📋 Financial Statements Overview

Understanding financial statements, their role in banking, accounting concepts, standards (AS & Ind AS), and format under Companies Act 2026.

What is a Financial Statement?

A Financial Statement (FS) is a formal, legally required record that shows the financial activities and overall financial position of a business, firm, or individual over a specific period of time.

At their core, these statements tell you exactly where a company stands financially by breaking down four key pillars:

- Assets: How much the business owns (e.g., cash, factories, inventory).

- Liabilities: How much the business owes (e.g., bank loans, unpaid bills).

- Income (Revenue): How much money the business has earned.

- Expenses: How the business has used its money to operate.

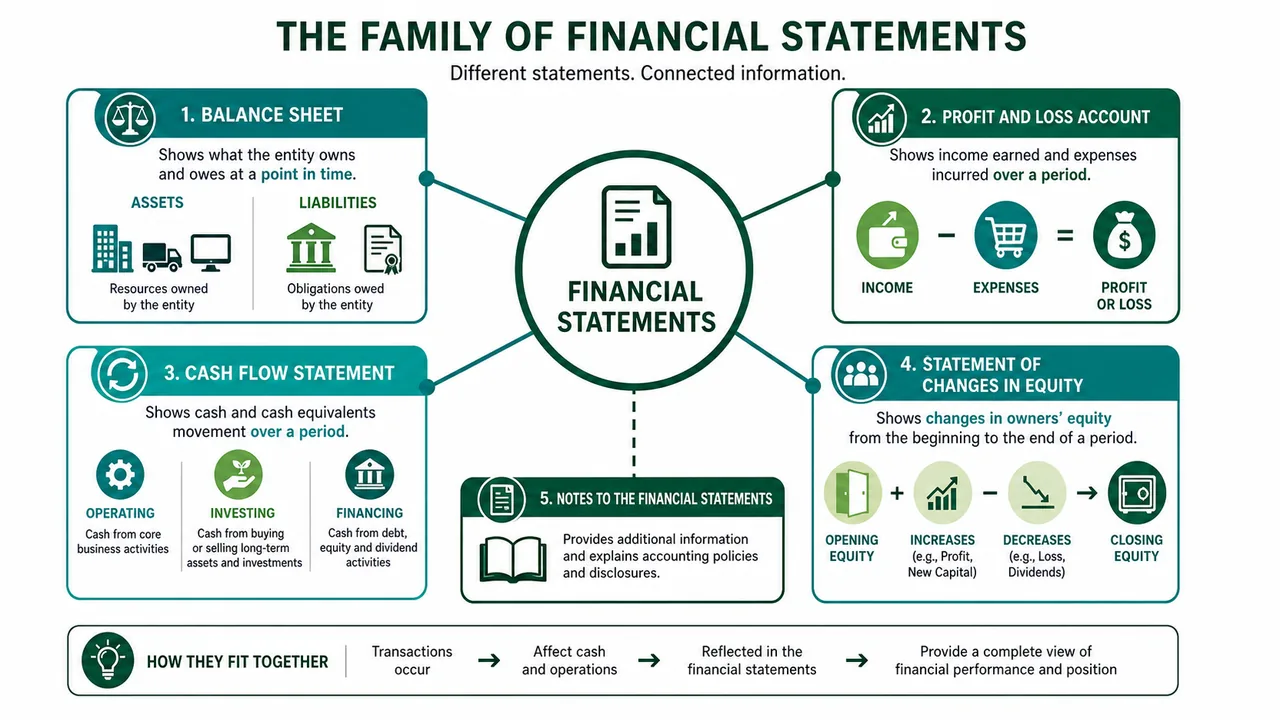

The 5 Types of Financial Statements

To get a complete picture, a company must prepare a "family" of five interconnected statements:

- Balance Sheet: Shows the exact financial position (Assets vs Liabilities) as at the end of the financial year.

