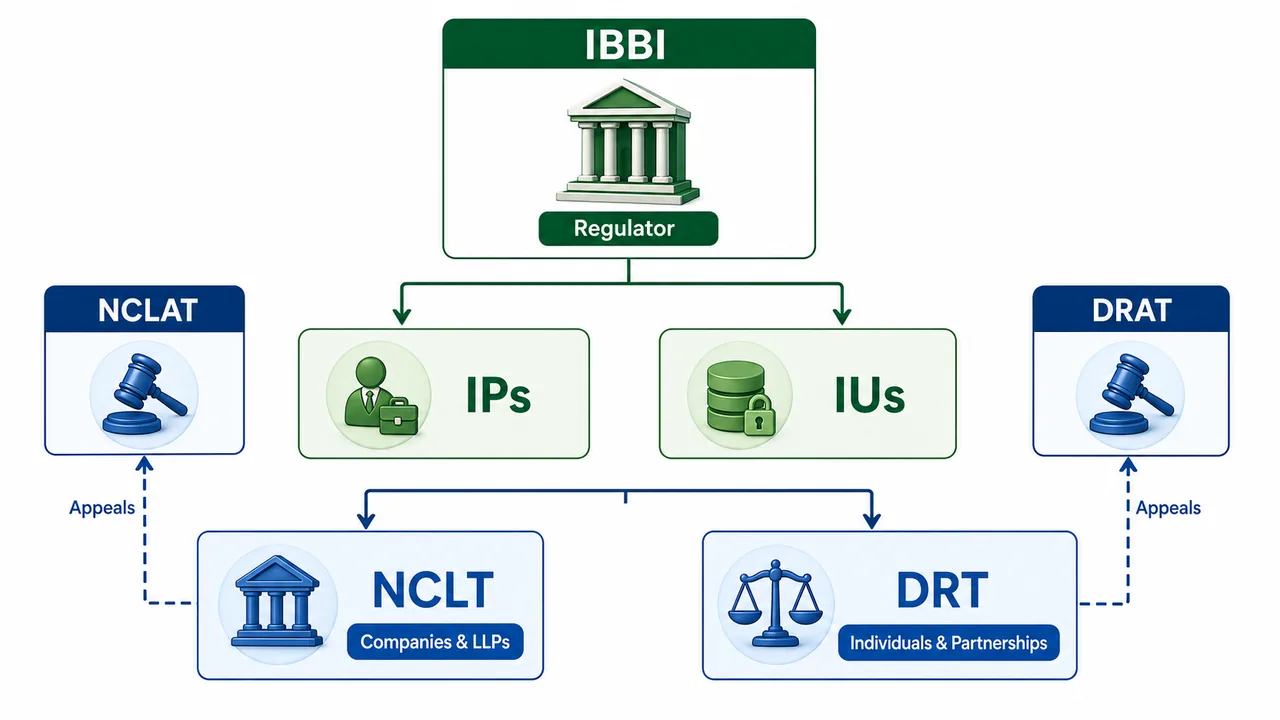

4 Tiers of Institutional Infrastructure

To execute its mandate, the Code establishes a robust, 4-pillar regulatory and judicial ecosystem.

Pillar 1: Insolvency & Bankruptcy Board of India (IBBI)

The apex regulatory body overseeing the entire insolvency ecosystem, including Insolvency Professional Agencies (IPAs), Insolvency Professionals (IPs), and Information Utilities (IUs).

- Established: 01.10.2016

- Composition: 10 members (including representatives from RBI and Ministries of Finance, Law, and Corporate Affairs).

- Leadership: Current Chairperson is Ravi Mital (Appointed February 2022).

- Core Function: Drafts regulations, registers professionals, and enforces compliance across the IBC ecosystem.

Pillar 2: Insolvency Professionals (IPs)

Licensed intermediaries responsible for executing the insolvency resolution process on the ground.

- Regulatory Body: Must be enrolled with an Insolvency Professional Agency (IPA) and registered with the IBBI.