- Profit and Loss (P&L) Account: Shows the Income and Expenditure over the entire period. (Note: For NGOs and not-for-profit entities, this is called an Income & Expenditure Account).

- Cash Flow Statement: Tracks the physical movement of actual cash and cash equivalents in and out of the business.

- Statement of Changes in Equity: Tracks any changes in the owners' or shareholders' equity, if applicable.

- Explanatory Notes: Detailed annexures attached to, and forming a part of, the above statements to explain accounting policies and breakdown the numbers.

NOTE

Pro Content Locked

Upgrade to Pro to access this lesson and all other premium content.

₹99 charged monthly · Cancel anytime

- All Agriculture & Banking Courses

- AI Lesson Questions (100/day)

- AI Doubt Solver (50/day)

- Glows & Grows Feedback (30/day)

- AI Section Quiz (20/day)

- 22-Language Translation (100/day)

- Recall Questions (20/day)

- AI Quiz (15/day)

- AI Quiz Paper Analysis (100/day)

- AI Step-by-Step Explanations (100/day)

- Spaced Repetition Recall (FSRS)

- AI Tutor

- Immersive Text Questions

- Audio Lessons — Hindi & English

- Mock Tests & Previous Year Papers

- Summary & Mind Maps

- XP, Levels, Leaderboard & Badges

- Generate New Classrooms

- Voice AI Teacher (AgriDots Live)

- AI Revision Assistant

- Knowledge Gap Analysis

- Interactive Revision (LangGraph)

🔒 Secure via Razorpay · Cancel anytime · No hidden fees

What is a Financial Statement?

A Financial Statement (FS) is a formal, legally required record that shows the financial activities and overall financial position of a business, firm, or individual over a specific period of time.

At their core, these statements tell you exactly where a company stands financially by breaking down four key pillars:

- Assets: How much the business owns (e.g., cash, factories, inventory).

- Liabilities: How much the business owes (e.g., bank loans, unpaid bills).

- Income (Revenue): How much money the business has earned.

- Expenses: How the business has used its money to operate.

The 5 Types of Financial Statements

To get a complete picture, a company must prepare a "family" of five interconnected statements:

- Balance Sheet: Shows the exact financial position (Assets vs Liabilities) as at the end of the financial year.

- Profit and Loss (P&L) Account: Shows the Income and Expenditure over the entire period. (Note: For NGOs and not-for-profit entities, this is called an Income & Expenditure Account).

- Cash Flow Statement: Tracks the physical movement of actual cash and cash equivalents in and out of the business.

- Statement of Changes in Equity: Tracks any changes in the owners' or shareholders' equity, if applicable.

- Explanatory Notes: Detailed annexures attached to, and forming a part of, the above statements to explain accounting policies and breakdown the numbers.

NOTE

Exemption under Companies Act, 2013: A One Person Company (OPC), Small Company, Dormant Company, and recognized Start-up Company are legally exempted from preparing a Cash Flow Statement.

Why? Preparing an accurate cash flow statement is a complex, expensive accounting task (it requires strictly reconciling accrual accounting back to pure cash movements). To promote "ease of doing business," the government granted this exemption to drastically reduce the compliance burden and accounting costs for tiny, early-stage, or inactive businesses.

Why Do We Analyze Them? (The Banker's Role)

Financial Statements form the absolute backbone of bank loan appraisal. However, reading the statements is not enough; a credit officer must analyze them to assess the past performance and future viability of the business. Here is why analysis is required:

- Inherent Bias: Financial Statements are prepared by the company's management, not by independent auditors.

- Auditors Only Opine: While independent auditors check the statements, they do not make business decisions; they merely give an opinion.

- Different Objectives: Different users (banks vs tax agencies) have different objectives, meaning the raw data must be customized for decision-making (not just compliance).

- True Interpretation: Because of this, financial analysis is not duplication, but interpretation of the numbers.

What Bankers Look For

When a bank analyzes these statements using ratio and trend analysis, they are checking the borrower's risk levels across three critical survival metrics:

- Liquidity: Can the borrower easily pay their short-term bills? (Short-term payment ability).

- Solvency: Can the borrower survive their long-term debt? (Long-term survival).

- Profitability: Does the business actually have the earning capacity to repay the bank? (Earning capacity).

Who Else Uses Financial Statements?

Because these statements reveal the true health of a company, different groups use them for very specific objectives:

- Lenders (Banks): To assess the repayment capacity of the borrower.

- Creditors (Suppliers): To check short-term solvency (will I get paid if I supply raw materials on credit?).

- Investors & Shareholders: To evaluate their potential return on investment and the associated risks.

- Government Departments & Agencies: To ensure the company is paying its fair share of taxation and complying with the law.

- Rating Agencies: To assign official credit ratings to the company's debt.

- Customers: To judge the long-term stability of the company (e.g., will this company still be around to honor my 10-year warranty?).

- Employees: To gauge job security and future salary growth prospects.

- General Public: To assess the overall credibility and economic impact of large corporations.

- Analysts: For professional evaluation and industry comparisons.

Verifying the Genuineness of Financial Statements

Borrowers often forge or inflate their financial statements to secure larger bank loans. Therefore, a credit officer can never blindly trust a printed Balance Sheet handed to them by a customer. They must follow a strict verification protocol:

- The MCA Cross-Check (Primary Check): The officer must download the official financial statements directly from the Ministry of Corporate Affairs (MCA) portal and cross-check them against the physical copy provided by the borrower. This ensures the borrower hasn't handed the bank a "cooked" version while submitting the real, weaker version to the government.

- The CA Direct Confirmation (Fallback): If the company is a partnership/proprietorship (which do not file on the MCA portal), or if the latest data isn't uploaded yet, the officer must contact the Chartered Accountant (CA) directly. The bank must receive an independent confirmation straight from the CA's official email/fax stating, "Yes, I audited this exact document."

- Regulatory Matching: Major figures (like Sales Revenue) in the P&L Account must be strictly cross-verified against the borrower's other statutory returns (like GST returns and Income Tax filings). If a borrower claims ₹10 Crore in sales to the bank but only paid GST on ₹2 Crore, it is a massive red flag for fraud.

WARNING

The golden rule for Credit Officers: Never accept financial statements solely from the borrower's hands without an independent third-party verification (MCA portal, GST returns, or direct CA confirmation).

Reading Beyond the Numbers

A common mistake made by junior credit officers and investors is looking only at the raw numbers in the Balance Sheet and P&L. However, financial statements should never be read in isolation.

The raw numbers only tell you what happened. To understand why it happened, and whether those numbers can actually be trusted, you must read the accompanying reports.

1. The Directors' Report (Management's Perspective)

The Directors' Report is essentially management's narrative to the shareholders. It provides the "story" behind the numbers. While it can sometimes be overly optimistic, it contains critical information that a simple Balance Sheet cannot show.

When analyzing a Directors' Report, a credit officer should specifically look for:

- Future Growth Strategy: What are the company's expansion plans, and how do they plan to fund them? Are they taking on too much risk?

- Dividend Declarations: Is the company aggressively paying out cash to owners instead of keeping it in the business to pay off bank loans?

- Directors' Responsibility Statement: A mandatory legal declaration where the directors take personal accountability. They must confirm they followed proper accounting standards, maintained adequate internal controls to prevent fraud, and that the company is a "Going Concern" (meaning it is not on the verge of bankruptcy).

TIP

The Directors' Report is where management explains their successes and justifies their failures. Always read it with a critical eye, as it represents the company's own biased perspective. The numbers must then be cross-verified using the Auditor's Report.

2. The Auditor's Report (The Independent Check)

The Auditor's Report is the ultimate cross-check against management's biased Directors' Report. However, it is not an absolute guarantee that no fraud exists. It is simply an independent professional opinion stating whether the financial statements present a "true and fair view" of the company's health.