- Operational Role: Upon admission of a Corporate Insolvency Resolution Process (CIRP), the Insolvency Professional (IP) takes over as the Interim Management, superseding the company's Board of Directors to run it as a "going concern."

- Accountability: They act under the strict supervision of the Committee of Creditors (CoC).

- Eligibility Criteria: Typically mandates 10+ years of experience as a Chartered Accountant, Company Secretary, Cost Accountant, or Advocate.

Pillar 3: Information Utilities (IUs)

Centralized repositories established under Section 210 to maintain secure, verifiable financial data.

- First IU in India: National e-Governance Services Ltd. (NeSL).

- Objective: To eliminate delays in proving debt default before tribunals by providing undisputed, digital evidence of liabilities.

- Statutory Obligations:

- Accept electronic submission of financial information from creditors.

- Authenticate and verify submitted data with the debtors.

- Safely store and disseminate certified default records to Adjudicating Authorities.

Pillar 4: Adjudicating Authorities (The Tribunals)

The judicial forums granted exclusive jurisdiction to hear and adjudicate IBC matters. Civil courts are strictly barred from interfering.

| Entity in Default | Adjudicating Authority (First Level) | Appellate Authority (Second Level) |

|---|---|---|

| Corporate Debtors (Companies & LLPs) | NCLT (National Company Law Tribunal) | NCLAT (National Company Law Appellate Tribunal) |

| Individuals & Partnerships | DRT (Debt Recovery Tribunal) | DRAT (Debt Recovery Appellate Tribunal) |

NOTE

Jurisdictional Exception: For Personal Guarantors to Corporate Debtors, the Adjudicating Authority is the NCLT (where the corporate debtor's case is proceeding), not the DRT. This ensures both the company and its guarantors are handled by the same judge simultaneously.

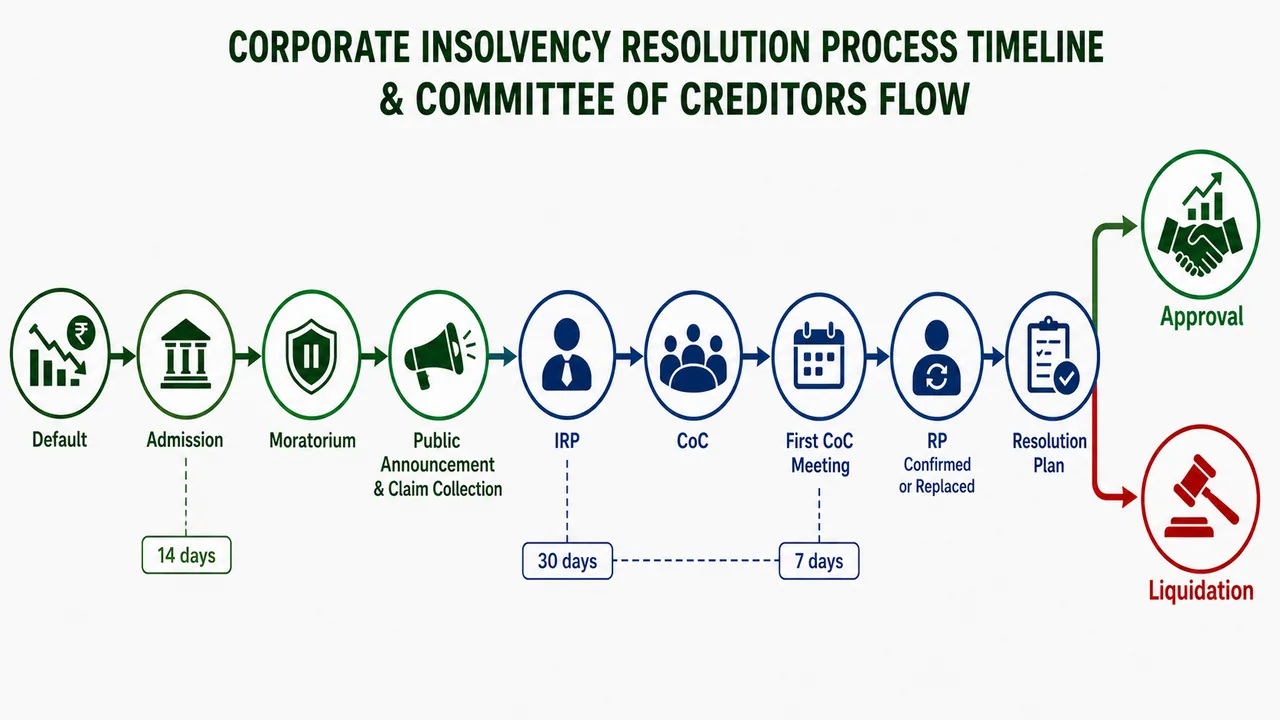

Corporate Insolvency Resolution Process (CIRP)

The primary goal of CIRP is not to kill the company, but to revive it. It operates as a strict two-stage mechanism:

- Resolution (Attempted Rescue): The creditors take control to assess if the business is viable. They invite "Resolution Applicants" to submit plans to restructure debt, inject capital, or buy the company as a going concern.

- Liquidation (Failure): If no viable resolution plan is found within the strict statutory deadlines, or if the creditors decide the company is beyond saving, the company is pushed into liquidation to sell its assets and pay off dues.

Statutory CIRP Timelines

To prevent the endless delays seen under older laws, the IBC enforces rigid timelines:

| Scenario | Statutory Time Limit |

|---|---|

| Normal CIRP | 180 days (NCLT can grant a one-time extension of 90 days = 270 days max) |

| Absolute Maximum Limit | 330 days (This is the hard stop, including all time spent in legal litigation/appeals) |

| Fast Track CIRP | 90 days (+ extension of 45 days = 135 days max) |

| NCLT Admission | The NCLT has exactly 14 days to either admit or reject a CIRP application. (Note: Before rejecting an application for errors, the NCLT must give the applicant 7 days to rectify the defects). |

Who Can Initiate CIRP?

Whenever a corporate debtor commits a default of at least ₹1 Crore, CIRP can be triggered by three specific parties:

- Section 7 (Financial Creditors): Banks or NBFCs who provided pure financial loans. They can file for CIRP immediately upon default.

- Section 9 (Operational Creditors): Suppliers, employees, or vendors who provided goods/services but weren't paid.

- Section 10 (Corporate Applicant): The defaulting company itself voluntarily admits it cannot pay its debts and asks the NCLT to take over.

WARNING

The 100 or 10% Rule (For Homebuyers & Debenture Holders) Previously, a single disgruntled homebuyer (who is legally classified as a financial creditor) could drag a massive real estate developer into bankruptcy over a minor delay. To stop this abuse, the law was amended: If the financial creditors belong to a "class" (like real estate allottees or bondholders), a single person cannot file for CIRP. The application must be filed jointly by at least 100 creditors of that same class, OR 10% of the total number of creditors in that class, whichever is lower.

The Operational Creditor Pre-Requisite (Section 8)

Unlike banks (who can file immediately under Section 7), Operational Creditors (like unpaid suppliers) must jump through an extra hoop before filing under Section 9:

- The 10-Day Warning (Demand Notice): The operational creditor must first serve a formal Demand Notice (along with a copy of the unpaid invoice) to the defaulting company.

- The Debtor's Window: The corporate debtor is given exactly 10 days from receipt of the notice to either:

- Pay the unpaid amount, OR

- Prove that there is a "pre-existing dispute" regarding the goods/services (e.g., the goods delivered were defective, which is why the invoice wasn't paid).

- Filing with NCLT: If the 10 days expire and the debtor has neither paid the money nor raised a valid pre-existing dispute, the operational creditor is legally cleared to file a Section 9 CIRP application before the NCLT.

The CIRP Process Flow

-

Occurrence of Default: Creditors (Financial/Operational) or Debtor can approach NCLT.

-

Admission & Moratorium: The NCLT has 14 days to review the application. Once they officially "admit" the case, a strict legal freeze called a Moratorium (or "calm period") instantly begins. During this time, no one can sue the company, banks cannot seize its assets, and critical services cannot be cut off. This gives the company total breathing room to attempt a rescue.