When a credit officer reads an Auditor's Report, the first thing they look for is the Opinion Type:

- ✅ Unqualified Opinion (Clean): The auditor found no major issues. The financials are accurate. (Banks want to see this).

- ⚠️ Qualified Opinion: The financials are mostly accurate, except for a few specific issues the auditor has explicitly listed. (The bank will heavily investigate these specific exceptions).

- ❌ Adverse Opinion: The financials are completely misrepresented, misleading, or do not follow accounting standards. (The bank will instantly reject the loan).

- ❓ Disclaimer of Opinion: The company refused to give the auditor access to their records, so the auditor refuses to give an opinion. (Massive red flag for fraud).

What is CARO 2020?

The Companies (Auditor's Report) Order, 2020 (CARO) is a mandatory legal questionnaire attached to the main report. Instead of just giving a general opinion, CARO forces the auditor to answer 21 highly specific questions that banks care deeply about. For example:

- Has the company defaulted on any existing bank loans?

- Have the fixed assets and inventory actually been physically verified, or are they just fake numbers on paper?

- Are there any illegal, unrecorded "benami" transactions?

TIP

Who is Exempt from CARO? To reduce compliance burdens, the government exempts certain companies from having to undergo CARO reporting. CARO is NOT applicable to:

- Banking & Insurance Companies (heavily regulated by RBI/IRDAI already)

- Section 8 Companies (Not-for-profit NGOs)

- One Person Companies (OPC) and Small Companies

Core Accounting Concepts

Instead of trying to memorize dictionary definitions, you need to understand how these concepts actually affect a company's balance sheet in the real world.