-

Public Announcement: The IRP issues a public advertisement announcing the insolvency and calls for the submission of claims (asking all banks, vendors, and employees who are owed money by the company to submit their formal proof of debt within 14 days).

-

Appointment of IRP: NCLT appoints an Interim Resolution Professional (IRP) to take complete charge of the corporate debtor.

- The Company Board is superseded (suspended). Why? Because the existing management drove the company into the ground, they cannot be trusted to run the rescue.

- Management vests solely with the IRP, who acts as the new temporary CEO.

- The IRP's critical task is keeping the company alive as a "going concern" (a living, working business) because a living company sells for much more to bidders than a dead, halted one. They even have the power to raise emergency fresh funds to keep the lights on.

- The IRP is granted 180 days to find a resolution, which can be extended by 90 days.

- If the IRP fails to find a resolution by then, the company is liquidated to pay the creditors.

Formation of Committee of Creditors (CoC)

- The interim resolution professional shall, after collation of all claims received against the corporate debtor and determination of the financial position, constitute a Committee of Creditors. (In step 3 above)

- The committee of creditors shall comprise all financial creditors.

- All decisions of the committee shall be taken by a vote of not less than 51% of voting share of the financial creditors.

- IRP shall constitute the CoC within 30 days from the date of appointment.

- IRP shall file a report certifying constitution of the committee to the Adjudicating Authority on or before expiry of 30 days from appointment.

First Meeting of CoC: IRP becomes RP

Once the CoC is formed, they must hold their first meeting within 7 days. The biggest agenda item at this meeting is deciding the fate of the Interim Resolution Professional (IRP).

Remember, the NCLT assigned the "Interim" RP temporarily. Now that the true owners (the creditors) are in charge, they get to vote on who runs the show:

- By a supermajority vote of 66% (by value of debt), the CoC must decide to either:

- Appoint the existing IRP as the permanent Resolution Professional (RP), OR

- Replace them and appoint a brand new RP.

From this point forward, the permanent Resolution Professional (RP) takes full control. They are responsible for managing the daily operations of the company, keeping it afloat, and actively finding a buyer to submit a resolution plan.

Moratorium During CIRP (Section 14)

Upon admission of the CIRP application, the NCLT immediately declares a Moratorium under Section 14 of the IBC. This functions as a statutory "calm period" or legal freeze designed to protect the corporate debtor's assets from fragmentation.

The core objective is to prevent a chaotic "run on the company" where multiple creditors individually file lawsuits or seize assets simultaneously. Such fragmentation would instantly destroy any chance of reviving the business as a going concern.

During the Moratorium period, the following actions are strictly prohibited:

- Institution of Lawsuits: No new or pending judicial proceedings, recovery actions, or debt executions can take place against the corporate debtor in any court.

- Asset Seizure: Creditors cannot enforce any security interest. Crucially, this means actions under the SARFAESI Act 2002 are completely suspended during CIRP.

- Transfer of Assets: The corporate debtor cannot encumber, alienate, or dispose of any of its assets or legal rights.

- Recovery of Property: Owners or lessors cannot recover any leased property currently in the possession of the corporate debtor.

TIP

Exceptions to Moratorium: The moratorium does not apply to the supply of essential goods and services (e.g., electricity, water) necessary to keep the company running as a going concern. Furthermore, the moratorium does not protect the Personal Guarantors of the corporate debtor—creditors can still initiate separate proceedings against them.

Withdrawal of CIRP (Section 12A)

Once the NCLT admits a case, the process belongs to all creditors. The original applicant cannot simply settle out of court with the debtor and quietly drop the case.

If the creditors decide they want to pull the plug and withdraw the CIRP application entirely (for example, if the promoters offer a massive out-of-court settlement), the NCLT will only allow it if an overwhelming supermajority of 90% of the CoC's voting share approves the withdrawal.

The Resolution Plan (The Rescue Phase)

The ultimate goal of the CIRP is to find a Resolution Plan—a concrete proposal to save the dying company. This process is managed entirely by the Resolution Professional (RP).