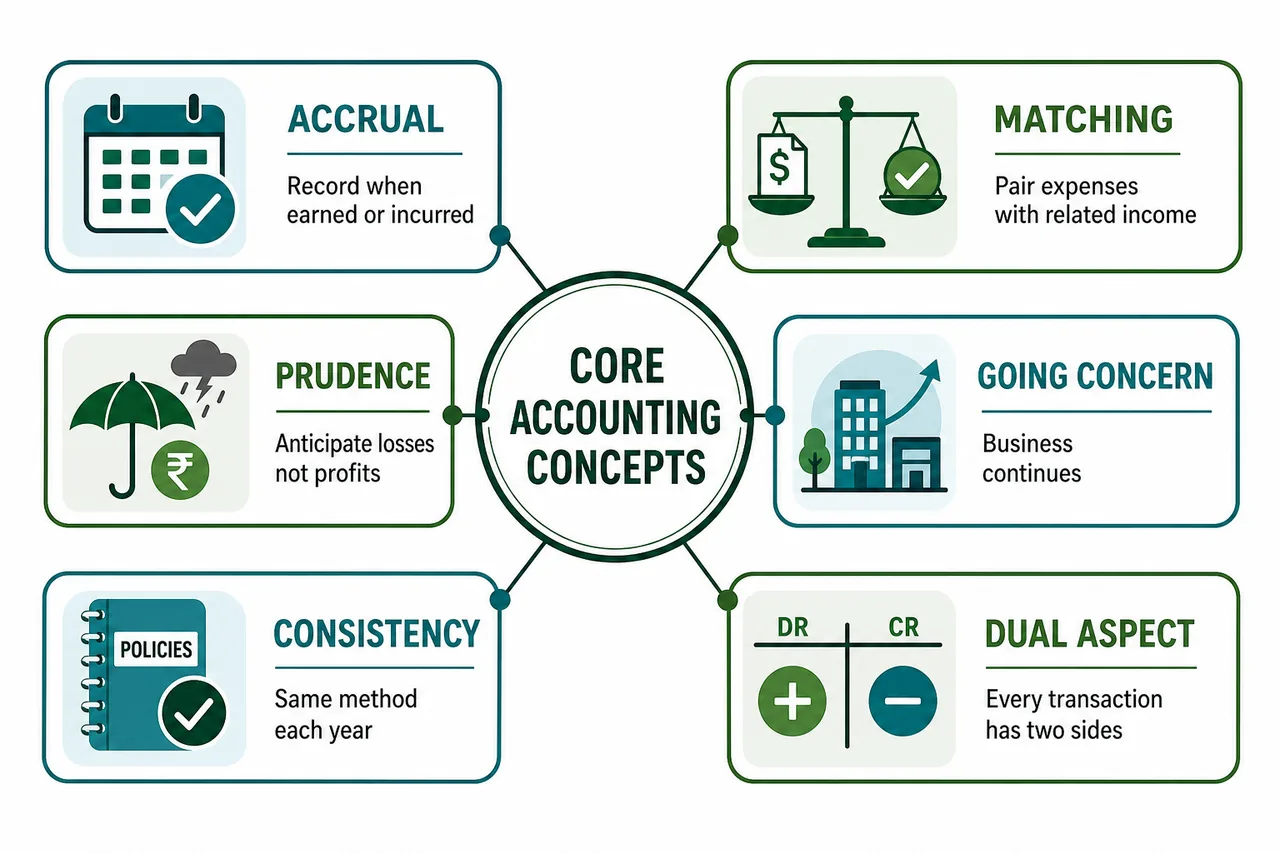

The 3 Fundamental Assumptions (AS-1)

Under Accounting Standard 1 (AS-1), if a company doesn't state otherwise, it is assumed they strictly followed these three rules:

- Going Concern: The assumption that the business will run forever. (Why it matters: If a business is about to shut down, its assets must be valued at "fire-sale" liquidation prices, not their original cost).

- Consistency: The company uses the exact same accounting policies year after year. (Why it matters: So investors can accurately compare 2024's profits to 2023's profits without being tricked by a formula change).

- Accrual: Income and expenses are recorded when they occur, not when cash physically changes hands. (Example: Recording a sale today even if the customer promises to pay next month).

Other Highly Tested Concepts

- Prudence (Conservatism): Anticipate no profit, but provide for all possible losses. This is the most important concept for bankers—it's the exact reason why banks are forced to create "provisions" for NPAs the moment they suspect a loan might go bad, long before the money is actually lost.

- Separate Entity: The business and its owners are totally separate legal persons. If the founder buys a personal car with company money, it is recorded as a loan to the founder, not a business expense.

- Matching Principle: If you record revenue this year, you must record all the expenses it took to generate that revenue in this same year.

- Dual Aspect (Double-Entry Bookkeeping): Every transaction has an equal and opposite Debit and Credit, affecting at least two accounts. This is why the Balance Sheet always balances! ()

- Historical Cost: Assets are recorded on the balance sheet at their original purchase price, not their current market value. (Example: Land bought in 1990 for ₹1 Lakh is still shown as ₹1 Lakh today, even if it's worth ₹50 Crore).

- Realisation: You only recognize revenue when the legal right to receive it is established (the sale is finalized), not just when someone hands you an advance payment.

- Money Measurement: Only transactions that can be measured in money are recorded. (e.g., A CEO's brilliant leadership is valuable, but it cannot be quantified in rupees, so it's not on the balance sheet).

- Stable Monetary Unit: The value of money is assumed to remain stable over time (inflation is largely ignored in historical accounting).

- Accounting Period: The infinite life of a business is divided into specific, artificial time periods (like a 12-month financial year) to measure performance regularly.

- Full Disclosure: All material (significant) information that could affect a lender's or investor's decision must be fully disclosed in the financial statements or its footnotes.

The Accounting Rulebook: AS and Ind AS

If every company calculated profits using their own unique logic, the stock market would collapse. To prevent chaos, the government enforces strict rulebooks.

What are Accounting Standards (AS)?

Accounting Standards (AS) are the written, legally-binding policy documents that dictate exactly how a company must recognize, measure, and present its financial transactions.