The 5-Step Process to Approval:

- The Information Memorandum: The RP creates a comprehensive financial profile of the company. Think of this as a detailed "sales brochure" that tells potential buyers exactly what the company owns, owes, and how it operates.

- Inviting Resolution Applicants: Potential buyers, investors, or restructuring firms (known as Resolution Applicants) review the Memorandum and submit their competing rescue proposals (Resolution Plans) to the RP.

- Examination by RP: The RP strictly vets all submitted plans to ensure they don't violate any laws (e.g., ensuring the applicant isn't a defaulting promoter banned from bidding under Section 29A).

- CoC Voting: The RP presents the legally valid plans to the Committee of Creditors. To be selected as the winning plan, it requires a supermajority consent of 66% of the creditors by value.

- NCLT Final Approval: The winning plan is submitted to the Adjudicating Authority (NCLT). If the NCLT confirms the plan is legally sound, they officially approve it.

What Happens After NCLT Approval?

- The strict statutory Moratorium instantly ends.

- The approved Resolution Plan becomes legally binding on everyone—the corporate debtor, employees, creditors, shareholders, and guarantors.

- The company is legally handed over to the new owners/management.

What does a Resolution Plan actually do? A successful plan might include:

- A "haircut" (creditors agreeing to write off a portion of the debt).

- Restructuring the loan repayment schedules.

- Converting outstanding debt into equity shares.

- A complete change of company management.

- Selling off non-core assets to raise immediate cash.

Persons Ineligible to File for CIRP (Section 11)

To prevent serial defaulters from abusing the legal protections of the IBC (like the moratorium freeze), Section 11 explicitly blocks certain entities from filing a CIRP application. A corporate debtor is not eligible if:

- Already in CIRP: They are currently undergoing an active resolution process.

- Recent Completion: They successfully completed a CIRP within the preceding 12 months.

- Serial Violator: The debtor (or a financial creditor) violated the terms of a previously approved resolution plan within the preceding 12 months.

- Already Doomed: A formal Liquidation Order has already been passed against them.

Appeals (Corporate Persons)

- Any person aggrieved by NCLT order may appeal to NCLAT within 30 days.

- Any person aggrieved by NCLAT order may appeal to Supreme Court within 45 days.

- Civil court has no jurisdiction in matters of NCLT & NCLAT.

Liquidation Process (Plan B)

Liquidation is the last resort. If the company cannot be saved, it is stripped down, and its assets are sold to pay off the creditors. When the NCLT passes a Liquidation Order, the Resolution Professional (RP) typically transitions into the role of the Liquidator.

The 4 Triggers for Liquidation (Section 33)

The NCLT will forcefully push the corporate debtor into liquidation under any of these four conditions:

- Time Expires: The CoC fails to submit an approved resolution plan within the absolute maximum deadline (330 days).

- CoC Decides to Kill It: The CoC votes (by a 66% supermajority) to liquidate the company at any point before a resolution plan is approved. (Note: This threshold was legally reduced from 75% to 66%).

- NCLT Rejection: The NCLT rejects the submitted resolution plan because it violates laws or fails on technical grounds.

- Plan Violation: A resolution plan was previously approved, but the corporate debtor contravened (broke) the agreed terms.

What Happens When Liquidation is Ordered?

Once the NCLT passes a formal Liquidation Order, the following legal changes instantly occur:

- The RP becomes the Liquidator: The Resolution Professional typically transitions into the role of the Liquidator to oversee the sale of assets. The Board of Directors remains completely suspended.

- New Public Announcement: The Liquidator makes a fresh public announcement asking all creditors to submit or update their claims within 30 days.

- Liquidation Estate Created: All assets of the company are legally pooled together to form a "Liquidation Estate" which the Liquidator holds as a fiduciary for the benefit of all creditors.

- Legal Freeze (Section 33(5)): A new moratorium applies. No legal suit or proceeding can be instituted against the company without explicit prior approval from the NCLT.

Priority in Liquidation (The Waterfall Mechanism)

When the Liquidator sells the company's assets, the cash generated cannot be distributed randomly. It must be paid out in a strict, non-negotiable mathematical order laid down in Section 53. This is called the "Waterfall Mechanism".

- CIRP & Liquidation Costs: Paid first. Why? Because nobody (lawyers, valuers, or the Liquidator) will work to salvage a dying company unless their professional fees are absolutely guaranteed.

- Secured Creditors & Workmen Dues (24 months preceding liquidation): The law rigorously prioritizes the lowest-level, vulnerable physical laborers ("workmen") alongside the highest-tier secured banks, ranking them above senior management and the government. They share this 2nd rank equally.

- Wages to Standard Employees (other than workmen) for the preceding 12 months.

- Unsecured Financial Creditors.

- Workmen's Dues (for any earlier period beyond the 24 months).

- Central & State Govt Dues (Taxes) and Secured Creditors (Unpaid Balance). Why is the Government so low? The IBC intentionally crushed the traditional "Crown Priority" (where the Govt historically took everything first). The IBC realizes that if the government always wins, commercial banks will never risk lending money to businesses.

- Remaining Debts & Dues (e.g., unsecured operational creditors).

- Equity Shareholders/Partners: They are the absolute last in line. (In almost all liquidations, the money runs out long before reaching this step, meaning shareholders lose everything).

NOTE

Exam Trick: The Waterfall Mechanism places Secured Creditors and Workmen (24m) at the exact same 2nd priority ranking. If the cash pool is insufficient to pay both fully, the money is distributed between them proportionately (pari-passu).

Voluntary Liquidation Process (Section 59)

Sometimes, a company is perfectly healthy (it has not committed any default), but the owners simply want to shut it down and distribute the remaining cash. This is called Voluntary Liquidation.

Mandatory Conditions:

- Declaration of Solvency: The majority of directors must sign a legal declaration stating they have made a full inquiry and the company is not being liquidated to defraud any person or evade taxes.

- Shareholder Approval: Within 4 weeks of the declaration, the shareholders must pass a Special Resolution (75% majority) to liquidate the company.

- Creditor Approval: If the company does have some outstanding debts, creditors representing 2/3rds in value must also approve the resolution within 7 days.

The Process: Once approved, a Liquidator is appointed to sell the assets, settle any remaining claims, and distribute the surplus to the shareholders. Finally, the NCLT passes an order for the formal Dissolution (legal death) of the company.

Fast Track CIRP (Section 55)

The standard 180-day CIRP can be too heavy and expensive for very small businesses. The Fast Track CIRP is designed for specific corporate debtors notified by the Government (typically small companies, startups, and unlisted companies with low asset values).

- Time Limit: The process must be completed within 90 days (NCLT can grant a one-time extension of 45 days = 135 days maximum).

Pre-Packaged Insolvency Resolution Process (PPIRP)

Introduced via an amendment in 2021, the PPIRP is a specialized, fast-tracked insolvency framework designed exclusively for Micro, Small, and Medium Enterprises (MSMEs).

- Objective: To resolve MSME insolvency faster while allowing the existing management to retain control ("debtor-in-possession" model), unlike normal CIRP where the IRP takes over.

- Minimum Default Threshold: ₹10 Lakh (Up to a maximum limit of ₹1 Crore).

- Time Limits: The entire PPIRP must be completed within 120 days from the date of admission.

- The Resolution Professional (RP) must submit the plan to NCLT within 90 days.

- NCLT has 30 days to approve or reject it.

Insolvency for Individuals & Partnerships (DRT Jurisdiction)

While the NCLT handles corporate bankruptcy, the Debt Recovery Tribunal (DRT) handles insolvency for individuals and unlimited partnerships. The minimum default threshold to trigger this is just ₹1,000.

The IBC provides two distinct tracks for individuals:

1. The Fresh Start Process (Debt Waiver for the Poor)

This is a unique, compassionate mechanism designed strictly for the lowest-income individuals. If they qualify, their qualifying debts are completely wiped clean (discharged) without them having to go through a grueling bankruptcy process.

A debtor can apply to the DRT for a "Fresh Start" only if they meet all these strict poverty thresholds:

- Income: Gross annual income does not exceed ₹60,000.