(Note: While Accounting Standards are the broad rules, Accounting Policies are the specific practices chosen by a company to apply those rules).

Objective of Accounting Standards:

- To reduce accounting alternatives

- To promote uniformity and comparability

- To provide reliable information for economic decision-making

How are they created in India? (The 3-Step Process):

- ICAI (Institute of Chartered Accountants of India) drafts and recommends the standard.

- NFRA (National Financial Reporting Authority) rigorously examines and approves it.

- MCA (Ministry of Corporate Affairs) officially notifies it into law for all companies.

The Shift to Global Rules: Ind AS

Historically, Indian companies followed local rules. However, as Indian companies started seeking massive foreign investment, foreign investors complained that Indian accounting rules were too different from global standards.

The global gold standard is IFRS (International Financial Reporting Standards). Instead of blindly copy-pasting IFRS, India adopted a "converged" version—we took IFRS and tweaked it slightly to fit the Indian legal and economic environment. This customized Indian version of IFRS is called Indian Accounting Standards (Ind AS).

Who MUST follow Ind AS?

From 1st April, 2017, the government mandates Ind AS for all major companies. It is legally required for:

- All Listed Companies (irrespective of their net worth).

- Large Unlisted Companies (Net worth of ₹250 Crore or more).

- All subsidiaries, holding companies, and joint ventures of the above companies.

(Note: Companies listed on SME Exchanges, Banks, and Insurance companies are currently exempt or have separate, delayed rollout phases for Ind AS).

Important Accounting Terminology

To read financial statements like a pro, you must know these specific terms:

1. GAAP (Generally Accepted Accounting Principles)

GAAP isn't a single law; it is the overall collective framework of all accounting standards, rules, and conventions that companies in a specific country follow. (e.g., US GAAP vs Indian GAAP).

2. Capital Expenditure (CapEx) vs Revenue Expenditure (OpEx)

- CapEx (Capital Expenditure): Money spent to buy or upgrade a long-term asset (e.g., Buying a new factory machine). It goes on the Balance Sheet as an asset and is slowly depreciated over multiple years.

- OpEx (Revenue Expenditure): Day-to-day money spent to run the business (e.g., Paying electricity bills or worker salaries). It goes on the P&L Account and is fully deducted from this single year's profits.

3. Consolidated Financial Statements

If a parent company (like Reliance Industries) owns several smaller subsidiary companies (like Jio or Reliance Retail), they cannot hide the losses of their subsidiaries. They must publish a "Consolidated" financial statement that combines the parent and all subsidiaries into one massive, single economic entity.

The Legal Format of Financial Statements

The Companies Act, 2013 legally prescribes exactly how a company's Balance Sheet and Profit & Loss Account must look.

Statutory Requirements (Schedule III)

- The Format: Financial statements must be prepared in the exact format prescribed under Schedule III of the Companies Act.

- True and Fair View: They must present a perfectly "true and fair view" of the company's state of affairs. (Note: If they do not, there are severe legal and financial repercussions for the MD, CFO, and the Auditor, including the auditor losing their ICAI membership).

- Accounting Standards: They must strictly comply with the Accounting Standards notified under Section 133.

WARNING

The Deviation Rule: If a company's financial statements do not comply with the applicable Accounting Standards, they cannot just hide it. The company is legally required to explicitly disclose:

- The exact deviation from the standard.

- The reasons why they deviated.

- The financial impact that the deviation caused.

Exceptions to Schedule III

Certain companies are governed by their own special sector regulators and therefore have their own separate formats. Schedule III does NOT apply to:

- Insurance Companies (regulated by IRDAI)

- Banking Companies (regulated by RBI)

- Electricity Companies

- Any other company governed by a special law

(Note: The mandatory statements to be filed are the Balance Sheet, P&L, Cash Flow (AS-3), Statement of Changes in Equity, and Explanatory Notes/Reports on Subsidiaries).

The Financial Year (Accounting Period)

In India, the standard Financial Year runs for exactly 12 months, ending on 31st March. However, there are two highly-tested special exceptions:

- New Companies (The 15-Month Rule): If a company is founded very late in the year (between 1st January and 31st March), its first financial year ends on 31st March of the following year. This means their first financial statement can cover up to 15 months.

- Foreign Subsidiaries: A wholly-owned Indian subsidiary of a foreign parent company can change its financial year-end (e.g., to December 31st) to perfectly match its parent company. However, this requires explicit approval from the NCLT (National Company Law Tribunal).

What is a Balance Sheet? (Three Perspectives)

A Balance Sheet is the ultimate summary of a business, but different professionals view it differently:

1. The Accountant's Perspective

To an accountant, it shows the Sources of Funds (Liabilities & Owner's Equity—where the money came from) and the Uses of Funds (Assets—where the money is currently invested).

2. The AICPA Perspective

The American Institute of Certified Public Accountants (AICPA) simply defines it as a "list of balances in the books" after all operational accounts are closed. It shows exactly what a company owns (Assets) and what it owes (Liabilities).

3. The Banker's Perspective (The "Snapshot")

To a credit officer, a Balance Sheet is a financial snapshot taken at one specific second in time (e.g., exactly at midnight on March 31st). It shows the financial health of the borrower at that exact moment.

NOTE

The Entity Concept Check: A Balance Sheet represents the business, not the individual owners. This is why it includes "Equity" as a liability (the business owes the owners their capital back). However, partnerships and sole proprietorships can maintain separate accounts for the business, distinct from the owner's personal money.

The Credit Officer's Job: Balance Sheet Analysis

When a borrower hands a bank their financial statements to request credit, the bank doesn't just read them—they tear them apart to examine the company's viability, financial strength, and objective repayment ability (Credit Risk).

The Two Core Survival Checks

- Liquidity Assessment (Short-Term): Can the company pay its bills this month? (Are there enough current assets to cover short-term payment abilities?).

- Solvency Assessment (Long-Term): Can the company survive the next 10 years? (Is the overall long-term debt load manageable?).

Critical Criteria for Credit Appraisal

Beyond survival, the credit officer appraises four pillars:

- Financial Stability (Solvency and leverage).

- Profitability Analysis (Are their margins growing or shrinking?).

- Cash Flow & Debt Servicing Potential (Do they actually generate enough hard cash to pay the monthly EMI?).

- Working Capital Adequacy (Do they have enough money to buy raw materials and keep the factory running?).

Methods of Analysis

To evaluate these pillars, bankers use specific documents and three primary analytical techniques:

A. Key Documents to Review:

- Auditor's Report: To get an independent opinion on the "true and fair view" of the financials.

- Management Report (Directors' Report): To read management's own commentary on financial performance.

- Statement of Changes in Equity: To track any movements in the shareholders' equity over the year.

B. The 3 Analytical Techniques:

- Comparative Balance Sheet: Comparing two or more years side-by-side to identify absolute changes.

- Common Size Balance Sheet: Expressing every single item as a percentage of Total Assets (e.g., "Inventory is 40% of our total assets") to quickly understand the company's structure.

- Trend Analysis: Looking at data across multiple years to see the long-term direction and magnitude of changes.

What Bankers Expect Over Time

When looking at trend analysis, a banker expects to see a healthy, growing company:

- The balance sheet should generally grow as accumulated profits add to the company's capital.

- Sales and profitability should show an increasing trend.

- There should be steady machinery additions (CapEx), leading to proper depreciation adjustments.

- Previous bank loan repayments should be clearly accounted for and reducing over time.

Spotting Red Flags (Factors Impacting the Balance Sheet)

If the balance sheet is shrinking or sales are lower, the credit officer must find out why. Is it due to a general revenue decline? Massive bad debts? Internal operating inefficiencies? Or temporary external factors?