- Assets: Aggregate value of assets does not exceed ₹20,000.

- Debts: Total qualifying debts do not exceed ₹35,000.

- Housing: They do not own a dwelling unit (they don't own a home).

- Clean History: They are not an undischarged bankrupt and haven't used the Fresh Start process in the preceding 12 months.

2. Insolvency Resolution Process (For Standard Individuals)

For individuals who don't qualify for the extreme poverty thresholds of the Fresh Start process:

- The debtor (or creditor) applies to the DRT.

- The debtor works with a Resolution Professional to prepare a Repayment Plan.

- If the creditors approve the plan, the DRT makes it legally binding.

- If the creditors reject the plan (or the debtor fails to pay), the creditors can apply for a formal Bankruptcy Order to seize and sell the individual's assets.

References

2 sources • [1] [2]

References

IBBI Board Members & Chairperson

OfficialUsed for: Official IBBI board composition showing Ravi Mital as the current Chairperson (since Feb 2022).

Used for: Primary source for the ₹1 Crore CIRP threshold, the 330-day timeline, and the Pre-Packaged Insolvency Resolution Process (PPIRP) for MSMEs with a ₹10 Lakh threshold.

Summary Cheat Sheet

| Parameter | Detail |

|---|---|

| Min Default (Corporate) | ₹100 Lakh (₹1 Crore) — w.e.f. 24.03.2020 |

| Min Default (MSME PPIRP) | ₹10 Lakh |

| Min Default (Individual) | ₹1,000 |

| Regulator | IBBI (Est. 01.10.2016, 10 Members, Chair: Ravi Mital) |

| Adjudicating Auth. | NCLT (Companies) / DRT (Individuals) |

| Appellate Auth. | NCLAT (for NCLT) / DRAT (for DRT) |

| First IU | NeSL (National e-Governance Services Ltd.) |

| IBC Parts | 4 — Definitions, Corporate Debtors, Individuals, Adjudicating Authorities |

| Acts Repealed | Presidency Towns Insolvency, Provincial Insolvency, SICA |

| Related Pre-IBC Acts | SARFAESI (2002), RDDBFI (1993), SICA (1985), Companies Act (1956/2013) |

| NCLT Admission | Within 14 days |

| Demand Notice Response | 10 days (for operational creditors) |

| Defect Rectification | 7 days notice before rejection |

| IRP Report to NCLT | Within 30 days of appointment |

| First CoC Meeting | Within 7 days of constitution |

| CoC General Decisions | 51% voting share |

| RP Appointment | 66% vote by value in first CoC meeting |

| CIRP Time Limit | 180 Days + 90 Days Ext = 270 Days |

| Total Limit | 330 Days (incl. litigation) |

| Fast Track Limit | 90 Days + 45 Days Ext = 135 Days |

| PPIRP Limit (MSME) | 120 Days (90 days for plan + 30 days NCLT approval) |

| CoC Voting for Plan | 66% by value for Plan Approval |

| Withdrawal from CIRP | 90% voting share of CoC |

| Liquidation Trigger (CoC) | 66% majority of CoC |

| Voluntary Liquidation | Special resolution within 4 weeks + 2/3 in value creditor approval |

| Appeal: NCLT → NCLAT | Within 30 days |

| Appeal: NCLAT → Supreme Court | Within 45 days |

| Home Buyer Filing | Min 100 allottees or 10% (whichever less) |

| Cannot Re-file CIRP | Within 12 months of previous completion/violation |

| Fresh Start (Income) | Max ₹60,000 annual income |

| Fresh Start (Assets) | Max ₹20,000 asset value |

| Fresh Start (Debts) | Max ₹35,000 qualifying debts |

| Fresh Start (Cooldown) | 12 months from previous fresh start order |

| Liquidation Priority | Cost → Secured/Workmen(24m) (pari-passu) → Employees(12m) → Unsecured → Workmen(earlier) → Govt/Secured(balance) → Remaining → Equity |

Lesson Doubts

Ask questions, get expert answers