The ultimate goal of analyzing these changes is to predict how the borrower's future financial health will affect their ability to repay the bank's loan.

Summary Cheat Sheet

| Concept / Topic | Key Details / Explanation |

|---|---|

| Financial Statement (FS) | Formal record of financial activities and position; shows assets, liabilities, income, expenses |

| 5 Types of FS | Balance Sheet, P&L Account, Cash Flow Statement, Statement of Changes in Equity, Explanatory Notes |

| Cash Flow Exemption | One Person Company, Small Company, Dormant Company, and Start-up Company may not include Cash Flow Statement |

| Role in Bank Loans | Backbone of loan appraisal; assess liquidity, solvency, profitability, and repayment capacity |

| Purpose of Analysis | Analysis is interpretation of the company's health, not just mere duplication of the numbers |

| FS are Prepared by | Management (not auditors); auditors only give an opinion |

| Users of FS | Lenders, creditors, investors, govt agencies, rating agencies, customers, employees, public, analysts |

| Genuineness Verification | Cross-check with MCA website; if not on MCA, get independent confirmation from CA; verify with statutory returns |

| FS Must Be Read With | Auditors' Report and Explanatory Notes |

| Directors' Report | Covers financial highlights, future plans, dividend, going concern, internal controls, compliance |

| Auditors' Report | Independent opinion; certifies true and fair view; issued per CARO 2020 (21 reporting clauses) |

| CARO Applicability | Not applicable to certain categories (similar to exemptions under Section 2(40)) |

| 14 Accounting Concepts | Accrual, Consistency, Going Concern, Prudence, Separate Entity, Money Measurement, Stable Monetary Unit, Cost, Conservatism, Dual Aspect, Accounting Period, Realisation, Matching, Full Disclosure |

| Accrual Concept | Income/expenses recorded when they occur, not when cash received/paid |

| Going Concern | Business assumed to continue operating in future |

| Prudence/Conservatism | Anticipate losses, do not anticipate profits |

| Dual Aspect | Every transaction has Debit and Credit (double-entry) |

| Accounting Standards (AS) | Issued by ASB of ICAI (constituted 1977); reduce alternatives, promote uniformity |

| GAAP | Generally Accepted Accounting Principles; governed by AS and Ind AS in India |

| Capital vs Revenue Expenditure | Capital: benefit >1 period, capitalised on BS; Revenue: benefit 1 period, expensed in P&L |

| Consolidated FS | Parent + subsidiaries as single economic entity; required under Companies Act 2013 |

| Ind AS | Indian Accounting Standards; converged with IFRS, not identical; effective from 1 April 2017 |

| Ind AS Applicable To | All listed companies; unlisted with NW Rs. 250 crore+; their holding/subsidiary/JV/associates |

| Ind AS Not Applicable To | SME exchange listed companies; banking/insurance/NBFC companies (separate guidelines) |

| Ind AS — Key Bodies | Recommended by ICAI; examined by NFRA; notified by Ministry of Corporate Affairs |

| FS Format | Prescribed by Companies Act, 2013 under Schedule III |

| Exceptions to Format | Insurance, Banking, Electricity companies; companies under special law |

| True and Fair View | FS must present true and fair view; non-compliance requires disclosure of deviation, reasons, and financial impact |

| Financial Year | Ends 31st March; typically 12 months |

| Companies Founded Jan–Mar | Year ends 31 March of following year; FS may cover up to 15 months |

| Foreign Subsidiary Year-End | Can change to match parent's date with NCLT approval |

| Balance Sheet Definition | Statement of assets & liabilities at a specific date (snapshot); Sources (liabilities/equity) vs Uses (assets) |

| BS Analytical Techniques | Comparative BS, Common Size BS, Trend Analysis |

| Key Documents Reviewed | Auditor's Report, Management Report, Statement of Changes in Equity |

| Banks Use FS For | Liquidity, solvency, profitability, and objective repayment ability assessment |

Lesson Doubts

Ask questions, get expert answers